A Case for Developing Life Science Real Estate in New York City by

Shaurya Batra

Master in Business Administration, 2009 Guru Gobind Singh Indraprastha University

Bachelor of Architecture, 2006 Guru Gobind Singh Indraprastha University

Submitted to the Program in Real Estate Development in Conjunction with the Center for Real Estate in Partial Fulfillment of the Requirements for the Degree of Master of Science in Real Estate Development

at the

Massachusetts Institute of Technology February, 2017

2017 Shaurya Batra All rights reserved

The author hereby grants to MIT permission to reproduce and to distribute publicly paper and this thesis document in whole or in part in any/edium now knowAor -reafier created.

Signature of Author

Signature redacted

/

'enter ffr Real E J a n u ar- I17,40-VZ-" tCertified by

Signature redacted

electronic copies of

7$tJ hfr% Kel'n d dy/

Lecturer, Department of Urban Studies and Planning Thesis Supervisor A

Signature redacted_

Prof Ibert Saiz-...- Oatfiel Rose Associate Professor of Urban Economics and Real Estate, Department of Urban Studies and Center for Real Estate

MASSACHUSETTS INSTITUTE

OF TECHNOLOGY

FEB 0 1 Z017

LIBRARIES

A Case for Developing Life Science Real Estate in New York City

by Shaurya Batra

Submitted to the Program in Real Estate Development in Conjunction with the Center for Real Estate on January 17, 2017 in Partial Fulfillment of the Requirements for the Degree of

Master of Science in Real Estate Development

ABSTRACT

New York City, arguably the world's financial capital and the world's biggest real estate market, and home to some of the finest medical and academic research centers houses a little over a million square feet of life science focused real estate. Despite tremendous academic research potential and financial wherewithal, the life science industry of the city is comparatively much smaller to other New York City industries. In addition, it is much smaller in comparison to life science industry in other parts of the country.

This thesis investigates the New York City market as a possible location for developing life science focused real estate assets. As a first step, the research will focus on identifying and analyzing the key demand indicators to establishing the demand for life science focused real estate.

Next, the thesis will focus on lab space as a real estate product to understand its main

components and value drivers. Upon understanding the market and the product, the research will put forward possible strategies for developing lab buildings in the city.

Further, in support of the development strategies the research will look to prove the financial feasibility of developing that life science real estate in the city. This would involve financial analysis and contrasting returns from life science assets against office assets.

Lastly, through real options framework the study will go on to demonstrate the benefits of applying flexibility to real assets, while financially valuing this flexibility using the Monte Carlo analysis.

Thesis Supervisor: John F Kennedy

Acknowledgements

My deepest gratitude to my advisor, John F. Kennedy for his guidance and constant support throughout the development of the research. It has been an absolute pleasure learning from you.

Thank you John for being a great teacher and mentor.

This thesis would not have been possible without the generosity of industry professionals who shared their knowledge and expertise about commercial lab buildings. Thank you Steve Lynch, Tom Ragno and Mike DiMinico. Thank you Bill Kane and Laura Woznitski Kaufman. Thank you James Kennedy. Thank you Tom Andrews and Andy Reinach. Your inputs and support have made the development of this research possible.

Thank you to Prof. David Geltner for introducing me to the concepts of real options during the spring semester. The underlying concepts, spreadsheets and data for this research, are based on Prof. Geltner's spring semester course and upcoming book.

Thank you Tod McGrath, Walter Torous, Peter Roth, and Dennis Frenchman for guiding me through the Master of Science in Real Estate Development program.

Special thanks to my classmates- my fellow MSREDers, and the entire MIT CRE team for the love, laughter and learning.

Thanks to my family and friends, for always being there. With affections for my mom, for always supporting me.

With love for my wife, without whom the last year and a half would not have been possible.

Contents

1 In tro d u ctio n ... -7

-1.1 Background ...

-7-1.2 Objective & M ethodology ...- 8

-2 NYC Life Science and Innovation M arket...- 11

-2.1 M arket Overview ... - 11

-2.2 Key Projects: Location, Time line, Developer, Tenants and Rents...- 12

-2.3 Developm ent Pipeline ... -

16-3 Decoding the NYC M arket for Life Science ... - 19

-3.1 Life Science Collaborations in the City ...-

19-3.2 Life Science Research Activity in the City... - 22

-3.3 Life Science Capital Activity in the City ... -24

-3.4 New York City Initiatives ...- 29

-3.5 Comparisons- New York City, Greater Boston and San Francisco ... - 32

-3.6 Lab Space - W hy New York City Now? ...- 34

-4 Deconstructing the Product- Lab Buildings in R&D ...- 37

-4.1 Understanding Lab Buildings... - 37

-4.2 Types of Lab Buildings ... - 38

-4.3 Speculative Labs Vs Build-to-Suit Labs ... -

40-4.4 Flexibility in Lab Design ... - 42

-4.5 Repositions and Conversions ... - 44

-5 Developing Labs in NYC... - 47

-5.1 NYC Planning Guidelines ... - 47

-5.2 Areas of Focus ... .

-47-5.3 Developm ent Strategies - Possible W ays Forward ... - 50

-6 Investm ent analysis and real options theory ... - 54

-6.1 Key assum ptions... - 54

-6.2 Build-out scenarios... - 56

-6.3 Determ inistic Cash Flow Pro-formas... - 57

-6.5 Cash Flow M odeling with M arket Uncertainty ...- 59

-6.6 Flexibility with Product Switch ... - 60

-6.7 Sensitivity analysis... - 64

-6.8 Valuation conclusion ... -66

-7 C o n c lu sio n s ... 6 7 -7.1 Conclusions ... 67

-7.2 Recom m endations and Areas for Further Study ... - 69

Bibliography...-71-1 Introduction

1.1 Background

Businesses in the fields of biotechnology, pharmaceuticals, biomedical technologies, life systems technologies, nutraceuticals, cosmeceuticals, food processing, environmental,

biomedical devices, and organizations and institutions that devote the majority of their efforts in the various stages of research, development, technology transfer and commercialization all together form the Life Science Industry. United States is the world leader in technology,

innovation and life sciences. United States boasts of the highest expenditure and highest employment of undergraduates or higher in the life science industry globally. Higher education institutions, for-profit and no profit organizations focused in research and development drive the advancements in life sciences.

Life science research takes place in controlled environments due to Human and environmental safety concerns together with the need for maintaining sterile conditions. These extremely specific real estate requirements for the life science industry and has led to the development of

a specific product type- Lab buildings. Although, considered an alternate asset, labs are becoming increasingly mainstream in Greater Boston, San Francisco and other life science clusters around the country. Specific planning, ventilation, temperature, humidity, utility and energy requirements characterize these lab buildings.

