MITLIBRARIES

*

/

N

*

UBKARES

Digitized

by

the

Internet

Archive

in

2011

with

funding

from

Boston

Library

Consortium

Member

Libraries

hb3i

\msmy

jy[415

Massachusetts

Institute

of

Technology

Department

of

Economics

Working

Paper

Series

Did

Mandatory

Unbundling

Achieve

Its

Purpose?

y

Empirical

Evidence from

Five

Countries

Jerry

Hausman

Gregory

Sidak

Working

Paper

04-40

Nov

1,2004

Room

E52-251

50

Memorial

Drive

Cambridge,

MA

02142

This

paper can be downloaded

without

charge from

the

Social

Science

Research Network

Paper

Collection

at

MASSACHUSETTS

INSTITUTEOF TECHNOLOGY

FEB

12005

Hausman Sidak Oxford vS 3:00

PM

Eastern11/08/04Did

Mandatory

Unbundling

Achieve

Its

Purpose? Empirical Evidence

from

Five

Countries

Jerry

A.

Hausmanf

J.

Gregory

Sidakf

tIn this article, we examine the rationales offered by telecommunications regulators

worldwide for pursuingmandatory unbundling. We beginbydefiningmandatoryunbundling,

with brief descriptions ofdifferent wholesaleforms and different retailproducts. Next, we

examinefourmajorrationalesforregulatory intervention ofthis kind: (I) competition in the

form oflowerprices andgreater innovationin retailmarkets isdesirable, (2)competition in

retail markets cannot be achieved with mandatory unbundling, (3) mandatory unbundling

enables future facilities-based investment ('stepping-stone' or 'ladder of investment'

hypothesis),and(4)competitioninwholesale access marketsisdesirable. Weproceedbytesting empirically the major rationales in the United States, the United Kingdom,

New

Zealand,Canada, and Germany. Foreach case study, we review themandator}' unbundling experience

with respectto retailpricing, investment, entrybarriers, andwholesalecompetition. Wereview

the lessons learnedfrom the unbundlingexperience. We also identify which rationales were

incorrect in theory and which rationales were correct in theoryyet were not satisfied in

practice. Forthesecondcategoryofrationales, weattempttoprovidealternativeexplanations forthefailureof mandatoryunbundlingtoachieveitsgoals.

I.

What

IsMandatory Unbundling?

3A. Different

Wholesale

Forms

41.

Mandatory Unbundling

at DifferentLevels oftheNetwork

42.

Mandatory Unbundling

Versus ServiceResale 5a.

Mandatory Unbundling

Versus Resale ofVoice

Services 6b. Line SharingVersus Bitstream

Access

ofData

Services 6B. DifferentResultingRetailProducts 8

1.

Voice

Services 8a.

Mass

Market

VersusEnterprise 8b. RuralVersus

Urban

102.

Data

Services 103. ExistingServices Versus

New

Services 11II.

Why

PursueMandatory Unbundling?

1 1A. Rationale 1:Competition inRetail MarketsIsDesirable 1

1

1. Innovation

and

Investment 122. Prices

and

Retail Margins 13B. Rationale 2: Competition in Retail Markets

Cannot

Be

Achieved

Without

Mandatory Unbundling

14| MacDonaldProfessorof Economics, MassachusettsInstituteofTechnology.

tt F.K. WeyerhaeuserFellowin

Law

andEconomicsEmeritus,AmericanEnterpriseInstituteforPublic PolicyResearch.Thisresearchwas commissionedby Vodafone.Theviews expressedhere are solely those ofthe authors and not those of

MIT

orAEI, neitherofwhich takes institutional2

Hausman

and Sidak1 .

A

Vertically IntegratedFinn

Generally PrefersItsOwn

Downstream

Affiliate 14

2. EntryBarriersPreventNaturalCompetition 15

C. Rationale 3:

Mandatory Unbundling

Enables Future Facilities-BasedInvestment 16

D. Rationale4: Competition inWholesale

Access Markets

IsDesirable 181.

A

Network

ofNetworks

182. Regulatory Withdrawal 19

E. Conclusion 19

III.

The Unbundling

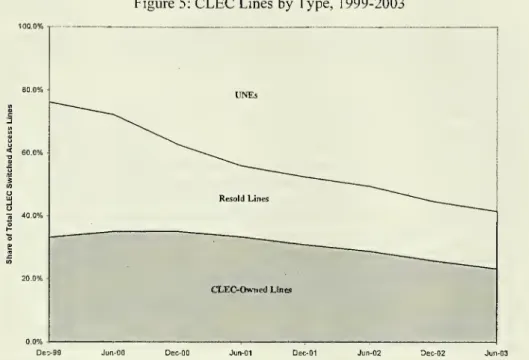

ExperienceinFive Countries 20A. UnitedStates 21 1. Retail Competition 21 a. Pricing 21 b. Investment

22

2. Entry Barriers24

3. Stepping-StoneHypothesis 28 4.Wholesale

Competition 325. Other Observations abouttheProcess 33

B. United

Kingdom

331. RetailCompetition 36

a. Pricing 36

b. Investment 37

2. EntryBarriers 38

3. Stepping Stone Hypothesis

40

4. Wholesale Competition

40

5. Other Observations

About

the Process 42C.

New

Zealand44

1. Retail Competition

46

a. Pricing

46

b. Investment

47

2. EntryBarriers 48

3. Stepping Stone Hypothesis 50

4. Wholesale Competition 50

5. Other Observations abouttheProcess 50

D.

Canada

511. RetailCompetition 53

a. Pricing 53

b. Investment 55

2. EntryBarriers

56

3. Stepping Stone Hypothesis 5.8

4. Wholesale Competition 59

5. Other Observations abouttheProcess 60

E.

Germany

61 1 . RetailCompetition 62 a. Pricing62

b. Investment 62 2. Entry Barriers 633. Stepping Stone Hypothesis 65 4. Wholesale Competition 65 5. Other Observations

About

theProcess 66November

2004 Did Mandatory Unbundling AchieveItsPurpose? 3F.

Summary

66IV. Lessons

Learned

from

theUnbundling

Experience 68A.

The

RationalesThatWere

Not

CorrectinTheory

68B.

The

Rationales ThatWere

Correct inTheory Yet

Were

Not

Satisfied inPractice 69

Conclusion 70

I.

What

IsMandatory Unbundling?

In the 1990s,

mandatory

unbundlingbecame

the proposedremedy

of choice inregulatory

and

antitrust proceedings. Foradecade

ormore, thedominant

theme

inregulatory and antitrust law has been

what might

be called 'the spirit ofsharing.'For example, in the United States, the

Telecommunications

Act

of 1996 restson

the hypothesis that requiring a firm to share the use of its facilities with itscompetitors will enable the competitors eventually to build their

own

facilities,presumably

to the eventual benefit of consumers.The

mandatory

sharing offacilities is thus the segueto eventual competition

between

rival infrastructures orplatforms.

The

corollary ofthis assumption is that, but for this exactform

ofregulatory intervention, natural market forces cannot be counted on to produce

facilities-basedcompetition.1

Any

firmmay

chooseto unbundle or leasecomponents

ofitsnetwork

with athird party at a voluntarily negotiatedrate.

The

firm is also able to decide thescopeofunbundlingitwantstoundertake

—

how much

ofitsnetwork

toresell.The

term 'mandatory unbundling' describes an involuntaryexchange

between

anincumbent network

operator and a rival at a regulatedratewhere

the scope ofunbundling is determined

by

regulators. Determination of the access rate thusbecomes

the majorbone

of contentionbetween

incumbent

and entrant, as aregulatory access rate that is equal to the voluntarily agreed-upon access rate

cannotreally besaid to constitute'mandatory' unbundling.

