MITLIBRARIES DUPL

Digitized

by

the

Internet

Archive

in

2011

with

funding

from

Boston

Library

Consortium

Member

Libraries

11 1-15

Massachusetts

Institute

of

Technology

Department

of

Economics

Working

Paper

Series

THE

ALTERNATIVE

MINIMUM

TAX

AND

EFFECTIVE

MARGINAL

TAX

RATES

Daniel

R.

Feenberg

James

M.

Poterba

Working

Paper

03-37

October

2003

Room

E52-251

50

Memorial

Drive

Cambridge,

MA

021

42

This

paper

can

be

downloaded

withoutcharge from

the SocialScience

Research Network Paper

Collection athttp://ssrn.com/abstract=47060

1MASSACHUSETTS

INSTITUTEOF

TECHNOLOGY

The

Alternative

Minimum

Tax

and

Effective

Marginal

Tax

Rates

Daniel R. Feenberg

NBER

James

M.

PoterbaMIT

andNBER

October2003

ABSTRACT

This paperexaminesthe impact ofthe Alternative

Minimum

Tax on

the weightedaveragemarginal tax rates thatapplytovarious

components

oftaxable income.It also considers theimpact ofseveral

AMT

reformproposalson thenumber

ofAMT

taxpayers, the totalrevenuecollected fromthe

AMT,

and the weighted averagemarginal tax rates thatapplytowages,capitalincome, anddeductionssuchasstate and localtaxes and charitable gifts.

The

paperuses theNBER

TAXSIM

model

toproject federalpersonalincome

tax liabilitiesaswell asAMT

liabilitiesbetween 2003 and2013.

The

AMT

hasonly amodest

impacton theaveragemarginal tax ratesfor

most

sources ofincome

becausesome

AMT

taxpayersfacehighermarginal taxrates,andotherslowertaxrates, as aresultofthetax.

The

projectionsshow

thatmodest

increases in theAMT

exclusion levelhavesubstantial effects on thenumber

ofAMT

taxpayers, andthatindexingthe

AMT

parameterswould

reduce thenumber

ofAMT

payers in2010 by more

thansixtypercent. These changes

would

alsoreduce theAMT's

impacton averagemarginal taxrates.We

areextremelygratefulto InnaShapiro for assistancewiththeTAXSIM

program,toRosanne

Altshulerforhelpfulcomments,

andtothe Smith RichardsonFoundation, theNational1

The

AlternativeMinimum

Tax

(AMT)

isaprovisionoftheU.S.income

taxcodethatcurrently affects amodest

number

oftaxpayers. Itwillbecome

anincreasingly importantcomponent

ofthe federal tax system inthecoming

decade.The

minimum

taxbeganin 1970asaten percent,andlatera fifteen percent, taxon preferences inexcess of $30,000. Preferences

included accelerated depreciation, oil depletion, andthe capitalgains deduction.

A

deduction ofonehalfofregulartax paid,andlaterofalltax,

was

allowedagainstpreferences. Netoperatinglosses andretirement

income

receivedspecialtreatment.The

minimum

taxexpired in 1981. Beforeits expiration, however,in 1979,anew

"Alternative

Minimum

Tax" was

establishedwithabase thatincludedall thecomponents

ofAdjustedGross

Income (AGI)

andthe capital gainsdeductionin additiontopreferences.The

new

AMT

allowedthe fullamount

of regularincome tax asa credit. Aside from changes in thetreatmentofnet operating lossesand slightchanges intheexclusion amount, thisisthe

AMT

thatiscurrentlyin force,andthat isscheduledtoremain inforce indefinitely.

When

apreferential taxrate forlong-termcapital gains

was

establishedin 1991, carewas

takentoavoid treating capitalgains asapreference.

A

number

of research studiespublishedsince the late 1990s have identified theAMT

asagrowing factor inthe

income

tax structure.Harvey

and Tempalski (1997)were

among

the firsttopoint outthatbecause theexclusionlevel for the

AMT

was

not indexed forinflation, whilemost

other keyparametersinthe tax code

were

indexed, theAMT

would

applyto agrowingnumber

oftaxpayers. Rebelein andTempalski(2000),theU.S. Congress Joint

Economic Committee

(2001),Tempalski (2002), and

Burman,

Gale,andRohaly (2002) provide furtheranalysis ofthegrowingimportanceofthe

AMT.

The

AMT

became

more

importantafterthepassageoftheEconomic

Growth

andTaxpayer

ReliefReconciliationAct of 2001(EGTRRA),

which

reduced ordinaryincome

taxtwo

examples ofstudies thatshow

thatbecauseEGTRA

loweredincome

tax liabilities formany

taxpayers, itwill raisethe

number

ofAMT

payers.The

Jobs andGrowth

TaxpayerReliefReconciliationActof

2003

reinforcesthis effect. Formany

upper middleincome

householdswho

willface the

AMT

as a resultofrecenttaxreforms,theAMT

"takesback" a substantial shareofthe potential tax reliefassociatedwiththesereforms.

Burman,

Gale and Rohaly (2003a,2003b)suggestthatin2010, 33.8 percentofthe

EGTRRA

tax cuts willbe"recaptured" intheform

ofhigher

AMT

liabilities. Thispercentageexceeds 65 percent fortaxpayerswithAGI

between

$100,000 and $500,000.

Sullivan (2002) offersa careful review ofthe issues associated withthe potentialrepealof

the

AMT.

Proponents ofrepealpointtothe potentialcomplianceburdenofthe tax,which caneffectivelyrequiretaxpayersto prepare

two

taxreturnsandtocompare

the results,andtotheunanticipated impacton taxpayerliabilities.

The

potentialrevenuecostofAMT

repealisasubstantial impedimenttosystematic reform.

Inthispaper,

we

use theNBER's

TAXSIM

program

to evaluate the impactoftheAMT

on

incentivestowork

andto save.We

presentsome

estimates ofthe growingnumber

oftaxpayers

who

will face theAMT,

but theyare notthe central focusofthe study.We

emphasizeprojectionsforcalendaryear 2010, sinceundercurrentlaw,this istheyear

when

theAMT

willaffectthe largest

number

oftaxpayers.A

number

ofincome

tax provisionsarecurrentlyscheduledtoexpire in2010,so the taxenvironmentin2011 will besubstantially different

from

thatin 2010. Although our projectionsrelyon strongassumptionstoproject the future

number

oftax returns andthe leveland composition of

income

on thesereturns, theyoffersome

insighton

the likely futurecourseofthe

AMT

relativetothe ordinaryincome

tax.The

paperisdividedinto six sections.The

firstdescribes thebasic structureoftheAMT

and comparesalternative

minimum

taxableincome

with taxableincome

asdefinedundertheanditpresentsour projections ofthe

number

ofAMT

taxpayersinaggregate, andinincome

sub-categories, for futureyears.

Our

results fromtheTAXSIM

analysis arebroadlyconsistentwiththose fromotherrecent studiesthatproject future

AMT

liabilities. Sectionthree describestheprobabilitythattaxpayers invarious

income

categories will face theAMT.

It also studieshow

various reformproposals

would

affectthese probabilities.The

fourth section investigates theimpact ofthe

AMT

onthe weightedaverage marginaltax rates thatapplyto wages, interestincome,dividend income, andseveral

income

taxdeductions. Itconsidersmarginal tax ratesassociated withthe federal

income

tax, aswell asthetotal effective tax ratethatcombines thefederal

income

tax withthe potentially-deductible stateincome

tax. Section fiveexplorestheeffectof various reformproposalson the weighted averagemarginal tax rates

on income

anddeductionflows. Thereisa briefconclusion.

1.