The extensive requirements for lab buildings culminates in a rather expensive product with gross development costs upwards of $500 per square foot and possibly exceeding $1000 per

square foot in some cases. High developments costs and extensive requirements create a high barrier to entry, this has resulted in a small but highly skilled set of developers involved with developing commercial lab buildings.

Greater Boston real estate market has greatly benefitted from the development of the life science and biotech industry. Kendall Square in Cambridge is one of the top real estate submarkets in the country today, with most of the growth coming from the biotechnology sector. New York City is the premier real estate market in the United States, the world's largest economy. Despite being at the forefront of finance, real estate, technology and scientific research, New York City has been unable to develop itself as a major biotech-life science cluster. New York City is recognized for the excellence of its academic medical centers; however, the city has lacked the thriving commercial hubs like California and Massachusetts.

New York City provides an opportunity to be one of the early movers in the innovation and life Science real estate. The core of this research will be to ascertain the feasibility for developing and investing in real estate specific for life science use and innovation centers in New York City.

1.2 Objective & Methodology

New York City is a rather nascent market when looking through the life science real estate lens. Thus far, multiple factors have impeded the growth of this sector resulting in academic

innovations ending up elsewhere in the country. A study conducted by Partnership Fund for New York City (PFNYC) in 2001, revealed the chief reasons being absence of collaboration between research institutions, lack of an entrepreneurial culture, dearth of biotech-focused

venture firms and, insufficient lab space. Much has changed in the New York life science landscape in the last few years. There has been a change in institutional leadership who have furthered collaboration amongst the academic institutions and with the industry. This in

combination with New York City's efforts in retaining the science within the city has led to the emergence of a small eco-system. Although nowhere close to Boston or San Francisco, this has generated interest from the big pharma. Venture capital money has started to find its way to startups and growth stage companies, and the city is witnessing instances of acquisition of startups by larger corporations.

This research presents a case for investing in life science real assets in New York City. With the case parsed into three aspects, the first piece of this puzzle focuses on status of the market, current demand and indicators for future demand. A critical look at the various aspects of development of the life science industry in the city and its impact on the real estate industry. The indicators include research pursuits at institutional and non-institutional levels, capital market activities and governmental initiatives focused on life science in the city.

The second part of this research will focus on understanding the engineering and planning for a lab building. While discussing various types of lab developments this part of the research will focus on building flexibility in the building systems. Flexibility in terms of use, scalability, supporting infrastructure and engineering systems, and further delving into conversion of existing office buildings for lab use.

The final piece of the three-part project is the financial analysis for a life science real estate development opportunity in New York City. The goal here is to find out if the lab product type

provides a higher risk adjusted return when compared to a typical office development. Further, using the Real Options Theory we will analyze the development opportunity. The real options theory is a rigorous and quantitative way to model the value of an investment decision by developing options to mitigate the effects of uncertainty inherent in these investment decisions.

This research is a combination of qualitative and quantitative analysis. Understanding the current market condition, demand & demand indicators and understanding different lab types,

and flexibility in design, planning and engineering would include literature survey, collating data from various industry sources and interviews with industry professionals involved in different

aspects of the life science and real estate businesses.

Construction and development costs, existing market rents, tenant improvement costs, and asset cash flow information are used to develop the quantitative basis for this research thesis. The costs and cash flow data are used to create deterministic model of office, lab and a flexible

building types. Further, information from industry professionals is used to identify various uncertainties. Using the uncertainties as decision triggers for Monte Carlo simulations will provide the valuation for the development opportunity.

2 NYC Life Science and Innovation Market

2.1 Market Overview

The New York City and New Jersey markets have generally been combined and considered a single cluster. The combined New York-New Jersey cluster consists of the five boroughs of New York City, Westchester County, Northern, and Central New Jersey. In New Jersey, the life sciences sector is a major driving factor in the state's economy with many of the pharma-giants owning or leasing large amounts of space in the state. On the other hand, New York City and Westchester do not house as many life sciences firms as New Jersey.

Premier academic research institutions like Columbia University, the Albert Einstein College of Medicine, Cornell University/Weill Cornell Medical College, Memorial Sloan Kettering Cancer Center, Rockefeller University, Mount Sinai Medical Center, CUNY, SUNY Downstate and Cold Spring Harbor Laboratory along with 28 research centers and 58 hospitals form the backbone of the New York City life science industry.

The Bloomberg administration started the plan to diversify the city's economy and looked at eight industries that offer significant growth potential for the City, life-science industry being one of the eight. With Wall Street's currently contributing 20% of the city's economy, the city looks to create new sectors for employment to remain attractive for businesses and talent, both domestic and international. At 6%, health care is the sixth largest sector of city's economy, the contribution mainly comes from the hospital and medical services part of this sector.

The city also has the highest number of graduate and postgraduate enrollment annually in life sciences courses, ahead of established life science hubs of Greater Boston and the Bay area. However, retaining biomedical sciences research for commercialization in New York has been the major challenge for the city. Majority of biotech innovations from many top New York

institutions have helped launch companies in other cities. Amgen, Progenics, and Millennium, are examples of New York City science developed into major businesses outside the city.

2.2 Key Projects: Location, Time line, Developer, Tenants and Rents

The current lab space supply stands at 1.7 million square feet up from a mere 120,000 square feet in 2006. Some of the life science real estate of note in the city include

-Alexandria Center for Life Science

The East River Science park project was proposed by the Bloomberg administration. Alexandria Real Equities (ARE) was selected as the developer through an RFP process. Considered by many as the flagship location for life science in the city, Alexandria Center for Life Science (ACLS) was kick-started with a $700 million commitment from ARE plus close to $60 million from various city, state and federal investments. Among those involved were the New York City Investment Fund and the New York City Industrial Development Agency, which committed $10 million and $5.6 million, respectively.

Of the committed $700million, ARE has so far spent $463 million on the development of the two towers bringing the cost of development to $636 per square foot. ARE ground leases the site from the city of New York and in exchange pays the city $3 million as annual rent and $1.7

million fee as part of a 25-year real estate PILOT annually. The ground lease has a term of 99 years upon exercising the extension options. ARE's development, 728,000 square feet currently, spans across two building- the East and the West towers.

Both East and West towers of the development are almost fully leased or under negotiation. Reported asking rents at the ACLS are in the $90-100 per square foot range. Initially conceived as a center for early and growth stage companies, ACLS is home to some of the big names of the pharma industry like Eli Lily, Roche, Pfizer, Nestle and NYU Langone Center. The early and

growth stage tenants include Cellectis S.A., Intra-Cellular Therapies Inc., Kallyope Inc., Kyras

Therapeutics Inc., Lycera Corp., Tara Biosystems Inc., Lodo Therapeutics Corporation, Petra Pharma Corporation, Firmenich, Kadmon Pharmaceuticals.

