HAL Id: pastel-00004737

https://pastel.archives-ouvertes.fr/pastel-00004737

Submitted on 9 Feb 2009HAL is a multi-disciplinary open access archive for the deposit and dissemination of sci-entific research documents, whether they are pub-lished or not. The documents may come from teaching and research institutions in France or abroad, or from public or private research centers.

L’archive ouverte pluridisciplinaire HAL, est destinée au dépôt et à la diffusion de documents scientifiques de niveau recherche, publiés ou non, émanant des établissements d’enseignement et de recherche français ou étrangers, des laboratoires publics ou privés.

Coal in Europe: what future? Prospects of the coal

industry and impacts study of the Kyoto protocol

Ekawan Rudianto

To cite this version:

Ekawan Rudianto. Coal in Europe: what future? Prospects of the coal industry and impacts study of the Kyoto protocol. Sciences of the Universe [physics]. École Nationale Supérieure des Mines de Paris, 2006. English. �pastel-00004737�

ED n° 430 : Matériaux, Ouvrages, Durabilité, Environnement et Structures

T H E S E

Pour obtenir le grade de

Docteur de l’Ecole des Mines de Paris

Spécialité : Techniques et Economie de l’Exploitation du Sous-Sol

Présentée et soutenue publiquement par

Ekawan RUDIANTO

Le 19 décembre 2006

Charbon en Europe : quel avenir ?

Perspectives de l’industrie du charbon

et étude des impacts du Protocole de Kyoto

devant le jury composé de :

René AÏD Examinateur

Christian BUHROW Rapporteur

Michel DUCHENE

Examinateur

Damien GOETZ Examinateur

Jan PALARSKI

Président

T H E S E

Pour obtenir le grade deDocteur de l’Ecole des Mines de Paris

Spécialité : Techniques et Economie de l’Exploitation du Sous-Sol Présentée et soutenue publiquement par

Ekawan RUDIANTO

Le 18 décembre 2006

Directeur de thèse : Mr. Michel DUCHENE

Jury :

M. Jan PALARSKI Président

M. Christian BUHROW Rapporteur

M. René AÏD Examinateur

M. Robert PENTEL Examinateur

M. Michel DUCHENE Directeur de thèse M Damien GOETZ Co-Directeur de thèse

SUJET DE LA THESE

Charbon en Europe : Quel Avenir ?

THESIS

Submitted to Ecole des Mines de Paris

L’ÉCOLE NATIONALE SUPERIEURE DES MINES DE PARIS by

Ekawan RUDIANTO

In partial fulfillment of the requirement for the degree of

DOCTEUR DE L’ÉCOLE NATIONALE SUPERIEURE DES MINES DE PARIS Specialisation : Techniques et Economie de l’Exploitation du Sous-Sol

COAL IN EUROPE: WHAT FUTURE?

Prospects of the coal industry and impacts study of the Kyoto Protocol

Thesis Supervisor Professor Michel DUCHENE

Professor Damien GOETZ

Centre de Géosciences - Ecole des Mines de Paris 35 rue Honoré - 77305 Fontainebleau Cedex

Prediction is very difficult, especially about the future

Niels Bohr

Danish physicist (1885 - 1962)

Acknowledgement

I would like to gratefully and sincerely thank Prof. Michel DUCHENE for his guidance, understanding, patience, and most importantly, his friendship during my studies at Centre de Geoscience – Ecole des Mines de Paris. His mentorship was paramount in providing a well rounded experience consistent my long-term career goals. He gave fully autonomy to finish this These and encouraged me to not only an instructor but also an independent researcher. I am not sure many graduate students are given the opportunity to develop their own individuality and self-sufficiency by being allowed to work with such independence. For everything you’ve done for me, Michel, I thank you. I would also like to thank all of the members of the Centre de Geoscience - ENMSP, especially Prof. Damien GOETZ for giving me the opportunity to do research at ENMP. These two friends and co-workers also provided for some much needed encouragement in what could have otherwise been a somewhat stressful laboratory environment.

I would also like to thank Prof. Michel TIJANI for his guidance in getting my post-graduate career started on the right foot and providing me with the foundation for becoming a researcher. Additionally, I am very grateful for the friendship of all of the members of Centre de Geoscience, with whom I worked closely and puzzled over many of the same problems. I would like to thank the members of my doctoral committee, Prof. Palaski, Prof. Buhrow, Dr. Aid, Dr. Pentel, for their input, valuable discussions and accessibility.

Finally, and most importantly, I would like to thank my wife Wieke Widayani and my sons Dimas and Dinan. Their support, encouragement, quiet patience and unwavering love were undeniably the bedrock upon which the past years of my life have been built. Her tolerance of my occasional vulgar moods is a testament in itself of her unyielding devotion and love. I thank my parents for their faith in me and allowing me to be as ambitious as I wanted. It was under their watchful eye that I gained so much drive and an ability to tackle challenges head on.

Abstract

From the industrial revolution to the 1960s, coal was massively consumed in Europe and its utilization was constantly raised. In the aftermath of World War II, coal had also an important part in reconstruction of Western Europe’s economy. However, since the late 1960s, its demand has been declining. There is a (mis)conception from a number of policy makers that saying coal mining and utilizations in Europe is unnecessary. Therefore in the European Union (EU) Green Paper 2000, coal is described as an “undesirable” fuel and the production of coal on the basis of economic criteria has no prospect. Furthermore, the commitment to the Kyoto Protocol in reducing greenhouse gases emission has aggravated this view. Faced with this situation, the quest for the future of coal industry (mining and utilization) in the lines of an energy policy is unavoidable.

This dissertation did a profound enquiry trying to seek answers for several questions: Does the European Union still need coal? If coal is going to play a part in the EU, where should the EU get the coal from? What should be done to diminish negative environmental impacts of coal mining and utilization? and finally in regard to the CO2 emission concerns, what will the state of the coal industry in the future in the EU?

To enhance the analysis, a system dynamic model, called the Dynamics Coal for Europe (the DCE) was developed. The DCE is an Energy-Economy-Environment model. It synthesizes the perspectives of several disciplines, including geology, technology, economy and environment. It integrates several modules including exploration, production, pricing, demand, import and emission. Finally, the model emphasizes the impact of delays and feed-back in both the physical processes and the information and decision-making processes of the system. The calibration process for the DCE shows that the model reproduces past numbers on the scale well for several variables. Based on the results of this calibration process, it can be argued that the DCE model can be used to do a forecasting for examining long-term behavior of coal industry in the EU-15. Finally, the algorithm and modules construction for the DCE model can be used to construct a model for other non-renewable energy sources for Europe.

Keywords: Coal, Kyoto Protocol, System Dynamics model

Résumé

Au cours de la période allant de la révolution industrielle aux années 60, le charbon a été massivement consommé en Europe et son utilisation s’est constamment accrue. Après la deuxième guerre mondiale, le charbon a joué également un rôle important dans la reconstruction de l'économie de l’Europe de l'ouest. Il faut noter cependant que la demande de charbon a commencé à décliner depuis le début des années 1960. Il en résulte de la part de certains décideurs une tendance à dire que l'extraction du charbon et son utilisation en Europe sont inutiles. Par conséquent, dans le livre vert de l’union européen 2000 (UE), le charbon est décrit comme un carburant «indésirable», et en se basant sur des critères économiques, sa production n'a aucune perspective. En outre, l'engagement du protocole de Kyoto dans la réduction de l'émission des gaz à effet de serre a aggravé cette perception. Face à cette situation, un nouveau débat sur l’avenir de l'industrie du charbon (extraction et utilisation) dans la perspective d'une politique énergétique communautaire est inévitable.

Cette dissertation a fait une enquête profonde en vue d’apporter des réponses à plusieurs questions. L'union européenne a-t-elle toujours besoin du charbon ? Si le charbon est appelé à jouer un rôle au sein de l’UE, d'où proviendrait-il? Que devrait-on faire pour diminuer les incidences négatives sur l'environnement consécutives à l'extraction du charbon et de son utilisation ? Finalement, au regard des soucis d'émission de CO2, quelle sera la situation de l'industrie du charbon dans l'avenir au sein de l’UE ?