When

formulatingthataccess rate,regulators havegenerally opted in favor ofa

measure

oftotal elementlong-run incremental cost

(TELRIC)

or total service long-run incremental cost(TSLRIC)

and

against ameasure

ofopportunity cost or optionvalue.21 .

Thenearestexampleinthe antitrust literaturewas anabandonedremedy inMicrosoftthat

wouldhave forced theincumbentoperatingsystem providertodiscloseitssourcecodeto rivals.See

J.GregorySidak,'AnAntitrustRuleforSoftwareIntegration', 18YaleJ.onReg. 1 (2001).

2. For a detailed analysis ofthe scope ofthe unbundling decision and the access pricing decisionbyatelecommunicationsregulator,see JerryA.Hausman/J. Gregory Sidak,'A

Consumer-WelfareApproachtoMandatory Unbundling of Telecommunications Networks', 109Yale L.J.

417 (1999). For areview ofunbundling in other contexts, see J. Gregory Sidak/Hal J. Singer,

'InterimPricingof LocalLoop UnbundlinginIreland: Epilogue', 4J.NetworkIndus. 119(2003);J.

Gregory Sidak/Allan T. Ingraham, 'Mandatory Unbundling, UNE-P, andtheCostofEquity: Does

TELRIC

PricingIncreaseRiskforIncumbent LocalExchangeCarriers?',20 YaleJ.Reg.389(2003);J. GregorySidak/HalJ. Singer,

How

CanRegulators SetNonarbitraryInterim Rates?The Case ofLocalLoopUnbundlinginIreland', 3J.NetworkIndus.273 (2002); Thomas M. Jorde/J. Gregory

Sidak/David J. Teece, 'Innovation, Investment, and Unbundling', 17 Yale J. Reg. 1 (2000). J.

Gregory Sidak/Daniel F. Spulber, 'The Tragedy ofthe Telecommons: Government Pricing of

UnbundledNetwork Elements UndertheTelecommunications Actof1996',97 Colum.L. Rev.

4

Hausman

and SidakIn this section,

we

definecommon

terms used inmandatory

unbundlingproceedings and identifyrelevantproduct marketsthat areaffected

by

unbundlingpolicy.

We

also analyze different wholesale forms ofmandatory

unbundling andthe resulting retail products, with a special emphasis on

new

versus existingproducts.

Although

we

rely extensivelyon

the U.S. experience to introduce thebasic concepts of

mandatory

unbundling, Part III of this reportexamines

theunbundling experience ofseveral other countries.

A. Different

Wholesale

Forms

Regulators

mandate

unbundling at various parts of an incumbent localexchange

carrier's

(ILEC)

network,including the loop,transport,andswitch.When

selectingwhich

elementstomake

availableto competitorsatregulated rates,regulators haveconsidered the effect of

mandatory

unbundling in conjunction with the potentialforresaleoffinal services.

1.

Mandatory Unbundling

atDifferentLevelsoftheNetwork

Mandatory

unbundling at a regulated ratemay

apply to various 'networkelements,'

which

are defined by the U.S.Telecommunications

Act

of 1996 as 'afacility or

equipment

used intheprovision ofatelecommunications service.'3The

Act

instructs theFCC

to consider whether 'the failure to provide access to suchnetwork elements

would

impair the ability of the telecommunications carrierseekingaccesstoprovidethe services thatitseekstooffer.'

4

Under

theAct, pricesfor

unbundled

network

elements(UNEs)

are basedon

the cost of providing theinterconnection or network element.5

The

FederalCommunications

Commission

(FCC)

interpreted that pricing rule as 'forward-looking, long-run, incrementalcost.'6 In practice, prices are 'based on the

TSLRIC

[total service long runincremental cost] of the network element . . .

and

will include a reasonableallocationof forward-lookingjoint and

common

costs.'7As

part ofits TriennialReview Order

ofits unbundling regulations, theFCC

explained that

ILECs

were

required toprovide accessto network elements 'totheextentthatthoseelementsare capableof being used

by

therequestingcarrier intheprovision ofa telecommunications service.'8

The

FCC

ordered allILECs

tomake

available atregulatedratesthe following

UNEs:

3. 47U.S.C.§153(29).

4. 47 U.S.C.§251(d)(2)(B).

5. 47 U.S.C. §252(d)(1) (stating that 'DeterminationsbyaStatecommission ofthejustand

reasonablerate forthe interconnectionoffacilitiesandequipmentforpurposesofsubsection(c)(2)of

section251,andthejustandreasonablerate fornetwork elementsforpurposesofsubsection(c)(3)of suchsection

—

'(A)shallbe—

'(i)basedonthecost(determined withoutreferencetoa rate-of-return or otherrate-based proceeding) ofproviding the interconnection ornetwork element (whicheverisapplicable),and'(ii)nondiscriminatory,and'(B)mayinclude areasonableprofit.').

6. Implementation ofthe Local Competition Provisions in the Telecommunications Act of

1996; Interconnection between LocalExchange Carriers and CommercialMobile Radio Service Providers,

CC

Docket Nos. 96-98, 95-185, First Report and Order, 11FCC.

Red. 15499, \620(1996) [hereinafterFirstReport

&

Order].7. Ibid,at1672

8. ReviewoftheSection 251 UnbundlingObligationsof Incumbent LocalExchangeCarriers,

ReportandOrder and Order onRemandand FurtherNotice of Proposed Rulemaking,

CC

Dkt.No.01-338, 20 August2003, at 42\ 59[hereinafter TriennialReview], rev'd, U.S.Telecom Ass'n v.

November

2004 DidMandatory Unbundling AchieveItsPurpose?(1) stand-alone copper loops

and

subloops for the provision ofnarrowband

and

broadband

services,(2) fiberloops for

narrowband

servicein fiberloop overbuildsituationswhere

the

incumbent

LEC

elects to retireexistingcopper loops,(3) subloops necessary to access wiring at or near a multiunit customer

premises,

(4)

network

interface devices (NID),which

are defined asany

means

ofinterconnecting the

ILEC's

loopdistribution plant to wiring at acustomerpremiseslocation,

(5) dark fiber,

DS3, and

DS1

transport, subject to a route-specific reviewby

thestates toidentify availablewholesalefacilities,

(6) local circuitswitchingserving the

mass

market,(7) sharedtransportonlytothe extentthat carriersareimpaired withoutaccess

to

unbundled

switching,(8) signaling

network

when

acarrierispurchasingunbundled

switching,and

(9) call-related databases

when

a requesting carrier purchasesunbundled

accesstothe

incumbent

LEC's

switching,(10) operations support systems

(OSS)

for qualifying services,which

consistsof pre-ordering, ordering, provisioning, maintenance and repair,

and

billingfunctionssupported

by

anILEC's

databasesandinformation,and(11) combinations of

UNEs,

including the loop-transportcombination(enhanced extendedlink, or

EEL).

9Based

onthisexhaustive list,itisreasonableto concludethat, at leastintheUnitedStates, virtually no

component

of an incumbent'snetwork

was

immune

from

unbundling obligations eight years after the passage ofthe

Telecommunications

Act.2.

Mandatory Unbundling

Versus ServiceResaleTo

introduce competition in the final service market, regulatorshave

made

network elements available for lease, or have

made

final services available forresale, orboth. In this section,

we

reviewthe choices oftheregulator intheUnitedStates and

New

Zealand withrespecttothatdecision.6

Hausman

and Sidaka.

Mandatory Unbundling

Versus Resale ofVoice

ServicesThe

Telecommunications

Act

allows for local service competition through threetypes ofentry: resale, leasing of

UNEs,

and investment in and ownership offullfacilities.10 Resale requires the least initial capital investment, but it limits the

entranttoresellingthe

ILEC's

products in their original form. Leasingsome

partsofthe network as

UNEs

provides an entrant greaterflexibility to develop servicesthan doesresale.