Columbia Audubon at Columbia University Medical Campus

Audubon Business and Technology Center is a 100,000 square foot, state of the art, research facility, managed by Columbia University. Columbia University, the City of New York and the State of New York together developed the Audubon Center to house early stage, private research and development companies in the Life Sciences industry. The commercial lab facility is part of an overall 600,000 square feet Audubon Biomedical Science and Technology Park. The Audubon center also has the distinction of being the first incubator in the city. Since its opening 46 companies have been started at the facility, current tenants include Exosome, Intra-Cellular Therapeutics, The New York Stem Cell Foundation, Oligomerix, and PIN Pharma.

SUNY Downstate Incubator

The Advanced Biotechnology Incubator for start-ups and early-stage biotech companies is part of the SUNY Downstate Medical Center in Brooklyn. Originally, an 11,000 square feet facility

built in 2004 the facility later expanded by 13,000 square feet. Earlier this year the facility completed another 26,000 square feet expansion taking the total incubator and lab space supply to 50,000 square feet.

The facility contains shared labs and lab suites sized between 400 - 1200 square feet and is home to 20 tenants, most notable amongst them are BioSignal Group and EpiBone. Current rent at the incubator range in the low $40s per square foot. The tenants at the incubator can access the Downstate Medical Center for specialized equipment and facilities. BioBAT at Brooklyn Army Terminal is a sister facility of the SUNY Downstate incubator, which is also allowed the use of SUNY Downstate medical center and the incubator resources.

BioBAT - Brooklyn Army Terminal

Conceived in 2006, BioBAT is a collaboration between the State University of New York Downstate (SUNY Downstate) and the New York Economic Development Corporation

(NYCEDC). 123,000 square feet has been occupied, over two phases, of the 524,000 square feet repositioned army terminal building for life science use. The project originally conceived as a hub for growth stage and manufacturing companies. However, according to industry sources the management is now altering its strategy in light of the increased demand for space from early stage companies emerging out the city's academic research centers.

The current rentals in Brooklyn hover in the low $30's and incentives include tenant

improvements, NYC Biotechnology tax credits and Start-Up NY tax credits. Current roster of tenants includes International AIDS Vaccine Initiative, IRX Therapeutics, Avatar Medical and Modern Meadow. Lower rentals, 12' floor heights and 250 pounds per square foot floor loading capacity, and the proximity to residential areas of Brooklyn are the main selling points for the space at BioBAT. However, the distance and long travel times from the academic research centers of Manhattan according to industry experts has been the obstacle for BioBAT.

Brooklyn Navy Yard

The 1 million square feet building 77 at the Brooklyn Navy Yard development according to some real estate industry reports was being repositioned for life science use. One of the main tenants is Sheil Medical Labs, occupying 250,000 square feet, is a business focused in medical resting and diagnostics. Given the floor heights of around 10' and the development's focus towards food and food service and current tenants it is unlikely that the building is usable for life science

lab space.

630 Flushing Avenue

The old Pfizer Building in Brooklyn contributes close to 430,000 square feet to the commercial lab space supply in the city. However, similar to the navy yard development there are no life science tenants operating out of this facility. With large number of tenants focused towards food and food production it is hard to think of this asset as a commercial lab facility.

Harlem BioSpace

By far the smallest biotech facility in the city of New York at a mere 2,300 square feet. Started by a Columbia University professor Sam Sia in 2013 the incubator is located in West Harlem area of the city. The project has received a $626,000 grant from the NYCEDC, to be paid over a period of 4 years. Called a bare-bones operation by some of the industry experts. Currently, twelve startups incubate at this facility and another seven early stage companies have

previously graduated. The $995 per month rent includes a desk, lab equipment, wet lab space

and legal help sponsored by Wilmer Hale.

2.3 Development Pipeline

The total development pipeline for commercial lab space is close to 550,000 square feet. The North Tower at ACLS represents a lion's share of the current development pipeline. ARE retains the option to develop one more building at the ACLS site, this would take the overall project size to 1.1 million square feet. The North Tower is expected to add another 417,000 square feet of supply to the city's lab space market. However, some industry experts suggest that the new development will be bigger, owning to the success of the first two buildings and due to lack of life science lab space in the city.

While life science real estate focused developers like Alexandria Real Equities and Blackstone owned BioMed Realty are actively scouting for development opportunities in the city. There has

also been a push from the city to redevelop some of its existing assets for biotech use. Recently, the city came out with an RFP for an existing asset near the First Avenue Medical Corridor, at

455 First Avenue. The 355,000 square feet, 14 floor building is currently occupied by the Health Department's Public Health Laboratory, long located on 11 floors of the 335,000 square feet building, would consolidate to six floors. The Aaron Diamond AIDS Research Center and NYU occupy an additional three floors. The city plans to consolidate the Department of Health labs to six floors freeing up 5 floors of space for commercial lab use. This effort once completed would add 120,000 square feet of commercial lab space to the city's supply.

Within the life science real estate industry, incubator spaces are considered a precursor to

future new demand. Of late, these incubator spaces have witnessed an increased demand and

a surge in potential supply in the city. Incubators provide a supportive ecosystem that allows nascent companies to shift their focus from startup operations to innovation so they can reach their scientific potential quickly and achieve business success. Three prominent groups are in the process of launching incubator or co-lab space initiatives in New York City.

Alexandria Real Equities - LaunchLabs

ARE's 15,000 square feet incubator project called Alexandria LaunchLabs and will be located at Alexandria's Center for Life Science. The opening of the facility is slated for summer 2017. A $1,995 per month charge at the incubator would include membership, an office workstation and a laboratory bench in a shared suite. In order to maximize the flexibility for its tenants, LaunchLabs offers the option to rent a single office desk, a laboratory bench in a shared suite, a private office and/or a private laboratory suite to accommodate the varying needs of

BioLabs - BioLabs New York

BioLabs is a membership-based network of shared lab facilities located in the nation's key biotech innovation clusters, designed exclusively for high potential, early-stage life science companies. With facilities in Cambridge, North Carolina and San Diego, BioLabs is now expanding its footprint to New York City. The operator spent close to twenty-four months researching the science coming out of the academic institutions in the city before deciding to open a new location. Expected to be in the 25,000-30,000 square feet range, the New York City shared lab facility is expected to open in the next early 2017. Currently, the operator is in the process of selecting applicants to incubate in their space. According to industry sources, BioLabs New York plans to house 20-25 early stage companies. The location and the rents are not known at this stage.

