MIT LIBRARIES

D£\NEVll

3

9080 03317

5941

Massachusetts

Institute

of

Technology

Department

of

Economics

Working

Paper

Series

THE

CRISIS:

BASIC

MECHANISMS,

AND

APPROPRIATE

POLICIES

Olivier

Blanchard

Working

Paper

09-01

December

29,

2008

Room

E52-251

50

Memorial

Drive

Cambridge,

MA

021

42

This

paper

can be

downloaded

withoutcharge

from

theSocial

Science

Research Network Paper

Collection at http://ssrn.con-)/abstract=1324280

w

The

Crisis:

Basic

Mechanisms,

and

Appropriate

PoHcies*

Olivier

J.Blanchard^

December

2008

Abstract

The

purpose of this lecture is to look beyond the complex events that characterize the global financial and economic crisis, identify the basic mechanisms, and infer the policies needed to resolve the currentcrisis, as well as thepolicies needed toreduce the probability ofsimilar events in the future.* "Munich

lecture'", delivered on November 18, 2008. I thank Stijn Clae.ssens, Giovanni DeH'Ariccia, Giaiuii de Nicolo, Haiiiid Faruqee, Luc Laeven, Krishna

Srinivasan, and

many

othersintheIMF

ResearchDepartmentfordiscussionsand help. I thank Ricardo Caballero. Cliarle.? Calomiris, Steve Cecchetti, Pi-ancesco Giavazzi. Anil Kashyap,Arviud Kri.shuanunthy.Andrei Shleifer, andNancyZim-merman, for discussions along tlie way. I thank loannis Tokatlidis for research assistance,

t

Digitized

by

the

Internet

Archive

in

2011

with

funding

from

Boston

Library

Consortium

IVIember

Libraries

It is

much

too early to give a definitive assessment of the crisis, notleast becauseit isfar from over. It is not too early

however

to look forthe basic

mechanisms

that have taken uswhere

we

are today,and

tothink

about

the policieswe

need to implement,now

and

later. Thisis

what

1 shall try todo

in this lecture.Take

it forwhat

it is, a first pass ill the midst ofthe action.'Figure

1IniliatSubprime Losses and SubsequentDeclinesInWorldGDP

and World StockMarket Capitalization(inTrillionsUSDollars)

EstimateofSubprimeLosseson Loans EstimateofCumulativeWorldGDP DeclineinWorldStockMarket andSecuritiesby 10/Z0O7 loss Capitalization9/07to10/08

SourceIMF GlobalFinancial StabilityReport, Wotid EconomicOutlookNovemberupdateand estimates, World Federationol

Exchanges.

The

bestway

of motivatiiij; tlic lecture is to start with the chart inFigure 1.

The

first l^ar (which is barely visible)shows

the estimated losses on U.S.subprime

loansand

securities, estimated as ofOctober

2007.at about $250billion dollars.

The

secondbarshows

theexpected1. Ill the interest of full disclosure: This is a first pass by an economist who, until rccentl.y, thought of financial intermecHation as an i.ssue ofrelatively little

cumulative loss in world output associated with the crisis, based

on

current forecasts. This loss is constructed as the

sum,

over allcoun-tries, of the expected cumulative deviation of output from trend in

each coimtry, based

on

IMF

estimatesand

forecasts of output as ofNovember

2008. for the years 2008 to 2015.Based

on these forecasts,thecumulativeloss isforecast to run at$4,700billion dollars,so about

20 times the initial

subprime

loss.The

third bar siiows the decreasein the value of stock markets,

measured

as thesum,

over all mar-kets, ofthe decrease in stockmarket

capitalization from July 2007 toNovember

2008. This loss is equal toabout

$26,400 billion, so about 100 times the initialsubprime

loss!The

question is an obvious one:How

could such a relativelylimitedand

localized event (thesubprime

loancrisis in the United States) haveeffects ofsuch

magnitude on

theworld

economy?'

To

answer this question, I shall proceed in four steps.First, by identifyingthe essential initial conditions which have

shaped

thecrisis. Isee

them

as fourfold: theunderestimation of riskcontainedin

newly

issued assets; the opacity of the derived securitieson

thebalance sheets of financial institutions; the connectedness

between

financial institutions, both within

and

across countries; and, finally,the high leverage ofthe financial system as a whole.

Second,

by

identifying the two amplificationmechanisms

behind the2. Ironically, theother shock which dominatedthe ncw.s until thefinancial crisis

led totheoppositecjuestion:

How

couldtheverylargeincrea,se inoilpricesfromthe early 2000s tomid-2008have sucha small apparent impacton economic activity?After all, similar increases are typically blamed for the very deep recessions of the 1970sand early 1980s. Theplausible answer, whichIshall notexplore in this lecture, but isvery muchworth exploring, mustbe that the economy hasbecome less fragile in somedimensions, more fragile in others.

' 'i' ; I. ,1 ;

crisis,oncethetrigger

had been

pulledand

some

oftheassetsappearedbad

or doubtful. Iseetwo

related, but distinct,mechanisms:

first, thesale of assets to satisfy liquidity runs

by

investors; and, second, thesale of assets to reestablish capital ratios. Together with the initial

conditions, these

mechanisms

ca.n lead,and

indeed have led, to verylarge effects of a small trigger on world

economic

activity.Third, by

showing

h(}w the amplificationmechanisms

have played outin real time,

moving

fromsubprime

to other assets, from institutionsto institutions,

and

from the United States, first to Europe,and

thento emerging countries.

