Digitized

by

the

Internet

Archive

in

2011

with

funding

from

Boston

Library

Consortium

IVIember

Libraries

Ao.

08-oi

DEWEY

ilMassachusetts

Institute

of

Technology

Departnnent

of

Econonnics

Working

Paper

Series

DO

HOUSING

SALES DRIVE PRICES

OR

THE

CONVERSE?

William

C.

Wlieaton

Nai

Jia

Lee

Working

Paper

08-01

January

28,

2008

Room

E52-251

50

Memorial

Drive

Cambridge,

MA

02142

This

paper can be

downloaded

withoutcharge from

theSocial

Science

Research

Network

Paper

Collection at http;//ssrn.com/abstract=1107525

HB31

Draft:January28, 2008.

Do

Housing

Sales

Drive

Housing

Prices

or

the

Converse?

By

William

C.Wheaton

Department

ofEconomics

CenterforRealEstateMIT

Cambridge,

Mass 02139

[email protected]

and

Nai

JiaLee

Department

ofUrban

Studiesand

Planning CenterforRealEstateMIT

The

authorsare indebtedto,theMIT

CenterforRealEstate, theNational AssociationofRealtors

and

toTortoWheaton

Research.They

remain

responsiblefor allresultsand

conclusions derivedtherefrom.ABSTRACT

Thisempiricalpaper

examines

the questionof whether

movements

inhousingsalespredict subsequent

movement

inhouseprices - ortheconverse.The

former(positive)relationship iswellhypothesized

by

severalfrictional searchmodels of

housingmarket

transactions or"chum".

The

latterrelationship hasbeen

hypothesizedby

two

theories.Both

loss aversionand

liquidity ordown-payment

constraints suggest anotherpositive relationship inwhich

lowerprices generate lowersalesvolume.

Our

contributiontotheproblem

of unraveling causalityis touse apanelof

101 markets overthe periodfrom

1980

through 2006.With

several differentestimation techniqueswe

conclusivelyfindthathighersales

volume

always generateshigher subsequentprices.Higher

prices,however

always generatelower

subsequent sales volume.Our

conclusionis thattheoriesofhousing loss aversionorfinancial

down

payment

constraintsjustare notconsistentI. Introduction.

The

relationshipbetween

housingtransactionvolumes

{"sales")and

pricemovements

hasbeen

the subjectofseveraleconomic models

-

with thedirectionofcausalitybeingquite different. In one

camp,

severalpapers in"behavioralmicroeconomics" have

arguedthatwhen

pricesfall,homeowners

have

an aversion tosellingata loss-

no

matterhow

"rational" sellingmay

be [Genesove and

Mayer

(2001),Englehardt(2003)].

Another

group of paperscomes

to a similarconclusion,butthrough usingliquidityand

down

payment

constraints[Chan

(2001), Stein (1995),Lamont

and

Stein (1999).The

implicationof

bothmicro-economic

theoriesisthat afterprice declines, salesshouldbe

reduced,and

followingpriceincreases, sales shouldrecover.A

differentgroup ofpapers,examine

how

owners

trade housinginthepresence ofsearch frictions

[Wheaton

(1990), Berkovicand

Goodman

(1996),Lundberg and

Skedinger(1999)].As

istrue withmost

frictionalmarket

models

(e.g.Pissarides 2000), increasesinturnover(sales)tendstomake

trading easierand

inthe housingmarket

thiswill increaseprices.

Hence,

in thiscamp

thehypothesisis thatpositive shocksto sales will thenincrease priceswhile negative shocks will depressthem.There

have

been

onlyafew

attempts to testwhether

actualmovements

insalesand

pricessupport one, or the other,orboththeories-

using timing asthe testofcausality. This is complicated

by

the factthatboththeoriespredict positiverelationships.Berkovec and

Goodman

(1996) findsome

empirical supportforthe frictionalmodels

by

showing

thatdemand

shocks firstshow up

in salesvolume,

and

subsequentlyimpactprices. Leung, Lau,

and

Leong

(2002) undertakea fulltime seriesanalysisof

Hong Kong

Housing and

concludethatsimpleGranger

Causality isfound

more

oftenfor salesdrivingprices.

Andrew

and

Meen

(2003)examines

thetimeseries fortheUK

and

usingaVAR

model, concludethattransactionsrespondto shocksmore

quicklythanprices,butdo

notGranger Cause

price responses. Allofthese studiesarehampered

by

shorttimeseries

and

relativelylow

frequency.Granger

tests areknown

tomore

validwhen

undertaken with

more

extensive observationsathighfi-equency.Inthispaper,

we

trytosolvesome

oftheseproblems

with apanel approach-

we

examine

themovements

inpricesand

salesover27

years(1980-2006) in 101US

metropolitanareas.

With

almost2500

observationswe

effectively askhow

thetwo

seriesare related collectively acrossall

major

US

markets.We

find strongevidencethat salespositivelyimpact subsequentprices,butthatpricesnegativelyimpact subsequentsales.

We

obtain theseresultswith FixedEffects estimationand

alsowithGLS

IV

estimatesthatcorrectforthepanelHeteroskedasticityidentified

by

Holtz-Eakin,Newey

and

Rosen

(1988). Furthermore, ourresults arerobustto

whether

themodels

are estimatedin levels(whichare

non

stationary)orinfirst-differences(which

arestationary).We

concludethattheoriesof

Loss Aversion and

Liquidity constraints arejustnotconsistentwiththeaggregatebehavior

of

US

housingdata,whilethere iscomplete consistency withfrictionaltradingmodels.

Our

paperis organizedas follows. In sectionIIwe

reviewthe varioustheoreticalarguments

and

empirical supportforthetwo

typesofrelationshipsbetween

salesvolume

and

housingpricemovements.