Harlem BioSpace

Buoyed by the success of their current location, the operators of the 2,300 square feet facility are looking to expand through another 25,000 square feet facility. Industry sources expect the new incubator space to be closer to midtown and downtown away from its current West Harlem location. Harlem BioSpace is also in talks with the NYCEDC for another $1 million grant for setting up the new location, according to industry sources. Exact details concerning location, timing and rents are unknown at this time.

3 Decoding the NYC Market for Life Science

A 2001 PFNYC report suggested that the growth of the life science industry in the city was hampered due to four main reasons:

-1. Lack of collaboration amongst the city's academic and research institutions 2. Absence of an entrepreneurial culture

3. Lack of venture capital funding 4. Lack of lab space.

Since then there have been number of initiatives focused towards resolving the issues identified in the PFNYC report. This chapter will look at these efforts addressing three of the four highlighted reasons.

3.1 Life Science Collaborations in the City

For long, New York City has been faulted for failing to foster a collaborative culture amongst its premier academic research institutions. This is considered as one of the key factors hindering the growth of a major life science cluster akin to Cambridge and San Francisco. In the past few years, the city has tried to address this problem primarily by recruiting academic leaders with

industry experience and launching commercially focused translational programs. Some of the high profile appointments include Marc Tessier-Lavigne as president of The Rockefeller University, Louis Walcer as head of Cornell University's life science business incubator and Laurie Glimcher as dean of Weill Cornell Medical College, all in 2011. Tessier-Lavigne was previously EVP and CSO at the Genentech Inc. (now Roche); Walcer was senior

commercialization officer at Cleveland Clinic Innovations; and Glimcher was a professor at

serving on the board of Bristol Myers-Squib. The changing landscape of the city's life science industry over the years has encouraged other academics from established hubs to relocate their research efforts to the city. Prominent among them are Tom Maniatis and Lewis Cantley, both moving from Harvard Medical to Columbia University and Weill Cornell Medicine

respectively.

Tom Maniatis, a molecular biology pioneer and the founder of the Genetics Institute, was instrumental in setting up the New York Genome Center; a collaborative effort of the city's 10 top academic institutions. Backed by $140 million in funding from founding members,

philanthropic funds like Bloomberg Philanthropies, and NYCEDC. Stressing on the collaborative effort Maniatis mentioned in an interview, "The [NYGC] came to life based on the common

understanding that medical genomics is far too expensive and complex for any one institution to tackle on its own."

Other academic alliances of note include the New York Structural Biology Center (NYBC), Tri-Institutional Therapeutics Discovery Institute (Tri-I TDI). The NYBC is a joint effort of Columbia University, the Albert Einstein College of Medicine, Weill Cornell Medical College, Memorial Sloan Kettering Cancer Center, Rockefeller University, Mount Sinai Medical Center, New York

University, City University of New York, and Wadsworth Center. The Tri-I TDI is a venture between the Rockefeller University, Weill Cornell Medical, Memorial Sloan Kettering Cancer Center and pharma giant Takeda. Takeda has made an investment of $20million at the inception and makes an annual payment of $1.5 million in addition to stationing 15 of its scientists at the institute. The partnership's purpose is to help the academic institutions successfully translate research from bench to bedside. New York City is also trying to leverage

their proximity to the Big Pharma companies in New York to attract industrial partners as well. Takeda and the Tri-I TDI alliance is one such alliance. The NYU Langone Medical Center has established a drug discover accelerator to collaborate with the pharma industry called the Office of Therapeutic Alliances (OTA). NYU Langone describes the OTA as 'an innovative, nimble program that advances the discovery of novel therapeutic projects by combining the scientific strengths of NYU Langone investigators in dissecting disease pathways with the expertise of external professional drug discovery and development partners in the biopharma industry.' With approximately $260 million in annual research funding NYU is creating a new model of collaboration to overcome the translational gap. The NYU OTA has seen some success in its endeavors. Earlier this year, a startup iBeca was launched by NYU School of Medicine professor Ramanuj Dasgupta. iBeCa is a subsidiary of what's known as Allied-Bristol Life Sciences, a joint venture between Bristol-Myers Squibb and British investment firm Allied Minds. The startup has been created on a Build-to-Buy model, NYU Langone will get equity in the company and a mix of near- and long-term financial rewards if the startup progresses.

Various institutions in the city have taken steps in the right direction by not only partnering with other research centers, but also by collaborating closely with the industry, something that both Boston and San Francisco have clearly benefitted from.

The latest partnership in the city involves two local venture firms- Bay City Capital, Deerfield Management, three research centers- Memorial Sloan Kettering Cancer Center, Rockefeller University, Weill Cornell Medicine), and one pharmaceutical company- Takeda. The partnership is called Bridge Medicines. VCs at Bridge will help create the business and scientific

point that they are ready for clinical trials. Once the drugs get to that point, Bridge would then work with scientists to form startups that will own each of these individual projects and take them forward. The idea is that these companies will be based in New York City.

3.2 Life Science Research Activity in the City

The efforts from the institutions and the city have yielded some results and New York is

witnessing birth and growth of an increasing number of biotech startups. An increased merger, acquisitions and VC funding activity that are being witnessed, can ascertain success of New York

based startups.

Foresight Bio-therapeutics: A startup focused in eye and ear conditions, and developing a pink eye treatment raised $17 million over two rounds, and was later acquired Shire for $300 million.

Turing Pharmaceuticals: Is a startup researching on orphan diseases and recently raised $90 million in series A funding.

Ovid: Is a brain disease focused venture, started by ex-Teva chief Jeremy Levin, and recently received $75million in series B funding. The investors include Fidelity, Sanofi-Genzyme, Spera Global among others.

Petra Pharma: Is a New York based startup emerging from the Weill Cornell Medicine, focused on treating a range of cancers and metabolic diseases. The startup based on the science from Weill Cornell biochemist Lewis Cantley, a former Harvard Medical School professor, and Nathanael Gray of Harvard and the Dana-Farber Cancer Center in Boston. Petra recently received $48 million in funding from a group of investors including Eli Lilly, Johnson & Johnson, AbbVie, Pfizer, Arch Venture Partners and Accelerator.