Fourth, by turning to policies. It is too late to change the initial

conditions for this crisis... So, current policies should be

aimed

atlimiting the

two

amplificationmechanisms

atwork

at this juncture.Future regulation

and

policies should alsoaim however

at avoiding a repeat ofsome

ofthose initial conditions. In short,we

need to bothfight current fires

and

reduce the risk of fires in the future.1

Initial

Conditions

The

trigger for the crisiswas

the decline in housing prices for theUnited States. But, in the years preceding, four evolutions

had

com-binedtopotentially turnsuchapricedeclineinto a

major

world crisis.1. A.s,set.s were created, sold,

and

bought, which iippenicdmuch

lessConditional on no housing price decline,

most subprime

mortgages appeared relatively riskless:The

value ofthemortgage

might be highrelativeto theprice ofthe house, but it

would

slowly decline over timeas prices increased. In retrospect, the fallacy of the proposition

was

in its premise: If

and

when

housing prices actually declined,many

mortgages

would

exceed the value of the house, leading to defaultsand

foreclosures.^Why

did the peoplewho

took these mortgages,and

the institutionswhich

held them, so underestimate the true risk?Many

explanationshavebeengiven,

and

many

potential culpritshave beennamed.

To

listsome

ofthem: Large saving by Chinese households, leading to a low world mterest rate,and

thus a "search for yield" by investorsdisap-pointed with the return on truly safe assets; large private

and

pul)liccapital inflows into the United States in search of safety, leading

sup-pliers to offer

what

looked like safe assets to satisfy thedemand;

tooexpansionary a

monetary

policy in the United States, with theim-plicit promise oflow interest rates for a long time; the "originate

and

distribute"

model

ofmortgage

financing, leading to insufficient mon-itoringby

the loan originators.Each

ofthese explanations contains a grain oftruth, but only a grain.Why

would

a low world interest ratenecessarily lead to "search for yield"?

Why

shouldAlan

Greenspan

have set a higher

US

interest rate, if low interest rates reflected low equilil:)iium world rates,and

therewas

no pressure on inflation?Why

should investors havebought

mortgages fromoriginators iftheyknew

that monitoring

was

deficient?3.

On

the relation between property values, mortgage.s, and foreclosui'es, read Foote et al [2008JI suspect that the

fundamental

explanation ismore

general. History teaches us that benigneconomic

environments often lead to creditbooms,

and

to the creation of marginal assetsand

the issuance of marginal loans. Borrowersand

lenders look at recent historicaldis-tributions of returns,

and

become

more

optimistic, indeed tooopti-mistic

about

future returns.''The

environmentwas

indeed benign inthe 2000sin

most

ofthe world, withsustainedgrowth

and

low interestrates.

And,

looking in particularatUS

housing prices, both borrowersand

lenders could point to the fact that housing priceshad

increased every year since 1991.and had done

so even during the recession of2001.^

Nor was

thisunderstatementof riskconfined tosubprime

loans.Credit defaultswaps

(CDS), whichsound

complex

but are ineffect insurancepolicies, were issued against

many

risks. For low premia, firmsand

institutions could insure themselves against specific risks, be it the

risk of default by a firm, by a financial institution, or by a country.

And

CDS

issuers werehappy

to accept these low premia, as theyassumed

the probability ofhaving topay

outwas

nearly negligible.2. Securitization led to

complex

and hard

to value assets on the bal-ancesheets offinancial institutions.Securitization

had

started nuich eaxliei', butchanged

scale in the lastdecade. In mid-2008,

more

than60%

of all U.S. mortgages werese-curitized. In the

mortgage

market, mortgages were pooled to form4. For an analysis ofcredit. Ijoonis and hnsts over a large number of countries,

.see Claessens et al [2008].

5.

A

point that CharlesCalorniris [2(J08] hascalled "plausihie deniahilit\-" (that prices wouldever go down).mortgage-basod securities

(MBS), and

theincome

streamsfrom thesesecurities were separated ("tranched") further to offer

more

or lessrisky flows to investors.

Figure 2, taken from the 2007

IMF

GlolDal Financial StabilityReport

(GFSR)

gives a sense of the complexity of that part of thefinan-cial system. It

shows

how

initial mortgages were securitized, cut intranches,

and

thenheld by various investorsand

financial institutions, with different degrees of risk aversion.Going

through the variousar-rows

would

take the rest of the lecture.''My

intent is simply to give avisual impression ofthe complexity of the financing arra.ngements.Figure

2.Mortage

Finance

Bough! hy

more

risk-MtkiiiK i^vL^Ul^^

Rou«hhv Uilh ,1icr

h..,.-seeking ioMMiirs

r

—

" ABrprondiiil.s/SIVshuyABS

andissue

shori-lurm dehi i SubpniiiL-1"/(;.Ji-rt Sul>|)riiiH' Suhprijiw Servicer Slit)prililt

l*ndcr BuiJu/irin-tJrirtttil

linr.iiatiiinluiis/SIVs ; * .Vrriu^.-O-'i"" "l*"*^'-//-.,. jJ: ,!.,.. Sll-U.IUK t i f,n..r,nnM'-lIl'' liisuren. AHS.lfvt»llJ.'lll hyCTM^S.11^ ir.iiichv'diiuf ..inicnirvJ

If

SIV' 1/1 lpi>^\^ equii. r niKhihyli'-s sk^s^H-'kioL nviisiiirs s nK)s livi.ssuiiigdt^lii Hinj^Jiib risk-SI illVLS kiiiuSource.

Adapted

from Figure 1.10:Mortgage Market Flows

and

RiskExposures''

Chapter

I, p. 11,October

2007

GFSR.

Why

did securitization take off in such away?

Because it was,and

still is, a

major

improvement

in risk allocationand

a fundamentallyhealthy development. Indeed, looking across countries before the

cri-sis,

many

(includingme)

concludedthatthe U.S.economy

would

resista decrease in housing prices better tlian

most

economies:The

shockwould

be absorbed by a large set of investors, rather than just by afew fina,ncial institutions,

and

thus bemuch

easier to absorb... This arginnent. ignored two aspects which turned out to be important.The

first waij that, with complexity,

came

opacity.While

itwas

possibleto assess the valueofsimple

mortgage

pools (theMBS),

itwas

harderto assess the value ofthe derivedtranched securities (the

CDOs),

and

even harder to assessthe value ofthe derived securities resulting from

tranches of derived securities (the

CDO^s).

