The impact of risk on three initial public offerings market anomalies : hot-issue market, underpricing, and long-run underperformance

Texte intégral

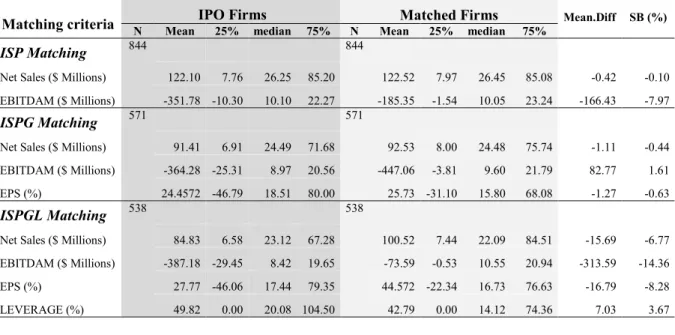

Figure

Documents relatifs

Using 4200 individual year observations on the board of Indonesian bank including 21 ethnicities within the 2001-2011 period, we construct indicators of diversity in four

Copyright and moral rights for the publications made accessible in the public portal are retained by the authors and/or other copyright owners and it is a condition of

Hence, the purpose of this article is (a) to review and evaluate the methodology, research design, critical findings, and limitations in current research involving the effects

However, at least two alternative explanations could justify underpricing even in our setting where symmetric and transparent information on the fundamental asset value is given:

Second, we re-estimate the specifications of Table 6 using, as dependent variables, the buy- and-hold abnormal performance (BHMAR) 12 months after the Brexit announcement and the

Methodologically, we develop a dynamic conditional version of the capital asset pricing model (CAPM) which allows for time-varying quantity and price of risk and

The tools considered for analysis are first the precautionary saving provision for symmetric risk management and an insurance contract on farm revenue for

We demonstrate that a merger involving leveraged …rms increases the bankruptcy probability of the merging …rms while a similar merger concerning unleveraged …rms or between the