MIT LIBRARIES DUPL

IIIHIIIIIIIIIIIMI

3

9080 02617 8233

Digitized

by

the

Internet

Archive

in

2011

with

funding

from

Boston

Library

Consortium

Member

Libraries

1

15

c4

->i

Massachusetts

Institute

of

Technology

Department

of

Economics

Working

Paper

Series

BANKING

AS

AN

EMERGING

TECHNOLOGY:

HOARE'S

BANK

1702-1742

Peter

Tern

inHans- Joachim

Voth

Working

Paper

04-01

Dec.

4,2003

Room

E52-251

50

Memorial

Drive

Cambridge,

MA

021

42

This paper can be

downloaded

without charge from theSocial Science Research

Network

PaperCollection atMASSACHUSETTS

INSTITUTEOF

TECHNOLOGY

JAN

1 52QM

Banking

as

an

Emerging

Technology: Hoare's

Bank

1702-1742*

Peter

Temin

and

Hans-Joachim

Voth

Abstract

Analysis of the financial revolution in England has often focused on

changes in public debt management and the interest rates paid by the

state.

Much

less isknown

about the evolution of the financial systemproviding credit to individual borrowers.

We

document the transitionfromgoldsmith tobanker in the case ofRichard Hoare, andexamine the

operation ofthe loanmarketduringthe early eighteenthcentury. Learning

how

to use therelativelynew

technologyofdepositbanking was crucial for thebank's success and survival. Innovation duringthe early stages ofthe British Industrial Revolution was not limited to manufacturing and

transport, butplayedacritical rolealsointheservice sector.

Keywords:

Banking

and

credit, English Industrial Revolution, interestratedetermination, credit rationing, technological

change and

learning.JELcode:

G21, N23, N83, 016,

031.

We

thank Henry Hoare for kindly permitting access to the Hoare's Bank archives, and to VictoriaHutchings and Barbra Sands for help with the ledgers. Claudia Goldin, FarleyGrubb, Ephraim Kleiman,

Bob

Margo, Petra Moser, Dick Sylla and Stephen Quinn helped us with their comments; seminarparticipants at Harvard offered important suggestions. Financial support by the Leverhulme through a Philip Leverhulme Prize for Hans-Joachim Voth is gratefully acknowledged. Chris Beauchamp, Anisha

1.

Introduction

London's

financialmarket

underwent

a dramaticchange

after 1700.While more

limited than Paris or

Amsterdam

in the 17th century,London became

the leadingfinancial center in

Europe

in the 18th.There

is an extensiveand growing

literatureon

thecauses

of

this change, butcomparatively

littleon

thechange

itself. Thispaper

providesdetailed information

on

the operationof

theLondon

financialmarket around 1700

by

describing the actions

of

a nascentLondon

bank.We

have

awindow

intoan

importantmarket

during aperiodof

dramatic change.Our

view

is into the detailed recordsof

aWest

End

bank

in its formative years,during a crucial period

of

London's

evolution as a financial market.Richard

Hoare

was

agoldsmith

who

moved

to Fleet Street in1690 and

began

tomake

the transitionfrom

all-purpose jeweler

to banker.He

was

successful in this effort,and

Hoare's

Bank

still exists as anindependent

private bank, operatingfrom

thesame

address asRichard

Hoare

and

serving a selected

group of

families,some

of

whom

have been

with thebank

formany

generations

-

sometimes

from

the 1700s.The

Bank's

archives contain records for theearly 18thcentury that

document

the processby

which

Richard

Hoare

made

the transitionfrom goldsmith

tobanker.The

increasing sophisticationof

Richard

Hoare

and

his successorscan be

seen as the learningneeded

in the useof

new

technology. Initially,when

switchingfrom

goldsmith

to banker,Richard

Hoare had

toadopt

banking

practices thathad

been

in use atmerchant banks

for a while.Once

Hoare's

had

caughtup

with

eighteenth-century "bestpractice",

he

joined a selectgroup of

West End

bankers thattransformed

the processof

creditprovision.

Hoare

did not introduce anew

spinning device, buthe

was

engaged

inanew

economic

activity, the extensionof

credit outside the tight-knitcommunity

of

merchants, or the

even

smallercommunity

of

princely rulers. Organizationand

operatingprocedures

had

tobe

created almostwithout

priormodels.

This

is not todeny

theexistence

of

banks

before 1700, but rather to note that theywere

specialized almost exclusively in the financingof

trade, in providingpayment

servicesand

extending loansto a small

group of

international merchants.1We

assert that to switchfrom goldsmith

tocredit intermediary at that

time

was

to venture into a largelyunknown

activity.2 Just asthe use

of any

new

machine

requires a processof

learningand

adaptation, so too theintroduction

of

commercial

banking

to thewider

publicof

London

required organizational innovationby

Richard

Hoare and

his associates.He

was

not alone in this exploration.Hoare's

joined a smallgroup of goldsmith

bankers

such

as Child's, a handfulof

financial pioneers.3 Joslinobserved

that itwas

notuntil

1725

thattherewere two dozen

privatebankers

intheWest

End;

thetotalnumber

of

banks

inLondon

did notexceed 42

in 1700.Many

firmsand

individuals drifted into thebanking

business,only

to give itup

after afew

years-

most

bankers

in1700

were no

longer in the business

by

1725.Richard

Hoare

learned faster than most,and

Hoare's

Bank was

a survivor.This transition is

of

interest to three separate literatures. First, the discussionof

the long-run

development

of

financialmarkets

makes

frequentmention of

the transitionwe

observe, butseldom

containsmuch

about the actual process. Kindleberger, forexample,

dated the transition to themiddle of

the 17th century, citing the experienceof

afew

goldsmiths withoutmuch

informationabout

theirbanking

activities.5He

also failed tomake

the important historical distinctionbetween

thegrowth

of

merchant bankers

concerned

with international tradeand

privateLondon

bankers

extending creditdomestically.

The

principal innovation that occurred in the transitionfrom

goldsmith

tobanker

was

to provide credit to agrowing group of

clients-not just theking

and

afew

noblemen

and

merchants-and

to finance this lendingthrough

deposits.One

of

themost

1

L. Neal, The Rise ofFinancial Capitalism (Cambridge: Cambridge University Press, 1990); Stephen

Quinn, "Goldsmith-Banking: Mutual Acceptance and Interbanker Clearing in Restoration London,"

Explorations inEconomicHistory 34,no.4 (1997);

Herman

Van

derWee, "Monetary,CreditandBankingSystems," in The Cambridge EconomicHistory of Europe, ed. E.E. Rich and C.H. Wilson (Cambridge:

CambridgeUniversityPress, 1977).

