Airline Revenue Management Based on Dynamic Programming

Incorporating Passenger Sell-Up Behavior

by

Chiu Fai Wilson Tam

B.S., Civil and Environmental Engineering University of California, Berkeley (2006)

Submitted to the Department of Civil and Environmental Engineering in partial fulfillment of the requirements for the degree of

MASTER OF SCIENCE IN TRANSPORTATION at the

MASSACHUSETTS INSTITUTE OF TECHNOLOGY June 2008

© 2008 Massachusetts Institute of Technology. All rights reserved..

MASSACHUSETTS INSTEt-TE OF TECHNQLOcY,

JUN

12

2008

LIBRARIES

ARCHI•VE

A uthor: ... ...Department of Civil and -nnvironm tal agineering May 9, 2008

Certified by ...

Peter P. Belobaba Principal Research Scientist, Department of Aeronautics and Astronautics Thesis Supervisor

Certified by ...

Cynthia Bamhart Professor, Department of Civil and Environmental Engineering and Co-Director, Operations Research Center

Accepted by ...

Daniele Veneziano Chairman, Departmental Committee on Graduate Students

Airline Revenue Management Based on Dynamic Programming Incorporating Passenger Sell-Up Behavior

by

Chiu Fai Wilson Tam

Submitted to the Department of Civil and Environmental Engineering on May 9, 2008 in Partial Fulfillment of the Requirements for the Degree of Master of Science in Transportation ABSTRACT

Low-fare carriers with simplified and unrestricted fare structures have rapidly grown and captured an important share of demand in the markets they enter, forcing legacy carriers to inevitably simplify their fare structures to avoid distraction of their competitiveness. Consequently, traditional Revenue Management (RM) systems, which assume independent demand of fare classes, have become less effective for legacy carriers in dealing with passengers who tend to purchase the lowest fare available in the absence of distinctions among fare products.

This thesis studies two RM optimization algorithms based on dynamic programming, Lautenbacher DP (DPL) and Gallego-Van Ryzin DP (DP-GVR), that aim to control fare class closure using maximum expected revenue. The underlying principle of both DP methods considers the actual arrival pattern of passengers as a Markov decision process. DPL assumes independence of fare classes as do traditional RM methods, and determines which classes should be open for a given time frame. DP-GVR considers the fact that passengers may sell-up or buy down between fare classes, and determines which fare class should be the lowest class open for a given time frame.

The goal of this thesis is to evaluate the effectiveness of DPL and DP-GVR when they account for sell-up, using not only arbitrary sell-up assumptions but also estimated sell-up rates. Based on results obtained with the Passenger Origin-Destination Simulator (PODS), we compare the performance of both methods to traditional methods under various competitive settings.

Simulation results in a single origin-destination market demonstrate the potential of DPL over traditional methods when high passenger sell-up rates are assumed or estimated. The use of DPL achieves as much as 7.3% revenue improvement over EMSRb with Q-Forecasting at high demand. In contrast, the performance of DP-GVR is weaker especially against an advanced RM method, regardless of sell-up input or estimator used. On the other hand, results from a bigger network illustrate that an airline that practices DP-GVR performs much better against both simple and advanced competing RM methods. We conclude that the performance of the theoretically appealing DPL and DP-GVR depends on the environment in which they are used, the types of passenger sell-up estimator employed, as well as the Revenue Management method applied by the competitor.

Thesis Supervisor: Dr. Peter P. Belobaba

Title: Principal Research Scientist, Department of Aeronautics and Astronautics Thesis Reader: Dr. Cynthia Barnhart

Title: Professor, Department of Civil and Environmental Engineering; Co-Director, Operation Research Center

Acknowledgements

I must express my sincere gratitude to my research advisor, Dr. Peter Belobaba, for

bringing me to the world of revenue management. This thesis would not be possible

without his continuous guidance and support. I really appreciate the research opportunity

he has given me during my tenure at M.I.T and his tolerance of my mistakes. His vast

knowledge of the airline industry and professional intuition towards revenue management

has contributed tremendously to my research findings.

I must thank Craig Hopperstad, the creater of the Passenger Origin-Destination

Simulator on which my results are based, for his technical support and patience in his

explanations of sophisticated PODS techniques during our discussions. My understanding

of the dynamic programming methodologies would not be complete otherwise.

I must also hereby extend my appreciation to the members of the PODS Consortium

that include Air France-KLM, Air New Zealand, Continental Airlines, LAN, Lufthansa,

Northwest Airlines, SAS, and Swissair. At the 3 PODS conferences that I participated in,

their representatives provided invaluable advices regarding my results and guidance on

future research based on their professional experience in the real world. Special thanks

are given to Bill Brunger of Continental Airlines for his caring and enjoyable stories

during our stay in Frankfurt, Los Angeles, and Auckland.

I am blessed to have the opportunity to study in M.I.T. This 2-year journey has never

been easy, but my focus has been on becoming a better person through learning from

mistakes in both my profession and interactions with people. Special thanks are given to

the PODS team (Matt, Charles, Fabien, Claire) for their full support in my research and

thesis. I also treasure all the friendships and love from the MST program (Shiyin, Shunan,

Joanne), ICAT (James, Emmanuel, etc), HKSS, CSSA, and Friday-Basketball (Yaoqi,

Jianye, Wenjun, Jingbo, Tiejun, Sheng, etc). My mandarin would not have improved

immensely without the help of many of you!

Last but not least, I must heartily thank my family and friends back home in the Bay

Area and Hong Kong for their unconditional love and support. Thank you for always

being there for me whenever I lost my path in the dark. This thesis is dedicated to my

mother, who has invested her entire life on developing me to become who I am today.

Table of Contents

LIST OF FIGURES 11

LIST OF TABLES 15

LIST OF ABBREVIATIONS 17

CHAPTER 1: INTRODUCTION 19

1.1 Overview of Airline Revenue Management ... 19

1.2 Evolution of the Airline Industry... 21

1.3 Forecasting and the Concept of Sell-Up... ... 23

1.4 The Need for a Dynamic Programming Approach ... 24

1.5 Objectives of the Thesis... 25

1.6 Structure of the Thesis ... 25

CHAPTER 2: LITERATURE REVIEW 27 2.1 Evolution of Revenue Management Methods ... 27

2.1.1 Seat Allocation Algorithms ... ... 28

2.1.2.1 Leg-Based Fare Class Control ... ... 28

2.1.1.2 Network Origin-Destination Fare Class Control ... 29

2.1.2 Advent of the LCC Model and Fare Simplification ... 31

2.2 Dynamic Programming Based RM methods ... 32

2.2.1 Standard Lautenbacher DP method ... 34

2.2.2 Gallego-Van Ryzin DP method... ... 36

2.3 Forecasting methods and Recent Developments ... 39

CHAPTER 3: DYNAMIC PROGRAMMING RM AND FORECASTING METHODOLOGY 41 3.1 Standard Lautenbacher DP ... 43

