Mesure et Prévision de la Volatilité pour les Actifs Liquides

Texte intégral

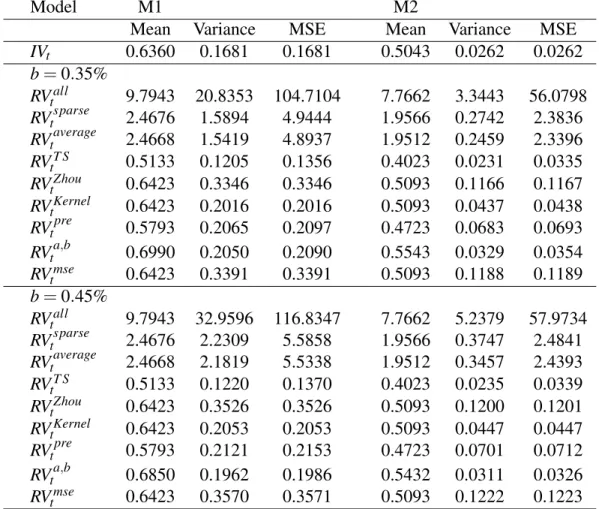

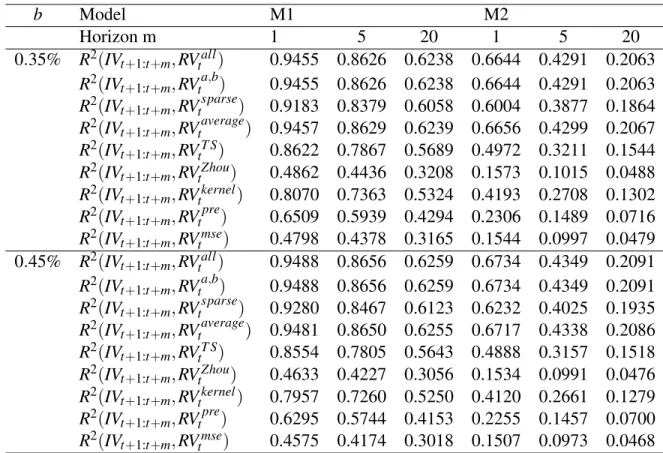

Figure

Documents relatifs

Jerzy Urbanowicz Institute of Mathematics Polish Academy of

Dans ce troisième chapitre, nous étudions le problème classique de la consommation optimale dans le modèle de Kabanov avec des sauts, c’est à dire les marchés avec coûts

The main contribution of this paper is to propose a bootstrap method for inference on integrated volatility based on the pre-averaging approach, where the

The goal of this section is to propose a new variational model for denoising images corrupted by multiplicative noise and in particular for SAR images.. In the following, if X is

Finally, we test for the effect of jumps on several market measures and find that jumps have a positive impact on market activity as proxied by volume and number of traders and

For more extended edge profiles (several pixels), the effect on the variance estimate decreases, because the slope corresponding to the extending edge profile is smaller and the

Dans le chapitre 3, nous étudions les relations lead/lag à haute fréquence en utilisant un estimateur de fonction de corrélation adapté aux données tick-by-tick9. Nous illustrons

Using a sample of sixty stocks over a six-month period, we implement the optimal quoting policy (OQP) of liquidity provision from Ait-Sahalia and Saglam's (2014) dynamic inventory