2

Earlierbankers had learnedtheir trade in the form ofapprenticeships,but again, theirmainbusinesswas

either in offering payment services or very limited access to credit. Cf. Quinn, "Goldsmith-Banking:

Mutual Acceptance andInterbanker ClearinginRestorationLondon," .

3

Stephen Quinn, "The Glorious Revolution's Effect on English Private Finance:

A

Microhistory,1680-1705," Journal ofEconomic History 61, no. 3 (2001).

We

thank Stephen Quinn for pointing out thatinitially, Hoare's was simply adopting practices pioneered by other goldsmith banks that had

made

theswitch atanearlierstage.

4

D.M.Joslin,"LondonPrivateBankers, 1720-85,"EconomicHistoryReview7 (1954).Quinn,

substantial

goldsmith

bankers,Alderman

Backwell,

lent very considerablesums

toCharles II, as did other

goldsmith

bankers.6 Their businesswas

notfundamentally

different

from

thatof

theFugger

in the 16th centuryand

of

the Ricciardi in thefourteenth.7

Goldsmith banking

in the late seventeenth centuryhad

alreadyprovided

forefficient

payments,

and

itallowed customers

tokeep

their surplus cash in a safe place."Scriveners offered the

kind

of matching

servicesprovided

by

Paris notariesthroughout

the eighteenth century,

and

also accepted deposits.Yet

in contrastwith

theFrench

experience,

banks

and

not notariesbecame

thekey

financial intermediaries inEngland.

The

transitionwas

gradual.Competition

continued foran extended

period, given thatwe

find scriveners

mentioned

as importantmiddlemen

as late as 1713. Also,Hoare's

itselfwould

passon mortgages

to itscustomers

ifitdidnotwant

to takethem

itself."Second,

thesewere

turbulent years forLondoners

involved in finance.North

and

Weingast argued

that the GloriousRevolution of 1688

putgovernment

financeson

asolid footing providing a

base

on which

theLondon

financialmarket

couldgrow.

~They

also

emphasized

theimportance

of

financialdeepening

forsubsequent

economic

development, an

argument

that is in line with recentmacroeconomic

research.13This

claim has recently

been

disputedthrough

anexamination of

private interest ratesby

Clark

and

by

Quinn.

14Sussman

and Yafeh, examining

yieldson

government

bonds,claimed

5

Charles P. Kindleberger,

A

Financial History of Western Europe, 2nd ed. (Oxford: Oxford UniversityPress, 1993),p.53-4.

6

R.D. Richards, The Early History of Banking in England (P.S.King

&

Son, 1929), p. 67-73. See alsoQuinn,"Goldsmith-Banking: Mutual Acceptance andInterbankerClearing inRestorationLondon," .

7

Kindleberger,

A

Financial Histoiyof Western Europe,p.448

One

ofthe earliest recordskept at Hoare's bank details paymentsmade

onthe note ofSamuel Pepys in1680. While Pepys had an overdraft with the bank, most other customers deposited funds first, and then

made

payments through notes presentedat thebank (Richards, The EarlyHistoiyof Bankingin England,Appendix2).

9

Philip T. Hoffman, Gilles Postel-Vinay, and Jean-Laurent Rosenthal, Priceless Markets : The Political

Economy

ofCredit inParis, 1660-1870 (Chicago: TheUniversity ofChicago Press, 2000); Richards, TheEarlyHistoiyof BankinginEngland.

10

An

Act underQueenAnn

(12Anne,Stat. 2,c. 16, s. 2)mentionsthem prominently (Richards, The EarlyHistoiyof BankinginEngland,p. 17).

" HenryPeregrineHoare,Hoare'sBank.

A

Record1673-1932 (London: ButlerandTanner, 1932).' Douglas North and Barry Weingast,

"Constitutions and Commitment: The Evolution of Institutions

GoverningPublicChoiceinSeventeenth-Century England,"Journal ofEconomicHistoiy49, no.4(1989).

13

Ross Levine and Sara Zervos, "Stock Markets, Banks, and Economic Growth," American Economic

flevfew88(1998).

GregoryClark, "ThePolitical Foundationsof

Modem

Economic Growth: England, 1540-1800," JournalofInterdisciplinaryHistoiy26, no.4 (1996); Quinn, "TheGlorious Revolution's EffectonEnglish Private

that the financial innovations

needed

topay

forEngland's wars

in the early 18th centurywere

more

important for thedevelopment

of

the financialmarket

thanany

constitutionalchange

in 1688.15O'Brien

alsoemphasized

thatKing

William

involvedEngland

in aseries

of expensive

wars,and

brought with

him

Dutch

bureaucratswho

facilitated thefinancing

of

his martial ambitions.This

broad

view

supports themore

technicalarguments

made

by Sussman

and

Yafeh.Authors

from Ashton

toBrewer and

Ferguson have noted

the elasticsupply of

17

savings in 18th century

England.

The

government

was

able toborrow

freely, financingits military adventures

without

causing interest rates to risemuch,

and without causing

French-style crises.

While

the literature focuseson

thegovernment's

ability toborrow,

itcontains the corollary that private savings

were

increasinglychanneled

through

thefinancial

system

-

and

that,when

the countrywas

at peace,numerous

individualscould

borrow

as well. Joslin articulatedthis position in a qualitativesurvey of

privatebanks

in1Q

London.

He

argued

that the privatebanks loaned

domestically,while

quite separatemerchant houses provided

credit for trade, asdescribedby

Neal.1Quinn

recentlymade

a starton

the quantificationof

the privatedomestic

financialmarket.

He

analyzed

the recordsof

Child'sBank,

testing theNorth

and

Weingast

hypothesis.20

Quinn

therefore did not detailhow

London

banks

operated in these criticalyears.

He

alsoassumed

that earlyLondon

banks

were

thoroughly

modern

in theirdomestic

operations,perhaps

by

analogy with

the sophisticated international transactionsof merchant

banks.We

assert that thisanalogy

is not validand

thatdomestic bankers

atthe start

of

the 18th centurywere

entering anew

business, serving anew

clientele.This

was

symbolized

by

theirmoves

from

the City to theWest

End; Hoare's

Bank

moved

to alocation just steps

away

from

the Strand.Nathan Sussmanand Yishay Yafeh, "Constitutions andCommitment: Evidence on the Relationbetween

InstitutionsandtheCost ofCapital," unpublishedmanuscript,

Hebrew

University,Jerusalem(2002).16

Patrick O'Brien, "Fiscal Exceptionalism: Great Britain and Its European Rivals

—

from CivilWar

toTriumphatTrafalgarandWaterloo,"

LSE

EconomicHistoiyWorkingPaper65 (2001)17

T.S.Ashton, TheIndustrialRevolution, 1760-1830 (London,

New

York[etc.]: OxfordU.P., 1968);JohnBrewer, The Sinews of

Power

: War,Money

andtheEnglish State, 1688-1783, 1stAmer. ed.(New

York:Alfred A. Knopf, 1989);NiallFerguson, TheCashNexus:

Money

andPower

in theModern World,1700-2000

(New

York:BasicBooks,2001).18

Joslin,"LondonPrivateBankers, 1720-85," .

