12th International Conference on Socio-economic and Environmental Issues in Development, 2020 At National Economics University, Hanoi, Vietnam

Access to Credit Markets and Selection of Credit Sources of Rural Households: The Case Study of the Red River Delta, Vietnam

Ta Nhat Linh: [email protected] Phan Thu Trang: [email protected] Nguyen Thanh Huyen: [email protected]

School of Banking and Finance, National Economics University, Hanoi, Vietnam Philippe Lebailly: [email protected]

Econmic and Rural Development Unit, Gembloux Agro-Bio Tech, University of Liege, Gembloux, Belgium

---Abstract

The role of agriculture sectors in the economic development of a country is undeniable, especially in developing and least- developed ones, ensuring food supply, increasing national income, export earnings and poverty reduction. Vietnam is known as an emerging market, depending directly on agriculture-related activities for their livelihood. However, the issue of rural credit access still remains a confounding problem. The paper focuses on identifying the determinants of credit access in rural areas of Vietnam using the Red River Delta as the case study, including formal and informal credit. The paper uses data from Vietnam Household Living Standard Survey 2018 (VHLSS 2018) of General Statistics Office of Vietnam. The probit and linear regression models are applied to investigate the factors that determine household credit accessibility, i.e., the households’ decision to borrow and borrowing amounts. Results of this analysis reveal the different significant determinants of formal and informal credit market access. The implications of these findings for enhancing formal credit accessibility and reducing reliance on informal markets are considered.

Keywords: access to credit, developing countries, rural credit market, Vietnam 1. Introduction

In many developing countries, agriculture is regared as one of the most crucial sectors of the whole economy, especially in developing nations, as it is believed to be of importance for not only internal food security but also employment growth and poverty reduction. Vietnam is known as a developing country with the high rural penetration rate, at nearly 65% of total population. Moreover, in rural areas, the proportion of household in which main income derives from agriculture account for approximately 48% (GSO, 2020). Nevertheless, the access to credit for farmers in rural areas in emerging countries still appeared to be of difficulty, which can lead to a more severe consequence due to capital shortage: decline in total output and GDP and lower national food security (Godfray et al., 2010; Malik & Nazli, 1999). In rural areas of Vietnam, formal and informal credit markets commonly exist, in which informal ones are prone to be prevalent to the formal one. The formal credit constraints is possibly due to market imperfections as well as the lending procedures.

The Red River Delta (RRD) is the flat low-lying plain formed by the Red River and its distributaries in the northern of Vietnam. The Delta has the smallest area but highest population density among 8 regions of Vietnam. The RRD is the economic center of northern Vietnam with Hanoi as the capital of Vietnam. Although the RRD makes up only 5% of Vietnam land, about 15,000 square kilometers, 30% of the country’s populations live there. Moreover, 80% of the population are employed in agriculture with the proportion 65% of

total agricultural output of Vietnam, which implies the important role of agriculture in raising income and increasing farmers’ livelihood (GSO, 2017).

In practice, farming households, especially poor and low-income rural households are often limited to access formal credit because they do not have enough collateral as well as cannot borrow on the basis of their income. The number of research aiming at the importance of rural credit in some provinces of Vietnam has strongly increased in recent years. However, there have been few studies conducted in rural areas of this important northern delta as a whole. Therefore, significant results of this study will arise.

Based on the consideration above, the aim of this study is to find out the determinants of household credit accessibility in rural areas of Vietnam with the case in the Red River Delta. The rest of this paper is organized, as follows. Section 2 summarizes some previous literature on rural credit access of Vietnam and some developing countries. Section 3 is the description of rural credit markets in Vietnam. Section 4 presents the methodology used in this paper. Some results and discussion about the determinants of the research site are shown in section 5. Based on that, some implications proposed to accelerate formal credit access of households for agriculture production and conclusions are presented in section 6.

2. Literature Review

2.1. The perception of access to credit markets

Credit sources are generally divided in three categories: formal, semi-formal and informal credit sources. The semi-formal ones make up a very small share in the total so, it is the reason that they are excluded in the study. Formal institutions in the rural markets are commercial banks or credit funds while informal sources can come from moneylenders, local sellers, informal credit associations, relatives or friends.

Households’ access to rural credit markets can be simply defined as approaching credit services (Zeller et al., 1996). In other words, rural credit access means that households have access to specific sources among many available ones. Subsequently, access to credit is measured by the amount of money that a household can borrow from lenders (Diagne & Zeller, 2001). Formal credit accessibility of farming households should be considered under the two main actors: borrowers—households/credit demand and lenders—credit suppliers (Zeller, 1994), in which the demand factors are to provide information if a household is constrained to a credit source or not, while the supply factors present the amount that borrowers can obtain from the given source. In some other studies, credit constraints are considered to measure credit accessibility, in which there is a mismatch between borrowers’ credit demand and lenders’ lending decisions (Lin, Wang, Gan, Cohen, & Nguyen, 2019). However, there are some differences of between the meaning of credit constraints and credit accessibility in some research.