3.1.1 Q-Forecasting method ... 44

3.1.2 Hybrid-Forecasting method ... 47

3.1.3 Optimizer Based on DPL algorithm ... ... 49

3.1.4 Fare Adjustment ... 53

3.2 Gallego-Van Ryzin DP ... 55

3.2.1 Optimizer Based on DP-GVR algorithm... .... 55

CHAPTER 4: SIMULATION ENVIRONMENT 61

4.1 Overview of the PODS Structure ... ... 61

4.2 Probabilities of Sell-up in PODS ... ... 65

4.2.1 Q-Forecasting in PODS ... ... 67

4.2.1.1 Forecast Prediction Estimator... ... 70

4.2.1.2 Inverse Cumulative Estimator ... 72

4.2.2 Hybrid-Forecasting in PODS... ... 74

4.3 Seat Inventory Control in PODS ... ... 75

4.3.1 Adaptive Threshold ... 75

4.3.2 Fare Class Yield Management (FCYM) ... 75

4.3.3 Displacement Adjusted Virtual Nesting (DAVN) ... 76

4.4 DP Optimizers and Fare Adjustment in PODS ... 77

4.5 Chapter Summ ary ... ... 80

CHAPTER 5: SIMULATION RESULTS 81 5.1 Single M arket ... ... 82

5.1.1 Overview of Single M arket ... 82

5.1.2 Test Case 1: A gainst AT90 ... 83

5.1.2.1 Specifications of Base Case and Simulations... 83

5.1.2.2 DPL with Standard Leg Forecasting vs. AT90 ... 85

5.1.2.3 DPL with Q-Forecasting vs. AT90 ... 86

5.1.2.4 DP-GVR vs. AT90 ... 88

5.1.2.5 Investigation of DP methods against AT90 ... 91

5.1.3 Test Case 2: Against EMSRb with Q-Forecasting ... 97

5.1.3.1 Specifications of Base Case and Simulations... 97

5.1.3.2 DPL with Q-Forecasting vs. EMSRb with Q-Forecasting ... 98

5.1.3.3 DP-GVR vs. EMSRb with Q-Forecasting ... 100

5.1.3.4 Investigation of DP methods against EMSRb with QF ... 102

5.2 N etw ork D 6 ... 112

5.2.1 Overview of Network ... 112

5.2.2 Test Case 3: Against AT90 ... 114

5.2.2.1 Specifications of Base Case and Simulations ... 114

5.2.2.2 Investigation of DP methods against AT90 in Network D6 .... 115

5.2.3 Test Case 4: Against EMSRb with QF and Fare Adjustment ... 121

5.2.3.1 Specifications of Base Case and Simulations... 121

5.2.3.2 Investigation of DP methods against EMSRb with Q-Forecasting and Fare Adjustment in Network D6 ... 122

5.2.4 Test Case 5: Against Symmetric RM Method ... 127

5.2.4.1 Specifications of Base Case and Simulations ... 127

5.2.4.2 Investigation of DP methods against Symmetric RM methods in Network D6 ... 128

CHAPTER 6: CONCLUSION 133

6.1 Summary of Thesis Objectives ... 133

6.2 Summary of Results ... 134

6.3 Directions for Future Studies ... 138

6.3.1 Validation of DP methods in Mixed-fare Networks ... 139

6.3.2 Improvement of Sell-Up Estimators ... ... 140

List of Figures

Figure 1: Third G eneration RM S ... 28

Figure 2: Spiral-Down Effect ... 32

Figure 3: The Standard Lautenbacher DP method (DPL) ... ... 36

Figure 4: The Gallego-Van Ryzin DP method (DP-GVR) ... . 38

Figure 5: Traditional Revenue Management Process... ... 42

Figure 6: Example of an optimal policy based on a DP algorithm ... 43

Figure 7: Q-Forecasting Process flow-chart... ... 47

Figure 8: Hybrid-Forecasting process flow-chart ... ... 48

Figure 9: Bookings-to-come forecasts processed in DPL optimizer ... 50

Figure 10: Modeling the arrival pattern of passenger types in DPL... 52

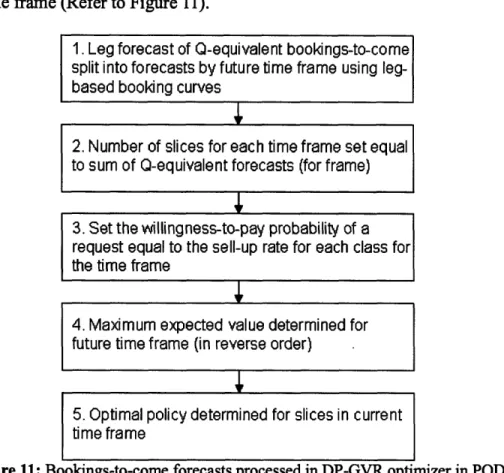

Figure 11: Bookings-to-come forecasts processed in DP-GVR optimizer in PODS... 56

Figure 12: Example of lowest fare class to be open based on DP-GVR... 59

Figure 13: PO D S A rchitecture... 62

Figure 14: Booking Arrival Curves by Passenger Type ... 64

Figure 15: Willingness-To-Pay Curves by Passenger Type... 65

Figure 16: Relationship between FRAT5 and WTP Curves... 66

Figure 17: Typical FRAT5 Curve... ... 67

Figure 18: Different sets of FRAT5 Curves in PODS... 68

Figure 19: Forecast Prediction Estimator Flow Chart... ... 72

Figure 20: Inverse Cumulative Estimator Flow Chart ... 74

Figure 21: Nested Bookings Limits ... ... 76

Figure 22: FA FRAT5s Values with Different Scaling Factors... 79

Figure 23: Route Map of the Single Market Case ... ... 82

Figure 24: Base Case Fare Class Mix of Airline 1 against AT90 in Single Market... 84

Figure 25: Revenues for DPL with Std. Leg Forecasting against AT90 in Single M arket ... . . . 85 Figure 26: Fare Class Mix for DPL with Std. Leg Forecasting against AT90 in Single

M ark et ... 86

Figure 27: Revenues for DPL with Q-Forecasting against AT90 in Single Market ... 87

Figure 28: Fare Class Mix for DPL with Q-Forecasting against AT90 in Single Market ... ... ... ... 88

Figure 29: Revenues for DP-GVR against AT90 in Single Market ... 90

Figure 30: Fare Class Mix for DP-GVR against AT90 in Single Market ... 90

Figure 31: Load Factor and Yield for DP-GVR against AT90 in Single Market ... 91

Figure 32: Revenue Comparison of Best Cases for different RM methods with FRAT5-C against AT90 in Single M arket ... 92

Figure 33: FRAT5 Curves for input FRAT5-A, FRAT5-C, and FRAT5-E ... 93

Figure 34: Sensitivity of different RMs to input FRAT5 sets against AT90 in Single M ark et ... ... 93

Figure 35: Impacts of Fare Adjustment on DPL with Q-Forecasting against AT90 in Single M arket ... 95

Figure 36: Revenue gains and Load Factors of RM methods against AT90 in Single Market using different methods of Sell-up Estimation ... 96

Figure 37: Comparison between Average Estimated FRAT5 Curves and input FRAT5 Curves for DP-GVR against AT90 in Single Market... . 97

Figure 38: Revenues for DPL with Q-Forecasting against EMSRb with Q-Forecasting in Single M arket ... ... ... 100

Figure 39: Fare Class Mix for DPL with Q-Forecasting against EMSRb with Q-Forecasting in Single M arket ... ... ... 100

Figure 40: Revenues for DP-GVR against EMSRb with Q-Forecasting in Single M ark et ... ... ... ... 10 1 Figure 41: Fare Class Mix for DP-GVR against EMSRb with Q-Forecasting in Single M ark et ... 10 2 Figure 42: Sensitivity of FRAT5 values against EMSRb with Q-Forecasting in Single M ark et ... ... . ... 103

Figure 43: Revenue Comparison of Best Cases for different RM methods with FRAT5-C against EMSRb with Q-Forecasting in Single Market ... 103

Figure 44: Impacts of FA aggressiveness on DPL with Q-Forecasting against EMSRb with Q-Forecasting in Single Market... 104

Figure 45: Revenue gains and Load Factors of RM methods against EMSRb with Q-Forecasting in Single Market using different methods of Sell-up Estim ation ... ... ... 105 Figure 46: Comparison between Average Estimated FRAT5 Curves and input FRAT5