With

regardtothe resaleof telecommunication services,theAct

clearly states that prices are to be based

on

the retail price less any associatedmarketing,billing, collection, orother costs forgone

by

theILEC."

Accordingly,theresalepricingstandardset forth

by

theFCC

requires statecommissions

to: '(1)identify

what

marketing, billing, collection, and other costs will be avoidedby

incumbent

LECs

when

they provide services at wholesale; and (2) calculate theportion ofthe retail prices for those services that is attributable to the avoided

costs.'12 In practice, resale prices are determined either through avoided cost

studies or

by

default discountrates set forthby

theFCC.

13The

FCC

believedthatthis form ofpricing

would

induce competition in the telecommunications marketandincrease efficiencyinthearbitrationandnegotiation processes.

In its Triennial

Review Order

in 2003, theFCC

commented

that competitivelocal

exchange

carriers'(CLECs)

purchase oftotal serviceresale forvoice servicehaddeclined froma peak of almost5.4 million lines in

2000

tobelow

3.5 millionlines by mid-2002.14

By

contrast, thenumber

ofUNEs,

which

includes loopsacquiredseparatelyandinconjunctionwith switching (the'unbundled platform' or

UNE-P),

increasedfrom

1.5 millionto 11.5 millionover thesame

period.15Many

scholars in the United States attributethe massive substitution

from

resale towardUNEs

tothemispricingofUNEs.

16b. Line SharingVersus Bitstream

Access

of DataServicesBitstream access provides service-level (resale) entry to digital subscriber line

(DSL)

data provision.Under

the bitstreamapproach, the entrantbuys thecompleteservice fora high-speed link totheconsumer, and the serviceincludes delivery to

the firstdataswitch in the incumbent's network. Line sharing,

by

contrast, allowsthe entrant to acquire the high-frequency portion of the copper connection but

requiresitto

make some

investmentsininfrastructure.Mandatory

line sharingwas

attempted and thenabandoned

in the UnitedStates. Inthe

FCC's

LineSharingOrder

released in 1999, theFCC

directedILECs

to provide the high-frequency portion of the local loop

(HFPL)

to requesting10. 47U.S.C.§251.

11. 47 U.S.C.§ 252(d)(3)(stating that 'aStatecommissionshalldetermine wholesalerateson

the basis of retail rates charged to subscribers for the telecommunications service requested,

excludingtheportion thereofattributable to anymarketing, billing,collection, andother coststhat

willbeavoided bythelocalexchangecarrier.').

12. SeeFirstReport

&

Order,aboven6, at\908.13. Ibid

14. SeeTriennialReview, aboven8,at32J 41

.

15. Ibid

16. See, e.g., RobertW. Crandall/Allan T.Ingraham/Hal J. Singer, 'Do UnbundlingPolicies

Discourage

CLEC

Facilities-Based Investment?', 4 Topics in Economic Analysis&

Policy_

November

2004 Did Mandatory Unbundling AchieveItsPurpose? 7carriers as a

UNE.

17The Commission

found inthe LineSharingOrder

that '[t]herecord

shows

that lack ofaccesswould

materially raise the cost for competitiveLECs

toprovideadvanced

services [suchasDSL]

toresidential andsmall businessusers, delay broad facilities-based marketentry and materially limitthe scope

and

quality of competitorserviceofferings.'18In

May

2002, however,theU.S.CourtofAppeals

for the D.C. Circuit vacated the Line Sharing Order, finding that theCommission

had failed to give adequate consideration to existing facilities-basedcompetition in the provision of

broadband

services, especiallyby

cable systems.19In its

August 2003

TriennialReview

Order, theFCC

decided not to reinstate thevacated line-sharing rules because itdetermined that 'continued

unbundled

accessto stand-alonecopper loops

and

subloops enables a requesting carrier to offerandrecover its costs

from

all of the services that the loop supports, includingbroadband

service.'20The

FCC

rejected its prior finding that lackof

separate access to the highfrequency portion

would

cause impairment for four reasons. First, theFCC

explained that its earlier impairment finding

had

been

basedon

a notion thatbroadband

revenueswould

notjustifythe costofthewhole

loop. Afterconsideringrevenues

from

voiceand

video, theFCC

determined that such revenueswould

offset the costs associated with purchasing the entire loop.21 Second, the

FCC

explained that

CLECs

interested only inbroadband

could obtainbroadband

frequencies

from

otherCLECs

throughline-splitting, inwhich

oneCLEC

providesvoiceservice

on

thelow

frequencyportionofthe loopandtheotherprovidesDSL

on

the high frequency portion.22 Third, theFCC

noted thatthe difficultiesofcostallocation for different portions ofa single loop

had

ledmost

states to price thehigh frequency portion of the loop at approximately zero,

which

distortedcompetitive incentives.23 Fourth, the

FCC

recognized the substantial intermodal competitionfrom

cable companies,which

lessened any competitive benefitsassociatedwith linesharing.24

In its

March

2004

opinion, the D.C. Circuit Court of Appeals upheld theFCC's

decision to eliminate line sharing, concluding that theFCC

'reasonablyfound thatother considerations

outweighed

any impairment.'25With

respecttotheincentive

problem

raised by theFCC,

thecourt opined: '[I]t is of course true thatalternative cost allocations could have reduced the skew, but any alternative

allocation of costs

would

itself havehad

some

inescapable degree of17. Deploymentof Wireline Services OfferingAdvancedTelecommunications Capabilityand

Implementation ofthe Local Competition Provisions ofthe TelecommunicationsAct of1996,

CC

Dkt.Nos. 98-147, 96-98, ThirdReport andOrder in

CC

Dkt. No.98-147 and Fourth Report andOrderin

CC

Dkt.No. 96-98, 15F.C.C.Red. 3,696 (1999)[hereinafterThirdOrder].18. Ibid, at20,9161(5

19. U.S.TelecomAss'nv.FCC,290F.3d415,428-29 (D.C.Cir.2003).

20. SeeTriennialReview,aboven8, at 125atU199. 21. Ibid, atH 258

22. Ibid, at11259

23. Ibid, atH260

24. Ibid, atH 263. Interestingly, the chairman ofthe FCC, Michael K. Powell, didnot agree with the decisiontoterminatelinesharing, arguingthat'thecontinuedavailabilityoflinesharingand

thecompetitionthatflowedfromitlikelywouldhave pressured incumbentstodeploymoreadvanced

networks in orderto move from the negative regulatory pole to the positive regulatory pole, by

deployingmorefiber infrastructure.'SeparateStatementofChairmanMichael K.Powell,Dissenting

in Part,20February 2003, at1 (availableat http://hraunfoss.fcc.gov/edocs_public/attachmatch/DOC-231344A3.doc).

8

Hausman

and Sidakarbitrariness.'26

The

courtadded

that 'intermodal competition from cable ensuresthepersistenceofsubstantial competitioninbroadband.'27

Regulatorsinothernations have chosenbitstreamaccess overline sharing.For example, in

December

2003, theNew

ZealandCommerce

Commission

recommended

the designation of an 'asymmetricDSL

bitstream access service.'28The

agency

definedADSL

bitstream access service as 'a high speed IP accessservice

which

providesgood

performance, but could not typically supportextensive use of mission critical applications

which

require excellent real-timenetwork performance oravailability.'29

The

Commission

defined bitstream accessas a situation in

which

the incumbent's access link 'ismade

available to otheroperators,

which

are then ableto providehigh-speed servicesto end-consumers.'30The

agency concluded the netsocial benefitsfrom

bitstream access exceeded thenet social benefits of line sharing due to the lower total cost of providing the

unbundled

service (collocation costs are avoided in bitstream access).31

The

Commission

reasoned that, under bitstream access, entrants face a lower risk ofinvesting in

network

components

such asDSLAMs

thatmight

not be fullyutilized.32

We

discuss theNew

Zealand experience in greater detail in a latersection.

