What if dividends were tax-exempt? : evidence from a natural experiment

Texte intégral

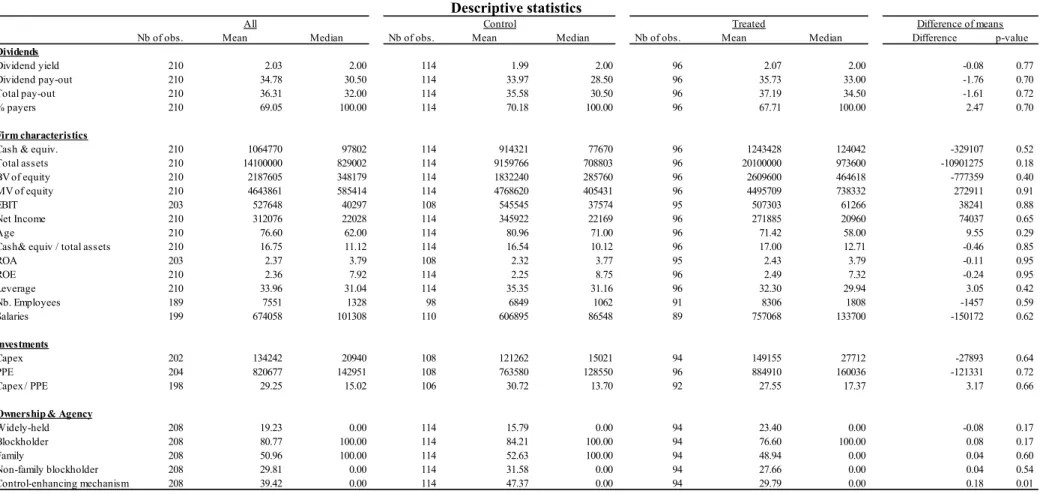

Figure

Documents relatifs

Benzo-fused analogues of the indeno[2,1-c]fluorene skeleton containing the as-indacene core have been synthesized. The addition of the extra benzene ring enables

Le rôle de l’hôpital Broca dans ce projet a été dans un premier temps de recueillir les besoins des personnes âgées, de faire émerger leurs opinions et d’observer

ing Specular Neutron Reflectivity; all experimental details concerning GISAXS measurements; description of protocols designed to transfer the PS-b-PAA monolayer onto

facteurs déclencheurs des crises d’épilepsie (habituellement aigus comme une hyponatrémie). 3) L’existence d’un « faible facteur déclenchant » qui serait

Although this is stronger than 100 nT quoted by Pulkkinen (1996), type I spikes could be the ab- sorption signature of pseudobreakups due to their short and sharp temporal

The adaptations of the YOUNG-INT group were consistent over directions in both, anticipated and non-anticipated perturbations (see Fig. The older training group, however, decreased

[r]

L’infection, les luxations et le descellement constituent la majorité des complications de la chirurgie prothétique de la hanche, mais l’infection de prothèse