An Application of Deep Reinforcement Learning to Algorithmic Trading

Texte intégral

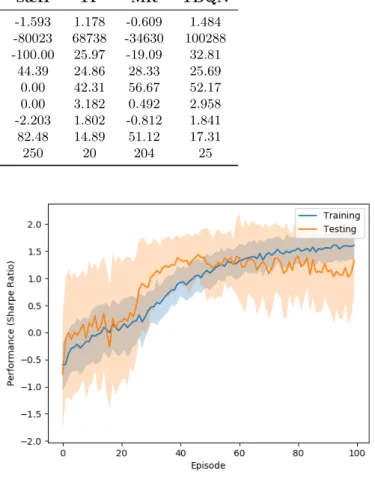

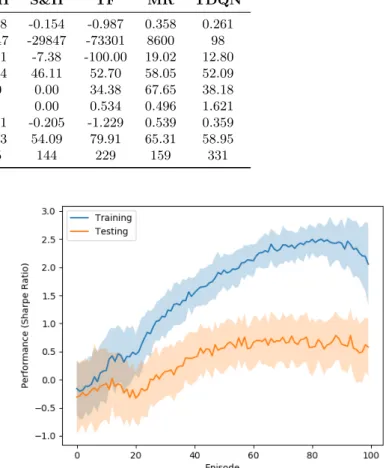

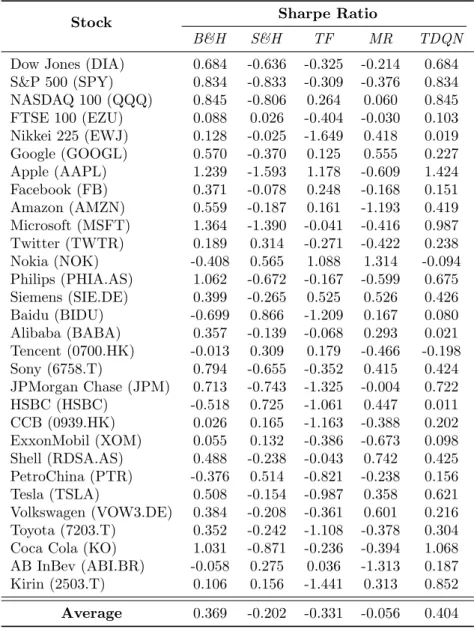

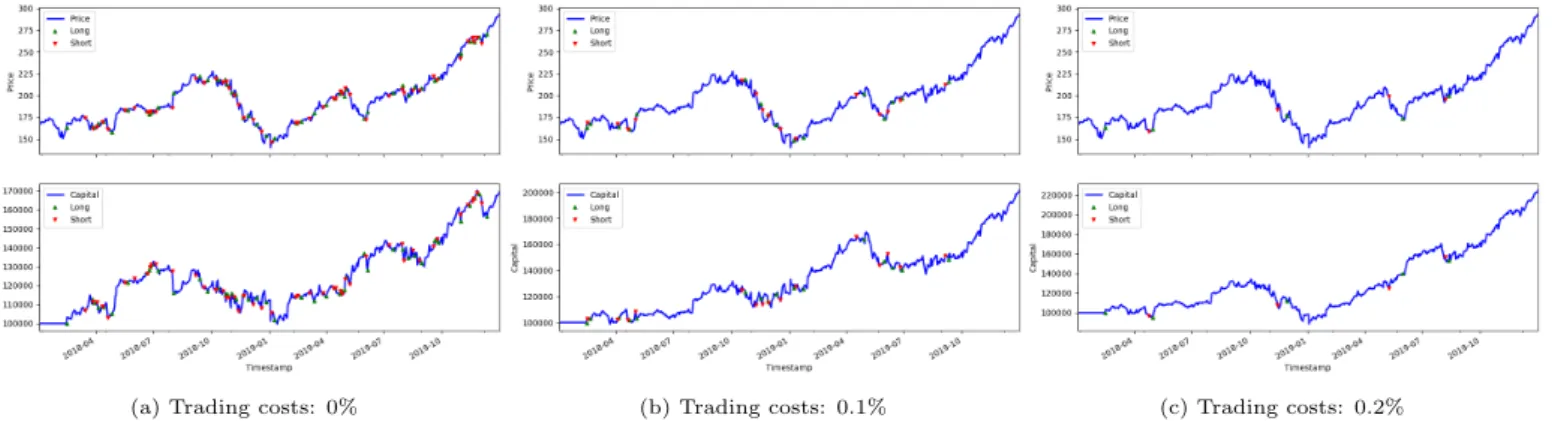

Figure

Documents relatifs

Distribution and Abundance of Resting Cysts of the Toxic Dinoflagellates Alexandrium tamarense and 751. catenella in sediments of the eastern Seto Inland Sea, Japan,

De plus, comme cela a été évoqué dans la section précédente, cette méthode de pré- diction de l'intervalle RR pourrait servir à l'attribution du signal de phase cardiaque

In addition, we use the most general (and powerful) server assignment policy, where the requests of a client can be served by multiple servers located in the (unique) path from

Zhou, F., Zhou, H., Yang, Z., Yang, L.: EMD2FNN: A strategy combining empirical mode decomposition and factorization machine based neural network for stock market

Volume, relative strength index, price-to-earnings ratio, moving av- erage prices from technical analysis, and the conditional volatility from a GARCH model are considered as

We tested Deep reinforcement learning for the optimal non-linear control of a chaotic system [1], using an actor-critic algorithm, the Deep Deterministic

Pham Tran Anh Quang, Yassine Hadjadj-Aoul, and Abdelkader Outtagarts : “A deep reinforcement learning approach for VNF Forwarding Graph Embedding”. In IEEE, Transactions on Network

To overcome these issues, we combine, in this work, deep reinforcement learning and relational graph convolutional neural networks in order to automatically learn how to improve