Neal, TheRiseofFinancial Capitalism.

20

Third, the process

of

learningundertaken

by

the firstWest

End London

banks

isthe

same

as the processes involved in the adoptionof

othernew

technology. Productivityin services industries

can

be

akey

determinantof

aggregateeconomic

performance."1Entrepreneurs using a

new

machine

or adopting anew

production process oftenhave

tocontend

with a periodof

low

earnings while they adapt procedures,change

the layoutof

factory building,

and

locate their markets.This

period often isaccompanied

by

low

profits,

and even

by

frequent failures."" Joslinnoted

the very highattrition rateof

aspiringWest

End

bankers

in theearly 18th century.Hoare's

bank

was

one of

the successful ones,which

ishow

we know

about

its experience.Our

argument

is similarto theone

advanced by

Alfred Chandler."He

chronicledchanges

in business structuresand

strategies in a seriesof volumes,

arguing thatchanges

in

managerial

practiceswere

innovations as important as introducingnew

machines.

Hoare's

Bank

did nothave

any

new

machines

to use; itwas

extending its expertise intonew

dimensions.There

had

been

goldsmithsand merchant

bankers, butonly at theend of

the 17th centuiy

were

afew

pioneers bringing thesetwo

activities together.Hoare's

was

one of

these pioneers, extending credit to aWest End

clientele in thecompany

of

only asmall

group

of

peers.As

Chandler

did,we

use the recordsof

a successful business torepresent

changes

in the industry.We

describe aspiringbankers

around

1700

in the processof

learninghow

tooperate as a deposit-taking bank.

They

experimented

with all aspectsof

their business,from

theamount

of

required reserves to the treatment of familymembers.

The

transitionfrom goldsmith

tobank

was

gradual,and

thebank

conducted

business that it later shed,such

as acting asan

elevatedpawnbroker

and

amortgage

broker.Bankers

thereforeengaged

in amore

variedmenu

of

activities than amodern

bank, only learningover

time"' StephenBroadberryand Sayantan Ghosal, "From

theCounting Houseto the Modern Office: Explaining

Anglo-American ProductivityDifferences in Services, 1870-1990,"Journal ofEconomicHistory 62,no. 4

(2002).

""

JoelMokyr, The Lever of Riches : TechnologicalCreativityand EconomicProgress

(New

York: OxfordUniversity Press, 1990). Paul David and Gavin Wright, "General Purpose Technologies and Surges in

Productivity: Historical Reflections on the Future ofthe let Revolution," in Economic Challenges ofthe

21stCentuiyinHistorical Perspective,ed. Paul David (London: 2003);A. Hornsteinand P. Krusell,"Can

Technology Improvements Cause Productivity Slowdowns?," in Nber Macroeconomics Annual, ed. J.

which

activitieswere

dependable

and

profitableenough

to endure. It is this processwe

try to illuminate.

Hoare's

Bank

kepttwo

kindsof

accounts in addition to theircorrespondence.One

ledger

recorded

the periodicbalancing of

thebank's

books

in theform of

periodicbalance

sheets.The

loan registerwas

a sequential recordof

loansmade

by

the bank,whether

forinterest or not.We

first analyze thebank's

balance sheets,and

thenproceed

by

describing the natureof Hoare's

accountsand our

treatmentof them.

Only

thencan

we

discoveran

'average' interest rate in private transactions,whose

meaning

we

willexplain

below.

Finally,we

analyze thelearningprocessof Richard

Hoare

and

hispartners thatis ourprimary

focus.2.

Balance

Sheets

One

typeof

ledger kept atHoare's

contains annual totals for thebanks

assets,liabilities,

and

profits.The

bank's

total assets fluctuated stronglyfrom

year to year,reflecting the short-term nature

of

many

loansand

deposits, as well as varying levelsof

capital

committed

tobanking

activitiesby

the partners at Hoare's. Total asset values areshown

in Figure 1up

to 1742,with

only afew

missing

balance sheets during theSouth

Sea Bubble.

In the firstyear

after the "initial" accountswere

drawn

up,Hoare's

assetsjumped

from

£146,000

to£207,000,

but then declined;by

1711,Hoare's

lendingand

otheractivities

were

smallerthanin 1702.The

high point in1703

was

not surpassed until1720, during the

South

Sea

Bubble

itself,and

itwas

followed

by

a sharp contractionand

wide

swings

in overall lending activity.Only

after surviving the financialchaos of

theSouth

Sea

Bubble

didHoare's

assetsbegin

togrow

steadily, except for atemporary

windfall in 1727/28.

The

troubledtwo

decades

prior to theSouth

Sea

Bubble

appear

tohave

been

a periodof

learningand

exploration. Itwas

only after thebubble

thatHoare's

Bank

found

amodus

operandi

thatgenerated sustained growth.Alfred Dupont Chandler, Strategy andStmcture : Chapters in theHistory ofthe IndustrialEnterprise

(Cambridge,Mass.: M.I.T. Press, 1990); idem,Tlie Visible

Hand

: TheManagerialRevolution inAmericanSize ofbalance sheet

600,000

1702 1704 1706 1708 1710 1712 1714 1716 1718 1720 1722 1724 1726 1728 1730 1732 1734 1736 1738 1740 1742