Pour approfondir l’analyse, un modèle dynamique de système appelé « The Dynamics Coal for Europe” (DCE) a été développé. Le DCE est un modèle qui prend en compte trois dimensions : l'énergie, l’économie, et l’environnement. Il s’appuie sur plusieurs disciplines telles que : la géologie, la technologie, l'économie et l'environnement. Il intègre plusieurs modules comprenant l'exploration, la production, l'évaluation, la demande, l'importation et l'émission du CO2. En conclusion, le modèle met l’accent sur l'impact du temps de réaction (retard et recto-action) sur deux processus : physique (par exemple le temps pour faire l’exploration du charbon) et de l'information.

Le procédé de calibrage pour le DCE prouve que le modèle reproduit le même résultat que les données réelles. Basé sur les résultats de ce procédé de calibrage, il se peut que le modèle de DCE puisse être employé pour faire des prévisions pour examiner le comportement à long terme de l'industrie du charbon dans l'EU-15. Finalement, l'algorithme et la construction de modules pour le modèle de DCE peuvent être employés pour construire un modèle pour d'autres sources d'énergie non-renouvelables pour l'Europe.

TABLE OF CONTENTS

Acknowledgments iv

Abstract vii

Table of Contents ix

List of Figures xii

List of Tables xvii

Introduction xix

Background to the problem xix

Research objective xxiv

Research approach xxiv

Dissertation structure xxv

PART I: Coal in Europe: What Future?

Chapter 1:

Coal as Energy Systems

1.1 Introduction to coal 1.1.1. What is coal ……….. 1 1.1.2. Origin of coal ……… 2 1.1.3. Coalification ……….. 3 1.1.4. Classification ………. 3 1.1.4.1. Types of coal ………. 4 1.1.4.2. Characteristic of coal ………... 4

1.1.4.3. Classification based on the degree of coalification ……… 5

1.1.4.4. Classification based on the trade and its uses ……… 6

1.1.4.5. Coal analyses ……… 8

1.2 Reserves 1.2.1. Coal resources/reserves classification system ………. 9

1.2.2. World Coal Reserves ……… 11

1.3 How to mine coal 1.3.1. Surface mining techniques ……….. 16

1.3.2. Underground mining techniques ……… 18

1.3.3 Unconventional coal mining techniques ………. 22

1.4 Global Coal industry 1.4.1. Coal utilization ………. 24

1.4.2. Coal Consumption ……… 26

1.4.3. Coal Supply ………... 29

1.5 Discussion: Coal future : opportunities under gloominess 1.5.1. Impact on Environment ………... 30

1.5.3. Sectoral Demand ……….. 33

1.5.4. Production Prospects ……….. 34

1.6 Closing remarks

Chapter 2:

Inquiries on coal prospect in Europe

2.1. Inquire no 1: Does Europe still need coal? 2.1.1. Energy scene in Europe ………... 382.1.1.1. Primary Energy Consumption ……….. 38

2.1.1.1. The impossibility of energy self-sufficiency ………. 40

2.1.2. Role of coal in Europe ………. 42

2.1.2.1. Introduction ……… 42

2.1.2.2. Evolution of demand and supply ……….. 43

2.1.2.3. Coal for Energy and Industry ………... 48

2.1.2.3.1. Coal for balancing energy sources for power sector 48 2.1.2.3.2. Coal as a raw material for Steel Industry …………. 49

2.1.2.3.3. Coal for other uses ………. 51

2.1.3. Discussion : Europe still needs coal at least for the next two decades ……. 52

2.1.3.1. Coal for satisfied future electricity demand and steel production 52 2.1.3.2. Coal for balancing security of energy supply ……….. 54

2.1.3.2.1. High concern on security of energy supply ……….. 54

2.1.3.2.2. Actions to strengthen security of energy supply ….. 56

2.1.4. Global warming: a major challenge of coal to Environment ………. 58

2.2 Inquiry no 2: Where should coal come from then? 2.2.1. Supply from indigenous production is declining ………... 60

2.2.1.1. Reserves and quality ……….. 60

2.2.1.2. Present Coal mining in Western Europe ………. 64

2.2.1.3. Supply from indigenous is under pressure ……….. 66

2.2.1.4. Operating Cost ………... 67

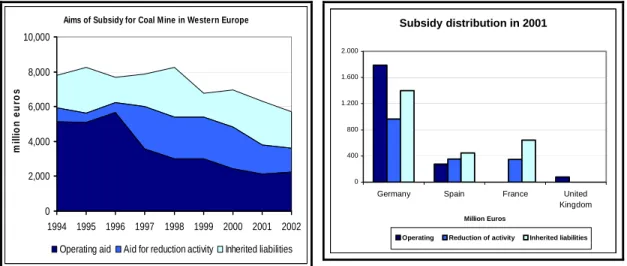

2.2.1.5. Subsidy ………... 68

2.2.2. Supply from outside community for balancing demand ………... 71

2.2.2.1. World coal trade in ways to maturity ………... 71

2.2.2.2. The evolution pattern of hard coal trade in Atlantic ………….. 73

2.2.2.3. Mechanism of coal transaction: move forward to be a transparent market ……… 76

2.2.2.4. Price formation ……….. 78

2.2.3. Discussion : while indigenous is in doubt supply from outside secure …… 82

2.2.3.1. World coal reserve can secure the demand ………. 82

2.2.3.2. Supply can fulfil demand in the Atlantic coal market ……….. 83

2.3 Inquire no 3: What efforts to reduce coal environmental impacts? 2.3.1. The environmental challenges ……… 87

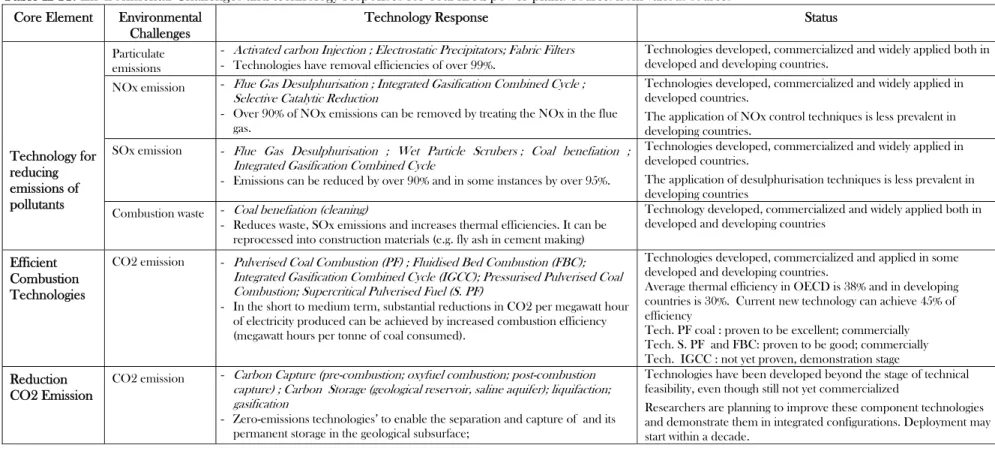

2.3.2. Discussion: A road map of Clean Coal Technology ……….. 90 2.4. Closing remarks

Chapter 3:

European Community and Climate change Protection

3.1 What is climate change3.1.1. The greenhouse Effect ……… 96

3.1.2. Origin emission of greenhouse gases ………... 98

3.1.3. Coal and climate change ……….. 100

3.2. Action against climate change 3.2.1. A global binding commitment: international effort to halt climate change .. 102

3.2.2. The Kyoto Protocol and European Community : Ratification and its current status of GHGs emission ……… 104

3.2.2.1. Ratification ………... 104

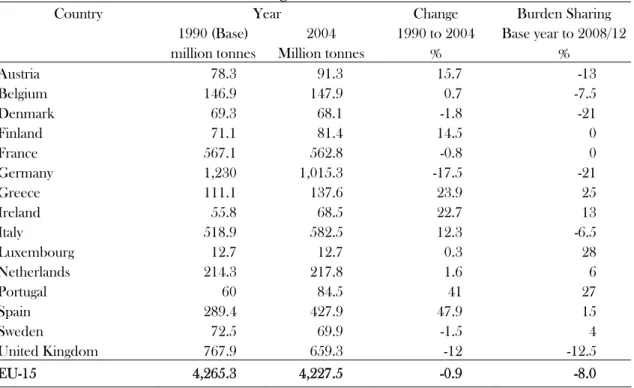

3.2.2.2. Currents status of GHGs in EU-15 ……… 105

3.3. Policy strategy for combating climate change in the EU-15 3.3.1. The Kyoto Protocol mechanisms ……… 109

3.3.2 European mechanism : ETS, carbon taxes and policies and measures to promote energy efficiency ………... 111

3.3.2.1. Emission trading scheme ……….. 111

3.3.2.2. Carbon and energy taxes ……….. 116

3.3.2.3. Promote energy efficiency ……… 118

3.3.2.4. Green Paper on Energy ……… 119

3.3.3 Strategy of Clean Coal Technology in Europe ……… 121

3.4. Discussion : climate change economics 3.4.1. Cost of avoidance ………. 123

3.4.2. Economics of Clean Coal Technology ………. 125

3.4.3. Price or Quota instrument? ………. 128

3.5. Closing remarks

PART II : MODELLING COAL PROSPECT IN EUROPE

Chapter 4 :

