HD28 .M414

Ki'i^-B}

^<^%. »«s,,TsS;;--NOV

12

1987 «PrWORKING

PAPER

ALFRED

P.SLOAN SCHOOL

OF

MANAGEMENT

DETERMINISTIC CHAOS

INMODELS

OFHUMAN BEHAVIOR:

METHODOLOGICAL ISSUES AND EXPERIMENTAL RESULTS

JOHN

D.STERMAN

OCTOBER

1987WP 1945-87

MASSACHUSETTS

INSTITUTE

OF

TECHNOLOGY

50

MEMORIAL

DRIVE

CAMBRIDGE,

MASSACHUSETTS

02139

r

'^

DETERMINISTIC CHAOS

INMODELS

OFHUMAN BEHAVIOR:

METHODOLOGICAL ISSUES AND EXPERIMENTAL RESULTS

JOHN

D.STERMAN

D-3921

Deterministic

Chaos

inModels

of

Human

Behavior:

Methodological

Issues

and

Experimental

Results

John D.

Sterman

Associate Professor Sloan School ofManagement

Massachusetts Institute of

Technology

Cambridge,

MA

02139

Forthcoming

in theSpecial Issue

on

Instabilitiesand

Chaos

System

Dynamics

Review

D-3921

ABSTRACT

Recent

work

hasshown

that severalwell-known models

in the systemdynamics

literature contain previously unsuspected regimes ofdeterministic chaos.

Two

of themost

extensively analyzed are Sterman's

model

of theeconomic

longwave

and

theproduction-distribution

model

of theBeer

DistributionGame.

The

significance of these theoreticaldevelopments hinges

on

whether the chaotic regimes lie in the realistic region of parameterspace. Further there are

major

questions regarding the descriptive accuracy ofmodels

ofhuman

systemswhich

exhibit chaos. Data limitations and the inability to conduct controlledexperiments

mean

empirical studies at the aggregate level are not likely to resolve thesequestions.

An

alternative approach is basedon

laboratory experiments inwhich models

provide a simulated environmentfor the study of

human

decisionmaking behavior. Recentlylaboratory experiments have been conducted to analyze decisionmaking behavior in the long

wave

model

and theBeer

DistributionGame.

This paper describes the experiments andshows

that the behavior ofthe subjects is explained well with a simple heuristic long used insystem

dynamics modeling

and wellgrounded

in behavioral decision theory.The

parameters ofthe proposed decision rule are estimated econometrically for each subject.The

parameterswhich

characterize a significant minority of the subjects areshown

to produce chaos. Thisdirect experimental evidence thatchaos can be

produced by

the decisionmaking behavior ofrealpeople has important implications for the formulation, analysis,

and

testing ofmodels

ofD-3921

Recent

work

hasshown

that severalwell-known models

in the systemdynamics

literature contain previously unsuspected regimes of deterministic chaos.

The

work

ofDay

(1982a, 1982b) provides an earlyexample

of chaotic behavior ineconomic

models, whileMosekilde

and others (1987) have developed corporatemodels which

exhibit chaos.Two

ofthe

most

extensively analyzed suchmodels

are Sterman'smodel

oftheeconomic

longwave

(Sterman 1985, 1986,

Rasmussen,

Mosekilde,and Sterman

1985) and theproduction-distribution system or

Beer

DistributionGame

(Forrester 1961, Jarmain 1963,Sterman

1984,Mosekilde and

Larsen, this issue).While

the demonstration that chaos can beendogenously

produced

in these systems is an important theoretical development, the significance of theresults hinges in large

measure

on whether the chaotic regimes lie in the realistic region ofparameter space or

whether

they are mathematical curiosities never observed in the realsystem. Further there are

major

questions regarding the descriptive accuracy of the decisionrules postulated in the

models

ofhuman

systems developed to datewhich

contain strangeattractors.

The

practical significance of chaosand

otherphenomena

such as self-organizationin policy-oriented

modeling

remains unclear until it can be determined that thesephenomena

can occur inmodels

whose

decision rules aregrounded

in empirical study ofthe actualdecision processes of the agents. It is difficult if not impossible to resolve such issues

by

appeal to the aggregate empirical data. In the case of the long wave, for example, there

have

been at

most

fivelong-wave

cycles since the industrial revolution, toofew

for statisticallyreliable results.

Worse,

the data required are simply unavailable, andmuch

ofit is corruptedby

measurement

error (Chen, this issue).An

alternative approach is basedon

laboratory experiments inwhich models

provide asimulated

environment

for the study ofhuman

decisionmaking (Sterman 1987a). Recently,the long

wave

model and Beer

DistributionGame

(traditionally used as a teaching rather(Sterman 1987b, 1987c).

These

experimentswere

conducted primarily to study the heuristicswith

which

peoplemanage

acomplex dynamic

environment. In both experiments the decisiontask ofthe subject

was

tomanage

a stock in the face oflosses, delays in acquiringnew

units,multiple feedbacks

and

other environmental disturbances.This paper describes the experiments

and

shows

that decisionmaking behavior in thetwo

experiments is significantly suboptimal.The

departuresfrom

optimal behavior aresystematic, suggesting subjects use

common

heuristics for stockmanagment.

The

experiments

show

that the behavior of the subjects can bemodeled

well with a simplestock-management

heuristic long used in systemdynamics modeling and

wellgrounded

inbehavioral decision theory.

The

parameters of the proposed heuristic are estimatedeconometrically for each subject.

The

systems are then simulated with the estimated parameters.The

parameterswhich

characterize a significant minority of the subjects areshown

to produce chaos. This direct experimental evidence thatchaos can beproduced by

the decisionmaking behavior ofreal people has important implications for the formulation,

analysis, and testing of

models

ofhuman

behavior.The

Stock

Management

Problem

The

regulation ofa stock or system state is one of themost

common

dynamic

decisionmaking tasks.

The

manager

seeks to maintain a quantity at a target level, or at leastwithin an acceptable range. Stocks cannot be controlled directly but rather are influenced by

altering the stock's inflow

and

outflow rates. Typically amanager must

set the inflow rate soas to

compensate

for lossesfrom

the stock and to counteract environmental disturbanceswhich

may

push

the stockaway

from

its desired value. Frequently there are lagsbetween

the initiation ofa control action and its effect

on

the stock, and/or lagsbetween

a change inthe stock and the perception ofthat change

by

the decisionmaker.The

duration of these lagsmay

vary andmay

be influenced by the manager'sown

actions.D-3921

Stock

management

problems occur atmany

levels ofaggregationfrom

the micro to themacro.

At

the level ofa firm,managers

must

order partsand

raw

materials so as to maintaininventories sufficient for production to proceed at the desired rate, yet prevent costly

inventories

from

piling up.They must

adjust for variations in the usage and wastage of thesematerials

and

for changes in theirdelivery delays.At

the level ofthe individual, peopleregulate the temperature ofthe water in their

morning

shower, guide their carsdown

thehighway, and

manage

their checking account balances.At

themacroeconomic

level, theFederal Reserve seeks to

manage

the stock ofmoney

so as to provide sufficient credit foreconomic growth

while avoiding inflation and compensating for variations in creditdemand.