The

Structure ofthe AlternativeMinimum

Tax

Although the

AMT

issometimes describedasacomplex

andmysterioustax, formany

taxpayers

who

face theAMT,

theAMT

calculationis straightforward. Fortaxpayerswho

do notitemize,the "tentative

AMT"

is 26percentofAG

I inexcessofan exclusionamount. Fortaxpayers withalternative

minimum

income

above $175,000,theAMT

tax rate is 28percent.The

AMT

is paid asanactual tax liability onlytotheextent that itexceeds thetaxpayer's regulartaxliability. For2010,the year

when

theAMT

isprojectedtogeneratethe largest revenue flow, theexclusionequals$45,000 forjoint filersand $33,750forsingle individuals. Fortaxpayerswith

incomesabove $150,000 onjoint returnsand$112,000 on single returns, theexclusionisphased

outat therateof 25 centsforeachdollarof

AGI

abovethe threshold. This implies thatthe28%

AMT

rate appliestojointfilerswithAGI

above $206,000,and forsinglefilerswithincome

aboveminimum

income

will equal 175,000. Forexample

forjointfilers,thisrequiresAGI

-

(45000-.25*(AGI - 150000))

=

175000.Severalfeatures ofthe

AMT

arescheduledtochangebetween2003

and2010

undercurrentlegislation. For example,after2005, thezero bracket

amount

isno

longeraddedto theexclusion. For

2003

and2004, theexclusionis $58,000forjointfilers and $40,250 forsinglefilers. It declinesin lateryears.

Foritemizers,the

AMT

calculationismore

complicated. Allitemized deductions exceptthose forstateand localtaxes, medical expenses inexcessof

2.5%

ofAGI,

and miscellaneousdeductions are available as deductions against alternative

minimum

income.The

taxpayermust

identify eligibledeductionsand subtract

them

from alternativeminimum

income. Itemizeddeductions underthe

AMT

are notsubjectto thephase-outthatispresentintheregularpersonalincome

tax. In rarecasesthismay

invalidatethe usualrule thattaxpayers should itemize ifitemized deductionsexceedthe standard deduction.Foravery few, thedecreased

AMT

from

itemizationwillcompensatefor a largertaxable income.

For

most

taxpayerswith longtermcapital gains, theAMT

iscalculatedon

non-gainincome

plus20%

oflong-term gains. Forlowincome

taxpayerswithgains, the10%

capitalgainsrateisapplied togainsthat

would

notpushtaxable income abovethe15%

bracketboundary. Alltax credits exceptthe foreigntax creditcan be creditedagainst

AMT

liability,ascanthetaxpayer's regulartax liability. Sincetaxyear 2000,tax creditsdo notaffectthe total liability

calculation.Priorto that year,the taxformsdistinguishedbetween

AMT

liability,recorded onform

6251, and creditswhose

value, iftaken,would

befullyoffsetby theAMT.

Thesewere

referredtoas "lostcredits"andthe credit formsincluded lines toavoid takingsuch credits.

While

theAMT

may

requiretaxpayers tocompute

theirtax liabilityundertwo

regimes,none

ofthe calculationsrequireanyspecial recordkeepingbeyond

whatis requiredby the regulartrue that

some

taxpayers withnetoperating losses,or accelerated depreciation orinothersimilaresoteric situations are subjecttoadditionalrecord keeping,and

may

besubjecttoadditionalAMT

by

2010, but there are few suchtaxpayers. Formost

taxpayerswho

will faceAMT

liability,theAMT

calculation isnotparticularly burdensome.Figure 1 provides informationon the pattern of

AMT

andordinaryincome

tax liabilityforataxpayerfilinga joint return with

two

dependentsandclaimingthestandard deduction.Tax

liabilitiesunderbothtaxschedulesare

shown

atdifferent levels of adjusted gross income.The

figuregraphs

AMT

andordinaryincome

tax liabilityforboth2003 and2010, withthe taxpayer'sreal

AGI

held constantin2003 dollars.The

graphsshow

thatAMT

liabilityexceedsincome

taxliability fora substantialrangeof incomes, beginningatroughly $50,000, and endingatroughly

$375,000,in2010.

The

figure alsoshows

thatthe rangeofincomesoverwhich

AMT

exceedstheincome

tax iswiderin2010

than in2003.The

fourlinesdemonstratehow

similar the shapes ofthe fourtaxschedules are, sothatasmall shiftleftward in thereal

AMT

schedule,such asthe onethattakesplace

between

2003 and2010,shiftsmuch

oftheincome

distribution ontotheAMT

schedule.

2. ProjectingFuture

AMT

Liabilities:The

TAXSIM

Model

The

NBER

TAXSIM

model

isa computerprogram

thatcalculates federal incometaxandpayroll tax liabilitiesfora representative sample of U.S. families. Itanalyzes datafromthe

Statistics of

Income

(SOI)PublicUse

File, a stratifiedrandom

sampleof U.S. taxpayersthatoversampleshigh-incometax returns. Feenbergand Coutts (1993) describethe personal

income

tax sectionsofthe

TAXSIM

model

insome

detail.The

TAXSIM

algorithm includesdetailed computer code basedonthe personalincome

tax systemthat, basedoncurrentlegislation, willbe inforceinfuture years.

To

constructindividual

income

tax return file,the 1999SOI

datafile,to2010. This "aging" processrequiresforecasts ofthe growthrateofthe aggregate

amount

ofvariousincome components

anddeductionflows.

We

assume

annualgrowthratesof1.2percent forpopulation,2.2 percent for realincomesanddeductions, and2.5 percent forthe price level forall

income

anddeductionitems. Thesegrowthratesare

drawn

fromCBO

projections.Long

term gainsare normalizedto5.6 percentofAGI, which was

theiraverage valueovertheyears 1981-1999.When

thegrowthrates describedabove are appliedtothe 1999cross-section dataon

taxreturns,the resulting

income

taxrevenue forecasts for2004-2013 aresubstantiallyhigher thanthose

made

by

the CongressionalBudget

Office.A

one-timeten percent reductioninallnominalmagnitudes,appliedfor examplein 1999, brings our aggregaterevenueestimates into

much

closeragreementwiththe

CBO.

We

thereforereduce allnominal 1999 magnitudesby

tenpercentbefore

we

make

ourfutureprojections.TAXSIM

calculates federal aswell asstate marginalincome

tax rates.AMT

payerscannot deductstate

income

taxesfrom

theirtaxableincome, sotheireffective stateincome

taxrate is higher thanthe comparable ratefacing those

who

payordinary federalincome

taxandclaim an itemized deduction for statetaxes.

To

recognizetheimpactofthe effectivestatetax rateon

the total taxburdenon

wages, interest, dividends, andotherincome

components,we

thereforecalculate federalmarginaltax rates underthe

AMT

aswellasthecombined

tax ratethatequalsthe federalmarginaltaxrateplusthe net-of-federal-deductibilitystate

income

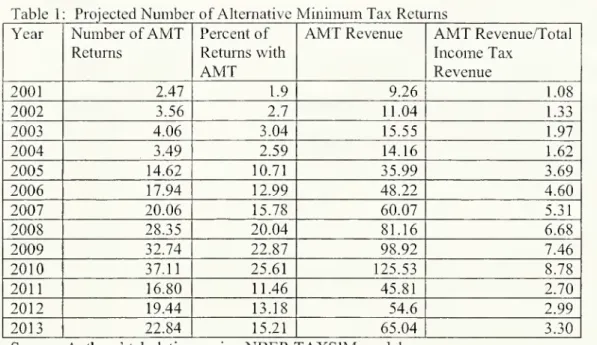

taxrate.Table 1 presentsinformation

on

our projections regardingtheAMT

undercurrent law.The

tableshows

the totalnumber

oftaxpayerswho we

project will face theAMT,

thetotalamount

ofAMT

revenue,andtheratioof revenuefrom

theAMT

torevenuefrom

the ordinaryincome

tax.The

tableshows

thatprojectedAMT

revenue peaks in2010,when

itaccounts fornearlynine percentoftotal

income

taxrevenue.We

project that 37milliontaxpayers-

nearly one7

have no itemized deductions, no capital gains,no phase-out ofthe

AMT

exclusion, and nootherpreferences. Thisgroup of taxpayerswill face relativelysimple

AMT

calculations.Table 1

shows

thatthenumber

ofAMT

filers andthe revenue collectedfromtheAMT

declineafter2010,

when

various provisionsofEGTRRA

expire. Ifthis legislativechange occursin2011, the

number

ofAMT

filers will fallbymore

thanonethird,andAMT

revenues willdecline

by

more

than half.The

projections inTable 1 aresimilartothoseinseveral other studiesoftheAMT.

