The CEO-Merger Connection:

A Top Leadership Perspective on Large Intercorporate Combinations

by

Kathleen Marshall Park

SUBMITTED TO THE SLOAN SCHOOL OF MANAGEMENT

IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF DOCTOR OF PHILOSOPHY IN MANAGEMENT

AT THE

MASSACHUSETTS INSTITUTE OF TECHNOLOGY JUNE 2005

( Kathleen Marshall Park. All Rights Reserved. The author hereby grants to MIT permission to reproduce

and to distribute publicly paper and electronic copies of this thesis document in whole or in part.

Signature

of Author:

...

"

. TT

.;;

Sloan School of Management

May 17, 2005 /_ /' C ertifi ed B y : ... ...

Certified

By:

By

...

.

...

John S. CarrollProfessor of Behavioral and Policy Sciences and Engineering Systems Thesis Supervisor

A ccepted B y : ... ... ... ...

Birger Wemerfelt Protessor ot Management Science Chair, Ph.D. Program . ", /., MASSACHUSETTS INSTT OF TECHNOLOGY ,- .- i .. SEP 0 1 2005 - -I- r r o r .rig -~~~~~~~~~~~r- , -16'

Abstract

To better understand large mergers and acquisitions (M&A) as major intercorporate strategic maneuvers, I study a key concern from the chief executive perspective at each stage of

combining two firms. For the inception stage, I explore CEO merger motives; for the implementation stage, I examine CEO leadership; for the outcome stage, I consider the

postacquisition mobility consequences for CEOs as well as the financial performance of the merged firms. ][ study these issues in the total sequence of merging from the perspectives of the acquiring and the target CEOs. The investigation relies on interviews with selected CEOs and

also secondary data on all CEOs and firms participating in the 158 largest U.S. public M&A

deals announced during the 1990s worldwide merger wave and completed during 1993-2002. These large deals embodied unprecedented valuation and complexity requiring the sustained attention and commitment of chief executives from both sides of the transaction.

The first empirical section explores CEO motivations for merging. Merger motives have not been well understood, and previous research has tended to segment perspectives from different disciplines. Drawing on strategic management, organization studies, and financial economics, I examine the five merger motives advanced to date-synergy, managerialism, hubris, free cash flow, and imitation-and add the overarching motive of metamorphosis. The metamorphosis motive proposes that mergers create profound organizational change in three dimensions: (1) management structure, (2) strategic direction, and (3) corporate culture.

The second section examines CEO leadership roles in M&A transactions. Drawing on the knowledge and resource based views of the firm and the literature on the chief executive function, I identify three phases in the similar merger-related roles of acquiring and target CEOs.

In the context of large U.S. mergers in the financial services, computer software, oil and gas,

telecommunications, and utilities industries, the purview of acquiring and target CEOs included: (1) making the merger, (2) placing and displacing people, and (3) fulfilling the strategic vision.

The third section applies perspectives from human capital, social capital, market

discipline, and dyadic relative standing to analyze the impact of mergers and acquisitions on the subsequent career mobility of the merger architects. My analysis differs from previous research by providing a finer-grained operationalization of relative status, examining the fates of both acquiring and target CEOs, and determining postacquisition career outcomes beyond stay or go. Based on a sample of completed large M&A transactions, I conclude that acquiring as well as target CEOs experience elevated departure rates compared to non-merged CEOs; that human capital, social capital and market discipline do not explain departure incidence but that the status parity or discrepancy between the partnering CEOs does; and that merger-displaced CEOs continue to have elite job prospects in public and private firms. Moreover, I determine that the average financial performance of the merged firms in the dataset confirms the established finding of null return to the acquiring firm shareholders relative to the appropriate market benchmark.

Acknowledgements

I am grateful to many people for varied assistance in bringing this research project to fruition. To the members of my dissertation committee I offer my very deep thanks and appreciation. John Carroll, the chair of my committee, encouraged me from the very beginning to immerse myself in qualitative and ethnographic data as well as statistical and secondary sources, so that I might better understand mergers and acquisitions as lived by the people experiencing and

enacting them. Without his consistent encouragement to venture out of my office and away from my computer screen, this thesis would be a much poorer piece of work. Moreover, John was there throughout the journey to critique countless drafts toward refining my conceptualization, methodology, and analysis. He always read quickly and commented incisively on whatever content I gave him, and for this unfailing munificence as well as his many other contributions to my research development, I cannot thank him enough. The other members of my committee have been no less compelling in their presence or generous with their insights. Jesper Sorensen and Rakesh Khurana both began their involvement with my thesis on the strength of a few good ideas, and they were incredibly helpful with meaningful feedback toward developing those ideas

as the thesis journey progressed. Jesper encouraged me to reach further, to keep digging and

analyzing and also summarizing succinctly (as possible!). His uncanniness for zeroing in on key

contributions as well as key areas for improvement, and for slicing off the excess, served me

time and again. Rakesh bolstered my courage to interview CEOs with detailed and discerning suggestions as to how to proceed at each stage of the process from contact through questions, analysis, summation and presentation. He also supplied ongoing reinforcement concerning the value of the chief executive interviews, for which his own work provided the most persuasive

example and a fascinating model to emulate. The above sentences scarcely capture the full

collective impact of my esteemed committee members.

I have also benefited immensely from the input of management scholars at various universities who took the time to comment on work in progress that I presented in talks or at conferences. To

everyone who listened to my presentations or read my papers and then asked questions or made suggestions I am truly grateful. For in-depth commentary and overall inspiration to continue the work, I thank Paul Hirsch, Paul Lawrence, Peter Marsden, Harold Daniel, Barbara Hilkert

Andolsen, Freek Vermeulen, Michael Szenberg, Rita McGrath, Willie Ocasio, Amy Edmondson, Leslie Perlow, Mary Tripsas, Marguerite Schneider, Ella Edmonson Bell, Stella Nkomo, Nejdet Delener, Asli Arikan, David Thomas, David King, Jeffrey Krug, Damon Phillips, Robert Vambery, Hayagreeva Rao, Alessandro Gandelli, Mohammed Hamza, Pam Haunschild,

Laurence Capron, Hugh Gunz, Misiek Piskorski, Yigal Newman, Mike Geppert, Diana Sharpe, Christoph D6rrenbacher, Don Hambrick, Bert Cannella, Hans Hansen, David Boje, Gavin Schwarz, Ursula Mense-Petermann, Ian Palmer, Koen Dittrich, Ben Gomes-Casseres, Brian Pentland, Elaine Yakura, Mark Ackerman, Alexander von Boehmer, Allan Afuah, Ahbijit Mandal, Johann de Jaeger, Peter Cebon, Peter Ras, Jane Salk, Pat Obi, Leon Schiffman, Erol Eren, Guhan Subramanian, Mauro Guill6n, Wendy Cukier, Jim Detert, and Bobby Banerjee. Whether at a reception in Barcelona, on the train to Venice, on the streets of Budapest, on a lake

in Ljubljana, over coffee in Seattle, tea in Boston, lobster in Cape Town, walking in Denver,

getting rained on in London, exploring in Cape Town, touring in Banff, in a taxi leaving New

communicating by intemet, phone or in person, they have all at different times and in different ways been tremendously helpful in following up with ideas, comments or suggestions.

The faculty at MIT Sloan have been wise and available teachers and research avatars. I thank Deborah Ancona, Lotte Bailyn, Eleanor Westney, Roberto Fernandez, Tom Allen, and John Van Maanen for many helpful words along the way. Paul Healy provided an early tutorial on merger finance. Bill Pounds provided endgame confirmation of the CEO findings.

Thanks to funding received through the MIT Undergraduate Research Opportunities Program and the Cambridge-MIT Institute, I was fortunate to have excellent research assistance from MIT

mand Cambridge University undergraduates Pravin Bagree, Neil Desai, Ashish Gupta, Timothy Lee, Sheryl Lim, Elizabeth Park, and Chirag Shah. While all mathematically gifted and interested in post-graduation jobs in the financial services world, they came to my project with mature appreciation for the human side of mergers and acquisitions. As one of the students spontaneously expressed the essence of the project right at our first meeting, "I don't just want to

manalyze numbers--I also want to understand the people and the thinking behind the deals." Over two years, their numerous hours of detailed data collection on mergers, firms and CEOs

established the statistical foundation for the dissertation. Moreover, their perceptive questions, capacity for collaboration, and preliminary data summaries further contributed to the research

effort. I wish them the best in their future careers on which they have all now embarked.