Thus, worries about theoriginal mortgages translated into large uncertainty about the values

ofthe derived securities.

And,

in that environment, the fact that thesecuritieswere held

by

alarge set of financial institutions implied thatthis large uncertainty affected a large

number

ofbalance sheets in theeconomy.

3. Securitization

and

globalization led toincreasingconnectedness be-tween financial institutions, both withinand

across countries.In the

same

way

securitization increased connectedness acrossfinan-cial institutions, globalization increased connectedness of financial

in-stitutions across countries.

One

of the early stcnies uf the crisiswas

the surprisinglylargeexposure of

some

regionalGerman

bankstoU.S. suliprime loans.But

the reality goes far l)eyoiul tins anecdote.major

fiveadvanced

countries, an increase from $6.3 trillion in 2000to $22 trillion

by June

2008. In mid-2008, claimsby

thesebanks

juston emerging market

countriesexceeded $4 trillion.Think

ofwhat

thisimplies if, for

any

reason, thosebanks

decided to cuton

their foreignexposure; unfortunately, this is indeed

what

we

are seeingnow

(the figure stops inJune

2008.Much

of the decrease hashappened

sincethen.) •

Figure

3ConsoMcfatad Foreign ClaimsolReportingBanks ontheRestoltheWorld eyNaiionalllv otReportingBanks.Trillions oTUSdoQars

<a*# p^1?i'o"' &»'^'S^jS'^fS'^J" ^sf.d*S*"»S''i'J'^ # tJ's?"J*^o^5^ ^P'^#:*

*?'/<if^o'" x^'i-'''<^*'Q'f'«?'=•'

V*""^'©-^*^'1^"<,^</-1^^/'b*'*©^*'''v**'';."''o='^'^/'i?''ci^•»*v»^ fb*'

o''*'**/

1

—

France - Germany~"^J^pan UnlladKingdom- United Slates(Source: Table 9a,

BIS

Banking

statistics)4. Leverage increased.

The

fourth important initial conditionwas

the increase in leverage.Put

another way, financial institutions financed their portfolios withWhat

werethe reasons behind it? Surely, optimism,and

theunderes-timation of risk,

was

again part of it.Another

important factorwas

a

number

of holes in regulation. For example,banks

were allowed to reduce required capital bymoving

assets offtheir balance sheets in so called "structured investment vehicles" (SIVs). In 2006, for example,the value of the off-balance sheet assets of Citigroup, $2.1 trillion,

exceeded the value of the assets on the balance sheet, $1.8 trillion.

(By

mid

2008, writedownsand

returns ofsome

ofthe assets back tothe balance sheet

had

decreased this ratio back to less than one half.)The

problem went

farbeyond

banks. Fur example, at theend

of2006,"monoline insurers" (that isinsurersinsuring aparticular risk, for

ex-ample

default on municipal bonds), operating outside the perimeter ofregulation,had

capital equal to $34 billion toback insurance claims againstmore

than $3 trillion of assets...Whatever

the reason, the implications of high leverage for the crisiswerestraightforward. If, forany reason, the valueoftheassets

became

lower and/or

more

uncertain, then the higher the leverage, the higher the probability that capitalwould

bewiped

out, the higher theprob-ability that institutions

would

become

insolvent.And

this is, again,exactly

what

we

have seen.2

Amplification

mechanisms

Aromid

the end of2006,US

housingprice indexesstopped risingand

thenstarted decliningmore

steadily. This implied thatmany

marginal mortgages, especially the subprimes extended duringthe previousex-pansion,

would

default.As

we

saw

in Figure 1, the expected lossfrom

10these defaults, as of

October

2007,was

$250 billion.One

might

havehoped

that this losswould

be easily absorbed byfinancial institutions, with limited financialoreconomic

implications. But, aswe

know,

this has not been the case.The

larger crisis isthe result oftwo

amplifica-tion

mechanisms,

interacting with the initial conditions I focusedon

earlier.

1.

The

first amplificationmechanism

is themodern

version of banli runs.Let

me

first go quickly back to basics.Think

of financial institutions in the simplest terms, i.e. with assetson

the left sideof their balance sheet, liabilitieson therightside,and

capitalasthedifferencebetween

the value oftheassets

and

the valueoftheliabilities.So

longas capital is positive, the institution is solvent; if it isnegative, the institutionis insolvent. So,when

the prol^ability ofdefaultonsome

assets increases,both

the expected lossand

the uncertainty associated with the asset side of the balance sheet increases.The

value of capitalbecomes

bothlower

and

more

uncertain, increasing the probability of insolvency.The

first amplificationmechanism

then has two parts:Depositors

and

investors are likely towant

to take their funds outofthe institutions

which

mightbecome

insolvent. In traditionalbank

runs, sayduringthe Great Depression, it

was

thedepositors that tooktheir

money

out of the banks.Two

changes have taken place since then. First, inmost

countries, depositors arenow

largely insured, so they have few incentives to run.And

banks

and

other financialinsti-tutions largely fina.nce themselves in

money

markets, through shortterm

"wholesale funding".Modern

runs are no longer literally runs:What

happens

is that institutions that are perceived as being at riskcan nu longer finance themselves on these markets.