In sectionIII,we

reviewthedatasourcesand

findsome

interesting

and

yetpuzzlingtrends intheonly availabletimeseries forsales.These

trendsgeneratenon-stationarity

and

encourage estimation indifferences. In sectionIV

we

discuss the applicationof panel datatoourquestion, theuseof conditioning variables

and

thealternativeestimationapproaches, whilein section

V

we

discuss the resultsof eachspecification. Section

VI

illustrateshow

our equations operatetogether as aVAR

model

and

SectionVI

draws

some

conclusions as towhy we

getaggregateresults thatare sodifferent fi^omthemicro-level research.

IL

SalesVolume-

Price relationshipsin the Literature.There

are aseriesofpaper'swhich

propose a relationshipinwhich

prices orchanges inprices will subsequently "cause"sales

volumes

to adjust.The

firstofthese isby

Stein (1995) followedby Lamont

and

Stein (1999)and

thenChan

(2001). In thesemodels,liquidity constrained

consumers

aremostlymoving

from one house

to another (market"chum")

and

must

make

adown

payment

inordertopurchase housing.Wlien

prices declineconsumer

equitydoes likewiseand

fewer householdshave

theremainingdown

payment

tomake

thelateralmove.

As

pricesrise, equityrecoversand

sodoesmarket

liquidity. Ineffectprice changes shouldpositivelycausesalesvolumes

-

bothup

and

down

-

althoughnot necessarilywithsymmetry.

A

second series of papers suggestadifferentmechanism

which

also generatesatleastapartialpositive causal chain

between

pricesand

salesvolume. Relyingon

"behavior economics",

Genesove and

Mayer

(2001)and

thenEnglehardt (2003)testforwhether

sellerswho

will experiencealosswhen

theyselltendto sethigherreservationsthanthose

who

willnotexperiencealoss. This suggests that aspricesbegintodrop,onlyrecentbuyerswill experience such "loss aversion".

As

aperiod ofpricedeclines extends,however,

an ever greaternumber

of

buyers experience "lossaversion"and

withthistransaction

volume

willincreasinglydryup

asmore

and

more

potentialsellers setoverly highand

unattainable reservations.As

long asprices arerising,however,

thetheorymakes

littleprediction aboutwhat

willhappen

to salesvolume

otherthaneliminating thesource of

any

"loss aversion".The

theory alsodoes notaddress the equilibriumquestion ofwhat

eventuallyhappens

toprices ifallpotential sellershave

higherreservations.Do

prices stopfalling forexample?

A

different group ofpapers,explicitlymodels

how

owners

tradehousingin thepresence ofsearch frictions

[Wheaton

(1990),Lundberg and

Skedinger(1999)]. In thesemodels, buyers

must

alwaysbecome

sellers-

there areno

entrantsorexitsfrom

themarket. Insuch a situationprices arelike "ftinny

money" -

withparticipantspayingmore

butalsoreceivingmore. It isonly thetransaction costofowning

2homes

(during themoving/tradeperiod) that groundsprices. Ifpricesare high, thetransaction costs can

make

moving

soexpensive as toerasewhatever

gainsfrom

moving

were

there originally.Inthis

environment

Nash-bargainedpricesbecome

almostinverse toexpectedsales times -where

thelatterequalsvacancy

dividedby

the sales flow. Inthese models,vacancy

isexogenous, butsales flowis

endogenous

-

depending

inparton

anexogenous

rate of"chum".

As

long as anincrease inthe"chum

rate"does not reduce searcheffort, salestimewill

be

shorterwithmore

chiomand

pricestherefore higher. In a similarmanner,and

followingPissarides (2000),Berkovec and

Goodman

(1996) developamodel

inwhich

areduction (increase) insales

volume

generatesa greater (smaller) inventoryof

unsoldhomes, and

this intum

leadstolower

(higher) sellerreservations. Inbothofthesemodels,there is cleartemporal causality: a

shock

occurs firstto salesvolume

which

thenThere have been few

attemptsto testwhether

actualmovements

insalesand

prices supportone, or theother, orboththeories. This is complicatedby

the fact thatboththeories predict positiverelationships,justwithdifferent timing. Berkovic

and

Goodman

(1996)initiallyfoundthat

movements

involume

did leadmovements

inpricesand

inferredthat thiswas

consistentwiththeirtheory. Leung, Lau,and

Leong

(2002) undertake atime series analysisofHong Kong

Housing and

concludethatstrongerGranger

Causality is foundfor sales driving prices ratherthanpricesdrivingsales.Andrew

and

Meen

(2003)examines

atime seriesfortheUK

and

usingaVAR

model, conclude thattransactionsrespond toshocksmore

quickly thanprices,butdo

not necessarily"Granger

Cause"

price responses. IntheirVAR

model

itturnsoutthattheestimated coefficientof laggedprices

on

transactionsvolume

isnegativeand

notpositiveas suggested

by

thetheoriesofloss aversion orliquidityconstraints.III. Sales

Volume

and

Price Data.The

price datawe

chose touseis theOFHEO

repeatsales series [Baily,Muth,

Nourse

(1963)]. This data serieshasrecentlybeen

severely questionedfornotfactoring outhome

improvements

ormaintenance and

fornotfactoring indepreciation orobsolescence [Case,

PoUakowski,

Wachter

(1991),Harding, Rosenthal,Sirmans

(2007)].These

omissions couldgenerate a significantlybias inthe long termtrendof

theOFEHO

series. Thatsaidwe

areleftwithwhat

isavailable,and

theOFHEO

index is themost

consistentseries availableformost

US

markets overalong timeperiod.The

onlyalternative istopurchase similarindices

from

CSW/FISERV,

although theyhave

thesame

methodologicalissues as theOFHEO

data.The

sales datawe

usewere

providedby

theNational Associationof

Realtors(NAR).