System Dynamics for Energy Modeling

4.1 Fundamental of system dynamics ……… 1354.2 Modeling and Simulation ……….. 137

4.3 Energy modeling by using system dynamics ………... 139

Chapter 5 :

System Dynamics Model for Coal

5.1 Model Structure 5.1.1 Model description ………. 1475.2 Problem Definition

5.2.1 Objective of the model ………. 161

5.2.2 Time horizon ………. 161

5.2.3 Boundary ……… 161

5.2.4 Characteristic the model ……….. 162

5.3 Model Construction 5.3.1 Demand module ……… 154

5.3.2 Supply module ……….. 148

5.3.3 Price module ………. 152

5.3.4 Policy Analysis module ……… 153

5.4. Dynamic behavior of system 5.4.1. Parameters Calibration ….……….. 164

5.4.2. Model Simulation under deterministic variable ……… 161

5.4.2.1. Comparison analysis ……… 151

5.4.2.2 Deterministic policy analysis ……….. 172

5.4.3. Model Simulation under uncertainty variable ………. 177

5.5. Closing remarks 5.5.1. Model robustness ……….. 180

5.5.2. Import dependence ………... 181

5.5.2. The need for a model for the development of Carbon Capture and Storage 183

Chapter 6:

Application of the DCE model for

Simulating Carbon Tax Policies

6.1. Constant carbon tax ………. 1906.2. Adaptive carbon tax ………. 194

6.3. Permit price ………... 198

6.4. Closing remarks ……….. 203

General Conclusions 209

Recommendation for future researches 212

References 214

APPENDIXES

A. Brief coal mining activity in Germany, Spain, UK and Greece 229 B The derivation of analytical solution for positive feedback system 237 C. Documentation of Dynamics Coal for Europe (DCE) 240

LIST OF FIGURES

PART I: Coal in Europe: What Future?

Chapter 1

Figure 1.1. Different types of coal 2

Figure 1.2. Different coal uses by coal type 8

Figure 1.3. Coal Resources Classification System 10

Figure 1.4. Coal Resources Classification System 11

Figure 1.5. Composition of world coal reserve 12

Figure 1.6. Global coal deposits 14

Figure 1.7. Open Cut Coal Mining 15

Figure 1.8. Room and Pillar Coal Mining 16

Figure 1.9. Long Wall Coal Mining 18

Figure 1.10. Short Wall Mining 21

Figure. 1.11. Post mine gas drainage 24

Figure 1.12. Electric generation by coal 25

Figure. 1.13. Used of Coke for Blast furnace 26

Figure. 1.14. World Coal Consumption by Region 34

Figure. 1.15. World Coal Demand by Sector 35

Figure. 1.16. Coal Production by Region 35

Chapter 2

Figure 2.1 Primary Energy Consumption in EU-15 39

Figure 2.2. Energy Balance in EU-15 39

Figure. 2.3. External dependence of fossil fuel in Europe 42

Figure. 2.4. Role of coal in Energy consumption 43

Figure. 2.5. Hard coal production in EU-15 44

Figure. 2.6. Hard coal consumption and production in EU-15 44

Figure 2.7. Electricity generation in EU-15 48

Figure 2.8. Hard coal consumption for steel making in EU-15 50

Figure 2.9. Agents consumption per ton of steel production 51

Figure 2.10. Power requirement in EU-15 53

Figure 2.11. Power generation capacity in EU-15 53

Figure 2.12. Emission CO2 from fossil fuel combustion in EU-15 59

Figure 2.13. Climate balance statement in EU-15 59

Figure 2.14. Coal production and import in Europe 64

Figure 2.15. Employee in coal mining in Europe in 2004 65

Figure 2.16. Mining Productivity in German Hard Coal 66

Figure 2.17. Operating cost in coal mining in EU-15 68

Figure 2.19. Aims of subsidy for coal mining in EU-15 69

Figure 2.20. Development of world hard coal trade 70

Figure 2.21. Main trade flow in maritime hard coal trade 72

Figure 2.22. Spot coal freight rates 73

Figure 2.23. World hard coal market mechanism 75

Figure 2.24. Spot transaction in the Atlantic market 76

Figure 2.25. World coal supply capacity 77

Figure 2.26. Relation coal price index in the Atlantic market 79

Figure 2.27. Evolution of fossil fuel in Europe 82

Figure 2.28. World coal reserve distribution 83

Figure 2.29. Major coal exporter in the Atlantic market 84

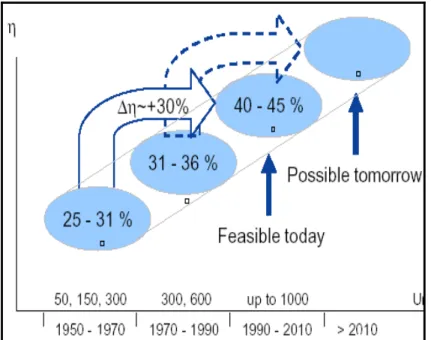

Figure 2.30. Development in the capacity (MW) & thermal efficiency (%) of coal-fired power plant 88

Figure 2.31. Coal-fired route to CO2 reduction. 91

Figure 2.32. CO2 capture and storage 92

Chapter 3

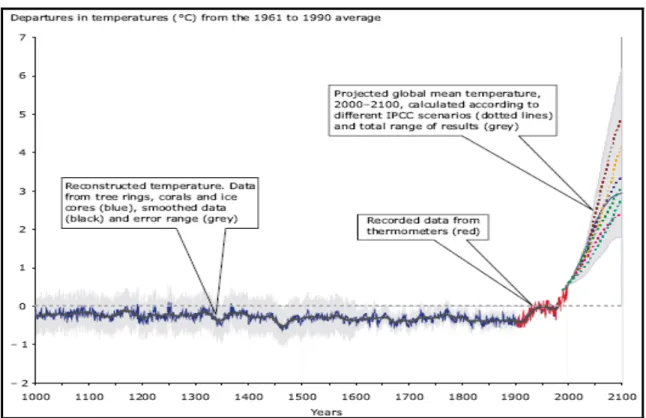

Figure 3.1. Reconstructed, measured and projected temperature in Northern hemisphere 96

Figure 3.2. Greenhouse effect 98

Figure 3.3. EU-15 Greenhouse emission by sector in 2003 100

Figure 3.4. World CO2 emission by fossil fuels 101

Figure 3.5. Distance to the Kyoto’s target for EU-15 106

Figure 3.6. Actual and projected EU-15 GHGs compared with Kyoto target 108

Figure 3.7. The Kyoto Protocol mechanisms 109

Figure 3.8. Traded of emission traded and its price 112

Figure 3.9. Use and Development of Clean Coal technology 123

Figure 3.10. Specific CO2 avoidance costs 124

Figure 3.11. European coal-fired power plant building activity (1920-2000) 125 Figure 3.12. C02 emissions and capital cost by electricity generating technology 126

Figure 3.13. Indicative generating cost range 128

Figure 3.14 Balance on marginal cost and benefit 129

Figure 3.15 Balance on marginal cost and benefit when cost uncertain 130

Figure 3.16 Price instrument to mitigate climate change 131

PART II : MODELLING COAL PROSPECT IN EUROPE

Chapter 4

Figure 4.1. Stock-Flow-Feedback loop structure 136

Figure 4.2. Extended Stock-Flow-Feedback loop structure 137

Figure 4.3. Stock-Flow structure representating Hubbert’s view of non-renewable resource 139 Figure 4.4. Hubbert’s life cycle theory of non-renewable resource discovery and production 141