The

result ishow-ever the

same

as in the oldbank

runs; Faced with a decrease in their ability to borrow, institutions have to sell assets.To

the extent that this is amacroeconomic

phenomenon

(i.e. to the extent thatmany

institutionsand

investors are affected at thesame

time), there

may

be few deep pocket investors willing tobuy

assets.If, in addition, the value ofthe assets is especially difficult for outside investors to assess, the assets are likely to sell at "fire sale prices",

i.e. prices below the expected present value of the

payments

on theasset. This in turn implies that thesale oftheassets by oneinstitution

further contributes to a decrease in the value ofall similar assets, not onh" on the l^alance sheet of the institution which is selling, but on

the balancesheets ofall the institutions

which

hold these assets. Thisin turn reduces their capital, forcing

them

to sell assets,and

so on.The

amplificationmechanism

is at work,and you

can seehow

the size ofthe amplification is determinedby

initial conditions:To

the extent that the assets aremore opaque and

thus difficult tovalue, the increase in uncertainty will f)e larger, leading to a higher perceived riskofsolvency,

and

thus toa higher probabilityof runs. For thesame

reasons, finding outside investors tobuy

these assets will bemore

difficult,and

the fire sale discount will be larger.To

the extent that securitization leads to exposure of a larger set of institutions,more

institutions will be at risk of a run.And

finally, to the extent that institutions aremore

leveraged, that is, have less capital relative to assets to startwith, the probability ofinsolvencywillmcrease more, again increasing the probability of runs.As

we

have seen, all thesefactors were very

much

present at the start of the crisis. This iswhy

this ampHfication

mechanism

has been particularly strong.2.

The

second nnipUfication inechnnism conies from the needby

fi-nancial institutions to maintain an adequate capital ratio.

Faced

with a decrease in the value of their assets,and

thus a lowercapital,financialinstitutionsneedtoimprovetheircapitalratio,either

to satisfy regulatory requirements, or to satisfy investors that they

are taking measures to decrease the risk of insolvency. In principle, they then have a choice.

They

can either get additional funds fromoutside investors, additional capital.

Or

they can "deleverage", thatis, decrease the size of their balance sheets, by selling

some

of their assets or reducingtheir lending.In a

macroeconomic

crisis, finding additional private capital is likelyto be difficult. This is for the

same

reasons as earlier:There

may

be few deep pocket investors willing to put funds.And

to the extent that the assets held by the financial institutions are difficult to value,investors will be reluctant to put theii' funds in the institutions that hold them. In that case, theonly option for theseinstitutions is tosell

some

of their assets.The same

mechanism

as before is then at work:The

sale of assets leads to fire sale prices, affecting the balance sheetsofall the institutions that hold them, leading to further sales

and

soon.

And,

for thesame

reasons as before, opacity, connectedness,and

leverage all imply

more

amplification.The

two

mechanisms

are distinct. Conceptually, runscanhappen

even in the absence ofany

initial decrease in the value of assets. This is 13the well-known multiplicity of equilibria: Iffundingstops, assets

must

be liquidated at fire sale prices, justifying the stop in funding in the first place. But, clearly, runs are

more

likely, the higher the doubts about the value of the assets. Conceptually, firmsmay

want

to takemeasures

to reestablish their capital ratio even if they have noshort-term

fundingproblem

and

do not face runs.The

two

mechanisms

interact

however

inmany

ways.A

financial institution subject to arun may, instead of selling assets, cut credit to another financial

in-stitution, which

may

in turn be forced to sell assets. Indeed, one ofthechannels through which the crisis has

moved

fromadvanced

coun-tries to emerging

market

countries has been through cuts in creditlines

from

financial institutions inadvanced

economies to theirfor-eign subsidiaries, forcing

them

in turn to sell assets or cut credit todomestic borrowers.

3

Dynamics

in

Real

Time

The

amplificationmechanisms

arenow

clear, but this is true only inretrospect. In real time,

when

housing prices started dechning,most

economists

and

policymakers

expected the impact to bemuch more

limited.

The

scopeofthe amplificationmechanisms

onlybecame

clearover time. Here is the story in real time.

1. Contagion across assets, institutions,

and

countries.The

widening of the crisis to a steadily growing munlier of assets, nistitutions,and

countries isshown

in Figure 4.The

figure is a "heatmap",

constructed l>v theIMF,

whichshows

the evohition of heat indexes for anumber

of asset classes.The

construction of the index is complex, but the principle is simple:The

larger the decrease in theprice oftheasset, or thehigher thevolatility oftheprice, eachrelative

to its average value in the past, the higher the value of the index.

As

the heat index increases, the color goesfrom

green to yellow to orangeand

to red (corresponding to 1, 2, 3and

4 standard deviationsrespectively, so orange

and

red should be seen as very rare events).The

figure tells the history of the crisis. Starting from the bottom, seehow

the crisis started withsubprime

mortgages in early 2007.extended to financial institutions

and

money

markets (the marketswhere

financial institutionsborrow

and

lend to each other) in thesummer

of 2007, to regularmortgage

pools (PrimeRMBS)

and

cor-porate credit at theend

of 2007,and

to emergingmarket

countriesin the fall of2008.

At

the time of this writing, all classes are in red,showing

an exceptional decrease in pricesand

increase in volatility.2. Increase in counterparty risk.

Figure 5

shows

how

the crisis led to an increase in counterparty riskbetween

banks, i.e. to an increase in the perceived probability that abank

borrowing from anotherbank

may

not be able to repay. It plots the"Ted

spread",which

is the differencebetween

the averagerate charged by

banks

to each other for ,3-month loans (the "Libor"3-month

rate),and

the three-month T-bill rate, the rate at whichthe

government

can borrow, for fourdifferent countries.Note

how

thespreads increased

from

themiddle of2007on, especially inthe UnitedStates

and

the UnitedKingdom, and

how

theyjumped

when

the U.S.Figure

4.Heat Map: DevelopmentsinSystemicAssetClasses Emergingmarkets Corporatecredit PrimeRMBS CommercialIVIBS Moneymarkets Financial institutions SubprimeRMBS '"^%

Jan-07 Jul-07 Jan-08 Oct-08

!IMF, GlobalFinancial StabililyReporl.Oclobei 200B

government

letLehman

Brothers to file forbankruptcy

inSeptember

2008.

