JV

14r

CEO PAY

AND

FIRM

PERFORMANCE:

DYNAMICS, ASYMMETRIES,

AND

ALTERNATIVE

PERFORMANCE

MEASURES

Paul L. Joskow

Nancy

L. RoseMassachusetts Institute of Technology

DYNAMICS, ASYMMETRIES,

AND

ALTERNATIVE

PERFORMANCE MEASURES

Paul

L.Joskow

Nancy

L.Rose

MIT

and

NBER

;/;assachusettsinstiiute

OFTECHNOLOGY

MAY

3 1995LIBRARIES

First draft:

March

1994

This

revision:December

1994

We

thank CatherineWolfram

for superb research assistance, and theMIT

Center for Energy and Environmental PolicyResearch andtheNational ScienceFoundation forfinancial support. Rose gratefullyacknowledges

fellowship support fromthe Center forAdvanced

Study inthe Behavioral Sciences.We

appreciate thecomments

of seminar participants atUCLA.

DYNAMICS,

ASYMMETRIES,

AND

ALTERNATIVE

PERFORMANCE MEASURES

Paul L.Joskow

Nancy

L. RoseDecember

1994

ABSTRACT

This study explores the

dynamic

structure of the pay-for-performance relationship inCEO

compensation and quantifies the effectof introducing a

more complex model

offirm financialperformance on the estimated performance sensitivity ofexecutive pay.

The

results suggest thatcurrent compensation respondstopastperformanceoutcomes, but that the effectdecays considerably withintwo

years. This contrasts sharply with models of infinitely persistent performance effects implicitlyassumed

inmuch

ofthe empirical compensation literature.We

findthatbothaccounting and market performance measuresinfluence compensation andthat the salary and bonus

component

of pay as well as total compensation havebecome

more

sensitive to firm financial performance over the past

two

decades. There is no evidence that boardsfailto penalizeCEOs

forpoor financial performance orrewardthem

disproportionately well for good performance. Finally, the data suggest that boardsmay

discount extreme performance outcomes--both high and low-relative to performance that lies withinsome

The

relationshipbetween

firmperformance and

executivepay

hasbeen one

ofthe

most

widely studied questions In the executivecompensation

literature.^A

substantial theoretical literaturedevelops

optimal executivecompensation

contracts that linkpay

to variations in firmperformance

as ameans

of aligning the incentives ofmanagers

(the "agents") with the interests ofshareholders (the "principals"). Thistheoretical literaturehas

spawned

numerous

empirical tests ofthe presence,form and

strength of the relationship

between

executivecompensation

and

firm financialperformance.

The

desirability of "incentive pay"based

on

firmperformance

hasbecome

so widelyaccepted

that itwas

written into recent reforms in the corporateincome

taxcode

intended toreduce

or limit overallCEO

pay. EffectiveJanuary

1,1

994,

executivecompensation

inexcess

of $1 million per yearis not deductible as anexpense

for corporateincome

taxpurposes

unless It isbased on

objectivemeasures

of

firmperformance

(sec. 162(m)).^As

atheoretical matter, the preciseform

of the optimalcompensation

contractis complicated (Rosen, 1992). In general, it will

depend

on such

factors as the preferences ofmanagers

toward

risk, the sensitivity of managerial effort tocompensation, and

the informationon

true managerialperformance

providedby

themeasures

of firmperformance

that are observable byboards

of directors. Empiricalanalyses of the pay-for-performance relationship in contrast tend to

employ

quitesimple specifications of

how

firmperformance

influencescompensation.

These

specifications vary across a

number

of dimensions, including the choice of stock' See Rosen (1992) for an overview of both

the theoretical and empirical literature onthis

subject.

^ This revision to the tax code

was

itself a response to political pressures resulting from widely-readpopular commentariesthatarguedthat

many CEOs

areovercompensated andpaidmarket

oraccounting

performance

measures,

thedegree

towhich

performance

sensitivities are

assumed

to be constant across allCEOs

and

firms or are allowed to vary withsome

set of observable factors, theassumed

functionalform

of thecompensation-performance

relationship,and

the use of absolute returns or returnsrelative to

some

referencegroup

of similar firms.There has been

little effort to standardize specifications acrossempirical studies, oreven

tocompare

results acrossalternative specification choices.^

This

paper

has

two

primary objectives. First,we

examine

how

more

complex

measures

of firmperformance

affectthe estimatedpay

forperformance

relationship.In this analysis

we

allow firmperformance

tobe

measured

by

a vector of indicators that includesboth

market

returnand

accounting

returnmeasures

of financialperformance,

allows the sensitivity ofpay

toperformance

tochange

over time,and

allows the

performance

sensitivity todepend

on

how

good

orbad

the firm's financialperformance has

been.We

believe that this richer specification of firm financialperformance

is essential given that traditionalmeasures

necessarily are noisy signalsof underlying managerial

performance.

A

broader setofmeasures

is likely to provide a better signal of managerialperformance

thandoes

a single unidimensionalperformance

measure,

and

appears

to accordmore

closely with institutionaldescriptions of the

compensation process

(seeMilgrom and

Roberts,1992,

chapter 13).Our second

objective is to explore thedynamic

structure of thepay-for-performance

relationship.A

variety of different functionalforms has

been

used

in theliterature,

embodying

quitedifferent implicitassumptions about

the persistenceof firmperformance

effectson

executive pay.At

one

extreme

are specifications thatassume

^ Gibbons and

Murphy

(1990) provide one of thefew

analyses that report results fordifferent functional forms, but even their study focuses on choosing one form (using a

minimum

least squares based criterion), rather than on interpreting the differences in the results.3

no

memory

in thecompensation

process. Currentcompensation

is influencedby

current

performance

only; past financialperformance has no

impact.At

the otherextreme

are specifications thatassume

complete

persistence: currentcompensation

is

determined

by

current financialperformance

and

all previousperformance

realizations, with all realizations

weighted

equally/Few

authorshave

acknowledged

the implication ofthese differing assumptions,

and

this paper, along withindependent

work

by

Boschen

and Smith

(1994) isamong

the first to testthem

explicitly.^Our

empirical analysis relieson

data for 1009

CEOs

in678

firms over the 1970

through 1

990

period. It leads to the following general conclusions:1

CEO

compensation

became

significantlymore

sensitiveto firmperformance

during the

1980s compared

to the1970s, even

when

those portions of executivecompensation

derivedfrom

stock optionsand

related instruments are excluded.2.

CEO

compensation

is influencedby both accounting

profitsand

shareholderreturns.

Our

resultssuggest

that boards of directors treateach

of theseperformance

measures

as a useful independent signal of managerial performance. During the1980s,

a givenpercentage

point increase inaccounting

returns yields three to fourtimes the

average

overallcompensation

increasegenerated by

thesame

percentage

* That

is, agiven return realization hasthe

same

effecton current compensation whetherit reflects the current return or the return 10 years ago.