Chapter 5

Figure 5.1. The steps of the DCE modelling process 150

Figure 5.2. Sector boundary, internal variables and external relationships 154

Figure 5.3. Major Feedbacks Processes 156

Figure 5.4. Causal diagram for coal demand module 158

Figure 5.5. Causal diagram for coal exploration 160

Figure 5.6. Causal diagram for coal production 161

Figure 5.7. Causal diagram for coal depletion 162

Figure 5.8. Causal diagram for coal price module 163

Figure 5.9. Causal diagram for coal policy module 164

Figure 5.10. GDP model (developed using Vensim® version 5) 165

Figure 5.11. Comparison of data and simulation results for Gross Domestic Product in the EU-15 167 Figure 5.12. Comparison of data and simulation results for Population in the EU-15 167 Figure 5.13. Comparison of data and simulation results for Electricity Demand in the EU-15 167 Figure 5.14. Comparison of data and simulation results for Steel Production in the EU-15 168 Figure 5.15. Comparison of data and simulation results for Hard coal demand in the EU-15 168 Figure 5.16. Comparison of data and simulation results for Hard coal Production in the EU-15 168 Figure 5.17. Comparison of data and simulation results for Hard coal Domestic Price in the EU-15 169 Figure 5.18. Comparison of base case and tax case for Hard coal domestic price in the EU-15 174 Figure 5.19. Comparison of base case and tax case for Hard coal demand in the EU-15 175 Figure 5.20. Comparison of base case and tax case for total carbon emission from Hard coal

domestic price in the EU-15

175 Figure 5.21. Comparison of base case and tax case for Hard coal production in the EU-15 175 Figure 5.22. Comparison of base case and tax case for Consumption per capita in the EU-15 176 Figure 5.23. Further results of coal model for base scenario and tax scenario 176

Figure 5.24. Steps of Monte Carlo Simulation in the VENSIM® 177

Figure 5.25. Hard coal domestic price (€/GJ) in the EU-15 under uncertainty scenario 179 Figure 5.26. Hard coal demand (GJ) in the EU-15 under uncertainty scenario 179 Figure 5.27. CO2 emission from hard coal (TonC/year) in the EU-15 under uncertainty scenario 179 Figure 5.28 Hard coal production (GJ) in the EU-15 under uncertainty scenario 180 Figure 5.29 CO2 in atmosphere and temperature change under uncertainty scenario 180 Figure 5.30 Comparison of base case and tax case for Import dependence for Hard coal 182

Figure 5.31 Cumulative emissions abatement as a function of the penalty level 186

Figure 5.32 CO2 capture at various policy incentive level 187

Chapter 6

Figure 6.1. Hard coal price (€/G ) after being introduced constant tax 192

Figure 6.2. Hard coal demand (GJ/year) after being introduced Constant tax 192 Figure 6.3. Carbon emission (TonC/year) from hard coal after being introduced Constant tax 193

Figure 6.4. Constant carbon tax (€/TonC) under uncertainty scenario 193 Figure 6.5. Hard coal demand (TonC/year) under uncertainty and constant tax scenarios 193 Figure 6.6. CO2 emission from hard coal (TonC/year) under uncertainty and constant tax scenario 194

Figure 6.7. Adaptive and constant carbon tax sub-models (Vensim®) 195

Figure 6.8. Hard coal price (€/G ) after being introduced Adaptive tax 196

Figure 6.9. Hard coal demand (GJ/year) after being introduced Adaptive tax 197 Figure 6.10. Carbon emission (TonC/year) from hard coal after being introduced Adaptive tax 197

Figure 6.11 Adaptive carbon tax (€/TonC) under uncertainty scenario 197

Figure 6.12 Hard coal demand (TonC/year) under uncertainty and adaptive tax scenarios 198 Figure 6.13 CO2 emission from hard coal (TonC/year) under uncertainty and adaptive tax scenario 198

Figure 6.14 Permit Price sub-model (Vensim®) 199

Figure 6.15 Hard coal price (€/G ) after being introduced Permit price 201

Figure 6.16 Hard coal demand (GJ/year) after being introduced Permit price 201 Figure 6.17 Carbon emission (TonC/year) from hard coal after being introduced Permit price 201

Figure 6.18 Permit Price (€/TonC) under uncertainty scenario 202

Figure 6.19 Hard coal demand (TonC/year) under uncertainty and Permit price scenarios 202 Figure 6.20 CO2 emission from hard coal (TonC/year) under uncertainty and Permit emission

scenarios

202

Figure 6.21 Controlling CO2 emission using economic incentives 203

Figure 6.22 Carbon constant and adaptive tax (€/TonC) for comparison study 204

Figure 6.23 Permit price (€/TonC) for comparison study 204

Figure 6.24 Hard coal prices (€/GJ) for comparison study 205

Figure 6.25 Hard coal demand (GJ) for comparison study 205

Figure 6.26 Total Carbon Emission (TonC/year) from hard coal for comparison study 206

LIST OF TABLES

PART I : Coal in Europe : What Future?

Chapter 1

Table I-1. Different coal classification based on the degree of coalification 6 Table I-2. Different free mine cost in several hard coal producing countries 15

Table I-3. Distribution of World coal reserves in country in million ton 17

Table I-4. World hard coal consumption 27

Table I-5. Hard coal consumption, by region 28

Table I-6. Main impacts of coal 31

Table I-7. Coal demand projection 32

Chapter 2

Table II.1 Primary Energy Consumption (2003) 38

Table II-2 Fossil fuel reserve in EU-15 41

Table II-3 Hard coal consumption in EU-15 45

Table II-4 Hard coal Production in EU-15 46

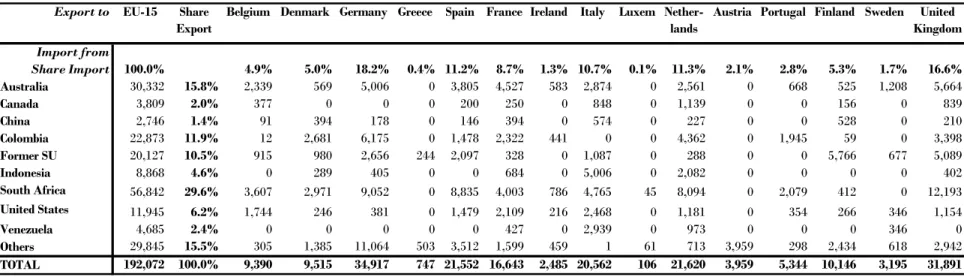

Table II-5 Hard coal Trade Balance in EU-15 47

Table II-6. Electricity generation in the European Union, 2002 49

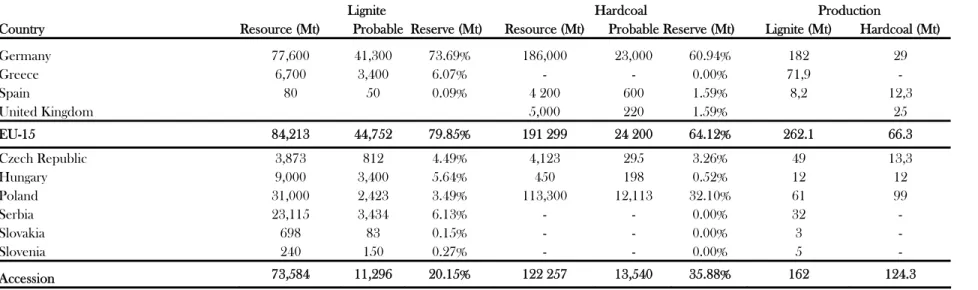

Table II-7. EU-15 and EU-25 : Coal Resources and Reserves (2002) 62

Table II-8. Coal Qualities in EU-25 63

Table II-9. Coal Industry Subsidies in Western Europe, 2001 70

Table II-10. World hard coal trade (Mt) 77

Table II-11 Environmental Challenges and technology response for coal-fired power plant 89

Chapter 3

Table III.1 Carbon content of different fossil fuels 101

Table III-2 Global Warming Potential (GWP) coefficient 103

Table III-3 Greenhouse Gases’ emission target for the EU-15 and its status in 2002 105

Table III-4 Emission trading in EU-15 for period 2005-07 115

Table III-5 Rates of CO2 taxation in EU-15 countries which introduced carbon taxes 117

Table III-6 Current capital cost estimates for power plant 127

PART II : MODELLING COAL PROSPECT IN EUROPE

Chapter 5

Table V-1. Main Model Boundary 152

Table V-2. GDP Variables for the EU-15 166

Table V-3. Result for Calibration process for GDP variable 166

Table V-4. Comparison for results of Data and Simulation for certain main variables 170 Table V-5. Summary response of the model to the introduction of a 135 €/TonC constant carbon tax 173