In addition, the data collected for this thesis would not have been possible without the repeated and invaluable assistance of Chris Allen of Harvard Business School Research Services who

gave me the guidance in the early stages to begin constructing the unique database later fully

developed with the aid of the undergraduate research assistants. I also thank Sandra Nunley at HBS who always commended my progress and made me welcome.

A dissertation of the depth encouraged by my committee fundamentally depended on the time unstintingly given by the CEOs interviewed. They reinforced the Kennedy credo that

"leadership and learning are indispensable to each other." While I cannot thank them here by name, I am profoundly grateful for the hours they spent in describing to me their merger

aspirations and experiences. They not only spoke at length in our interviews and were agreeable

to answering numerous wide-ranging questions, they also referred me to fellow CEOs and

verbally expressed support for this type of research examining merger issues. To the first CEOs interviewed in the course of the project, I am especially thankful for your insights and interest that spurred the development of the CEO leadership and motives parts of the dissertation. Without Ike Colbert, Margaret Daniels Tyler, David Thomas, Bill Qualls, and Phyllis Wallace, this dissertation would never have left the starting gate. Rachel Bulbulian and Araceli Isenia helped give me the courage to persist. The faith earlier demonstrated by educational and

workplace mentors Constantine Simonides, Laurence Bishoff, Linda Rounds, Uri Treisman, John Gioia, Peter Senge, and D.G. Ganesan, who repeatedly enlarged my responsibilities and their expectations, helped spur me through the homestretch.

I treasure the tremendous affirmation and affection from longstanding friends Carla Williams, Maiya Verrone, Karen Routt, Lori Miley, and Suhnne Ahn. In addition to being a stalwart friend

in innumerable ways, Claude Poux helped me pick the perfect piano of my dreams-and

encouraged me toward the professional achievements that would enable me to afford it. Kathryn Welter cheered me on when I needed a boost. Varghese George, Vera Ballard, and Ann Wiggins shared with me many meals and hours of conversation. Four years ago, as I strove to be

conventional and conformist in my business outlook, Shelby Putnam Tupper (we went to

elementary school together!) inspired me with the words that is it not only possible but desirable to make a positive impression by being different.

Friendship also flourishes in the midst of scholarly pursuits. I thank MIT Sloan officemates Jean-Jacques Degroof, John Hammond, David Rabkin, Annique Un, and Nancy Staudenmeyer. Jeff Furman dispensed consistently sage advice. Sandra Rothenberg put it all in perspective. Gregg Scott shared car magazines, fine chocolate, and favorite sushi restaurants. Fellow merger-oriented doctoral students at Harvard-David Ager, Lisa Haueisen Rohrer, and Saikat Chaudhuri-helped make the dissertation journey more productive and enjoyable. They

understood working long hours at night and sending email at three in the morning.

The mothers of Boston Ballet, Montessori Educare, Longy School of Music, Rhythmic Dreams, and the Teddy Bear Club alternately commiserated and praised. Magdalena Luca, Becky Derby, and Lisa Houh always asked how the thesis was progressing and always appeared convinced, even when I wasn't, that it soon would be done. Lydia Kankunnen, Marcia Yamada, Maryann Houglet, Laurisa Neuwirth, Zeina Kahhale, Sonoyo Riseborough, Anne Joyce, Mary Mullen, Mary Wong, Aixa Beauchamp, Smaranda Moisescu, Natalia Balabai, Joanne Haney-Tilton, Ellen Zientara, Yongshu Chen, Ann Bible, Alexa Dulchinos, and Donna Supko shared play

dates, parenting, and work-family experiences in a manner supporting each of us to accomplish

our respective goals in multiple arenas. Kerstin Allen showed how statistics and motherhood go well together. For babysitting help and so much more, I forever applaud the Tramontozzi family. To my family, who have helped in so many ways, who have inspired and encouraged, comforted, coddled and prodded, I thank them for everything they have done. I dedicate this thesis to the memory of my father, Ernest Timothy Marshall, Jr, and of my grandparents-Ernest Timothy Marshall, Sr, Louise Conger Marshall, Charles Atwood Stevenson, and Kathleen Isabella

McCaughan Stevenson-who were all present so much in the early years and whose love I

remember daily. My mother, Brenda Stevenson Marshall, has been a rock. Her hours of patience and nurturing are priceless. My two brothers, Timothy and Steven, have joint

stewardship of our family history and are not only my siblings but also my spiritual companions in life. From the extended family, many have been repeatedly positive influences, including my

cousins Mary Jo, Linda, Janice, Bruce, and Ruth and my aunts Bernice, Madge, and Cheryl as

well as many other aunts, uncles, and cousins from the community of family and friends which my grandparents helped create and in which they strongly participated. My relatives by marriage-Jim, Kay, John and Mary Park-have amazed me with their thoughtfulness and consideration during my thesis research. Most of all, I thank my husband, James Kimbrough Park, whose constant love and belief in me has been the foundation for my combined family and work endeavors. Our daughter, Charlotte Isabella, has blessed our lives throughout.

Table of Contents

A bstract ... ...3 Acknowledgements ...4 Table of C ontents ...7 ist of T ables ...9 IList of Figures ... 10 Chapter 1: Introduction ... 11 Research Questions ... 11Summary of Key Findings and Contributions ... 12

Merger Waves and the 1990s Merger Era ... 15

Political, Economic and Historical Context ... 24

Modem M&A Activity: The Importance of Large Deals ...26

Outline of the Dissertation ... 29

Chapter 2: CEO Leadership, Motivation and Mobility in Large M&A Deals ...33

Disciplinary Foundations ... 33

Spanning Disciplinary Boundaries ... 36

Does Leadership Matter? ... 37

Why Do Mergers Occur? ... 44

What Are the Postacquisition Career Moves of Business Elites? ... 53

Chapter 3 : Methods and Data ... 59

Research Strategy and Setting ... 59

A Brief Review of M&A Research Approaches ... 59

Data Collection and Analysis in Two Studies ... 61

Study One: Exploring CEO Merger Motives and Leadership Roles from In-Depth Interviews with CEOs ... 61

Interview Process and Data Analysis ... 66

Study Two: Examining Postacquisition CEO Mobility Based on an Expanded Merger and CEO Dataset from Secondary Sources ... 69

Secondary Data Sources on Mergers, Firms and CEOs ...75

Methodology Overview ... 80

Chapter 4: The Metamorphosis Motive for Merging ...91

Merger Occurrence, Performance and Motivation ...93

The Motivation for Large M&A Deals ... 97

Discussion ... 125

Chapter 5 : CEO Leadership Roles in the Merger Process ... 132

Focus on the CEO ... 135

Acquiring and Target CEOs in the Merger Process ... 139

Discussion ... 153

Chapter 6 : The Merger-Careers Connection: Dyadic Relative Status and the Postacquisition Departure Rates of Acquiring and Target CEOs ... 159

Motivation for Studying Acquiring CEOs ... 160

Theory and Hypotheses ... 164

Results ... 181

Discussion and Conclusions ... 199

Chapter 7 : Postacquisition Career Fates of Acquiring and Target CEOs ...236

Mergers and Chief Executive Careers ... 236

Conceptualization of the Postacquisition Career ... 240

Results on Postacquisition Career Paths ... 242

Discussion and Conclusions ... 248

Chapter 8: Conclusions and Implications for Future Research ...260

Contributions ... 260

Future Research Directions ... 262

CEO-Merger Connections ... 264

References

...