2.2. Determinants of rural credit access

Determinants of credit access are factors of household characteristics and capacities that affect household credit demand and decisions to participate in the credit markets. In other words, credit-side and supply-side factors should be taken into account (Zeller, 1994). Credit-side or household-related factors are demographic characteristics which often affect households’ credit demand while supply-side factors are often socio-economic characteristics or capacities which the lenders employ as criteria in selecting and screening potential borrowers who are eligible to receive loans (T. G. Evans, A. M. Adams, R. Mohammed, & A. H. Norris, 1999).

Households’ socio-economic characteristics have been recognized in several studies with empirical results from many developing countries. Diagne indicates the significant impact of household asset composition to credit accessibility (Diagne, 1999). To be more specific, the more share of land and livestock of total assets, the less formal credit borrowers can access. Notably, the author also figures out that informal and formal credit are not perfect subsitues as different types of credit meet the different demand of household and resource

transferability. Okurut suggests that the poor have limited access to formal as well as semi-formal financial sectors (Okurut, 2006). Research results also points out female borrowers, educational level, household size and household’s expenditure per capita have significantly negative relation to formal credit access. The results is also congruent with the case of Eastern Cape Province in South Africa (Baiyegunhi, Fraser, & Darroch, 2010), the case of China (Lin et al., 2019), the case of Zanzibar (Mohamed, 2003) and the case of Madagascar (Zeller, 1994). Farmer’s awareness of lending institutions also positive impact to microcredit access in the research of Northen Ghana (Anang, Sipiläinen, Bäckman, & Kola, 2015).

In short, age, number of family members, household income, family size, bank distance, loan duration, loan processing, interest rate, and loan size are factors affecting households’ credit accessibility all affect access to rural credit. Education is found to be a significantly positive factor (Bashir, Azeem, & Sciences, 2008; Chandio, Jiang, & Trade, 2018; Ugwumba, Omojola, & Science, 2013). Dependency ratio (often found as family size and family income) can also a factor can partially explain the rural credit participation. The more dependent members, the higher probability of being poor, which can lead to credit constraints (Li, Gan, & Hu, 2011; Okurut, Schoombee, & Van der Berg, 2005). Group membership can help households easily access to credit (T. G. Evans, A. M. Adams, R. Mohammed, & A. H. J. W. d. Norris, 1999; B. Hananu, A. Abdul-Hanan, & H. J. A. J. o. A. R. Zakaria, 2015b). Gender, especially female borrowers have higher probability to access to credit. Experience, area of land in agricultural production, farm size, and collateral can also be viewed as influential factors(Bigsten et al., 2003; Chandio et al., 2018; Zeller, Diagne, & Mataya, 1998).

The same results can also be applied in the case of Vietnam. Some papers also confirmed these above-mentioned factors. Education, farming land ownership is found to be significantly positive while financial and non-financial savings are negative in connection to household borrowing. (Quach, Mullineux, & Murinde, 2005). Households’ heads with higher level of education (i.e. people with education at primary and secondary) are dominated in this case while head with university degree and never attendted school do not borrow much. Household heads’ age has the negative relation to credit participation (Nguyen, 2007). A negative relation is seen in testing such variable as distance to the market center/province, education and total land size (Duy, D’Haese, Lemba, & D’Haese, 2012).

All variables indicated above are observable factors. However, unobservable factors, i.e. social capital/networks have been found out in relationship with farmers’ credit accessibility. Social capital is known as the numbers of helpers and contacts with agricultural extension in the last 12 months (Bauer, 2016). It can also be seen as acquaintances in existing credit institutions or reputation and social status (Duong & Izumida, 2002). In informal sector, social network can be seen as the most important factor affecting credit participation as it contains available information and potential resources of borrowers while household characteristics do not have much effect, (Dufhues, Buchenrieder, Quoc, & Munkung, 2011; Yuan & Xu, 2015).

3. The organisation of rural credit markets in Vietnam

The salient characteristics of rural credit markets in Vietnam can be described as lender participation constrained with heavy subsidization and strongly segmented (Linh, Long, Chi, Tam, & Lebailly, 2019). The segmentation of rural credit markets is due to borrowing purpose differences. While formal loans are often used for production, informal credit is seemingly referred to in order to meet diverse demand of rural households (Bao Duong & Izumida, 2002; Barslund & Tarp, 2008). The constraints of rural credit participation, especially formal participation, result from the nature of agricultural production and the imperfection of formal markets. That is the reason why the informal credit sources are likely to be prevalent in rural areas. The agricultural production can be considered to be so risky, attributed to complicated uncertainties of weather or diseases (Thornton, van de

Steeg, Notenbaert, & Herrero, 2009). The uncertainties will grow up in developing countries such as Vietnam with the lack of technology, skill and inappropriate agriculture policies (Marsh, MacAulay, & Hung, 2006; Tanaka, Camerer, & Nguyen, 2010). Then, financial institutions, such as commercial banks in Vietnam, are reluctant to enter the agricultural credit markets in rural zones. They have the rights to choose good low-risk potential customers instead of high-risk ones.

