This project is funded by the European Union under the 7th Research Framework Programme (theme SSH) Grant agreement nr 290752. The views expressed in this press release do not necessarily reflect the views of the European Commission.

Working Paper n° 75

From Microcredit to Microsavings:

the Dilemma of Microfinance as a Financial

Inclusion Tool

Dr. Edgar Aragón

School of Government and Public Transformation,

Tecnológico de Monterrey

Nopoor Teaching Case

From Microcredit to Microsavings:

the Dilemma of Microfinance as a Financial Inclusion Tool

1Microfinance has been widely discussed in the literature as a tool to increase financial inclusion for the poor. As a late comer in the microfinance world, Mexico is facing several policy dilemmas in the process of catching up with the rest of the world. They include: (i) setting up legislation which promotes the formal economy and protection for financial consumers; (ii) creating bank accounts for participants of cash-transfer social programs; (iii) dealing with innovative but disruptive business models of private actors; and (iv) making the market for mobile banking and digital money a tool that promotes financial inclusion. All of which is occurring within the context of recent anti money-laundering measurements across the financial sector. This case looks more specifically into the savings component of microfinance, identifying key actors, current trends, and policy actions. Can microsavings increase financial inclusion?

I.

Financial Inclusion and Microsavings

According to the World Bank, “financial inclusion means that individuals and businesses have access to useful and affordable financial products and services that meet their needs – transactions, payments, savings, credit and insurance – delivered in a responsible and sustainable way.”2 Even though great progress was achieved between the years 2011and 2014, in which 0.7 million people opened bank accounts, there are still 2 billion people who have been excluded from the formal financial system worldwide (GPFI, 2015, p. 1).3 Thus, the promotion of polices that increase access to financial services for all has recently become a target of the United Nations sustainable development

1

This case was written by Dr. Edgar Aragón, School of Government and Public Transformation (ITESM) with support from the Nopoor FP7 Framework Programme for Research of the European Union – SSH.2011.4.1-1: Tackling poverty in a development context, Collaborative project/Specific International Cooperation Action. Grant Agreement No. 290752

2

World Bank’s Financial Inclusion page: http://www.worldbank.org/en/topic/financialinclusion/overview#1, consulted on 19 March 2017.

3

goals (SDG 8).4 Governments (regulators, development agencies, policy-makers)5, foundations and private actors are looking for new formulas to expand financial services to the poor.

Financial inclusion, however, is not just about holding a bank account. Holding an account does not guarantee financial inclusion per se and it does not represent an accurate indicator (Singh & Yadav, 2012). Plus, there are several degrees of financial inclusion, from a basic savings or current account to fully using the diversity of products (Singh & Yadav, 2012). In policy circles it is believed that once people have an account, they would likely “use other financial services, such as credit and insurance, to start and expand businesses, invest in education or health, manage risk, and weather financial shocks, which can improve the overall quality of their lives.”6 Others understand financial inclusion as a way of “helping the poor turn their savings into sums large enough to satisfy a wide range of business, consumption, personal, social and asset-building needs” (Matin, Hulme, & Rutherford, 1999). This last view is compatible with the traditional concept of microfinance, aiming to bring people out of poverty by providing them with financial services.

Within the microfinance literature, however, too much emphasis has been placed on microcredits and less on the other fields such as savings, insurance, and remittances. Research, data gathering, and policy have been focused on microcredits, while the concept of microsavings has been neglected (Hulme, Moore, & Barrientos, 2009). According to Shepherd, Scott, & Mariotti (2014), “In places where people are particularly vulnerable to shocks and stresses, savings and insurance are better at preventing impoverishment than micro-credit schemes, which can, if not well-designed, contribute to debt-driven impoverishment”. This case looks into the ways, governments and financial

institutions promote microsavings as a tool to reach the financial needs of the poor.