Figure 1

Just as in the case

of

modem

balance sheets,Hoare's

was

separated into assetsand

liabilities. Assetswere

grouped

into sixbroad

categories-

goldand

silver,diamonds

and

pearls,"money

due

as lentupon

interestand purchasing

stocks", loans withoutinterest, "several people for plate",

and

a balanceremaining

in cash.The

composition

of

Hoare's

assets isshown

in Figure 2.Some

of

the assets inthe1702

balance sheetappear

to

be

theremnants

ofHoare's goldsnuthing

business-

such

as the£9,489

the firm held inSeptember

1702

in theform of

precious metalsand

stone.Loans

tocustomers

for platefall into the

same

category. In hisdays

as a goldsmith,Richard

Hoare

had

financedclients' purchases

of

jewelry,with

banking

operations facilitating the transaction in thesame

way

as the finance divisionsof

GM

orFord today extend

loans tocustomers

wishing

tobuy

their cars.The

bank

also acted as abroker

for its customers, executingtrades in a variety ofsecurities

-

and

financingthepurchases via short-term loans.The

initial balance sheetshowed

about two-fifthsof Hoare's

assets stillwere

in the goldsmithing businesswhen

this first balance sheetwas drawn

up."Customers

diamonds and

pearlsaccounted

foran

additional eight percentof

assets.These

assetsquickly declined as a share

of Hoare's

total; thebank

terminatedalmost

allof

itsgoldsmithing

activitiessuch

asproducing

silverware,mending

plateand

craftingjewellery,

and

redirectedits activitiestoward

banking. Assetsused

forgoldsmithing

were

initially replaced

by

loanswithout

interest,which

may

be seen

as holdoversfrom

thegoldsmithing

business.They

show

Hoare's

providing liquidity tosome

of

its customers.We

cannot

know,

how many

of

these interest-free loanswere

courtesies to oldcustomers

and

how many

were

introductory offerings to potentialnew

customers.At

leastsome

non-interest loans

and

lendingtocustomers

for plateappear

tobe

partof

apawnbroking

operation.

The

largest individual categoiyof

assetsthroughout

the early 18

th

century

was

loans against interest (as well as

money

lent for securities purchases), fluctuatingaround

half

of

the balance sheet.Loans

bearingno

interest (but not for plate) declined relativelyquickly.

The

firmextended

62

loanswithout

interest in 1704;by

1721, therewere

only13 transactions inthiscategory.

Richard

Hoare

appears tohave

taken longertoreduce

thevolume

of

loanswithout

interestthanhe took with

loans against plate, buthe

clearlywas

reducing

both

in the firstdecades

of

the 18l century.As

he

learnedbanking

and

conceptualized

himself

as abanker,he

moved

outof

these otheractivities.The

years beforeand

during theSouth

Sea

Bubble

showed

a rise in the shareof

cash holdings.

As

theLondon

financialmarket

entered a periodof

great turbulence,Hoare's

Bank

reverted tosome

of

its older practices toweather

the financial storms.For

1718, there

were

£28,189 of diamonds,

pearls,gold

and

silveron

the balance sheet,equivalent to

one

fifthof

its total value.These

assetsof

Hoare's

previous professiondecreased

inimportance

during the 1720s, butwere

not totallyabandoned

adecade

after the bubble. Offsetting this conservative stance,Hoare's

also invested in thenewest of

financial instruments:

South Sea

stock, hi 1720,when

the accountswere

drawn up on

June

24

th,and South Sea

stock stood at 250, thebank had

14 percentof

its assets investedinit.

The

bank

continued to trade (andhold

positions) inSouth Sea

stock after thebubble

deflated,

even

though

these transactionswere

not capturedby

successive balance sheets(usually

drawn

up

in September).Some

dealing inSouth

Sea

stockwas

recorded as late as 1731.Compositionofassets

m

OSouthSeastock loansforplale olcustomers

siNrer.gold,diamonds,pearls loans without interest

acash

nloansagainsl interest

1702 1704 1706 1708 1710 1712 1714 1716 1718 1720 1722 1724 1726 1728 1730 1732 1734 1736 1738 1740 1742

Figure2

Cash

balances rose sharply as a percentageof

all assets after theend of

theSouth

Sea

Bubble-where

thebank

had

made

do

with£100

before the crisis, itnow

kept£172

inliquid funds.25 If

withdrawals

had

followed anormal

distribution, thebank

would

have

faced a 3 percent

chance of running

outof

cashand

consequently

facinga crisisevery 30

years. After the bubble, the

bank

reduced

the risk toonce

every 1,500 years.26This

is ahighly conservative stance, but

may

have been warranted

in aworld

without a lenderof

last resort

when

all theHoare

family assetswere

inthe bank.We

tested the hypothesis that asset allocationschanged

significantly after 1720.The

tests aresummarized

inTable

1.The

shareof

assets in loans against interest did notchange

much

after 1720.The

shareof

cash increasedenormously and

significantly,from

20

percent to34

percentof

assets.Hoare's

had

been

scaredenough by

the turmoilof

the" This result assumes thatvariances

are equal. If

we

allow forthe possibility of unequal variances, thet-ratio falls to3.93, equivalentto asignificance levelof99.93percent.

16

We

calculated the average cash balanceand the standard deviations, andderived the probability ofthereserve ratio falling belowzero.There isgood reasonto think thatdepositwithdrawals follow alognormal

distribution,which would

mean

thatbank'srisk ofrunning out ofreserveswasmarkedlyhigherbeforeandafter 1720 - and that the relative difference is probably somewhat smaller. Cf. Roger Chen and Dale

bubble

years towant

amore

securecushion

against a recurrenceof

financial turbulence.The

rise incash

was

accomplished

by

an almost

equally large fall in the shareof

non-interest bearing loans after 1720.

Hoare's

thus did not losemuch

revenue.This

findingdocuments

our

assertion thatHoare's

was

learninghow

to charge interest forits loans, asbankers

do.The

gamble

of

providing interest-free loans frequently in the earlier years inan effort to stimulate loans later

seems

tohave

paid off. It also is interesting thatwhile

the process

was

gradual,we

can

see acceleratedchange

after 1720.This confirms

ourview

thatthe learning period forthisnew

activitywas

alongone. 7Table

1:Asset

Shares

atHoare's

-

before

and

aftertheSouth Sea

Bubble

pre-

1720

1720-42

difference t-statistic +interest-bearingloans 51.8 52.8 1 0.22

Cash

19.6 33.8 14.24.13*

non-interestbearing loans 19.8 9.9 -9.9 3.2*

loans forplate

purchases

3.5 0.24 -3.26 2.2*Plate 4.7 1.9 -2.8 0.74

Note: indicatessignificanceatthe

1%

level+

assumingequal variances

The

examination of Hoare's

assets clearlyshows

abank

in themaking.

Startingfrom

abase

in thegoldsmith

business,Hoare's

began

to loanmoney

both with

and

without interest. Gradually,

over

the courseof

a generation, thebank abandoned

its previousmodes

of

activity.To

seehow

modern

thebank

inthe early 18

l

century

was,

we

need

toexamine

its liabilities aswell asits assets.Hoare's

liabilitieswere

recorded

as depositsby

individualsof

cash,money

owed

for plate

and

jewels, debts to goldsmithsand

jewelers (as well asemployees,

insome

years), the capital

of

the partner(s), plusprofits for the past year.28 In 1702, forexample,

Osborne,

"Random

Deposits, Liquidation Discount and Deposit Insurance Pricing," University ofTexasworkingpaper(2002).