... ... ... 1 0 5 Figure 47: Fare Class Closure Rates for DP-GVR against EMSRb with Q-Forecasting

in Single M arket ... . 107 Figure 48: Cumulative Bookings by Fare Class for DP-GVR against EMSRb with

Q-Forecasting in Single M arket ... 107 Figure 49: Fare Class Mix for DP-GVR against EMSRb with Q-Forecasting at

D em and Factors 0.8 and 1.0 ... 108 Figure 50: Fare Class Mix for DPL with Q-Forecasting against EMSRb with

Q-Forecasting at Demand Factors 0.8 and 1.0 ... 109 Figure 51: Fare Class Closure Rates for DPL with Q-Forecasting against EMSRb with

Q-Forecasting in Single M arket ... 109 Figure 52: Fare Class Closures of DP-GVR against EMSRb with Q-Forecasting at

various input FRAT5 sets and corresponding Cumulative Bookings by

F are C lass ... 111 Figure 53: Route Map for Airline 1 (left) and Airline 2 (right) in Network D6...113 Figure 54: Fare Class Mix of Base Case in Network D6 ... 115 Figure 55: Revenue Summary of different RM methods against AT90 in Network D6..116 Figure 56: Load Factors and Yields of Airline 1 using different RM methods against

AT90 in N etw ork D 6 ... 117 Figure 57: Comparison between Average Estimated FRAT5 curves and input

FRAT5-C for DP-GVR against AT90 in Network D6 ... 118 Figure 58: Comparison of Fare Class Closure Rates between DP-GVR with IC and

EMSRb/FA with QF and IC against AT90 in Network D6 ... 119 Figure 59: Comparison of Cumulative Bookings by Fare Class between DP-GVR

with IC and EMSRb/FA with QF and IC against AT90 in Network D6 ... 120 Figure 60: Comparison of Fare Class Mix between DP-GVR with IC and EMSRb/FA

with QF and IC against AT90 in Network D6 ... 120 Figure 61: Fare Class Mix of Base Case against EMSRb with QF-FP and FA in

N etwork D6 ... 122 Figure 62: Revenue Summary of different RM methods against EMSRb with QF-FP

and FA in Network D6 ... 123 Figure 63: Load Factors and Yields of Airline 1 using different RM methods against

EMSRb with QF-FP and FA in Network D6 ... ... 124 Figure 64: Comparison between Average Estimated FRAT5 curves and input

FRAT5-C for DP-GVR against EMSRb/FA with Q-Forecasting in

N etw ork D 6 ... ... 125 Figure 65: Fare Class Closures and Fare Class Mix for DP-GVR with IC estimator

against EMSRb/FA with QF-FP in Network D6 ... 126 Figure 66: Fare Class Closures and Fare Class Mix for DP-GVR with FP estimator

against EMSRb/FA with QF-FP in Network D6 ... ... 126 Figure 67: Revenue, Load Factor, and Yield for different RM methods against

Symmetric RM method in Network D6 ... 129 Figure 68: Results for different RM methods using input FRAT5-C against Symmetric

RM method in Network D6 ... 130 Figure 69: Flow Charts of DAVN and DAVN/DPL RM methods... 140

List of Tables

Table 1: Example of Restricted Fare Product (AA, BOS-SEA, 10/1/2001) ... 20

Table 2: Example of Less restricted Fare Product offered by LCC ... 22

Table 3: Example of Less restricted Fare Product offered by a legacy carrier ... 23

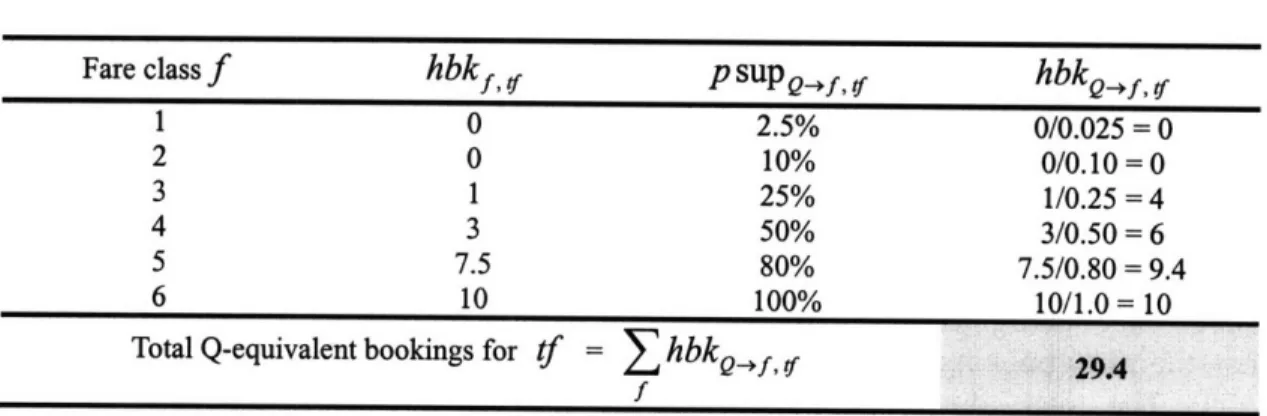

Table 4: Example of calculating Q-equivalent bookings in time frame tf ... 45

Table 5: Example of calculating mean potential class forecasts in time frame tf ... 46

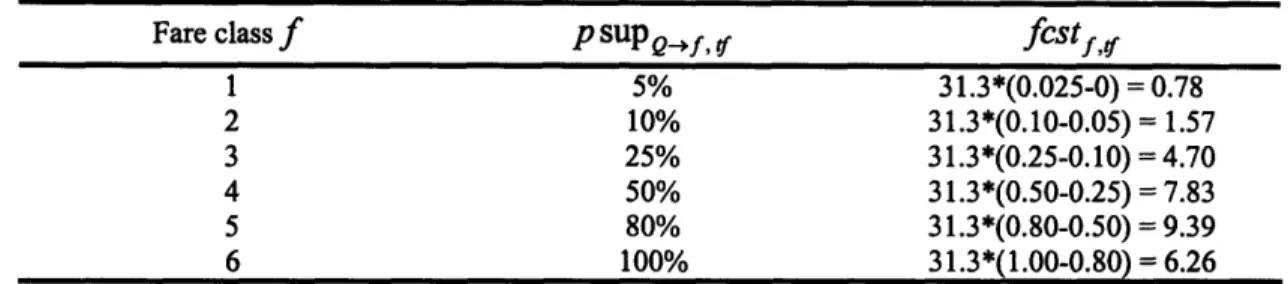

Table 6: Example of calculating forecasted bookings-to-come in time frame tf ... 46

Table 7: Example of Arrival rate of class bookings in current time frame... 51

Table 8: Example of computing the expected revenue for DPL... 51

Table 9: Computation of psame from Zfactor adjustment ... 53

Table 10: Example of Arrival rate of class bookings in current time frame... 58

Table 11: Example of computing the expected revenue for DP-GVR... 58

Table 12: Booking Process Time Frames ... ... 63

Table 13: Example of Calculating Observed Sell-up Probabilities in FP estimator... 70

Table 14: Example of Calculating Observed Sell-up Probabilities in IC estimator ... 73

Table 15: Fare Structure and Restrictions in Single Market... 83

Table 16: Specifications of Test Case 1 (Against AT90, Single Market) ... 84

Table 17: Base Case Results of Airline 1 against AT90 in Single Market ... 84

Table 18: Results of DPL with Std. Leg Forecasting against AT90 in Single Market at D em and Factor 1.0... . 85