This datais for singlefamilyunitsonly (it excludescondominium

sales), andwas

obtainedforeachmarket

from

1980-2006.Raw

saleswere

thencompared

with annualCensus

estimates ofthenumber

oftotalhouseholds inthose markets. Dividingsinglefamilysales

by

totalhouseholdswe

getacrudesales rate foreach market. In1980

thissales ratevaried

between

1.2%

and

5.1%

across ourmarkets with an average of 2.8%.By

contrast, inthe1980

Census,the single family mobilityrate(inthe previousyear)(1989)

Census

annual mobility ratefellto 6.5%.By

2000,theNAR

sales ratereached 5.0%, whiletheCensus

mobilityraterecoveredabitto7.1%).Thus

duringthis25 yearperiod, ourcalculatedaverage sales ratesarealways lower thanthe censusreported

mobilityrates. This isbecausethe householdseriesusedtocreatetherate is total

householdsratherthanjust singlefamily

owner-occupied

households. Separaterenter/ownersinglefamily

household

series atyearlyfrequency

arejustnot availableby

metropolitanmarket.'However,

the observationthatthetwo

datasources trenddifferentlyis

more

disturbing.Over

1980-2000, boththeUS

homeownership

ratioand

thefraction ofsingle familyunits in thestock are virtuallyunchanged.

As

such, thedifference

between

thetrue mobilityand

ourconstructedsale rate shouldbe

constant. It is not,and

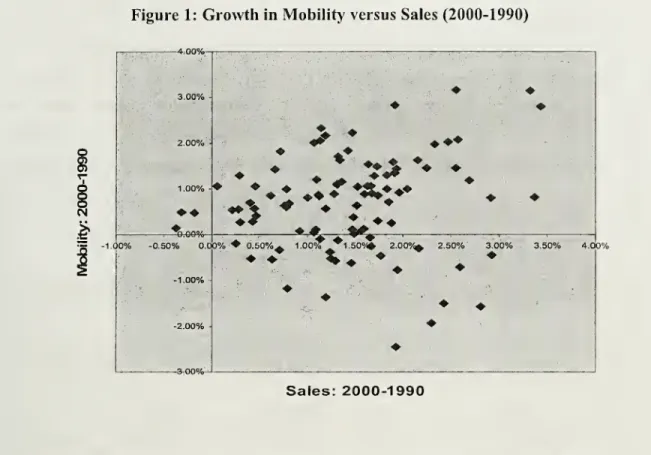

inFigure 1we

show

ascatterplot that illustratesthe relationshipbetween

thechanges

inthesetwo measures

across our 101 markets.The

NAR

sales rateincreasessignificantly

between

1990 and

2000

inmost

MSA,

whiletheCensus

mobilityratedecreases inalmostas

many

areas as itincreases. Itis clearthatthere isno

associationoverthis

decade

between

which

marketssaw

an increaseinNAR

salesand

which

experiencedany

underlying increase inCensus

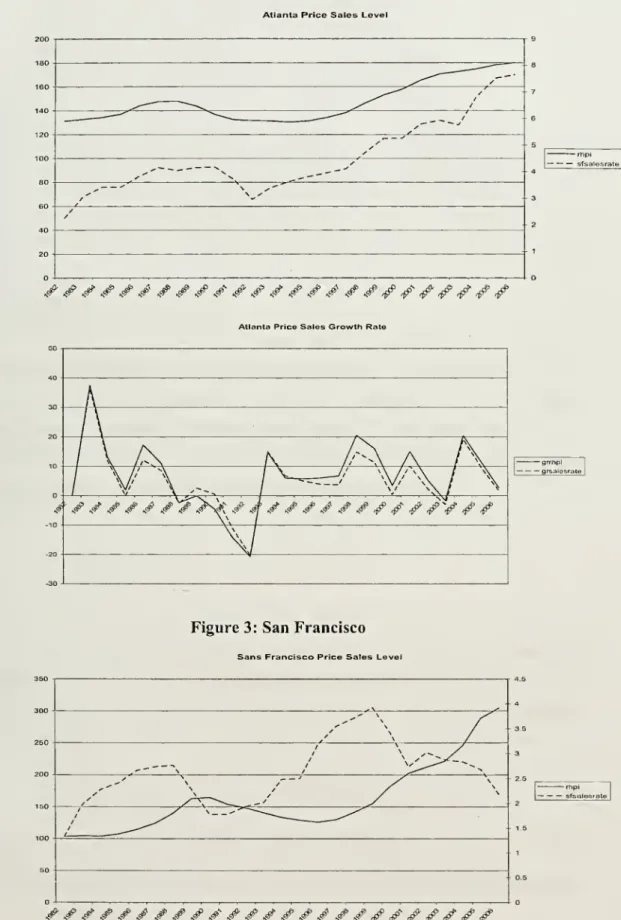

mobility(R~=.002).InFigures2

and

3we

illustratetheyearlyNAR

sales rate data, along with theconstant dollar

OFHEO

price series-

bothin levelsand

differences fortwo

marketsthatexhibit quitevaried behavior, Atlanta

and San

Francisco.Over

thistime frame, Atlanta's constant dollar prices increaseverylittlewhileSan

Francisco's increasedalmost200%).San

Francisco prices,however,

exhibit fargreaterpricevolatility. Atlanta'saverage sales rateis closeto5%

and

trends quite sharply,whileSan

Francisco's is almosthalfofthat(2.6%))

and

exhibits onlya slight trend.'

Inmorerecent years the calculated

NAR

sales ratesare closetobeing60%

ofthetruesinglefamilymobilityrate-aswouldbedictatedbythe national differencebetweenthenumberoftotalandsingle

Figure

1:Growth

in Mobility versus Sales(2000-1990) CM 1.00% ^.00% 1,00% -0.50% O.OO'/i.

%

—

-

—

^>

^

'—

^ • ' • % 0.50%^ 1.00% ^^1.50°/* 2.00°/,^ 2.50% 3.00% 3.50% 4.'^*

Sales:

2000-1990

Both

ofthese individualmarketsillustrate thetrendtothe sales ratedatathatis *presentin virtuallyall

MSA.