^ Since completing our original analysis for this paper,

we

have discovered a study that independently addresses this topic (our thanks to the Financial EconomicsNetwork

for itsdissemination of working paper abstracts!).

Boschen

and Smith (1994) use a vector autoregressive approach that relates the level of current compensation (in logs; either salary and bonus or total compensation) to current and past financial performance (measured by stockmarketratesof return) andlagged compensation, and the level of financialperformance tocurrent andpastcompensation and laggedfinancialperformance. Their analysisuses3lagsin both compensation and marketrates of return. Their estimates, based ondata for 16firms

over the

1948-1990

period, yield thesame

general conclusions as our results. Pastperformance appearsto have a significant influence on current compensation, butthe effect

is not permanent. Their study also indicates changes in performance sensitivity of pay

over

the 4 decades spanned bytheir data, although the relatively small size of their cross section

point increase in

market

returns, although thisappears

tobe

due

at least partially tothe smaller variance of

accounting

returns. For our overall sample, aone

standard deviation increase inaccounting

returns leads to roughly twice thecompensation

increase of a

one

standard deviation inmarket

returns. Failing to includeboth

accounting

and

market

returnperformance

measures

in thecompensation

equationsubstantially

underestimates

the overallimpact

of financialperformance on

CEO

pay. 3. Past financialperformance,

in addition tocontemporaneous

performance, has an importantimpact on

currentCEO

compensation.

During the1980s,

thecontemporaneous compensation

effect of an increase inmarket

return is less thanforty percent of the

cumulative compensation

increase, all else equal. For accountingreturns, the

contemporaneous

effect is roughly sixty-five percent of the overallcompensation

response.The

impact

is not infinitely persistent,however,

as implicitlyassumed

inmany

previous studies.Our

findingssuggest

that neither ofthe functionalforms

most

common

in the executivecompensation

literature accurately captures the temporal structure of the pay-for-performance relationship.4.

The

data provide virtuallyno

support for the popularview

thatboards

failto penalize

CEOs

forpoor

performance

orreward

them

disproportionately well forgood

performance.

While

much

of the increased sensitivity ofpay

toperformance

inthe

1980s

appears

due

to an increase in therewards

for positiveperformance,

thisgenerallyhas

brought

theresponse

of executivepay

togood

and bad performance

intorough

symmetry.

5.

There

issome

evidence

thatboards

discountextreme

realizations ofperformance-both

highand

low-

relative toperformance

that lies withinsome

"normal"

performance

band. This could be consistent, forexample,

withtheview

thatextreme

performance

realizations are noisyoutcomes more

likely tobe

due

to eventsbeyond

the influence or control ofmanagement,

or with efforts to limit theextreme

The

paperproceeds

as follows. In section II,we

discuss the choice of anempirical specification of the pay-for-performance relationship. Section III describes

the data

and

oureconometric

model

ofCEO

compensation.

Results are presented insection IV, followed

by

a brief conclusion.II. Empirical

Models

of the Pay-for-Performance RelationshipAn

extensiveempiricalliteratureinvestigatesthesensitivityoftop executivepay

to variations in firm performance.

Rosen

(1992) provides anoverview

ofmany

of these analyses; Sloan (1993) provides additional references to the accountingliterature

on

this topic.We

have

identified fourdimensions

alongwhich

empirical analyses tend to vary.These

are: 1)The

choice ofperformance

measure

(accounting-based, stock market-based, or both); 2)

Whether

performance

sensitivities are restricted to be the

same

or are allowed to vary across firms; 3)The

functionalform

of the compensation-return specification;and

4)The

use

of absolutereturns or returns relativeto otherfirms inthe

same

industryor overall market.To

the best of ourknowledge,

the literature is uniform in imposingconstant

performance

coefficients over time^

and

estimating a constantperformance

slope over the entirerange

of thechosen performance measure.

We

describebelow

each

of thesedimensions

ofthe pay-for-performancespecificationand

sketch itsimplicationsforourinvestigation.

1).

Stock-market

v.accounting

performance: In theeconomics

and

financeliteratures,

most

studies of the pay-for-performance relationship focuson

stockmarket-based

measures

of financialperformance

(e.g..Murphy,

1985; Jensen and

Murphy,

1990;

Gibbons and

Murphy,

1990;

Barroand

Barro, 1990; and

Hubbard

and

Palia, 1994). In contrast, studies in the accounting literature typically

use

eitheraccounting-based

measures

offirmperformance,

or includebothaccounting

and

stockmarket

measures

ofperformance

in their analysis (e.g., Antleand

Smith,1986;

Lambert and

Larcker, 1987;and

Sloan, 1993).^While

the appropriate choice ofperformance

measure

is notobvious

a priori, itseems

reasonable to expect bothaccounting

and market

measures

of firm financialperformance

to influencecompensation.

Boards

must

confront the taskof extractinginformation

about

true managerialperformance from

noisy financialperformance

realizations. Both accounting

and

market

returns aredetermined

in partby

factorsbeyond

the control or influence of the firm'smanagers.

To

the extent thatthey

alsoareinfluenced

by

thequality ofmanagerial inputsand

actions,theymay

provideuseful informationon

managerialperformance.

Given

the imperfect correlationbetween

these financial

performance

measures,

the theoretical literaturesuggests

thatcontracting

on

bothmay

enhance

the firm's ability to filter the signal of truemanagerial input (e.g.,

Holmstrom,

1979). Institutional factorssupport

this conclusion, as firmsappearin practicetouse both measures.

Compensation

contractsmost

frequently linkbonuses

toaccounting

earnings (Sloan, 1993)

whilestock-based

forms

ofcompensation,

particularly options grants, tie realizedcompensation

to stockmarket

returns.We

exploremodels

that include bothaccounting

and market-based

measures

in the specification of firm

performance.

2).

Changes

inperformance

sensitivities overtime:Most

studies of executivecompensation

estimate a single return coefficient for a panel of firmsand

CEOs

overtime.

The

primary exceptions are:accounting

studies,which

tend to estimateperformance

slopeson

a firm-by-firm basis (e.g.,Lambert and

Larcker,1987

and

^ Exceptions tothis division byfield are Kaplan (1994),

who

includes both marketreturns and adummy

variable for negative accounting earnings; and Joskow, Rose and Shepard (1993) and Rose and Shepard (1994), discussed below.Sloan,

1993,

who

explorehow

the relativemarket and

accountingperformance

sensitivities vary with their signal-to-noise ratios for

each

firm);Gibbons and

Murphy

(1992),

who

findevidence

thattheperformance

sensitivity ofpay

variesover aCEO's

career;

Schaefer

(1 993),who

developstheoreticaland

empiricalsupportfor aninverserelation

between

performance

sensitivityand

firm size(measured by

dollarchanges

in

compensation on

dollarchanges

inmarket

value);and

Boschen

and

Smith (1994),who

analyzehow

the pay-for-performancerelationshipvariesover 1948-1990

fortheirsample

of16

largecompanies.