Table 19: Results of DPL with Q-Forecasting using FRAT5-C against AT90 in Single M ark et ... 87

Table 20: Results of DP-GVR using FRAT5-C against AT90 in Single Market ... 89

Table 21: Revenue gains for different RM methods with FRAT5-C against AT90 in Single M arket ... 92

Table 22: Specifications of Test Case 2... ... ... 98

Table 23: Base Case Results of Airline 1 against EMSRb with Q-Forecasting in Single M arket ... 98 Table 24: Results of DPL with Q-Forecasting (FRAT5-C) against EMSRb with

Q-Forecasting (FRAT5-C) in Single Market... ... 99

Table 25: Results of DP-GVR (FRAT5-C) against EMSRb with Q-Forecasting (FRAT5-C) in Single M arket... ... ... 101

Table 26: Revenue gains for RM methods against EMSRb with QF in Single Market... 103

Table 27: Fare Structure and Restrictions in Network D6 ... 114

Table 28: Specifications of Test Case 3 ... 115

Table 29: Base Case Results of Airline 1 against AT90 in Network D6 ... 115

Table 30: Revenue gains of Airline 1 against AT90 in Network D6... 117

Table 31: Specifications of Test Case 4... 122

Table 32: Base Case Results of Airline 1 against EMSRb with QF-FP and FA in N etw ork D 6 ... ... 122

Table 33: Revenue gains of Airline 1 against EMSRb with QF-FP and FA in Network D 6... ... . . . ... ... ... 123

Table 34: Specifications of Test Case 5... 128

Table 35: Revenue gain for different RM methods against Symmetric RM method using Estimated FRAT5s as compared to AT90 vs. AT90 in Network D6...129

Table 36: Revenue gain for different RM methods against Symmetric RM method using FRAT5-C as compared to AT90 vs. AT90 in Network D6 ... 130

Table 37: Summary of Revenue gains over FCFS using FRAT5-C at Low demand in Single M arket ... ... ... 135

Table 38: Summary of Revenue gains over FCFS using FRAT5-C at High demand in Single M arket ... 135

Table 39: Summary of Revenue gains over AT90 base using FRAT5-C at High dem and in N etwork D6 ... .... 137

Table 40: Summary of Revenue gains over AT90 base using FP Estimator at High dem and in N etw ork D 6 ... .137

Table 41: Summary of Revenue gains over AT90 base using IC Estimator at High dem and in Network D6 ... ... 137

List of Abbreviations

ALF AP ASM AT90 BTC CAB CFP DAVN DAVN/DPL DF DFW DP DP-GVR DPL DWM EMSRb FA FC FCFS FCYM FP FRAT5 FT HBP HF IC KI KS Fix LCC Loco LP MDP MR MSP NetBP NLCAverage Load Factor Advance Purchase Available Seat Mile

Adaptive Threshold of 90% Load Factor Bookings-to-Come

Civil Aviation Board

Conditional Forecast Prediction estimator Displacement Adjusted Virtual Nesting

Displacement Adjusted Virtual Nesting with DPL control Demand Factor

Dallas-Fort Worth International Airport Dynamic Programming

Gallego-Van Ryzin Dynamic Programming Lautenbacher Dynamic Programming Decision Window Model

Expected Marginal Seat Revenue Fare Adjustment

Fare Class

First Come First Serve

Fare Class Yield Management Forecast Prediction estimator

Fare Ratio at which 50% of passengers will sell up Fixed Threshold

Heuristic Bid Price Hybrid-Forecasting

Inverse Cumulative estimator

Karl Isler's discrete Marginal Revenue Fare Adjustment Ken Sejling's modification to Fare Adjustment

Low Cost Carrier

Lowest Competitor Open Class Linear Programming

Markov Decision Process

Thomas Fiig's continuous MR Fare Adjustment Minneapolis-St. Paul International Airport Network Bid Price

OD PE PODS ProBP QF R1, R2, R3 RM RMS RPM SAS SF TF WTP Z-Factor Origin-Destination Price Elasticity

Passenger Origin-Destination Simulator Prorated Bid Price

Q-Forecasting

Minimum-Stay, Change-fees, and Non-Refund. Restrictions Revenue Management

Revenue Management System Revenue Passenger Mile

Scandinavian Airlines

Scaling Factor of Fare Adjustment Time Frame

Willingness-to-Pay

Chapter 1

Introduction

The goal of this thesis is to evaluate the revenue benefits of using dynamic programming based models in airlines' revenue management systems. Airlines have been looking for ways to improve models of passenger behavior in their systems, which is a challenge to airlines since the industry has evolved to the point where the assumptions made in the original systems are no longer valid. Despite recent developments to improve traditional models, revenues generated may still be non-optimal, and new optimizers that eliminate those assumptions may be required to reach optimality.

We will employ a simulation approach using the Passenger Origin-Destination Simulator (PODS), originally developed by Hopperstad, Berge, and Filipowski at the Boeing Company, to model the airline booking process with competing carriers trying to maximize passenger revenues over different competitive network configurations. Further development has been conducted by the PODS Consortium, a partnership between Massachusetts Institute of Technology and eight major international airlines.

1.1

Overview of Airline Revenue Management

Revenue management, or yield management, serves to design and manage service products to maximize revenue (Weatherford, 1991). It is an effective scheme to allocate a

service provider's relatively fixed capacity and to achieve increased earnings from segmented markets. In the context of the airline industry, by thoroughly understanding customers' "willingness-to-pay" (WTP), airlines implement revenue management to maximize revenue by attracting as many high fare passengers as possible and filling up the airplanes at the same time. Ticket pricing, seat allocations, and overbooking are some important elements of a revenue management system. In the rest of this thesis, the term revenue management (RM) will be used as a synonym for seat allocation aspect of the

The concept of revenue management can be traced back to four decades ago, when American Airlines implemented a computer reservation system (SABRE) in 1968, which had the capability of controlling reservations inventory (Smith et al., 1992). During that period when the airline industry was regulated and the Civil Aeronautics Board (CAB) controlled all fares, reservation controls practiced by many airlines emphasized primarily controlled overbooking to reduce revenue loss due to no shows. The lack of flexibility to decide fare structures and fares consequently led to competition on service provision, trying to capture passengers through better quality of service and higher frequency. Simple inventory control was first practiced in early 1970s when British Oversea Airways Corporation (known as British Airways nowadays) began to deviate from single fare product and introduce discounted fares for reservations that were made twenty-one days before flight departure (McGill and van Ryzin, 1999).

The widespread development of revenue management came after the Airline Deregulation Act of 1978. This act loosened governmental control of airlines prices and schedules, and has led to more complicated fare structure offerings with sets of restrictions that included (1) advance purchase, (2) Saturday night minimum stay, (3) change fee, and (4) non- or limited refundability of cancelled bookings. Airlines have also differentiated fare classes by offering classes with different cabins and level of services, such as the First Class, the Business Class, and the Economy Class. Table 1 shows an example of a restricted fare structure offered by American Airlines for its BOS-SEA market in 2001.