Kallyope Pharma- Founded by three Columbia University professors Tom Maniatis, Richard Axel, and Charles Zuker, focusing on the gut-brain axis functions. The startup received a $44

million from venture firms venture firms Lux Capital, The Column Group, and Polaris Partners. Rgenix: Based on research coming out of Rockefeller University and is currently prepping its drug candidate, a cancer immunotherapy agent, to enter clinical trials. The venture was formed with an $8 million series 'A' round and recently received a $33 million series B round. The series

B round was largely funded by well-known biotech investors Novo A/S and Sofinnova Partners. Sapience Therapeutics: Is developing a cancer drug based on the IP licensed by Columbia University, and recently received $22 million in funding led by Celgene, Eshelmen Ventures among others. Columbia University is also a shareholder in the company.

Lodo Therapeutics: Built around the work of Rockefeller University researcher Sean Brady. The startup is trying to effectively sequence and understand the genetic information of microbes in dirt samples, to unearth new drugs. Bill and Melinda Gates Foundation, Accelerator, AbbVie Biotech Ventures, ARCH Venture Partners, Johnson & Johnson Development Corporation, Pfizer Venture Investments and others have invested $17 million in the startup.

Between the 13 institutions that compose the New York Academic Consortium the number of startups to emerge each year has doubled between 2013 and 2015 from 37 to 73. The number of licensing deals jumped from 309 to 398 over the same timeframe. Large part of the success achieved by Boston and San Francisco has been due to emergence and subsequent success of the startups. While still in its early stage, New York City is witnessing a spurt of growth in the biotech startup sphere and also prevailing is the desire for these new business to stay in the city as against moving their science to other established hubs.

3.3 Life Science Capital Activity in the City

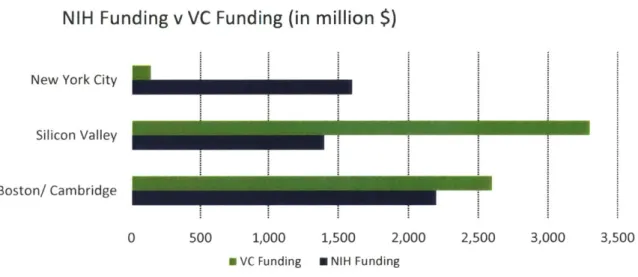

While New York State ranks third behind California and Massachusetts in total NIH grant funds received, New York City ranks second behind Boston, owning to the city receiving 78% of New York State's NIH grant amounting to $1.6 billion. In the Life Science sector, during 2006 to 2015,

$9 million of angel funding and $11 million of seed funding was invested in New York City. Angel and seed funding for the same duration in Greater Boston and the Bay Area totaled $110

million and $184 million respectively. New York City is amongst the top five destinations for VC money however, the VC funds directed to life sciences form only 2% of overall VC activity in the city, compared to 45% in Greater Boston and 12% in the Bay Area. For every dollar of NIH grant received, only $0.06 is generated in VC capital in New York City compared to $1.27 in the Silicon Valley and $1.32 in the Greater Boston area.

NIH Funding v VC Funding (in million $)

New York City

Silicon Valley

Boston/ Cambridge

0 500 1,000 1,500 2,000 2,500 3,000 3,500

a vC Funding M NIH Funding

Figure 3.1- NIH v VC Funding Comparison

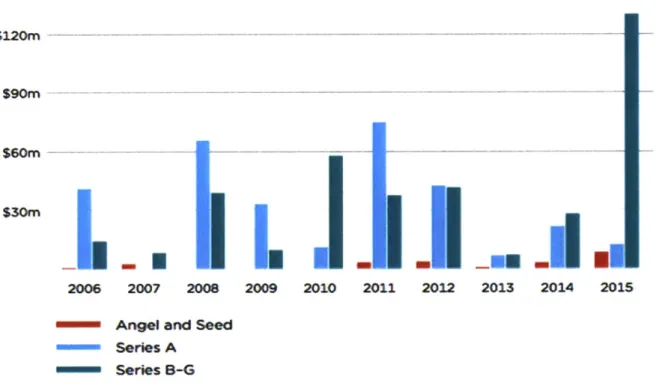

While the above statistics paint a grim picture the activities in the recent past help strengthen confidence in the Life Science sector in the city. In 2014-15 venture capital funding in the city

tripled over the previous year, although only a fraction of what is being garnered in Greater Boston and San Francisco, it is still a considerable leap from the previous year.

During the same period, five biotech focused VC firms have set up operations in the city in the last year. Three of these five firms, Versant Ventures, Flagship Ventures and Arch Ventures are ranked amongst the top ten biotech focused VC's. The five all together manage over $10 billion in capital and have helped launch over 400 companies.

$12-$90Mu

$60m - _ _

30m

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Angel and Seed

Series A

-

Series B-GFigure 3.2 - VC investments in New York City over the years. Source: Source: New York's Next Big Industry: Commercial Life Sciences, PFNYC

Deerfield Management, a New York based Venture Capital firm, has raised $550 million for their Healthcare Innovations Venture Fund. The fund will specifically focus on innovative

treatments for genetic disorders, cancer, and orphan diseases. The fund currently has a 12-year life cycle, and investors include New York-Presbyterian Hospital, Memorial Sloan Kettering

among others. Deerfield is also talking with Memorial Sloan Kettering and other medical research organizations about developing formal relationships.

Versant Ventures, known for known for Quanticel Pharmaceuticals from San Diego and CRISPR from Cambridge, has set up Highline Therapeutics an incubator in Chelsea. Versant intends to use the incubator to create Build-to-buy startups, companies often created around a single drug with a prearranged buyer, generally big drug makers that are eager to gain access to new ideas and technologies.

In 2013, NYCEDC joined with Celgene, Eli Lilly, and GE Ventures to create "City of New York Early-Stage Life Sciences Funding Initiative." Flagship Ventures ($1.4 Billion under management) and Arch Ventures ($ 2 Billion under management) are now backing the $150 million biotech fund for investing in 15-20 startups managing $90 million and $60 million respectively. Flagship Ventures will direct investment activities in therapeutics, while ARCH Venture Partners will pursue investment activities in non-therapeutics. The fund is expected to have specific provisions that both incentivize startups to grow in New York and dis-incentivize them from leaving the city.