Variables Description

Age Age of household head (year)

Gender Gender of household head, man=1, woman=0

Marital status Marital status of household head, married=1, otherwise =0

Vocational education Having vocational education=1, otherwise =0

Ethnicity Kinh=1, otherwise =0

Number of working people Number of people with income

Dependency ratio Dependent people/ total people in family Group membership Member of a credit group: 1=yes, 0=no

Saving 1=yes, 0=no

Occupation Head of family is farmer only =1, otherwise=0

Ln_owned_land Log of value of dwelling land with ownership certificate (m2)

Having land ownership certificate

1=yes, 0=no

Ln_farm_land Log of value of farm land (m2)

Ln_agri_income Log of value of income from agriculture (thousand dong) Ln_agri_expenditure Log of value of expenditure from agriculture (thousand

dong)

Vietnamese rural credit markets are divided in three categories: formal, informal and semi-formal. Semi-formal sources in Vietnam are excluded in the paper. The three state-owned financial institutions are the three main formal sources in rural Vietnam, i.e., Vietnam Bank for Agriculture and Rural Development (VBARD), Vietnam Bank for Social Policies (VBSP) and the People’s Credit Funds (PCFs). The three institutions control around 70% rural credit market share. VBARD is a commercial bank whose targeted customers are larger-scale households, requiring collateral for almost all loans offered. The Vietnam Bank for Social Policies, formerly known as the Vietnam Bank for the Poor, often provides low-interest rate credit to poorer people without collateral. The People’s Credit Fund system operates mainly in rural areas. Especially, PCFs often lend the locals in the commune where it is located. Each of the PCFs has specific lending policies, requiring collateral or not.

Concerning the informal credit sector in rural Vietnam, there are many studies that have indicated its importance in financing household production in case of formal credit shortage (Bao Duong & Izumida, 2002; Barslund & Tarp, 2008; Khoi, Gan, Nartea, & Cohen, 2013). Informal credit sources in rural areas of Vietnam are mainly from relatives, friends, informal revolving credit associations (“ho, hui, phuong”), and local lenders with high interest rates or goods on credit from local sellers. Informal credit includes interest and no-interest loans as well as collateral-required and no-collateral loans. A major informal credit source from moneylenders in Bangladesh is also indicated in the research of Ghosh et al. (Ghosh, Gupta, & Maiti, 2008).

4. Materials and Method 4.1. Data

The study has used data from VHLSS 2018 with selected 937 rural households of the Red River Delta. Information on socio-economic characteristics, income and production factors are also collected and captured in the table 1 below.

Table 1. Description of Variables 4.2. Empirical Models

The probit and normal regression model was applied to identify the determinants of credit access at the household level. Household credit accessibility includes households’ participation in credit markets and the borrowed loan amounts based on previous literature, which are assumed to be influenced by a number of household characteristics as two equations as follows: Yi¿ =α1+β1Xi+ui (1) Yi=1 if Yi¿ >0 Yi=0, otherwise Yi¿ '=α1+β1Xi+ui (1’) Yi=1 if Yi¿ >0 Yi=0, otherwise Bi ¿ =α2+β2Xk+ei(2) Bi=Bi¿=α2+β2Xk+ei, if Yi¿=1 Bi=0, otherwise

In equation (1) Yi=1 if a household has access to credit (including formal and informal sources) and 0 if otherwise, Xi and Xk captures all household socio-economic characteristics, income, credit and production factors, as shown in the table 1. In equation (1’) Yi'=1 if a household has access to formal credit and 0 if a household has access to informal one.

Next, household characteristics are also assumed to have effects on the size of loans the household takes up in equation (2). Under the case Yi=1 , Bi represents the log of the expected value of the amount received by each household. That means Bi is observed only when Yi=1 , i.e., the household i has access to credit. The equation (1) and (1’) is estimated using the probit model while normal OLS is used for equation (2).

5. Results and Discussion

5.1. Socio-economic description of the sample

Table 2 describes the sample respondents and sources of credit. Of the 937 respondents, there are 206 borrowers and 731 non-borrowers. Of the 206 borrowers, 124 borrowed from the formal sectors while 82 borrowed forms the informal sectors.