Advance

Round Fare ($) Class Purchase Minimum Stay Change Fee Comments

458 N 21 days Sat. Night Yes Tue/Wed/Sat

707 M 21 days Sat. Night Yes Tue/Wed 760 M 21 days Sat. Night Yes Thu-Mon 927 H 14 days Sat. Night Yes Tue/Wed 1001 H 14 days Sat. Night Yes Thus-Mon 2083 B 3 days None No 2X OW

2262 Y None None No 2X OW

2783 F None None No First Class

Table 1: Example of Restricted Fare Product (AA, BOS-SEA, 10/1/2001)'

Using RM systems, airlines can determine how many seats to allocate initially to each fare class and how to dynamically adjust this allocation as bookings arrive and the departure time of the flight approaches (General Accounting Office, 1999). One key to maximize an airline's revenue is to keep the right number seats available for the full-fare business passengers who make reservations relatively close to the departure date, and prevent them from buying lower fare class available even if they meet all restrictions. Another key is to capture leisure passengers who have flexible schedules and are only willing to buy lower fare tickets. The seat allocation problem developed from the challenge of selling seats within the same cabin of a flight at different prices to the

customers of different fare classes. Airlines protect some seats away from the lower revenue fare classes in order to be able to satisfy demands from the higher revenue

classes (Belobaba, 1998).

In addition, deregulation of the airline industry triggered a major restructuring of networks that further complicated seat allocation. Under deregulation the airlines moved to develop a hub and spoke system that often had passengers flying into a hub on their way to their final destination. The revenue management system must take into account that some seats on flights between cities must be reserved for connecting flights. Since then, airline revenue management systems have developed significantly from single-leg control to origin-destination, or network, control. New information technologies have played a critical role in the development of revenue management, and have led to more sophisticated revenue management capabilities. Since airline deregulation, revenue management techniques have had a significant impact on the development of in the industry, providing up to 4% to 10% increase in company revenues (Fuchs, 1987). For example, in 1997, American Airlines collected one billion dollars by implementing revenue management, representing most of the company's profit (Cook, 1998).

As mentioned above, seat allocation is one of the three major aspects of typical revenue management practices. RM is developed to address the problem that prices are usually substantially affected by external factors such as prices set by the competitors. To avoid losing market share, few legacy carriers nowadays are actually willing to set their fare structures substantially different, even if optimal, from what are practiced by their legacy counterparts or low-cost carriers. An effective seat capacity control results in revenue gains that may compensate for the limitation of price options and is thus necessary.

1.2

Evolution of the Airline Industry

Network legacy carriers (NLCs) traditionally apply RM to fully-restricted fare structures assuming demands for each fare product are independent and segmented. However, over the past few years, low-cost carriers (LCCs) with simplified or unrestricted fare structures have managed to capture an important part of the demand in the markets they enter. For example, they may set their fare scheme as simple as charging one-way tickets half that of round-trips and far less differentiated than that of legacy carriers. They also have lower operating costs and can offer low-fare products and frequent service on popular routes. An example of a less restricted fare product offered by Southwest Airlines is shown in Table 2.

Advance

Round Fare ($) Class Purchase

Purchase

Minimum Stay Non-Refund Comments178 M 3 days 1 Night Yes Special Sale

402 H 7 days 1 Night Yes

438 Q 14 days None Yes 2X OW

592 B 7 days 1 Night Yes Off-Peak

592 B 7 days 1 Night Yes Peak

634 Y None None No Unrestricted

Table 2: Example of Less restricted Fare Product offered by LCC (SWA, PVD-SEA, 10/1/2001)1

Furthermore, the air traffic demand has changed in recent years - there have been huge losses of business traffic, and passenger willingness to pay has been decreasing. This trend can be accounted for by a number of factors, most notably the economic downturn since 2000. The loss of business bookings has lead to a serious decline in the average fare. In addition, both fuel prices and labor cost surges have placed most major airlines in financial jeopardy. Most of the largest US airlines have undergone bankruptcy protection, and the industry has reached a point where changes have to occur in the firm of consolidation, bankruptcy, and liquidation for U.S. major airlines. The surviving airlines have been trying to reduce their costs and at the same time increase their revenues in order to end the downturn of the current industry cycle.

To make the situation worse for legacy carriers, passengers are now getting an increased amount of information through the Internet. Online travel consolidating sites, such as Travelocity, Expedia, and Orbitz, enable LCCs to offer their discount fare much easier than before; higher level of transparency is provided to customers who can easily compare fare products of different airlines before making their booking decisions.

Full-fare passengers prefer to buy down to the lowest available class open of its competing airline, a low-cost carrier or a matched legacy airline, that offer fare structures with few restrictions and relatively cheaper prices. In response to these developments, legacy carriers have departed from their traditional differentiated, fully restricted products and matched the simpler fare structures set by LCCs. As a result, for markets where LCCs are present, legacy carriers would likely match some if not all fare structures of their competitors to avoid losing too much market share and revenue. In other words, fare structures of legacy carriers have become less-restricted by allowing certain fare classes to have same types of restrictions (or no restrictions) but differ by price only. Means of matching include compression of fare ratios, and total or partial removal of restrictions and advance purchase requirements. Table 3 shows an example of less restricted fare product by Delta Air Lines in 2005.

One-Way Fare One-Way Fare Booking Class AdvanceAdvance Minimum Stay Change Fee ($) Comments

($) Purchase

124 T 21 days None 50 Non-Refund

139 U 14 days None 50 Non-Refund

184 L 7 days None 50 Non-Refund

209 K 3 days None 50 Non-Refund

354 B 3 days None 50 Non-Refund

404 Y None None No Full Fare

254 A None None No First Class

499 F None None No First Class

Table 3: Example of Less restricted Fare Product offered by a legacy carrier (DAL, BOS-ATL, 4/2005)1

Between 2000 and 2004, fares decreased on average by 31% in U.S. markets where LCCs reached 10% market share (Geslin, 2006). Based on the analysis of the fare data of the largest six legacy carriers of the United States, ECLAT Consulting found that the collapse in business revenue accounts for virtually all of the revenue loss the carriers have suffered (Aviation Daily, 05/2004). The need exists to improve the RM currently practiced to adapt to evolution of fare products and passenger behavior.

1.3

Forecasting and the Concept of Sell-Up

The objective of forecasting is to estimate bookings-to-come by fare class and by flight using historical unconstrained data obtained from previous booking records of the same flight. Forecasts need to be as accurate as possible in order for revenue management systems (RMS) to work optimally. In the absence of restrictions among fare products, the general trend is that passengers purchase in the lowest fare available, making it difficult for a conventional RMS to segment demand for different fare classes in its optimizer.

One way to address this problem is to apply the concept of sell-up probability, which is defined as the probability that a passenger is willing to buy a ticket at a higher fare for the same flight if the fare product of the initial booking request is closed. By taking this probability into consideration, the RM optimizer will close down lower fare classes whenever necessary and protect more seats for higher fare passengers, and passengers will higher willingness to pay higher fare will sell-up.

1.4

The Need for a Dynamic Programming Approach

Most traditional airline revenue management methods consider two types of booking passengers: (1) business passengers who are price-inelastic but may buy down to fare class at price lower than their WTP under simplified fare structure, as we discussed in the previous section, and (2) leisure passengers who are price-oriented but may be flexible to

sell-up to the next lower fare classes open.

Traditional RM models assume that the arrival of fare class bookings is sequential in increasing order. That is, the closer the booking process approaches departure date, the more the bookings that come from business passengers and flexible, discount-fare passengers who are willing to sell-up. However, if the assumption of sequential bookings arrival is incorrect, or if passengers' flexibility to sell-up does not necessarily increase over time, then those methods may not generate optimal results.

Furthermore, conventional methods consider that passengers buy in all open fare classes no matter what the lowest open fare class is, but in unrestricted fare structures they will only buy in the lowest available fare class open. Consequently traditional RM methods are unable to distinguish between business and leisure demand, making airlines difficult to reach revenue optimality under less differentiated fare structures. Clearly, besides modifying traditional RM models to incorporate the concept of sell-up, the need exists to develop a new optimization method to determine what the lowest open class should be at each time of the booking process by considering demand that may potentially purchase the lowest fare class open at any particular time.