Until then, financial markets

had

assumed

thatthegovernment

would

not let large, systemic,

banks

fail.The

failure ofLehman

Brothers,and

the fact that claimson

Lehman

became

frozen for a long time,convinced

them

otherwise, lea.dingto a very largejump

inthe spread.(Note the partial decline at the very end. I shall return to it later.)

Associated withthis largeincrease in perceived counterparty risk,

was

asharp decrease in the maturity ofthe loans that banks were willing to

make

to each other.The

resultwas

the attempt, by each bank, to keepenough

cash onhand and

linrit its reliance^ on borrowing fromother banks.

Figure

5.Counterparty

Risk. 5.0 4.0 3.0 2.0 1.0-TedSpreads:3-monthLiborRateminusT-billRate

(inpercent)

0.0

Sep15.2008

LehmanFiles lorBankruptcy

j

P

'' 1;

us Euro Japan UK

3. Tightening banking standards

One

ofthewa,ys a,financial crisisaffects theeconomy

is throughcredit rationing, i.e. the tightening of lending standardsby banks

who

are deleveraging. This is indeedwhat

has happened.Figure 6

shows

the evolution of an index for changes inbank

lendingstandards in the United States

and

theEuro

Area, for bothmortgage

loans

and

for commercialand

inthistrial loans.The

index, wliich isbased

on

a cjuarterly survey ofbank

loan officers, reflects thediffer-ence

between

the balance ofrespondentsbetween

those wlio sa.y they have "tightened considerably-tightenedsomewhat" and

thosewho

saythey have "eased

somewhat-eased

considerably".The

figureshows

how, since

mid

2008, credit hasbecome

steadily tighter for firmsand

households.

Figure

6.Bank Lending Standards

^^ ^;^ ,t> V^ \^i J-' Vt> ,<^' .-^ fl ivl \^ ^J It^- f"-V -o^ r^^ ,^- V "o^ fV 'l* -^^ 'o' ^,' .-.^ V ^ *^

U.S.:C&lloans -U.S.:Mortgages

ECB Largecompanyloans ECB Mongages

4.

Emerging market

spreadsand sudden

stopsDeleveraging has not been limited todomestic credit. For a longtime after the start of the financial crisis, it looked as if emerging markets

might

beshielded fromthe crisis.The premium

most emerging market

countrygovernments had

to pay relative to theUS

government

(the"sovereign spread")

was

small,and

did not increasemuch.

As

Figure7

shows

however, thingschanged

dramatically in the fall of 2008. In the process of deleveraging,advanced

country banks started drasti-cally reducingtheirexposiu'e toemerging markets, closing credit linesand

repatriating funds.Other

investors did the same.The

sellingwas

acrosstheboard, but not totally indiscriminate:

The

figureshows

tha.tthe

premium

jumped up

substantiallymore

for countries with largecurrent account deficits.

Deleveragingintheformofcapitaloutflows presents additional

macro-economic

problems.Not

onlydo

countrieshavetodealwithadomesticFigure

7.SovereignCDSSpreads

(index7/2/07 =100)

9.'2'07 1l'2'07

Curreniaccountdeticillargerthan5%of2007GDP

Currentaccountsurplus,orsmalldelicil

credit

problem

(asbanks

experience a run,and

themechanisms

we

saw

earlier are at work), but they have to deal witli pressure on theexchange rate. If they have reserves, or if they have access to

for-eign credit, for

example

credit from centralbanks

or loans from theIMF,

they can usethem

to limit the depreciation. Otherwise, theymay

have to accept a large depreciation which, if domestic liabilitiesare

denominated

in foreign currency (which they often are) leads tofurther burdens on debtors, be they households, firms, or financial

in-stitutions.

The

mechanism

is familiar from past crises, especially theAsian crisis,

and

can lead tomajor economic

disruptions. It is playingout in a

number

of countries today.5.

From

the financial crisis to a full-Hedgedeconomic

crisisFor

some

time after the start of the financial crisis, the effects ofthe financial crisis on real activity appeared limittd. This

however

did 19notlast.

Lower

housingprices, lower stockprices, triggered initially bythe decreased stock

market

value of financial institutions, higher risk premia,and

creditrationing,started takingtheirtollin thesecondhalf of2007. In the fall of2008 however, theeffect suddenlybecame

much

uicnt' pronounced.

The

worry that the financial crisiswas

becoming

worse,

and

might lead to another Great Depression, led to adramaticdecreaseinstock markets,

and

toadramatic fall in consmrierand

firm confidencearound

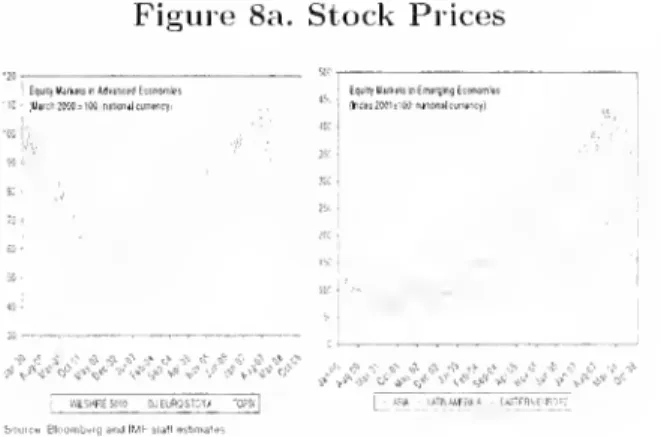

the world.Figure

8a.Stock

Prices

EqurnltartnisrAdvincHjEccnwifc! "^fe 6*=-JB^^.1^ * .^."i'.^ytv*"_»_*'.'j"p,"-".>i* v" /v'*^*ti^^-i^Q*-><,«*«,«?v"-^^/-;** v'"**^

iiiuiceBloumtiBigandIMHslallo^Iiioal^s.