Forexample,

Burman,

Gale, and Rohaly (2003b) projectthat there willbe33.1 millionAMT

filers in2010.

They

note that inthe absenceofEGTRRA,

theywould

have projected 14.3 millionAMT

filers. Theirprojectionsuggests

AMT

revenue of$124

billionin2010, only $1 billion lessthanourprojection. Kiefer,etal. (2002) projectthatthere willbe35.1 million

.AMT

filersin2010

andthat the

AMT

willyield $133billioninrevenuethatyear. Their projections includethe effectofEGTRRA,

but theydonotincorporate any ofthe2003 tax changes.The

prospective growth ofAMT

liabilitiesandthenumber

ofAMT

taxpayers hasgenerated a

number

of proposals for legislativereformsthatwould

slowthe growthoftheAMT.

We

usetheTAXSIM

model

toevaluatethe impactofsixpotentialreformson

thenumber

ofAMT

taxpayersandtherevenue generatedby theAMT.

Table2 presents these findings.The

first

row

reportsbaselinecalculations for2010, correspondingtothe informationinTable 1.The

nextsix

rows

considerreform proposals.The

firstproposalwe

considerwould

allow personal exemptionstobe subtractedfromotherincome indefiningalternative

minimum

income.Such

exemptions arepermittedundertheordinaryincometax,thereby reducing ordinary taxable

income

relativetoalternativeminimum

taxable income.

The

secondrow

of Table2shows

thatthisreformwould

sharplyreduce thenumber

ofAMT

taxpayersin2010, from37 millionto 12 million, and itwould

also reduce8

A

secondpotential reformcalls fortheextensionofincome

taxprovisionsthat expirebetween

2005

and2010

sothattheywould

remainin forcein2010.The

twomost

significantprovisionsareone that

would

raisetheAMT

exclusionin2010

to $13,000forjointfilers and$6,500forsingle filers,and one that

would

continuethe preferentialtaxation of dividends.The

formergreatlyreducesthe

AMT,

andthe latterreduces boththeregularincome

tax andtheAMT

by

similar amounts.The

thirdrow

of Table 2shows

that extendingall expiring provisionswould

reduce the

number

ofAMT

filersfrom

37millionto 14.1 millionin2010,witha decline in totalAMT

revenue from$126

to $58 billion.The

thirdAMT

reformthatwe

consider involveschanges in the relativetreatmentof

single andmarried taxpayers.

The 2010

jointtaxpayer exclusionof $45,000 undertheAMT

issubstantiallylessthantwicethe singletaxpayer exclusionof$33,750. In principle, the single

exclusioncould simplybedoubledto $67,500, butthat

would

substantiallyincrease themarriagebonusforcoupleswithnon-workingspouses.

We

havethereforemodeled

a lessgenerous optionwhich

offers the couplethe greaterofthecurrent joint deduction, orthe singlededuction plus thesecondary earner's

wages up

tothe single exclusion. Thismeans

thatthefull $67,500isofferedonlyto

two

earner couples, with bothearnersmaking

more

than $33,750.Our

analysisofthisreform

shows

thatitleads to amore modest

reduction inAMT

taxpayers thanthetwo

earlierreformproposals.

The

number

ofAMT

filers in2010

dropsfrom

37 millionto25millioninthiscaseand

AMT

revenuedeclinesby

roughly onethird, from$126

to $87billion.The

lastthreeproposalswe

consider involvechangestotheAMT

exclusionlevel.One

involves indexingtheexclusion, whilethe secondandthird involveraisingtheexclusion

by

$3,000 and$10,000respectively.

The

nominal,un-indexed characteroftheAMT

exclusionisakey contributortotheprojected growthof

AMT

revenuesandtaxpayers.We

project 14.0millionindexation.

AMT

revenuesin thiscase are$48 billion. Indexing theexclusionthereforereducesAMT

revenueinour projectedpeak revenueyearby oversixtypercent.The

findings onthe impact ofindexing theAMT

underscore the importance oftheinflationrate indetermining the relativerevenueyield oftheregular

income

taxandtheAMT.

Figure 1

showed

thatsmallchanges inthe real threshold atwhich

taxpayers areaffectedby theAMT

canhave substantial effectson revenues and onthenumber

ofAMT

filers.By

comparison,real growthinthe aggregate

economy

has amuch

more modest

effect onAMT

revenue, becauserealbracketcreepraises the regular

income

tax as well astheAMT

base.The

lasttwo

reformsthatwe

consider involve specificnominal changes intheAMT

exclusion. Raisingthe exclusionby

$3000

in2010

reducestheprojectednumber

ofAMT

taxpayers

by

6.4 million, from 37 millionto31 million. Raisingthe exclusionby $10,000 reducesthe

number

offilers to 17million.Revenues

drop from$126

billion in the statusquo,to$100

billion ifthe exclusion israised

by

$3000, to$65billion ifthe exclusionrisesby $10,000.The

burden oftheAMT

doesnot fall equally acrosstheincome

distribution. Table3shows

theAMT

tax burdenas a shareofAGI

forhouseholds stratifiedby

AGI.

The

entriesshow

total

AMT

liabilitydividedby totalAGI

forthehouseholds ineachcategory; theyare notrestricted tohouseholdswith

AMT

liability.The

calculationsapplyto2010, andtheyassume no

changes between

now

andthen in the federal tax law.The

AMT

burden ishighestforthosewithAGI

between

$200,000 and$500,000. This groupfacesAMT

liabilitythataverages2.7%

ofAGI.

The

burdenis halfasgreat,1.3%

ofAGI,

fortaxpayers withAGI

of $50,000 to$75,000. It islower for

AMT

taxpayerswith higher-

greaterthan $500,000,and lower-

less than $50,000-AGI.

Figure2 plots information similarto that inTable3.

The

figureshows

average taxrates,10

rate fortaxpayerswith

AGI

between

$200,000 and $500,000, andvery littleimpacton

averagetaxrates forhouseholds

whose 2003

AGI

isbelow

approximately$50,000.3.

The

Probability of FacingtheAMT:

CurrentTax

Policyand VariousReforms

The

results inTable3 andFigure2 underscorethe importanceof disaggregating taxpayersby

income classwhen

analyzingtheAMT.

One

usefulway

to illustratehow

theAMT's

impactvaries acrosshouseholds withdifferent characteristics and

income

levelsis toproject theprobability that ataxpayer willbe an

AMT

filer.Burman,

Gale, andRohaly(2003a, 2003b) andotherearlierstudies estimatetheAMT-filing probabilities fortaxpayers invarious

income

categories.

Our

analysis exploreshow

various reformproposalswould

affect theincome-specificlikelihoodoffacingthe

AMT.

Table4presents resultsbasedon ourprojections ofthe

AMT

in2010.The

table reportsprobabilitiesundertheassumption thatcurrent tax legislationremains in forcethrough

2010

andunderthe variousreformsdescribed inTable 2.

The

results inthe firstcolumn

indicate theprojected

AMT

payment

probabilitiesunderthe status quo.The

tablepresents results forthreesetsoftaxpayers: the

whole

taxpayer population,the thirtypercentof taxpayerswho

areprojectedtoitemize in2010, andthesubsetofalltaxpayers with

two

ormore

dependents.The

probabilitiesoffacingthe

AMT

differacrossthesegroups.The

resultsinthe firstpanelofTable4show

that thetaxpayerswho

havethe greatestchance ofenteringthe

AMT

regimein2010

arethosewithAGI

between

$75,000 and$500,000.These

income

thresholdsare specifiedinconstant $2003. At lower incomelevels, theAMT

exclusion

makes

itunlikelythatataxpayerwill faceAMT

liability.At

AGI

levelsabove$500,000, theprogressivityofthe personal

income

tax schedulemakes

itlikely that formost

taxpayers,personal

income

taxliabilitywillexceedAMT

liability.The

resultsunderscorethe11

facingthe

AMT

is56.3%

fora $50-75,000AGI

taxpayer,77.2%

for ataxpayer withAGI

between$75,000 and$100,000, and

more

than90%

fortaxpayers withAGI

between $100,000 and$500,000.

The

results inthesecondpanelof Table4, foritemizers, arebroadlysimilartothoseforthe universeofall taxpayers.