Table 2. Formal and Informal credit market participation

Source: Authors’ summary from VHLSS 2018

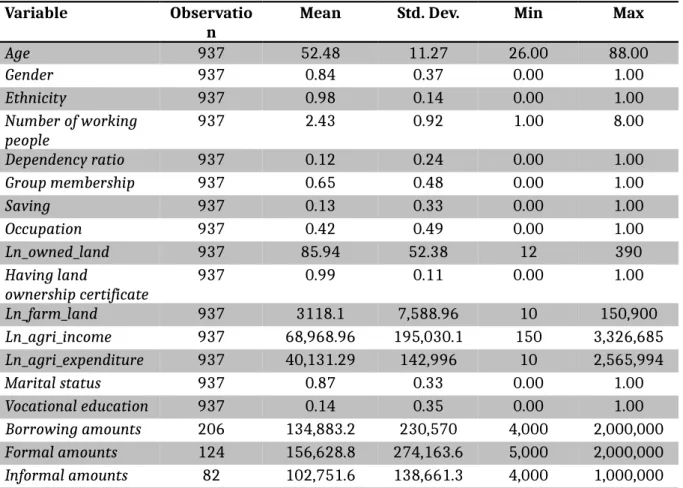

Table 3 below shows the means and standard deviations of some key indicators of all samples. The average age of farmers is quite high at 52.48. In reality, younger people in rural areas, especially in urbanized communes/districts, have a big chance to work at industrial zones in the urban areas or seek a free job in the city with higher income. The dependency ratio is quite low. The reason is that the average age of farmers is around 52 whose children are often mature. The notable feature of surveyed households is that land area for farming, income as well as expenditure from agriculture activities per household varies dramatically.

Formal Informal Total

Borrowers 124 82 206

Non_Borrowers - - 731

On average, the amounts of formal loans are greater than the informal loan. In the

rural areas, a formal loan from VBARD and PCFs has usually a short-term loan while the longer-term loan is from VBSP. The term of informal loans is very flexible, depending on the negotiation between lender and borrowers. In addition, the informal interest rate is often excessively higher than the formal one.

Table 3. Means and Standard Deviations of some indicators Source: Authors’ calculation from VHLSS 2018

5.2. Determinants of households’ participation in the credit markets

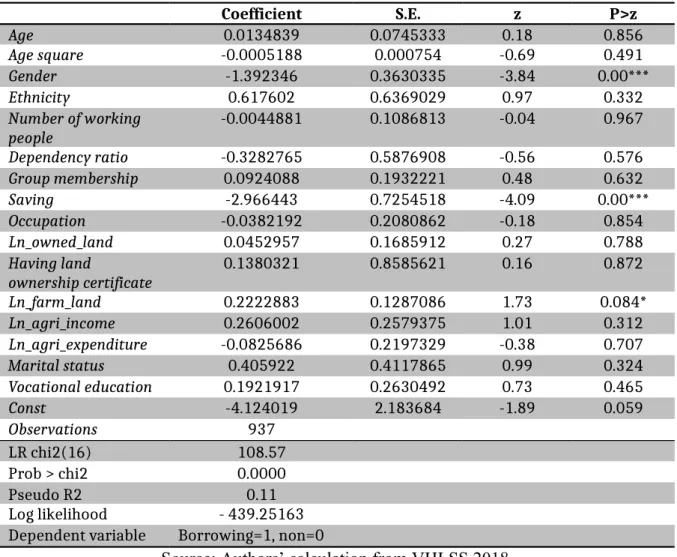

Table 4 explains the determinants of households’ credit market participation in rural areas of the Red River Delta as shown in function (1). However, households in the research site borrow from both formal and informal sources, so the results will be bias if we pool informal and formal demand. To deal with the issue, table 5 reports the results from estimation of function (1’) to indicate the factors affecting households’ credit source selection after borrowing decisions, i.e. their decisions to borrow from formal or informal markets. Probit regression is used in function (1) and (1’).

When we study credit accessibility as pooled sources, the factors significantly affecting households’ participation in credit markets are: gender, saving and farming land. The coefficient of gender variable is significantly negative at 1%. That result suggest that the households whose head are women have greater demand in borrowing money. This is consistent to the studies of Hananu et al. and Akudugu (Akudugu, 2012; B. Hananu, A. Abdul-Hanan, & H. Zakaria, 2015a). The variable of saving also presents a significantly negative influence on credit market accessibility at the 1% level. On the other words, the presence of household savings significantly declined the demand of credit. This is reasonable because saving can be regarded as a substitute source of credit or a self-financing source of family. This result is confirmed by some authors in Vietnam and some other countries (Fenwick & Lyne, 1998; Khoi et al., 2013). As expected, the variable of farming land are

Variable Observatio

n

Mean Std. Dev. Min Max

Age 937 52.48 11.27 26.00 88.00 Gender 937 0.84 0.37 0.00 1.00 Ethnicity 937 0.98 0.14 0.00 1.00 Number of working people 937 2.43 0.92 1.00 8.00 Dependency ratio 937 0.12 0.24 0.00 1.00 Group membership 937 0.65 0.48 0.00 1.00 Saving 937 0.13 0.33 0.00 1.00 Occupation 937 0.42 0.49 0.00 1.00 Ln_owned_land 937 85.94 52.38 12 390 Having land ownership certificate 937 0.99 0.11 0.00 1.00 Ln_farm_land 937 3118.1 7,588.96 10 150,900 Ln_agri_income 937 68,968.96 195,030.1 150 3,326,685 Ln_agri_expenditure 937 40,131.29 142,996 10 2,565,994 Marital status 937 0.87 0.33 0.00 1.00 Vocational education 937 0.14 0.35 0.00 1.00 Borrowing amounts 206 134,883.2 230,570 4,000 2,000,000 Formal amounts 124 156,628.8 274,163.6 5,000 2,000,000 Informal amounts 82 102,751.6 138,661.3 4,000 1,000,000