:'i"'^

I

-Witt—

L

ATHocnffA-^5TFn^ElBo'=:'

Figure 8a

shows

the evolution of stock price indexesfrom

marketsboth

inadvanced

economiesand

inemerging

market countri(\s: Aftera long

and

steatiy increase from 2002on. stock prices started decliningm

the second half of 2007,and

then fell abruptly in the fall of 2008.Figiu"e 8b

shows

the evolution of business confidenceand consumer

confidence. It

shows

the dramatic fall in both intlexes, for the United States, the euro area,and

emerging economies, in the fall of2008.These

evolutions haveled inturn toalargedecreaseindemand

and

inFigure

8b.Business

and

Consumer

Confidence

- -UnlwaSt»rt» EmBrglna^conomloi I ;A ./^^^^^-EU(rightscale) U.S. (Inn acaln)output. Figure9

shows

theIMF

growth

forecasts as ofmid-November.

Most

advanced

countriesnow

havenegative growth,and

theforecastsare fornegative

growth

in 2009 (year on year) as well.Emerging

mar-ket countries are forecast to have positive growtli, but

much

lowerthan they have

had

in the past.The

world is clearlynow

facing amajor economic

crisis.Figure

9.RealandPotentialGDPForecastedGrowthRates

for2009;inpercent

-0.4 -0.2

52

hi

Euro Area Japan

SRealGDP@PotentialGDP

Emerging & Developing Economies

,

4

Policies

for

the

short

run

It is clearly too late to change the initial conditions which led to the crisis... Thus, in thinking about policiesfor the short run, the purpose

must

be todampen

the two amplification mechanisms.1.

Dampening

theruns.The way

tolimit runsisconceptuallystraight-forward: It is for the central

bank

to provide liquidity againstgood

(enough) collateral. If they have access to such funds, financial

in-stitutions

do

not need to sell assets at fire sale prices,and

the first amplificationmechanism

does not operate.This isexactly

what

central banks have done, actingas "lendersoflastresort" since the beginning of the crisis. Traditionally, such liquidity

provision

was

limited to banks,and

the list of assets which could be usedas collateralwas

relativelynarrow. VVliat centralbanks

havedone

duringthis crisisistosteadilyincrease boththeset ofinstitutions

and

the list of assets that qualify as collateral. Since mid-2008, the U.S. Federal Reserve, in particular, has pursued a particularly aggressive

liquidity policy.

As

a result, themonetary

base has increased from $841 billion inAugust

2008to $1,433trillion inNovember,

an increaseof $592 billion in four months...

Has

this provision of Ht|ui(lity been successful?The

answer appears largely yes, at least with respect to domestic institutions. However,for countries suffering from capital outflows

—

largely, but not onlyemerging

market

countries—

thingshave beentougher.A

fewcountrieshave

had

access to credit in foreign currencyfrom

themajor

centralbanks, in the

form

ofswap

lines.But

the others havebeen

exposed. Iceland,which

had

averylargebankingsystemrelativetoitseconomy,with assets aiifl liiil)ilili(\s la,rf);(>ly (IcMioiiiiiiat-cd in ciiios, i;)eca,iiic one

of \hv first

major

casualtic's ol' Ihe crisis. I<"a.('(!cl witli runs (in tliis cfise, the inabihty to borrow inmoney

markets)and

not Ix'inf; |)a.rtof the

Evuo and

thus not, lia.viufi, access to the iiquidil y provided hythe

European

Central Bank, the tlireemajor

Icela.nihc l)a,nks weul, bankrupt, creating a deepeconomic

crisis ior the country as a whole.Few

counlries ar(> as exposed as Iceland was.Mut

many

are likely to face similar inns,and

may

need (|Mick a.c;c:ess to ibreign iitiuidity. 2. Asset j)nrchiisrsand

ix'c:ij)ilnli'/.ii1i(iii. 'The provision of li(|iiidity eliminates the first amplification m(>clianisni. it does not however ad-dress the scH'ond,namely

the icestablishment ofcapital rat.icjs.Based

ontheevidence iiom the resolulion ofa largennmbei-ofbanking crisesinalargenumber

oi'count,lies in the past, what, needs to bedone

is fairly well established, and has two components:

First, tlie state must, isolate bad or potentially bad ass(>ts. 'i'heic are

various ajjproaches to doing this.

One

is lo leave tlie a,ssets on the balcUiee sheet, of the institutions, but have the state provide a floorto theii' value,

m

exchange for (^xa)nple h)i' slifUcs in the institution. Another,whit;h 1lintl nujreattra.ctive, is fortiiestate totake theassetsoffthe balance sheet altogether, by buying

them

in exchange forcash,or for' safe assets such as goveiiirnent. bonds.

The

ccutra.l {|uest.ion isthatofthe price at which to i)uy tlicm.

One

can think of twoextreme

prices: the (pre-intcivention) market piice. which

may

well be a, hresale |)ric(> a.nd thus

embody

a large hcinidily discount: or Ih(> I'stimatedexiXHicd |)resenl value

known

as the "iiold to maturity" price.The

right solution is lo set, Ihe piice belwceii these two exilemcs. giving,

on Iheone hand, institutions incentivcs tosell and. on the ot hci' hand.

taxpayers areasonable expectation that, ifthe assets are indeed held

to maturity by the state, they will actually benefit from the purchase

in the long run.

The

effect ofsuch asset purchases istwofold. First, it setsthe value ofthe assets on the balance sheets,

and

by reducing uncertainty, allows investors to better assess the risk of insolvency. Second, it increasestheprice oftheseassetsfromtheirfiresaleprice to

something

closerto theirmulerlying expected value,and

thus improves the balancesheetsofall the institutions which hold these assets, directly or indirectly.