Table V-6. Variable Distribution 178

Table V-7. Estimation of CCS costs 185

Chapter 6

Table VI-1 Summary response of the model to the introduction of a 135 €/TonC tax 191 Table VI-2 Summary response of the model to the introduction of an adaptive carbon tax 195 Table VI-3 Summary response of the model to the introduction of a permanent cap on hard coal

emission at 208 million ton carbon per year 200

Glossary and Acronym

ASTM : American Society for Testing Materials

Bcf : Billion cubic feet

BOF : Basic Oxygen Furnace CBM : Coal Bed Methane CCS : Carbon Capture & Storage CCT : Clean Coal Technology CIF : Cost, Insurance and Freight CMM : Coal Mine Methane

DCE : Dynamic Coal for Europe : a modelof system dynamics EC : European Commission

ECBM : Enhanced coal bed methane recovery

ECSC : European Coal and Steel Community

EEA : European Environment Agency EIA : Energy Information Administration EOR : Enhanced oil recovery

EU : European Union GHG : Green House Gases GJ/t : Giga Joule per tons

Gtce : billion metric-ton of coal equivalent (1 Gtce=29.31 exajoules or EJ). GtC : billion metric ton of carbon.

GtCO2 : billion metric ton of carbon dioxide. GTL : Gas To liquid

GW : Gigawatt [=1 million kilowatt (kW)=1000 megawatt (MW)] HC : Hard Coal

IEA : International Energy Agency

IGCC : Integrated Gasification Combined Cycle IPCC : Intergovernmental Panel on Climate Change JORC : Joint Ore Reserves Committee

MCIS : McCloskey Coal Information Service MJ/kg : Mega Joule per kilogram

Mtce : Million tons coal equivalent Mtoe : Million tons oil equivalent Mt : Million tons

MWh : Megawatt-hour. 1 MWh is the amount of electricity generated by an 1 MW-unit in 1 hour. OECD : Organization for Economic Co-operation and Development

PCI : Pulverized Coal Injection

PFBC : Pressure Fluidized bed combustion TWh : Terrawatt-hour

TonC : Tons Carbon

Tce : Ton Oil Equivalent

UNECE : United Nation Economic Commission for Europe

UNFCC: United Nations Framework Convention on Climate Change

USGS : United States Geological SUrvey WCI : World Coal Institute

WEC : World Energy Council

Introduction

Background to the problemEvery type of energy has its legend. Although the role of coal in energy supply has now been taken by oil and gas, coal once had a glorious role as one of the factors that shaped Europe’s economic and political development in the nineteenth and twentieth centuries. From the beginning of the industrial revolution to the 1960s, this fossil fuel was massively consumed and its utilization was constantly raised. In the aftermath of World War II, coal had also an important part in the reconstruction of Western Europe’s economy.

Challenged by a great decline in demanding coal and steel in the post-war period which could have plunged Western Europe into an economic recession, some European countries (France, West Germany, Italy, Belgium, Luxembourg and the Netherlands) created the European Coal and Steel Community (ECSC)1

on April 18th

, 1951. The ECSC introduced a common free steel and coal market, with freely set market prices, and without import/export duties. The ECSC functioned by striking a balance between production and distribution. Subsequently, when the coal and steel industry crashed into crisis in the 1970s and 1980s, the ECSC was able to lead a response which made it possible to carry out the industrial restructuring. The ECSC ceased to exist on July 23th, 2002, and its responsibilities and assets were then assumed by the European Committee (Council Decision (2002/596/EC).

Nevertheless, coal still has an important role in Europe’s economy today. The power supply system of the European Union (EU) is currently based on a mix of nuclear energy, coal, gas and hydroelectric power. Coal has been an essential part of the European energy primer consumption and electricity production. Indigenous coal production and import together supply almost 15% of the European primary energy consumption. About 26% of the EU’s electricity is coal based, while large quantities of coal are also required by the steel making industry and raw-materials industries, such as cement works, paper mills and briquetting.

Coal, as any other energy sources, has intrinsic disadvantages as well as advantages. Being a solid and heavy mineral, coal is bulky and requires large storage areas. With a lower calorific value than oil and gas coal does not have the ease of use of a liquid or gaseous fuel. Coal also generates pollution at stage of the production and utilisation cycle. The physical disadvantages of coal have considerably reduced its markets for expansion. However, the world coal reserve is plenty, so that it can be exploited more than 200 years. It is safe to be transported and the fluctuation of its price is less than that of oil as well gas.

Today, difficult decisions will have to be taken regarding the future of the European coal industry on account of its lack of competitiveness. Coal is described by the Green Paper as an “undesirable” fuel and its production on the basis of economic criteria has no prospect either in the former European Union or in the applicant countries (Green Paper, the European Commission, (EU), 2001). Furthermore, the commitment to the Kyoto Protocol in reducing greenhouse gases emission might aggravate the coal prospect.

1

It was the fulfillment of a plan developed by a French economist Jean Monnet, publicized by the French foreign minister Robert Schuman

In the late 1960s, the role of coal as source of energy was overtaken by oil. Since years the demand has been declining, not only in the EU-15 but also in new member (accession) countries. The demand of hard coal in Western Europe declined from about 600 Mt in the early 1960s to less than 60 Mt in 2004, whilst lignite declined from 396 Mt in 1973 to 262 Mt in 2002. Following the closure of last remaining coal mines in Netherlands in 1975, Belgium in 1992, Portugal in 1994 and France in 2004, only three member states of the EU-15 (the United Kingdom, Germany, and Spain) continue to produce hard coal, while Greece produces mainly lignite.

Three reasons can explain this declining production. First is competition with other fuel sources. Coal has to compete with other fuels, particularly natural gas. Market deregulation of energy and electricity has brought many benefits but it has also had undesirable consequences for coal industry. Energy security is not adequately valued in energy markets and deregulation has lowered its economic returns to and increased the risk aversion of the major utilities, making the financing of new technology in coal-fired power plant more difficult – especially when that technology requires large investments of capital and relatively long capital-recovery periods.

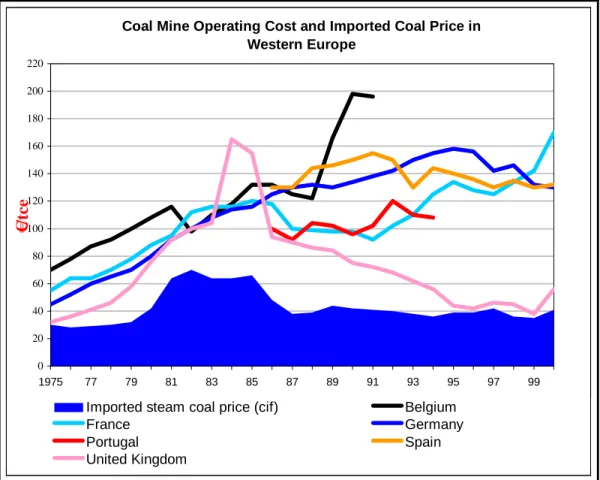

Second is high operating cost. As the most easily accessible seams are exhausted, hard coal has to be mined under current mining methods in increasingly difficult geological conditions and at greater depths. The result is high mining cost. The operating cost of most hard coal exploitations in Western Europe is higher than those in other countries and than the imported coal price2

. This has called the member countries to import coals to satisfied domestic need rather than to produce internally. Today, almost 45% of EU coal needs is covered by imported production. Concerning hard coal in EU-15, 70-75% of its demand is covered by imported coal.

There is a general (mis)-conception that coal mining (and utilization) in Europe is unnecessary because of growing world coal trade and untapped possibilities for importing cheap coal from outside the European Community. Added to those beliefs is the view that, albeit some deposits are still economically exploitable, most Europe’s coal deposits are nearly depleted to the point where the exploitation is relatively inefficient and high operating costs. Such viewpoints have spilled over into the formation of policies towards the industry that are not always beneficial.

Last reason is the growing environmental concerns, and particularly emission reduction. Environmental concerns have highlighted the weaknesses of solid fuels. Under the Kyoto Protocol, the European Community committed itself to reduce its emissions of six greenhouse gases (GHGs) by 8% during the period 2008 to 2012 in comparison with their levels in 1990. This target is shared between the member states under a legally binding burden-sharing agreement, which sets individual emissions targets for each member state.