B. Different Resulting Retail

Products

As

we

describe in Part II,one

objective ofmandatory

unbundling is to increasecompetition in certain final services markets.

Below,

we

describe the relevantproductmarketsthatareaffectedby

mandatory

unbundling.1.

Voice

ServicesThe

voice services market is typically divided intotwo

markets: themass

marketfor

consumers

andthe enterprise marketforbusinesses.a.

Mass

Market

VersusEnterpriseUnbundling

rates andtherelativesizeofthoserateswithrespecttotheactual costsoffacilities-based entry influence a

CLECs

entry strategy acrossmass

marketsand enterprise markets.

Using

the United States as an example,CLECs

began

competing

withILECs

in the enterprise market for voice services in themid-1980s. Competitive access providers

(CAPs)

began

providing competitiveexchange

access service tolarger business customers inNew

York

inthe 1980s/3CLECs

self-provision facilities, lease facilitiesfrom

other competitive facilities26. Ibid, at46

27. Ibid

28.

New

Zealand Commerce Commission, Section 64 Review and Schedule 3 Investigationinto Unbundling the Local Loop Network and the Fixed Public Data Network, Final Report,

December 2003 (availableathttp://www.comcom.govt.nz/telecommunications/Hu/finalreport.PDF).

29. Ibid,atAppendix5

30. Ibid, at117

31. Ibid, at20

32. Ibid, at21

33. SeeTriennialReview,aboven8,at34J44.Forareview ofCAPs,seeDanielF.Spulber/J.

GregorySidak,Deregulatory TakingsandtheRegulatoryContract: The Competitive Transformation

November

2004 DidMandatory Unbundling Achieve ItsPurpose? 9providers, or purchase high-capacity

(DS1

and above) loops either asUNEs

orspecial-access services

from

theILECs.

34As

ofAugust

2003,CLECs

reportedabout 51 percent oftheircustomeraccess lines served

medium

and large businesscustomers/5

According

to the estimate ofone

regional Bell operatingcompany

(RBOC),

theCLECs'

share ofspecial-access revenueswas

at least 28 percent in 2002.36In contrasttothe enterprisemarket, the

mass

marketforvoice serviceswas

notserved extensively

by

CLECs

before 1996. Since the passage of theTelecommunications Act

in 1996, however, severalCLECs

began

to providecompetitive voice service to

many

residential customers in the United States.According

totheFCC,

by June 2003,the latestdateon

which

theFCC

reportssuchdata, 95.5 percent ofthe U.S. population lived in a zip (postal) code served

by

atleast

one

CLEC

providingsome

kind of service/7 Figure 1shows

the consistentincrease inthe percentage of households inzipcodes served by atleast

one

CLEC

(including cabletelephonyproviders) from

2000

to2003.Figure 1:PercentageofU.S.

Households

inZipCodes

withatLeast

One

CLEC

OC^paOOOOOOOOOOOOOOOOOOOOO

^ c 3 cb a. T1 > u £ -o i Js > c "5 a a. t; > o e J3 — ;= > c

^•<twOzo-iL.S<:5-'<w

ZC)-

>u-S<S"><wOzo-)ii_s<5->

Source:

FCC

Local Competition Bureau, Local Telephone Competition December 2003 Report, atTable 15 (available at

http://www.fcc.gov/Bureaus/Common_Carrier/Reports/FCC-State_Link/IAD/lcoml203.pdf)

34. SeeTriennialReview,above n8,at34 144.

35. FCC,LocalTelephone Competition:Statusasof31 December 2002,attbl.2(rel. 12June

2003) (available at

http://www.fcc.gov/Bureaus/Common_Carrier/Reports/FCC-State_Link/IAD/lcom0603.pdf)[hereinafter

FCC

Local Competition Report2002].36.

BOC

UNE

FactReport 2002, App.L,atL-l, L-2.37. FCC,LocalTelephone Competition:Status asof 30 June 2003,attbl. 15(rel.22December

2003) (available at

10

Hausman

and SidakAs

of June 2003,theCLECs

had

nearly27

million access lines, or 14.7percentof total U.S. access lines.38 Sixtytwo

percent ofCLEC

lines serve themass

marketforvoice services,

whereas

more

than 78 percent ofBOC

lines serve this group.39UNE-based

CLEC

expansion is expected to slow in the United States, asevidenced by

AT&T

andMCI's

announcements

that they are withdrawingfrom

theresidentialmarket, citingan adverseD.C. Circuit decision.

b. RuralVersus

Urban

Universal service obligations in the United States created a

complex

system ofcross-subsidies, in

which consumers

in urban areas subsidized the service ofconsumers

in rural areas.41The

degree towhich low

rates in rural areas aresupported by high ratesin urbanareas should, intheory, have a negative effect

on

UNE-based

competition in rural areas.Because

CLECs

prefer higher margins tolower margins,

and

because theCLEC

margin

is equalto the differencebetween

the retail rate and the access rate,UNE-based

CLECs

have tended to avoid ruralareas. Indeed,

CLECs

aremore

often found in urban than rural areas. Close to 26percent ofall zip codes, serving only 4.5 percent ofthe U.S. population, have

no

CLEC

presenceaccording toFCC

data.42Another

factor thatmight preventCLEC

entry in rural areas is that

many

ruralLECs

areexempt

from the unbundlingrequirementsofthe

Telecommunications

Act.432. DataServices

In the United States,

demand

for Internet access has spurred greaterdemand

forDSL

service. Line sharing,which

we

described above,was

not available for U.S.CLECs

until 2000.By

contrast,CLECs

could lease an entire copper line for dataservices as early as 1998.

As

of June 2003, about 7.7 millionDSL

lineswere

inservice.44

Of

thoselines,ILECs

were

themajor

providersofDSL

servicewith94.6percent of

DSL

lines, whileCLECs

accounted for 5.4 percent.45With

theelimination ofline sharing in the United States, the

CLECs'

share ofDSL

lines isnotexpectedtoincreaseatthe

same

rate.It bears emphasisthat

DSL

service doesnot constitute itsown

product market,as cable

modem

service is considered an extremely close substitute forDSL

service for a majority of

broadband

users.46As

ofDecember

2003, U.S. cablecompanies

offered cablemodem

service capability to 88.2 percent of U.S.households with a penetration rate of 16.8 percent. 7 In 2003, cable

companies

38. Ibid,atTable1

39. Ibid,atTable2

40. See,e.g.,BruceMeyerson,DetroitFreePress, 8October2004, *1

41. See,e.g., RobertW.Crandall/LeonardWaverman, WhoPaysforUniversal Service?: When

Telephone Subsidies Become Transparent, (Washington, DC: Brookings Institution 2000) 9-11.

[hereinafter WhoPaysfor Universal Sennce]

42 See

FCC

LocalCompetition Report2003,aboven 37,at tbls. 14, 15.43. 47U.S.C.§251(f)(1),(2).

44. See

FCC

LocalCompetitionReport2003,aboven 37,at tbl. 5.45. Ibid

46. See, e.g., Jerry A. Hausman/J. Gregory Sidak/Hal J. Singer, 'Cable

Modems

and DSL:BroadbandInternetAccess forResidentialCustomers', 91 Am. Econ.Ass'n Papers

&

Proceedings302(2001).