1

We

experimentedwith our sample selection,excluding thesomewhat unusual yearof 1718-the resultswerealmostidentical.Theyareavailablefromtheauthors uponrequest.

8

This practice changed in later years,

when

the partners' capital is subsumed under the category ofamounts duetoothers.

Richard

Hoare

held£31,788 of

thebank's

capital.29

The

bank

alsoowed

£113,997

todepositors, as well as

£537

for plateand

£42

to "several plateworkers

and

otherworkmen".

From

1703 onwards,

Henry

Hoare was

inpartnership with his father,Richard

Hoare,

and

profitswere

dividedaccording

to a 2/3rd, l/3rd

allocation formula.

Both

Hoare's

appear

tohave

kept substantial fractions oftheir fortune invested in the bank.By

1706, forexample,

we

seethem

dividing profitsof

£1,839.Henry Hoare

also received£241

for intereston

the£4,029 he

had

invested inthe firmby

then (for an interest rateof

exactly 6 percent). In the

same

year, his father's invesmient stoodat £52,934.Equity in the firm fluctuated considerably

from

year to year, as theHoares

invested in the

bank

insome

yearsand took

money

out in others.By

1710,Henry

and

Richard

Hoare

togetherhad

investmentsworth £74,939

in the bank, equivalent to44

percent

of

all liabilities. In 1720,Henry Hoare was

in businesswith

Benjamin

Hoare, hisson, yet their

combined

equity in thebank

onlyamounted

to £39,608,approximately

halfthe partner's capital in 1710.

Family

events,such

as the deathof an

individual partner,were

important determinantsof

theamount

of

business the firmcould

undertake,and

of

its financing structure.

The Hoare

family did not attain the favorableupward

trendof

joint equity until after the initial learning period.

They

clearlywere

invested (financiallyand

materially) in thebank

for the long term, althoughRichard

Hoare

did not live to seehisson

and grandson

create a steadilygrowing

business.Note that, with unlimited liability partnerships, this concept of equity in the family firm is somewhat artificial. Yet Hoare's usedthisas a distinctcategory ofliability,anditisnot identicalwithcash-on-handat

the timeofdrawing upbalancesheets.

Returnon AssetsandEquity,LeverageRatio 20.0% B 10.0% / \returnonequity1 / \" i

—

i i i i , i iA

i i .^

i—

\—

; 1 1 1 1 1 1 1 1 \A — ' §* L-W

[ \ | | | | [ | | |iAi

leverageratio1 , -i — m— i— i— i 1 1 i i. 1 1 1 1 1 1 1 i-i—

i 1 1 l_: ;a\**

: ;a ; / ; ; ; : :"^rtT

"T

V! 4! "1\~Y'~~

"TA

\\

/v •, i / . :A

</v-A' ' ;' * /v ! t\ ' Al i .Oi : Or< :O

c>-<^

tt ro 1a

J

! ! ! ! !__p] ! : relurnon assets1' ' "v-/ ~ l . "*,.I

i i i i i • returnon assets i i i i iiii

o

i—

: 12.00 2.00 *withoutinterest paidonpartners' . equity 1702 1704 1706 1708 1710 1712 1714 1716 1718 1720 1722 1724 1726 1728 1730 Figure3The

partners atHoare's

leveraged theirown

investment

inthebank

via themoney

kept in the cash accounts

of

their clients. Since theirmove

to Fleet Street, thebank

as ageneral rule

no

longer paid intereston

the depositsof

its clients.30

Before

theSouth

Sea

Bubble,

the sizeof

the balance sheetstended

tobe

between

2and

6 times largerthan theequity

of

the Hoares. Thereafter, theHoares

appear

tohave

been

more

aggressive,with

aleverageratio thatrose rapidlyto 12

by

1725.The

years aftertheSouth

Sea

Bubble saw

amarked

reductioninpartner's equity- down

to aminimum

of

£16,567

in 1723, amere 22

percent

of

the pre-bubble peak.The

balance sheet did not contract to thesame

extent,leading to higher leverage.

At

itsmost

extreme,Hoare's

had

approximately

£11

pounds

in assets for every

pound

of

partners' equity. This is aremarkably

low

figure for abank

that ultimately survived for centuries

-

the Basel I accords forcemodern

banks

tomaintain a similarequityratio to fulfill capital

adequacy

requirements.50

Richard Hoare to

Madam

Jane Hursey, dated Oct. 9th

, 1703, cited in: Hoare, Hoare's Bank.

A

Record1673-1932,p. 16.

The

decline in equity is themirror-image

of

the rise in cash holdings.The

two

changes

appear in facttobe

largely offsetting.Richard

Hoare

may

have

initially acted as a goldsmith,where

his equity stoodbehind

his offerings. This practice carriedover

to thebanking

business,and Richard

and

Henry Hoare

may

wellhave

tided overthebank

with

their personal assets in the

hard

years after 1710.They

certainly derived little orno

income

from

thebank

in those years. After theSouth Sea Bubble,

the partnersappear

tohave used

cash reserves to serve the function that their equity formerly had.Cash

would

deal with

temporary

fluctuations indemand,

and

only inextreme

caseswould

thepartners' equity

be

called upon. After 1720, the balance sheetof

Hoare's

bank began

toresemble

amodem

bank's

balance sheet, albeitavery

conservativemodem

bank.Only

some

informationon

profits survived.The

bank

calculated "excess profits",after

paying

intereston

partners' capital.We

calculate the overall return, includinginterest

payments.

The

average

returnon

assets fluctuatedbetween

2and

4

percent.But

while

Hoare's

bank

showed

a gainof

2.7 percenton

assets in 1703, this translated into areturn

on

equityof

15.8 percent.The

following yearwas

the best thebank had

beforetheSouth Sea

Bubble.The

balance sheet contracted modestly, but profits roseby

12 percent.The

Hoares took

capital out,and

their returnon

equity accordinglyrose to 19 percent.By

1710, gearing

had

declinedto 1:2.2,and

theexisting assets generated a verylow

returnof

only 2.5 percent. This translated into a return

on

equityof

5.5 percentfor thisyear.While

"excess" profits

had averaged £2,775

in prior years, theydropped

to£216,

leavingHenry

Hoare, as thejuniorpartner,with

£72

for his efforts in 1710.Between

1702

and

1715, thepartners earned 10 percent

on

average,and probably

less.The

Hoare's

did receive areturn over

and

above

the interest thatthey couldhave earned

iftheyhad

put theirmoney

into (relatively safe)

government

bonds, but themargin

was

at timesvery

small."' In1710

and

thereafter, it appears that the partnersmight

have

been

at a point toabandon

thebusiness,but

Hoare's

Bank

didnot closeits doors.Information

on

profits isvery

rare for the years after 1720.When

we

find itrecorded,

however,

profitability appears tohave been

high-

"excess" profitsaveraged

£9,492

after 1726, or nearly twice asmuch

as for the years1703-1715.