Much research effort has focused on deriving booking limit algorithms using dynamic programming that eliminate the assumptions of segmented fare class demand and sequential bookings. Methods based on dynamic programming consider the actual demand arrival pattern of passengers as a Markov decision process (Stidham et al., 1999). They divide the reservation processes into multiple decision periods, each of them small enough for one booking request, and decide whether or not to accept the request using dynamic programming optimization algorithms, the output of which can translate into an optimal protection of fare classes. Formulations of the two DP methods examined in this thesis are presented in more depth in §3.1 and §3.2.

1.5

Objectives of the Thesis

The objective of this thesis is to study the performance of two revenue management methods based on dynamic programming in unrestricted fare environments, namely the Standard Lautenbacher DP method2 (DPL) and the Gallego-Van Ryzin DP method3 (DP-GVR). Both the two DP methods and several traditional RM will be implemented in our simulations. Experimental results obtained from the simulator will be used to evaluate the performance of DP-based RM under various competitive settings.

As mentioned in §1.3, considering the concept of sell-up in the forecast and in the optimization process will allow more seats to be protected for higher fare passengers and force them to sell-up when they will be denied booking for this initial request. The key is to figure out how to use these sell-up probabilities accurately, and how to estimate them dynamically throughout the entire forecasting period as inputs in RM. Several advanced forecasting methods are included in the simulations. We also explore the efficacy of adapting these forecasting methods to competition by dynamically estimating the passengers' willingness to sell-up when competition comes into play.

All simulations and quantitative evaluations will be performed by the Passenger Origin-Destination Simulator (PODS), first developed by Hopperstad at the Boeing Company. Various levels of control over the passenger choice model, the environment of interest, and the airline RM methods settings are the main components that make the simulated booking process of an airline as accurate as possible.

1.6

Structure of the Thesis

This thesis will be divided into three major parts: (1) the literature review, (2) a discussion of revenue management method based on dynamic programming and the adaptive approaches to demand and sell-up forecasts, (3) and an analysis of the results of DP-based simulations with those modified forecasters and Fare Adjustment.

Chapter 2 presents a discussion of previous work done on airline revenue management with an emphasis on the problem of unrestricted fare environment examined in this thesis. Topics covered in this chapter include forecasting techniques, traditional revenue management models, and a discussion of recent work on developing dynamic models in seat allocation problems.

2 Lautenbacher and Stidham (1999)

Detailed methodologies for the dynamic programming based models incorporating recent development of forecasting techniques are presented in Chapter 3. Chapter 4

describes an overview of the Passenger Origin-Destination Simulator (PODS), and the simulation environments related to the new DP methods that are used to obtain statistical reports on traffic and revenue generated by the carriers.

In Chapter 5, we evaluate the performance of two dynamic programming methods by comparing outputs obtained from those simulation tests with results of previous studies. Such outputs include total revenue from bookings, load factors, fare class mixes, fare class closure patterns, and booking patterns by time before departure.

Finally, Chapter 6 serves to summarize the findings of this thesis and the potential of the use of dynamic programming in airline revenue management. Directions for future research are proposed as well.

Chapter 2

Literature Review

Airlines offer various fares to capture demand coming from different market segments and different time of seasons. Because of the keen competition in the airline industry since deregulation, competitors' fares often limit the ability of airlines to effectively segment demand. Revenue management has since become as indispensable tool to generate economic gain for airlines. Solely under the control of airlines, an effective seat inventory control determines optimal seat allocation strategies among fare classes. Major carriers worldwide have committed tremendous effort to design and study optimal seat allocation policy over the past two decades.

This chapter starts by reviewing the evolution of Revenue Management in traditional environments. We then present the advent of new fare environment associated with the emergence of low-cost carriers and the need of changes to both conventional optimization and forecasting methods. Finally, we will specifically focus on two dynamic programming based models to be used for simulations, Lautenbacher DP method (DPL) and Gallego-Van Ryzin DP method (DP-GVR). They are widely theoretically promising optimization tools to improve airline revenues.

2.1

Evolution of Revenue Management Methods

The first generation of Revenue Management systems appeared in the early 80s in the form of databases that airlines used to collect, store, and keep track of bookings. The second generation of RMS arrived in the mid-80s when airlines were able to follow bookings prior to a flight departure and compare to expected booking patterns. Thanks to the advances of operations research during the late 80's and early 90's, the third generation of RMS was born with three important revenue management components: (1) Overbooking, (2) Forecaster, and (3) Seat Allocation Optimizer (Refer to Figure 1). Using database of historical bookings, overbookings, cancellations, no-shows, and fare structures, the RM optimizer generates the optimal booking limits for each flight and fare class. More information about the evolution of RMS in the airline industry can be found in McGill and van Ryzin (1999), Barnhart et al. (2003), and Talluri and van Ryzin (2004).

Figure 1: Third Generation RMS4

2.1.1

Seat Allocation Algorithms

The fundamental problem of the seat inventory control lies in managing the fixed and shared inventory of seats on a leg, so that a sufficient amount of seats are saved at full fare for passengers who are willing to pay higher fares, and seats that are not expected to be sold at low demand can be sold at discounted fares to passengers with lower WTP. There are two basic types of approaches for addressing the seat inventory control problem: leg-based models and network Origin-Destination models.

2.1.2.1 Leg-Based Fare Class Control

The application of fare class mix allocation to the seat inventory control problem was first developed for the case of a single-leg, two-fare class environment by Littlewood (1972), and subsequently extended by Buhr (1982), Richter (1982), and Wang (1983) to problems with multi-leg networks and multiple fare types. This commonly used approach is based on the concept of "serial nesting" of fare classes. Instead of allocating seats to partitioned classes, nesting protects seats for higher fare classes by limiting the number of seats sold in the lower fare classes according to demand forecast and expected seat revenue for each class.

Belobaba (1987) and Belobaba (1989) later developed a more generally applicable solution framework to the nested seat allocation problem that works with any number of fare classes using the concept of Expected Marginal Seat Revenue (EMSR). He 4 Barnhart et al. (2003)

subsequently updated the framework that allows for joint upper classes to be protected from the next booking class right below, the algorithm known as EMSRb that has since become a prevalently used industry standard for establishing booking limits on a flight leg basis. Optimal formulations for the multi-nested class problem have been developed by Brumettle and McGill (1988), Curry (1990), Wollmer (1992), and Robinson (1995), whose results show that the nested booking limits produced by much simpler, computationally practical EMSRb techniques are indeed close to optimality.

The EMSRb method involves weighing expected seat marginal revenues, defined as "the expected fare of the booking class under consideration multiplied by the probability that demand will materialize for this incremental seat" (Belobaba, 1992), for each fare class and used them to derive leg-based protection levels for those fare classes. In other words, seats are protected for a booking fare class so long as the expected marginal of those seats is greater than or equal to the fare of the next lower class. Early simulation tests by Wilson (1995) show that implementing the leg-based EMSRb methods in a symmetric single market environment generated revenue benefits to the airline as well as the industry as a whole. Thorough description of the EMSRb heuristic can be found in Belobaba and Weatherford (1996).

The basic EMSRb algorithm is classified as a leg-based model because all legs are assumed to carry one itinerary. However, for most airlines that sell multiple-leg itineraries, their inventory is shared not only among fare classes but also between local and connecting passengers. The next advent in the development of RM from control by leg and fare class alone to joint control by both fare class and path is known as the Origin-Destination control. A path is defined as a set of single flight legs that comprise an itinerary between an origin and a destination within a network.