The

generic stockmanagement

controlproblem

may

be divided intotwo

parts: (i) thestock and flow structure ofthe system;

and

(ii) the decision rule usedby

themanager

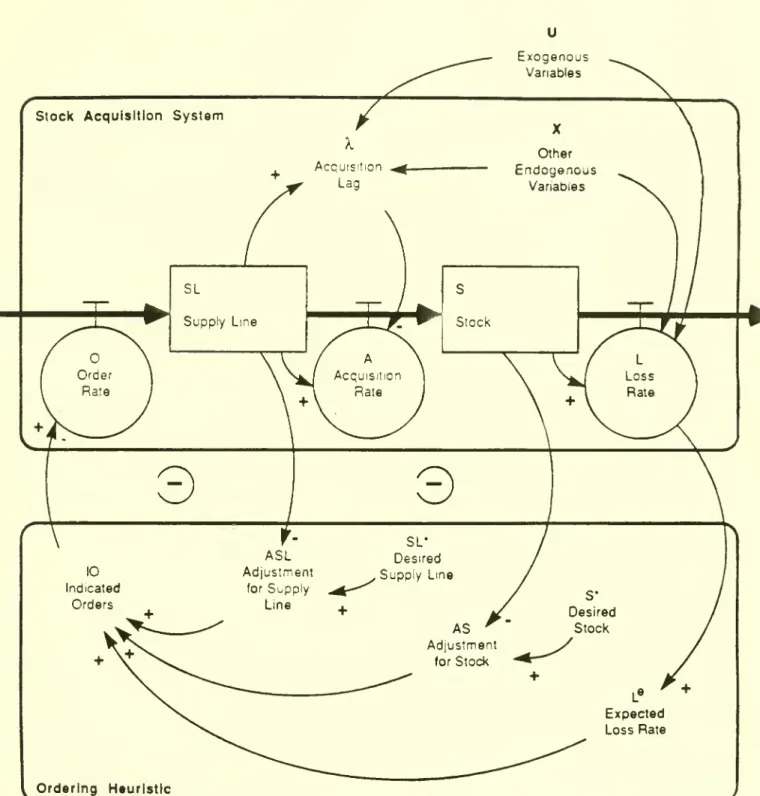

(figure1). Considering first the stock and flow structure, the stock of interest S is the accumulation

ofthe acquisition rate

A

less the loss rate L:Si=

I(A,-L^)dx+S,

' 'K

^ (1)Losses

from

the stockmust depend on

the stock itself,and

may

alsodepend on

otherendogenous

variablesX

andexogenous

variables U:Lt

=

fL(St,Xt,Ut). (2)The

acquisition rate willdepend on

the supply lineSL

ofunitswhich

have been ordered butnot yet received, and the average acquisition lag X. In general,

X may

be a function of thesupply line itself

and

the otherendogenous

andexogenous

variables:At

=fA(SLat).

(3)The

supply line is simply the accumulation ofthe orderswhich have

been placedO

less thosewhich have

been delivered:SL,=

I(O,-

A,)dx+SL,

The

structure represented by figure 1 and eq. (1-4) is quite general. There isno

presumptionthat the functions governing losses

and

the acquisition lag are linear. Theremay

bearbitrarily

complex

feedbacksamong

theendogenous

variables,and

the systemmay

beinfluenced by

numerous exogenous

forces including noise and nonstationarity oftheunderlyingequilibrium.

Consistent with the behavioral foundations of system

dynamics modeling

(Morecroft1983, 1985,

Sterman

1987a), behavioral decision theory (Hogarth 1987,Tversky

andKahneman

1974), and the theory ofbounded

rationality(Simon

1979, Cyert andMarch

1963),the proposed decision rule utilizes information locally available to the decisionmaker and does

not

presume

themanager

has globalknowledge

of the structure of the system.The

genericdecision rule recognizes three motives for ordering

which

any stockmanagement

heuristicmust

include:Order

enough

to (1) replace expected lossesfrom

the stock, (2) reduce thediscrepancy

between

the desiredand

actual stock,and

(3) maintain an adequate.supply line ofunfilled orders.

1.

Replacement

oflosses.The

replacement motive is straightforward. In equilibrium,when

the desiredand

actual stock are equal, themanager must

continue to orderenough

toreplace

ongoing

losses. Lossesmay

arisefrom

usage (e.g. shipmentsfrom

an inventory offinished goods) or decay (e.g. the depreciation of plant

and

equipment). Failure to replacelosses

would

cause the stock to fallbelow

the desired level, creating steady-state error.2. Stock adjustment. Errors in forecasting losses or changes in the desired stock

demand

amechanism

to adjust ordersabove

orbelow

replacement. Orders to reduce thediscrepancy

between

thedesired and actual stockform

a negative feedback loopwhich

regulates the stock

(shown

in thebottom

part of figure 1).Any

rulewhich

fails tocompensate

for discrepanciesbetween

the desired and actual stock fails to control the stockD-3921

the desired value ifdisplaced.

The

stockwould

follow arandom

walk

as the system isbombarded

by shocks.3. Supply line adjustment. Delays

between

the initiation and impact ofcontrol actionsgive stock

management

systems significant inertiaand

should be accounted forby managers

to ensure a stable response to shocks. Failure to account for the supply line results in

overcorrection and instability. Consider cooking dinner on an electric range. Ifone turns the

heat

down

just as thepotcomes

to a boil the supply line ofheat in the coils of the range willcontinue to heatthe pot, boiling it overand ruining dinner.

The

following equations formalize the ordering heuristicproposed

above. First, ordersin

most

real life situationsmust

be nonnegative,Ot

=MAX(0,IOt)

(5)where

10

is the indicated order rate, the rate indicated by other pressures. ^The

indicated order rate is basedon

the anchoringand

adjustment heuristic (Tverskyand

Kahneman

1974).Anchoring and

adjustmentis acommon

judgmental strategy inwhich

an

unknown

quantity is estimated by first recalling aknown

reference point (the anchor)and

then adjusting for the effects of other factors

which

may

be less salient orwhose

effects areobscure.

Anchoring and

adjustment has beenshown

to apply to awide

variety ofdecisionmaking tasks

(Einhom

and Hogarth

1985, Davis,Hoch,

and Ragsdale 1986,Johnson

and

Schkade

1987,Lopes

1981, Hines 1987,Sterman 1987dX

Here

the anchor is theexpected loss rate L^. Adjustments are then

made

in response to discrepanciesbetween

thedesired and actual stock

AS

andbetween

the desired and actual supply lineASL:

lOt = L^t +

ASt

+ ASLt. (6)The

expected loss ratemay

beformed

in various ways.Common

assumptions inequilibrium value), regressive expectations L^t= yLt-l + (l-Y)L*, 0<y<l, adaptive

expectations

L«t=

6Lt-i+

(l-6)L^t-l,0<9<1, and

extrapolative expectations, AL^t =lcoi*ALt-i,

where

A

is the first-difference operatorand

coi>0.The

adjustment for the stockAS

creates the chiefnegative feedback loopwhich

regulates the stock.

The

proposed

heuristicassumes

for simplicity that the adjustment islinear in the discrepancy

between

the desired stockS*

and the actual stock:ASt

=

as(S*t-St)

(7)where

the stock adjustment parameteras

is the fraction ofthe discrepancy ordered eachperiod.

The

adjustment for the supply line is formulated analogously asASLt

=

asL(SL*t-

SLt) (8)where

SL*

is the desired supply lineand asL

is the fractional adjustment rate for the supplyline.

The

desired supply line in general isnot constant butdepends

on

the desired throughputO*

and the expected lagbetween

ordering and acquisition of goods:SL*t =

Xh*0*t.

(9)The

adjustment for the supply line creates a second negative feedback loopwhich

avoids overorderingand

alsocompensates

for changes in the acquisition lag X. IfX

rises, forexample,

ASL

induces sufficient additional orders to restoreA=0*.

There

are a varier>' ofpossible representations for X^ and

O*,

rangingfrom

constants through sophisticatedforecasts.

Experiment

I:The

Economic

Long

Wave

The

experimental protocol for the longwave

model

is described inSterman

andMeadows

1985 andSterman

1987a, 1987b).The

methodological foundations of experimentaleconomics

are discussed in the seminalwork

of Smith (1982) and Plott (1986).The model

D-3921

hypothesis behind the long

wave

can be stated intwo

parts. First,due

to construction lags,the process by

which

individual firms adjust production capacity todemand

is inherentlyoscillatory. In isolation an individual firm

would

producedamped

fluctuations with aperiod ofabout 15-25 years in response to a shock. Second, in the aggregate the capital-producing

sector of the

economy

orders and acquires capitalfrom

itself. This multiplier effect or'self-ordering' creates a positive feedback loop

which

destabilizes the oscillatory tendencies ofindividual firms, changing the

damped

oscillation to a limit cycle with a40-60

yearperiod.Simulation

and

formal analysis confirm thedynamic

hypothesis (Sterman 1985;Rasmussen,

Mosekilde

andSterman

1985).As

the self-ordering loopbecomes

stronger,damping

dropsrapidly.

The

system goes through aHopf

bifurcation and produces a limit cycle. Furtherincreases in the strength of self-ordering proceed through period doublings and ultimately to

chaos.

In the experiment the

model

is transformed into agame

inwhich

subjectsmanage

thecapital-producing sector of a simple

economy.

Subjectsmust

balance the supply ofand

demand

for capitalby

adjusting their production capacity tomeet

desired production. Ordersfor capital arise

from

theexogenous

consumer goods

sector andfrom

the subject'sown

orders.