The

distribution ofitemizers acrossAGI

categoriesis shifted towardhigherincomes, however,sothat while only

25.7%

ofall taxpayersareprojectedto face theAMT,

52.5%

ofall itemizers areprojectedto face theAMT.

The

lastpanelof Table4,which

presentsresults fortaxpayers with

two

ormore

dependents,shows

thatthepresence ofdependentschanges theAGI-specificprobability offacingthe

AMT.

In the $25-50,000AGI

category, forexample,

15.8%

ofall taxpayersareprojected topaytheAMT,

whilemore

than halfofthetaxpayersin this

AGI

category withtwo

ormore

dependents areprojected toface theAMT.

There isalsoasharp increase intheprobability offacingthe

AMT

atincomes between $50,000and $75,000.

The

overallprobability offacing theAMT

isgreaterthan50%

forthe subsetoftaxpayerswith

two

ormore

dependents.The

next sixcolumns

of Table 4presentresults similartothose inthe firstcolumn, butcorrespondingtothe various

AMT

reform optionsdescribed above.The

secondcolumn

considerstheimpact of allowing personal exemptionstobe subtractedfrom alternative

minimum

taxableincome. In thiscase,the overallprobability offacingthe

AMT

drops from25.7%

to8.4%.The

effectis strongestfortaxpayers with

AGI

below

$100,000. Forthe$75-100,000income

category,forexample,the probabilityoffacingthe

AMT

drops from77.2%

to 15.8%.The

effectofthisreformisalso verypowerfulfortaxpayers

who

havepositiveincome and twoormore

dependents.Thisreformreduced theirprobabilityoffacingthe

AMT

in2010

from56.1%

to 15.6%.The

thirdcolumn

of Table 4considers theimpactofextendingtheexpiringEGTRRA

provisionsthrough 2010. Foralltaxpayers, this reformreducestheprobability of payingthe

12

income

AMT

payers. Fortaxpayers withtwo

ormore

dependents,the impact ofthisreform issmallerthanallowing personal exemptionstobe deducted from alternativetaxable income.

The

probabilityoffacing the

AMT

drops from56.1%

underthe statusquo

to27.8%

withthe extensionofexpiringprovisions.

The

nextcolumn

considers the"AMT

marriagepenalty reform"describedin thelastsection. Thisreform reducesthe percentageoftaxpayers facing the

AMT

from25.7%

to 17.4%.The

threepanels ofTable4show

thatthe impact ofthisreformon theprobabilityof payingAMT

islessconcentrated atlower

income

levelsthanathigherlevels. Inparticular,the probability thattaxpayersinthe $50-100,000

AGI

range face theAMT

declines lessforthisreformthan for eitheroftheprevious reforms that

we

considered.The

lastthreecolumns

considerchanges intheAMT

exclusionlevel.Comparison

ofthefindingsinthese

columns

shows

thatindexing generatesthe largestreductionintheprobabilityoffacingthe

AMT

fortaxpayers withAGI

between

$50,000 and $200,000.Even

withindexation,the probabilityof payingthe

AMT

remains83.7%

fortaxpayerswithAGI

ofbetween $200,000and$500,000.

The

probabilityis92%

forthisgroupwhen

the exclusionisraisedby $3000

orby

$10000.

The

thirdpanelofTable4

shows

thatvirtuallyallofthetaxpayersinthisAGI

categorywith

two

ormore

dependentsfacetheAMT.

Indexing theAMT

exclusion hasa smallereffecton

thepercentage oftaxpayerswith

two

ormore

dependentswho

paytheAMT

thanitdoeson thefraction ofalltaxpayers facing this tax.

Figure 3

shows

the impact ofraising theAMT

exclusiononnumber

ofAMT

taxpayersand on therevenueyieldofthe

AMT.

The

marginaleffectof an incremental increaseintheexclusion declinesas theexclusionrises.

A

$10,000increase intheexclusion in2010, forexample,is predictedtoreduce

AMT

revenueby

nearly fiftypercent, and ithas a similar13

the

number

ofAMT

filersby

28million, from34.8 million to6.7 million, and itreducesthe totalrevenue generated

by

theAMT

from $121.2billionto$41.5 billion.4.

The

AMT

and MarginalTax

RatesMost

ofthepopular discussionsurroundingtheAMT

focusesonthenumber

of taxpayerswho may

face thetax, oron theimpactoftheAMT

on federal taxrevenues.The

effectoftheAMT

on incentives forworking, saving,and engaginginvariousactivitiesthatgenerate taxdeductions has received

much

lessattention.To

explorethe incentive effects oftheAMT,

we

compare

the ordinaryincome

tax rateandtheAMT

rate facingtaxpayerswho

areprojected tobesubject to the

AMT

in 2010. Sinceataxpayermay

face differentmarginal taxrates ondifferentincome

flows,we

presenttabulations forvariouscomponents

oftaxableincome. Foreachincome

component,

we

compute

the fractionofthatcomponent

that isreceivedby

AMT

taxpayers.We

then

compute

the percentagewhose

tax raterises, andthepercentagewhose

taxratedeclines, asaresult ofthe

AMT.

We

constructmarginal tax ratesby

calculating theincremental tax that ataxpayerwould

pay ifoneofhis income elementsordeductions

was

onepercentgreaterthanthereportedvalue.The

tax rateon a specificincome component

foragivenhouseholdisdefinedasthechangeintaxliability dividedby .01 timesthe initial taxreturn entry, i.e.,the changein taxdividedby the

changein

income

or the change inthe deductionamount.We

calculatethesemarginal tax ratesunderthe assumptionthatall currently legislated tax rulesremaininforceunless theyarechanged

by

legislation thathas alreadybeenenacted.We

thereforeassume

thatphase-outsofsome

ofthetax provisions thatwereenacted in2001 and

2003

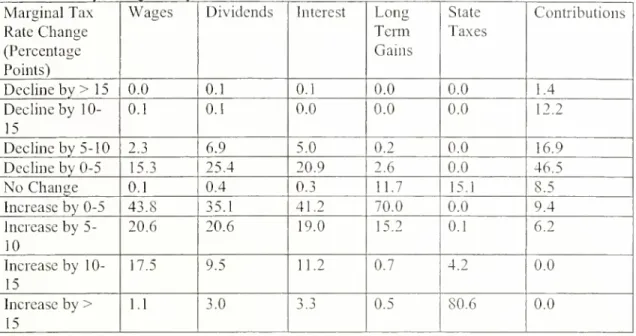

will take effect asplanned.4.1 Marginal

Tax

Rate Increasesand Decreases with theAMT

Table 5presents ourfindings with regardtothe disparity betweenataxpayer'sordinary

14

marginal

income

taxrate. Table 6reports parallel calculations thatconsiderthe impactoftheAMT

onthe taxpayer'scombined

federaland statetaxrate, netoffederal tax deductibility.The

first

column

inTable5 considerswages

and salaries. Nineteenpercentofthewages

receivedbyAMT

taxpayersfaces alower marginaltax rateas a resultoftheAMT,

whilethe remaining 81percentfaces ahighertax rate.

The most

common

outcome

isa taxrateincreaseofbetween

zeroand fivepercentage points, for

example

reflectingamove

fromthe 33 percent bracketontheordinary

income

tax scheduleto 28percenton

theAMT

schedule.Almost

onetenthofthewage

and salary

income

receivedby

AMT

payersistaxedata rate 5 to 10 percentagepoints loweras aresultofthe

AMT,

with aroughly equalamount

ofwage

income

taxed atarate 5 to 1 percentagepointshigher.

The

nexttwo

income

categories thatwe

consideraredividends andinterestincome. Forbothofthese income categories, thereisa greaterchance ofa declineinthemarginaltax ratethan

there

was

forwage

andsalary income.More

than32%

ofdividends,and26%

ofinterestincome,facesalowermarginaltax rate asaresultofthe

AMT.

A

largeshare ofboth dividendsandinterest

-

35.1 and41.2percent, respectively-

faces marginaltax rates that arehigher, butno

more

than fivepercentage pointshigher, as a resultoftheAMT.

The

remainingcolumns

of Table5 present similarcalculations for longtermgains, stateincome

tax deductions, andcharitable contributions.Each

ofthesethreeincome

components

ordeductions istreatedina different

way

undertheAMT.