In this study,

we

explorewhether

the sensitivity of executivepay

to firmperformance has

been

constant overtime.The

rhetoric ofcorporate proxystatements

and

business press discussions ofCEO

compensation

stronglysuggest

that incentivepay

hasbecome more

visibleand

widespread

over the last20

years.Some

empiricalsupport for this

view

is providedby

thecompensation

levels equations estimatedby

Joskow,

Rose,and Shepard

(hereafter,JRS,

1993),which

suggest

thatperformance

sensitivities for unregulated industries increased steadily

between

1970

and

1990.

To

accommodate

potentialchanges

in the sensitivity of executivepay

to firmperformance,

we

estimate separateperformance

slopes for the1970s

and 1980s.^

3).

Asymmetries

inperformance

sensitivities:We

examine

avarietyofpotentialasymmetries

inthe responsiveness of executivepay

to variations infirmperformance.

Ofparticular interestistheclaim that executive

pay

packages

have

"more

upsidethan

downside

elasticity" (Crystal,1992,

p. 98). Thisargument,

which

has attracted considerable popular attention, suggests that executivecompensation

ismore

sensitive to positive

performance

realizations than to negativeperformance

realizations.

We

test for potentialasymmetries

inperformance

sensitivitiesby

®

JRS

estimated separate slope coefficients overfive-year intervals. While there appearsto be

some

additional variation within decades, the 10-year splits reported in this paper capturemuch

of the differences over time while preservingsome

parsimony in the length ofinvestigating

whether

compensation

is unusually sensitive to very poor financialperformance

(measured by

accounting losses),whether

compensation

responds

more

to

performance

gains than toperformance

losses,and

whether

compensation

responds

differentially toperformance changes

that are withinsome

"normal" range asopposed

to outside that band.4). Functional

form

and

the temporal structure of pay-for-performance: Thisis the

dimension

on

which

empirical studies exhibit the least consistency orconsensus,

even

across differentstudiesby

thesame

author.Common

specificationscorrespond

to regressions ofthe logofcompensation

on

the share price (e.g..Murphy,

1985), dollar

compensation

on

the dollarmarket

value of the firm (e.g.,Jensen and

Murphy,

1990);changes

in the log ofcompensation

on

themarket

rate of return (e.g.,Gibbons and

Murphy,

1 990);and

the log ofcompensation on

the rate of return (e.g.,JRS,

1993).Compensation

equationsmay

be estimated in levels or first differences(changes

incompensation),

inwhich

case bothcompensation

and performance

aremeasured

aschanges

in the described variables. Studies thatuse

both accountingand market-based

returnscommonly

model

changes

in the log ofcompensation

as afunction of the level of

market

returnand

thechange

in theaccounting

return.^These

alternative specifications imply quite differentdynamic

models

of thecompensation

process. Forexample,

amodel

ofchanges

in logcompensation on

thelevel of return implies

complete

persistence in theperformance

component

ofCEO

compensation.

^°A

one-timeshock

to the firm's"normal"

return generates a^See Lambert and Larcker (1 987) and Sloan (1 993)for examples.

Some

of these studiesusethe dollar

change

incompensation, ratherthanthechange

inthe log of compensation, as thedependent variable.The

resultsreported inthispaper all uselog compensation (orits firstdifference) rather than the dollar value of compensation, to limit the potentially

disproportionate influence of observations with extremely high compensation levels.

'° Models that specify compensation to be a function of market value or share price

suggestthatsuperiorfinancialperformance priortothe currentexecutive's tenure increasehis or her current compensation, all else equal.

permanent change

incompensation,

even

asretum

recedes to itsnormal

level insubsequent

years. Alternatively, amodel

ofchanges

in logcompensation

on

changes

in return implies that the relationship

between

compensation

and performance

iscontemporaneous

only.A

one-timeshock

to return generates highercompensation

only in the current period.

Most

models

that relate logcompensation

to returnscan

be nested within asimple

dynamic

model

of the relationbetween

compensation and

firmperformance

over time: t In Compensationi t = 'n

Cq

, , +J^

pj Return j, t - s "^ ^i t *^' s=0where

Cqj, is thebase

(non-performance

related)compensation

forCEO

i in yeartand

RETURN

is themarket

return ineach

year ofCEO

i'stenure (0through

t).An

increaseof X

percentage

points inRETURN

in year (t-s) increasescompensation

in year t by ftgin this model.

The

first differenceform

of thismodel

is:'nCi , - InC i ,.1 = ( InCo ^ , - InCg j, ,., ) + Po ( Returni , - Returni ^^, ) + Pi ( Returnj ,., - Returni ,.2 ) + • . . + p,., ( Returni , - Returni g ) + p, Returni

M

e j , - e ,_ ,., ) (2)If all the return coefficients are equal (Bq

=

fi,=

...=

fi,), thismodel

collapses to a specification that relateschanges

in logcompensation

to the current level of return:(3) ( InC i , - InC ,,,_, ) = ( InC i

, - InC i,,_i ) + Po Return ^ ,

M

e

i

, - e ,,_, )

In this specification, an increase of x

percentage

points inRETURN

inany

yearincreases the

CEO's

compensation

in that yearand

everysubsequent

yearby

x(Jpercent.^^

Alternatively, if current

compensation

is a function ofcontemporaneous

financial

performance

only , then (i^=

Q>2=

=

^^=

0,and

the generalmodel

collapses to a specification that relates

changes

in logcompensation

to the firstdifference in return: ( InC i , - InC i,.i ) = ( InC i , - InC i,.i ) + Po (

Retum

, , - Return i, . , )(4,M

e i t - e i.t-1 )We

explicitly testtheseextreme

specificationsby

nestingthem

within themore

general

model

ofequation (2)and

testingwhether

therestrictions impliedby

either (3)or (4) are satisfied

by

the data.Our approach

allows us todetermine

whether

thecompensation

process

includesany

"memory,"

inthat previous financialperformance

affects current

compensation

levels, as well aswhether

this effectdecays

over time.There

is littlereason

to thinkthatthecompensation-performance

relationshipmust

be

entirely

contemporaneous

or perfectly persistent,^^even though

most

studies in the'^

Note that there is a problem of

asymmetry

in this representation of the notion ofpersistence. Ifthe marketreturn is 10 percent this year and -9.09 percent next year, so that the net

compounded

returnoverthetwo

yearsiszero,compensation ineverysubsequentyearwill be .91)9percent higherthan it would have been if the return

were

identically zero in eachyear.