positive and highly significant at the level of 10%, indicating that the households with larger farming land are very likely to have grater borrowing demand. The effect of total farming land on credit access is found in a lot of research of some developing countries (Akudugu, 2012; Chandio & Jiang, 2018; Saleem, Jan, Khattak, & Quraishi, 2011; Sharma, Gupta, & Bala, 2007) and of Vietnam (Barslund & Tarp, 2008; Duy et al., 2012). On the other hand, the result indicates the increasing of borrowing demand of households for agricultural production in rural areas.

Table 4. Determinants of households’ participation in the credit markets

Coefficient S.E. z P>z Age 0.0134839 0.0745333 0.18 0.856 Age square -0.0005188 0.000754 -0.69 0.491 Gender -1.392346 0.3630335 -3.84 0.00*** Ethnicity 0.617602 0.6369029 0.97 0.332 Number of working people -0.0044881 0.1086813 -0.04 0.967 Dependency ratio -0.3282765 0.5876908 -0.56 0.576 Group membership 0.0924088 0.1932221 0.48 0.632 Saving -2.966443 0.7254518 -4.09 0.00*** Occupation -0.0382192 0.2080862 -0.18 0.854 Ln_owned_land 0.0452957 0.1685912 0.27 0.788 Having land ownership certificate 0.1380321 0.8585621 0.16 0.872 Ln_farm_land 0.2222883 0.1287086 1.73 0.084* Ln_agri_income 0.2606002 0.2579375 1.01 0.312 Ln_agri_expenditure -0.0825686 0.2197329 -0.38 0.707 Marital status 0.405922 0.4117865 0.99 0.324 Vocational education 0.1921917 0.2630492 0.73 0.465 Const -4.124019 2.183684 -1.89 0.059 Observations 937 LR chi2(16) 108.57 Prob > chi2 0.0000 Pseudo R2 0.11 Log likelihood - 439.25163 Dependent variable Borrowing=1, non=0

Source: Authors’ calculation from VHLSS 2018. *: Significant at 10% level.

**: Significant at 5% level. ***: Significant at 1% level.

While gender, saving and farming land are demonstrated to have strong impacts on credit accessibility, vocational training is found to have positive relationship with credit source selection in table 5. That means household heads having vocational education (i.e. graduated from collage, university or vocational school) have greater demand than the others. This result is consistent with the study of Hanunu et al. (Hananu et al., 2015a) and Sebatta et al. (Sebatta, Wamulume, & Mwansakilwa, 2014). Higher levels of education infer better knowledge, farming skills as well as ability to obtain more information on credit markets so more educated farmers often have easier access to credit.

Coefficient Std. Err. z P>z Age -0.0173695 0.14773 -0.12 0.906 Age square 0.0001417 0.0015039 0.09 0.925 Gender 0.0918301 0.5514311 0.17 0.868 Number of working people 0.0086827 0.2104567 0.04 0.967 Dependency ratio 0.6472104 1.262436 0.51 0.608 Group membership 0.2920156 0.3583468 0.81 0.415 Occupation -0.3252587 0.3779394 -0.86 0.389 Ln_owned_land -0.4838973 0.3007692 -1.61 0.108 Having land ownership certificate 1.215413 1.480832 0.82 0.412 Ln_farm_land 0.0112807 0.2399821 0.05 0.963 Ln_agri_income -0.1925978 0.4656426 -0.41 0.679 Ln_agri_expenditure 0.4115489 0.4002805 1.03 0.304 Marital status -0.3932767 0.6256727 -0.63 0.53 Vocationla education 0.8942388 0.5083798 1.76 0.079* Const -0.1913955 4.31621 -0.04 0.965 Observations 206 LR chi2(16) 12.47 Prob > chi2 0.5688 Pseudo R2 0.045 Log likelihood -132.24287 Dependent variables

Borrowing from formal sources = 1, Borrowing from informal sources = 0

Source: Authors’ calculation from VHLSS 2018. *: Significant at 10% level.

**: Significant at 5% level. ***: Significant at 1% level. 5.3. Determinants of borrowing amounts of households

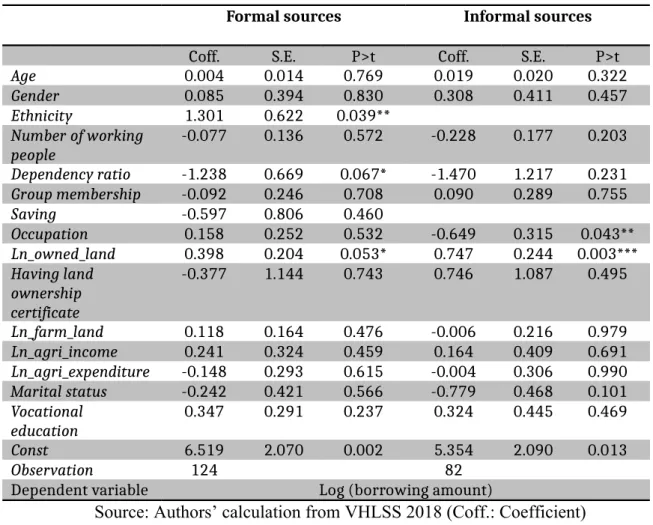

Table 6 presents the determinants of borrowing amounts of rural households in the Red River Delta. As shown in section 5.2, the result is likely to be biased if we pool formal and informal credit. Therefore, determinants of formal and informal amounts are separately investigated in table 6.