268

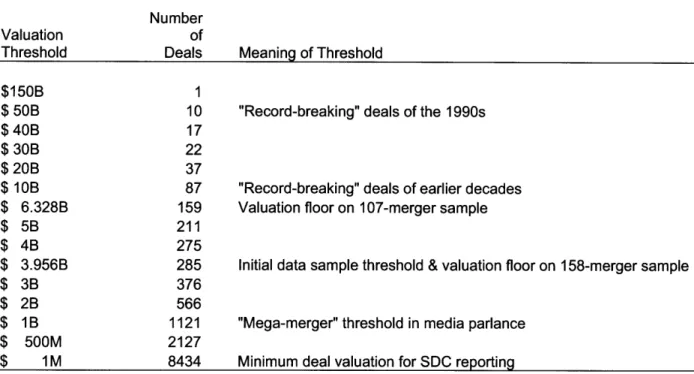

Appendix A: The 158 Largest Combinations of Public U.S. Companies in the Fifth Merger Wave, 1993-2000 ... 300

Appendix B: Acquiring and Target CEOs in the 107 Largest U.S. Public M&A Deals, 1993-2000 ... 305 Appendix C: Acquiring and Target Firms in the 107 Largest U.S. Public M&A Deals, 1993-2000

List of Tables

Table 1.1: U.S. Merger Waves of the Nineteenth and Twentieth Centuries ... 30

Table 3.1: CEO Informants by Deal Rank and Value for Top 50 U.S. M&A Deals, 1993-2000.83 Table 3.2: CEO Informants by Industry of Merger for Top 50 U.S. M&A Deals, 1993-2000 ...84

Table 3.3: Sample Questions in Semi-Structured CEO Interviews . ... 85

Table 3.4: Completed M&A Deals by Valuation at $500 Million and Above, 1993-2000 ...86

Table 3.5: CEO Interactions, Strategic Framings, Pricing, Financing and Advising in Major M ergers ... 87

Table 3.6: SEC Documents Commonly Filed in Connection with Mergers and Acquisitions ...88

Table 6.1: Literature Summary: Incidence, Antecedents and Effects of Postacquisition Target Top M anagement Turnover ... 209

Table 6.2: Characteristics of Acquiring and Target CEOs in Large Mergers ...210

Table 6.3: CEO Postacquisition Departures over Three Years ...212

Table 6.4: Postacquisition Departure Rates from Multiple Studies ...213

Table 6.5: Postacquisition Departure Results for Testing Hypotheses Hi, H2, H3, and H8 ... 215

Table 6.6: Comparing Postacquisition Departure Results for Different Groups of Top Executives ... 2 16 Table 6.7: Co-CEOs and Other Power Sharing Arrangements ...218

Table 6.8: Target CEO and Acquiring CEO Reversals of Status ...220

Table 6.9: Means, Standard Deviations and Correlations ...221

Table 6.10: Event History Analysis on the Probability of Postacquisition CEO Departure ...223

Table 7.1: Matrix of Postacquisition Career Outcomes ...255

Table 7.2: Career Outcomes for Acquiring and Target CEOs at Three Years Postacquisition ..256

List of Figures

Figure 1.1: M&A Incidence and Contemporaneous Valuation by Year, 1968-2004 ...31

Figure 1.2: Big Deals of the Eighties and Nineties ... 32

Figure 2.1: M erger Black Boxes ... 57

Figure 2.2: Vicious and Virtuous Cycles in Large M&A Deals ... 58

Figure 3.1: Connectivity Among Core CEO Interview Informants and Dealmaking CEOs in the 50 Largest Public U.S. M&A Deals of 1993-2000 ... 89

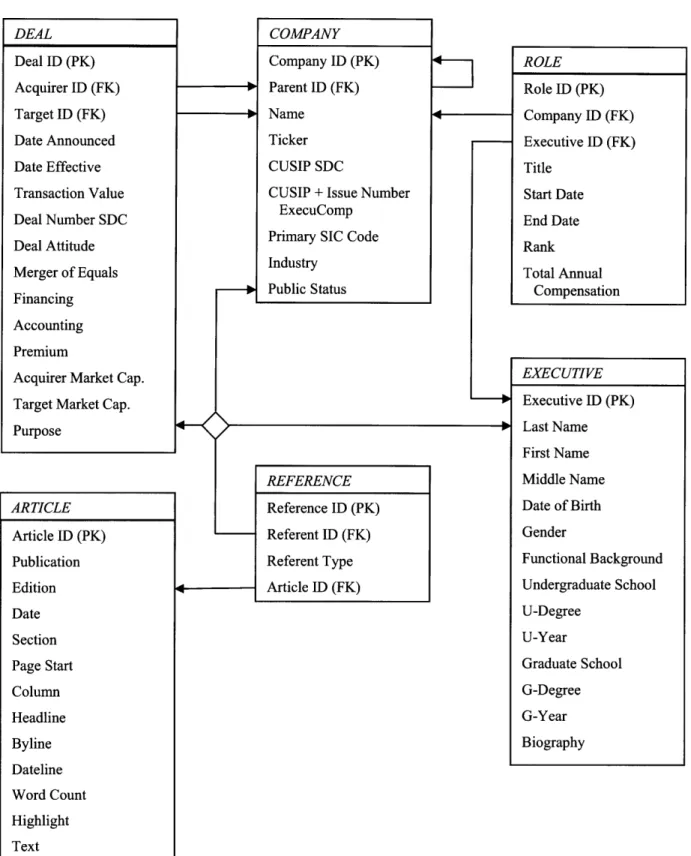

Figure 3.2: Entity-Relationship Diagram ... 90

Figure 4.1: A Metamorphosis Model of Merging ... 130

Figure 4.2: Interrelated Components of the Metamorphic Strategic Shift ... 131

Figure 6.1: Departure of Acquiring and Target CEOs by Time Elapsed Since Acquisition ...227

Figure 6.2: Voluntary and Forced Departure of Acquiring and Target CEOs by Year ...228

Figure 6.3: Frequency of Joint Outcomes: Acquiring CEO Postmerger Rank by Target CEO Postmerger Rank in Year 1 ... 229

Figure 6.4: Frequency of Joint Outcomes: Acquiring CEO Postmerger Rank by Target CEO Postmerger Rank in Year 2 ... 230

Figure 6.5: Frequency of Joint Outcomes: Acquiring CEO Postmerger Rank by Target CEO Postmerger Rank in Year 3 ... 231

Figure 6.6: Distribution of CEO Relative Status by Year ...232

Figure 6.7: Postacquisition Departure Rates of Acquiring and Target CEOs within 3 Years by Relative Status in Year 1 ... 233

Figure 6.8: Postacquisition Departure Rates of Acquiring and Target CEOs within 3 Years by Joint CEO Ranks in Year 1 ... 234

Figure 6.9: Distribution of Jensen's Alphas as Market-Based Measure of Acquiring Firm Performance in the 105 Largest Public U.S. M&A Deals of 1993-2000 ...235

Chapter 1:

Introduction

This dissertation concerns the linkage between strategists and strategy. I examine the close connection between chief executives as chief strategists of large U.S. corporations and the mergers and acquisitions, or intercorporate combinations, as prime strategies in which those companies engaged during the global M&A wave of 1993-2000. My research addresses three interlinked CEC) and merger issues at the inception, implementation and outcome of the deals:

(1) CEO motives for merging, (2) CEO leadership in large M&A deals, and (3) the consequences

of large mergers for CEO career trajectories. The focus on motives, leadership and mobility applies equally to acquiring and target CEOs, and the dissertation therefore covers crucial dimensions of merging based on the top leadership perspective from both sides of the

transaction. The current chapter begins by describing the motivating questions as well as the key empirical and conceptual contributions of the research. I then provide historical and theoretical background on M&A deals, merger waves, and the importance of studying large mergers. The chapter concludes with an overview of the dissertation and a guide to subsequent chapters.