Forlong-termgains, 12percentofthelong-term gains reported

by

AMT

taxpayers face thesame

tax ratewiththeAMT

aswithout it.Becausestate andlocaltaxes are not deductible incomputing alternative

minimum

income, butthey aredeductible for ordinary

income

tax calculations, virtuallyall taxpayers facemuch

highermarginaltax ratesonthese deductionsunderthe

AMT

than undertheordinaryincome

tax. Forsuch taxpayers,the changeinthemarginaltax rateis large

-

thefullvalueoftheAMT

rate.15

charitablecontributionscan be deducted. In partbecausecontributions tendtobe

made

bytaxpayersinupper

income

brackets, forwhom

theAMT

tends toreducemarginal taxrates, nearlythree quarters of these contributionsaredeductible ata lowermarginal tax rate as aresultofthe

AMT.

Table6

shows

the impact oftheAMT

onthecombined

federal andstatemarginal taxratesthat taxpayersface

on income

anddeductions.The

effective marginalstateincome

tax raterises from(l-tfCdcrai)*tSiatetotstatefor an itemizerundertheordinary

income

taxwho

switches tobecome

anAMT

payer.Comparing

theresults inTables 5 and6shows

how

substantial thiseffectcanbe. For example, thepercentage of

wage

incomethatexperiencesa to5 percentage pointtax increase as aresult ofthe

AMT

dropsfrom 55 to44%,

whilethepercentage witha5-10percentage point increase rises from 10 to

21%.

The

effectofrecognizing stateincome

tax rateson the distributionof marginaltax ratechangesforinterest

income

and fordividend income is similarto thatforwage

income. Forlong-termgains, the shareofgainsreceived

by

AMT

payers with no changein theirmarginal tax ratesdeclines from

42%

inthe upperpanelof Table 5 to 11.7%

inTable 6, andthe sharereceivedby

those with marginaltax rate increases betweenzeroand fivepercentrises from

16%

to72%.

Forstatetax deductions, thereisvery littlechange as aresultofthe inclusionofstatetaxes.

4.2

Weighted Average

MarginalTax

RatesTables 5 and6 offer

some

insightsonhow

theAMT

affects taxpayerincentives.The

tables do not consider

how

many

taxpayersface theAMT,

however, andthey donotyield singlesummary

measuresofthe impactoftheAMT.

To

address these needs,we

compute

weightedaverage marginal tax rates ona rangeofdifferent

income

components

receivedby alltaxpayers.We

includebothAMT

payers andothertaxpayers, andthereby obtainameasure oftheAMT's

16

category

by

averaging marginaltax ratesacross taxpayerswith weights equalto theshareofaggregate

income

or deductions inthatcategory receivedby

eachhousehold.Table7

shows

theweightedaverage marginalincome

tax rateson

fourincome

components

andon

four deductioncategories.The

tableshows

weighted average marginal taxrates everythreeyears

between

2001 and2013

both with and withouttheAMT.

Forthe"withoutAMT"

casewe

assume

thattheAMT

isrepealed butthatthere are no otherchangesinthepersonal

income

taxschedule. In practice,AMT

repealwould

presumablycoincide with changesinthe

income

tax lawthatwould

restoreatleastpartoftherevenue thatiscurrentlycollectedby

the

AMT.

Because

there aremany

possibleways

inwhich

theincome

taxcouldbe modifiedtorecoup lost

AMT

revenue, however,we

decided nottomake

anarbitrary choiceandreport theassociatedresults.

Comparing

thecolumns

for2001 and2004

inTable 7shows

thattheAMT

hasa relativelyminor

effecton

weighted averagemarginalincome

tax rates intheseyears. For2004, forexample,the estimatedweightedaveragemarginal tax rate

on

wages

is22.6%

with theAMT,

and22.3%

withoutit.The

onlyincome

ordeduction categoryforwhich

the weighted averagemarginaltax ratediverges

by

more

thanonepercentage pointis stateincome

taxes,where

thedisparityin

2004

isnearlysixpercentagepoints.The

weighted averagemarginaltax rateswithandwithouttheAMT

divergeby

more

in2010

thaninthe earlieryears ofthedecade. Forwages,the weightedaveragemarginal tax rateisprojectedtobe 1.5percentage points higherin

2010

as a resultoftheAMT.

Because themaximum

AMT

rate of28 percentismuch

lowerthanthemaximum

regular bracketrates,itmay

be surprising that the

AMT

raisesaveragemarginal taxrates.However,

the lowestAMT

bracketrateof26percent ishigher thanthe incometax bracketof15 percentthatanon-itemizing family

offourwill leave only at$78,500 ($2003), andit is slightlyhigher thanthe25percent ordinary

17

showed

a substantial fractionofwage income

receivedby

AMT

taxpayers facing ahighertaxratewith, ratherthan without,the

AMT.

The

marginal taxratepatterns forinterestincome

and fordividendsare similartothoseforwages. In2004, the

AMT

hasanegligible effect onthe weightedaverage marginal taxrateforinterestincome, and itraisesthe dividendtax rate

by

0.3 percentagepoints.By

2010,however,the effects are larger. Thereis a0.9percentage point increase inthe marginal taxrateon interest

income, anda 0.7 percentage point increaseinthe tax rateon dividends.

The

distributionofdividend

income

ismore skewed

toward high-income householdsthanthe distributionofinterestincome, soa higherfractionofdividend recipients have marginal incometax rates that areabove

theirmarginal taxrateunderthe

AMT.

The

fourthrow

in Table 7shows

the impactoftheAMT

on themarginaltaxburden oncapital gains.

The

weightedaveragemarginal tax ratewith theAMT

is higher thanthatwithoutthe

AMT,

with thedifferencereaching itsmaximum

at0.7percentagepoints in2010.The

differenceis0.2 percentagepoints in2004.

The

tablealsoshows

thattheweightedaveragemarginal tax rateundercurrentlawis lowerin

2004

than in2001,reflecting thereduction inmarginal tax rates that

was

enacted in 2003. Forrealized long-termcapital gains,JGTRRA

reduced theweightedaverage marginal tax rate by aboutfourpercentage points.

The same

tax actloweredthemarginaltax rateon dividend income,andthe third

row

ofTable7shows

the impactofthischange:a tenpercentage pointdrop inthe weightedaverage marginal taxrate.

The

last fourrowspresentinformation onhow

theAMT

affects theweightedaveragemarginaltax rates that applytovarious personal incometaxdeductions. Forstateand local

income

taxdeductions,shown

inrow

five,the effectis dramatic. Thesetax paymentsarenotdeductible from alternative

minimum

taxableincome,but theyaredeductible from taxableincome

undertheordinaryincome

tax. In2004, theweightedaveragemarginal tax subsidy onhavebeen 24.1 percent.

The

disparityisthe resultof roughly onethirdofstateand localtaxdeductionsbeing claimedby taxpayers

who

are intheAMT

regime, and forwhom

these taxes donot generate adeduction.

The

disparitybetween

theaveragemarginal taxratewith andwithoutthe

AMT

isprojectedtogrow

overthenext decade. In2010,theweighted averagemarginal taxrate

on

stateand localtax deductionsisprojectedtobe9.4 percentwiththe currentAMT

in effect,compared

with26.9 percent iftheAMT

did notexist.The

projectionsalsoshow

that expirationofthe

EGTRRA

provisionsin2011 bringsthetwo

sets ofweighted average marginaltax ratesinto closerproximity,withthe weighted marginaltaxrateunderthe statusquo, withthe

AMT,

rising

from

9.4%

in2010

to18.2%

in2013.The

AMT

hasa smallerimpactonthe weightedaverage marginaltax rates fortheotherdeductionsthat

we

consider. In2004, forexample, ithasno effecton

the weighted averagemarginal tax rateon medical deductions,and itaffectsthemortgage interestdeduction

by

0.4percentage points andcharitablecontributions

by

0.7 percentagepoints. In2010, allofthesedisparities are larger.