The second big column of the table 6 presents the determinants of formal borrowing amounts. Interestingly, ethnicity, dependency ratio and owned land are figured out to have significant impacts on formal credit amounts. As expected, the variables of ethnicity and owned land are positive and significant at the level of 5% and 10%, respectively. The positive coefficient of ethnicity means people of King majority could borrow more money from formal sources than the other minorities. Kinh majority have chance to access more

information as well as are more educated than the minorities. Therefore, Kinh are believed to have more ability of debt repayment. This is one of criteria that affect lenders’ decision. This result is consistent with many studies in Vietnam (Duy et al., 2012; Khoi et al., 2013).

The coefficient of dependency ratio is significantly negative at 10%. The results suggest that families with less dependent people could obtain larger amounts. Families with higher dependency ratio reflect the lower earning capacities as well as lower repayment ability. The explanatory variable owned land indicating the areas with ownership certificate has positive effect on formal amounts and is significant at the 10% level. On the other words, households with better land ownership status could obtain more formal credit amounts

(Chandio & Jiang, 2018; Rahman, Hussain, & Taqi, 2014). In practice, land area with ownership certificate is a substitute of asset possession and collateral security. Almost all financial institutions or commercial banks are only willing to offer amounts on the basis of collateral value.

Concerning the determinants of informal amounts, owned land are also found out to have positive correlation informal amounts. Most informal lenders decide to approve loans based on borrowers’ assets. Collateral is believed to reflect household wealth and increase repayment possibility (Hussain & Thapa, 2012; Saqib, Ahmad, & Panezai, 2016; Zeller, 1994). The sign of occupation is negative that means households whose heads are farmers seemingly borrow less money than others from informal sources. This enhances the fact that households are reluctant to borrow informal credit for agriculture production. Agriculture production in developing countries still remains risky due to shortage of technology, dependence on weather and uncertainties of diseases. On the other hand, informal interest rates are quite higher than formal ones, which is the reason why farmers prefers borrowing formal loans rather informal ones.

Table 6. Determinants of borrowing amounts

Formal sources Informal sources

Coff. S.E. P>t Coff. S.E. P>t

Age 0.004 0.014 0.769 0.019 0.020 0.322 Gender 0.085 0.394 0.830 0.308 0.411 0.457 Ethnicity 1.301 0.622 0.039** Number of working people -0.077 0.136 0.572 -0.228 0.177 0.203 Dependency ratio -1.238 0.669 0.067* -1.470 1.217 0.231 Group membership -0.092 0.246 0.708 0.090 0.289 0.755 Saving -0.597 0.806 0.460 Occupation 0.158 0.252 0.532 -0.649 0.315 0.043** Ln_owned_land 0.398 0.204 0.053* 0.747 0.244 0.003*** Having land ownership certificate -0.377 1.144 0.743 0.746 1.087 0.495 Ln_farm_land 0.118 0.164 0.476 -0.006 0.216 0.979 Ln_agri_income 0.241 0.324 0.459 0.164 0.409 0.691 Ln_agri_expenditure -0.148 0.293 0.615 -0.004 0.306 0.990 Marital status -0.242 0.421 0.566 -0.779 0.468 0.101 Vocational education 0.347 0.291 0.237 0.324 0.445 0.469 Const 6.519 2.070 0.002 5.354 2.090 0.013 Observation 124 82

Dependent variable Log (borrowing amount)

Source: Authors’ calculation from VHLSS 2018 (Coff.: Coefficient) *: Significant at 10% level.

**: Significant at 5% level. ***: Significant at 1% level. 6. Conclusion and implication

This research attempts to identify the determinants of farming households’ credit accessibility in rural Vietnam with the case of the Red River Delta. Our results confirm the segmentation of rural credit markets in the research site, in which the informal credit markets coexist with the formal ones.

The results of the paper confirm that households’ credit market participation is significantly influenced by the following factors: gender, saving and ln_farm_land while vocational education determines households’ credit source selection. From the regression

model OLS, it was shown that ethnicity, dependency ratio and ln_owned_land has significant impact on the borrowing amounts in only formal markets. Ln_owned_land have significantly positive relationship with informal amounts while occupation is proven to have negative impact on informal amounts.