The

constructedsales ratesalvv^aysriseupwards

overthis 25 year period-

sometimes

increasingcumulativelyby

asmuch

as 2to4

percentagepoints.As

mentioned

relative to Figure 1,theCensus

reportsonly aslightincrease inbothowner

and

renter"move"

ratesbetween 1990 and

2000 and

adeclinebetween 1980 and

1990.Thus

theNAR

trendwould

appeartorepresentsome

artifactofreporting. Perhaps agrowing

shareof brokersbecame

members

oftheNAR

or agrowing

share ofmembers

participatedinreportingdata.

Whatever

thereason,itseems

clearthatthetrenddoes notreflect a truedoubling in

US

mobility. Itisdifficulttothinkof reasonswhy

saleswould

trend significantly different

from

mobility-

particularly acrossmarkets^. InappendixIwe

present thesummary

statistics foreach market'spriceand

sales rateseries.Given

thereservations overthetrends inbothseries itisusefuland

important totestfor series stationarity.

There

aretwo

testsavailable forusewith panel datasuchaswe

Salesduetodeathsdonot generateamove.Transfersof propertybetweenindividualscouldgeneratea

"sale"withoutamove. Thesebiasesshouldbesmallandstationaryhowever. Itis also believedthat For-Sale-by-Owner"transactionshaveincreasedanderoded brokerage businessrecently-the oppositeofthe

have. In each, thenullhypothesis is that allofthe individualseries

have

unitrootsand

are

non

stationary. Levin-Lin (1993)and

Im-Persaran-Shin (2002) both developateststatistic forthe

sum

oraverage coefficientofthe laggedvariableof

interest-

across the individuals (markets) within the panel.The

nullis thatall or the average ofthese coefficients isnotsignificantly differentfrom

unity. InTable 1we

report the resultsof

thistestforbothhousingprice

and

sale rate levels,aswellas a 2" orderstationarity test forhousingpriceand

sales ratechanges.TABLE

1RHPI

(Augmented

bv

1 lag)Levin

Lin'sTest

Coefficient

T

Value

T-StarP>T

Levels -0.10771 -18.535

0.22227

0.5879First Difference -0.31882 -19.822 -0.76888 0.2210

IPS

testT-Bar

W(t-bar)P>T

Levels -1.679 -1.784 0.037

FirstDifference -1.896 -4.133 0.000

SFSALESRATE

(Augmented

by

1 lag)Levin

Lin'sTest

Coefficient

T

Value

T-StarP>T

Levels -0.15463 -12.993 0.44501 0.6718

FirstDifference -0.92284 -30.548 -7.14975 0.0000

IPS

testT-Bar

W(t-bar)P>T

Levels -1.382 1.426 0.923

FirstDifference -2.934 -15.377 0.000

With

the Levin-Lintestwe

cannotreject thenull (non-stationarity) for eitherhouse

pricelevels ordifferences. Interms ofthesales,we

canrejectthe null fordifferencesin sales ratedifferences, butnotfor levels.

The

IPS test(which

isarguedtohave

more

power)

rejects thenull forhouse

price levelsand differencesand

for sales ratedifferences. In short,bothvariables

would seem

tobe

stationary indifferences,butlevels aremore

problematicand

likely non-stationary.Figure

2:Atlanta

AtlantaPriceSales Level

* sfsalesrate

^ ^

.^ ^#^

/

^

.^^

^^^ ^

^

^

.#,^\^.^^^^^^^^^

AtlantaPriceSalesGrowthRate

Figure

3:San

Francisco

SansFrancisco Price Sales Level

-rtipl

'sfsalesrate

SansFranciscoPricesSalesGrowth

IV.

Panel Estimation

Approaches.

Our

panelapproachuses awell-known

application of Granger-lypeanalysis.We

will ask

how

significantlagged salesareinapanelmodel

ofpriceswhich

uses laggedprices

and

thenseveral conditioning variables.The

conditioning variableswe

choose aremarket

areaemployment,

and

nationalmortgage

rates.The

companion

model

isto askhow

significant laggedprices are inapanelmodel

ofsalesusinglagged salesand

thesame

conditioningvariables. This pairofmodel

isshown

(l)-(2).P,j

= ^0 +

«i-^-,r-i+

«2'5'/,r-i+ P'Xfj

+

^,+

£,j (1)s^j

=

ro+

y^s,,T-^+

riPi.T-i+ ^'^ij +

+7,-+

^,, (2)Inpanel models, all ofthe estimation issues raisedintime series continueto exist. Inourcase thereisconcern about the stationarityof bothprice

and

sales rate levels. Thissame

concernis notpresentfordifferences.Hence

clearlywe

willneed

to estimate themodel

in firstdifferencesas wellaslevels-

asoutUned

inequafions (3)and

(4).''AP.j

=

«(,+

a^AP.j._^+

a2AS.j._^+

fi'AX-j.+

+S,+

£,j (3)A5,,r

=n+

rAS,,T-^+ Yi^.j-x +

^'^X.j

+

+TJ.+

£,., (4)Inpanel

models

with a cross-section fixedeffect(theS.and

rj.) there exists apotential specification issue. Sincethe fixedeffectsare presentnotjust in current, but laggedvalues ofthe

dependent

variables,OLS

willnot leadtoconsistent estimates.The

problem

isabuilt in correlationbetween

the laggeddependentvariableand

the laggederror term.

Thus

estimatesand

testson

theparameters ofinterest (thea

and/

)may

not bereliable.