47. National Cable Television Association, Statistics

&

Resources (available atNovember

2004 Did Mandatory Unbundling AchieveItsPurpose? 1 1provided cable

modem

service to approximately 13.7 million subscribers,48which

was

nearly doublethenumber

ofDSL

subscribers.3. Existing ServicesVersus

New

ServicesFrom

anentrant's perspective, leasingsome

parts ofthenetwork

provides greaterflexibility to develop existing services than does resale, but it

may

result in lessflexibility to add

new

services than does full facilities ownership.The

unbundlingdecision cannot be

made,

however, without consideration ofhow

it affects anincumbent's incentive to invest in

new

services. In 2003, theFCC

decided toremove

all unbundling obligations forbroadband

platforms enabledby

thedeployment

offiber-to-the-home(FTTH)

loops.49These

platforms areexpected tocreate a variety of

new

services,which

willcompete

directly withcablebroadband

offerings and the

broadband

offerings providedby

satelliteand

wireless carriers.The

FCC

reasoned thatthethreatofmandatory

unbundling foranew

servicethatrequired a large sunk investment

would undermine

theILECs'

incentive todeployfibernetworks.50

II.

Why

PursueMandatory Unbundling?

In this section,

we

examine

the theoretical underpinnings ofmandatory

unbundling.

We

also survey the rationales offeredby

regulatory agencies insupportof

mandatory

unbundling. In general,mandatory

unbundlingwas

believedto,

among

other items, (1) generate competition in retail markets through greaterinnovation and investment and lower prices, (2) generate greater competition in

wholesale markets,

and

(3) encourage entrants to migratefrom

unbundling tofacilities-based approach.

Because

our focus ison

the benefits ofmandatory

unbundling,

we

do

not consider its regulatory costs, such as the difficulties inimplementation or

compliance

costs for operators.When

consideringunbundling,a regulator also should take account of a full range ofefficiency considerations,

includingallocative

(consumer

welfaregains associatedwithgreaterpenetrationatlowerprices),productiveefficiency(producersurplus associatedwithreductionsin

marginal costs),

and

dynamic

efficiency(how

welfare is generated anddistributedovertime).

A. Rationale 1:

Competition

inRetailMarkets

Is DesirableIn a static

model

that does not consider investment in future periods,consumers

benefit from

mandatory

unbundlingtothe extentthat such regulation lowersretailprices. In a

dynamic

model,mandatory

unbundling at regulatedrates runs theriskof decreasing investment

by

bothILECs

(by truncating returnsby

granting a 'free48. FCC, High-Speed ServicesforInternetAccess: Status asof30 June 2003,attbl.5 (rel.22

December 2003) (available at

http://www.fcc.gov/Bureaus/Common_Carrier/Reports/FCC-State_Link/IAD/hspd1203.pdf)[hereinafter

FCC

High-SpeedServices]49. SeeTriennialReview,above n8, at10.

50. Ibidat 125 f200('As explainedmorefullybelow,thisunbundling approach

—

i.e.,greater

unbundling for legacy copper facilities and more limited unbundling fornext-generation network

facilities

—

appropriatelybalancesourgoalsofpromotingfacilities-basedinvestmentand innovation againstourgoalofstimulatingcompetitioninthemarketfor localtelecommunicationsservices.').12

Hausman

and Sidakoption' to

CLECs)

51 andCLECs

(by increasing the relative return ofUNE-based

entry).Despite these factors, proponentsarguedthatthe netofeffect of

mandatory

unbundling

was

toincreaseinvestmentby

bothILECs

andCLECs.

1. Innovationand Investment

According

to its proponents,mandatory

unbundling at regulated rates encouragesinnovation and investment on behalf ofboth incumbents andentrants. In its Third

Order

implementing theTelecommunications

Act, theFCC

explained that apositive by-product of

mandatory

unbundling atTELRIC

was

greater innovationon behalf ofentrants

and

incumbents:Unbundling rules thatencourage competitors to deploy their

own

facilities inthe long run will provide incentives for both incumbents and competitors to

invest and innovate, and will allow the Commission and the states to reduce

regulationonceeffective facilities-basedcompetitiondevelops.52

The

more

competitorsinthe market, theFCC

reasoned, the greater the incentivetointroduce a

new

technology to gain a technological edge.With

the correctincentivesinplace,theneed forwholesaleregulation

would

disappear:The unbundling standards

we

adopt in this Order . . . seeks [sic] to createincentives forbothincumbents andrequesting carrierstoinvest andinnovatein

new

technologiesbyestablishingamechanism bywhichregulatory obligationsto provide access to network elements will be reduced as alternatives to the

incumbentLECs'network elements

become

availableinthefuture.53With

greater facilities-based investment, theFCC

reasoned, the market could oneday berelied

upon

todisciplineILEC

prices for local services.Although

itwas aware

ofarguments thatmandatory

unbundling at regulatedratesmight discourage

ILEC

investment, theFCC

believedthatotherfactors inthemarketplace

would

mitigatethesenegativeeffects:We

acknowledge that the incumbentLEC

argument that unbundlingmay

adverselyaffectinnovationisconsistentwitheconomictheory,butevents inthe

marketplacesuggestthatotherfactors

may

bedrivingincumbentLECs

to investin

xDSL

technologies,notwithstandingtheeconomictheory.54For example, investment

by

cablecompanies

incablemodem

servicewas

believedto be sufficient motivation for

ILECs

to invest inDSL

facilities.Although

thenegative investmenteffects might not

overcome

these other factors, itis not clearhow

mandatory

unbundling at regulated rates actually increases investmentby

ILECs.

One

theory isthat anILEC

would

have to respondto greatercompetition fromCLECs

by

investing innew

facilities. But to the extent that thosenew

investments

would

be subjectto unbundlingrules, thoseinvestments might notbe51. See Jerry A. Hausman, 'Valuation and the Effect of Regulation on

New

Services inTelecommunications',Brookings PapersonEcon.Activity: Microeconomics(1997).

52. See ThirdOrder,aboven 17, atH7.

53. IbidatH9n. 12

November

2004 Did Mandatory Unbundling AchieveItsPurpose? 13undertaken.55

Another

theory is that theILEC

will invest innew

accesstechnologiesthatpotentiallywill notbesubjecttounbundlingrules.

2. Prices

and

RetailMargins

When

aCLEC

obtains an access line at incremental cost, it is free to charge theenduser an

amount anywhere between

the incremental cost andthe retail price.A

CLEC

can chargebelow

incremental costifitcanbundletheaccess line withotherservices such as vertical services or long distance. Competition

among

CLECs

ispredicted in theory to discipline

CLECs

in their pricing behavior. Ifcompetitionamong

CLECs

is intense, then the retailprice offeredby

CLECs

shouldequal theaccess price for the

unbundled

loop plus the incremental cost of other inputs.Finally,

ILECs

must

respond to price cutsby

CLECs

with theirown

price cuts.The

equilibriumoutcome

ofthatgame

islowerprices.The

FCC

believedthat theTelecommunications

Act

encouragedtheagencytopromote

retailpricecompetition throughmandatory

unbundling:[T]he 1996 Actsetthe stage fora

new

competitiveparadigm inwhichcarriersin previously segregated markets are able to compete in a dynamic and

integrated telecommunications market that promises lower prices and more

innovative services toconsumers.56

Even

if themandatory

unbundling atTELRIC

never led to facilities-basedcompetition, the

FCC

reasoned,consumers

would

be better offto the extent thatprices for local services declined:

National requirements forunbundling allow [sic] requesting carriers, including

small entities,to take advantageofeconomiesofscale in network. Requesting

carriers, which

may

include small entities, should have access to the sametechnologies and economies ofscale and scope available to incumbent LECs.

Having such access will facilitate competition and help lower prices for all

consumers,including individualsandsmallentities.