Results of the research pose some policy implications focusing on enhancing household credit accessibility in rural areas. In practice, banks are focusing on high-return customers rather than agriculture-production customers. The salient constraint of taking big-amount loans from commercial banks is collateral. Almost all commercial banks just accept households’ dwelling land with ownership certificate instead of farm land while the value of farmers’ dwelling land as collateral is much smaller than farming land so large-production households can hardly borrow the amounts as big as they want. Therefore, the government should have policies to fill the gap between borrowers and formal lenders, meeting credit demand to maximize their production.

This study is subject to certain limitations due to VHLSS data restrictions, however, it also provides insights for further research in rural Vietnam. In spite of the limitation, the results of the paper can be applied for the other provinces of the Red River Delta.

7. References

Akudugu, M. (2012). Estimation of the determinants of credit demand by farmers and supply by rural banks in Ghana’s Upper East Region. Asian Journal of Agriculture and Rural Development, 2(393-2016-23992), 189-200.

Anang, B. T., Sipiläinen, T., Bäckman, S., & Kola, J. (2015). Factors influencing smallholder farmers’ access to agricultural microcredit in Northern Ghana. African Journal of Agricultural Research, 10(24), 2460-2469.

Baiyegunhi, L., Fraser, G., & Darroch, M. (2010). Credit constraints and household welfare in the Eastern Cape Province, South Africa. African Journal of Agricultural

Research, 5(16), 2243-2252.

Bao Duong, P., & Izumida, Y. (2002). Rural Development Finance in Vietnam: A

Microeconometric Analysis of Household Surveys. World Development, 30(2), 319-335. doi:https://doi.org/10.1016/S0305-750X(01)00112-7

Barslund, M., & Tarp, F. (2008). Formal and informal rural credit in four provinces of Vietnam. The Journal of Development Studies, 44(4), 485-503.

Bashir, M. K., Azeem, M. M. J. P. J. o. L., & Sciences, S. (2008). Agricultural credit in Pakistan: Constraints and options. 6(1), 47-49.

Bauer, S. J. J. o. r. s. (2016). Does credit access affect household income homogeneously across different groups of credit recipients? Evidence from rural Vietnam. 47, 186-203.

Bigsten, A., Collier, P., Dercon, S., Fafchamps, M., Gauthier, B., Gunning, J. W., . . .

Söderbom, M. J. J. o. A. E. (2003). Credit constraints in manufacturing enterprises in Africa. 12(1), 104-125.

Chandio, A. A., & Jiang, Y. (2018). Determinants of Credit Constraints: Evidence from Sindh, Pakistan. Emerging Markets Finance and Trade, 54(15), 3401-3410.

Chandio, A. A., Jiang, Y. J. E. M. F., & Trade. (2018). Determinants of Credit Constraints: Evidence from Sindh, Pakistan. 54(15), 3401-3410.

Diagne, A. (1999). Determinants of household access to and participation in formal and informal credit markets in Malawi. Retrieved from

Diagne, A., & Zeller, M. (2001). Access to credit and its impact on welfare in Malawi (Vol. 116): Intl Food Policy Res Inst.

Dufhues, T., Buchenrieder, G., Quoc, H. D., & Munkung, N. (2011). Social capital and loan repayment performance in Southeast Asia. The Journal of Socio-Economics, 40(5), 679-691.

Duong, P. B., & Izumida, Y. J. W. d. (2002). Rural development finance in Vietnam: A microeconometric analysis of household surveys. 30(2), 319-335.

Duy, V. Q., D’Haese, M., Lemba, J., & D’Haese, L. (2012). Determinants of household access to formal credit in the rural areas of the Mekong Delta, Vietnam. African and Asian studies, 11(3), 261-287.

Evans, T. G., Adams, A. M., Mohammed, R., & Norris, A. H. (1999). Demystifying nonparticipation in microcredit: a population-based analysis. World Development, 27(2), 419-430.

Evans, T. G., Adams, A. M., Mohammed, R., & Norris, A. H. J. W. d. (1999). Demystifying nonparticipation in microcredit: a population-based analysis. 27(2), 419-430.

Fenwick, L., & Lyne, M. C. (1998). Factors influencing internal and external credit rationing among small-scale farm households in Kwazulu-Natal. Agrekon, 37(4), 495-505. Ghosh, R., Gupta, K. R., & Maiti, P. (2008). Development Studies (Vol. 3): Atlantic

Publishers & Dist.

Godfray, H. C. J., Beddington, J. R., Crute, I. R., Haddad, L., Lawrence, D., Muir, J. F., . . . Toulmin, C. J. s. (2010). Food security: the challenge of feeding 9 billion people. 327(5967), 812-818.

GSO. (2017). Statistic Year Book.

GSO. (2020). Average population by sex and urban and rural areas.

Hananu, B., Abdul-Hanan, A., & Zakaria, H. (2015a). Factors influencing agricultural credit demand in Northern Ghana. African Journal of Agricultural Research, 10(7), 645-652.