Combustion of coal, like other fossil fuels - gas and oil – produces carbon dioxide (CO2),

nitrogen oxides (NOx), and sulfur dioxida (SO2). Among other fossil fuels, coal is a more

carbon-intensive fuel per energy unit, and thus the increase in carbon dioxide emissions from coal combustion is higher than the increase in emissions from natural gas or oil.

Some 94% of man-made CO2 emissions in Europe are attributable to the energy sector as a

whole. Fossil fuels are the prime sources. In absolute terms, oil consumption on its own accounts for 50% of CO2 emissions within the EU, natural gas for 22% and coal for 28%. In terms of consumer

sectors, electricity generation and steam raising are responsible for 37% of CO2 emissions and

2 For example, in 2002 the German’s average operating cost was 150 €/ton while over the same year the imported coal price was 41 €/ton.

transport for 28%. Some 90% of the projected growth in CO2 emissions will be from the transport

sector. Almost 75% of coal utilization in Europe is for electricity generation. In 2002, of 2,670 TWh (Terrawatt hour) power generation, coal accounted for some 26% of the electricity supplies, others are oil (6%), natural gas (16%), nuclear (33%) and renewable resources (17%).

Combating climate change and minimizing its potential consequences requires substantial reductions in global greenhouse gas emissions. Three steps are adopted in Europe to reduce emission of GHGs from coal burning, including reducing emissions of pollutants, increasing thermal efficiency, and reducing CO2 emissions to near zero levels through carbon capture and storage. In practice, this will require in reducing coal consumption and or deploying lower emission technology.

Energy policy predominantly security of supply is backed in fashion in Europe. The events in Ukraine in the beginning 2006, where it witnessed gas supply cuts from Russia (Gazprom), the slow progress to liberalize European energy markets, and the growing European fossil fuel import dependency, have contributed to a sense of unease with reliance solely on market forces and conventional regulation. The tripling of oil prices in 1999 and its high prices3

in the first semester of 2006 reinforced this nervousness.

The European Union is now consuming and importing more and more energy products. If no measures are taken, in the next 20 to 30 years, 60% of the Union’s fossils energy requirement as opposed to the current 35% will be from imported products. As a result, external dependency on energy is constantly increasing. In geopolitical point of views, 45% of the EU-15 oil imports are from the Middle East and 40% of natural gas from Russia, while for coal, the imports are not dictated by certain countries (Green Paper, the European Commission, (EU), 2001). The fact that the price of crude oil has increased in the last two years may reveal the European Union’s structural weakness regarding security of energy supply. In reality, security of supply does not seek to maximise energy self-sufficiency or to minimise import dependence, but aims to reduce the risk linked to such dependence.

The above circumstances would give any government pause for thought. However, they also occur in a context of climate change, and the requirement to cut greenhouse gas emissions. While gains were made on the environmental front as a result of the rapid contraction of the coal mining and utilization in the 1990s, the EU Environmental Council’s suggest that cuts of the order of 65% in CO2 emissions below the 1990 level might be needed by the middle of the century (European Environmental Agency, (EEA), 2005).

Security of energy supply is now becoming one of the actual concerns in every country in the World, including the EU-15. Moreover, through a common agreement known as the Lisbon Strategy, which was announced in 2000, Europe has committed to make European Union as region with "the most dynamic and competitive knowledge-based economy in the world, capable of sustainable economic growth with more and better jobs and greater social cohesion, and respect for the environment". Optimum and secure energy supplies will be needed to achieve these targets and, inevitably, this will mean a significant growth in electricity demand.

Faced with the above challenges, the European Union has unfortunately few non-renewable resources and hardly any effective policy instruments to meet these challenges. The amounts of indigenous fuels available to Europe are limited. Oil reserves are very unevenly distributed across the world, and the European Union in particular has very few, with only 1% of global reserves. Natural gas reserves are more evenly distributed on the global level, but the European Union is once again unfortunate, with just 2%. The European Union is home to barely 1% of the world’s natural uranium

reserves, however last uranium production was stopped in France (in 2001) and Spain (in 2002) following the decommissioning of some other mines in Sweden and Poland. More uranium could be made available, but only at a higher price. About 80% of Europe’s fossil fuel reserves are solid fuels (including hard coal, lignite, peat and oil shale). At present production level, coal might last for more than 100 years. However, this optimism has to be tempered by the fact that the quality of solid fuels is variable and under current mining methods production costs particularly for hard coal are high.

The appropriate energy policy in securing energy supply is extremely important to achieve the Lisbon targets. Nowadays, there is still no common energy policy in Europe. The Europe's external energy policy remains within the competence of EU member states' foreign policies and a matter of national sovereignty. Addressing the security of supply problems will require a major investment program across Europe and much greater cooperation among EU member countries, and between EU and its partners. In these circumstances, it is time for Europe to launch a review for its energy policy.

The production of fossil energy in Europe is projected to decline over the next two decades (2030) while the consumption will increase (IEA, 2004; EIA, 2006; WETO, 2004). The International Energy Agency’s (IEA’s) reference scenario shows that the energy consumption in the EU-15 in 2030 will reach 2,191 Mtoe, where oil will represent 36% of EU-15 energy consumption, 33% of gas and 13% of hard coal and lignite. It argues that the EU-15 still depends heavily on fossil energy for the forthcoming decades.

All those dilemmas have to be solved. Governments in Europe should better seek ways to balance the social, economic and environmental needs of society. Government policies need to provide long-term strategic solutions for achieving sustainable energy use and economic growth. To secure the energy supply and reduce its emission, all possible energy option has to be left open. Policy on rapid decline of coal mining and utilization together with nuclear moratorium might only exacerbate problems of energy supply. In this context, government support for Energy policy involves three main components in general: low supply costs, security of supply and environmental considerations.

In regard to the future of coal industry in Europe, it has to separate the issues between indigenous coal mining and coal utilization (consumption). It is undoubted that high mining costs and the lack of competitiveness of European coal-mining have led several Member States to abandon coal. However, concerning coal utilization, the coal industry has a proven track record of developing technology pathways, which have successfully addressed environmental concerns at local and regional scales. Ongoing research under the title of Clean Coal Technology (CCT) puts efforts into improving the efficiency of coal-fired electricity generation and technologies for carbon capture and storage (CCS). They offer routes to reduce carbon dioxide (CO2) emissions now and in the future. They are enabling the energy security benefits of coal-fired power generation to continue to be realized. The future of coal industry is largely pinning its hopes on the Clean Coal Technologies and on policy of energy supply security.

Nowadays, the issues of security of energy supply and the high prices of oil and gas, in one hand, and the progress of clean coal technology, in other hand, have evoked the EU-15 to rethink its energy policy, in particular the future of coal utilization. Coal is still likely called in for balancing the energy supply inside the Community and even more called in for helping to meet Kyoto’s target.

Research objective

The quest for the future of coal industry in the lines of an energy policy in the European Union is unavoidable. This research tries to portray and to investigate the current status of (hard) coal mining and its utilization in the EU-15. In addition, by using a simulation analysis this research attempts to forecast the state of coal industry in the EU. Having understood the actual and the future roles of coal, it is hoped that the results of this research may contribute in analysing appropriately the future of (hard) coal and in determining an appropriate energy policy in Europe.

Fundamentally, the research will seek answers for four questions. A profound enquiry requires to seeking the appropriate response to the following question 1) Does the European Union still need coal? 2) If coal is going to play a part in the EU, where should the EU get the coal from? 3) What should be done to diminish negative environmental impacts of coal mining and utilization? and finally 4) concerning the CO2 emission, what will the states of the coal industry in the future?

In this dissertation, the European Community is particularly defined as the European Union pre-May 2004, which consists on 15 countries (Fig. 1). It is defined as such because the Kyoto’s targets bind principally to the EU-15 countries. And also the word “coal” refers to mainly hard coal.

Research approaches

Two approaches will be used in this research. They are a profound investigation analysis and a simulation analysis. The purpose of the first analysis is to examine the present and the future roles of coal in Europe and to seek answers to the first three main inquires above.

In the second approach, a Coal model, called the Dynamic Coal for Europe (the DCE) is developed by using system dynamics. The DCE is an Energy-Economy-Environment model. It synthesizes the perspectives of several disciplines, including geology, technology, economy and environment. It integrates several modules including exploration, production, pricing, demand, import and emission. Finally, the model emphasizes the impact of delays and feed-back in both the physical processes and the information and decision-making processes of the system.