At

its high-pointin 1730,the

bank

managed

a returnof

6.2 percenton

assets,which

implies thatthe returnWe

disregardtheyearsafter 1710,when

returnswerepossiblynegative.on

equitymust

have

easilybeen

in thedouble

digits.For

the years 1702-12,when

we

have

informationon

both

total lending against interestand

on

profits for the partners,jo

interest

income

constituted84

percentof

overall earnings. " This suggests that, inits

early years at least, lending against interest

was

one of

themain

sourcesof

profits-

butby no

means

did itdominate

completely.One

additional sourceof

profitability forHoare's

was

proprietary trading. In therun-up

to theSouth

Sea Bubble,

the partners earnedample

profits.They

were

alsowise

enough

to sellwhile

priceswere

still high.After the

bubble

burst, inNovember

1721, theytook

some

of

their trading profits outof

the

bank

(amounting

toover

£27,000).Joslin stated that

1710

was

abad

year forLondon

banks

and

thatmany

privatebanks

disappeared in that year.Hoare's

suffered, butRichard

Hoare

stuck it out.The

tumultuous

yearsof

theSouth

Sea

Bubble

alsowitnessed high

bank

mortality.Hoare's

was

involved inthe asset inflation, asnoted

earlier, butemerged

intactfrom

this crisis aswell.

Even

though

the rateof

return earnedby

theHoare's

does

notlook

impressive inallof its early years, their continuation in business while others

were

exitingshows

greatdetermination

and

considerable skill.They

were

making

theirinvestment

in theintellectual capital

needed

to operate in thisnew

business.3.

Loans

The bank

reported loans in its register usingtwo

pages

at a time. Creditswere

listedon

the left-handpage

and

debitson

the right-hand page.Each

page

was

ruledinto severalsections in advance,

where

a customer's transactionswere

recorded.Only

the simplesttransactions,

however,

consistedof

a single loanand

repayment.

The

fixed space oftencontains records

of

multiplepayments and

receipts thatwere

organizedby

thebank

aspart

of

a single transaction.The modern

experiencewhere

interestis paid either regularlyor at the

end

of

a loan, signifiedby

a singlerepayment

of

principal, describessome,

butby no

means

all ofthebank's

loan activities.The

clerks atHoare's

were

meticulous in recording the titlesand

positionsof

theirclients, although all classes

were

entered sequentially in thesame

register.Whether

inthe32

We

assumethatHoare's earned5%

ontheamountlabelled"aslentwithinterest"in thebalancesheet.33

Joslin,"London PrivateBankers, 1720-85," .

case

of

Lady

Charlottede

Roye

(borrowing

£50

on

a"yellow

brilliantdiamond

ring") or theHon.

Brigadier Hastings, the exactpositionwas

recorded in a separatecolumn

in theledger. In the years before the

South

Sea Bubble,

it included inter alia SirSamuel

Barnadiston,

governor of

the East IndiaCompany,

John

Beaumont,

geologistand

Fellow

of

theRoyal

Society,Brooke

Bridges, chancellorof

theExchequer,

SirWilliam Booth,

commissioner of

theNavy,

a bishopof

Chichester, a directorof

theBank

of

England,

SirThomas

Davies,Lord

Mayor

of London,

theCountess

of

Dorchester,and

Edmund

Dunch,

themaster of

theRoyal

Household.

Bank

clerksappear

tohave

recorded loans in the following order. First, the loan itselfas a credit.

Then, repayments

as debits. Finally, there issometimes

an entryon

the creditside for the interest, seen as a claim

by

thebank

on

the borrower,which

enabled

thedebits

and

credits to agree.The

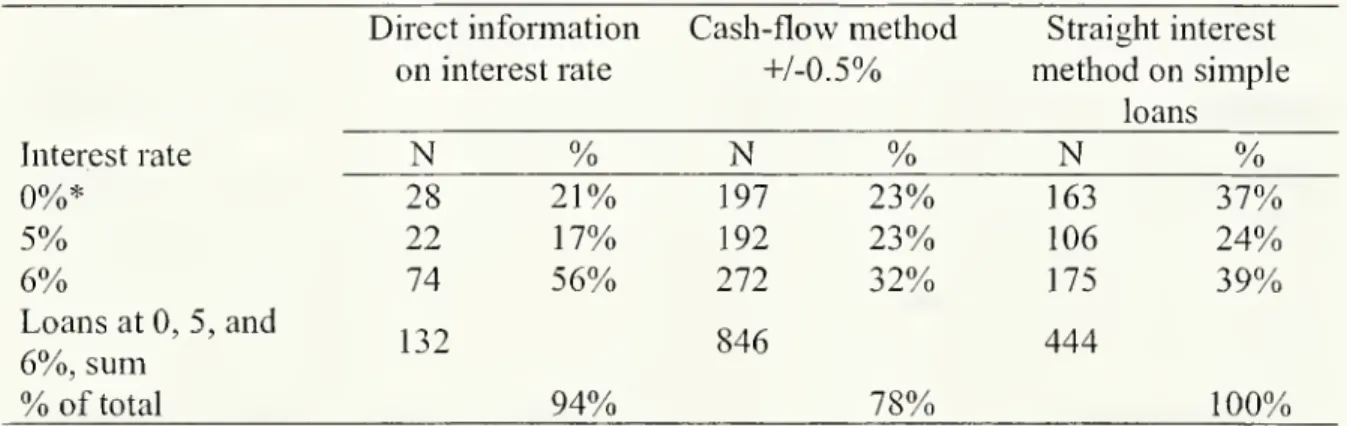

rate of interestwas

almost

never

recorded,nor

was

theterm of

the loan. Occasionally, the clerkwould

enter the agreed interest ratealong

withinterest

payments.

Inmost

cases,we

can only infer the expost

rateof

interest,based

on

the

payments

recorded. Thismode

of

recordkeeping

makes

it hard for the 21st-centuryeconomic

historian to recover the interest ratebeing

charged. It is anopen

questionwhether

itmade

it hard for the early 17th-centurybanker

toknow

what

he

was

charging.One

possible reason forthismode

of

recordkeeping

may

have been

to avoid prosecutionunder

the usuiylaw

that restricted interest to six percent before1714

and

five percentthereafter.

We

will see later,however,

thatHoare's

Bank

generallywas

incompliance

with the

usury

laws.This

mode

of recordkeeping

insteadmay

have been

a hold-overfrom Hoare's days

as agoldsmith

where

making,

pawning

and

sellingjewelry

was

allpart

of

a day'swork.