RESEARCH QUESTIONS

In this dissertation, I investigate three interrelated research questions involving CEOs and

mergers: (1) Why do mergers occur? (2) What are CEO roles in the merger process? and

(3) What are the consequences of merging for CEO postmerger career paths? The three

questions stem from in-depth interviews with dealmaking CEOs. The initial aim in interviewing was to understand the lessons learned in the process of merging. Identifying the lessons learned fiom merging led to the questions "what are CEO motivations for undertaking major M&A deals?" and "what are specific CEO leadership functions in the merger process?" Pursuing interview evidence of unexpected developments in CEO postmerger career outcomes led to the question "what is the impact of major mergers on chief executive mobility?" The last question required the collection of additional secondary data on mergers, firms and CEOs to ascertain large-scale mobility results. The conclusions emerged through examining large U.S. M&A deals of the 1993-2000 merger wave from the chief executive perspective.

This set of research questions merits consideration for several reasons. Mergers happen frequently, often radically restructuring the corporate landscape, and there is value in studying such simultaneously common and intensive events. Regarding the question of why mergers occur, merger motives have been investigated less often than merger consequences such that our understanding of motives, despite a variety of explanations advanced to date, is still incomplete.

Mergers typically have unfortunate financial and personnel outcomes, and an enhanced understanding of motives might contribute to our comprehension and avoidance of mergers

going awry. Regarding the question on the leadership responsibilities of merger architects and heads of firms, how CEOs direct mergers and acquisitions has been a relatively neglected issue. Although CEOs are lightning rods for praise or discontent concerning organizational

performance, and although voluminous literature exists on the definition and delivery of leadership, considerably less attention has been paid specifically to the leadership mandate of

CEOs in the merger process. Regarding the question on the mobility consequences of M&A transactions, it is useful to study CEO postmerger career paths to obviate the reductionist and

often inaccurate impression of binary outcomes in the corporate hierarchy (up or down, stay or go, success or failure) in favor of a more nuanced understanding of mobility possibilities. An additional motivation was to investigate the previously ignored fates of acquiring CEOs, who

may not be as secure in their positions as assumed. In every question, I study the perspectives of

acquiring as well as target CEOs, countering the tendency in previous research to study senior executives from only one side of the transaction.

Having stated the research questions, I next summarize the key findings. The remainder of the introductory chapter then proceeds as follows. After the findings summary, I explain the occurrence of merger waves, the uniqueness of the 1990s merger era, and the extreme deals of that time. By comparing types of M&A transactions to modes of national expansion, I enlarge

the economic, political and historical context for studying large M&A deals and the CEOs at the

helms of the combining firms. The subsequent section turns to how the importance of studying large intercorporate combinations derives from reasons of investor capitalism, globalization, and

the presence or absence of leadership in large companies and behind large deals. I then explain

the economic and institutionalist ramifications of high-valuation transactions as lodestars in the realm of deals. The chapter concludes with an overview of the dissertation.

SUMMARY OF KEY FINDINGS AND CONTRIBUTIONS

CEO Motivations for Merging

The first of three key findings in this dissertation is that metamorphosis, a profound form of organizational renewal and competitive repositioning, occurs as both strategic intention and outcome in major mergers and acquisitions. The target firms are not merely "bolted," "grafted," or "glued" to the acquirer (to use terms from the business press), and the result is not simply

business as usual. These deals create business entities of revised form and function in the national and international marketplace. The combined firms are very large in size, which both

Browne, the results of these business combinations are the "super-majors" (Financial Times 2002c). Browne uses the term to describe the enormous global oil firms formed through recent or historic mergers. The phrase applies equally well to behemoths in other industries that have become a new type of firm by virtue of size, market penetration, technology leadership, and overall changes in many respects. The metamorphosis motive complements the previously identified motives by encompassing both managerial and financial concerns. My central finding from analyzing hours of CEO interview data is that the metamorphosis in large mergers occurs in

(1) management structure (2) strategic direction, and (3) corporate culture. CEO roles in the

management restructuring include jolting top managers, regenerating management teams, and comparing, balancing, and integrating managerial capabilities from two sides of the transaction. The strategic shift involves internationalizing the firm, realizing synergies, increasing firm size and status, attaining technology and market leadership, and obtaining additional cash toward those ends. The cultural dimension encompasses-with leadership both acknowledging and ignoring-the systemic turmoil and emotion upheaval accompanying major mergers.

CEO Leadership in Major Mergers and Acquisitions

The second key finding addresses the importance of CEO leadership in mergers and acquisitions. CEOs play a vital role as architects of major intercorporate transactions, but leadership of M&A deals has been little explored in either the mergers or leadership literatures. The absence of the leadership factor in the literature is striking because in major strategic maneuvers requiring substantial resource commitments and organizational re-arrangements, the decisions and convictions of the acquiring and target CEOs are a priori critical to the process. Leadership in the merger process is manifested in the tripartite executive roles of (1) making the merger, (2) placing and displacing people, and (3) fulfilling the strategic vision. Leadership differs from management in transcending quotidian concerns to focus on mobilizing people to face difficult circumstances and decisions (Heifetz 1994). Previous research has viewed CEO influence as controlling (leadership matters), constrained (top managers have little or no effect

on firm performance), or contingent (leadership matters in industries with scarce or slack resources). I add a contextual perspective: leadership depends on the firm, societal, or national

setting and should be studied in conjunction with that background. The investigation of CEO motivation and leadership in large deals contributes to the evolving literature on merger motives and the little examined topic of chief executive leadership in mergers and acquisitions.

CEO Postmerger Career Moves

A finding related to the existence of CEO leadership and the metamorphosis motive in major mergers concerns dual negative career consequences. As the large deals proliferated in the

1990s, so did the attrition rates for target and acquiring CEOs. Previous research has confirmed target senior executives as experiencing abnormally high turnover (e.g., Krug and Hegarty 2001; Buchholtz, Ribbens and Houle 2003), and CEOs nowadays are generally susceptible to

increasingly short tenure (Conger and Nadler 2004). However, little attention has been paid to the job survival rates of acquiring CEOs. The crucible of the major merger abbreviates the tenure of CEOs from each side and also opens new career opportunities in other firms.

Mergers have long been recognized as having the potential to alter or even derail careers. Acquiring or target CEOs after the merger may find themselves jobless, in figurehead positions, or elevated to new and stronger positions of power. The matrix of postacquisition career

outcomes includes possibilities representing different combinations of organizational affiliation and positional power. The acquiring or target CEO is reigning (same organizational affiliation and high positional power), relegated (same organizational affiliation and lower positional power), renewed (different organizational affiliation and high positional power), or redefined (different organizational affiliation and lower positional power). Retirement, where the CEO has departed from paid executive employment in any business organization, is another possible

outcome. In the reigning outcome, the acquiring or target CEO has become the chief executive

or anointed heir of the merged entity. The relegated CEO has a relatively ineffectual

postacquisition position such as a vice chairman without operational or budgetary responsibility

in the merged firm. The renewed CEO has obtained a top leadership position as CEO, chairman, or designated successor in a comparable corporation. The redefined CEO has a non-equivalent

position (such as an advisory vice-chairmanship or non-executive chairmanship) in a comparable firm or a top-ranking position in a non-equivalent firm (such as a not-for-profit organization,

private equity company, or early-stage entrepreneurial venture). On a related note, some CEOs

were temporarily redefined through brief stints at start-up firms or investment boutiques before returning to head major public corporations. Retired CEOs, whether they resigned voluntarily or involuntarily, may be philanthropists, directors, private investors, or otherwise occupied with assorted interests, but are not employed as officers in corporations. My analysis differs from previous turnover research in considering the fates of both acquiring and target CEOs and in examining the sequence of postmerger career moves beyond a simple stay-or-go outcome. This investigation of CEO postmerger career outcomes contributes to research on postacquisition

integration and departures, management turnover, executive labor markets, and CEO succession. I now turn to the focal deals in the context of past merger eras.