In the literature, it is widely understood that the poor do save, either informally or through formal channels. Informal savings have existed historically to smooth consumption and reduce income shocks (Fiorillo, Potok, & Wright, 2014, pág. 4). Quite frequently, informal savings take the form of in-kind products, such as grain, farm animals (livestock), jewelry and so on. Some people prefer informal savings when there is uncertainty regarding inflation and the viability of financial institutions. However, when a family needs cash to pay for medical care, a major cause of people falling into poverty (Shepherd, Scott, & Mariotti, 2014), the lack of liquidity of some of these items make families in need vulnerable to losing a significant part of their assets in the transaction. Some institutions, such as pawnshops, have specialized in turning informal savings into liquid assets to fill the gap left by formal institutions.

4

http://www.un.org/sustainabledevelopment/economic-growth/ consulted on 29 September 2016.

5http://www.worldbank.org/en/topic/financialinclusion/overview#1, consulted on 19 March 2017. 6

Formal savings are cash deposits made in regulated financial institutions. When savings are made by the poor in small amounts then they are called microsavings, a service traditionally provided by microfinance institutions (MFIs).7 Microsavings have major advantages over informal saving due to the “good mix of accessibility to cash, security, rate of return and divisibility of savings” (Wisniwski, 1998, pág. 1). They also provide insurance t by helping the poor manage vulnerability, reducing the impact of external shocks and building an asset base (Hulme, Moore, & Barrientos, 2009, pág. 2). As the number of MFIs multiplied and funding from donors became scarce, MFIs looked at savings partly to finance their own credit operations. Microsavings reduce the cost of external financing and represent a more stable source of funding than donors, because withdrawals of small amounts do not represent a liquidity risk (Wisniwski, 1998). If properly designed with cost accountability and financial discipline, microsavings schemes are profitable (Wisniwski, 1998).

More recently, it seems that microsavings can also be achieved through digital and mobile

technologies. Digital financial technologies have helped to expand financial services to populations difficult to reach.8 Mobile technologies have been implemented in developing countries to increase financial inclusion with mixed results. The successful case of M-PESA in Kenya, where 65% of the households used the system in 2009 (Jack & Suri, 2011), has been the source of inspiration for setting up m-banking systems in several countries. The introduction of a bank that provides cards in the Philippines proved to have generated more savings than a control group (Fiorillo, Potok, & Wright, 2014). In Malawi, the provision of microfinance services through mobile banking have had limited results: “developing m-banking systems is expensive, time consuming, and complex” (Kumar, McKay, & Sarah, 2010, pág. 3). Digital government payments (government to person or G2P), however, seem to have reduced cost, corruption and fraud.9 G2P are rather significant for providing accounts to people in cash transfer anti-poverty programs.

From this review, we now also understand that there are two components to the policy problem of making formal savings schemes accessible to the poor. On the one hand, there is a behavioral component determined by society and the needs of the poor to have a diversified savings portfolio, which varies from place to place. The behavior and the needs determine the type of savings product needed. If the product does not fit the need, then it is not going to be used, even if access to

financial institutions is generated through policy. Thus, “improving financial inclusion outcomes requires a deeper understanding of client financial behaviors, preferences and desires in order to

7

Microsavings can be defined in three different ways: as savings conducted by the poor (income minus consumption); as small amounts of cash being deposited in financial institutions; or as the deposits in savings accounts at microfinance institutions (Hulme, Moore, & Barrientos, 2009, pág. 3). The latter is the one most frequently discussed mainly because of the role already played by microfinance institutions (MFIs) in providing financial services to the poor.

8http://www.worldbank.org/en/topic/financialinclusion/overview#1, consulted on 19 March 2017. 9

improve the design, development and implementation of financial products” (Fiorillo, Potok, & Wright, 2014, pág. 5). Identification of the financial needs of the poor can take place through

competition in financial markets, where private actors design convenient and affordable products to expand the usability of people’s accounts (Demirgüç-Kunt et all, 2015).

On the other hand, there are the physical and legal components of the equation. This entail having financial infrastructure available, including adequate legislation that provides security to investors, viable markets that allow competition among financial institutions, and digital and mobile

technologies to accommodate new players. Such a vision requires integral policies that coordinate anti-poverty and financial inclusion priorities.