In that business, the interest receivedwas

of secondary importance

and

possiblynot recorded oreven

charged.We

transcribed the loan register,keeping

the entries inany

single space in theregister together. Ifa loan

was

repaid in full before anotherwas

made

to thesame

person,we

recordedthem

as separate transactions,even though

the clerktook

the trouble to lookup

an old entry for thatperson

and

enter thenew

loan in thesame

space as the old. Ifthelender stayed indebted in part during several or

even

many

payments

and

receipts offurther loans,

we

counted

this as a single,complex

loan.We

calculated the lengthof

theloan as the time

between

the initial loanpayment by

thebank

to the final receipt of theprincipal

by

the bank.We

recorded

the sizeof

the loan as themaximum

borrowed

in thistime period.

While

thisprocedure

over-estimates the averageamount

loaned outby

thebank

in thecourseof

thesecomplex

loans, itprovidesa simple decision rule forus to usein recording the ledger

—

one

possibly in tunewith

the ruleused

by

thebank

at the time.The

clerk oftenrecorded

the source or intentof repayments,

particularly incomplex

transactions,

and

we

recorded

thesecomments

as well.They

often indicatewhich

repayments

areof

principaland

which

of

interest.The

bank

made

a distinctionbetween

loans at interestand

loanswithout

interest inits

balance

sheets, but they allwere

entered sequentially in the loan register.We

do

notknow

with

certainly ifthebank

decided

that the interest ratewould

be

zero at the timethat the loan

was

made.

It does,however, appear

that thebank

provided

some

financingas part

of

itsgoldsmithing

business,and

that the grantingof

small, interest-free loanswas

an

echo of

this earlier practice.We

argued

earlier that the grantingof

short zero-interestloans

may

have

been

partof

a deliberatebanking

business strategy, leading to futurelending business.

Other

loans at zero (or negligible) interest arewhat

we

would

calldefaults, that is, loans

of

long durationwhich were

paid finallyby

selling the collateral(typically,jewelry) or

by

transferringthe loanto a partner.Many,

butby no

means

all, loanswere

made

against collateral assets.The

collateral typically

was

jewelry

at the startof

the century, but it increasinglywas

stocksor

bonds

inthe 1710s. Aristocraticborrowers

were

identified assuch

in the loan register,but they

were

recorded sequentiallywith

other loans. Aristocratsmay

possiblyhave

had

easier access to credit in general, but they did not get segregated into a separate account.

London

had

become

sufficiently egalitarianby

1700

for aristocratand

commoner

touse

the

same bank

inthesame

way.

We

concentrateon

the yearsbetween

the GloriousRevolution

and

theSouth

Sea

Bubble

in ourexamination of

loans to detailHoare's

learning process. SinceHoare's

Bank

onlymoved

to Fleet Street in1690

and

the surviving records start later in thatdecade, this gives us slightly

more

thantwo

decades of banking

activities.As

we

count them,Hoare's

Bank

made

about800

loans in this time.A

typical setof

payments

entered in the loan ledger reads as follows:On

April 1st

,

1700,

John

Egerton, Esq.borrowed

£200,

using plate as collateral.He

repaid the loanon

the

22

ndof October

in thesame

year, with principaland

interestamounting

to a totalof

£206

s.10.Between

1700

and

1702,John Egerton took

outtwo

more

loans,both

also for£200,

which

he always

repaid within less than a year.Sometimes, both

principaland

interest

were

paid simultaneously; occasionally, interestwas

paid

separately.John

Austin, for

example,

borrowed

a totalof

£800

in 1698, offeringmortgages

on houses

asasecurity. In

January

1699,he

was

charged

£24

for 6months'

interest, equivalent toan

annualized interest rate

of

exactly 6 percent.John Austin

remained

in debt withHoare's

until April 1711,

when

he

repaid all interestand

principal-

having

serviced the debtthrough

frequent (but not regular)payments

of

accumulated

interestand

repayments.

Inaddition to the original £800,

John

Austinborrowed

another£789

before all his debts withHoare's

were

cleared.The

bank

lent against awide

rangeof

collateral, rangingfrom

asword

hilt todiamonds and

plate,from mortgages

to bonds,and from Westphalian

ham

toTuscan

wine.

Depending

on

itsassessment

of

a client's trustworthiness, it pressed for securitiesto

back

up

the loan.Thus

Richard

Hoare

wrote

toThomas

Povey,

Esq.,who

had

asked

for a loan:

"The

respect Ialways

had

foryou

makes

me

willing tocomply

withwhat you

desire in

your

letter, but Ihope

that inmy

Patience&

Civilitie will notdoe

me

prejudice that ifit shall please

God

to takeyou

tohimself

....you

willnow

giveme

the satisfactionof

one

line to leftme

know

how

Ishallbe

paid."Ifa client defaulted, the security deposited in

exchange

for the loanwas

often sold.On

the

29

lof

June, 1706, forexample,

one

Lady

Adams

received a loanof

£100

againstdiamonds.

InMay,

shehad

alreadyborrowed

£80

against a necklace.One

year later,on

the 21st

of

May

1707,Hoare's

soldthe necklace. Eightdays

later, the restof

the loanwas

paid off in full, with interest, yielding

proceeds

of£185

s.10 for the bank.36Not

allof

these transactions turned out as well for the bank. Its expertise in valuing jewellery

and

plate

made

it relatively simple to protect itself againsthaving

to write off a loan'sprincipal. Interest

due

appears tohave been

another matter.The

long lagsbetween

theoriginal loan

and

the eventual decision to sell the collateral oftencaused

the return tobe

One

ofthese isagainst collateral,theother(the lastone)isnot.35

paltry:

Madam

Dorothy

Kennett, forexample,

borrowed

£10

against candlesticks in1687. It

was

not before1709

thatHoare's

decidedto sellthem,

netting thebank £10

s.12 d.6-

equivalent toan

annualized percentage rateof

0.7 percent. Overall, the vastmajority

of

clearly identifiable defaults in our dataset (12 outof

15) involved lending againstjewelry, gold, silver, or plate. This underlines the declining roleof

pawns

in theactivities

of

Hoare's Bank.

Lending

against collateral constitutedapproximately

halfof

total lending againstinterest for the firm. Table 2

shows

thenumber

of

loansand

their value,by

typeof

security offered.

The

sizeand

durationof

most

loans is similar to those at Child's.37Transactions

without

collateral typicallywere

relatively small,with an average

valueof

£676.