MERGER WAVES AND THE 1990S MERGER ERA

Merger Waves

Mergers occurred in five distinct waves during the late nineteenth through twentieth centuries, with the years 1993-2000 representing the last and largest cycle of the past century (Figure 1.1). The previous waves ran from 1890-1905 (Dewing 1921; Eiteman 1930; Livermore

1935), 1924-1928 (Florence 1937), 1961-1969 (Beckenstein 1979), and 1981-1989 (Flom 2000). The emblematic deals varied with the merger era, as shown in Table 1.1. The first wave created

monopolies, the second oligopolies, and the third conglomerates; the 1980s saw the hostile takeover or disciplinary wave (Lamoreaux 1985; Golbe and White 1988; Lubatkin and Lane

1996); the 1990s wave does not yet have a universal label but was strategic and deregulatory in nature as seen in numerous expedient consolidations in response to industry-level deregulation (Whitford 1997; Andrade, Mitchell and Stafford 2001; Holmstrom and Kaplan 2001; Auster and Sirower 2002; Shleifer and Vishny 2003; Harford 2005).

The 1890-1905 wave heralded the massive, anti-competitive, monopolistic trusts such as Standard Oil, American Tobacco, American Sugar Refineries, and US Steel. Unfettered growth, social Darwinism, and adulation of Horatio Alger-like robber barons defined the era. The 1920s oligopoly wave facilitated rather more streamlined companies, such as Allied Chemical or Bethlehem Steel, that in small but powerful cabals dominated their market niches. Founders and heads of firms amassed largely unresented riches as many would-be millionaires rushed to invest

in the stock market. In the 1960s merger era, portfolio diversification characterized the

conglomerate transactions in which rapidly growing firms such ITT, Teledyne and LTV enacted

serial acquisitions across many industries. Despite the end of the Great Depression and the

prosperity of the post-World War II years, the middle classes of the 1930s to 1970s had retreated from equity investments as social security programs and defined-benefit pension plans arose.

Next came the disciplinary wave of the 1980s, symbolized by the exploits of investment bankers, corporate raiders, and inside traders. The high-grossing movie Wall Street (1987) and bestselling books Liar's Poker (Lewis 1989) and Barbarians at the Gate (Burrough and Helyar

1990) chronicled the implicit "greed is good" motto. This fourth merger wave became known for leveraged buyouts (LBOs) entailing privatization through innovative junk bond financing, and hostile takeovers (unsolicited, coercive and contested acquisition maneuvers) undertaken to remove supposedly underperforming management target teams from undervalued firms (Shleifer

and Vishny 1990). A return to firm specialization and a new focus on core competencies further

The strategic-deregulatory wave of the 1990s followed. This fifth wave resembled the second in the emphasis on horizontal combinations and in the standard backdrop of transient stock market ebullience (Shiller 2000) but was international in reach (Calori, Lubatkin and Very

1996). Nationwide or state-by-state deregulation in industry sectors such as financial services,

telecommunications, and utilities precipitated much merger activity (Andrade, Mitchell and Stafford 2001). Technological advances reinforced the hospitable impact of deregulation on merging (Gorton, Kahl and Rosen 2000). Unprecedented numbers of large, friendly transactions distinguished the fifth wave, where bilateral corporate governance involvement and accounting arrangements conducive to stock swaps diminished the incidence of hostile, debt-laden deals

(Holmstrom and Kaplan 2001). The modal deal shifted from unfriendly to amiable to the extent

that mergers of equals-characterized by approximate size parity, self-described equality, and a balanced distribution of postmerger stock and directorships between the participating

firms-were a standout feature of the new wave (Wulf 2004). As reflected in U.S. Security and

Exchange Commission (SEC) filings, mergers-of-equals rose from two to 10 percent of total domestic combinations during the decade (EDGAR Online 2001).

Deals and Dealmakers

Supporting the typology of eras and differentiation of deals and firms, each merger wave

transpired under different dealmaking styles of the participating CEOs (Table 1.1). Whether the merger architects received contemporaneous applause or approbation, whether they were labeled visionaries or deviants, each wave of M&A deals has been followed by a wave of criminalization and indictment of the managers and financiers whose behavior in retrospect was increasingly judged more by statutory and ethical standards than by short-term financial metrics (Park 2004).

A distinguishing characteristic of the most recent merger wave was the close connection between CEOs as strategists and interfirm combinations as strategy: CEOs were active architects and not simply unwilling or unwitting participants in these transactions. This connection contrasts with the merger waves of the 1980s, which were frequently brokered by outsider corporate raiders or takeover specialists rather than the insider acquiring and target CEOs and board members. To be

sure, the merger-making CEOs of the 1990s acted in concert with other corporate governance

insiders from senior management or the board of directors, and they also relied to differing degrees on intermediary investment bankers and legal advisors. Yet, I argue, they further played pivotal roles, unique to their positions, from deal inception through implementation. Moving on

from merger waves and different deal and dealmaking styles, I now consider industry membership as another important feature of the merger context.

Industry Effects in Merger Formation

As in previous merger waves, the 1990s M&A transactions did not occur evenly across industries. As the conglomerate deals of the 1960s gave way to the disciplinary and deregulation deals of the 1980s and 1990s, horizontal transactions superseded vertical combinations in

frequency (Mergerstat 1997; 1998; 1999b). Not only did most acquiring and target firms come from within the same broad sector, certain industries-financial services, telecommunications, media and entertainment, oil and gas, utilities, pharmaceuticals, and computer software and services-experienced especially intensive merger activity. Ravenscraft (1987:34) in analyzing the first four merger waves rightly observed that "further research needs to focus on the

development of more detailed industry-specific merger data." The disproportionate distribution of M&A deals across industries reflects the multiplicity of precipitating factors beyond

managerial predilections (Roll 1988). Although this dissertation spotlights the leadership

connection, the 1990s merger story is one of industries as well as CEOs. Accordingly, a greater

number of CEO informants are drawn from the financial services, telecommunications, and

energy sectors, as documented in the methodology chapter.

Researchers have investigated the relationship between acquisitions and industries in various ways. Earlier work positing the motive of risk reduction through acquiring firms in different industries has been discredited (Smith and Schreiner 1969; Smith 1970; Amihud and Lev 1981), though more recent work demonstrates the latent efficiency of large diversified conglomerates in the 1960s (Andrade, Mitchell and Stafford 2001). Resource dependency theory proposed that merging across industry boundaries would increase competitive advantage by internalizing critical suppler-distributor relationships (Pfeffer 1972; Finkelstein 1997). Yet others have wondered whether the exclusive supplier-distributor relationships forced by vertical integration are advantageous (Dreazen, Ip and Kulish 2002). Both the upstream and downstream parties might forfeit valuable alternative partnerships in their unitary reliance. Additionally, the idea of escaping the pressures of a declining industry (Rumelt 1974:82) through acquiring firms in growth industries has been shown to be ineffective for rectifying the poor performance of the acquirer (Anand and Singh 1997; Stimpert and Duhaime 1997b). Morck, Shleifer and Vishny (1988) discerned that the likelihood of a hostile versus friendly takeover is associated with the performance of the target firm and its industry. Low Tobin's-q firms in low-q industries were more likely to become the targets of hostile takeovers, whereas higher-q firms in higher-q

industries were more likely to be the targets of friendly transactions in the 1980s. (Tobin's q is

the ratio of the market value of a business entity to the replacement cost of its physical assets, such that higher q values imply higher levels of intangible assets and hence overall investment performance at the designated business unit, firm or industry level of analysis.)

Further related to patterns at the industry level, evidence exists for the cultural

convergence of firms from the same industries (Pennings and Gresov 1986; Gordon 1991). Firms within the same industry vary in organizational culture, but shared norms, values, and behaviors exist across firms within a given industry. Chatman and Jehn (1994) found that the cultural similarity of firms within service industries corresponded to firm growth and the use of new technologies. Some industries succeeded better than others in adopting innovation.

Lubatkin, Schweiger and Weber (1999) found differences in fourth-year post-merger executive turnover in the banking and manufacturing sectors. Turnover was mediated by cultural

compatibility (at the top management team level) for financial services mergers and autonomy

removal (again at the senior level) in manufacturing firms.