The

weighted average marginaltaxrate formedicaldeductions is0.5percentagepoints lowerwiththe

AMT

thanwithoutit,whileboththe mortgage interestandcharitablecontributions deductionsare atweightedaveragesthat arenearly

two

percentage pointsgreaterunderthe

AMT

thanwithoutit.Table 8 presentsweighted average marginaltaxratecalculations similar tothoseinTable

7, butitincludestheeffectofthe

AMT

on net-of-deductibilitystateincome

tax rates aswellasthe effect

on

federalrates.The

levelofthemarginaltax rates in thistable ishigher than the levelinTable7, andthe differences that resultfromthe

AMT

are also larger. For wages, forexample,theprojected impactofthe

AMT

in2010

is an increaseintheweightedaverage marginaltaxrateof2.2percentagepoints,

compared

with 1.5percentagepointswhen

onlyfederaltax rates are19

interest,the weightedaveragemarginal taxrate ondeductions risesto2.6 percentage points in

Table 8,

compared

with2.2 percentagepointsinTable 7.The

weightedaverage federal marginalincome

tax ratesinTable 7 are projections.To

provide a base forcomparison with boththe level andthevariation in similarmarginal tax rates in

thepast, Table 9 presents data foryearssince 1960on theweighted average marginaltax rates on

wages, several different

components

ofcapitalincome, and several deductions.The

dataintheappendixrepresentanupdated version ofthetimeseries formarginal tax ratesin Poterba(2002).

The

tableshows

thatthe changesassociatedwith theAMT,

evenin2010, are inmany

casessmallerthanthechangesassociated with significant taxreforms inthepast.

The Tax Reform

Actof1986, forexample,reducedthe weightedaverage marginal

income

tax rate onwage

income

by4.3 percentagepointsover the 1986 to 1988period.

The

marginalincome

tax ratereductionsassociated with

ERTA,

the 1981 tax legislation,were

comparable inmagnitude.5.

Reform

OptionsandTheirImpactonWeighted

Average

MarginalTax

RatesThe

foregoinganalysis consideredhow

various reformproposalswould

affect thenumber

of taxpayers facing the

AMT

and the distributionofAMT

payers acrossAGI

categories.We

havenotconsidered

how

reformswould

affectweightedaveragemarginal taxrates. Table 10 presentssuch informationfor

two

income components,wages

and interest income, and for stateincome

taxdeductions. Thisdeductionisthe onewith the largestchange in the weightedaveragemarginal

taxrateasa resultofthe

AMT.

The

results inTable 10show

thatall oftheproposed reforms havethe effect of reducingthe marginal taxrateson

wages

and on interest income,although the magnitudeofthese effectsvary acrossproposals.

The

proposalstosubtractpersonalexemptions from alternativeminimum

taxable

income

andto indextheAMT

exclusion forinflationarethetwo

thathave the largest20

overapercentage pointas aresultofthesereforms. Forinterest income, thesetwoproposals

along with extendingthe expiringprovisions in

EGTRRA

andJGTRA

havethe greatestmarginaltaxrateimpact. Indexingand allowing personalexemptionsunderthe

AMT

have significanteffects on theweightedaverage marginal

income

taxratethatapplies tostate incometaxdeductions. Indexing, forexample,

would

raisethismarginal tax rateby

nearlyfive percentagepoints in2010. This isthe largestabsolute effectofany ofthe proposed reforms on any ofthe

marginal tax ratesinTable 10.

Given

thattheAMT

hasmodest

effectsonmost

marginal taxrates, itisnotsurprising that the effectof

most

ofthereformproposals isalsomodest.6. ConclusionsandFuture Directions

Thispaperpresents

new

evidence onthegrowth ofAMT

liabilitiesoverthenextdecade,andthe incentive effects associatedwiththisgrowth.

Our

baseline projectionsconfirmthewidelydocumented

patternthatbecausetheAMT

exclusionlevelis not indexed,there will berapidgrowth inthe

number

ofAMT

taxpayers, andintheamount

of revenue collectedby

theAMT,

until 2010. After 2010,

when

anumber

ofprovisions inthe2001 taxreformarescheduledtophase out,the

number

ofAMT

taxpayerswilldecline, butitwillrise againinsubsequent yearsfromthe lower post-2010base.

Althoughthe

AMT

creates substantial changesinmany

aspectsoftheincome

tax system,we

find that theaverage marginaltax ratesonmany

income

components, suchaswages

andinterestincome, areaffectedonlymodestly by growth ofthe

AMT.

In2010, forexample,we

project that the

AMT

will raise theweightedaveragemarginaltax rateonwage

incomeby

1.3percentagepoints relativeto

what

itwould

be iftheAMT

were

repealed andno

othertaxchangeswere enacted. For interest income,the effect ontheweighted average marginal taxrateisjust

below

onepercentagepoint. These changesconceal largerchanges inmarginaltaxrates for21

ordinaryincometax into the

AMT

brackets of26 and 28percent. Othersdrop from marginaltaxratesabove 30percentunderthe

income

taxtotheAMT

rateof 28 percent.Our

resultsarebased on stylizedassumptions aboutthe rateatwhich

aggregate income,population, andtheprice level will

grow

overthe nextdecade. Allof our analysisusesthesame

underlyingassumptionsto "age"

income

taxrecords from 1999 through2013. Itwould

be usefultogauge the sensitivity ofour findingstotheseassumptions, andtoexplore

how

differencesingrowthrates or

more

importantlyinthe rate ofinflationbetween

2003 and2010

would

affect themagnitude of

AMT

liabilities.One

oftheunder-studied issuesassociatedwith theAMT

concernsthe impactofthistaxonthe tax liabilityofsinglehouseholds andmarried couples.

The

effectofa changein householdstatus ontax liabilitiesisdifferent

when

thetaxpayers facetheAMT

thanwhen

they facetheregular

income

tax schedule. Gravelle (2001) has notedthis potentiallyimportanteffect.The

growingsignificanceofthe

AMT

may

thereforecallinto questionthe traditionalanalysisofthe"marriagepenalty"andrelated featuresofthe

income

tax system. Future research shouldconsiderthisaspectofthe distributionof

AMT

liabilities, along with potentialreformsto address22

REFERENCES

Burman,

Leonard, WilliamGale, andJeffrey Rohaly."The

AMT:Problems

andPotentialSolutions,"National

Tax

Journal 55 (September2002), 555-596.Burman,

Leonard, WilliamGale, andJeffreyRohaly."The Expanding Reach

oftheAlternativeMinimum

Tax." Journal ofEconomic

Perspectives 17(Spring 2003a), 173-186.Burman,

Leonard, WilliamGale, andJeffreyRohaly."The

AMT:

Projections and Problems,"Tax

Notes (July 7, 2003b), 105-117.Feenberg, DanielR.,and ElisabethCoutts.

"An

IntroductiontotheTAXSIM

Model." JournalofPolicyAnalysisand

Management

12 (Winter 1993), 189-194.Gravelle, Jane.

"The

IndividualAlternativeMinimum

Tax: Interactionwith MarriagePenaltyReliefand Other

Tax

Cuts." Congressional Research Service,June 12,2001.Harvey, RobertP.andJerry Tempalski.

"The

IndividualAMT:

Why

it Matters,"NationalTax

Journal 50 (1997),453-473.

Kiefer,Donald, RobertCarroll,JanetHoltzblatt, AllenLennan, Janet

McCubbin, David

Richardson, andJerryTempalski.

"The

Economic Growth

andTax

Relief ReconciliationAct of2001:

Overview

andAssessment ofEffectson

Taxpayers." NationalTax

Journal55

(March

2002), 89-118.Poterba, James. "Taxation, Risk-taking, andPortfolio Behavior."In

Alan

Auerbach

and MartinFeldstein, eds.:

Handbook

of PublicEconomics:Volume

3 (NorthHolland,Amsterdam,

2002).

Rebelein, Robert,and JerryTempalski.

"Who

Pays the IndividualAMT?"

Washington: U.S.Treasury Department,Office of

Tax

AnalysisPaper 87, 2000.23

Tempalski,Jerry.

"The

Impact ofthe2001Tax

Billon the IndividualAMT."

Proceedings ofthe94thAnnual National

Tax

Association Conference onTaxation. NationalTax

Association: 2002. 340-348.