12

literature implicitly

have

assumed

one

ofthetwo

extremes. Ifexecutivecompensation

depends

on

both pastand

current performance, but thecompensation impact

of pastperformance

decays

over time,we

would expect

to find that the estimated {(i] arenon-zero for

some

period, but decline as firmperformance

recedes further into the past.We

assess

thedynamics

of the pay-for-performance relationship with amodel

that includes current, one-

and

two-year lags in both accountingand

market

returns.^^

4).

Absolute

v. relativeperformance

measures:

A

number

of studies explorewhether

executivecompensation responds

to absolutemeasures

offirmperformance

or to

performance

relative to that ofsome

referencegroup

of firms (e.g., Antleand

Smith,

1985;

Barroand

Barro, 1990;Gibbons

and

Murphy,

1990; Janakiraman,

Lambert and

Larcker,1992; and

Sloan, 1993).Apart

from

Gibbons and

Murphy,

however,

most

studiesconclude

that relativeperformance

evaluation (RPE)tends

toplay a

minor

role in determining executivecompensation.

That

is,compensation

responds

primarily to a firm'sown

return rather than to its return relative tosome

benchmark

group

of firms. Moreover, itappears

thatRPE,

if it operates at all, isstrongest for quite broad reference groups,

corresponding

to 1 -digit SICcode

industries or

perhaps

themarket

as a whole. Finally, the slope of thepay-for-performance

relationshipseems

to be quite robust to the inclusion or exclusion ofreturns for alternative reference

groups

(seeGibbons and

Murphy,

1990). In light of these previous results,and

to limitthedimension

oftheperformance parameter

vectorwe

estimate,we

adopt

a specification that implicitlymeasures

returnand

'^ First-difference models with

two

lagsmay

be estimated only for observations inwhich

the

CEO

has four ormore

years oftenure.We

have experimented with longer lag structures, but these lead to substantial loss in data given the averageCEO

tenure of 7 years in our fulldataset. Forthis reason,

we

restrictthe resultsreported hereto relatively short performancehistories. Because the performance impact on current compensation declines considerably over even the

two

year lagswe

consider, this restriction does notseem

unreasonable.compensation

relative to the overallmarket

(by including individual year effects in theregression model), but

do

not investigate theRPE

hypothesisany

further.'*III.

Data

and

EmpiricalMethodoloqv

We

model

CEO

compensation

as a function of firm scale, firm financialperformance,

CEO

characteristics,and

industryand market-wide

norms

in executivepay.

The

dataused

tomeasure

these variables are describedbelow.

We

next sketch the basic regression model,which

is similar tomodels

used by

JRS

(1993) toinvestigate

compensation

differentials acrossregulatedand

unregulated industriesand

by

Rose

and

Shepard

(1994) to explore the effects of firm diversificationon

compensation.

We

finallysummarize

our tests of thekey

restrictionson

theperformance

sensitivityparameters

of executivepay

that are implicit in this model.Data

Our

database

isdeveloped from

three primary sources. Informationon

CEO

compensation

and

CEO

characteristicswere

obtainedfrom

Forbes' annualCEO

compensation

survey

over1970-1990.

Informationon

firm characteristicsand

accounting profitability

come

from

COMPUSTAT,

and

fiscal year stockmarket

returns arefrom

theCenter

forResearch

on

Security Prices(CRSP)

return files.'^To

reduce

non-comparability across firms

we

exclude those in industries subject toeconomic

regulation

and those

in financial services, usingCOMPUSTAT's

primary SICcode

"*

We

also include aggregated 2-digit SIC industry fixed effects,which

implicitly controlfor industry average performance over the entire sample period (see

JRS

for a description).The

dimension ofthe performance parameter space (K) for ourchosen specification suggests theprudenceofsuppressing anexplicitinvestigation ofRPE

parameters,which

would increase the parameter vector to 2K. In our simpler specifications, K=

10; this increases quickly to K= 20

or K= 30

aswe

relax various restrictions.assignment

to deternnine industry affiliation.^^Because

some

of the specifications thatwe

present include first differences incompensation and up

to two-period lagsin

performance

variables,we

work

with a basicsample

ofCEO-years

forwhich

we

observe

at leastone

prior year ofcompensation and

three prior years ofperformance

data.

These

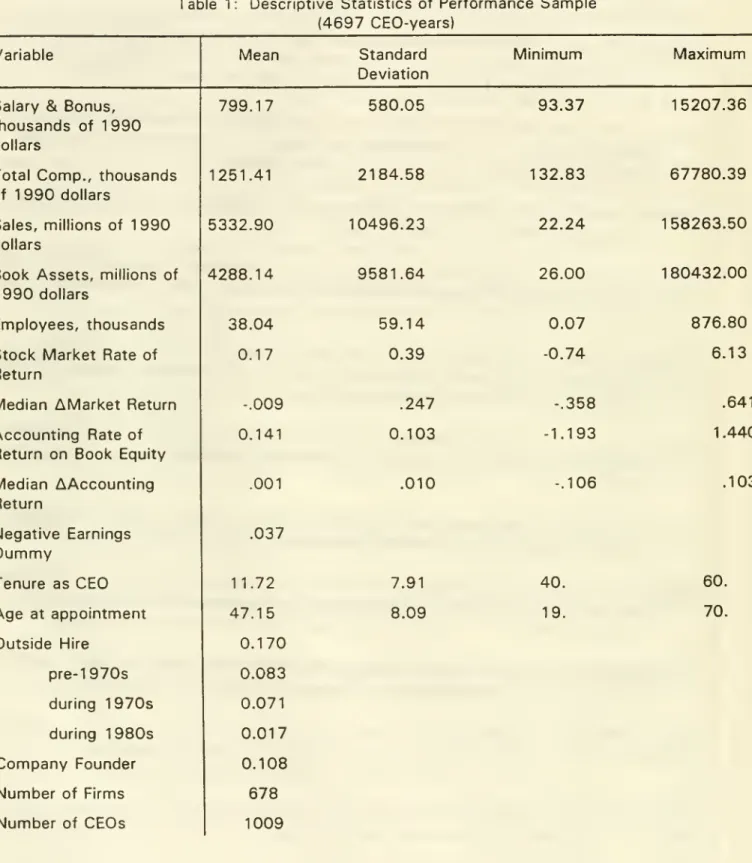

criteria yield a panel data set of4697

observationson

1009

CEOs

in678

firms. Descriptive statistics for this

sample

are reported in Table 1 . Variables aredescribed below.

Compensation

Measures:

We

reportresults fortwo measures

ofcompensation.