“To be successful in achieving financial inclusion, it’s essential for a country to have a strong political commitment and coordination across relevant public and private stakeholders, and be able to create an enabling environment and wide-reaching policies that promote

responsible financial access, financial capability, innovative products and delivery mechanisms, and high quality data to inform policy-making”.10

This case shows how Mexico, a late comer in the microfinance business, developed legislation and policies to foster financial inclusion in todays’ complex financial markets.

II.

Methodology

Evidence from the case study in Mexico has been gathered through field work in Mexico City from March 13 to April 1, 2015. Key stakeholders were identified and then more players were contacted through a snowball technique. Moreover, public officials, technology providers, bank executives, and financial consultants were interviewed during the event “Mobile Money and Digital Payments - Americas” (13-15 March) in Mexico City. In addition, qualitative open ended interviews were conducted with representatives of microfinance institutions, pawnshops, and former officials at the Mexican Congress in order to understand the challenges of financial inclusion in Mexico. Each stakeholder was asked specific questions (see Table 1). Finally, the 2012 and 2015 National Surveys of Financial Inclusion; official reports from regulators and supervisors such as CNBV, CONDUSEF, PROFECO; company reports of major banks, retail chains and convenience stores were consulted for recent financial figures.

Table 1. Example of Questions Asked to Stakeholders

10

Stakeholder Type of Question

Financial Inclusion institutions

Why did the attempt at financial inclusion through setting up bank accounts for the recipients of government support fail?

Banks To what degree have banks created savings instruments for the poor?

What are the major challenges in providing the poor access to financial instruments? Pawnshops What are the savings schemes available through pawnshops?

What have been the major factors of growth? Why have they increased so fast?

Government officials

What is the current legislation on microfinance institutions (microsavings)?

In terms of policy, what are the main strategies to generate more saving accounts among the poor?

III. The Mexican Case

The Mexican case is relevant for policy discussions for three reasons. Firstly, as a late comer, the government has made significant efforts in terms of setting up the physical and legal components to expand financial services to the poor. They include (a) creating and upgrading legislation over time that protected people’s savings and provided a legal status to all financial and microfinance institutions; (b) linking financial inclusion objectives to anti-poverty programs via Government to Person (G2P) efforts; and (c) accommodating new private players with new business or

digital/mobile technologies. Secondly, Mexico caught everybody’s attention when Compartamos, a former microfinance institution, turned into a formal bank and placed a successful IPO in

international markets. After that, other disruptive and successful business models have been implemented by retail chains of consumer products for low income segments by opening bank branches within their stores (i.e.: Banco Azteca) and by pharmacies, convenience stores, and small shops, which set up points of service (POS) for basic financial transactions (see OXXO retail chain operations below). These additions not only multiplied the financial options for people with limited access to formal banking, but increased competition among the traditional players for better serving the financial needs of the poor. Thirdly, actors have tried digital and mobile technologies in the financial sector, but with limited success. Why have these technologies worked in other developing countries, but not yet in Mexico? This case helps to broaden the policy discussion on how to increase financial inclusion among the poor.

3.1 Legislation: formalizing microfinance institutions and protecting

financial consumers

Before the Ley de Ahorro y Crédito Popular (2001), most of the microfinance organizations were NGOs (or Asociación Civil, A.C.) and savings deposited there were not backed up or secured. That is,

most microfinance institutions (MFIs) were informal, except for cooperatives which operate under the Cooperative General Law (Ley General de Cooperativas). Since then, the Mexican Congress has been trying to develop a legal framework for the highly diverse credit and savings institutions targeting the poor and to secure people’s savings in formal institutions. In 2001 Congress passed the Savings and Credit Social Law (Ley de Ahorro y Crédito Popular), which first provided a legal figure to MFIs (called SOFOL, but expired in 2013)11, and with a strict regulatory framework. However, the law did not consider that many of the microfinance institutions were too small and too rural to be able to comply with standards set up for the formal banking system.12 For example, the law required all institutions to create professional councils as part of their governance structures. Small rural MFIs could not comply with this requirement. The emphasis on making microsavings safe for consumers limited people’s options (Hulme, Moore, & Barrientos, 2009, pág. 17). Since then, the legal

framework has been reviewed several times to provide a realistic transition to formalization (see Table 2).

