Using survey data to resolve the exchange risk exposure puzzle

Texte intégral

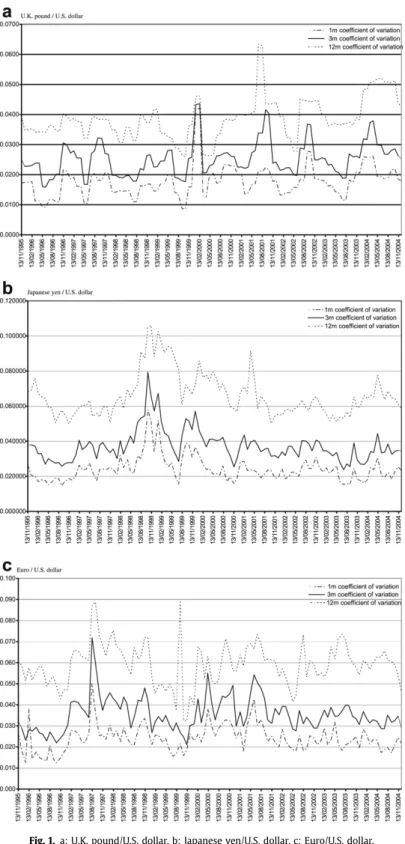

Figure

Documents relatifs

In line with Lewis (1995), Andrade and Bruneau (2002) (AB) proposed a partial equilibrium model where the risk premium, defined as the difference between the expected change in

In our analysis we account for this persistent nature for both, the crude oil market and the USD exchange rate markets and then investigate whether volatility series share a

Of course the fact that the DM-bloc produces different parameter estimates does not allow us to conclude that the difference is due to exchange rate volatility since, for example,

Our goal is to identify whether the degree of trade openness of a country has an impact on the relationship between current account and exchange rate changes during episodes of

The paper investigates if the most popular alternative to the purchasing parity power approach (PPP) to estimate equilibrium exchange rates, the fundamental

But for those who do not believe in this Nemesis theory, a procyclical evolution of the real exchange rate appears all but normal. Of course exchange rates are usually

Moreover, an increase in the cost of external funds (relative to cash flow) makes profits less sensitive to exchange rate shocks for firms whose liquidity is positively affected by

The description of the evolution of the imbalances networks over time reveals an increase in complexity along, at least, three dimensions. The first one is the number of nodes,