The

problem

canbe

amelioratedtosome

extentby

normalizing thevariablestomake

the fixedeffectsvanish -forexample

when

prices aremeasured

asan index thatbegins with avalueof 100 for each cross sectioninthesample. Similarlyusingasales

rate(ratherthan theactual sales

volume)

willhelp alleviate the specificationproblem.To

be

safe,however,

we

also estimatedthemodels

followingan estimation strategyby

Holtz-Eakin et altobetter estimate the causalvalues oftheparametersofinterest.

As

discussedin

Appendix

II,thisamounts

tousing 2-periodlaggedvaluesofsalesand

prices as instrumentswithGLS

estimation.From

eitherestimates,we

conducta"Granger"

causalitytest. Sincewe

areonlytesting for a singlerestriction, the/statistic isthe squarerootofthe

F

statistic thatwould

be

used

to testthe hypothesisinthepresenceofa longer lagstructure (Green, 2003).Hence,

we

can simply use attest(appliedtothea,and

y^)as thecheck ofwhether

changes

in sales"Granger

cause" changes inprice and viceversa.V. Results.

Intable 2

we

report theresults ofequations(1) through(4) ineachsetof rows.The

firstcolumn

usesOLS

estimation, the second theRandom

EffectsIV

estimatesfrom

Holtz-Eakinetal.The

first setof equationsis in levels, whilethe second setof

rows

reports theresultsusingdifferences.Among

the levels equations,we

firstnoticethatthetwo

conditioningvariables,thenational

mortgage

rateand

localemployment

canhave

thewrong

signs-

here intwo

cases.

The

mortgage

interestrateintheOLS

pricelevelsequationand

localemployment

inthe

IV

sales rateequation aremiss-signed.Thereis alsoan insignificantemployment

troublesomeresultisthatthepricelevelsequationhas excess

"momentum" -

laggedprices

have

a coefficient greater than one.Hence

prices(levels)might

grow

on

theirovm

withoutnecessitating

any

increases infundamentals, orsales.We

suspectthatthesetwo

anomalies arelikelythe resultofthenon-stationary featuretoboththe priceand

salesseries

when

measured

in levels. Interestingly,thetwo

estimationtechniquesyield quitesimilarcoefficients

-

as wellas anomalies.When we

move

totheresultsof

estimating theequationsindifferences theseissues alldisappear.

The

laggedpricecoefficients are small, the price equations stable inthe 2"^degree,

and

the signs ofallcoefficients are both correct-

and

highly significant.As

to the questionofcausality, inevery price or pricegrowth

equation, laggedsales or

growth

in salesis always significant.Furthermorein everysales rate orgrowth

insales rateequation, laggedprices(orits growth)arealsoalways significant.

Hence

thereisclear evidenceofjoint causality, butthe effect

of lagged

priceson

sales isalwaysof

thewrong

sign!Holding

lagged sales(andconditioning variables) constant, ayear afterthereis

an

increase inprices-

salesfall-

ratherthanrise!The

impactis exactly the opposite ofthatpredictedby

theoriesoflossaversionorliquidityconstraints.TABLE

2FixedEffects

E

Holtz-Eakinestimator LevelsRHPI

(Dependent

Variable) ConstantRHPI

(lag 1)SFSALESRATE(lagl)

MTG

EMP

SFSALESRATE

(Dependent

Variable) ConstantRHPI

(lag 1)SFSALESRATE

(lag 1) -25.59144" (2.562678) 1.023952** (0.076349) 3.33305** (0.2141172) 0.3487804** (0.1252293) 0.0113145** (0.0018579) 2.193724** (0.1428421) -0.0063598** (0.0004256) 0.8585273** -12.47741** (2.099341) 1.040663** (0.0076326) 2.738264** (0.2015346) -0.3248508** (0.1209959) 0.0015689** (0.0003129) 1.796734** (0,1044475) -0.0059454** (0.0004206) 0.9370184**(0.0119348) (0.0080215)

MTG

-0.063598** -0.0664741** (0.0069802) (0.0062413)EMP

-0.0000042 -0.0000217** (0.0001036) (0.0000103) FirstDifferenceGRRHPI

(DependentVariable) Constant -0.4090542** -0.49122** (0.1213855) (0.1221363)GRRHPI

(Lag 1) 0.7606135** 0.8008682** (0.0144198) (0.0148136)GRSFSALESRATE

0.0289388** 0.1826539** (Lag1) (0.0057409) (0.022255)GRMTG

-0.093676** -0.08788** (0.097905) (0.0102427)GREMP

0.3217936** 0.1190925** (0.0385593) (0.048072)GRSFSALESRATE

(DependentVariable) Constant 0.7075247 1.424424** (0.3886531) (0.3710454)GRRHPI(Lagl)

-0.7027333** -0.8581478** (0.0461695) (0.0556805)GRSFSALESRATE

0.0580555** 0.0657317** (Lagi) (0.0183812) (0.02199095)GRMTG

-0.334504** -0.307883** (0.0313474) (0.0312106)GREMP

1.167302** 1.018177** (0.1244199) (0.1120497) ** indicates significance at5%.

We

have

experimented withthesemodels

usingmore

than a singlelag,butqualitativelytheresults arethesame. Inlevels, the priceequationwith

two

lagsbecomes

dynamically stable inthe sense thatthesum

ofthe laggedprice coefficientsislessthanone.

As

to causal inference, thesum

ofthe laggedsales coefficients ispositive,highlysignificant,

and

passes theGranger

F

test. In thesales rateequation, thesum

ofthetwo

laggedsales rates is virtually identical tothe single coefficient

above

and

the laggedpricelevels areagain significantlynegative (intheir

sum) and

collectively"Granger

cause" areduction in sales.

We

have

similarconclusionswhen

two

lags areused

inthe differences equations, butindifferences, the2" lagis always insignificant.As

a finaltest,we

investigatea relationshipbetween

thegrowth

inhouse

pricesand

the levelofthe salesrate. In the search theoreticmodels

sales ratesdetermine pricelevels,butifprices are

slow

to adjust, the impactofsalesmight

bettershow

up on

pricechanges. Similarly the theories oflossaversion

and

liquidity constraintsrelatepricechangesto sales levels.