The

equations underlying thegame

reflect a simplifiedform

ofthe originalmodel

butpreserve its essential structure

and

dynamics. In thegame

decisions aremade

in discretetime intervals representing

two

years, and themodel

becomes

a third-order differenceequation system.

The

equations ofthegame

are given below. ProductionPR

is the lesser ofdesiredproduction

DP

orProduction Capacity PC. Capacity is proportional to the capital stock.The

capital/output ratiok

isone

period (two years):PRt

=

MIN(DPt,PCt)

(10)The

capital stock ofthe capital sector isaugmented by

acquisitionsAK

and diminished bydepreciation

CD.

Depreciation is proportional to the stock.The

average lifetime ofthecapital stock x is 10 periods (20 years):

Kt+i

= Kt + (AKt-CDt)

(12)CDt

=

Kt/t. (13)The

acquisition ofcapital by both the capital andgoods

sectors(AK

and

AG)

dependson

thesupply line ofunfilled orders each has accumulated (the backlogs

BK

andBG)

and

the fractionof

demand

satisfiedFDS.

Each

period both the capitaland goods

sectors acquire the fullsupply line of unfilled orders unless the capital sector is unable to produce the required

amount. In this case acquisition

by

each sector is reduced in proportion to the shortfall.The

acquisition lag

X

is thus 1/FDS,and

AK+AG=PR

at all times, ensuring that output isconserved:

AKt

=

BKt*FDSt

(14)AGt

=

BGt*FDSt

(15)FDSt

= PRt/DPt

(16)DPt

=

BGt

+

BKt. (17)The

supply lines of unfilled orders foreach sectorBG

and

BK

areaugmented

by orders forcapital placed by each sector

and

emptiedwhen

those orders are delivered:BKt+i

=

BKt

+(OKt

-AKt)

(18)BGt+i

=BGt

+ (OGt-AGt).

(19)New

orders placedby

thegoods

sector are theexogenous

input to the system towhich

thesubject ofthe experiment

must

respondby

choosing an appropriateamount

ofcapital to orderfor their

own

use:OGi

= exogenous

(20)OKt

=

determinedby

subject. (21)D-3921

9of the subjects in

making

these decisions is to minimize their total score for the trial.The

score is defined as the average absolute deviation

between

desired productionDP

and production capacityPC

over theT

periods of the experiment:T

S

=

(1/T)S

I

DPt

-

PCt

|. (22)t=0

The

score indicateshow

well subjects balancedemand

and supply. Subjects are penalized equally for both excessdemand

and

excess supply.The

experiment isimplemented on

IBM

PC-type

microcomputers.A

'gameboard' isdisplayed

on

the screen providing subjects with perfect information. Color graphics andanimation highlight the flows oforders, production, and shipments to increase the

transparency ofthe structure.

The

conversion ofthe originalmodel

to aform

suitable forexperimental testing is described in

Sterman

1987a.The

subject population(N=49)

consisted ofMIT

undergraduate, master's and doctoral students inmanagement

and

engineering,many

with extensive exposure toeconomics

andcontro^ theory; scientists and economists

from

various institutions in theUS,

Europe, and theSoviet Union; and business executives experienced in capital investment decisions including

several

company

presidents andCEOs.

Typical experimental results are

shown

in figure 3. All trials begin in equilibrium. Inperiod 3 there is a one-time step inputof

10%

in the orders ofthegoods

sector.The

optimalresponsereturns the system toequilibrium within 6 periods, producing a score of 19. In

contrast the vast majority ofsubjects

produced

significant oscillations (table 1).The

averagescore for the

sample

was

591; the lowestwas

77.Next

theproposed

stockmanagement

heuristic (equations 5-9)was

tested againstthe ordering behavior of the subjects. Adapting the heuristic to the experimental context is

proportional to desired production.

The

loss rateL

is simply the depreciation ofthe capitalstock

CD. The

desired supply lineDSL

was

specified according to equation 9, with theexpected acquisition lag X^

=X=

1/FDS

and desired throughput0*=

CD.

Allowing

anadditive disturbance term E, the proposed ordering rule for capital investment

becomes:

OKt

=MAX(0,CDt

+ASt +

ASLt

+ Et) (23)ASt

=

as(DKt-Kt)

(24)ASLt

=

asUDSLt

-BGt)

(25)DSLt

=

?.e*CDt=

(l/FDSt)*CDt.'

(26)

To

test the rule only thetwo

adjustment parametersas

andasL

need

be estimated. All otherdata required to determine orders are presented directly to the subjects.

Maximum

likelihood estimates of the parameters for each trialwere

found by grid search of the parameter space,subject to the constraints as,

asL

^0.Assuming

the errors £ are independent, identical, andnormally distributed then the

maximum

likelihood estimates of such nonlinear functions aregiven

by

the parameterswhich minimize

thesum

of squared errors.Such

estimates areconsistent

and

asymptotically efficient, and the usual measures of significance such as thet-test are asymptotically valid.

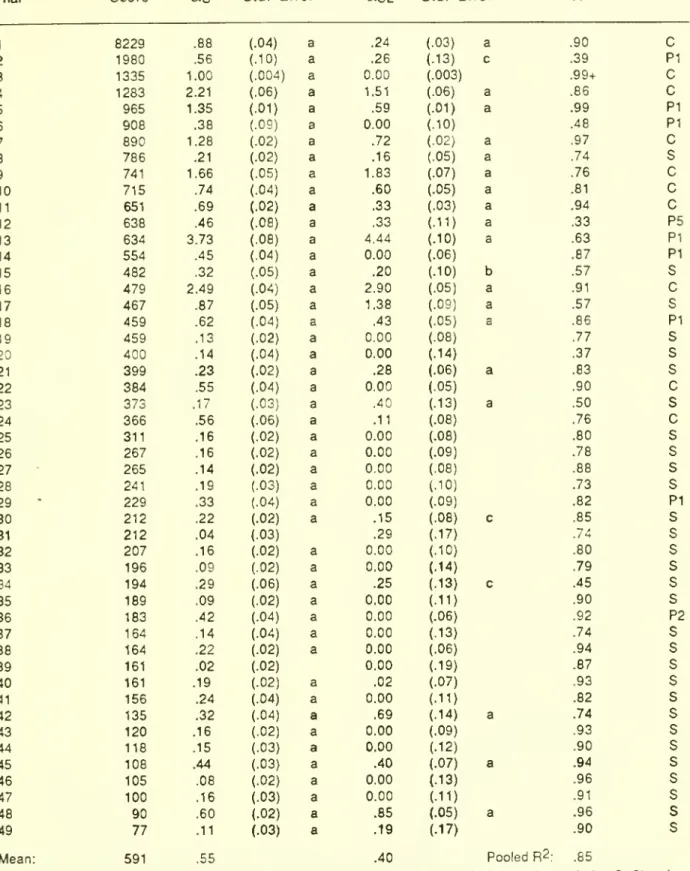

Estimates for

49

trials together with t-statistics are given in table 2.The

model'sability to explain the ordering decisions ofthe subjects is excellent.

R2

variesbetween

33%

and99+%,

with an overallR^

for the pooledsample

of85%.2

All buttwo

ofthe estimatedcapital stock adjustment parameters are highly significant.

The

supply line adjustmentparameter is significant in 22 trials.

Sterman 1987b

analyzes the estimation results and identifies several 'misperceptionsof feedback'

which

are responsible for the subjects'poor performance.One

ofthese is theD-3921

11continue ordering even after the construction pipeline contains sufficient units to correct any

stock discrepancy.

The

present concern, however, is the relationshipbetween

the estimatedparameters and the regimes of behavior in the model.

The

estimated parameters characterizethe decision

making

behavior of actual people.When

simulated in themodel

are theestimated decisoin rules ofthe subjects inherently stable, or

do

theyproduce

limit cycles,period multiples, or chaos?

Table 2 also indicates the

mode

of behavior produced by simulation ofthe decision rulewith the estimated parameters.

The

parameters estimated for thirty subjects(61%)

arestable.

Most

of these produceoverdamped

behavior of the capital stock in response to thestep input.

Seven

parameter sets produce limit cycles of period 1, and 2 produce periodmultiples.

