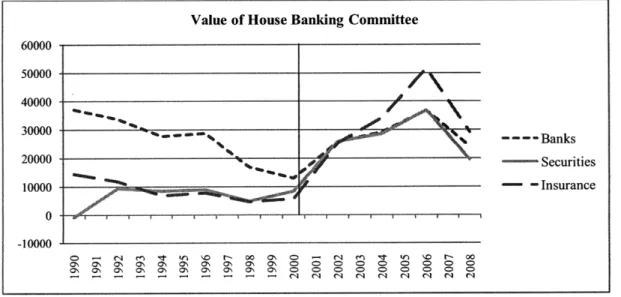

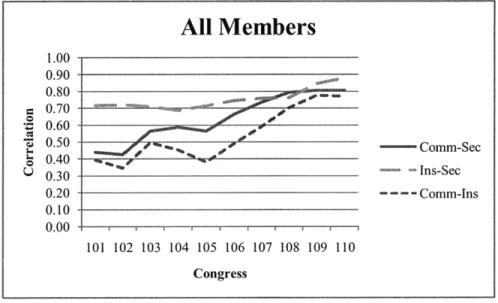

Congress and the Financial Services Industry, 1989-2008

Texte intégral

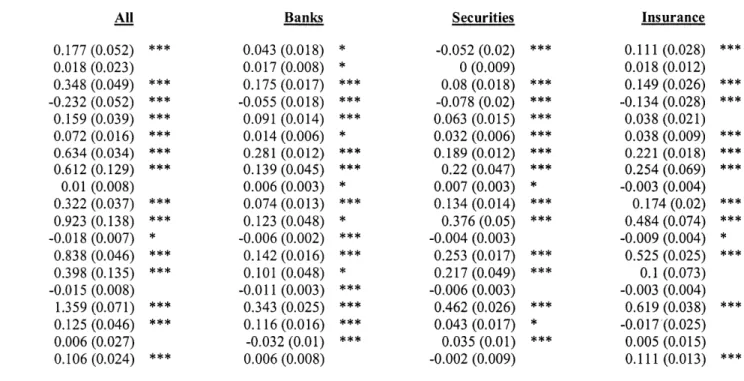

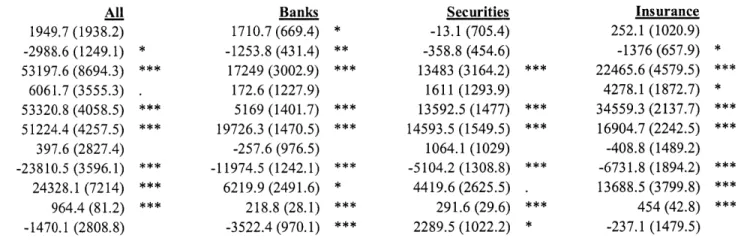

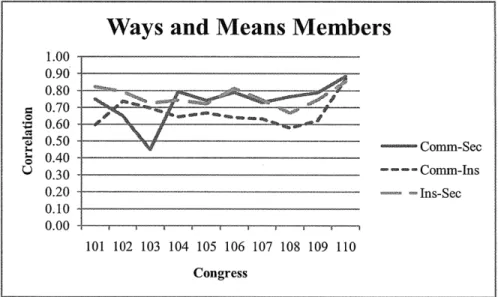

Figure

Documents relatifs

If the contract is awarded to a tenderer intending to rely on another entity to meet the minimum levels of economic and financial capacity, the Contracting Authority may require

In contrast, this research provides evidence that a common governance infrastructure can create a ‘common mechanism’ that would prioritise risks, support

financial performances has been generated by the world economic crisis and European regulation adjustment in the cosmetic industry. The most important result shows the Ln_E has

In order to recreate a 3D Cartesian space distribution, the helicoidal ion coordinates can be mapped back to Carte- sian space with respect to a chosen helical axis, with typi-

French authorities — both in the public sector and banking sector — were generally unwilling to raise the prospect of EU-wide financial instability caused by

The estimated parameters of the cost function with their standard errors are presented in table 2. These estimates are obtained using the wage rate w, which is corrected

[r]

Net-present value approach to determine yearly cash flows Reflecting on farmers’ performance: High costs vs.