While

themixing of

levelsand

changes in timeseries analysisisgenerally not standard,

we

offerup

Table 3where

pricechanges

are tested against thelevelofsales (as arate).

TABLE

3Differences

and

Levels Fixed EffectsE

Holtz-EakinestimatorGRRHPI

(Dependent

Variable) ConstantGRRHPI

(lag 1)SFSALESRATE

(lag 1)GRMTG

GREMP

SFSALESRATE

(Dependent

Variable) ConstantGRRHPI

(lag 1)SFSALESRATE

(lag 1)GRMTG

-6.61475** (0.3452743) 0.5999102** (0.0155003) 1.402352** (0.0736645) -0.1267573** (0.0092715) 0.5059503** (0.0343458) -0.0348229 (0.0538078) -0.0334235** (0.0024156) 1.011515** (0.0114799) -0.0162011** (0.0014449) -1.431187** (0.2550279) 0.749431** (0.0141281) 0.2721678** (0.0547548) -0.0860948** (0.0095884) 0.3678023** (0.0332065) 0.0358686 (0.0026831) -0.0370619** (0.0026831) 1.000989** (0.0079533) -0.0151343** (0.0014294)GREMP

0.0494462** (0.0053525) 0.043442** (0.0049388) ** indicates significance at5%

Interms ofcausality, theseresults are

no

differentthanthe traditionalmodels

estimatedeither in all levelsorall differences.

One

yearafteranincrease inthe levelofsales,theaccelerates thelevel

of

home

sales falls(ratherthanrises). All conditioning variables aresignificant

and

correctlysignedand

laggeddependent

variableshave

coefficientless thanone.

VI.

VAR

System

Behavior.The

final step in our analysis is to investigate thedynamic

relationshipbetween

the

two

variables: salesand

prices.When

taken together, they represent a 2-equationVector

Auto

Regression(VAR).

VARs

aremost

useful for understanding the long-term response ofa system of equations to ashock

orchange

in a conditioning variable.Thus

for

example what happens

to pricesand

sales ifmortgage

ratespermanently

decrease oremployment

permanently increases? In Figure 4we

examine what happens

to in arepresentative

market

(Atlanta in this case)when

mortgage

rates take apermanent

drop.The model

uses the levels equationsand

the base line steady stateassumes

that currentAtlanta

employment

levelsand

mortgage

rates prevail indefinitely. This generates asteady state price index of

273 and

sales rate of 1.24%.''When

rates permanently drop200

bps sales initially rise but then settledown

just slightlyabove

their original value.Prices rise

10%

butfollow themovement

in sales.Both

ofthese response patternsseem

in accord with theory

and

suggest thatwhen

taken together the levels equations closelyreflect

how

housing markets shouldreacttodemand

shocks.In Figure 5

we

examine

the behaviorof

the pair of equations estimated indifferences.

Here

our base line steadygrowth

path has Atlantaemployment

increasing2%

yearlywhilemortgage

rates are stable.The

impulse responsetracesoutwhat happens

ifthe

employment

growth

rate permanentlyjumps

to a very robust4%.

Prices,which

were

trendingat0.057%,

now

grow

at a littlemore

than5.53%

while the sales ratejumps

from

2.27%

to3.15%

at steady state. In impulse responses there is the appearance thatsales

move

"before"prices.Thesimulations reported incorporate the fixedeffectfor the Atlantamarket,whichlike that formost

marketswasnotstatistically significant.

We

attribute thistotheuseofsalesratesandtoprice indicesFigure

4:ChangeinMortgage Rate by 200 bps

Quarters

-rhpi

sfsalesrale

Figure

5:NewSteadyStates:IncreaseinEmployment GrowthRateby4%

o 6 0. 2 -gntipi -grsfsalesrate 1 2 3 4 5 6 7 8 9 101 112 13 14 15 16 17 18 192021 22 23 24 25 26 27 28 29 3031 32 33 34 3536 Quarters

VI. Discussion

and

Extension.On

theone

hand, theresultsof

thisanalysis arecompletelyconsistentwiththeories

of

frictionalmarketsinwhich

changesto housingsales should"Granger

cause" housingpricesto increase.On

theotherhand

theyarecompletelyinconsistentwiththeoriesoflossaversion or liquidity constraints,

wherein

falling (rising)house

pricesshouldconstrain(free up)buyers

and "Granger

cause"sales to fall(rise). Instead, sales inthemarket

tendtoreactnegatively topriorpricemovements.

This occurs inmodels

of bothprice levels aswellas differencesand

is alwaysstatisticallysignificant.As

towhy

we

getthisresult,herewe

offersome

possible explanations.First,with the increased sophisticationof

mortgage

marketsinthe lasttwo

decades,

down

payment

constraintsmay

have

been

reducedtothepointwhere

theyrarelyexercise influence

on

home

buying.Secondly, duringaperiod

when

nominal house

pricesrose almost every yearinmost

markets,thepresenceof

lossaversionmay

likewiseexistonlyinafew

marketsand

during onlyafew

periods.Such

episodesare simplytoo infrequentto impactthemarket

as awhole even though

theycanshow

up

in individual decisions.Finally,itcould bethe casethattheaggregate

movement

in housingsales islargelydriven

by

flows intohome-ownership.

If infact, firsttimehome

buyers arean important source ofsalesfluctuations, thenitis nothardto understandhow

such purchasesarenegatively correlatedwithprices.As

prices rise(fall) fewer (more)firsttimebuyersare abletoafford

and

enter theownership

market. This isprobably ourbestexplanationfor

why

ourresultsusingaggregatedatastandinsuchcontrasttotheREFERENCES

Andrew,

M.

and

Meen,

G. (2003)."House

price appreciation, transactionsand

structuralchange

inthe Britishhousing market:A

macroeconomic

perspective."Real

EstateEconomics,

31, 99-116.M.J. Baily, R.F.