Accelerator, the last of the five, has raised $51.1 million for its fourth fund and has also struck partnerships with seven New York institutions- Albert Einstein College of Medicine of Yeshiva University, Columbia University, Icahn School of Medicine at Mount Sinai, Memorial Sloan-Kettering Cancer Center, NYU, Rockefeller, and Weill Cornell-to tap into their research. Alexandria Real Equities, in addition to starting Alexandria LaunchLabs - an incubator in its facility at the East River Science Park, is also starting a seed fund. The Alexandria Seed Fund will provide seed-stage capital to support entrepreneurship and emerging companies across the

New York City life science ecosystem at the critical transition point between scientific discovery and early translational development. Alexandria LaunchLabs' tenants will have priority access to the Alexandria Seed Fund. The fund is targeting investments in the $10 million to $25 million range. Alexandria Venture Investments -Alexandria's strategic venture capital arm - lead the seed fund with capital contributions from other strategic and financial life science investors. Alexandria plan to allocate the Seed funding to select companies based on the quality of each applicant's management team, intellectual property, business strategy and financial plan. Similar to Alexandria, BioLabs in addition to the soon to open incubator facility is also planning to launch a life science focused venture fund. The fund is expected to be $150 million in size and will invest across 25-30 ventures with a cap of $10-15million cap per investment.

Other than NIH funding, which is mainly responsible for helping create new life science business in the city, and the venture capital inflows philanthropic funding is another important source of capital that supports research. Funding for basic research was at least $2.2 billion in 2015, with $1.2 billion going to the life sciences, physical sciences, and mathematics. Life sciences received a significantly higher percentage of total funding than the physical sciences and mathematics, capturing 47%, or $1 billion.

According to life science industry sources, philanthropic support of basic science at universities is more important than ever as support of basic research in industry declines, and government funding becomes more constrained and tilts toward shorter-term goals. This support could come in the form of support for individual faculty members, their students, and postdoctoral researchers, or for the facilities, they need to do their research.

New York City, ranks number one in philanthropic donations made to academic and medical centers, accumulated $2.68 billion from 2011-2015, beating the $2.12 Billion received by

Boston/ Cambridge institutions during the same period.

140 9121I 82012 a ao 8201 * l0ll

Iliii

SF .. il so Figure 3.3: Philanthropic Funding byCommercial Life Sciences, PFNYC

city over 2011-15. Source: New York's Next Big Industry:

Most of the philanthropic funding is directed towards the academic institutions, like the $400 million donated to the Cornell University by Sanford Weill and $200 million donated to

Columbia University by Mortimer Zukerman. However, lately some startups have also received capital from philanthropic sources. Epibone based on science coming out of Columbia

120 Aom 800 600 200 .' M 1 1 1 IIII Bomas

Ii

IUniversity, incubated at the Harlem BioSpace and now housed at SUNY's Downstate Incubator, received grant from Breakout Labs a Peter Theil Foundation initiative that uses philanthropic funds to support early stage companies. Bill and Melinda Gates foundation have also made an equity investment in Lodo Therapeutics, one of up and coming startups from the city.

New York City also serves as the location for headquarters of almost half of the top 35 disease focused foundations. These foundations combined grant $400 million annually in research funds. As understood from some industry experts, philanthropic funds can guarantee continuity for long-term biomedical research progress and foster burgeoning careers for young scientists, especially in times when it is harder to obtain NIH funding. The availability of philanthropic money reinforces New York City's competitive advantage in producing academic science. 3.4 New York City Initiatives

The Bloomberg administration is credited for starting the diversification of the city's economy, which was mainly finance, focused at the time. To attract life science business and talent the administration along with the New York City Economic Development Corporation (NYCEDC) pushed for creating an ecosystem of life science companies, and developing real estate to house these ventures. Initially known as the East River Science Park and later as Alexandria Center for Life Sciences (ACLS), and Brooklyn BioBat are a result of the city's efforts in establishing life science real estate cluster in the city. Initiatives focused towards life science companies include tax credits, financial grants and incentives for operations, facilities, workforce training and real estate space.

ACLS is the only life science real estate development in the city, and has put the city on the life science map. The success of the ACLS would not have been possible without help from the city

and quasi-governmental agencies. Assistance includes a 25-year tax pilot, $60 million in grants, and tenant incentives like the NYCIF Alexandria Lab Space Loan Fund offering a $15 million loan program to companies seeking to establish operations at the ACLS.

Taking cues from the academic and industrial collaborations, resultant of a mindset shift within the institutional community, The City of New York Early-Stage Life Sciences Funding Initiative

created a public-private partnership across academic institutions, industry leaders, top-tier investors, and the philanthropic community. The $150 million fund seeks to launch 15 to 20 breakthrough ventures by 2020.

The incremental steps being taken by the city, while appreciated, have been compared to the $1 billion support offered to life science companies in 2008 by then Massachusetts Governor Deval Patrick. Over seven years, the state, through the Massachusetts Life Sciences Center (MLSC), has invested or committed $595 million, which has been matched by over $2 billion in private and federal funds.

Mid-December 2016 over two days, both the city and state governments in New York have combined to commit a total of $1.15 billion to the development of the life sciences industry in the New York. New York State Governor Andrew Cuomo announced a $650 million plan for life sciences in the state. The DeBlassio administration and NYCEDC's city focused initiative called the "LifeSci NYC" is a $500 million, 10-year commitment to biotech in New York City, a plan meant to create 16,000 jobs in the area. The key areas of emphasis for the city's plan include:

-* Modernize land use policies to encourage new space for life sciences firms. To increase potential areas for life sciences jobs by more than double, the administration has clarified regulations to make explicit that lab space for life sciences R&D is permitted in

any commercial zone. The administration will also leverage upcoming rezoning to include life sciences sites where appropriate.

0 $300 million in a tax incentive program to attract investments towards developing commercial lab spaces in the New York City. Given the high cost of construction for lab spaces, through this initiative the city aims to defer some of these costs, in order to

unlock lab space for growing companies and provide jobs.

0 $100 million towards creating a new Applied Life Science Campus to drive innovation, research & development and entrepreneurial training with the campus serving as an institutional anchor for the city's life science industry.

* $50 million in capital to a network of up to eight nonprofit research facilities to help create new workspaces for research with a high potential for commercialization. To remain at the forefront of the innovative research that leads to new businesses, the administration will make targeted investments in New York City's existing academic medical centers and research institutions.

* $10 million to expand the network of incubators for life sciences start-up facilities. To provide affordable space for the next generation of life science startups, the City will invest in up to five new incubator and innovation centers, with the first expected to open as soon as late 2017. Incubators will be located near existing research centers to

better support innovators and connect skilled workers with jobs.

* $20 million a year in matching funds to support early-stage businesses. Young life

sciences startups require significant levels of risk capital, and even growing companies

and growth funding-and seeking matching funds from private sources-the City will help spur the growth of up to eighty companies, which will help them expand.

* $20 million investments to create internships and life sciences curricula and expand training programs for entrepreneurs and provide financing to life sciences startups to help them secure experienced entrepreneurs. These entrepreneurs will be committed to growing companies, cultivating new talent, and creating good and accessible jobs in the five boroughs. $7.5 million out of the $20 million is towards paid internship

programs for more than 1,000 students. Positions with an average salary of $75,000 at life sciences companies. Roche, Eli Lilly, the New York Genome Center, and Deerfield have already agreed to take part.