The

first,SALARY,

includes currentand

deferred salaryand bonus.

This generally isthe least inclusive

measure

ofcompensation

reported by Forbes,and

its definition isrelatively consistent over the entire

sample

periodwe

analyze.^^ RealSALARY,

in1990

constant dollars,grew

at anaverage

annual rate of4.0%

for our sample,and

averaged

$799,000

overall. Despite this growth,SALARY

accounts

for a decreasing share of overallcompensation

over time. Salaryand

bonus payments

averaged

82%

of total

compensation

reportedby

Forbes

for our sample,and

the ratio of salaryand

bonus

to totalcompensation

declinedby

an average of 1 .1percentage

points peryearbetween

1972

and 1990.

The

second

measure

ofcompensation,

TOTAL,

is themost

inclusivecompensation measure

reportedby

Forbes, although itscomponents

vary considerablyover time as

SEC

reporting requirementsand

Forbes's reportingformat change.

TOTAL

includes salaryand bonus,

contingentcompensation excluded from

SALARY,

the

cash

value ofcompany-provided

benefits (such ascompany-paid

life insurance,private automobiles,

and

drivers),and

realized net gainsfrom

the exercise of stockoptions, stock appreciation rights,

and

stock accrual rights.TOTAL

compensation

in^^JRS discussthe significant differences inthe compensation relationship

between

CEOs

of firms subject to economic regulation and those that are not.

'^ Forbes does not report base salary

1

990

constant

dollars averaged $1 .25 million for our sample,and

grew

at anaverage

annual rate of

5.9%

between

1972

and 1990.

While

TOTAL

is themost

inclusivemeasure

ofcompensation

we

have, itstreatment of stock options, appreciation rights,

and

accrual rights prevent itfrom

accurately

measuring

overall currentcompensation.^®

This will induce a "lumpiness"in reported

TOTAL

compensation

thatmay

limit its usefulness in our analysis,even

though

totalcompensation

(correctlymeasured)

is the theoretically appropriateconstruct

on

which

this analysis should focus.Firm Scale:

The

relationshipbetween

CEO

compensation and

firm size isone

of the

most

consistent empirical results in thecompensation

literature, withmost

studies reporting a

compensation

elasticity with respect to firmrevenues (SALES)

ofabout

.25 (Rosen, 1992).We

have experimented

with a variety of scalemeasures,

including

SALES, book

assets,and employees.

The

firms in oursample

are largeon

all three dimensions.

They

average$5.3

billion in1990

constant dollar sales,$4.3

billion in

constant

1990

dollar assets,and

38,000

employees.

Because

the estimatedpay-for-performance

relationshipappears

tobe

reasonably robust to alternativedefinitions of firm scale,

we

report results only for specifications thatuse

SALES,

thedominant measure

of firm scale in thecompensation

literature.Firm Financial Performance:

The

basic constructs thatwe

use

tomeasure

firmperformance

are stockmarket

rates of returnand

accounting rates of return.The

market

return(MKTROR)

is the annual rate of return tocommon

equity shareholders during the firm's reported fiscalyear,and

is constructedfrom

CRSP

return tapes.The

'^

As

noted inJRS

(1993), an ideal

measure

of total compensation would include the ex ante value of options grants (or similar instruments) in the yearthey areawarded

and the ex postchange

in the value of previouslyawarded

(as yet unexercised and unexpired) options each year. Itseems

impossible to construct these exactmeasures, and difficult to construct even close approximations to them, from1970

through1990

proxy statements.SEC

reportingrequirements inplacefor1993

and subsequentyears'proxystatementsshouldmake

accounting rate of return

(ACCROE)

is defined as reported earnings excludingextraordinary items divided

by

totalcommon

equity (book value),and

is constructedfrom

COMPUSTAT

data.^^Although

themeans

of thesetwo

returnmeasures

areroughly

comparable,

stockmarket

returns exhibitmuch

greater variance:Stock

market

returns for oursample

average17%,

with a standard deviation of39%.

Accounting

returnsaverage

14%,

with a standard deviation of10%.

The

two

measures

are correlated at the .18 level in our data.From

these basic constructswe

define anumber

of additionalperformance

measures

that areused

in our analysis ofasymmetric performance

sensitivities.

NEGATIVE

EARNINGS

isan

indicator variable equal toone

forobservations with

negative reported

accounting

earnings during the period.MEDIAN_^MKTROR

and

MEDIAN_^ACCROE

are variables thatdenote

the annualmedian

change

inmarket

and

accounting returns, respectively, for the fullJRS

dataset of unregulated,nonfinancial

companies.

We

use these variables to separate oursample

observationsinto

companies

thathave

close tomedian performance

changes

in a given year

and

those

whose

performance

change

is substantiallyabove

orbelow

the median.This

allows us to test

whether

performance

sensitivities aredampened

at the highor

low

extremes

ofperformance.

CEO

Characteristics:The

levels equationsmodel

logcompensation

as afunction of

CEO

characteristics as well as the variables described above.These

characteristics include the

CEO's

tenure in theCEO

position(TENURE),

his/her

age

atappointment

totheCEO

position (AGE)

, anindicator variable forwhether

theCEO was

an

appointment

from

outsidethe firmasopposed

toan

internalpromotion (OUTSIDE),

and

an indicator variable forwhether

theCEO was

thefounder

ofthefirm(FOUNDER).

^«This definition poses a problem

when

a firm's chron.caccountmg

'°=^^^%^^7,"^'^^,\^°°^value of its

common

equ.ty through zero.We

defineACCROE

to be ^'^^^;:^9jf he book ,^3

of equity is negative and therefore exclude these observations

16

These

variablesand

their empirical effectson

compensation

are described inconsiderable detail in

JRS

(1993).To

conserve

space, their coefficients are not reported in the tables below.^°A

regressionmodel

ofCEO

compensation

The

basiceconometric

specification ofthecompensation

equation followsfrom

our earlier

work

(JRS), but isexpanded

to investigate a richer specification of theperformance

variables thatmay

influence aCEO's

compensation.

The

basiccompensation

equation is specified as:ln(CEO

COMPENSATION,,,,

) = /ff, ln(SALES,, ) + yff'zPERFORMANCE;

i

^)S3CE0TEN,i, -)?4AGE,,

+ /?5OUTSIDE,,

+ /?6FOUNDER,

j ^ Oy * ^r ^ f„k, . [5]where

Idenotes

theCEO,

j

denotes

the firm, kdenotes

the primary industryidentification,

and

tdenotes

the year. Industry effects, a,^, aremeasured

at anaggregated

two-digit SICcode

level.These

incorporate theimpact

of industry-level variables, including industry-widecompensation norms,

on

executive pay.Year

effects, 6^ ,

accommodate

nonlinear (andnon-monotonic)

economy-wide

trends inrealCEO

compensation

over thesample

period.The

error term, Sjj^j ,may

includeCEO-specific effects.