57

Because

ILECs

enjoyeda costadvantage vis-a-visCLECs,

theFCC

argued, itwas

preferable

from

a social welfare perspective for retail prices to be basedon

theILECs'

costsand

noton

theCLECs'

costs.Because

ILECs

are subject tostate-sponsored price regulation, it

was

not clear that priceswould

decrease absentsubsidized

UNE

rates.Although

theFCC

was

concerned about stimulating retailcompetition for local telephone and

broadband

access services,most European

regulators focused exclusively

on

stimulating retail competition inbroadband

markets.

55. See

AT&T

Corp.v.IowaUtilitiesBd.,525U.S.366(1999) (Breyer,J., concurringinpartanddissenting inpart) ('asharingrequirementmay diminishthe original owner'sincentive tokeep

up orto improve the property by depriving the ownerofthe fruits ofvalue-creating investment,

research,orlabor.').

56. See ThirdOrder,above n 17, at1)2.

14

Hausman

and SidakB. Rationale 2:

Competition

in RetailMarkets

Cannot Be

Achieved

Without

Mandatory Unbundling

Even

ifcompetition in retail markets is desirable, itis still necessary toshow

thatcompetition

would

not occur in the absence ofmandatory

unbundling. In thissection,

we

explain thereasoning articulatedby

unbundling proponents as towhy

natural marketforces cannotdeliver the benefits of competitionin local services.

1.

A

Vertically IntegratedFirm

Generally Prefers ItsOwn

Downstream

Affiliate

In general, a vertically integrated firm prefers retail sales by its affiliated retail

division to sales

by

an unaffiliated retailer. This preference can be reversed,however, ifthe access price exceeds the retail margin.

Much

academic

work

hasbeen dedicated to analyzing the incentives

of

vertically integrated firms todeny

access to key inputs to unaffiliated

downstream

rivals.58 Ifa vertically integratedfirmcan solidify its market

power

in future periodsby

refusingtodeal withrivalsin a

downstream

market, then that firm has an anticompetitive reason for such arefusal to deal.59

A

vertically integrated firm mightalso refuse to deal with otherunaffiliated firmsinthe

downstream

marketasameans

toacquiremarketpower

inthatmarket.60

Although

no

ILEC

prefers unbundlingitsnetwork

elementsata regulatedrateto selling its servicesthroughits

own

retail division,some ILECs

havevoluntarilyunbundled

theirnetwork

elements to rivals at a commercially negotiated rate. Forexample, in January 1995, Rochester

Telephone

implemented

itsown

'Open

Market

Plan' for unbundling network services inNew

York.61Under

theOpen

Market

Plan,Rochester restructured itselfinto anetwork

servicescompany, which

retained the Rochester name, and a competitive

company,

FrontierCommunications

ofRochester,which

theNew

York

Public ServiceCommission

regulated as a

non-dominant

carrier. Rochester providedon

an unbundled,non-discriminatory basis the local loop, switching, and transport functions as a

wholesaler,at discounted(yetvoluntary) priceslower than itsstandardretailrates.

More

recently, duringa periodofregulatory uncertainty dueto litigationin theD.C. Circuit, several U.S.

ILECs

entered into voluntary agreements withCLECs

for

unbundled

access. In April 2004, BellSouthannounced

that it had signedcommercial

agreements with DialogicaCommunications,

Inc., InternationalTelnet, and

CI2

for pricingofand access to BellSouth's incumbent network.52 Inthe

same

month,AT&T

offered itsown

proposal for voluntary agreements.6358. See, e.g., Michael H. Riordan/Steven C. Salop, 'Evaluating Vertical Mergers:

A

Post-Chicago Approach', 63 Antitrust L. J. 513 (1995); J. Gregory Sidak/Robert W. Crandall, 'Is

StructuralSeparationofIncumbentLocalExchangeCarriersNecessaryforCompetition?', 19YaleJ.

Reg. 335(2002).

59. Dennis W. Carlton, 'A General Analysis of Exclusionary Conduct and Refusal to Deal:

Why

AspenandKodakAreMisguided'. 68AntitrustL.J.669 (2001).60. Ibid

61.

FCC

NewsRelease,Rochester TelephoneCorporationGrantedRule WaiverstoImplementits Open Market Plan, 7 March 1995 (available at http://www.fcc.gov/Bureaus/Common_Carrier/

News_ReIeases/1995/nrcc5030.txt).

62. TRDaily,29April2004,*1

November

2004 Did Mandatory Unbundling AchieveItsPurpose? 15

AT&T

suggestedthat thecommercial

rates be basedon

AT&T's

averageUNE-P

per-linecostinaparticular state as of

March

1,2004.64

According

to Deutsche Bank,AT&T

was

prepared in2004

to settle formonthly

costs $1 to $4 higher than its then-current rates determined underTELRIC,

implying an increasefrom $14

to $15 tonearer$17

to$18

per linepermonth.65BellSouth's

May

2004

offertoCLECs

would

providethatthetopend

forUNE-P

rateswould

not increaseby

more

than $7 permonth

above

rates then inplace.66 In April 2004,

SBC

offered allCLECs

access to theunbundled network

element platform

(UNE-P)

in its 13-stateincumbent

region fora fixed rate of$22

per

month

through theend of

2004.67 In thesame month,

Verizon offered allCLECs

arate of$20

to$24

per linepermonth,which

exceededitsthen-regulatedaverage

monthly

rateby

$1.50to$5.50.6SThese

voluntary negotiationswere

largely in response to the regulatoryvacuum

createdby

theD.C. CircuitvacaturoftheFCC's

TriennialReview

Order,which remained

in effect until June 15, 2004. In addition, federal regulatorsand

the

Bush

administrationhave

urged theRBOCs

and

such rivals asAT&T

tonegotiate access rates

on

theirown.

69On

August

20, 2004,theFCC

releasedasetof stop-gaprules thatrequired the

RBOCs

tocontinueleasingtheir lines toCLECs

atregulatedrates for sixmonths.70

As

ofthiswriting, theFCC

isdraftingnew

rulesfor governing access to local

phone

networks,which

should encourage facilities-based entry overUNE-based

entry.On

October 12, 2004, theSupreme

Court declinedtohearcases filedby

AT&T

Corp.,MCI

Inc., and anassociation ofstateutility regulators seeking to reinstate the original unbundling rules.71 Ifthe

FCC

cannot

meet

the six-month deadline, theRBOCs

would

be free to increase accessrates

by

asmuch

as 15 percent forexisting customerswho

purchase their servicethrough

CLECs.

2. EntryBarriersPrevent Natural Competition

In the United States, a

CLEC

is considered 'impaired'when

lack ofaccess to anincumbent

LEC

network

element poses a barrier to entry that is likely tomake

entryinto amarket 'uneconomic.'72Inits Triennial

Review

Order,theFCC

offeredthe following factors that contribute to entry barriers in the provision of local

telephone service: (1) scaleeconomies, (2) sunk costs, (3) first-moveradvantages,

(4) absolute cost advantages, (5) and barriers within the control of

ILECs.

7jThe

FCC's

explanation ofsunk

costs providessome

insight as to the regulator'sdecision-making:

Sunk costsincreasea

new

entrant'scost offailure. Potentialnew

entrantsmay

also fear that an incumbent

LEC

that has incurred substantial sunk costs willdroppricesto protectits investment in thefaceof

new

entry. In addition, sunk64. Ibid

65. DeutscheBankSecurities,

AT&T

Corporation,30April2004,at1.66. TRDaily, 5

May

2004,*167. TRDaily,20April2004,at *1 .