The goal of the simulation by the DCE is to simulate and to understand the behaviour of coal industry in Europe as well as to predict the impact of implementation of emission reduction policies, i.e carbon taxes and permit instrument, under the frame of Kyoto Protocol. The DCE model’s focus is on long-term dynamics and is primary meant as a tool for analysis, and clearly not for exact prediction. It aims to fill at least partly a gap in understanding the coal industry in the EU-15.

Dissertation structures

This dissertation is divided mainly in two parts. The first is entitled Coal in Europe: What Future? and the second part is called Modelling Coal Prospect in Europe.

The first part of the dissertation consists of three chapters: Coal as an Energy System (Chapter 1), Inquiries on Coal Prospect in Europe (Chapter 2) and European Community and Climate Change Protection (Chapter 3). The first chapter mainly investigates some fundamental knowledge of coal, including the understanding of coal, world coal reserve, mine exploitation and global coal market. The second chapter will be dedicated to seek answers of three important questions about coal in Europe. Those are: (1). Does the European Union still need coal, (2), If coal is going to play a part in the Union Where should EU get the coal from? (3). and finally what should

be done to diminish negative environmental impacts of coal mining and utilization? The last chapter will discuss several issues on climate change, the Kyoto Protocol and its impact on coal. Each chapter will be completed by a section of analysis and discussion where the subject of discussion will follow to the chapter’s theme.

The second part of the dissertation is dedicated to the modelling and simulation of coal prospect in Europe by using the DCE model. The construction of the model is very much assisted by knowledge of current coal status acquired from the investigation’s result in the first part. This part consists of three chapters, namely System Dynamic for Energy Modelling (Chapter 4), System Dynamic Model for Coal (Chapter 5) and Application of the DCE model for Simulation of Carbon Tax Policies (Chapter 6). Chapter 4 explains briefly a fundamental of system dynamics and the use of the methodology for modelling energy systems. Chapter 5 will mainly discuss structure of the DCE model. The model itself consists principally of four main modules, which are energy demand, supply/production, price, and policy analysis module. Several sub-modules are also developed to support the main modules. The dynamic behaviour of the coal system industry will be investigated in the section on dynamic behaviour of the system.

The last chapter will be dedicated to simulating the implementation of emission reduction policies. The aim of the last chapter is also to compare the performance of each emission reduction instrument, including constant carbon tax, adaptive carbon tax and permit instrument, targeted to the coal industry in the EU-15. The aim of this simulation is also to forecast the trend of coal import dependence in the region.

Chapter 1:

Coal as Energy Systems

1.1. Introduction to coal

1.1.1. What is coalCoal is a solid, brittle, combustible, carbonaceous rock formed by the decomposition and alteration of vegetation by compaction, temperature, and pressure. It varies in colour from brown to black and is usually stratified. Coal deposits are usually called seams and can range from fractions of a half to fifty of meters in thickness.

Coal is found on every continent in almost seventy countries and world coal reserves is nearly 1 trillion tons. However, the largest reserves are found in the U.S., former Soviet Union, and China. Currently, coal is produced in nearly 50 countries.

Coal is generally classified according to rank. Rank classifications are based on a coal's content of fixed carbon, volatile carbon compounds, water, and ash, its heating value, and its coking properties. In the coalification process, coal first takes the form of peat, then progresses through lignite (brown coal), bituminous, and finally to anthracite and graphite. Lignite has a low heating value and a high moisture content of 30 to 40%. Bituminous coal is black and contains bands of both bright and dull material. The moisture content of bituminous coal is usually under 20%. Anthracite is shiny black with a high luster. It is the highest rank of economically usable coal with moisture content less than 15%. Fig. 1.1 summaries the different types of coal.

Bituminous coals are dense black solids, frequently containing bands with a brilliant lustre. The carbon content of these coals ranges from 78 to 91% and the water content from 1.5 to 7%

Sub-bituminous coals usually appear dull black and waxy. They have carbon content between 71 and 77% and a moisture content of up to 10%.

Brown coals or lignites have high oxygen content (up to 30%), a relatively low carbon content of 60-75% on a dry basis, and a high moisture content of 30-70%. These lower ranked coals are browner and softer.

Figure 1.1. Different types of coal

Source: World Coal Institute (WCI) (2002)

1.1.2. Origin of coal

Coal is found in deposits called seams that originated through the accumulation of vegetation that has undergone physical and chemical changes. These changes include decaying of vegetation, deposition and burying by sedimentation, compaction, and transformation of the plant remains into the organic rock found today. Coal differs throughout the world in the kinds of plant materials deposited (type of coal), in the degree of metamorphism or coalification (rank of coal), and in the range of impurities included (grade of coal).

The beginning of most coal deposits started with thick peat bogs where the water was nearly stagnant and plant debris accumulated. Vegetation tended to grow for many generations, plants materials settling on the swamps became submerged and were covered by sedimentary deposits, and a new future coal seam was formed. When this cycle was repeated, over hundreds of thousands of years, additional coal seams were formed. These cycles of accumulation and deposition were followed by diagenetic (i.e., biological) and tectonic (i.e., geological) actions and, depending upon the extent of temperature, time, and forces exerted, formed the different ranks of coal observed today.

A part from the theory that assumes the coal formed insitu11

, as explained above, there is another theory that assumes coal appearing to have been formed through accumulation of vegetal matter (such as wood) that has been transported by water. According to this theory2

, the fragment of plants have been carried by streams and deposited on the bottom of the sea or in lakes where they build up strata, which later become compressed into solid rock.

Major coal deposits formed in every geological period since the Upper Carboniferous Period, 350 to 270 million years age (Miller, 2002). The considerable diversity of various coals is due

1

it is known as the theory of autochthonous process 2

to the differing climatic and botanical conditions that existed during the main coal-forming periods along with subsequent geophysical actions.

1.1.3. Coalification

The geochemical process that transforms plant material into coal is called coalification and is often expressed as:

PeatÆ ligniteÆ subbituminous coal Æ bituminous coal Æ anthracite

Coalification can be described geochemically as consisting of three processes (Miller, 2002): (1). microbiological degradation of the cellulose of the initial plant material, (2). conversion of the lignin of the plants into humic substances, and (3). condensation of these humic substances into larger coal molecules.

The kind of decaying vegetation, condition of decay, depositional environment, and movements of the Earth’s crust are important factors in determining the nature, quality, and relative position of coal seams. Of these, the physical forces exerted upon the deposits play the largest role in the coalification process. Variations in the chemical composition of the original plant material contributed to the variability in coal composition. The vegetation of various geologic periods differed biologically and chemically. The conditions under which the vegetation decayed are also important. The depth, temperature, degree of acidity, and natural movement of water in the original swamp are important factors in the formations of the coal.

1.1.4. Classification

Two types of coal classification system arose. Some schemes are intended to aid scientific studies, and others are designed to assist coal producers and users. The scientific systems of classification are concerned with origin, composition, and fundamental properties of coals, while the commercial systems address trade and market issues, utilization and technological properties.

The commercial systems typically consist of two primary systems, the American Society for Testing Materials (ASTM) system (ASTM, 1992) and United Nation Economic Commission for Europe (UNECE, 1988).

1.1.4.1. Types of coal

Generally, coals are grouped according to particular properties as defined by their "rank" (degree of metamorphism or coalification), "type" (constituent plant materials) and "grade" (degree of impurities and calorific value). Of these, rank is a fundamental concept that involves a qualitative expression of the coalification sequence and is universal to all classification schemes. Coalification is a term that describes the maturation of plant tissues from peat through different stages of lignite/brown coal, sub-bituminous and bituminous coals to anthracites. Apart from these classifications, coal can be classified based on its uses in industry, such as coking coal (metallurgical coal) and steaming coal.

Direct and indirect utilization of coals for production of energy and chemicals as well as for smelting of base metals is the foundation upon which the interest in classifying this resource is built. However, heterogeneous nature and the variety of coals used throughout the world, classification of different types of coal into practical categories for use at an international level is a difficult task. This because divisions between coal categories vary between classification systems both national and

international based on calorific value, volatile matter content, fixed carbon content, coking properties, or some combinations of these criteria. Currently, there are several coal classifications developed by either certain countries or organization (JORC, 2004; ASTM, 1992; UNECE, 1988).