Any

endogeneity

between

theseand

theindependent

variablesinthe^°These variables are incidental to our current analysis. Their estimated coefficients are

quite stable and consistent with our earlierresults.

CEO

compensation increasesveryslightlywith a

CEO's

ageatappointment and tenure.CEOs

appointed from outside are paidmore

and founders are paid less, other things equal.model

can

be treated by estimating themodel

in first-differences rather than levels,and

we

investigate both specifications in the results reported below.^'Performance

Specification:The

influence offirmperformance on

executivepay

is represented inthisequation

by

theterm

yS2'PERF0RMANCE, where

PERFORMANCE

is a vector of financial

performance

variablesand

132 is the vector of associatedparameters.

We

begin with a highly restricted model, similar to that estimated inmany

previouscompensation

studies, inwhich

RETURN

is a single variable,MKTROR,

and

p2 's a scalar parameter.We

next relax theassumption

of a singleperformance

parameter

aswe

introduce progressivelymore

flexibility into the estimatedpay-for-performance

relationship.We

expand

thedimension

of theRETURN

vector to include current accounting returns(ACCROE),

relax the restrictionon constant performance

sensitivities over time, explore the role of

memory

in the pay-for-performancerelationship,

and

finally test forasymmetries

inperformance

sensitivities.IV. Empirical Results

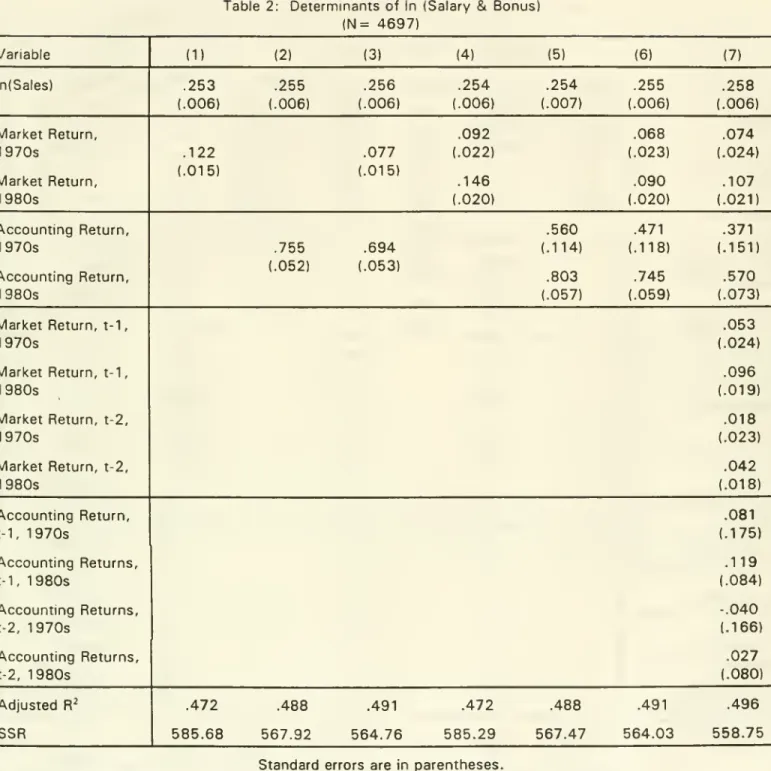

Table 2 presents results

from compensation

level equations thatuse

In(Salary&

Bonus)

as thedependent

variable.To

keep

the size of the tablesmanageable,

we

suppress

all coefficientsexcept

those for firm sizeand

theperformance measures.

Column

1 displaysresultsforthe simplest model,which

includes current stockmarket

return as the sole

performance

measure

and

restrictstheperformance

semi-elasticityto

be

thesame

for all observations.The

coefficienton market

return implies that a10

percentage

point increase in themarket

return (about one-quarter of thesample

standard deviationof

MKTROR)

increases salaryand

bonus

by

roughly 1.2%

(standarderror, .2%). This is broadly similar to results

from

previous empirical studies (see21

A

fixed-effects estimator also would be appropriate, but is not as widely used in this

literature as thefirst-differencemodel.

To

enhancethe comparability ofour results with those ofmost

earlier studies,we

therefore choose to use first-differences.Rosen, 1992).

Column

2,which

substitutes the accounting rate of return as the singleperformance measure,

impliesthata 1percentage

point increaseinaccounting

return (corresponding to

one

standard deviation increase in this variable) increases salaryand

bonus

by about

7.6%

(.5%).The

results incolumn

3 include bothaccounting

and market

returns,and

suggest

thatboth

measures

are important determinants of executive pay. In thisspecification, the

pay

sensitivity to a 1percentage

pointmovement

in return is0.8%

(0.2%)

formarket

returnsand

6.9%

(.5%) foraccounting

returns. Thus,even

when

both return

measures

are included in the regression, the semi-elasticity ofpay

isan

order of

magnitude

larger for accounting returnsthan formarket

returns. This patternis consistent with results

from

previous studies thathave

includedaccounting

rates of returnand

with the observation thatcompensation

contracts aremuch

more

likelyto

base

bonuses

on

explicit accountingperformance

targets thanon market-based

targets (e.g.,

Lambert and

Larcker, 1987).Given

theeconomic

and

statistical significance ofboth

accountingand market

returns in determiningCEO

pay,we

focus

our remaining attention

on

specifications that include bothmeasures.

Columns

4

through

6 repeat the first three specifications, but allow theperformance

slopes to differbetween

the1970s

and 1980s.

The

data clearly reject the restriction of constant slopes over time.^^ Incolumn

6,which

allowsboth

market and accounting

returnparameters

to differ overtime, theperformance

slopes increaseby

one-third to one-halfbetween

the1970s

and

the1980s.

Thissuggests

that the increasing

emphasis on

incentivepay

over thesample

period carriesthrough

to salaryand

bonus

decisionsand

is not solely a function of increaseduse

of stock options incompensation

packages.^^

The

test of constant performance slopes over the 1

970s

and 1980s

for thespecifications that include both accounting and marketreturn (column 3 v.

column

6oftable2) yields an F-statistic of 3.04, distributed as F(2,4697).

The

critical value for F(2, oo, .95)Finally,

column

7 estimates themore

generaldynamic

performance

specification,

based on

equation (1). Thiscolumn

reports resultsthat include currentand

two

lags foreach

returnmeasure."

The

resultsfrom

thismodel

ofcompensation

level strongly reject both of the simplemodels

of pay-for-performancedynamics:

pastperformance

has an influenceon

currentcompensation,

but thatinfluence is not perfectly persistent overtime.^'*

The

dynamic

pattern ofperformance

effectson

compensation

differsconsiderably

between

accountingand market performance measures.