I extend the concept of industry-level culture to consider industry-level cultures of

merging. In the 1993-2000 wave, certain industries not only witnessed greater merger activity

but also experienced different types of deals. Exceptions exist, but patterns can be discerned. For instance, the oil and pharmaceutical industries inclined toward takeovers: e.g., Exxon acquired Mobil in 1999; Pfizer acquired Warner-Lambert also in 1999; internationally, British Petroleum acquired Amoco in 1998, followed by BP Amoco acquiring ARCO in 1999, after which the merged firm became simply BP. The financial services sector inclined toward partnership transactions: e.g., Travelers combined with Citicorp to become Citigroup in 1998,

and Chase Manhattan combined with JP Morgan to become JP Morgan Chase in 2001. Even

when NationsBank acquired Barnett Banks in 1997 and then BankAmerica in 1998, there was discussion of harmonizing and integration. The media and entertainment industry as well as the telecommunications industry saw a shifting balance of power between the acquirer and target firms: America Online combined with Time Warner in 2000 to become AOL Time Warner; Viacom joined with CBS; and internationally, Vivendi acquired Seagram's. Examples leaning toward the takeover style occurred when SBC acquired Ameritech, Qwest acquired US West, and AT&T acquired Continental Cablevision; but then Bell Atlantic combined with NYNEX and

GTE in peer mergers. As the wave matured, the espoused ethos became the "merger-of-equals"

to the extent that even a conquest-oriented deal in the oil industry, the Chevron takeover of Texaco to become ChevronTexaco in 2001, adopted the language (Park 2002c).

A striking industry-related feature in the fifth merger wave has been the partial reaggregation of the Standard Oil trust and the statutory Bell System, as can be inferred from examples in the preceding paragraph. From the more than 30 companies separated after the 1911 antitrust ruling in Standard Oil of New Jersey v. U.S. that dismantled the Rockefeller monopoly, six of those remaining have recently combined into three: Exxon Mobil, ChevronTexaco, and ConocoPhillips. (British Petroleum acquired Amoco, ARCO, and in 1987 the Standard Oil

Company of Ohio.) From the seven Baby Bells created after the 1984 mandated divestiture of the Bell System (AT&T), four central competitors remain: SBC acquired Pacific Telesis and Ameritech; Verizon formed from the mergers of Bell Atlantic with NYNEX and GTE; Qwest acquired US West; and Bell South has grown mostly organically and in relative isolation. Consolidation is ongoing. In 2004, SBC agreed to purchase the relatively new entrant to long distance, MCI (formerly WorldCom), while in early 2005, Verizon and Qwest battled to acquire the long-distance remnant of the original AT&T, which had become three separate firms starting in 1998. The mobile division AT&T Wireless had been acquired by Cingular (a Bell South and SBC wireless joint venture) in 2004, and the broadband component AT&T Broadband had been acquired by cable company Comcast in 2001. The potentially higher cultural compatibility for firms originating in the same industry or from a shared monopolistic progenitor may have facilitated the historic and continued consolidation in the telecom and oil sectors.

Likewise concentration within other industries is remarkable. The big eight accounting firms have shrunk to four: Ernst & Young International, PricewaterhouseCoopers, KPMG International, and Deloitte Touche Tohmatsu. The international pharmaceuticals industry is a narrower array of merged and renamed players: e.g., GSK was formed from the merger of Glaxo Wellcome and SmithKline Beecham; Novartis arose from the merger of Ciba-Geigy and Sandoz; and Aventis originated in the union of Rh6ne-Poulenc and Hoechst (then Sanofi-Synthdolab acquired Aventis in 2004, winning out over a counterbid from Novartis). Even within the previously merger-inimical computer industry, deals have occurred. Where there was once Digital Equipment Corporation, Compaq, and Packard, there is now only Hewlett-Packard (Compaq acquired DEC in 1990 and H-P acquired Compaq in 2001). Sheth and Sisodia (2002) argue that industries naturally incline to three main competitors. The horizontal

combinations of the past decade recall the monopolies and oligopolies of the early twentieth century, indicating that the series of merger waves has gone full cycle. This historic perspective contextualizes the recent deals-and perhaps also hints at perils of ongoing consolidation.

Factors Contributing to Merger Waves

The distinctive character of merger waves stems from unique combinations of factors concerning the regulatory climate, capital markets, financial instruments, liquidity levels, technological innovations, laborforce participation, economic conditions, and management proficiency and personality during each time period (Jensen 1988; Hitt, Harrison and Ireland

2001; Harford 2005). In addition, exogenous shocks such as large-scale terrorism, disease, natural disasters and unanticipated economic downturns represent wildcard influences affecting

investor confidence. Strong stock market performance helped trigger and sustain each wave, with mergers increasing in times of soaring but ultimately unsustainable bull markets (Shleifer

and Vishny 1990; Jensen 1993). Though the danger exists of deceptive equity valuations

susceptible to sudden deflation (Shiller 2000), economic disturbances embodied in upward stock prices coincide with and may provoke merger waves (Gort 1969).

Not only the state of the economy but also the confluence of legislative and political

forces has affected the dealmaking climate, facilitating or hindering merger formation over the

past 115 years (Manne 1965; Shull and Hanweck 2001). From the Sherman Antitrust Act of 1890 through the Clayton (Northern Securities) Act of 1914, the Williams Act of 1968, and the

Hart-Scott-Rodino Act of 1976, legislation has tended to restrict merger activity. Government and regulatory agencies, often headed by political appointees and subject to political winds, have

ranged from strict to lax in interpreting provisions to ensure the financial transparency of firms and adequate competition in industry sectors. For instance, the EU Commission rejection of the

proposed 2001 GE acquisition of Honeywell International and the consequent inter-firm and international acrimony demonstrated the importance of regulatory oversight in general and the rising impact of international review in particular (Financial Times 2001; Wall Street Journal

2001d). In the U.S., the Financial Accounting Standards Board (FASB) in 1999 determined to

eliminate the pooling method of accounting for merger transactions (Fortune 1999; Mergers and

Acquisitions 2002). This method had been commonplace in large, stock-swap deals because it enhanced the postmerger return on equity and earnings per share (Rocker 2001).

The Impact of Accounting Provisions

Regarding accounting issues, the FASB has played a vital oversight role. Up through the end of the 1990s merger wave, there were two methods of merger accounting: purchase and

pooling. Under the purchase method of accounting for a merger or acquisition, the deal was

purely an expense paid with cash, debt, or stock at the negotiated purchase price. The acquiring

firm using the purchase method had to capitalize goodwill, which was the difference between the purchase price and book value of the target firm amortized over 40 years. By the pooling of

interest method, the acquiring firm accountants simply added together the balance sheets of the

merging firms and treated the historic assets and liabilities as if the combined company had

always been one firm. The acquiring firm management subsequently decided the best use for the

target firm cash. (See Hitt, Harrison, and Ireland (2001:37-38) on how acquirers readily

accessed target firm cash under pooling-of-interest accounting.) Large acquisitions during times of high equity valuations usually culminated in a pooling of interest, and the pooling method

usually coincided with stock swap financing of the deal.

The FASB determined to eradicate the pooling provision (and also the postmerger R&D write-off) due to concern that firms chose this option to deliberately avoid goodwill

capitalization and thereby inflate accounting performance measures (research expense write-offs also boosted the accounting appearance of success). Since ROE, for instance, is based on the book value of assets recorded, avoiding the goodwill capitalization required by the purchase provision would keep the book value low, increase the apparent equity return, and promulgate the impression of success for the merger (see Rocker 2001 on "fantasy accounting"). The intention had been for all mergers to be accounted for through the purchase method as is done in continental Europe (Great Britain remained an exception, see Financial Times 2002b). The FASB later altered the original plan of completely eliminating the pooling method and requiring the full capitalization of goodwill. The softened stance reduced progress toward uniform

international merger accounting standards but allowed the continued creative computation of

"value" in mergers where U.S. firms are the acquirers. After the final demise of Enron and its

accounting firm Arthur Andersen, the FASB itself came under review, and by 2003 progress resumed toward increased rigor and shared international standards.

