Risk and Financial Management Article Systemic Risk Indicators Based on Nonlinear PolyModel

Texte intégral

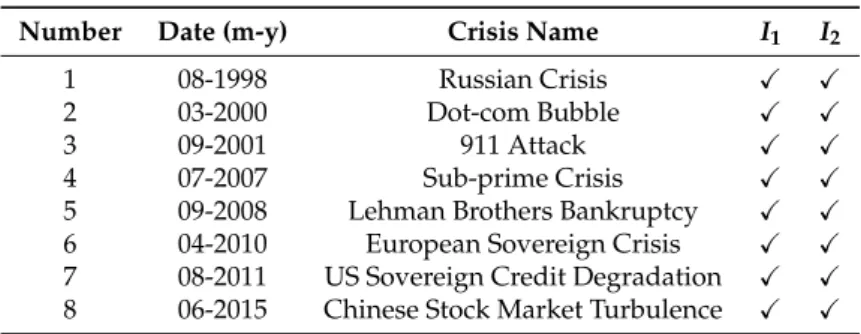

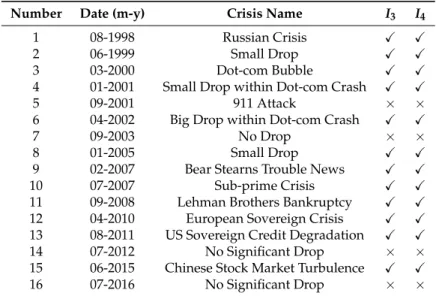

Figure

Documents relatifs

Hence, the measured 1.3mm residual dust is in strong agreement with the magnitude of the attenuating line-of-sight circumbinary disk material, and its location and orientation is

Le Palais Rouge était la base des rois de Bani Nasr. Ceroyaume a défini le plan du jubilé, commeun mode entre l'autorité et la paroisse. Le ministère est considéré

De l’algorithmique au C - v1.1 – p.. Passage de paramètre par valeur.... Passage de paramètre par adresse.... Traduire écrire .... ) La chaîne de formatage spécifie le type

Even more recently, a polynomial description for the neutron flux has been introduced [2]: along the axial (extruded) direction a per-region constant (“step-constant”)

An exploration of Uranus or Neptune will be essential to understand these planets and will also be key to constrain and analyze data obtained at Jupiter, Saturn, and for

Les résultats de l’analyse des actes de prise en charge en chirurgie de la verge et des organes génitaux externes sont présentés dans la figure 12 et les éléments les

Premièrement, il fait état des quatre bords du cadre, latéral (gauche et droite), inférieur et supérieur, le cinquième renvoie à l'espace situé derrière la caméra

Chez Ford, on peut noter que la pluralité des plans par rapport au tableau On the Fence– dans l’un, on voit les jambes nues, le ciel, dans l’autre il y a un chapeau, un homme –