Secured

loanswere

almost

twice as large: £1,147.Loans

without

collateral alsowere

relatively short; theywere

repaid after an averageof 461

days,whereas

some

kindsof

secured loanshad

substantially longer duration.Mortgages

recordedan

average

duration

of

2,013 days,comparable

tosome modern

mortgages.

The

Marquis

of

Winchester, for

example,

borrowed

£3,000,and

only repaid aftersome

14 years.Legally

speaking,

however,

mortgages

had

asix-month

term,and could be

recalledby

the lenderafter that.

38

Table

2:Loan

valuesby

type ofcollateral, 1692-1724Collateral

Median

Mean

N

Value

durationoffered value value

%

oftotal%

oftotal (days)securities 1000

2214

538%

117,34220%

497

mortgage 12792432

315%

75,39213%

2013

plate 200454

528%

23,6084%

1411bond

300 727 7311%

53,0719%

1121 note 100 610 264%

15,8603%

594

penalbill 65478

102%

4,7801%

1667 other 170 883 345%

30,0225%

444

none 200 676 37858%

255,52844%

461 total 657 575,603 6The bank thus receivedpayment equivalent tothe full principal, plus interest at 6 percent onthe £100.

Theinitial loanwasapparentlyinterest-free. '7

Quinn, "The Glorious Revolution's Effect on English Private Finance:

A

Microhistory, 1680-1705," ,table4, p. 608.

38

Brewer, The Sinews of

Power

: War,Money

andtheEnglishState, 1688-1783 .The

composition of

lendingby

security offeredassummarized

in Table 2does

notreveal the striking

changes

that occurred in the firstdecades of

the eighteenth century.Loans

against plate declinedfrom

14 percentof

the total before1700

to three percent in thefirstdecade of

thenew

centurytoone

percent thereafterasHoare's

Bank became

evermore

distinctfrom Richard Hoare's

previous enterprise.Mortgages were

the singlemost

important security offered in the years before 1710,

accounting

forapproximately

one

third of collateralized lending. Securities

were

also popular,and

theirimportance

grew

significantly after 1710.

Over

halfof

all lending securedthrough

assets heldby

thebank

was

in theform

of

securities in the years1710-1721,

which

contain theSouth

Sea

Bubble.39

Loans

without interestappeared

alongside all other transactions, as partof

thecontinuous records

of

transactions with all customers. Insome

cases, these loanswere

clearly

designed

tohelpovercome

atemporary

cash shortage.While

themean

durationof

502 days

suggests long-term lending, it is heavily influencedby

afew

outliers.The

maximum

length recordedwas

inthe caseof William

Dobbs,

who

borrowed £40

in1707

and only

repaid in 1715. In amore

typical case,on

April 14th, 1699,Madam

ElizabethGough

received £10, leaving candlesticks as collateral.According

to the loan ledger, shereturned the next

day

torepay

the loan.The median

durationof an

interest-free loanwas

84 days

(versus334

days

fornon-zero

loans).The

typical zero-interest loan lasted lessthan3

months,

whilethemedian

interest bearing loan lastedalmost

a year.Some

transactionseem

puzzling to themodem

historian's eye.Ann

and

CatherineGoare borrowed £20

inAugust

1698,and

repaid£20

s.8 inDecember

(equivalent toan

APR

of 6.3 percent-

Hoare's

evidentlyaimed

tocharge

them

6 percent interest). InFebruary

ofthe next year, thetwo

Goares

borrowed

again, for thesame

amount,

leavingthe

same

typeof

collateral-

abond

-

and

repaidsome

ninemonths

later. This time,however,

therewas

no charge

forinterest.The

evolutionand

thepayment

detailsof

non-interestbearing loans at

Hoare's

castsdoubt

on Quinn's

interpretation ofthem

atChild's,a rival

London

bank.4He

argued

thatthese loans containedhidden

interest charges, inan

effort to

circumvent

theusury

laws that limited themaximum

interest rates thatcould be

This was partly because of the bank's role in the market for South Sea stock and other speculative

securities,which

we

exploreinaseparatepaper.paid. In effect,

according

to this interpretation, theGoares

would

have

actually only received a fractionof

the £20,and

thenhad

torepay

in full, a practiceknown

aspaying

out

amounts

loaned withan

agio.We

findno

evidence

to support this hypothesis in thecase

of

Hoare's.Given

thatthebank had

justcompleted

a successful transactionwith

theGoares, receiving its

money

back on

timeand with

interest,what

possible reasoncould

there

have been

tocharge

a higher interest rate? Also, thebank

recorded

loanswith

interest separately

from

other loanson

its annual balance sheet, again suggesting that theother loans

were

notinterest-bearing.Average

yieldsof

4-5 percenton

this portionof

thebalance sheet

can account

for almost allof

the recorded profits. Finally, in those yearswhen

the annual balance sheets recorded interest received separately, thesemust

refer to"loans against interest"

-

otherwise, the ratioof

interest received to loans outstanding suggests thatloanswith

an agiowere

charged

interestbelow

theusury

rate.Why

would

abank

provide interest-freeloansat all,given

thatthis entailsopportunitycosts?

Hoare's

may

have decided

thattherewere no

interest-bearing loan opportunitiesof

sufficiently high quality available,

and

that lending outsome

fundsmay

atthesame

time

be

good

for future business.As

timewent

by,Hoare's

learnedhow

to acquirecustomers

and provide

them

with

a service that theyvalued

-

and

eventuallycame

topay

for.The

statistical tests in

Table

3demonstrate

that the decline in zero-interest loanswas

permanent.

Note

that there aregood

theoretical reasons forsuch

a pattern.Recent

work

by

AbhijitBanerjee

on

credit intermediation inemerging

markets

alsoemphasizes

theimportance

of

"loss leading",and

predicts that it willbe

particularly prevalent inenvironments

where

informationon

thequalityof borrowers

is rare.The

bank

faced almostno problem

with

defaults.This

was

not the resultof

adiversified loan portfolio. Instead,

low

default rateswere

key.Over

the period1692-1724, there are only 15 cases that

were

clear defaults.The

average valueof

these defaulted loanwas

£387,

for a total lossof

£5,817.There

may

have

been

othernon-performing

loans, notmarked

clearly assuch

in the loan ledgerand

so identifiedby

usonly as interest-free loans.

We

should note that ourmethod

of

constructing a databaseof

40

Quirm,"TheGlorious Revolution's EffectonEnglishPrivateFinance:

A

Microhistory, 1680-1705,".41

This does not rule out that the bank could have

made

additional profits, and hidden them in annualbalance sheets, too. Yet this would have been a highly complicated undertaking at a time

when

balancesheetswerenotpublishednorauditedandtherewere no taxesonprofits.