The FASB had first voted in 1999 to eliminate the pooling option, and a curtailed version of pooling took effect in 2001 (Boston Globe 2002b). Firms completing acquisitions that had been announced toward the end of the fifth merger wave suffered financially under the new accounting rules from having to take huge write-downs several years later (Financial Times

2002a; Wall Street Journal 2002d, 2002f). By the new rules, the value of an acquisition had to

be written down in a fashion similar to any other asset-that is, when its fair market value declined below the book value. Since goodwill was the market value in excess of book value, the write-downs of the target-firm value become interpreted as write-downs to goodwill. These downgrades in valuation indicated that the target firm yielded fewer assets than expected, and that the acquiring firm may have made an unwise strategic commitment of its own resources.

Accounting maneuvers such as corporate inversions (establishing an offshore subsidiary

and then "inverting" so that the main company is headquartered in the location with the more

favorable tax treatment and the U.S. operation becomes technically the subsidiary) persist. While Tyco Ltd and Global Crossing Ltd, among others, adopted this strategy in the 1990s, the rules have tightened (Mannino 2003). As described by SEC chairman William Donaldson, the thrust of the 2002 Sarbanes-Oxley corporate governance and reporting reform is to encourage "business risk taking" while not sanctioning "legal risk taking" (Financial Times 2003a).

Three Factors in Three Industries

Three factors in particular-technology, accounting, and deregulation-predisposed the

heightened M&A activity in three sectors-telecommunications, financial services and energy. The telecommunications sector is inherently technology-intensive to address the needs of our

increasingly wired "global village." Acquisitions in that sector not only generally strengthened the capacity for product and process innovation, they also specifically increased the span of underground cable or broadband spectrum under a single company's control. Telecom firms fought to build and service the "last mile" connecting vast fiber-optic, electronic or coaxial networks transmitting voice, video or other data into consumers' businesses and homes. While telecommunications providers overinvested in capacity and slashed rates to remain competitive, the banking and energy sectors increasingly relied on technology in the form of computer models to predict consumer creditworthiness and spending patterns, the probable location of oilfields in the Arctic or Africa, or the complex manipulation of value spreads in the burgeoning market for energy trading. Questionable accounting procedures became common practice, including the use of special purpose entities, hollow swaps, indefatigable rights of usage, mark-to-market

treatment of assets and revenues (Bryce 2002), pre-pays to disguise loans as cash flow (Business Week 2003a), and various deceptive off-balance-sheet transactions.

Deregulation accelerated to the extent of becoming perhaps the foremost precipitating characteristic of mergers in the 1990s (Andrade, Mitchell and Stafford 2001). At the same time that technology had advanced and questionable accounting flourished, regulatory restrictions had loosened regarding the merging or joint venturing of firms in related lines of business:

commercial banking, investment banking, mutual funds, and insurance in financial services; local, long-distance, wireless and broadband in telecommunications, and therefore capacity and content in media and entertainment; and exploration, refining, and marketing in oil and gas. Measures facilitating deals in the relevant industries included the Telecommunications Act of

1996 enabling the joint offering of local and long-distance service by a single firm; the Financial

Services Modernization Act of 1999 repealing the 1933 Glass-Steagall prohibitions against investment banking, commercial banking and insurance offerings within a single firm; state-level legislation deregulating utilities or lifting regional restrictions on interstate banking; and

regulatory rulings such as the Federal Trade Commission allowing entertainment firms to own more than one TV or radio station per market and the Federal Energy Regulatory Commission

permitting upstream or downstream alliances in the oil industry (Dymski 1999; Manning 2000).

Record-Breaking M&A Activity and Valuation Levels in the 199os

Given favorable conditions for merging, widespread corporate restructuring occurred during the 1990s. During that decade, over 58,000 U.S. firms, including over 30 percent of the 1990 Fortune 500 firms, engaged in domestic or cross-border transactions (Mergerstat 2005).

The aggregate deal value for the decade exceeded $6.1 trillion (Mergerstat 2004: 1990-2000),

with the total transaction value nearing $1.4 trillion a year in each of the frenzied last three years of the merger wave (Wall Street Journal 2000; Business Week 2003b). In comparison, in the

1980s more than 24,000 U.S. firms merged for a total value of $1.36 trillion (Haunschild 1993; Mergerstat 2004: 1980-1989)-thus the annual deal value for each year during 1998-2000 approximated the total deal value of 1980-1989.

After the slowdown in dealmaking during the recession of the early 1990s, an upswing in

merger frequency and value resumed in 1992 domestically and 1993 internationally (see Bleeke, Ernst, Isono and Weinberg 1993; Calori, Lubatkin and Very 1996). Very large transactions followed one another in rapid succession until by the end of the cycle, 90 of the 100 largest U.S. M&A deals in history had been announced during the fifth wave (Mergerstat 2005). Worldwide the number and value of acquisitions set new records each year (Wall Street Journal 200 la), such that total global M&A activity since the start of the era surpassed $12 trillion by the year 2000

(Selden and Colvin 2003). About half the global transactions value originated in deals involving at least one U.S. firm and half in deals involving exclusively firms from abroad. (The foreign and cross-border deals involved predominantly countries in Europe and Asia, with Latin American and African nations contributing a smaller fraction of transactions, and with the

Canadian and Australian economies also as active participants in markets for corporate control.) Billion-dollar deals repeatedly set new records. While few deals from the 1980s met the billion-dollar mark (inflation-adjusted to 2002 dollars), corporate combinations beyond this threshold-popularly termed mega-mergers or mega-deals-abounded in the next decade. Over

900 deals valued at minimum $1 billion and involving U.S. firms took place in 1993-2000; (luring the 1998-2000 intensification of the wave, U.S. firms participated in a total of 557

billion-dollar deals; at the 2000 culmination of the 1990s merger wave, before the decline of 2001-2003, acquirers announced 208 transactions worth $1 billion or more (Mergerstat 2004: 1990-2000).

At the year 2000 apogee, billion-dollar deals amounted to $1.05 trillion in annual domestic value and represented a striking 74 percent of the total M&A valuation involving U.S. targets for the year. In contrast, during the subsequent merger trough, the total average deal value fell to $552 million per year, while the average number of domestic mega-deals dropped to

91 per year: 119 for 2001, then 68 for 2002, with an uptick to 87 in 2003, and a continuing upturn to 140 in 2004 (Mergerstat 2001, 2002; FactSet Mergerstat 2003, 2004). Worldwide the

2001-2003 decrease in high-value transactions was uneven, with European mega-merger activity outstripping that in the U.S. (Mergerstat 2003). The number of billion-dollar deals began to climb again in the fourth quarter of 2003 (Business Week 2003b), signaling the start of another merger wave as confirmed by the total M&A incidence and valuation the following year (FactSet

Mergerstat 2004). The 2003 turnaround in large merger frequency heralded the rise in overall

Mergers valued at $10 billion and above also hit new highs in the 1990s, eclipsing the size and incidence of very large deals from any previous decade (Figure 1.2). From the 1980s to the 1990s, these outsized deals increased over six-fold in inflation-adjusted frequency relative to

the mere doubling of billion-dollar deals. Examples of record-breaking M&A deals illustrate the

valuation disparity across the decades. In the largest transaction of the 1980s, LBO firm Kravis

Kohlberg Roberts acquired RJR Nabisco in a largely debt-financed deal valued at $24.6 billion

in 1988 ($37.4 billion in 2002 dollars); in the largest transaction of the 1990s, nominal acquirer

America Online combined with nominal target Time Warner in a stock-swap merger of equals

worth $165 billion in 2000 ($172 billion in 2002 dollars).

Behemoth deals not only increased more dramatically than the billion-dollar category

during the 1993 to 2000 wave, they also declined more precipitously in the 2001 to 2003

quiescence (Wall Street Journal 2001b; Financial Times 2003b). Specifically, U.S. combinations

valued at $10 billion and above rose over the course of the fifth wave from none in 1993 to 22 in

2000. Comparing the fourth and fifth waves, from 1980 to 1989 there were 12 such

combinations, while from 1993 to 2000 there were 75 total. Then the number of $10-billion U.S. deals fell to 15 in 2001, five in 2002, one in 2003, and nine in 2004. Unlike the billion-dollar category where the 2003 upturn preceded the 2004 general M&A revival, in the $1 0-billion

category the deal frequency tracked the trend of general merger activity. Large and very large M&A deals constitute the main part of the present research domain, as will be described further in this chapter. (Sources for data to determine inflation-adjusted merger numbers: SDC

Platinum, Mergerstat, and Consumer Price Index) Building on the work of economic historians who compare imperialism in nations and firms, I now turn to a quick overview of the

interweaving of political and economic factors in historic national expansion and modern M&A.