The

parameterswhich

characterize ten subjects(20%)

produce chaos. Inspectionof table 2

shows

that the subjectswhose

parameters are stableperformed

best in the taskwhile those

whose

parameters produce limit cycles and chaos generallyhad

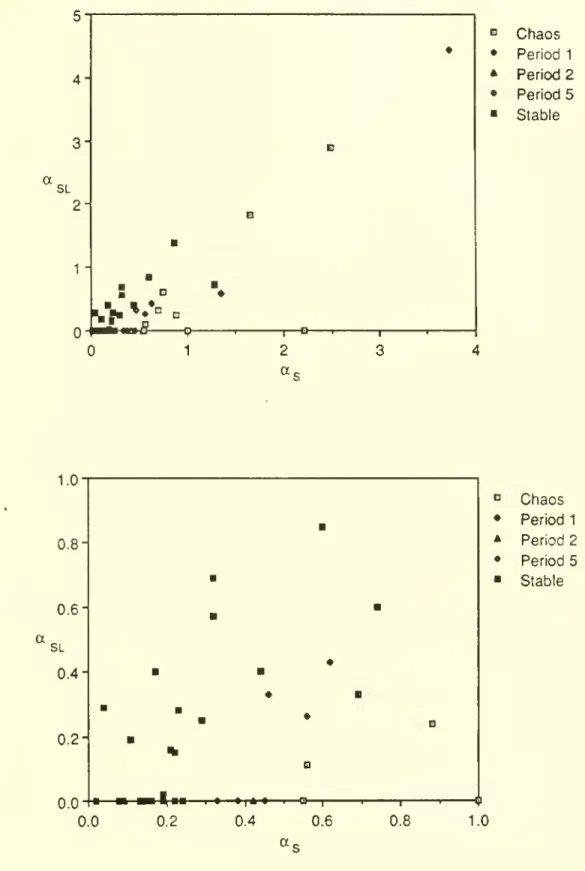

the highest scores.Figure 4

shows

the phase portrait for several of themore

interesting parameter sets.Note

the period 5 cycleproduced

by (as, asL)=

(.46, .33).The

apparent period 2 cycleproduced

by (.42, 0) is,upon

closer inspection, seen tobe chaotic.Figure 5 locates the

modes

of behavior in parameter space. Consistent with bothintuition

and

formal stability analysis, stability isenhanced

by small values ofas

and largevalues of asL.

More

aggressive attempts to correct the discrepancybetween

the desired andactual capital stock are destabilizing: by ordering

more

aggressively the self-ordering loopcauses a larger increase in total

demand,

thus exacerbating disequilibrium and encouragingstill larger orders in future periods. Conversely,

more

aggressive response to the supply lineThus

the periodic and chaotic attractors tend to occur for large values ofas

and smallvalues ofasL- Yet the route to chaos is apparently

more

complex. Consider the route tochaos as

as

increases for asL=0. Stability givesway

to periodone

limit cycles, then to period2 at (.42, 0), and ultimately to chaos for

as

^.55.Yet

the parameterswhich

produce theslightly chaotic period 2 are surrounded

on

the rayasL

=

by parameterswhich

produceperiod 1 limitcycles. Similarly, the period 5 attractor

produced

by the parameters (.46, .33)lies

between

the region ofstability and the region ofperiod 1 behavior.The

resultsshow

that the parameterswhich

characterize actual decisionmakingperformance in a

common

and importantmacroeconomic

situation canproduce awide

range of behavior, including chaos.Experiment

II:The

Production-DistributionSystem

The

"Beer DistributionGame"

is a role-playing simulation ofan industrial productionand

distribution system developed atMIT

to introduce students ofmanagement

to theconcepts of

economic dynamics and computer

simulation. In use forneariy three decades, thegame

has been played all over the worid by thousands of people rangingfrom

high schoolstudentsto chief executive officers

and government

officials.The

game

is playedon

a boardwhich

portrays in a simplified fashion the productionand

distribution of beer (figure 6). Orders for and cases of beer are representedby

markersand

pennieswhich

are physically manipulatedby

the players as thegame

proceeds.Each

brewery

consists of four sectors: retailer, wholesaler, distributor,and

factory (R,W,

D, F).One

personmanages

each sector.Customer

demand

is representedon

adeck

of cards.Customers

demand

beerfrom

the retailer,who

ships the beer requested out of inventory.The

retailer in turn orders beer

from

the wholesaler,who

ships the beer requested out oftheD-3921

13distributor,

who

in turn orders and receives beerfrom

the factor^'.The

factory produces thebeer.

At

each stage there are shipping delays and order receiving delays.These

representthe time required to receive, process, ship, and deliver orders, and as will be seen play a

crucial role in the dynamics.

The

subjects' objective is tominimize

cumulativeteam

costs over the length ofthegame.

Inventory holding costs for each sector are $.50 per case perweek,

and stockout costs(costs for having a backlog of unfilled orders) are $1.00 per case perweek.

The

decision task of each subject is a clearexample

ofthe stockmanagement

problem. Subjects

must keep

their inventory aslow

as possible while avoiding backlogs andsatisfying customer

demand.

Inventory cannot be controlled directly butmust

be ordered.The

lag in receiving beer is potentially variable: ifthe wholesaler has beer sufficient to coverthe retailer's orders the retailer will receive the beer desired afterthree weeks.

But

if thewholesaler has run out, the retailer

must

wait until the wholesaler can receive additional beerfrom

the distributor.Only

the factory, theprimary producer, faces a constant delay inacquiring inventory (there is

no

limit to the production capacity ofthe factory).The

protocol forthe experiment is described inSterman

1987c.The

game

is initializedin equilibrium.

Each

inventory contains 12 cases.Customer

demand

is initially four cases perweek.

To

disturb the system customerdemand

increases to eight cases perweek

inweek

5and

remains at that level thereafter.The

results reported herewere

drawn from

fourdozen

games

(192 subjects) collectedover a period offouryears.

