Essais sur le cycle économique et de la transition de la grande inflation à la grande modération

126

0

0

Texte intégral

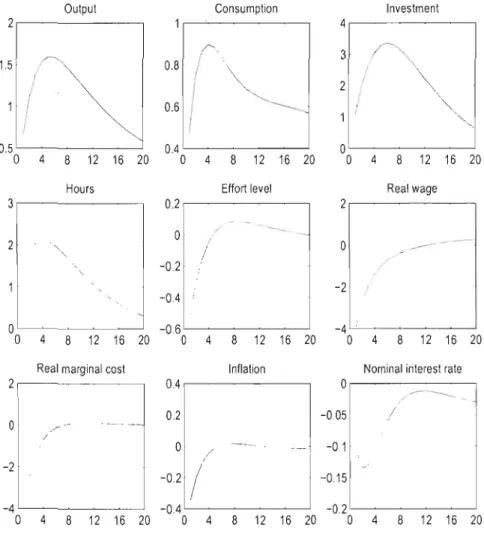

Figure

+2

Documents relatifs