2.1.1.2 Network Origin-Destination Fare Class Control

For an airline that applies leg-based inventory control to accept a booking coming from a connecting itinerary, seats for all legs of the itinerary have to be available in the same fare class. Priority can thus be given to local passengers on a given flight leg at the expense of connecting passengers even though they may have higher contribution to the total revenue. O-D control models have been developed to account for network effects and produce booking limits of fare classes in an effort to maximize total revenue as opposed to yield. This approach is particularly important in the hub-and spoke networks that have

flourished after deregulation of airline operations.

Optimal formulations mentioned in §2.1.1.1 for the multi-class problem have been extensively solved at the network level during the 80s. Glover et al. (1982) first framed the problem to be a large network flow problem that identifies flows on paths that maximize revenue using deterministic demand. Wollmer (1986) extended the model to implement with stochastic demand. Curry (1990) further extended Glover's formulation by formulating for multiple legs with multiple nested fare classes using continuous

demand distribution, but assumed that capacities cannot be divided among nests for each path. Brumelle and McGill (1988) extended the models by Wollmer that assume discrete demand distribution, and found an optimal solution to a leg with multiple nested fare classes. There are both theoretical and practical difficulties in applying these models in real airline settings. Williamson (1992) and McGill and van Ryzin (1999) have performed critical reviews of these network optimization algorithms.

There are two approaches of Origin-Destination control models in common practice - virtual nesting methods and bid-price methods. The concept of "virtual bucketing" was initially developed by Williamson (1992), Vinod (1995), and Smith and Penn (1998). The initial idea was to nest all local and connecting fares of a given leg in various hidden buckets, known as virtual buckets, in the airline's own inventory system grouped by fare. Booking limits of each bucket is then determined by a leg-based inventory control model (EMSRb) using path forecasts aggregated into virtual buckets

-demand forecasts for a given O-D routing. However, as these approaches gave higher priority to connecting passengers with higher fare, they did not address the situation that the connecting passenger may displace two local passengers whose total contribution to the overall revenue may actually be higher.

The Displacement Adjusted Virtual Nesting (DAVN) method, an adjustment to virtual bucketing made by Wysong (1988) and Smith and Penn (1998), addresses the problem based on the Network Revenue value, which is defined as the total itinerary fare minus the expected displacement cost that might occur on other legs when a request for a multiple-leg passenger is accepted on a given leg. These expected displacement costs are

obtained by solving linear programming (LP) models, and the displacement-adjusted fares are put in virtual buckets. Williamson (1992) suggested a variety of methods to calculate those displacement costs. These displacement cost techniques were further refined by Tan (1994), and further developments can be found in Wei (1997) and Lee (1998). While incorporating network effects, inventory control algorithm is still implemented at the leg level. Further details about virtual bucketing and DAVN can be found in Lee (1998) and Belobaba (2002).

Another approach to O-D inventory control was the use of bid prices developed by Simpson (1989), Williamson (1992), and Smith and Penn (1998). The bid-price is calculated by summing up the displacement cost associated with each crossed leg in a given itinerary. In other words, the bid-price is the sum of the marginal values for an incremental seat on the all the legs of a given itinerary, local or connecting. Instead of generating protection levels for fare classes, the Bid-Price Control provides a standard as to the minimum amount an airline should accept a booking request - the request will be accepted if the bid-price is lower than the O-D fare, and will be rejected otherwise. Specific bid price algorithms consist of the Network Bid Price (NetBP) method, the Heuristic Bid Price5 (HBP) method, and Prorated Bid Price6 (ProBP) method.

2.1.2 Advent of the LCC Model and Fare Simplification

The success of low-cost carriers in recent years has had a significant impact on legacy carriers throughout the world. The major difference between the fare structure of low-cost carriers and that of a legacy carrier is the degree of demand segmentation. While legacy carriers typically offer multiple fare products ranging from high to low fare with various restrictions and capture higher revenue gains by inducing passengers to pay fares close to their WTP, LCCs have relatively much lower cost structures that allow them to offer unrestricted product structure and still be profitable. To avoid loss in market share for markets where a LCC is a competitor, legacy carriers are often forced not only to match fares but also simplify their own fare structure by removing certain restrictions and/or reducing the advance purchase requirements. Detailed analyses of comparison between traditional legacy carrier and LCC business models are provided in Gorin (2000), Weber Thiel (2004), and Dunleavy and Westermann (2005).

Ratliff and Vinod (2005) suggested that in this new competitive environment, the revenue management systems of legacy carriers based on segmented market structures have made it difficult for them to effectively segment demand, as legacy carriers are often compelled to match the fare structures and sometimes the lowest fare seat availability of their LCCs counterparts. More information about lowest open class matching can be

found in Lua (2007).

As restrictions separating business and leisure passengers into their corresponding fare classes are removed, passengers naturally buy the lowest fare available regardless of their WTP. Boyd and Kallesen (2004) call these demand segments price-oriented and product-oriented passengers. Product-oriented demand refers to passengers who purchase a fare based on the product (i.e. restrictions and advance purchase requirements) it represents. Traditional RM methods assume independent fare class bookings in this behavior. Price-oriented demand, in contrast, corresponds to passengers who purchase at the lowest available fare regardless of product restrictions.

Hence, under less differentiated fare structures, the fundamental assumptions of traditional RM methods are violated because as business passengers are more willing to purchase at the lowest fare available when restrictions among fare classes become less differentiated, the traditional RM methods no longer can distinguish price-oriented from product-oriented passengers based on historical booking data. It becomes impossible to produce accurate independent demand forecasts for the higher fare classes. As a result, the forecaster produces a lower projection of higher fare demand, causing the optimizer to protect fewer seats in the higher fare classes and make more seats available for the

lower fare classes. This "buy-down" phenomenon leads to an iterative effect known as "spiral-down", causing the airline that implement the traditional RM methods to generate

lower total revenue after each cycle (Ozdaryal and Saranathan, 2004) (Refer to Figure 2). Cooper et al. (2003) and Kleywegt et al. (2004) develop mathematical models of the spiral down effect that occurs when traditional forecasting methods are used. Further detailed analyses about the buy-down phenomenon and spiral-down effect can also be

found in Cusano (2003) and C16az-Savoyen (2005).

1. Under undifferentiated fare structure,

customers buy down to the lowest fare available

2 F 'a r b d,. b k, li h -q. inJ k -. •

I,,,-5. More observed bookings in and associated revenues decrease lower fare classes. Spiral-down

continues

3. Forecaster predicts lower demand for high fare classes

4. Optimizer decreases protection for higher fare classes as demand has shifted to lower fare classes

Figure 2: Spiral-Down Effect

2.2

Dynamic Programming Based RM methods

Most traditional airline revenue management methods assume that the arrival of fare class bookings is based on a predetermined, sequential order. That is, the closer the booking process approaches departure date, the more the bookings that come from business passengers and flexible, discount-fare passengers who are willing to sell-up. In addition, seat capacity control based on these models assumes that passengers' willingness to sell up is generally stable or increasing over time. Zhao and Zheng (1998) show that if this assumption is true, then traditional RM methods can lead to close to optimal results.

However, if the assumption of sequential bookings arrival is incorrect, or if passengers' flexibility to sell-up does not necessarily increase over time, then traditional methods likely lead to non-optimal solutions. This is particularly the case when a matching to LCC fare structures induces passengers with high WTP to buy down to lower

fare classes. Dynamic programming models are theoretically the preferred optimization approach to seat allocation problems as they assume passengers to arrive in any order and consider explicitly the arrival process of passengers.