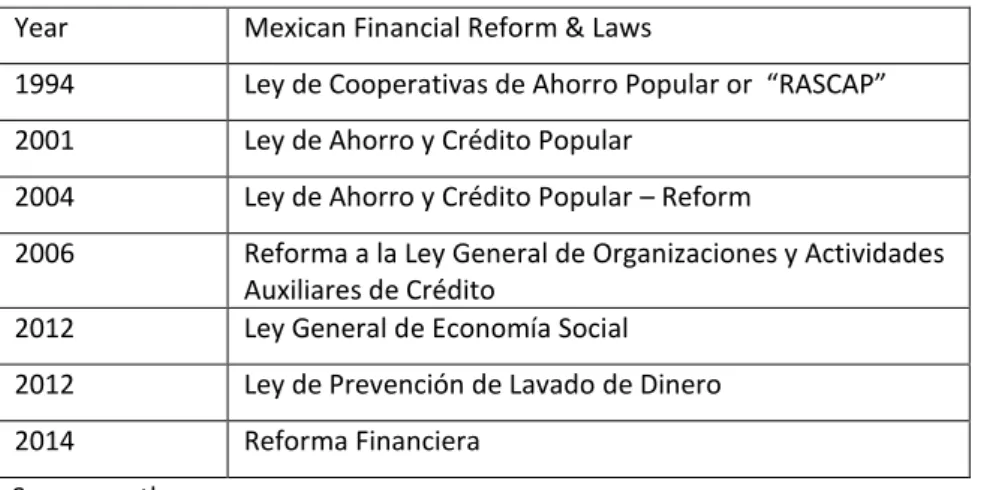

Table 2. Key Financial Reforms in the Social Sector Year Mexican Financial Reform & Laws

1994 Ley de Cooperativas de Ahorro Popular or “RASCAP” 2001 Ley de Ahorro y Crédito Popular

2004 Ley de Ahorro y Crédito Popular – Reform

2006 Reforma a la Ley General de Organizaciones y Actividades Auxiliares de Crédito

2012 Ley General de Economía Social 2012 Ley de Prevención de Lavado de Dinero 2014 Reforma Financiera

Source: author

By 2004, Congress made reforms to the 2001 law by creating two sets of financial institutions, the

regulated and the unregulated, plus supportive bodies or Federations to assist the latter in their

formalization process. 13 Thus, 9 Federations registered, audited and provided technical assistance to the unregulated MFIs. They actively engaged institutions in the formalization process with relative success.14 A 2006 reform of the General Law of Credit Organizations (Ley General de Organizaciones

y Actividades Auxiliares de Crédito) gave a legal framework to the unregulated MFIs; called SOFOM

11

In July 2013, SOFOLs stopped operating and were encouraged to transform into a different financial figure.

12

In fact, the Mexican government did not know how many microfinance institutions existed in the country, especially in the rural sector.

13

Both types of institutions lobbied Congress intensively, becoming the issue highly political. If the regulation would apply directly to all institutions, many would simply disappear.

14 Recent changes to the law reduced the roll of Federations, becoming only support institutions rather than a

E.N.R.15 They could provide some financial operations, but no savings. By 2014, there were 132 regulated credit unions and savings and credit associations, and 125 unregulated, which were operating under a separate provision under the revised law (CNBV, 2014).16 In principle, as

institutions become formalized they could conduct more financial operations (such as savings) and manage a larger amount of assets. There were other institutions which could not “formalize” their operation due to the strict financial regulation. However, they had a legal figure (SOFOM E.N.R.) and could provide microcredits. The government supported this transition by providing them with subsidized funding via PRONAFIM17, with the policy objective that they become larger, formal and independent.

