Particle methods in finance

Texte intégral

Figure

Documents relatifs

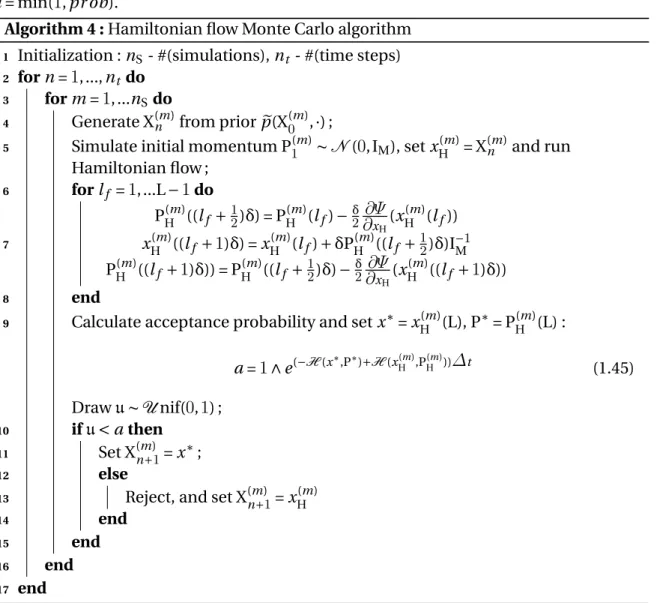

To tackle large dimensions, other methods have been devised that are based on a non-independent sampling: Markov chain Monte Carlo methods (MCMC).. The prototype of MCMC methods is

FLØTTUM,,,, les sources d’inspiration de cette recherche, pour leur générosité et pour le rôle qu’elles ont joué dans l’élaboration de ce travail. Un grand merci à ma

It is of course possible to generalize the little example from a probability λ = 1/6 to a general value of λ, and from a single spin to a general statistical mechanics problem

This approach can be generalized to obtain a continuous CDF estimator and then an unbiased density estimator, via the likelihood ratio (LR) simulation-based derivative estimation

When & 2 − & 1 becomes small, the parameters of the beta distribution decrease, and its (bimodal) density concentrates near the extreme values 0 and 1.. 82) say in

A methodological caveat is in order here. As ex- plained in §2.1, the acoustic model takes context into account. It is theoretically possible that the neural network learnt

The remediation of toxic metals by plant can be divided into two most important strategies: (1) phytostabilization: plants are used to stabilize contaminated soil from the

In the case of a trigger having inputs that belong to different remote triggers, the Subscription Manager implements the simple strategy of installing default