The "LifeSci NYC" plan aims to create 9,000 life science jobs, 7,000 jobs in related fields, while adding another 7,400 construction jobs. Financial targets of the plan include a $2.5 billion in economic output per year, attracting $6.5 billion in private investments, and increasing the tax revenue by $1 billion.

3.5 Comparisons- New York City, Greater Boston and San Francisco

Among Greater Boston, San Francisco Bay Area and New York City the highest enrollment of graduate and postgraduate students in life sciences during 2015 was in New York City. The 6,644 enrollments in New York City is narrowly ahead of Greater Boston at 6,614 and both of these are considerably ahead of the Bay Area at 4,543 enrolments. Despite the highest enrollments, New York City has the lowest life science jobs at 14,438. Bay Area on the other hand has the highest life science focused jobs at almost sixty-five thousand. The Greater Boston Area comes in second here as well at a little over fifty-six thousand jobs. This statistic is an

indicator of the city's inability to hold on to talent and science trained and generated from the city's institution.

When comparing life science industry's contribution towards the GDP of the states,

Massachusetts leads at third spot followed by California at sixth while New York comes in at 24th. New York City and New York State generate 4 percent and 8 percent of nationwide GDP, respectively, but account for just 1 percent and 5 percent of the nation's economic output in life sciences'.

New York City leads Greater Boston and the Bay Area in philanthropic funding, while it received the second highest NIH funds annually ahead of the Bay Area and behind Greater Boston. During 2014-2015 New York City received $140 million in life science dedicated venture capital funding behind both Bay Area and Greater Boston at $3.3 billion and $2.6 billion respectively. The total commercial real estate in Manhattan is close to half a billion square feet as per the latest Colliers data. Greater Boston (Boston, Cambridge and Suburbs) is close to 220 million square feet, with the Bay Area (San Francisco, Alameda and Oakland) close to 450 million square feet. Real estate dedicated to life science forms 8.9% of all commercial real estate in Boston at approximately 20 million square feet. A little over 31 million square feet of lab buildings form 6.5% over all real estate in the Bay Area. The 1.7 million of overall life science use real estate amounts to less than 0.3% of the island of Manhattan.

New York City is the largest commercial real estate market, and has the highest construction costs. Using the 2015 RLB comparative cost index data, which tracks the bid cost of

construction (inclusive of labor, materials, contractor and overhead costs), construction costs in

New York city are higher by around 10% over the other two cities with the Bay Area marginally ahead of Greater Boston.

3.6 Lab Space - Why New York City Now?

Resultant of its efforts over the last decade, the city has been able to increase the lab space supply from 120,000 square feet in 2007 to 1.7 million square feet in 2015. While there is 1.7 million square feet of commercial lab space in the city, there is only one commercial lab development in the true sense - Alexandria Center for Life Science. Other commercial life science spaces like the New York Genome Center are lab spaces within an overall commercial building and not a lab development.

Developments in Brooklyn- BioBAT, 630 Flushing Ave (Old Pfizer Building) and Brooklyn Navy Yard together make up an approximate 2.0 million square feet of real estate. BioBAT, a

potentially 524,000 square feet development started in 2011, currently has 123,000 square feet occupied with the remainder forming a pipeline. Building 77 at the Brooklyn Navy Yard is a 1 Million square feet development targeting life science companies slated to open in 2016 and currently has 240,000 square feet under agreement to Sheil Medical Laboratory, which is a sample processing and diagnostics company. With its low floor-to-floor heights life science use at the Navy Yard seems difficult. The old Pfizer building has no life science tenants to speak off, which makes marketing as a commercial lab space an up-hill task given the life science

businesses co-location and proximity desires. With little inclination to travel longer and lack of clustering possibilities the contribution from these developments, at best is theoretical supply.

Most industry experts peg the New York City commercial lab supply at a 1.2 million square feet and the current pipeline at 550,000-600,000 square feet. 70% of the development pipeline and 60% of the current supply is represented by one development -ACLS, indicating room for growth.

The VC funding in New York City at $140million is compared with $2.6 billion for Boston and $3.3 billion for the Bay Area. Further analysis reveals that New York City receives $82 of VC money per SF of life science real estate compared to $106 for the Bay Area and $131 for Greater Boston. The VC investments in New York City are only 5.4% of what is generated in Boston in overall value but 62% of Boston on a $/square foot basis.

A 2016 PFNYC report established the life science real estate demand at 3 million square feet over the next ten years. A surge in demand for incubator spaces is a good indicator for possible future demand for real estate. Out of the 25 companies incubated at a well-known incubator's 25,000 square foot Cambridge facility, the nine graduating startups leased a total of 90,000 square feet in the Boston/ Cambridge market. Based on a simple extrapolation, this gives an incubator to market multiplier of 3.6x. Considering a combined influx of close to 100,000 square feet of incubator space and using a similar multiplier, the city could need up to an additional 360,000 square feet of space to accommodate the needs of ventures growing out of the city's incubators every 15-18 months. Theoretically, this alone could potentially result in a demand of close to 2.5 million square feet over the next ten years. Many industry experts believe that the city will see sustained demand for real estate since researchers developing innovations in the city do not wish to relocate. While new ventures will need space to mature, existing science will need space to expand its operations.

Higher rentals in the city are generally blamed for lack of commercial lab space, and it is argued that second tier clusters provide lab space at a lower price point. Although many cities offer cost benefits over New York, it should be noted that many companies have also moved away from the idea of suburban research campus and have relocated their operations closer to clusters that offer similar companies, institutions and universities involved with similar research. Given the workforce's clear preference for urban cores over suburbia for the live-work-play, theme and companies' willingness to pay higher for accessing talent pool the cities have to offer, it is unlikely that the higher rents in Boston, Bay Area or New York City would be a deterrent for companies. Many industry experts reason that if start-ups can afford space in and around Cambridge, which is the hottest lab market in the country, why not New York City.

Especially given that real estate costs are probably the seventh or eighth line item on costs for such companies with human resource being the first.

There has been a growing infusion of capital from the VC's, improved collaboration amongst the academic institution and industry and an increase in the creation of entrepreneurial life

science ventures leading to a creation of an eco-system. All this combined has resulted in a 6.8% year on year growth in life science establishments.

Further, recently announced $500 million LifeSci NYC initiative that aims to add an estimated 16,000 new jobs in the coming years to the life science sector in the city. These together provide evidence that the above trends could be changing in times to come. However, it is unlikely that the city will be able to carry the momentum further without more real estate space to expand. As a shark can grow only as big as its tank, while other factors come together lack of real estate is the missing piece of the New York life science puzzle.