Muth, H.O.

Nourse,"A

RegressionMethod

forReal Estate PriceIndex

Constmction"

,Journalof

theAmerican

StatisticalAssociation, 58 (1963) 933-942.Berkovec, J.A.

and

Goodman,

J.L. Jr. (1996)."Turnover

as aMeasure of

Demand

forExisting

Homes."

Real

EstateEconomics,

24(4),421-440.Bradford Case,

Henry

O. Pollakow^ski,and Susan

M.

Wachter."On

Choosing

among

Housing

PriceIndexMethodologies,"^i?£'t/^^ Journal, 19 (1991), 286-307.Dennis

Capozza, PatricHendershott,and

CharlotteMack.

"An Anatomy

ofPriceDynamics

in IlliquidMarkets: Analysisand Evidence

from

LocalHousing

Markets,"Real

EstateEconomics,

32 (2004) 1-21.Chan,

S. (2001). "SpatialLock-in:Do

FallingHouse

Prices ConstrainResidentialMobility?"

Journal of

Urban

Economics,

49,567-587.Engelhardt,G. V. (2003).

"Nominal

lossaversion,housing equityconstraints,and

household

mobility: evidencefrom

theUnited States."Journal of

Urban

Economics,

53(1), 171-195.Genesove,

D.and

C.Mayer

(2001). "Lossaversionand

sellerbehavior:Evidence from

thehousing

market." QuarterlyJournal ofEconomics,

116(4), 1233-1260.John

Harding, S. Rosenthal, C.F.Sirmans. (2007). "Depreciation ofHousing

Capital,maintenance,

and house

priceinflation..."

Journal of

Urban

Economics,

61,2,567-587.Holtz-Eakin, D. ,

Newey,

W.

and

Rosen, S.H. (1988). "EstimatingVectorAutoregressions with Panel Data," Econometrica,Vol. 56,

No.

6. pp. 1371-1395.Kyung

So

Im,M.H.

Pesaran, Y. Shin(2002),"Testing forUnitRoots

inHeterogeneous

Panels",Cambridge

University,Department of

Economics

Lament,

O.and

Stein, J. (1999)."Leverage and

House

PriceDynamics

inU.S. Cities."RAND

Journal ofEconomics,

30, 498-514.Levin,

Andrew

and

Chien-Fu

Lin (1993). "UnitRoot

Tests inPanel Data:new

results."Discussion

Paper

No. 93-56,Department of Economics,

UniversityofCaliforniaatSan

Leung,

C.K.Y.,Lau,G.C.K. and

Leong, Y.C.F. (2002). "Testing AlternativeTheories ofthe Property Price-Trading

Volume

Correlation."The

Journalof Real

EstateResearch,23(3), 253-263.

Per Lundborg, Per Skedinger, "Transaction

Taxes

ina SearchModel

oftheHousing

Market", Journalof

Urban

Economics,

45,2,March

1999.Pissarides, Christopher,Equilibrium

Unemployment

Theory,2" edition,MIT

Press,Cambridge,

Mass., (2000).Seslen,T.N. (2003).

"Housing

PriceDynamics

and

Household

Mobility Decisions."Working

Paper,The

CentreforRealEstate,M.I.T.Stein, C. J. (1995). "Prices

and

TradingVolume

intheHousing

Market:A

Model

withDown-Payment

Effects,"The

QuarterlyJournal

Of

Economics,

110(2), 379-406.Wheaton,

W.C.

(1990)."Vacancy,

Search,and

Prices in aHousing

Market

Matching ModeX," Journal of

PoliticalEconomy,

98,1270-1292

APPRENDIX

I MarketCode

Market AverageGRRHPI

{%) AverageGREMP

(%) AverageSFSALES

RATE

AverageGRSALES

RATE

(%) 1 Allentown 2.03 1.10 4.55 4.25 2 Akron 1.41 1.28 4.79 4.96 3 Albuquerque 0.59 2.79 5.86 7.82 4 Atlanta 1.22 3.18 4.31 5.47 5 Austin 0.65 4.23 4.36 4.86 6 Bakersfield 0.68 1.91 5.40 3.53 7 Baltimore 2.54 1.38 3.55 4.27 8 BatonRouge

-0.73 1.77 3.73 5.26 9Beaumont

-1.03 0.20 2.75 4.76 10 Bellingham 2.81 3.68 3.71 8.74 11 Birmingham 1.28 1.61 4.02 5.53 12 Boulder 2.43 2.54 5.23 3.45 13 BoiseCity 0.76 3.93 5.23 6.88 14 BostonMA

5.02 0.95 2.68 4.12 15 Buffalo 1.18 0.71 3.79 2.71 16 Canton 1.02 0.79 4.20 4.07 17 Chicago IL 2.54 1.29 4.02 6.38 18 Charleston 1.22 2.74 3.34 6.89 19 Charlotte 1.10 3.02 3.68 5.56 20 Cincinnati 1.09 1.91 4.87 4.49 21 Cleveland 1.37 0.77 3.90 4.79 22Columbus

1.19 2.15 5.66 4.61 23 Corpus Christi -1.15 0.71 3.42 3.88 24 Columbia 0.80 2.24 3.22 5.99 25 Colorado Springs 1.20 3.37 5.38 5.50 26 Dallas-Fort Worth-Arlington -0.70 2.49 4.26 4.64 27 DaytonOH

1.18 0.99 4.21 4.40 28 Daytona Beach 1.86 3.06 4.77 5.59 29 DenverCO

1.61 1.96 4.07 5.81 30Des

Moines 1.18 2.23 6.11 5.64 31 DetroitMl 2.45 1.42 4.16 3.76 32 Flint 1.70 0.06 4.14 3.35 33 Fort Collins 2.32 3.63 5.82 6.72 34 FresnoCA