These

purchases arehowever

half ofwhat

needs to be done.Once

the value of the assets is clearer,some

institutionsmay

turn out to be insolvent,and

thus should be closed.Most

arelikely toshow

positive, but too low, capitalizationand

thusmust

be recapitalized. This can bedone

through public funds only or throughmatching

of publicand

private funds, in exchange for shares.The

purpose is to return these institutions to a level of capital so theydo

not need to further deleverage, to further sell assets or cut credit.Where

arewe

today on these two fronts? Forsome

time,governments

saw

the crisis as one ofliquidity, thus a prol)lem to be handled by thecentral banks throughliquidity provision. In thefall of2008. it

became

clear that undercapitalization

was

amajor

issue. InOctober

2008, theUnitedStatesintroduced the "troubledasset relief

program"

(TARP),

allowingtheTreasuryto

buy

assets or injectcapitalup

to $700billion.A

few weeks later, duringan

importantweek

end in October, with meetings both inWashington and

in Paris,major

countries agreed to put in place financialprograms

along the lines sketched above. Since then, France hascommitted

tospend

up

to 40billion euros,Germany

Figure

10. 5.0 4.5 4.0 3.5 3.0 2.5 2.0 1.5 1.0 0.5 O.OTed

Spreads:

3-month

Libor

Rate

minus

T-billRate

-/ \ ^-.J^'- ^

—

-._.-'''^

'

""

- --.__—

-^^

—

_^

, . , 8/1 8/16 8/31 9/15 9/30 10/15 10/30 US Euro JapanUK

|up

to 80 hilliuii eiuDS, the UnitedKingdom,

50 billicjii pcjunds. Inaddition, to alleviate worries about solveney before the

programs

arefully implenrented,

most govenmients

have extended the guarantees accorded to depositors to interbank claims, that is claims ofbanks

onother banks.

The

sizeand

the complexity of the requiredprograms

is enormous,and

many

governments

are still exploring their way. In the UnitedStates in particular, the

TARP

appears to havechanged

directiontwice, with an initial focuson the purchaseoftroubled assets through

auctions, then a shift in focus to recapitalization,

and

in themore

recent past, (for

example

in the case of Citigroup) a reliance on bothproviding a floor on the value of

some

of the assets on the balance sheet,and

recapitalization.Other

programs

appearmore

consistent, but the funds are being disbursed slowly.Are

theseprograms

working?The

vtndict is mixed.As

Figure 10shows, the spread

between

the interbaul'C lending rateand

the T-billrate has decreased, but remains surprisingly high, despite interbank

guarantees,

and

despite recapitalizationofsome

banks. Littlehasbeendone

to dispose ofbad

assets,and

public capital injections have been limited. Uncertainty about the courseand

the details of policy hasmade

private investors hesitant to invest funds withoutknowing

thenature of future public interventions.

The

result is that deleveraging continues, withbanks

continuing to reduce credit,both

domesticand

abroad.

Issues of coordination are also at work.

The

provision of guaranteesfor

some

assets can lead investors tomove

into those assets,mak-ing things worse for non-guaranteed assets.

We

have seen this in theUnited States for non-guaranteed mortgages.

The

provision of guar-antees by one country can lead investors tomove

to that country,making

things worse for other countries; thiswas

the case forexam-ple

when

Ireland unilaterally offeredguarantees to investorsin thefall of 2008. Putting capital controls in one country toslowdown

capitaloutflows can lead to the perception that other countries will

do

thesame, therefore triggering capital outflows in those countries. Pro-tecting domestic depositors

and

investors at the expense of foreigndepositors

and

investors can create the risk ofmajor

outflows fromdepositors

and

investors in similar situations elsewhere,and

the riskofsimilar measures by other countries.

The

attempt by Iceland todo

just that led the United

Kingdom

to invoke an anti-terrorist law toget Iceland tochangeitsmind. Finally, guarantees

and

othermeasures taken inadvanced

countriesmake

itmore

attractive for investors toput their funds in those countries,

and

thus can lead to furtherFigure

11. SovereignCDSSpreads 3000 (Index7'2;07=100) i 2500 \ 2000 i r 1500 A 1000 500 y / i\ \ \ 9(2/07 11/2/07 1,'2/OS 3/2/08 5/2/08 7/2/08 9/2/08-- Currentaccountdeficitlargerthan5%of2007GDP Currentaccountsurplus, orsmalldeficit

tal outflows from emerging

market

countries.As

Figure 11 shows, the sovereign spreadson

emerging countries have decreased from theirOctober

height, but they remain very high.I have focusedon themeasures needed on thefinancialside.

The

sharp fall indemand

and

inoutputin the pastcoupleofmonths

alsorequiresmeasures to increase

demand.

Interest rateson

government

bonds

are already very low, so the scope for using traditionalmonetary

policy is limited.The

focusmust

benow

on other policies.On

themone-tary side, "quantitative easing", that is the purchase of other assets than

government

Ijonds by the central bank, can reduce spreads indysfunctional credit markets. It is clear

however

that fiscal policy hasto play acentral role here.

At

the timeof this writing,most

countriesare developing fiscal packages, intended atincreasing

demand

directlyand

decreasing the perceived riskofanother "Great Depression".The

IMF

has argued for a2%

global fiscal expansion, with acommitment

to

do

more

if themacroeconomic

situationbecomes

worse thancur-rent forecasts. Sustaining world

demand

is likely to be a central issue in the next few months.5

Policies

to

avoid

a

repeat

Looking

forwardbeyond

the crisis (something difficult todo

these days), the question arises ofhow

we

can avoid a repeat of thesame

scenario,

how we

can decrease the fragility of the financial system, withoutimpeding

toomuch

its efficiency.Much

work

is already going on, both in international institutionsand

in

academic

departments, ranging from the examination of rules gov-erning ratings agencies, to constraints on executive compensation, torules for valuing assets

on

balance sheets, to the construction ofreg-ulatory capital ratios,

and

so on. I have neither the expertise, nor thetime here, to go into details.

But

I can try to giveyou

asense of thebroad directions.

Recall the basic

argument

of this lecture, that the scope of the crisisis due to the interaction

between

initial conditionsand

amplificationmechanisms.