In developing RM methods based on dynamic programming, Stidham et al. (1999) consider the actual demand arrival pattern of passengers as a Markov decision process. They divide the reservation processes into multiple decision periods, each of them small enough for one booking request, and decide whether or not to accept the request using dynamic programming optimization algorithms, the output of which can translate into an optimal protection of fare classes.

Revenue management based on dynamic programming was initially developed by Mayer (1976), whose model divides the booking process into multiple periods and assumes that in each period, the discount-fare demand always arrives prior to the full-fare demand. Gerchak et al. (1985) study a two-class dynamic seat allocation problem using constant demand rates. Lee and Hersh (1993) consider a discrete-time, multiple-class dynamic seat allocation model with nonstationary demand, and further extend to allow group booking. Fare class demand is modeled as a Poisson process, while the entire booking process is modeled through a Markov Decision process. In other words, the state of the system is dependent only on the remaining time prior to departure as well as the remaining capacity at any given point in time.

Stidham et al. (1999) extend Lee and Hersh to allow cancellations and no-shows of passengers. The above models use discrete-time formulations, assuming that there is at most one arrival (or cancellation) in each period. Zhao and Zheng (1998) and Liang (1999) found a solution to Lee and Hersh multiple-class model framework but with continuous time. Bertsimas and Popescu (2003) design dynamic optimization techniques based on stochastic demand for multiple classes using bid-prices from a linear programming relaxation. Bertsimas and de Boer (2005) propose a stochastic gradient algorithm and approximate dynamic programming ideas to improve the existing nested seat allocation by EMSRb.

Vanhaverbeke (2006) examined two revenue management methods based on dynamic programming in PODS under fare structures with few or no restrictions: (1) the Standard Lautenbacher approach (DPL) developed by Lautenbacher (1999), and (2) the Gallego-Van Ryzin approach (DP-GVR) that was proposed by Gallego and van Ryzin (1997). We will focus on these two dynamic programming approaches in this thesis, as described in the following section.

2.2.1

Standard Lautenbacher DP method

The Standard Lautenbacher DP method (DPL) is a basic model developed at the single leg level and several papers mentioned above work as an extension to this model. However, this model incorporates important components common to all of the existing dynamic programming models and thus serves as a backbone when it comes to analyzing the performance of dynamic programming compared with non-dynamic traditional RM methods. Thus, DPL does not consider cancellations, overbooking, or no-shows.

Lautenbacher and Stidham (1999) develop a discrete-time, finite-horizon Markov Decision Process (MDP) to solve the single-leg revenue management problem by backward induction on the remaining time before departure. The booking period is divided into N decision periods in such a way that, during each decision period, the probability of two or more requests is negligible. These decision periods are numbered in reverse order, with period N corresponding to the start of the booking period, and period

0 corresponding to the scheduled departure time.

Each of the K fare classes, 1, 2,..., K, may arrive throughout the reservations horizon. At the moment a request arrives, the decision to accept or reject involves three factors: (1) remaining capacity, (2) remaining decision periods before scheduled departure, and (3) the fare class of the request. Fare class demand is modeled as a Poisson process, but request arrivals are generated based on independent MDP. Price for various fare classes are denoted as p1 , p2, ..., P' , with pf being the price for the lowest fare class.

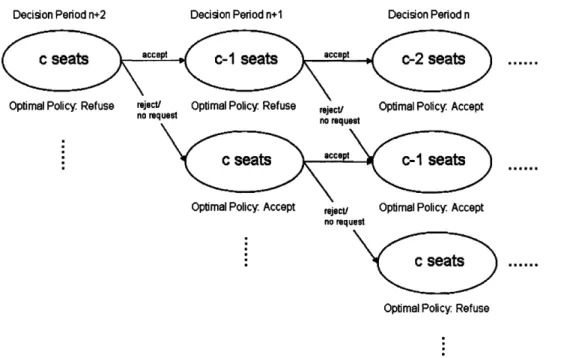

Maximum expected revenue is denoted as R,(b)wheren corresponds to the decision period 0, 1, ... , N, and b denoting the number of booking requests that have been accepted. C is the capacity of the single flight leg. (Refer to Figure 3)

The general idea is that for each fare class f there is a probability Pf,, that a request will arrive for this fare class during decision period n. P0,, is the probability that no booking request occurs for any fare classes during decision period n. If the request is accepted, the accepted fare Pj is contributed to the maximum expected revenue for the next decision period n -1. In other words, the maximum expected revenue for the next time frame is R,n1(b+l1) if the request is accepted, and Rn-(b)

otherwise. The maximum expected revenue for a given time frame with certain realized bookings is calculated by accounting for the probability that an accepted booking, a rejected booking, or no booking request may occur. The following algorithm summarizes the Standard DPL:

K

PI=. =1

K

R, (b)= = Pf, -max{Rn-I(b +1)+ p , R,_, -(b))+ Po, . R.-I(b.

f=1

with the boundary conditions:

Ro

(b)

0

if b_

C,

- R (b -C) if b > C,

whereR > maxf p }

At each booking arrival, the potential revenue generated with accepting the request is weighed against the expected future revenue loss due to the removal of that seat from the available capacity. The expected marginal seat revenue of the (b + 1)th seat in decision period n -1 when there are b realized bookings is defined as:

A_, (b) = R-_, (b) - R-_, (b + 1) Bf,1 =min(b O: A-_,(b)>p J

where

B,,. _C

Optimal booking limits, Bf,,n for DPL are produced by backward induction. The policy is to accept a class

f

request in decision period n if and only if the condition 05 b < Bf,. holds. DPL is developed and applied more appropriately for fully or less-restricted environments because the model, like traditional RM methods, assumes independent demand for fare classes. Implementation of DPL in PODS simulations will be performed and analyzed in §3 and §4.Decision window Fares

Fare Class Pi,n: Prob. of a Bkg Expected revenue Expected revenue request in FC i, TF n if accepted if refused

1

P

1,n

Rn.-(b+ 1) +

p,

Rn-i(b)

2 P2,n Rn-(b+l) + P2 Rn-l(b) f Pf,n Rn-1(b+1) + p, Rn-1(•) K PK,n Rn-1(b+1) + PK Rn-l(b) Nobody pon Rn-(b ) shows up P K Rn(b)=

f-1 Pf, n. Max{ Rn-1(b+1) + pf, Rn1 (b)} + PO, n Rn-1(b) Decision variable: b: Number of bookingsFigure 3: The Standard Lautenbacher DP method (DPL)7

2.2.2

Gallego-Van Ryzin DP method

While the DPL model is applied more appropriately for fully restricted environments because of the assumption of demand independence among fare classes, the Gallego-Van Ryzin DP model (DP-GVR) is appropriate in fully unrestricted fare environments. RM methods that assume independence of segmented demand, including DPL, consider that passengers buy in all open fare classes irrespective of what the lowest open fare class is. In an unrestricted fare setting, however, passengers only buy in the lowest available fare class. Consequently these RM methods may not reach optimality in less-restricted fare structures.

Instead of allocating seats for each fare class, the objective of DP-GVR is to determine the lowest class that should be open at any given time. Optimal booking limits are determined only by the probability of sell-up by the passengers. Under an unrestricted fare structure in which there is no restrictions among fare classes which differ only in price, passengers will purchase in the lowest open fare classes. The DP-GVR model assumes that no passengers buy a ticket higher than the lowest open fare.

Gallego and van Ryzin (1997) first frame the problem and explain how to dynamically find an optimal pricing policy in a fare environment with only stochastic, price-oriented demand. Gallego and van Ryzin (2004) conclude that pricing policies

7 Vanhaverbeke (2006) IIiililllllllllllllillltlll n=O .- " --"i Best expected revenue in Time-Frame (n-l) when b bookings occured Bookings