A

computer model

ofthegame

was

used to test the records forconsistency. Trials in

which

therewere

accounting errors ofmore

than afew

cases perweek

for

more

than afew weeks

in any of the four sectorswere

discardedfrom

further analysis.Eleven

games

were

retained, providing44

subjects.^That sample

consists ofundergraduate,MBA,

and

Ph.D. students atMIT's

Sloan School ofManagement,

executivesfrom

a variety offirms participating in short courses on

computer

simulation,and

senior executives of amajor

computer

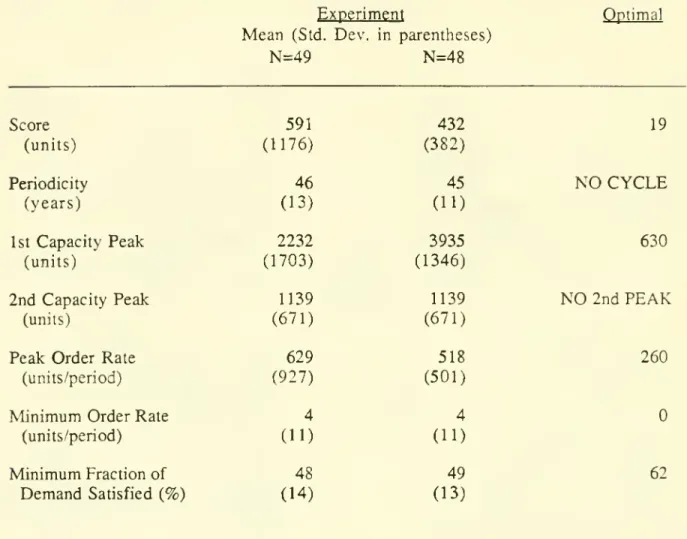

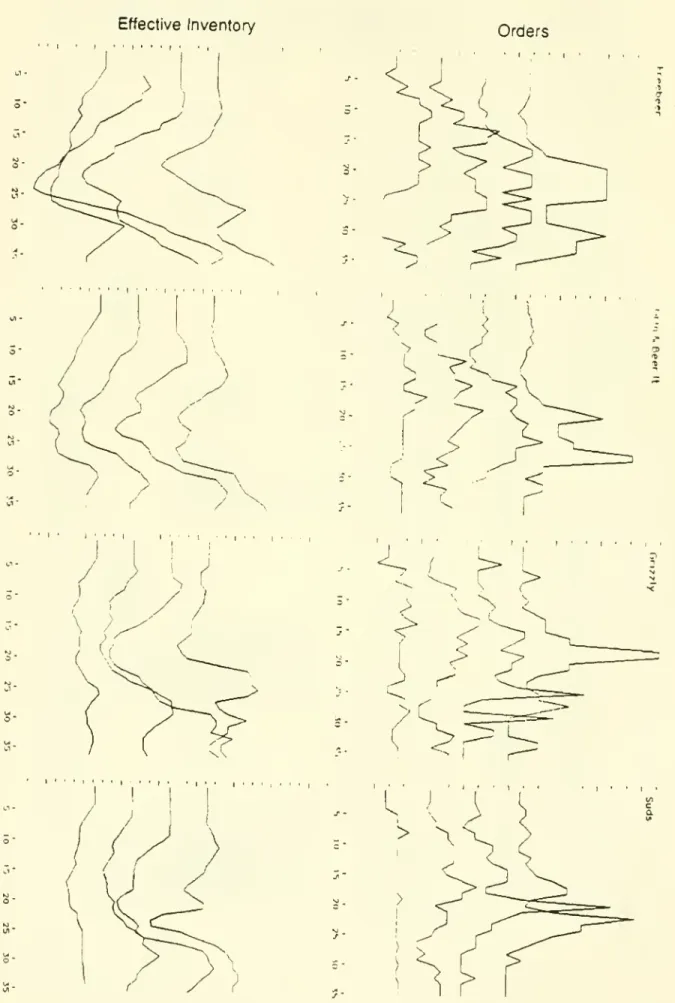

firm.Typical experimental results are

shown

in figure 7and summarized

in table 3.The

results

show

the behavior of the subjects to be farfrom

optimal.The

averageteam

cost isten times greater than optimal. Like the

macroeconomic

experiment, the results exhibitseveral strong regularities.

1. Oscillation:

The

trials are allcharacterizedby

instability and oscillation.The

pattern oforders and ofinventory is

dominated

by a large amplitudefluctuation with anaverage period of 21 weeks.

2. Amplification:

The

amplitude and variance of orders increases steadily as onemoves

from

customerto retailer to factory.The

peak

order rate at the factory level ison

averagemore

than double thepeak

order rate generated at the retail level.Customer

orders increasefrom

4 to 8 cases perweek.By

the time the disturbance has propagated to thefactor)', the order rate averages a

peak

of32 cases.3.

Phase

lag:The

peak

order rate tends to occur later asone

moves

from

the retailerto the factory.

The

phase lag is not surprising since the disturbance in customer ordersmust

propagate through decisionmaking and order delays

from

retailer to wholesaler and so on.Next

the proposed decision rulemust

be adapted to the particular situation in the beergame

and

cast in aform

suitable for estimation ofthe parameters.The

stockS

correspondsto the inventory of the subject

and

the supply lineSL

to thesum

of orders in the mail delays,the backlog ofthe subject's supplier (ifany), and the beer in the shipping delays.

The

lossrate is the rate at

which

each subject receives orders.To

test the rule it is necessary tospecify expected losses L^, the desired stock S*, and the desired supply line SL*.

Expected

lossesfrom

the stock are the rate atwhich

each subject expects theirD-3921

15the factory's forecast of the distributor's order rate, etc. Adaptive expectations are

postulated. Adaptive expectations are widely used in simulation

modeling

of corporateand

economic

systems, they are often agood model

of the evolution of expectations in theaggregate (Sterman 1987d, Frankel

and

Froot 1987),and

they areone

of the simplestformulations for expectations flexible

enough

to adapt to a nonstationary process.Because

the subjects lack the information and time to determine optimal inventory orsupply line levels

the desired stock

S* and

desired supply lineSL*

are bothassumed

to be constantswhich

must

be estimated.The

generic decision rule ofeq. (5-9) thus becomes:Ot

=

MAX(0,IOt)

(27)IOt=Let

+ ASt +

ASLt

(28)Let

=

eLt-l + (l-e)Lei.i.0<e<l

(29)ASt

=as(S*

- St) (30)ASLt

=asL(SL*

- SLt). (31)Defining P

=

asUct-s and S'= S* +

PSL*

yieldslOt

=Let

+

as(S'-St-pSLt).

(32)Note

that since S*, SL*,asL

and

as

are all >0, S'>0. Further, it is unlikely that subjects willplace

more

emphasison

the supply line thanon

the inventor)' itself: the supply line does notdirectly enter the cost function nor is it as salient as inventory. Therefore it is probable that

asLS

as,meaning

0<(3<1.Thus

(3 can be interpreted as the fraction of the supply line takeninto account

by

the subjects. IfP =

1, then the subjects fully recognize the supply line anddo

notdouble order. If P

=

0, then orders placed are forgotten until they arrive, encouragingoverordering

and

instabilitj.'^implemented

in the beergame

contains four parameters to be estimated (6, as, S', and p).The

parameterswere

estimated by thesame

procedure used in the longwave

experiment.An

additive disturbance term is assumed, and the disturbances areassumed

to be i.i.d.normal. Estimates for each sectorofeach trial

were

foundby

grid search of the parameterspace subject to the constraints

0<6<1

and

as, S', p >0.5The

estimated parameters are displayed in table 4.The

mean

R2

is71%;

R^

is lessthan

50%

foronly 6 of44

subjects.^A

large majority of the estimated parameters aresignificant.

As

in thelongwave

experiment the decision rule is an excellentmodel

of thedecisionmaking behavior ofthe subjects.

Sterman

1987c relates the estimated parameters tothe dysfunctional performance in the task. It is noteworthy that the

same

misperceptions offeedback structure

which

cause oscillation in themacroeconomic

experiment are responsiblefor thepoorperformance ofthe subjects in the beergame. Specifically, the supply line of

unfilled orders is given far too little weight by

most

subjects.Next

the beergame

was

simulated using the stock adjustment rule with theestimated parameters.

Each

trial involves four subjects, each ofwhom

could have differentparameters. In the simulations, however, the

same

parameterswere

assumed

for eachsector, vastly simplifying the analysis.*^

Table 4 indicates the

mode

of behaviorproduced by

each set ofparameters.Thirty-one parameter sets

(70%)

produce stable behavior.One

each produces limit cycles ofperiod1, period 5, and period 12.

Ten

yield chaos. Since the beergame

is a 19th order system thebehavior

produced

by the system is exceedinglycomplex

and there aremany

possibleprojections of phase space. Figure 8

shows

several of themore

interesting phase portraits.D-3921

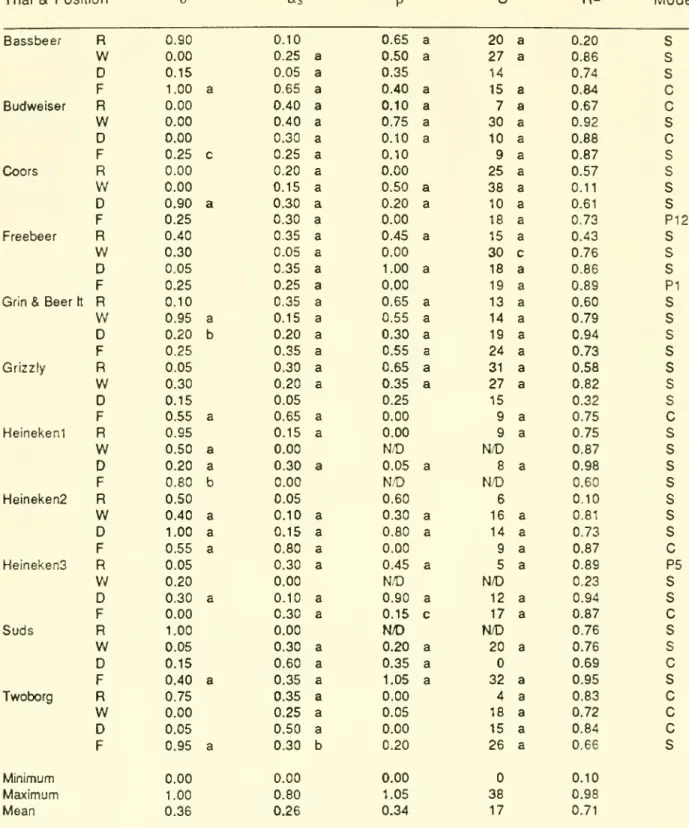

17parameters of the Bassbeer Factory (9, as, P, S' = 1, .65, .40, 15)

compared

to those of theHeinekenS

Factory (9, as, P, S'=

0, .3, .15, 17).The

parameters estimated for theCoors

Factory (9, as, p, S' = .25, .3, 0, 18) reveal a cycle ofperiod 12

when

distributorinventory isplotted against factory inventory.