We

have already discussedhow

liquidity provisionand

state intervention can

dampen

the amplification mechanisms.The

re-maining

question, in our context, becomes: Shouldwe

try to avoid recreatingsome

ofthe initial conditions which led to the crisis?Some

oftheseinitialconditions are clearlyhere tostay. Securitization,and, by implication, relatively

complex

derivative securities, allow fora

much

better allocation ofrisk.The

challenge is to preventcomplex-ity from turning into opa.city;

we

can probably domuch

better thanwe

have inthe past. Or, totake another initialcondition, cross border activitiesand

large cross border positions are also essential tocompe-tition

and

the allocation of fundsand

risk in the world.They

shouldnot

and

will not go away.Where

something

canand

probably should bedone

is in decreasingleverage. Leverageofthe financialsystemasawhole

was

almostsurely too high before the crisis. Regulation can force lower leverage. Thisrequires

however

increasing the perimeterofregulationbeyond

banksto

many

other financial institutions.The

challenge here ishow

and

where

todraw

the perimeter, whether, for example, to put hedge funds in or out, and, if they are in,what

rules to putthem

under.One

must

also gobeyond

leverage within the financial system,and

look at leverage for the

economy

as a whole; Highly levered firms orhouseholds are also highly exposed to small fluctuations in the value

of their assets.

The

irony is thatmany

existing tax rules favor such leverage,from

the tax deductability ofmortgage

interestpayments

by households, to the tax deductability of interest

payments

l)y firms.We

have to revisit these rules.Even

ifand

when new

regulati(;n is introducedand

tax laws arechanged,

we

should be under no illusion that systemic risk will be fully under control. Regulation will be imperfect at best,and

always lag behind financial innovation.There

will still benign times,and

they willlead to underestimation of risk (the first ofthe initial conditions Ilistedatthe beginningofthelecture). Thus, a

major

taskofregulatorswill be to monitor, and, if needed, to react to increases in systemic

risk. In doing so, they will face

two

sets of challenges:The

first is about monitoring itself,what

information to collect,and

how

to use it to construct measures ofsystemic risk, both at thena-tional

and

international level.Some

ofthe information needed isjust not available today.We

do not know, for example, the distribution ofCDS

positionsamong

investorsand

countries. This is one of therea-sons

why

many

advocatemoving

trading from over the counter to a centralizedexchange; thiswould

allow, in particular, foi' better collec-tion of information.And,

even if the informationbecomes

available,how

to construct measures of systemic risk is a difficult conceptual exercise.We

are surely not there yet.The

second challenge ishow

to reactwhen

measures ofsystemic riskincrease. Pro-cyclical capital ratios, in

which

capital ratios increaseeither in response to activity or to

some

index ofsystemic risk,sound

likean attractiveautomatic stabilizer.They

candampen

the buildup

of risk

on

theway

up,and

the amplificationmechanisms

on theway

down.

The

challenge is clearly in the details of the design, the choiceof an index, the degree of procyclicality.

Another

avenue is to usemonetary

policymore

actively.The

ideathatmonetary

policy should be used to fight asset priceor creditbooms

is an oldand

controversialidea. Before the crisis,

some

consensushad

developed thatmonetary

policy

was

a very pool tool to fight asset pricebooms,

and

it shouldcare only about asset prices to the extent that such prices

had

effectson current or prospective inflation.

The

crisis has certainly reopenedthe debate.

6

Conclusions

Let

me

end where

I started. This lecture is written in the middle ofthe crisis.

And,

asI writeit.the crisisappears tobeentering yet anew

phase, inwhich

a drop in confidence is leading to a drop indemand,

and

amajor

recession. This inturn raises aset ofnew

issues,from

thedangers arising

from

the interactionbetween

a deep recessionand

aweakened

financialsystem, to therisk ofdeflationand

liquidity traps,to furthercapital outflows from emerging comitries

and

sudden

stops, to an increased risk of trade wars, to the effects of the collapse ofcommodity

prices on low-income countries. Iam

afraidyou

will ha.veto invite

me

again next year for an update...References

(I have

made

no attempt to give a complete literature review, eitherin the lectureor in this bibliography.

Some

ofthe recent articles listedbelow trace the ideas to the earlier literature.)

Bank

of International Settlements, 78thAnnual

Report,June

2008.Brunnermeier,M., 2009, "Decipheringthe2007-08Lirjuidity

and

CreditCrunch"

,JEP

forthcomingCaballero, R.

and

A. Krishnamurthy, 2008, "Collective RiskManage-ment

in Flight to Quality", Journal of Finance, forthcomingCalomiris,

C,

2008,"The

Subprime

Turmoil:What's

Old,What's

New, and What's

Next", working paper, presented at PolakAnnual

Research Conference.

November.

Claessens. S. . A. Kose,

M,

Terrenes,"What

Happens

duringReces-sions, Crunches,

and

Busts'.''".IMF

working paper. 2008Diamond,

D.and

l-". Dybvig, 1983."Bank

Runs, Deposit Insurance,and

Liquidity", Journal of PoliticalEconomy,

91-5, 401-419Foote,

C,

K. Gerardi, L. Goette. P. Willen,"Subprime

Facts:What

(We

Think)We

Know

about theSubprime

Crisisand

What

We

Don't", Public Policy Discussion Papers, Federal Reserve ofBoston.

Global Financial Stability Report, Fall 2008.

IMF

Gorton, Gary, 2008,

"The

Panic of2007". working paperHolmstrom,

B.and

J. Tirole, 1998, "Privateand

Public Supply ofLiciuidit\-". Journal of Political

Economy.

1006-1. 1-40Krishnamurthy, Arvind, 2008, "Amplification

Mechanisms

inLiquid-ity Crises",

mimeo

Chicago,September

Shleifer, A.

and

R. Vishny, 1997,"The

Limits ofArbitrage", Journalof Finance, 53, 35-55