The

estimatedoverall

impact

of accounting returnon

pay

is roughly constantbetween

thecontemporaneous-only (column

6)and

generaldynamic

(column

7) specifications, but including laggedaccounting

returns shiftsabout

20%

of the estimatedweight

to theprevious years' return

measures."

The

resultssuggest

that a10

percentage point increase inaccounting

returns during the1980s

generates

anaverage

cumulativeincrease in salary

and

bonus

equivalent to7%

ofone

year'scompensation."

In contrast, the estimated impact ofmarket

returnson

executivepay

is

substantially higher in the unrestricted

dynamic

model, relative to the"

We

chose this cutoffto conserve data and because the effect of past performance oncurrent compensation appearstodecay considerably beyond the first

two

lags. Thisreflects

ourviewofthe trade-off

between

estimating additional lags inthe performance vanabies and reducing sample size by restricting the analysis toCEOs

with increasingly long average tenures.2*

The

F-statistic for the testthat the coefficients on all lagged return measures are zero is 5 48, distributed as F(8,4641). The F-statisticforthe test that thecoefficients on current

and lagged returns are equal (but different for market and accounting returns, and different

between

the1970s

and 1980s), is 5.82, distributed as F(8,4641).The

critical valuefor

F{8,oo,.95) is 1.94.

"

For example, in the 1980s, thesum

of the coefficients in column 7 (.707) is slightlylower than the point estimate in column 6 (.742), but well within the standard error of

the

estimates (.055 for

column

6).2^ Because this increase is realized over3 years, itspresent discounted value is

somewhat

contemporaneous-only

model

ofcolumn

6.The

effect of currentmarket

returnon

current

pay

is slightly higher incolumn

7 than incolumn

6 (though withinone

standard error),

and

the laggedmarket

returnterms

more

than double

that impact. Inthe 1 980s, for

example,

a 1percentage

point increase inmarket

return generatesan

average

1.1%

(.2%) increase in currentcompensation,

1.0%

(.2%)

increase in nextyear's

compensation,

and

0.4%

(.2%) increase in the following year'scompensation.

The combined

effect isequivalentto a one-timeincrease ofroughly2.5%

in salaryand

bonus.

These

resultssuggest

that levels specifications thatassume

thepay-for-performance

relationship isonlycontemporaneous

underestimate

theimpact

ofmarket

performance

on

CEO

pay.We

explore the intertemporal structure of thepay-for-performance

relationshipin further detail in table 3, using first-difference

models

ofcompensation.

These

regressions

model

changes

inIn(SALARY)

asa function ofchanges

in In(SALES), yearand

industry effects,and

alternative specifications of theperformance measures.

To

limit the size of the table,

we

use

changes

inaccounting

return in all specificationsthat include an

accounting

measure

of performance.We

vary the specifications toexamine

both levels ofmarket

returnand

changes

inmarket

return.Columns

1, 2,and

3 in table 3model

changes

inIn(SALARY)

as a function ofchanges

inmarket

returns.These

correspond

to simple first-difference estimates ofthe specifications reported in

columns

1 , 2,and

6of table 2.These

restricted models,based on

equation (3), implicitlyassume

no

"memory"

in thecompensation

process:a one-time

shock

to return generates a one-timeshock

tocompensation.

The

estimated coefficients are considerably smaller than

those

reported in table 2,suggesting that positive correlations

between

unobserved

CEO-specific effectsand

firm

performance

may

overstate theperformance

sensitivity ofpay

incompensation

Columns 4

and

5 of table 3model

changes

inIn(SALARY)

as a function of thelevel of

market

return.These correspond

to the restrictedmodel

of equation (4),which

assumes

thatperformance

effects are perfectly (and infinitely) persistent: a one-timeshock

to the firm'smarket

return triggers apermanent

increase in currentand

futurecompensation.

These

results implymuch

greater sensitivity of executivepay

tomarket

returns thando

thecolumn

1-3 results.The 1980s

market

returncoefficient of

.093

(.012) incolumn

5 implies that an additional 1percentage

pointsin

market

return generates an increaseof9.3%

insalaryand

bonus

inthe current yearand

in ailsubsequent

years.These

estimates arecomparable

tothose

reportedby

Gibbons

and

Murphy

(1990) for asomewhat

differentForbes sample and

slightly modified, but similar,compensation

equations.^'The

choice of functionalform

makes

a significantdifference to the fit of theserestricted equations.

A

minimum

leastsquared

errors testwould

preferthe restrictedmodel

of equation (4) to the restrictionsimposed

by

equation (3)(compare

theSSR

ofcolumns

1and

4

or ofcolumns

3and

5). Ifone

is forced tochoose between

one

of

these

two

highly simplified specifications,assuming

thatperformance

effects are perfectly persistent appears to better satisfy the data.As

in the levels equations,however,

this specification is strongly rejected in favor of themore

generaldynamic

model

of equations (1)and

(2).Column

6 of table 3 reports results for the generaldynamic

performance

structure. This

model corresponds

to first-difference estimates of the specification reported incolumn

7 of table 2,and

isbased on

the first-difference equation (2)."

The

Gibbons andMurphy

sample covers a shorter time period (1974-1986) but largersample of CEO-years than does ours (due partially to our exclusion of financial sector and

regulated firms and the elimination of the first three years of each

CEO's

tenure due to the data requirements of our lagged return structure tests). Gibbons andMurphy

do not includesales and do include various industry return measures as variables in their compensation equations.

These

estimates decisively reject both the restriction thatperformance

effects arecontemporaneous

only^^ and the restriction that theperformance

coefficients areconstant over time.^^

The

pattern of coefficients highlights thereasons

these restrictions are rejected. Focusingon

the1980s,

formarket

returns the previousyear's stock

market performance appears

tohave

about

thesame,

or slightlymore,

impact

on

currentcompensation

asdoes

currentmarket

returns (.078 (.010) forcurrent,

.095

(.011) for laggedonce

returns).The

impact

of previousmarket

performance

on

currentcompensation drops

quite sharply afterone

year,however.

The

coefficienton

returnsfrom

year t-2 is less than halfthemagnitude

of the returnscoefficient for year t-1, at .042 (.009).