The

retail sector ofthesame

team, however, produces alimit cycleofperiod 1.

The

difference inmode

is probably due to the integer constrainton

orders.

Figure 9

shows

the distribution ofthemodes

in parameter space.The

relationshipsbetween

the adjustment parametersand

stability are similar to those apparent in themacroeconomic

experiment,and

for similar reasons. In general, larger values ofas

andsmaller values of P are destabilizing. That is, to the extent the subjects ignore the supply

line of unfilled orders (P=0) a stock discrepancy will cause orders to be placed each period

even after sufficient orders are in the supply line, leading to excess inventories and

oscillation.

Such

overordering is exacerbated bymore

aggressive stock adjustment(as>>0)

since

more

will be ordered in response to a given discrepancybetween

the desiredand

actualstock. Figure 9 also indicates that in general the smaller the desired inventory S' the less

stable the system. Again, intuition readily explains

why

this is so. Consider the response ofthe retailer to an unanticipated increase in customer

demand.

Retail inventory fallsdue

to thelags in receiving beer.

The

retailer will place additional orders with the wholesaler throughthe stock adjustment term. Ifthe wholesaler has adequate inventory to fill

incoming

orders(S'»0)

incoming

orders can all be filled and the retailer's acquisition lag remains constant.If, however, the wholesaler runs out ofinventory the retailer finds orders placed fail to arrive.

The

delay in receiving beer lengthens, the retailer's stock drops still further,and

stillmore

orders swell the supply line in a vain attempt to replenish inventory.

When

sufficient beer(figure 7). S' plays such a crucial role in determining the stability of the system because it

determines

how

close the system operates to the fundamental nonlinear contraint thatshipments can only be

made

if inventor)' exists. Small values ofS'make

itmore

likely thesystem will run out ofinventory thus entering the unstableregion in

which

the acquisition lagX

is longand

variable.Those

subjectswho

maintained larger target inventory levelswere

thus

more

stableon

average than thosewho

attempted to cut costsby

reducing their bufferstock.

There

appears to beno

simple relationshipbetween

the parameter 6and

themodes

ofthe system. 6 controls the speed with

which

the adaptive forecast ofincoming

orders isadjusted and has

two

opposing effectson

stability. Faster adjustment of thedemand

forecast(9=1) increases the gain

between

orders placed andincoming

orders.Shocks

are transmittedup

the distribution chainmore

readily, destabilizing the systemby

causing larger inventoryexcursions upstream in response to a given

change

in ordersdownstream.

On

the other hand, sluggish adjustment (0=0)means

variations inincoming

orders are not quicklycountered by the replacement term ofthe ordering rule, causing inventory to decline further

than it

would

ifreplacement ofincoming

orderswas

swift.As

a result, inventoriesmay

beexhausted,

moving

the system into the less stable zone inwhich

backlogs buildup

and theacquisition lag lengthens.

As

in themacroeconomic

experiment the resultsshow

an unexpectedly rich array ofbehavior is generated

by

the interaction ofthe decision processes ofreal people with thefeedback structure of the environment.

Discussion

The

discovery of nonlinearphenomena

such as deterministic chaos in the physicalworld naturally motivates the search for similarbehavior in the world of

human

behavior. YetD-3921

19not to the

same

degree. Aggregate data sufficient for strong empirical tests simplydo

notexist for

many

of themost

important social systems. Social systems are not easily isolatedfrom

the environment.The huge

temporal and spatial scales ofthese systems, vastnumber

ofindividual actors, considerations ofcost

and

ethical concernsmake

controlled experimentson

the systems themselves difficult at best. Finally, the laws ofhuman

behavior are not asstable as the laws of physics.

The

social scientist is thus left withtwo main

options in the quest to understand therelevance ofnonlinear

phenomena

in thedomain

ofhuman

behavior.Formal models

of socialsystems

may

be constructed and analyzed. Previouswork

ofthis type has demonstrated theexistence of chaotic

modes

in awide

array of social andeconomic

models.However,

analysisofthese

models

frequentlyshowed

that the chaotic regime lay far outside the plausible regionofparameter space.

Worse,

without empirical tests ofthe decision rules the verisimilitude ofthe

models

was open

to doubt. In the absence of empirical data the relevance of nonlinearphenomena

remained

questionable.The

second

approach is to develop laboratory experiments with simulated socialsystems. Since experiments

on

actual firmsand

nationaleconomies

are infeasible, simulationmodels

of these systemsmust

be used to explore the decisionmaking heuristics ofrealpeople.

Such

experiments create 'microworlds' inwhich

the subjects face physical andinstitutional structures, information, and incentives

which

mimic

(albeit in a simplifiedfashion) those of the real world.

The

experiments described here presented subjects with a straightforwardstock-adjustment task. Results

show

that the subjects' behavior can bemodeled

with a highdegree of accuracy by a decision rulelong used in system

dynamics

models.The

decision ruleis consistent with a vast

body

of empiricalknowledge

developed in behavioral decisionbe robust: the feedback structure, information available, loss function, time available, "cover

story"

and

many

other dimensions of the experimental environment differed markedly.Performance in both settings

was

decidedly suboptimal.The same

misperceptions of thefeedback structure of the

system

are apparent in both cases.The

experiments reported here demonstrate that chaos can in fact beproduced

by thedecisionmaking processes of real people.

The

results are significant in several respects.The

demonstration that chaos can beproduced by

the decisionmaking heuristics people actuallyuse strengthens the

argument

for the universality of thesephenomena.

Chaos

thus appearsto be a

common

mode

of behaviornot only in physical systems butin socialand economic

systems as well.These

resultsdo

notshow

that, say, the evolution ofGNP

in the UnitedStates has in fact been chaotic. Further empirical

work

is required before such questions canbe settled.

But

the results suggest modelers can ignore nonlineardynamics

only at theirperil.

Models

ofeconomic and

socialdynamics

should portray the processesby which

disequilibrium conditions are created

and

dissipated, notassume

that theeconomy

is in ornear equilibrium at all times or that adjustment processes are stable.

Models

should beformulated so that they are robust in extreme conditions, since it is the nonlinearities

necessarily introduced by robust formulations that crucially determine the

modes

of thesystem.

These

principleshave

long been central to systemdynamics

(Forrester 1961,Forrester and

Senge

1980, Richardsonand

Pugh

1981)and

behavioraleconomics

(Da)' 1984) and are important even for systemswhich

do

not contain limitcycles or strange attractors(Sterman 1985b).

At

thesame

time anumber

ofquestions regarding the practical significance ofchaos and other nonlinearphenomena

in social systemmodeling

remain unresolved. Real socialsystems are

bombarded

bybroadband

noise, and it is wellknown

that suchrandom

shocksD-3921

21the existence of stochastic shocks

swamp

the uncertainty in trajectories caused by chaos?How

does the existence of chaotic regimes in amodel

influence its response to policies, andthe predictability of that response? Particularly troubling here is the apparent nonuniformity

of the distribution of

modes

in parameter space.Mosekilde and

Larsen's (this issue) carpetbombing

experiments with the simulated beergame show

that there are islands of chaos inparameter space,

and

that theboundary between

the periodicand

chaotic solutions is fractal,a finding consistent with analysis of such classic systems as Buffing's equation

(Thompson

and Stewart 1986).

The

response of stability to parameter variationsmay

not bemonotonic

or

even

predictable in such systems, raisingmajor

questions for policy analysis.The

dev-elopment

ofprinciples forpolicy design in such systems is amajor

area for future research.Similarly, chaos is a steady-state

phenomenon

which

manifests over very long timeframes, but

many

policy-orientedmodels

are concerned with transientdynamics

and nearlyall with time horizons

much

shorter than those used in the analysis ofchaoticdynamics

(e.g.Mosekilde

et al. 1986, Weidlich et al. this issue).Over

such extended time horizons theparameters ofthe system cannot be considered static but will themselves evolve with

learning

and

evolutionary pressures.How

does learning influence chaotic systems?The

macroeconomic and

corporate experiments described here, forexample,show

the behavior ofsystems simulated for thousands of years and weeks, respectively.