As legislators learned about all the different types of financial organizations and their limitations, they modified the law again in 2014 to create alternative microfinance legal entities (private, rural, regulated, supervised, etc.) and to clearly specify their regulatory bodies, such as regulated SOFOM (or SOFOM E.R.), SOFIPO, and SOFINCOS (see Table 3).The 2014 Financial Reform (Reforma

Financiera) allowed unregulated microfinance institutions to continue operating under a legal entity

(SOFOM E.N.R.), but under the supervision of the National Commission for the Protection and Defense of Users of Financial Services (CONDUSEF). SOFOMs for example, are required to register their credit contracts with CONDUSEF and to submit periodic reports (Lorenzo, personal

communication, 2015). In addition, there were SOFOMs created by or linked to existing formal financial institutions, which in turn became formal themselves (SOFOM E.R.).18

In the rural sector, small financial institutions with social goals able to comply with a more “soft” regulation were granted the legal status of SOFINCOs, allowing them to provide both credit and savings operations to their members. SOFINCOs were given 5 regulatory levels. The most basic one only mandated them to report to their Federation, the rest required the authorization of the CNBV to operate. Once they are authorized, savings in SOFINCOs are secured for up to 25,000 UDIs (US$ 7,750 approx.) per person. By 2017, there were 27 basic SOFINCOs and only one authorized by the CNBV. Together, they provide services to only 105,000 members, showing the limits of expanding financial services to the rural sector.19

15

E.N.R. was added later to specify “entity not regulated”.

16

http://www.cnbv.gob.mx/SECTORES-SUPERVISADOS/SECTOR-POPULAR/Documents/Listado%20Socap%20entidades%20en%20pr%c3%b3rroga%2028feb14.pdf retrieved on March 30th 2014.

17 Programa Nacional de Financiamiento al Microempresario y a la Mujer Rural (see

http://www.gob.mx/pronafim)

18

E.R. stands for “entity regulated”.

19http://eleconomista.com.mx/sistema-financiero/2016/02/22/sofinco-figura-que-no-despega-pese-ley

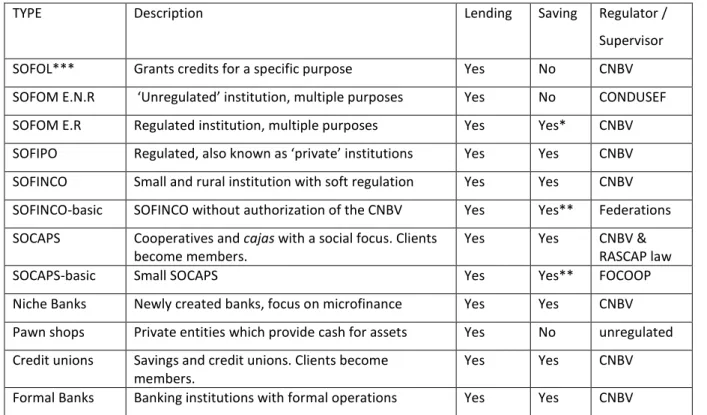

Table 3. Formal and Informal Microfinance Institutions (Lending, Savings and Regulator)

TYPE Description Lending Saving Regulator /

Supervisor SOFOL*** Grants credits for a specific purpose Yes No CNBV SOFOM E.N.R ‘Unregulated’ institution, multiple purposes Yes No CONDUSEF SOFOM E.R Regulated institution, multiple purposes Yes Yes* CNBV SOFIPO Regulated, also known as ‘private’ institutions Yes Yes CNBV SOFINCO Small and rural institution with soft regulation Yes Yes CNBV SOFINCO-basic SOFINCO without authorization of the CNBV Yes Yes** Federations SOCAPS Cooperatives and cajas with a social focus. Clients

become members.

Yes Yes CNBV & RASCAP law

SOCAPS-basic Small SOCAPS Yes Yes** FOCOOP

Niche Banks Newly created banks, focus on microfinance Yes Yes CNBV Pawn shops Private entities which provide cash for assets Yes No unregulated Credit unions Savings and credit unions. Clients become

members.