1.1.4.2. Characteristic of coal

Coals can be distinguished by their physical and chemical characteristics. These characteristics determine the suitability of coal for various uses. Coal is mainly composed of carbon and may also generate volatile matter when heated to decomposition temperatures. In addition, it contains moisture and ash-forming mineral matter. The elements of carbon, hydrogen, nitrogen, sulphur and oxygen are present in the coal matter. The combination of these elements and the shares of volatile matter, ash and water vary considerably from coal to coal. It is the fixed carbon content and associated volatile matter of coal that control its energy value and coking properties and make it a valuable mineral on world markets.

Some important characteristics of coal are:

o fixed carbon content influences the energy content of the coal. The higher the fixed carbon content, the higher the energy content of the coal

o volatile matter is the proportion of the air-dried coal sample that is released in the form of gas during a standardised heating test. Volatile matter is a positive feature for thermal coal. Yet high volatile matter can be a negative feature for coking coal

o ash content is the residue remaining after complete combustion of all organic coal matter and decomposition of the mineral matter present in the coal. The higher the ash content the lower the quality of the coal. High ash content means a lower calorific value (or energy content per tonne of coal) and increased transport costs. Most export coal is washed to reduce the ash yield (beneficiation) and ensure a consistent quality. The ash in residue can be broken down as the series of metal oxide, i.e. SiO2, Al2O3, CaO, MgO, P2O5, Fe2O3, SO3. These data are important in determining how a coal, steaming and coking coal, behave. o moisture content refers to the amount of water present in the coal. Transport costs increase directly with moisture content. Excess moisture can be removed after beneficiation in preparation plants but this also increases handling costs

o sulphur content increases operating and maintenance costs of end users. High amounts of sulphur cause corrosion and the emission of sulphur dioxide for both steel producers and power plants. Low sulphur coal makes installation of desulphurisation equipment to meet emission regulations unnecessary. Southern hemisphere coals generally have low sulphur content relative to Northern hemisphere coal

o Clorine usually occurring as the inorganic salt of sodium, potassium and calsium chloride. The relatively high amount of chlorine causes corrosion in boiler and when present in flue gas it contributes to pollution

o Phosphorous is undesirable for large amounts of phosphorous to be present in coking coals to be used in the metallurgical industry as it contributes to producing brittle steel

There are other minerals that may be present in coal which affect its potential use. Significant amounts of quartz in dust affect the incidence of silicosis. The mineral matter in the coal will also affect the washability of coal and consequently the ash content of the clean coal. Mineral impurities affect the suitability of a coal as a boiler fuel; the low ash fusion point causes deposition of ash and corrosion in the heating chamber. The presence in coal of phosphorous minerals causes slagging in certain boiler and steel produced from such phosphorous-rich coals tends to be brittle. Trace

elements may be present also in coal. Several of them, notably boron, titanium, vanadium and zinc, can have detrimental effect in the metallurgical industry.

1.1.4.3. Classification based on the degree of coalification

The degree of “metamorphism” or coalification undergone by a coal, as it matures from peat to anthracite, has an important bearing on its physical and chemical properties, and is referred to as the “rank” of the coal. Low rank coals, such as lignite and sub-bituminous coals, are typically softer, friable materials with a dull, earthy appearance. They are characterised by high moisture levels and a low carbon content, and hence a low energy content. High rank coals, such as bituminous and anthracite coals are typically harder and stronger and often have a black vitreous lustre. Higher rank coals have lower levels of moisture and volatile matter. They contain more carbon, have lower moisture content, and produce more energy.

Increasing rank is accompanied by a rise in the carbon and energy contents and a decrease in the moisture content of the coal. Anthracite is at the top of the rank scale and has a correspondingly higher carbon and energy content and a lower level of moisture. Between anthracites and peat there are three broad coal rankings: lignite, sub-bituminous and bituminous. Table I-1 shows different coal classifications based on its degree of coalification.

Table I-1. Different coal classification based on the degree of coalification

USA Peat Lignite Sub-Bituminous Bituminous Bituminous Anthracite

High volatile Low volatile

ECE Browncoal Hard coal

France Tourbe Lignite Flambant sec Flambant gras Gras Anthracite

Rank Low Low Medium Medium High High

Fixed Carbon, % < 38% 38-42% 42-64% 64-75% 75-84% 84-95%

Caloric value GJ/t 4.19 – 6.28 14.65-18.84 18.84 – 27.22 27.22 – 32.65 27.22 –32.65 32.65-35.59

Humidity % >50% 25-50% 14-25% 5-10% 5-10% 1-6%

Volatile matter % >75% 50%. 25-50% 30-40% 15-25% <10%.

Ash content 50%. 30-50% 20-30% 10-20% 10-20% 0-10%

Source: ASTM D388 (1992), UNECE (1988), Giraud (1983)

In the international commodity market, coal quality classification is more complex than that of crude oils. Analysis of crude oils price differentials has focused on two main properties: the specific gravity and the percentage of sulfur content by weight. Lighter crudes are expected to sell at a premium over heavier crudes. A high sulfur content has an adverse effect on the value of crudes, because it leads to higher operating costs for refineries. In general, a high-sulfur crude is expected to sell at a discount relative to a low-sulfur (sweet) crude.

1.1.4.4. Classification based on the trade and its uses

A number of coal classification schemes that relate to use, rather than science, have devised in different countries, as for example the American Society for Testing and Materials (ASTM), the UN Economic Commission for Europe (UNECE) or the British Industry. In general most are based on coal rank, often expressed as content of volatiles, sub-classified by calorific value, ash content,

sulphur content. The International Coal Classification of the Economic Commission for Europe (UNECE, 1988) recognises two broad categories of coal:

- Hard coal

Coal with a gross calorific value greater than 5,700 kcal/kg (23.9 GJ/t) on an ash free but moisture bases and with a mean random reflectance of vitrinite of at least 0.6. Within this category is including Bituminous coal and Anthracite.

- Brown coal

Coal with a gross calorific value less than 5,700 kcal/kg (23.9 GJ/t) containing more than 31% volatile matter. Sub-bituminous is coal with a gross calorific value between 5,700 kcal/kg and 4,165 kcal/kg (17.4 GJ/t) containing more than 31% volatile matter. Lignite, with a gross calorific value less than 4,165 kcal/kg (17.4 GJ/t), is reported in this category.

The fundamental classification of hard coal by end-use and also by trade category is into thermal or steam coal and coking or metallurgical coal. The fist type is used for burning in power stations and in other industrial and domestic uses, while the other type is used in the steel to de-oxidise iron ore in the blast furnace.

The properties that determine the economic viability and end-use category of coal are its rank (degree of coalification), chemistry and physical properties. The most basic properties of coal in respect of its uses are its content of moisture, volatiles, ash and fixed carbon (and sulphur). In general, the range of properties necessary in a coking coal are much more tightly constrained than those required for a steam coal.

- Coking coal (metallurgical coal)

This type of coal when heated in large ovens will produce coke and gases. Coke is a porous solid composed mainly of carbon and ash. Coke quality is related positively to coke strength. For the purposes of blast furnace applications, the coal used must be able to form large angular coke that retains its form despite constant heat, pressure, abrasion and collision in the blast furnace. Coking coal is classified as hard, soft or semi-soft. Hard coking coal, the highest quality coking coal, tend to have moderate volatile matter content, low inherent moisture, low ash and low sulphur levels. Hard coking coal commands the highest prices in world markets. Soft and semi-soft coking coals have lower fixed carbon content and higher levels of inherent moisture and volatile matter than hard coking coal.

Coking coal comes from the bituminous category. To be used as a coking coal it has to be capable of being converted to coke in a coke oven or other carbonisation process. This limits the number of coals that can be categorised as coking coal. Whilst all coking coals can be burnt in suitably designed power plants to generate electricity the reverse is not true in that not all bituminous steam coals can be converted into coke. An important feature of all coals used by the steel industry is that they should have as low a level of ash and sulphur.

- Steam coal (thermal coal)

This coal is burnt to have its heat. Higher the levels of ash, moisture, and sulphur, lower the quality of thermal coal. All categories of coal can be used for electricity generation, although power plants have to be designed to handle specific types of coal. For example a plant designed to burn bituminous coal would not be capable of burning brown coal.

The lower the quality, the lower the price received on world markets. Much of the world’s thermal coal is not of sufficient standard to be traded and its use is restricted to mine-mouth power stations. Also classified as thermal coals, pulverised coal injection (PCI) coal is used as a