68. Comm.Daily,22April2004,*1

69. See,e.g.,JamesS.Granelli,,LA. Times,4

May

2004,CI70. See,e.g.,YukiNoguchi,,Wash.Post,21August2004,E2

71. See,e.g.,HopeYen,,Wash. Post,\2October 2004,*1

72. SeeTriennialReview,aboven8,at 9.

16

Hausman

and Sidakcostscan givesignificant first-moveradvantagestotheincumbent

LEC,

whichhasincurred these costs over

many

yearsand hasalready hadtheopportunitytorecoup

many

ofthese coststhroughitsrates.74

According

to itsproponents,mandatory

unbundling isnecessarytoovercome

suchbarriers.

The

corollary ofthis proposition is that, withoutmandatory

unbundling,facilities-basedinvestmentcannotoccur. Inits

May

2002

decisionvacating certainportions of the

UNE

Remand

Order, the D.C. Circuit concluded that theCommission

had

failed to adequately explainhow

a uniform national rule forassessing impairment

would

help to achieve the goals ofthe Act, including thepromotion offacilities-based competition. In particular, the Court stated that '[fjo

rely

on

cost disparitiesthat are universal asbetween

new

entrantsand

incumbentsin

any

industry is to invoke a concept too broad, even in supportof

an initialmandate, to be reasonably linked to the purpose of the Act's unbundling

provisions.'75

Opponents

ofmandatory

unbundling also cite the largesunk

cost of theILEC's

network, but for different reasons.They

argue that sunk costs imply thatregulators should abstain

from

appropriating the quasi-rents ofILECs,

which

undermines the incentive of

ILECs

to invest innew

technologies.76They

alsoargue that, tothe extent that

network

investment cannot be directedtoward other usesin theeventoflow

marketdemand,

largesunkcostsrequirethataccess pricesare set higher than

what

would

otherwisebe necessaryto induce investmentundera standard presentdiscounted valuecalculation.77

C. Rationale 3:

Mandatory Unbundling

Enables

Future

Facilities-BasedInvestment

Access-based competition is supposedly the stepping stone to facilities-based

competition. This proposition, or hypothesis, lies at the heart of regulatory

decisions on unbundling and access pricing that the

FCC

and

its counterparts inothernationshave

made

since themid

1990s.To

put themattermore

precisely,thequestionis whetherregulated access-based entry is asubstitute foror

complement

to the

same

firm's subsequent sunk investment in facilities. Figure 2 provides agraphical depiction of one possible rendition ofthe stepping-stone or 'ladder of

investment'thesis.

74. Ibid

75. SeeUSTA,aboven8, at427 (emphasisinoriginal).

76. Fora descriptionoftheroleofsunkcosts inaccess pricingand unbundling, see generally Hausman

&

Sidak,above n2.November

2004 DidMandatory Unbundling AchieveItsPurpose? 17CLECs

cross-priceelasticityof investmentin facilitieswith respectto access-basedentryFigure

2:The

Metamorphosis of Access-Based

Entry

from

Complement

to SubstituteCLECs

cumulative useof access-basedentry

over time

In the telecommunications industry, the

examples

of the stepping-stonehypothesis are

numerous.

For example,MCI

successfullymade

thetransitionfromreseller oflong-distance services tofacilities-based carrier.

The

leasingofselectedunbundled

elements at regulated prices is vigorously defendedby

CLECs

and

regulators asa

complement

tosubsequentfacilities-based entry,not asubstitute forit. Within the strata of regulated access-based entry options, regulators

may

consider

UNE-P

to be a stepping stoneto aCLECs

subsequent investment in itsown

switchesand

itsmore

limited relianceon

unbundled localloops.78In implementingthe unbundling rules, the

FCC

soughtto follow the intent of Congressby

creating an intermediate phase ofcompetition, duringwhich

some

new

companies

would

deploy theirown

facilities tocompete

directly with theincumbents:

Although Congress did not express explicitly a preference for one particular

competitive arrangement, it recognized implicitly that the purchase of

unbundled network elements would, at least in some situations, serve as a

transitionalairangementuntil fledgling competitorscould develop a customer

baseand completetheconstructionoftheir

own

networks.79The

FCC

thus sought to force the incumbents to allow others to access theirsystems, in the

hope

thatmandatory

unbundlingwould

create competitorswho

would

laterinvestin theirown

facilities.Inthelongrun, the

FCC

expectedthatentrantswould

buildtheirown

facilities because doingsowould enhance

the entrants' ability tocompete

more

effectivelywithincumbents:

78. Similarly, regulatorsmayconsidermandatoryroamingatregulated pricestobeastepping stonetoa wirelesscarrier'seventualinvestmentinbasestationsand spectruminanothergeographic

region. However, a component ofthe relevant infrastructure is radio spectrum, the allocation of

whichiscontrolledbythegovernment(atleastintheprimarymarket). Consequently,itisnot clear

wherethestepping stoneofmandatedaccess leadsinwireless.

1

8

Hausman

and SidakWe

fully expect that over time competitors will prefer to deploy theirown

facilitiesinmarketswhere itiseconomicallyfeasible todoso,becauseitisonly

throughowningand operatingtheir

own

facilitiesthatcompetitorshavecontrolover the competitiveand operational characteristics oftheir service, and have

the incentive to invest and innovate in

new

technologies that will distinguishtheirservicesfromthoseoftheincumbent.80

Thus,

mandatory

unbundlingwould

allowentrantsto deriverevenuefrom

offeringservices over the

unbundled

network elements, and then use that revenue toconstruct their

own

networks oncethe technology shifted.Of

course, ifthe accessrate

were

settoo low, thetransition to facilities-based competitorwould

not occur,as

CLECs

would

never find it intheir interests to invest intheirown

facilities. Ifaccess rates

were

setjustright,thistransition tofacilities-basedcompetitionwould

generate additionalsocial benefits,

which

aredescribedinthenextsection.D. Rationale4:

Competition

inWholesale

AccessMarkets

Is DesirableCompetition in the input markets was,

by

itself, desirable. In this section,we

review

how

input-level competition can, in theory, generate technologicalinnovation and incentives for gains in productive efficiency

and

can eventuallyleadtoregulatorywithdrawal.

1.

A

Network

ofNetworks

Facilities-based entry

by

CLECs

in the current periodmeant

that future entrantswould

not have todepend

exclusivelyon

ILECs

to obtain network elements.The

FCC

believedthatmandatory

unbundlingwould

expeditethis process:Moreover, in

some

areas,we

believethatthe greatestbenefitsmay

beachievedthroughfacilities-basedcompetition,andthattheabilityofrequestingcarriersto

useunbundlednetworkelements, including variouscombinations ofunbundled

networkelements, isanecessary precondition tothesubsequentdeploymentof

self-provisionednetworkfacilities.81

Intheory, facilities-based entry generates 'greater benefits' than

UNE-based

entrybecause the former signals a credible

commitment

to stay in the market. If anentranthas not

made

sunk investments in infrastructure, itcannotusesunk costs tomake

thatsignal.Nor

willthe incumbent face theprospectofdurable capacitythatsurvives the demise ofthe

company

that investedtocreate it. Moreover,facilities-based competition leads to technological diversity,

which

increases choice andmay

providenewer and

better services because theCLEC

does notdepend

on alegacynetwork.

The

FCC

envisioned that facilities-based entrantswould

spawn

anew

generation of

UNE-based

entrants,who

in subsequent periodswould

become

facilities-basedentrants:

In orderfor competitive networksto develop, the incumbent LECs' bottleneck

control over interconnection must dissipate.

As

the market matures and thecarriers providing services in competition with the incumbent LECs' local

80. Ibid,atH 7

November

2004 Did Mandatory Unbundling AchieveItsPurpose? 19exchange offeringsgrow,

we

believethese carriersmay

establish directroutingarrangements with one another, forming a network of networks around the

currentsystem.82

Thus, the

FCC

believed thatmandatory

unbundlingatTELRIC

would

evolve intovoluntary access arrangements.