Accounting

return coefficients exhibit asmoother

pattern ofdecay

over time, decliningabout

60

percenteach

yearfrom

thecontemporaneous

return impact of.573

(.040). Nevertheless,assuming

that pastaccounting

returnshave no

impacton

currentcompensation

misses

about

35

percentofthe

cumulative

three-yearcompensation response

to ashock

inaccounting

returns.Finally,

we

note that themarket

return estimatesfrom

the generaldynamic

first-difference

model

incolumn

6, table 3, are quite similar to those of the levelsmodel

in

column

7 of table 2. Thismay

suggest

that the differencesbetween

thesetwo

estimation

methods

for thecontemporaneous-only

model

aredue

more

tomis-^^

The

F-tests forthe restrictionthat lagged marketreturn coefficients are zero is 22.08,

distributed as F{4,4647); that lagged accounting return coefficients are zero is 7.40,

distributed asF(4,4647);thatalilaggedperformancecoefficients arezerois 17.94,distributed

as F(8,4647).

The

.95 level critical values are: F(4,cx3)=

2.37, F(8,oo)=

1.94.^^

The

F-statistic for the testthat current and lagged market return parameters are equal (within decade) is 10.86, distributed as F(4,4647); that current and lagged accounting parameters are equal (within decade) is 25.54, distributed as F(4,4647); and that both of these sets ofrestrictions are satisfied is 21 .35, distributed as F(8,4647).

The

.95 level criticalspecification of the pay-for-performance relationship than to correlation

between

30

returns

and

a CEO-specificcomponent

of the error term.For

completeness,

we

report incolumn

7 of table 3 estimatesfrom

a firstdifference

model

that uses the level ofmarket

returnand

its lags rather thanfirst-differences in

market

return. This is similar to themodel

thatassumes

completelypersistent

market performance

effects incompensation

(e.g.,column

5 of table 3).Ifthis

assumption

is correct, thecoefficientson

the laggedmarket

returnterms

shouldbe zero.^*'

As

expected from

the results incolumn

6,which

nestthis

model

as a special case, the data reject this restriction.^^ For the1980s,

the previous year'smarket

returnhas

a slightly larger impacton

currentcompensation

thandoes

the current year's return (the coefficient of.023

(.011)on

lagged return is properlyinterpreted as the incremental effect over the current return coefficient).

The

market

return

from

two

yearsago has

less than half theimpact on

currentcompensation

as the currentmarket

return,however,

asevidenced by

its negative point estimate of -.049 (.010).Given thesuperiority ofthe general

dynamic

specification in boththe levelsand

first-difference equations,

we

focus our attentionon

variants of thismodel

in the

remaining analysis.

30

The

coefficients on current and lagged market return for the1980s

are quite similaracross these

two

tables.The

first difference estimates yield slightly lowercoefficient

estimates for market returns during the 1970s, and slightly higher estimates

for lagged

accounting returns (though within astandard error).

The

similarity of resultsacrosslevels and first-difference estimates providessome

incidental support for theconsistency ot the underlying model.

^'

Returning to the general dynamic specification in first differences, equation (2), the

coefficient on

contemporaneous

marketreturn is So, the coefficient on thefirstlag of market return is (fl, - %), and the coefficient on the second lag of market

return is ((^2 - li,).

me

complete persistence model

assumes

that Bg=

K,=

1^2=

•••~

^r32

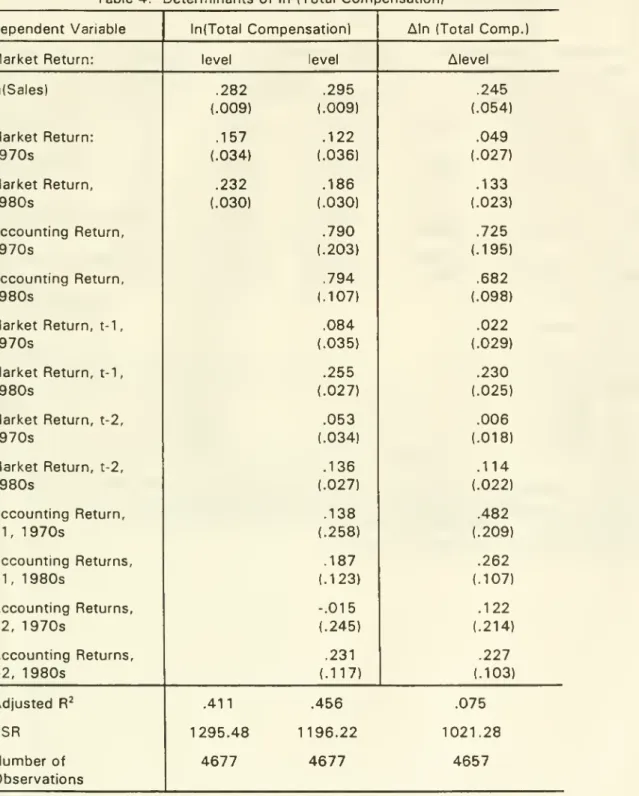

The

F-statistic fortherestriction thatthe coefficients onthe laggedmarket returntermsTable

4

replicates the analysis of Tables 2and

3 using totalcompensation

(TOTAL)

rather than salaryand

bonus

as the nneasure of executive pay.Column

1reports the simplest

performance

specification (market return only, with slopes splitby decade)

for comparability with table 2and

previous studies.Columns

2and

3report results

from

the "fulldynamic"

specification, estimated in levels (2)and

first-differences (3). Total

compensation

is, not surprisingly,more

responsive tomarket

performance

variations than is salaryand

bonus,and

the sensitivity increasedmarkedly

during the1980s.

As

in the salaryand

bonus

results, pastperformance

influences current

compensation

but the effectdecays

after the first lag.-^-' In thefirstdifference

model

ofcolumn

3, a10

point increase in currentmarket

return duringthe

1980s

increases totalcompensation by

1.3%

(.2%) this year,2.3%

(.3%) nextyear,

and

1.1%

(.2%) the following year, for a cumulative effect equivalent to a one-year increase of4.7%.

This ismore

than twice thecumulative

market

return effecton

salaryand

bonus

(column

6, table 3).^'*Perhaps

more

surprising is the strongersensitivity of total

compensation

to accountingperformance:

thecumulative

effectof a

10 percentage

point increase in accounting returns inthismodel

is 1 1.7%, about

a third larger than the cumulative effect of accounting return increase

on

salaryand

bonus

(column

6 of table 3)."

The

estimates in both columns 2 and 3 reject both ofthe restricted models ofthepay-for-perf

ormance

relationship. Forthefirst-difference model, the F-statisticforthetestthattherelationship is

contemporaneous

only is 21.00 formarket returns, 13.81 for both market andaccounting returns, distributed as F(4,4609) and F(8,4609) respectively.

The

F-statistic forthe test that the relationship is perfectly persistent (equal performance slopes over time) is

10.26 for market returns and 8.51 for both market and accounting returns, distributed as F(4,4609) and F(8,4609) respectively.

^*

The

larger impact of past marketreturns on total compensation than on salary and bonus is not unexpected, given the construction of