1.35 2.04 4.69 6.08 35 FortWayne

0.06 1.76 4.16 7.73 36 Grand Rapids Ml 1.59 2.49 5.21 1.09 37 GreensboroNC

0.96 1.92 2.95 7.2238 Harrisburg

PA

0.56 1.69 4.24 3.45 39 Honolulu 3.05 1.28 2.99 12.66 40 Houston -1.27 1.38 3.95 4.53 41 Indianapolis IN 0.82 2.58 4.37 6.17 42 Jacksonville 1.42 2.96 4.60 7.23 43 KansasCity 0.70 1.66 5.35 5.17 44 Lansing 1.38 1.24 4.45 1.37 45 Lexington 0.67 2.43 6.23 3.25 46 Los AngelesCA

3.51 0.99 2.26 5.40 47 Louisville 1.48 1.87 4.65 4.53 48 LittleRock

0.21 2.22 4.64 4.63 49 LasVegas

1.07 6.11 5.11 8.14 50Memphis

0.46 2.51 4.63 5.75 51 Miami FL 1.98 2.93 3.21 6.94 52 Milwaukee 1.90 1.24 2.42 5.16 53 Minneapolis 2.16 2.20 4.39 4.35 54 Modesto 2.81 2.76 5.54 7.04 55Napa

4.63 3.27 4.35 5.32 56 Nashville 1.31 2.78 4.44 6.38 57New

York 4.61 0.72 2.34 1.96 58New

Orleans 0.06 0.52 2.94 4.80 59Ogden

0.67 3.25 4.22 6.08 60Oklahoma

City -1.21 0.95 5.17 3.66 61Omaha

0.65 2.03 4.99 4.35 62 Orlando 0.88 5.21 5.30 6.33 63 Ventura 3.95 2.61 4.19 5.83 64 Peoria 0.38 1.16 4.31 6.93 65 PhiladelphiaPA

2.78 1.18 3.52 2.57 66 Phoenix 1.05 4.41 4.27 7.49 67 Pittsburgh 1.18 0.69 2.86 2.75 68 Portland 2.52 2.61 4.17 7.05 69 Providence 4.82 0.96 2.83 4.71 70 PortSt. Lucie 1.63 3.59 5.60 7.18 71 RaleighNC

1.15 3.91 4.06 5.42 72Reno

1.55 2.94 3.94 8.60 73Richmond

1.31 2.04 4.71 3.60 74 Riverside 2.46 4.55 6.29 5.80 75 Rochester 0.61 0.80 5.16 1.01 76 SantaRosa

4.19 3.06 4.90 2.80 77 Sacramento 3.02 3.32 5.51 4.94 78San

FranciscoCA

4.23 1.09 2.61 4.7379 Salinas 4.81 1.55 3.95 5.47 80

San

Antonio -1.03 2.45 3.70 5.52 81 Sarasota 2.29 4.25 4.69 7.30 82 Santa Barbara 4.29 1.42 3.16 4.27 83 SantaCruz 4.34 2.60 3.19 3.24 84San

Diego 4.13 2.96 3.62 5.45 85 Seattle 2.97 2.65 2.95 8.10 86San

Jose 4.34 1.20 2.85 4.5587 SaltLake City 1.39 3.12 3.45 5.72

88 St. Louis 1.48 1.40 4.55 4.82

89

San

Luis Obispo 4.18 3.32 5.49 4.2790

Spokane

1.52 2.28 2.81 9.04 91 Stamford 3.64 0.60 3.14 4.80 92 Stockton 2.91 2.42 5.59 5.99 93Tampa

1.45 3.48 3.64 5.61 94 Toledo 0.65 1.18 4.18 5.18 95 Tucson 1.50 2.96 3.32 8.03 96 Tulsa -0.96 1.00 4.66 4.33 97 VallejoCA

3.48 2.87 5.24 5.41 98 WashingtonDC

3.01 2.54 4.47 3.26 99 Wictiita -0.47 1.43 5.01 4.39 100 Winston 0.73 1.98 2.92 5.51 101 Worcester 4.40 1.13 4.18 5.77Notes: Table providesthe averagereal

average job

growth

rate, averagesalesprice appreciationoverthe25 years,

APPENDIX

IILet Apj.

=

[AP,j.,....,AP^j-] 'and Asj.=

[AS",7.,....,AS

^y.]',where

A'^is thenumber

ofmarkets. Let Wj.

=

[e,Apj.^^,Ay

j._,,AY,

7.]be thevector ofrighthand

side variables,where

eis a vectorof

ones. Let V^=

[£^j.,...,£f^-j.]

be

the//x

1 vectorof

transformeddisturbance terms. Let

B

=

[«(,,a,,a,,/?),<5|]' bethe vector ofcoefficients forthe

equation.

Therefore,

Ap^ =

W^B

+

Fj. (1)Combining

all theobservationsfor each time periodintoa stackofequations,we

have,Ap =

WB

+ V.

' (2)The

matrixofvariables thatqualifyforinstrumental variablesinperiodT

willbeZj =

[e,Apj_.,_,Asj._,,AX

-J]

,

(3)

which

changes with T.To

estimate B,we

premultiply(2)by

Z' to obtainZ'Ap

=

Z'WB

+

Z'V

.

(4)

We

thenform

a consistent instrumental variables estimatorby

applyingGLS

toequation(4),

where

thecovariance matrixQ

=

E{Z'

W

Z)

. Q. is notknown

and

hasto beestimated.

We

estimate (4) for each time periodand

form

the vectorofresidualsforeach periodand form

aconsistent estimator,Q

, forQ

.5

, theGLS

estimatoroftheparametervetor, ishence:

B

=

[W'z{Qy'

z'wy'w

z(Qy'

z'Ap

.

(5)