The

parameters of thedecision functions remain constant throughout.

Yet

there is evidence (Sterman 1987b,Bakken

1987) that subjects begin to learn withinjust afew

cycles, modifying the parametersoftheir ordering function. In the

macroeconomic

experiment, at least, learningmoves

thesubjects

away

from

the chaotic region intothe region ofstability.The

practical significance ofchaos and other nonlinear

phenomena

in policy-orientedmodels

of social andeconomic

behavior remains clouded while these questions are unanswered.human

behavior to experimental test.Many

models

ofhuman

systemsmay

be builtwhich

produce an astounding variety ofbehaviors. Unfortunatelymany

ofthesemodels

areformulated without regard to the vast

body

of empiricalknowledge documenting

the decisionprocesses ofindividuals.

For

example, rational expectationsmodels

ineconomics presume

agents have perfect

knowledge

ofand

the cognitivecapability to solve the system ofequations

which

characterize theeconomy

(Lucas 1976,Shaw

1984).These

assumptions arestrongly contradicted by evidence atall levels of aggregation

(Simon

1984,Hogarth

and

Reder

1986) andform

a poorfoundation fordescriptivemodels

ofeconomic

dynamics.Similarly, physical scientists frequentiy specify decision processes in

models

ofhuman

behavior

by

analogy with natural systems (Beylich 1986,Zeeman

1977,Zimmerman

1986), or simply assert that the processes studied in natural systems extendby

analogy to socialdynamics

(Ruelle 1984,May

1976).The

natural sciences can indeed be a fruitful source ofmetaphor

for theories ofhuman

behavior,and

there is encouraging progress in the applicationof nonlinear science to social systems (e.g. Prigogine and Sanglier, 1987).

But

without a firmempirical grounding in tiiepsychology ofchoice behavioral scientists will continue to

view

such

models

as ad hocand

continue to question their relevance. It has been difficult toassess the validity of such

models

because theassumed

decision ruleswere

not subject toempirical test. In the future experimental tests of

models

ofhuman

behavior shouldbecome

as accepted and

commonplace

as they are in the natural sciences.Over

time the application of thesemethods

should identify the processes ofjudgment

people actually use indynamic

decisionmaking tasks

and which

are acceptable as the basis foraccuratemodeling

ofhuman

affairs.

Models

formulatedon

the basis ofknowledge

of individual decisionmaking, analyzedwith the tools of simulation

and

modem

nonlinear science,and

subjected to experimental testoffer the best

hope

toimprove

our understanding ofthedynamics

and evolution ofsocialD-3921

23

Notes

1.

Order

cancellations aresometimes

possible andmay

exceednew

orders in extremeconditions (e.g. the U.S. nuclear

power

industry in the 1970s). Since cancellations arelikely to be subject to different costs and administrative procedures than

new

ordersthey should be represented separately as a distinct outflow

from

the supply line ofunfilled orders rather than as negative orders.

2.

Note

that the function OK=f(-) does not contain an estimated regression constant.Thus

the correspondence of the estimated and actual capital orders, notjust their variation

around

mean

values, provides an importantmeasure

of the model's explanatory power.Since the residuals e

need

not satisfy Zet=

the conventionalR^

is not appropriate.The

alternativeR2

= 1 - Set^ /lOKt^

is used (Judge et al. 1980). ThisR2

can beinterpreted as the fraction of the variation in capital orders around zero explained by the

model.

3. Analysis

showed

a slight tendency for the trials with themost

extreme amplitude andhighest costs to be

most

prone to accounting errors.Thus

the finalsample

of eleventrials is biased slightly towards those

who

understood andperformed

best in thegame.

The

effect is modest, however,and

reinforces the conclusionsdrawn below

regardingmisperceptions of the feedback structure

by

the subjects.4. In the experiment and in the simulations orders are restricted to the positive integers.

5.

The

parameters 6, as, p,and

S'were

estimated to the nearest .1, .05, .05, and 1 units,respectively.

The

searchwas

carried out over a sufficiently large range to ensure6.

Note

that S' functionsmuch

like a regression constant in eq. 32.However

thenonlinearity

Ot>0 means

the residuals will not, in general, satisfy Let = (estimatedand actual orders

need

not have acommon

mean).The

conventionalR^

is not thereforean appropriate

measure

of goodness offit.The

alternativeR^

=

r^is used,where

r isthe coefficient ofcorrelation

between

estimated and actual orders (Judge et al. 1980).7. Subjects

were

assigned positions randomly,and one-way

ANOVA

of the estimatedparameters

showed

no

strong relationshipbetween

the values of the estimatedparameters

and

the position one plays in thegame

(with the exception ofas

which

was

significant at the

4.3%

level).N.B.

The

longwave

game

runson

anyIBM

PC

orcompatible computer; disks are availablefrom

the author.The

estimation and simulations for both experimentswere

carried outon

Macintosh

computers using theTrueBASIC

language.The

dataand

computer

programs

are availablefrom

the authorupon

request.To

avoid transients, the phaseplots

shown

in figure4 were

generatedby

simulateing themodel

for 10,000 periods anddiscarding the first 9000. Similarly, the phase plots

shown

in figure 8were

simulated for1500 weeks.

The

first500 were

discarded for all except the Bassbeer factory, forwhich

D-3921

25References

Bakken, B. 1987. Learning

System

Structureby

ExploringComputer

Games,

unpublishedmanuscript,

System

Dynamics

Group, Sloan School ofManagement,

MIT,

Cambridge

MA

02139.Beylich, A. 1986.

On

the Modelling of VehicularTraffic Flow. In C. Kilmister (ed.)Disequilibrium

and

Self-Organization. Dordrecht: D. Reidel.Cyert, R.

and

J.March.

1963.A

BehavioralTheory

ofthe Firm.Englewood

Cliffs N.J.:Prentice Hall.

Davis, H. L., S. J.

Hoch, and

E. K. Easton Ragsdale. 1986.An

Anchoring and Adjustment

Model

of Spousal Predictions. Journal ofConsumer

Research. 13:25-37.Day,

R. 1984. DisequilibriumEconomic

Dynamics:

A

Post-Schumpeterian Contribution.Journal of

Economic

Behavior

and

Organization. 5, 57-76.Day,

R. 1982a. IrregularGrowth

Cycles.American

Ecoru>micReview. 72, 406-414.Day,

R. 1982b.Complex

BehaviorinSystem

Dynamics

Models.Dynamica.

8, 82-89.Einhom,

H. J., andR.M.

Hogarth. 1985.Ambiguity

and

Uncertainty in Probabalistic Inference.Psychological Review. 92:433-461.

Forrester, J.

W.

1961. IndustrialDynamics.

Cambridge,

MA:

MIT

Press.Forrester, J.

W.

and

P.M.

Senge. 1980. Tests for Building Confidence inSystem

Dynamics

Models.

TIMS

Studies in theManagement

Sciences. 14:201-228.Frankel, J. A.

and

K. A. Froot. 1987.Using

SurveyData

to Test Standard PropositionsRegarding

Exchange

Rate ExpectationsAmerican

Economic

Review

77:133-153.Hines, J.

1986

A

BehavioralTheory

of Interest Rate Formation.Working

paperWP-

1771-86,Sloan School of

Management,

MIT.

Hogarth, R.

M.

andM. W.

Reder

(eds). 1986.The

Behavioral Foundations ofEconomic

Theory

Journal ofBusiness. 59:S181-S505.Jarmain,

W.

E. (ed.) 1963.Problems

inIndustrialDynamics.

Cambridge,

MA: MIT

Press.Johnson, E. J. and D. A. Schkade. 1987. Heuristics and Bias in Utility Assessment.

Unpublished

manuscript,Wharton

School, University ofPennsylvania, Philadelphia.Judge et al. 1980.

The Theory

and

Practiceof Econometrics.New

York: Wiley.Lopes, L. L. 1981.

Averaging

Rules and Adjustment Processes:The

Role

ofAveraging

inInference. Report 13,

Wisconsin

Human

Information Processing Program, University ofWisconsin,

Madison.

Lucas, R.E. 1976. Econometric Policy Evaluation:

A

Critique. In K.Brunner

and

A. Meltzer(eds).

The

PhillipsCurve

and Labor

Markets.Supplement

to the Journal ofMonetary

Economics.May,

R.M.