U.S. Congress, Joint

Economic

Committee.The

AlternativeMinimum

Tax

forIndividuals:A

24

Table 1: Projected

Number

ofAlternativeMinimum

Tax

ReturnsYear

Number

ofAMT

Returns

Percentof

Returns with

AMT

AMT

Revenue

AMT

Revenue/TotalIncome Tax

Revenue

2001 2.47 1.9 9.26 1.082002

3.56 2.7 11.04 1.332003

4.06 3.04 15.55 1.972004

3.49 2.59 14.16 1.622005

14.62 10.71 35.99 3.692006

17.94 12.99 48.22 4.602007

20.06 15.78 60.07 5.312008

28.35 20.04 81.16 6.682009

32.74 22.87 98.92 7.462010

37.11 25.61 125.53 8.78 2011 16.80 11.46 45.81 2.702012

19.44 13.18 54.6 2.992013

22.84 15.21 65.04 3.3025

Table 2:

Number

ofAMT

TaxpayersLaw

andReform

Proposalsand

Ags

;regateAMT

Liabilities,,2001- 2013, CurrentTax

Filers

Tax

Liability2001

2004

2007

2010

2013 20012004

2007

2010

2013 StatusQuo

2.1 3.3 21.8 37.2 23.8 7.4 11.7 57.5 125.7 68.1Allow

Personal Exemptions 1.1 1.8 5.7 12.2 5.1 6.2 9.4 24.7 49.7 27.8 Extend Expiring Provisions 2.1 3.3 7.1 14.1 22.9 7.4 11.7 24.8 57.6 101.9Marriage

Tax

Relief1.7 2.7 14.2 25.3 15.0 6.8 10.5 40.0 87.4 46.6 Index

AMT

Exclusion 2.1 2.1 9.8 14.0 3.1 7.4 9.3 26.7 47.8 17.9Add

$3,000 toAMT

Exclusion 1.5 2.6 16.1 30.9 18.2 6.7 10.4 44.7 101.9 53.8Add

$10,000toAMT

Exclusion 1.0 1.7 7.7 17.0 8.6 5.8 8.6 27.0 65.3 33.5Note: Filers aremeasured in millions,

projections usingthe

NBER TAXSIM

liability in billionsofdollars. Entries are basedon

model, asdescribed inthe text.

Table 3:

AMT

Liabilityas aPercentageofAdjusted Gross Income,By AGI

Category,2001-2013

AGI

Class 20012004

2007

2010

2013<25K

0.1 o I o I 0.1 0.125-50K

0.1 0.4 0.350-75K

0.5 1.3 0.675-100K

0.1 0.1 0.8 1.6 0.5100-200K

0.1 0.1 1.3 2.4 1.2200-500K

0.4 0.6 1.8 2.7 0.9>500K

0.3 0.4 0.5 0.6 4TOTAL

0.1 0.2 0.7 1.3 0.626

Table4: Projected Probabilities of

AMT

Payment by AGI, 2010

Status

Quo

Allow

PersonalExemptions

Extend Expiring Provisions MarriageTax

Relief IndexAMT

ExclusionAdd

$3,000toAMT

ExclusionAdd

$10,000 toAMT

Exclusion AllTaxpayers<25K

0.9%

0.6%

0.6%

0.9%

0.6%

0.7%

0.6%

25-50K

15.8 2.2 3.2 13.1 3.2 10.1 3.950-75K

56.3 7.2 12.4 33.8 14.7 43.6 16.675-100K

77.2 15.8 20.7 41.4 23.9 66.0 28.5100-200K

94.7 57.5 56.6 67.1 49.7 90.1 66.2200-500K

91.6 88.9 91.1 89.6 83.7 91.5 91.2>500K

33.3 30.0 35.5 33.2 31.8 33.3 33.3 AllIncomes

25.7 8.4 9.8 17.4 9.7 21.3 11.7 All Itemizers<25K

1.2%

0.8%

0.8%

1.2%

0.8%

0.9%

0.8%

25-50K

11.2 2.6 2.6 9.2 2.9 7.7 3.350-75K

47.1 7.1 11.0 28.1 13.0 34.9 15.475-100K

74.8 16.2 21.2 37.7 25.1 60.9 30.1100-200K

94.9 58.6 58.7 67.2 52.4 90.1 67.7200-500K

92.5 90.0 92.1 90.6 84.8 92.5 92.1>500K

33.9 30.5 36.1 33.8 32.4 33.8 33.8 AllIncomes

52.5 22.2 24.3 34.8 23.9 45.1 29.0Taxpayerswith

Two

orMore Depe

ndents<25K

3.4%

2.3%

2.5%

3.4%

2.5%

2.7%

2.5%

25-50K

52.1 3.4 13.5 y).} 11.5 37.1 13.850-75K

91.9 17.4 39.9 50.4 48.0 84.5 53.675-100K

98.9 30.1 53.6 51.7 63.8 98.2 73.5100-200K

99.4 56.6 77.1 68.5 82.1 98.9 89.5200-500K

100.0 98.4 99.9 99.3 95.5 100.0 100.0>500K

12.3 12.3 12.3 12.3 12.3 12.3 12.3 AllIncomes

56.1 15.6 27.8 35.6 30.6 50.4 34.311

Table 5: Effectof

AMT

on MarginalTax

Rateson VaiTax

Rate Only,Weighted

byAmount

ofIncome

Itemsious

Income Components,

2010, FederalMarginal

Tax

Rate

Change

(Percentage Points)

Wages

Dividends InterestLong

Term

Gains State Taxes Contributions Declineby>

15 0.0 0.1 0.1 0(1 0.0 1.4 Declineby

10-15 0.1 0.1 0.0 0.0 0.0 12.2 Decline by 5-10 2.3 6.9 5.0 0.2 0.0 16.9 Decline by 0-5 15 3 25.4 20.9 2.6 0.0 4(> sNo

Change

0.1 0.4 0.3 11.7 15.1 8.5 Increaseby 0-5 43.8 35.1 41.2 70.0 0.0 9.4 Increaseby 5-10 20.6 20.6 19.0 15.2 0.1 6.2 Increaseby 10-15 17.5 9.5 11.2 0.7 4.2 0.0 Increaseby>

15 1.1 3.0 3.3 0.5 80.6 0.028

Table6: Share of

Income

and Deductions Affectedby

VariousChanges

inFederalandEffectiveState

Margin

alTax

RatesDue

toAMT,

2010

Marginal

Tax

RateChange

(Percentage Points)

Wages

Dividends InterestLong

Term

Gains State Taxes Contributions Declineby

>15

0.0 0.1 0.1 0.0 0.0 1.4 Declineby

10-15 0.1 0.1 0.0 0.0 0.0 12.2 Declineby

5-10 2.3 6.8 5.0 0.2 0.0 16.9 Declineby

0-5 15.3 25.5 20.9 2.6 0.0 46.5No

Change

0.1 0.4 0.3 11.7 15.1 8.5 Increaseby

0-5 43.8 35.1 41.2 70.0 0.0 9.3 Increaseby

5-10 20.6 20.6 19.0 15.2 0.1 6.2 Increaseby

10-15 17.5 9.5 11.2 0.7 4.3 0.0 Increaseby

>15

1.1 3.0 3.3 0.5 80.5 0.029

Table 7:

Weighted

AverageMe

irginal FederalTax

RatesonIncome

and DeductionsWith

AMT

WithoutAMT

2001

2004

20072010

2013 20012004

2007

2010

2013

Wages

24.1 22.6 23 9 25.1 27.4 23.9 22.3 22.5 22.6 26.6 Interest 32.4 30.0 3 1.4 32.9 35.8 23.5 21.2 21.5 21.9 25.5 Dividends 36.6 26.5 27.7 36.4 39.4 26.1 15.8 15.8 23.5 27.5 RealizedLong-Term

Capital Gains 20.4 16.3 16.6 16.8 15.6 16.9 12.9 12.7 12.2 11.2 State Taxes -17.2 -13.6 -8.0 -6.5 -13.7 -21.1 -19.1 -20.2 -22.3 -26.1 Medical Deductions -12.1 -11.1 -11.1 -11.5 -13.7 -12.1 -11.1 -11.4 -11.9 -14 4Mortgage

Interest -22.1 -20.8 -22.8 -24.4 -26.5 -21.8 -20.2 -20.6 -21.8 -25.4 Charitable Contributions -21.7 -20.0 -21.9 -23.6 -26.1 -21.5 -19.4 -20.0 -21.6 -25.3Notes: Without

AMT

scenarioassumes repeal oftheAMT,

butno otherchangestoincome

taxlaw.