4 Deconstructing the Product- Lab Buildings in R&D

4.1 Understanding Lab Buildings

As a building type, the laboratory demands our attention: what the cathedral was to the 14th century, the train station was to the 19th century, and the office building was to the 20th century, the laboratory is to the 21st century. That is, it is the building type that embodies, in both program and technology, the spirit and culture of our age and attracts some of the greatest intellectual and economic resources of our society2. The biggest differentiator between a lab building and an office building is the energy consumption. One of the larger consumers of this energy are the ventilation and air-conditioning (HVAC) systems. A typical office building is designed for 20 cubic feet per minute (cfm) per person of outside air, which roughly translates to one air change per hour (ACH). Traditional office space recirculates the existing air while adding 10-15% of outside air, lab spaces normally require 100% outside air and usually at exchange rates of 6-10 ACH. This is needed to meet the aggressive exhaust requirements for fume hoods. Recirculation of air in lab spaces could lead to hazards arising due to the cross-contamination as a result of the recirculation. The 100% outside air

requirement eliminates these hazards.

In addition to the HVAC needs the lab buildings also consume more energy due to higher process loads for running equipment like centrifuges and spectroscopes. HVAC needs tend to vary and are subject to the research work being carried out in these buildings. Animal testing or heavy chemistry usage places more stringent exhaust requirements, this further intensifies

Low-HVAC needs placed on the building. Office buildings have connected plug loads of about 0.5 - 1 watt per square foot; labs have loads that can vary from 2 - 20 watt per square foot. However, usually lab buildings also have high diversity factor which means that most equipment operates only intermittently.

The aggressive equipment, mechanical and electrical service needs have a direct correlation with the physical and the structural aspect of lab buildings. Lab building typically require higher floor loading capacities. Usually lab buildings are designed for 100 pounds per square foot or higher. While floor-to-floor heights for typical office buildings range from 11'-12', lab buildings are designed for 14'-16' floor-to-floor heights. This is done primarily to allow for distribution of ductwork facilitating the ventilation needs of lab buildings. Although lower floor-to-floor heights can be made to work, the tradeoff is usually lowered flexibility, reduced efficiency and higher costs. Another important consideration in development of lab buildings are vibrations, to which lab facilities are sensitive. General office buildings are designed for 16,000 mips while speculative lab developments are generally designed for 8,000 mips. This number can go up to 2000 mips in certain case based on specific tenant requirements.

4.2 Types of Lab Buildings

Various scientific research functions require specific space and infrastructure requirements, based on these uses lab buildings can be classified as chemistry lab, biology lab, animal care, GMP facility, nanotechnology research facilities etc.

The key participants involved in developing and running of lab buildings are:

-" Universities and Academic Research Institutions

" Nonprofit and Government institutions

" Private Real Estate Developers

The approach towards development of lab building by these protagonists may differ based on their long-term goals for the assets. The universities and academic research institutions are generally funded through the endowments received. The lab buildings here would serve the

purpose of a teaching lab and be used for research. Research work at these academic institutions is further dependent on the grants received by the institution. Hence, the lab building at universities need to be flexible to cater to teaching needs and to serve as research space for varied purposes.

Biotech and pharma companies' activities are focused towards developing new drugs, which can be introduced to the market. Flexibility for such companies would be the ability to expand from early stages of drug discovery to prototyping drugs for market. However, biotech and pharma companies occupying owned buildings, much like plants have a predetermined use. Private developers play an important role by being owners and providing lab facilities for lease. While they treat the lab building as an asset, they take on the risk of owning, developing, maintaining and leasing the space. This also allows other constituents to focus on their core activities of conducting research for academic and product development purpose. From the developer's perspective, the lab development can also be characterized based on the approach towards development. Developers could choose to begin the development activity upon

execution of an agreement with a tenant for an entire building. This approach is referred as

needs without necessarily having a tenant in place. This approach is generally referred as building on-spec or speculative development.

4.3 Speculative Labs Vs Build-to-Suit Labs

In preceding years, there has been a surge in demand for lab space, primarily in well-established urban markets, and this demand has outstripped the supply. Developers have stepped into this void to provide biotechnology companies of all scales with lab space to further their research. High value real estate and top end construction costs requires an extensive amount of investment and developmental work.

In case of a speculative development, tenants lease the space upon completion of core and shell. Experienced developers tailor their offering to match what is demanded by the market at large. This demand can vary from cold shell to a warm shell and extend to a fully built out space dependent on the market and the tenants. Speculative lab developments tend to be multi-tenant facilities. Developers focus on building flexible modular base building while leaving room for additional modules over time. Planning for sufficient clear height, adequate shaft space and control zones allows developers to effectively manage tenant needs on a case-by-case basis. This approach is more efficient and cost effective than building excess capacity from day one. On completion of the core and shell of the building, lab tenants lease all or part of floor or building. Improvements that meet the tenant's unique requirements are then carried out to the empty shell space. An experienced life science developer will provide a flexible warm shell with utilities that are appropriate for a modern day lab, while a less experienced or under-financed developer may only provide four walls and a roof i.e. a cold shell3.

Developers ensure they match their competitors' offerings in terms of the infrastructural services on offer at their buildings. Further, developers create value for their lab developments by ensuring that the tenants contribute towards scaling up the infrastructure of the building for desired standards. While the generic infrastructure costs are borne by the developer, tenants specific improvements are generally carried out at the tenant's expense. Once the tenant vacates the space on expiration of the lease, the additional equipment and improvements stay with the developer. These additional improvements are often used by the developer to market the facility to prospective tenants. Improved and existing infrastructure while enticing the new tenant ensures lower tenant improvement costs thus creating value for the building. Lab developments also have the benefit of being reutilized. In most cases one biotech tenant's space can be filled by another tenant quite seamlessly. While certain tweaks may be needed to certain areas, most of the space is normally good to be leased. This translates into lower future TI costs, and lower vacancy durations.

In a speculative lab building tenants fit their requirements in a generic lab building, a build to suit development offers tenants the opportunity to get a facility built to their exact needs and specifications. While the build-to-suit approach sounds very similar to building their own facility, there are benefits to adopting this methodology.

First and foremost, is access to prime land and location. Generally, in urban locations and prime markets developers own and control most land parcels. Further, developers could have the necessary approvals and entitlements in place. If not, they are adept at managing and

navigating the approvals and entitlement process. Moreover, specialized lab developers bring a wealth of lab construction experience that most is not possible for small and medium sized life