1976. Simple MathematicalModels

withVery Complicated Dynamics.

Nature. 261(5560):459-467.Morecroft, J. 1983.

System Dynamics:

PortrayingBounded

Rationalit>'.Omega.

11:131-142. Morecroft, J. 1985. Rationality in the Analysis of Behavioral Simulation Models.Management

Science 31:900-916.

Mosekilde, E., D.

Rasmussen,

H. Jensen, J. Sturis, and J. Jespersen. 1987. Chaotic Behaviorin a Generic

Management

Model. European

Journal of Operations Research. Forthcoming. Mosekilde, E. and E. Larsen. 1987. Chaotic Behavior in the Beer DistributionGame.

System

Dynamics

Review. 4(1).Nicolis, G.

and

I. Prigogine. 1977. Self-Organization in Nonequilibrium Systems.New

York:Wiley.

D-3921

27

Institutions. Science.

232

(9May),

732-738.Prigogine, I. and

M.

Sanglier (eds.) 1987.Laws

ofNature

and

Human

Conduct. Brussels:Task

Force of Research Information and Studyon

Science.Rasmussen,

S., E. Mosekilde, and J. D. Sterman. 1985. Bifurcationsand

Chaotic Behavior ina

Simple

Model

oftheEconomic

Long

Wave.

SystemDynamics

Review. 1(1):92-1 10.Richardson, G.P.and A.L. Pugh. 1981. Introduction to System

Dynamic

Modeling

withDYNAMO.

Cambridge

MA:

The

MIT

Press.Ruelle, D. 1984. Strange Attractors. In P. Cvitanovic (ed.)Universality in Chaos. Bristol:

Adam

Hilger, Ltd.Shaw,

G.K. 1984. Rational Expectations.New

York: St. Martins Press.Simon,

H. A. 1979. RationalDecisionmaking

in Business Organizations.American

Economic

Revie^^. 69:493-513.

Simon.,H. A. 1984.

The

Behavioral and Rational Foundations ofEconomic

Dynamics.

Journalof

Economic

Behavior

and

Organization. 5:35-55.Smith, V. 1982.

Microeconomic Systems

as an Experimental Science.American

Economic

Review.

72, 923-955.Sterman, J. D. 1984. Instructions for

Running

theBeer

DistributionGame.

System

Dynamics

Group

working

paperD-3679,

Sloan School ofManagement,

MIT.

Sterman,J. D. 1985a.

A

BehavioralModel

oftheEconomic

Long Wave.

Journal ofEconomic

Behavior

and

Organization. 6:17-53.Sterman, J. D. 1985b.

A

Skeptic'sGuide

toComputer

Models.Working

PaperD-3665,

System

Dynamics

Group, Sloan Scholl ofManagement,

MIT,

Cambridge

MA

02139. Sterman, J. D. 1986.The Economic Long Wave:

Theory

and Evidence. SystemDynamics

Sterman, J. D. 1987a. Testing Behavioral Simulation

Models

by DirectExperiment.Management

Science. 33(12).Sterman, J. D. 1987b. Misperceptions of

Feedback

inDynamic

Decisionmaking.Working

paperWP-

1899-87. Sloan School ofManagement,

MIT,

Cambridge

MA.

Sterman, J. D. 1987c. Managerial Behaviorin

Dynamic

Decisionmaking: FurtherMisperceptions of Feedback.

System

Dynamics

Group

working

paperD-3919,

Sloan School ofManagement,

MIT.

Sterman, J. D. 1987d. Expectation

Formation

in Behavioral Simulation Models. BehavioralScience. 32:190-211.

Sterman, J. D. and D. L.

Meadows.

1985.STRATEGEM-2:

A

Microcomputer

SimulationGame

ofthe Kondratiev Cycle. Simulationand

Games.

16:174-202.Thompson,

J.and

H. Stewart. 1986.NonlinearDynamics

and

Chaos.New

York: Wiley. Tversky, A.and

D.Kahneman

1974.Judgment

Under

Uncertainty: Heuristicsand

Biases.Science . 185 (27 September): 1124-1131.

Zeeman,

E. C. 1977. Catastrophe Theory: SelectedPapers, 1972-1977. Reading,MA:

AddisionWesley

Publishing Co.Zimmerman,

R. 1986.The

Transitionfrom

Town

to City: Metropolitan Behaviorin the 19th Century. In C. Kilmister (ed.). Disequilibriumand

Self-Organization. Dordrecht: D. Reidel.D-3921 29

Figure 1.

The

generic stock-management system.u

ExogenousVariables

Stock Acquisition System

Expected

Loss Rate

Figure 2.

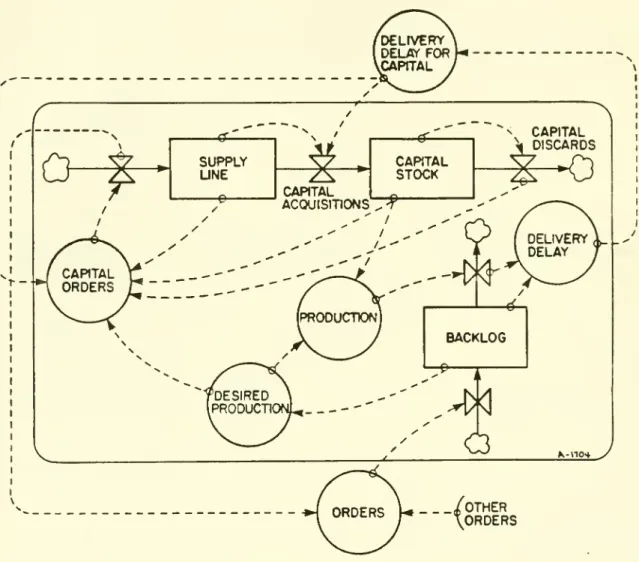

The

stockmanagement

system applied to aggregate capital investment.The model

portrays a firm

which

produces capital plant and equipment.The

demand

for the firm's productis exogenous, as is the delivery delay for acquiring

new

capital stock.When

the self-orderingmultiplier is introduced, the firm's

own

orders for capital add to theexogenous demand,

andthe delivery delay for capital

becomes

the firm'sown

delivery delay.SUPPLY

UNE

CAPITAL ACQUISITIONSCARTAL

STOCK N CAPITAL ^ DISCARDSo

/S^

( DELIVERYL

ill

DELAY 7 fpRooucnoNj\

J

BACKLOG

K-not _-/OTHER

\ORDERS

D-3921

31Figure 3. Typicalresultsofthe macroeconoinic experiment.

4

iitKaMaMMMMMa

D-3921

35Trial

Table 2.

Macroeconomic

experiment: Estimated parameters.Score

as

Std. Error*asL

Std. Error* R2 Mode1200n

1000-Gome18

600

100

Figure 4. Simulation ofthedecisionrule with estimated parameters.

eoo Proaucllon Capacity 1200 HOOn 1200 1000 600 Game36 800 Production CapecUij

*

1200 eoo 750 c TOO o o a. ^ 600 •> o 550 500 150 Game 12 500 600 700 Production Capacity eoo 880 1230 1250 Production Capacity 1270 1200-1 Game 10 100 800 ProductionCapacity 1200D-3921

35

a

Figure 5.

Modes

ofthe system inparameterspace.Lower

graphzooms

into areabetween (0,1).D-3921

37Figure7. T^'picalexperimentalresults oftheBeerdistribution

Game.

7a:

Customer

Orders. Inweek

5customerordersrisefrom

4 to 8 cases perweek.Compare

against the oscillations inthe subjects'orders(7c).30-25 - ro15 -'J -5

-Figure7b.

Key

toexperimental results (figure 7c).a

Factory ^ Distributor

_ Wholesaler

Retailer

Orders placed bysector.

Frombottom totop,

R. W.D,F,eachoffsetby15cases/week. Major tick-marks=l5 cases/week. Minortick-marks=5 cases.'week

Initialorders=4cases/weekinallsectors.

5 10 U 20 25 30 :5 Weeks o c 01 > c o o Factory Distnbutor Wholesaler Retailer

Effective Inventoryby seaor.

Effective lnventory=lnventory-Backlog.

Frombottomtotop,

R, W.D, F,eachoffset by40cases. Maior tick-marks=40cases. Minor tick-marks=lOcases.

Initial inventorysl2casesin allsectors.

3 10 13 20 23 30 33