Under

thisscenario,some

facilities-based entrantsmight chooseto

become

a purewholesalerofnetwork

elements, leaving the retailcomponent

tootherCLECs.

2. Regulatory

Withdrawal

Competition

among

facilities-basedproviderstosupplynetwork

elementstofuturegenerations of

CLECs

would

decrease the price ofthosenetwork

elements.The

nextgeneration of

CLECs

would, inturn, pass thosesavings alongto end users inthe

form

of lowerretailprices.At

some

point inthe process, the regulator could, intheory,

withdraw

and allowa competitivemarket

forinputs to discipline the priceofretailservice.

In practice, however, regulators are reluctant to relinquish their

power

tocontrol entry and allocate rents in a given market. This vision of

mandatory

unbundling also ignores the strategic use ofregulation

by

competitors.Given

thelarge rents at stake,it isnot realisticto believethattheregulatory machinery could

be dismantled very easily.Indeed, intheUnited States,thedegreeofregulationhas

increased since thepassage ofthe

Telecommunications

Act

of1996.83E.

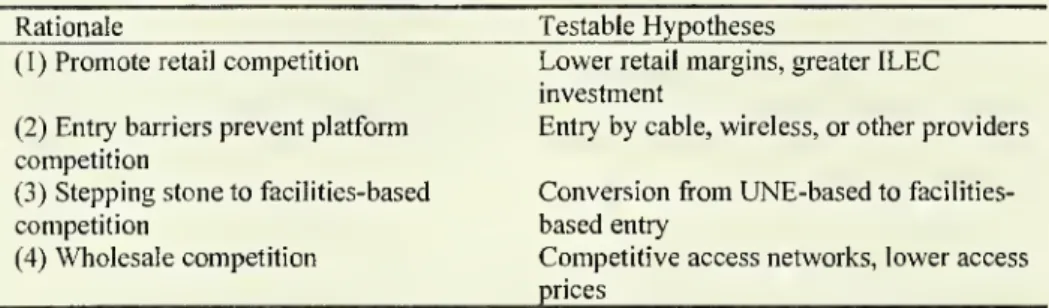

Conclusion

In

summary, mandatory

unbundlingwas

basedon

the following rationales: (1)competition in retailmarkets is desirable, (2) competition in retail markets cannot be achieved without

mandatory

unbundling, (3)mandatory

unbundling promotesfuturefacilities-basedinvestment, and (4)competition inwholesaleaccess markets

isdesirable. Fortunately, thereistestablehypothesisassociatedwitheachrationale.

Table 1

shows

thefourrationalesandtheirassociatedtestablehypotheses.82. Ibid, at 1 7 n. 12 (quoting Promotion of Competitive Networks in Local

Telecommunications Markets, Notice of ProposedRulemakingand Notice ofInquiryin

WT

Dkt.No.99-217 and Third Further Notice of ProposedRulemakingin

CC

Dkt.No.96-98,FCC

99-141,Iffl4,23(rel.7 July 1999)).

83. See,e.g.,J.GregorySidak,'TheFailureofGoodIntentions:TheWorldComFraudandthe

CollapseofAmericanTelecommunicationsAfter Deregulation',20 YaleJ.Reg.207 (2003) (showing

thattheaverage

FCC

appropriations increasedfrom $158.8million per yearin 1981-1995to$211.620

Hausman

and SidakTable 1: Rationalesfor

Mandatory Unbundling and

AssociatedHypotheses

Rationale TestableHypotheses

(1)Promoteretailcompetition

Lower

retailmargins,greaterILEC

investment(2)Entrybarrierspreventplatform Entrybycable,wireless,orotherproviders

competition

(3)Steppingstonetofacilities-based Conversionfrom

UNE-based

tofacilities-competition basedentry

(4)Wholesale competition Competitiveaccessnetworks,loweraccess

prices

Ifcompetition

among

CLECs

is robust (rationale 1 ), thenCLEC

margins shoulddisappear

and

consumers

should enjoy lower retail prices. Ifmandatory

unbundling is truly necessary for retail competition (rationale 2), then entry

barriers should prevent any firm

from

constructing arival platform. Ifmandatory

unbundling is a stepping stoneto facilities-based investment (rationale3), then

we

should observeindividual

CLECs

transitioningfrom

UNE-based

to facilities-basedapproaches over time. Finally, if

mandatory

unbundling promotes wholesale competition(rationale4), thenwe

should observefacilities-basedCLECs

acting aswholesalers of

network

elements. In the next section,we

use this analyticalframework

to assess theunbundling experience in fiveseparate countries.Because

mandatory

unbundling isarelatively recentphenomenon

inthe countriessurveyed,we

donotexamine

empirically whetherregulatorywithdrawalhas occurred.III.

The

Unbundling

Experience inFive CountriesThe

previous section consideredhow

mandatory

unbundling shouldwork

intheory.

With

the benefit of several years of experience,we

turnnow

to anevaluation ofthe extent to

which

the rationales formandatory

unbundlingwere

substantiated inpractice.

We

focus on the unbundling experience in the UnitedStates, the United

Kingdom,

New

Zealand, Canada, andGermany.

For eachcountry,

we

examine

whether any ofthe four primary rationales formandatory

unbundling at

TELRIC

was

substantiated in practice.We

relyon

datafrom

therelevantregulatoryagencythat

implemented

the unbundlingregime. Forexample,we

discusswhy

regulators inNew

Zealand did not adoptmandatory

unbundling.Each

section concludes with a review ofthe state offacilities-based competitionforlocaltelephone serviceasofearly2004.

In compilingthe country surveys,

we

observed a large variation inthe degreeto

which

economic

analysis informed the regulator's decision-making process. IntheUnited States, forexample, theprocess

was

informed by legal interpretationof

specific language (such asthe

meaning

of'impaired') orby engineering measuresof hypothetical operating costs. In

New

Zealand,by

contrast, the processwas

informed largely by

economic

analysis andby

international experience withmandatory

unbundling.Using

economic

methods, theNew

Zealand regulatorliterally assigned netwelfare gains toeach regulatory option and selected thepath

with the greatest net welfare gain.

To

be fair,New

Zealand had the benefit ofstudyingthe experienceofother nationsbeforeitdecidedontheoptimal regulatory

November

2004 DidMandatory Unbundling AchieveItsPurpose? 21despite the fact that the United States

now

hasmore

than six years of unbundlingexperience.

A.

United

StatesThe

Telecommunications

Act of 1996 ordered theFCC

to introduce competitioninto the local services market by forcing

ILECs

to provide entrants access to theILECs'

existing facilities at regulated rates. In 1999, theFCC

explained thatCongressdid notprovidetheagency

much

flexibilityintheexact form ofmanaged

competition: 'Congress directed the

Commission

toimplement

the provisions ofsection 251, and to specifically determine

which

network elements should beunbundled

pursuant to section 251(c)(3).7'84 Hence, theFCC

did nothave

thediscretionto rejector

embrace any

oftherationales formandatory

unbundling.The

only decisions left to the

FCC

concerned the extent ofmandatory

unbundling—

namely,

which

elementswould

be included inthe listofUNEs

and

theappropriatepricingofthose elements.

1. RetailCompetition

In this section,

we

review the unbundling experience in the United States withrespecttoretailpricingandinvestment.

a. Pricing

Retail competition triggered

by

mandatory

unbundling should manifest itself interms of lower retail prices.

Even

if price regulation of local servicesby

statePUCs

were

binding, the introduction ofUNE-based

competitioncould still reduceprice. In the United States, however,

mandatory

unbundling does not appear tohave decreased local service prices measurably

—

despite the fact thatCLECs

had

more

than 13 percent ofthe nation's access linesby

2003. Figure 3shows

theBureau

ofLabor

Statistics'(BLS)

Consumer

Price Index for local telephoneservices