POLITICAL, ECONOMIC AND HISTORICAL CONTEXT

Politics in Organizations

Despite the differing characteristics of mergers of different time periods, within each wave are discerned political as well as economic factors at work. To further contextualize M&A activity, I draw on the observation of Long (1962: 110), who noted that although it is commonly understood that governments are organizations, it has been less widely perceived that

organizations are governments, too. March (1962) also emphasized that organizations are both economic and political conflict systems, and Cyert and March (1963) further depicted political processes and irrationality in managerial decision making in organizations.

Organizational and political issues converge in the study of mergers and acquisitions, as

national bids for expansion and conquest (Grossman and Mendoza 2002), and historic empire-building provides useful comparisons for understanding modem manifestations of M&A deals.

Though legally there are no distinctions among mergers, acquisitions and takeovers, in the M&A vernacular deals vary in label and form. These variations resemble nationalist expansion

strategies ranging from invasion and annexation to equitable combinations. I develop these ideas further with brief comparisons between notable empires and 1993-2000 U.S. M&A deals.

Takeovers

The ancient Greek Empire under Alexander the Great spread from Persia, India and Asia

Minor in the East through Greece and into Italy in the West (Kagan 2003). In the present

framework, this conquering of the Mediterranean world to expand the ancient Greek Empire epitomizes annexation comparable to the takeover style of M&A deals. Similarly, the Roman Empire under successive consuls ranged from Egypt in the South and East to Britain in the North and West, with conquered territories brought swiftly under a uniform system of administration.

The extension of Japan into neighboring Asian countries in the early twentieth century also demonstrated rapid and, as in all cases of empire building, occasionally ruthless expansionism.

In a still darker episode, Hitler adopted the excuse of lebensraum and allegedly sympathetic local

citizenries while directing Nazi Germany to invade Austria, Czechoslovakia and Poland at the brink of World War II (Shirer 1960). Annexation implies hostility, force, coercion and sometimes illicit means. Examples from the pre-millennial merger era are in the takeover of Warner-Lambert by Pfizer (under William Steere), of US West by Qwest (under Joseph Nacchio), or of MediaOne Group by AT&T (under Michael Armstrong).

Acquisitions

The acquisition approach, absent the overt and sustained hostility of the annexation method, recalls the nineteenth-century U.S. notion of Manifest Destiny and the growth strategy

exemplified by the Louisiana Purchase (1803) from France under Thomas Jefferson or the purchase of the Alaska Territory (1867) from Russia under Secretary of State William Seward

(and President Andrew Johnson). Similarly, Great Britain from the seventeenth to the nineteenth centuries, under monarchs ranging from Elizabeth I to George VI, built the largest territorial empire to date, using a combination of conquest and negotiation, with a dual drive to expand commerce and spread Christianity (Ferguson 2003). In the 1990s business realm, the repeated acquisitions of JDS Uniphase (under Jozef Straus), NationsBank (under Hugh McColl), and Bank One (under John McCoy) illustrate iterative negotiations and routinized postacquisition integration with coercion applied to the target firms as necessary.

Mergers

In modem times, the union of Austria and Hungary into the Austro-Hungarian Empire (1867-1918) ruled by the Habsburgs (Ford 1989) or the assemblage of countries in the growing European Union typify mergers of (relative) equals. Though the combining entities may not be

entirely equal in size or stature at the inception of the union, there is a striving for evenhanded

treatment of the partners under the terms of the deal. Likewise, the 1990s combinations of Bell Atlantic, NYNEX and GTE into Verizon (predominantly under Ivan Seidenberg), Travelers plus Citicorp into Citigroup (under John Reed and Sanford Weill), or Manufacturers' Hanover plus Chemical Bank plus Chase Manhattan plus JP Morgan into JP Morgan Chase (predominantly under Walter Shipley) demonstrate corporate mergers of equals. In many examples in the three types of national and corporate deals, the heads of state or chief executives became strongly identified with the transactions, an idea underlying my central thesis of CEO-merger

connections. To simplify descriptions throughout the dissertation (while capturing the ambiguity and lack of legal distinction in classifying M&A deals), I follow standard practice in using the terms merger and acquisition interchangeably, unless otherwise noted. I turn back to the present to address further the significance of large M&A transactions and the value of studying these deals. Apart from apt comparisons between nation-states and multinational companies, large intercorporate combinations are of interest for reasons related to investor capitalism, geopolitical influence, and management theory.

MODERN M&AACTIVITY:

THE IMPORTANCE OF LARGE DEALS

Benefits and Risks of Investor Capitalism

The importance of large M&A transactions arises in part from the ubiquitous presence of

corporations in daily life as seen in the rise of investor capitalism in the developed nations

(Useem 1993). The previous era of managerial capitalism vested wider latitude in the general power and decision making authority of chief executives and boards (Berle and Means 1932; Chandler 1977; Lorsch and MacIver 1989). Fewer individuals owned stock, inspected corporate governance provisions, or demanded executive accountability. Today, in evidence of increased nationwide affluence, institutional and individual investors electronically trade debt and equity positions in international capital markets. The growth of public and private pension plans coupled with prolonged periods of economic prosperity and rising stock prices has corresponded to more institutional shareholders on boards and more individual shareholders as activists regarding corporate investments and strategic directions (Crystal 1991; Bok 1993).

The shift to investor capitalism raised the contradiction of individuals wanting both job

jobs on the target side and shareholder value on the acquirer side. The downside of individual-level job loss, financial and emotional turmoil, and family upheaval rivals the upside of corporate cost savings, productivity improvement, and synergy creation. These concerns highlight class boundaries, creating alternately conflict and alliance between the corporate executives and professional investors of Wall Street and the amateur investors, bystanders, and workers of Main

Street. Complicating the picture, mergers lead to "easy street" for some (top executives with

golden parachutes or in-the-money options, lawyers and investment bankers reaping huge fees, successful arbitrageurs, and other lucky or skillful investors) and dead-end street for others (those demoralized or dismissed in the restructuring or who otherwise lack economic cushion).

Sustaining a Competitive Advantage in the Global Economy

In addition to the consequences of organizational strategies for investors, mergers have geopolitical significance for firms. Intercorporate combinations represent a means for growing rapidly in size and securing control of vital resources across national boundaries (Mueller 1969);

mega-mergers express political and strategic aims in the global economy and the global market

for corporate control (Vlasic and Stertz 2000). Large mergers between multinational corporations build continued competitive advantage for firms in a worldwide economy with increasingly porous boundaries (Schweiger and Goulet 2000). In addition, consolidation within industries becomes a strategic imperative in the context of winner-take-all product markets where the advantage is sometimes more to the nimble than the large, but where size facilitates technological prowess (Sen and Egelhoff 2000) and defends against predation in the takeover arena (Dymski 1999). As companies from various countries continue to profitably enter each other's markets., the worldwide diffusion of products and services sustains the viability of all

firms open to international economic exchange. In the tenets of neoclassical economics, the

market-ruled economy ultimately benefits most producers and consumers. The near-term consequences are often substantially harsher for many people, as previously noted.

Management Theory: The Leadership Factor

As described above, large mergers are a multi-level phenomenon with international and individual ramifications, and merging confers a competitive advantage on multinational

companies in the global economy. The sociological, strategic, and leadership relevance of mega-mergers supplements their financial and economic importance to individuals, firms and nations.

From a sociological perspective, large corporate unions affirm isomorphic outcomes and legitimacy aspirations in the combining organizations. According to institutionalism, certain firms (often those large and established) become models for other firms to mimic in an effort to attain legitimacy (DiMaggio and Powell 1983; Zucker 1987). Firms will undertake large