Hananu, B., Abdul-Hanan, A., & Zakaria, H. J. A. J. o. A. R. (2015b). Factors influencing agricultural credit demand in Northern Ghana. 10(7), 645-652.

Hussain, A., & Thapa, G. B. (2012). Smallholders’ access to agricultural credit in Pakistan. Food Security, 4(1), 73-85.

Khoi, P. D., Gan, C., Nartea, G. V., & Cohen, D. A. (2013). Formal and informal rural credit in the Mekong River Delta of Vietnam: Interaction and accessibility. Journal of Asian Economics, 26, 1-13.

Li, X., Gan, C., & Hu, B. J. J. o. A. E. (2011). Accessibility to microcredit by Chinese rural households. 22(3), 235-246.

Lin, L., Wang, W., Gan, C., Cohen, D. A., & Nguyen, Q. T. (2019). Rural credit constraint and informal rural credit accessibility in China. Sustainability, 11(7), 1935.

Linh, T. N., Long, H. T., Chi, L. V., Tam, L. T., & Lebailly, P. (2019). Access to rural credit markets in developing countries, the case of Vietnam: A literature review.

Sustainability, 11(5), 1468.

Malik, S. J., & Nazli, H. J. T. P. D. R. (1999). Rural poverty and credit use: Evidence from Pakistan. 699-716.

Marsh, S. P., MacAulay, T. G., & Hung, P. V. (2006). Agricultural development and land policy in Vietnam. Canberra: Australian Centre for International Agricultural Research (ACIAR).

Mohamed, K. (2003). Access to formal and quasi-formal credit by smallholder farmers and artisanal fishermen: A case of Zanzibar: Mkuki na Nyota Publishers.

Nguyen, C. H. (2007). Determinants of credit participation and its impact on household consumption: Evidence from rural Vietnam. In.

Okurut, F. N. (2006). Access to credit by the poor in South Africa: Evidence from Household Survey Data 1995 and 2000. Stellenbosch: University of Stellenbosch.

Okurut, F. N., Schoombee, A., & Van der Berg, S. J. S. A. J. o. E. (2005). Credit Demand and Credit Rationing in the Informal Financial Sector in Uganda 1. 73(3), 482-497.

Quach, M., Mullineux, A., & Murinde, V. (2005). Access to credit and household poverty reduction in rural Vietnam: A cross-sectional study. The Birmingham Business School, The University of Birmingham Edgbaston, 1-40.

Rahman, S., Hussain, A., & Taqi, M. (2014). Impact of agricultural credit on agricultural productivity in Pakistan: An empirical analysis. International Journal of Advanced Research in Management and Social Sciences, 3(4), 125-139.

Saleem, A., Jan, F. A., Khattak, R. M., & Quraishi, M. I. (2011). Impact of Farm and Farmers Characteristics On Repayment of Agriculture Credit. Abasyn University Journal of Social Sciences, 4(1).

Saqib, S. E., Ahmad, M. M., & Panezai, S. (2016). Landholding size and farmers’ access to credit and its utilisation in Pakistan. Development in Practice, 26(8), 1060-1071. Sebatta, C., Wamulume, M., & Mwansakilwa, C. (2014). Determinants of smallholder

farmers’ access to agricultural finance in Zambia. Journal of Agricultural Science, 6(11), 63.

Sharma, R., Gupta, S., & Bala, B. (2007). Access to Credit-A Study of Hill Farms in

Himachal Pradesh. JOURNAL OF RURAL DEVELOPMENT-HYDERABAD-, 26(4), 483.

Tanaka, T., Camerer, C. F., & Nguyen, Q. (2010). Risk and time preferences: Linking experimental and household survey data from Vietnam. American Economic Review, 100(1), 557-571.

Thornton, P. K., van de Steeg, J., Notenbaert, A., & Herrero, M. (2009). The impacts of climate change on livestock and livestock systems in developing countries: A review of what we know and what we need to know. Agricultural Systems, 101(3), 113-127.

doi:https://doi.org/10.1016/j.agsy.2009.05.002

Ugwumba, C., Omojola, J. J. J. o. A., & Science, B. (2013). Credit access and productivity growth among subsistence food crop farmers in Ikole Local Government Area of Ekiti State, Nigeria. 8(4), 351-356.

Yuan, Y., & Xu, L. (2015). Are poor able to access the informal credit market? Evidence from rural households in China. China Economic Review, 33, 232-246.

doi:https://doi.org/10.1016/j.chieco.2015.01.003

Zeller, M. (1994). Determinants of credit rationing: A study of informal lenders and formal credit groups in Madagascar. World Development, 22(12), 1895-1907.

Zeller, M., Ahmed, A. U., Babu, S. C., Broca, S., Diagne, A., & Sharma, M. P. (1996). Rural Finance Policies for Food Security of the Poor: Methodologies for a Multicountry Research Project.

Zeller, M., Diagne, A., & Mataya, C. J. A. E. (1998). Market access by smallholder farmers in Malawi: Implications for technology adoption, agricultural productivity and crop income. 19(1-2), 219-229.