Table 8:

Weighted

Average MarginalTax

RatesonIncome

and Deductions, Federal PlusNetState

Tax

RatesWith

AMT

WithoutAMT

2001

2004

2007

2010 2013 20012004

2007

2010

2013

Wages

28.6 27.4 29.2 30.8-

(, 28.4 27.1 27.8 28.3 32.8 Interest 35.9 33.8 35.7 37.7 41.1 27.0 25.0 25.9 26.7 ;o.s Dividends 40.6 30.5 32.0 41.5 45.0 30.0 19.8 20.1 28.6 33.1 RealizedLong-Term

CapitalGains 24.9 21.0 21.5 22.0 21.2 21.3 17.6 17.6 17.4 16.7 State Taxes -19.7 -16.3 -11.0 -10.0 -17.7 -23.6 -21.8 -23.3 -25.8 -30.1 Medical Deductions -14.2 -13.4 -13.7 -15.0 -17.8 -14.3 -13.4 -14.1 -15.0 -17.8Mortgage

Interest -25.4 -24.3 -26.8 -28.8 -31.3 -25.2 -23.8 -24.6 -26.2 -30.2 Charitable Contributions -24.8 -23.2 -25.5 -27.6 -30.5 -24.6 -22.5 -23.6 -25.6 -29.7Notes: Without

AMT

scenarioassumesrepeal oftheAMT,

butno otherchangestoincome

tax30

Table9: Weighted AverageMarginal

Tax

andSubsidy Rates, 1960-2002Year

Wage

Income Interest Income Dividends RealizedLT

Gains Mortgage Interest Pension Income1960 21.86 n/a 41.64 18.99 n/a n/a

1962 22.11 25.55 42.03 17.53 n/a n/a 1964 20.52 23.18 39.37 17.43 -20.08 n/a 1966 20.11 22.39 37.09 17.73 -19.74 n/a 1967 20.46 22.61 37.86 17.81 n/a n/a 1968 22.89 25.76 40.94 20.27 -22.80 n/a 1969 23.90 26.88 41.34 20.92 n/a n/a 1970 22.89 25.99 38.52 18.08 -22.37 n/a 1971 22.01 25.07 37.16 17.98 n/a n/a 1972 22.46 25.43 36.87 17.86 -22.50 n/a 1973 23.33 26.58 38.00 17.89 -23.43 n/a 1974 24.17 27.53 39.31 18.17 n/a 21.35 1975 24.86 26.62 39.03 17.35 -24.73 21.97 1976 25.71 27.52 41.12 18.24 -25.72 24.70 1977 26.73 27.87 41.23 20.00 -27.62 22.81 1978 28.09 29.06 42.61 19.57 -28.50 23.88 1979 28.22 29.74 43.04 18.34 -28.23 24.03 1980 29.78 31.42 43.01 17.38 -29.12 26.15 1981 30.90 32.15 41.33 18.86 -29.99 27.54 1982 28.86 28.69 35.44 19.18 -27.14 25.89 1983 26.96 26.22 34.04 16.88 -24.83 23.77 1984 26.39 26.56 32.86 17.38 -24.36 24.18 1985 26.59 26.71 32.74 17.35 -24.99 24.10 1986 26.74 25.62 30.95 17.97 -24.82 23.73 1987 23.92 23.16 27.35 24.52 -23.08 n/a 1988 22.47 22.10 24.91 25.51 -22.36 22.80 1989 22.55 22.72 25.04 25.08 -22.44 22.31 1990 22.58 23.55 25.15 24.95 -22.26 22.52 1991 22.55 22.63 25.50 23.89 -21.80 22.22 1992 22.55 22.11 25.28 24.33 -21.63 22.43 1993 23.32 23.56 27.10 25.79 -22.41 22.87 1994 23.61 24.33 27.41 26.11 -22.71 24.02 1995 23.90 25.23 27.85 26.56 -22.77 24.48 1996 24.04 25.09 28.02 26.58 -23.08 25.33 1997 24.46 25.93 28.84 20.34 -23.23 26.08 1998 24.72 26.09 28.75 19.82 -23.26 26.53 1999 25.07 26.47 29.04 19.80 -23.42 27.03 2000 24.99 26.22 28.83 18.53 -23.15 26.82 2001 24.06 25.09 27.90 18.36 -22.32 25.65 2002 24.00 24.99 27.69 18.45 -22.49 25.59

m

I - CN NO On oo rn—

i <'-. oo CN NOd

"t r-~'o

—

. ,—

i oo i—

i CN i—

i cn i t i io

<r,©

ONo

d

rn r--' •^o

cnC

i i ON 1 ON 1 On t r- 00 ON '* rn On ^t_o

o

o

SI^

—

d

—

' OO -^ cn 1 1 i i r ~. -1-c

in NO—

C nO i— i ON 3j COO

o

CN ro*

rn Tf^

*' ^F 'J / -i "7 '"7 1 i 1 C ,~ <D ,_^ CN t> CN >n CN in ONo

o

r-; r~ r~ i> C~ r-^ r~ *-, Di s. CN i 1 1 1 i 1 i i _2m

s. CN _, NOq

NOm

2

<

O

CN iri in CNm

iri in in V.m

m

m

m

m

m

m

o ^ — u>

o

On ON •* r- r~- nOq

do

CN r 1 -J—

! CN—

• oi CNo

/ rn rnm

rom

m

m

—

s c/l *_> u bJD t^ -r NO r- CN f~ CN nO 3— C-o

o

CN __d

d

_;d

_Jd

^H g"

m

rnm

m

m

m

O z 1) -5U

o <*~

<*o

ON P~; oo in3

5o

o

CN~

ONd

ON On ON ONo

"

. (N rn CN Ol CN CN d — ^ 3 _o en (D_

-T On*

ro •* CN Ono

o

CN CN ,— < CN CN CN CN—

5>

cm

rnm

CO rnm

m

Cl> q " 3-©

ON CN oom

—

i CO CUo

CN f» l>^

r^ NO r-^ r^ o CN CN CN CN CN CN CN^

~uX

O

—

i NO OOm

nO r~-o

CL, —-

o

CN in rn rn •<tm

^J-^

CN CN CN Ol CN CN CN -J | C 5c r» Onq

>— 1 "* CN NO—

i 3 CO cao

—

CNm

rn ro' r^im

rnm

to 03 S CN CN CN CN CN CN CN 1) •3" no in NO NO ITj vq in CBO

o

CN CN CN CN CN CN CN CN 5 > CN CN CN CN CN CN CN CO<

v TD <L><

CO cao

o

CN -r «* ^r*

-i •^ *d-~3 CN CN CN CN CN CN CN 3 -J ca 3O

5

co CO O £ 3 Pi .2 " S—

<L> X co op § "3§

'55

•- "> x x £c

&

5 x5

§

X 3a

xO

o

O

X

" f—i2

f^C

'353

r^ XO

jHo

.2O

w

O

[-H3

3

o"5

o

35H

r/5<

Oh LUW W

Ch& w

<

2

w

<

&o<

m

Z

Figure1

RegularandTentative

AMT

Effective Rate in2003 and 2010JointFiling ,

No

Deductions and2 Dependents0.35

?e \oe i?p ztO

W

3ot itt> Vfft ffr&

Figure 2

EvolutionofAverageTaxRates 2002-2010

Fixed Distribution ofIncome1995-1999

800 c o J5

h-<

!11

140 120 100 80 60 40 20Figure 3

Effect ofRaising Exclusion in201

\AMT

sAMTforAGI>10C )K

^<\

-?Ss_ #with/kMT &AG >100K , v#withM

*•• AT/

j?

—

llliiiij-——

—

' 8. 10 20 30 40 50 60 70Increase in ExcercisefromS40,250(joint)

(thousands)

Date

Due

MITLIBRARIES