Yes Yes CNBV Formal Banks Banking institutions with formal operations Yes Yes CNBV Source: author with information from interviews; * depending on the type of association with a regulated financial institution; ** savings not guaranteed; *** no longer in operation

Institutions with a more profit-making orientation that have their own capital to operate and comply with regulation can operate under the SOFIPO legal status. They can provide credits and savings and investment services to their clients. However, only 25,000 UDIs (US$ 7,750 approx.) in savings per person are backed up by the authorities (compared to 400,000 UDIs, or US$123,970 in banks).20 SOFIPOs can even provide credits for consumption for non-productive activities. For this reason, SOFIPOs do not qualify for PRONAFIN state subsidized funds. In a way, the policy objective has been to transform SOFOM E.N.R. into SOFIPOs (Lorenzo, personal communication, 2015) or niche banks.21 For example, Forjadores Bank started as a SOFOM E.N.R in 2015 before it became a niche bank in 2012. By 2016 it had 224,000 clients in 9 Mexican states.22 SOFIPOs are regulated by the National Banking and Securities Commission (CNBV), which is the same body that regulates the banks. Another “social” financial entity which grants membership to their clients are the cooperatives (SOCAPs), also called cajas in the Mexican context. Cajas have existed for a long time. For example,

20

http://www.cnbv.gob.mx/Paginas/PADRÓN-DE-ENTIDADES-SUPERVISADAS.aspx, retrieved on 17 April 2017. UDIs is a monetary figure used in official documents Mexico which takes into account inflation. The conversion used in this case was 1 UDI = 5.74 pesos, and 18.52 pesos = 1 US$.

21

When the institutions become regulated, the interest rates of the funds received from government via PRONAFIN become lower by 1% (interview LORENZO, 2015).

22

Caja Popular Mexicana started operations in 1951. They have a social and territorial focus. Only members can receive credit and they do not have funding problems as they also receive savings from members. Thus, the interest rates charged by CAJAS tend to be lower than the ones from other institutions. Like SOFIPOS, they can lend to non-productive activities (consumption), thus they do not participate in PRONAFIN support programs (Interview LORENZO, 2015). Nevertheless, they can receive funding from the government run, development bank, BANSEFI. SOCAPs are regulated under the Cooperative and Popular Savings Law (Ley de Cooperativas de Ahorro Popular, or “RASCAP law”) and authorized by the CNBV.

There are a couple pending issues with SOCAPs. First, many smaller ones have not been able to comply with the authorization regulations yet. Thus, a new legal entity was created for SOCAPS with assets lower than US$ 713,000 called basic-SOCAPs which will not be regulated, but ‘supervised’ by a new regulatory body, FOCOOP. Second, 82 small and 73 larger SOCAPs did not pass a mandatory financial evaluation (level D) and should no longer operate according to the CNBV.23 Many went to court and some are still operating even though the savings of their members are not secured.24 The rest of the savings in SOCAPs (basic and CNBV authorized) are secured for up to 25,000 UDIs (US$ 7,750 approx.) per person. By 2017, there were 151 SOCAPs authorized by the CNBV with their total assets equaling $ 6.4Bn and providing services to almost 6 million members.25

Lastly, pawnshops have set up thousands of new offices in Mexico, capturing part of the “savings & credit” services for the poor. There are not clear statistics of the value of operations conducted by pawnshops in Mexico, but in 2017 there were 6,606 pawnshops registered in PROFECO, the Federal Consumer Protection Agency.26 It seems that this sector is also providing services to the poor and to people with no access to formal banks (Mortera, 2012). The system works by depositing a good in a pawnshop and receiving anywhere from 50-80% of the value of the object deposited (Mortera, 2012, pág. 178) making their savings liquid. Shops then charge an interest rate anywhere from 15-28% per month (180-336% per year), still lower to the 30% per month (360% annual) charged for a credit by some retailer banks, but without goods pledged as collateral. The charges cover the storage of the product, the insurance, and the money provided. If clients default, daily interest rate is

charged during a moratorium period (e.g., 30-40 days), losing their objects afterwards. According to the Mexican Association of Pawnshops, the idea is that people get the goods back in the end, so that

23

http://eleconomista.com.mx/sistema-financiero/2016/06/05/insolvencia-no-problema-las-socaps-nivel-d-alcona; retrieved on 17 April 2017.

24

http://eleconomista.com.mx/sistema-financiero/2016/06/05/insolvencia-no-problema-las-socaps-nivel-d-alcona; retrieved on 17 April 2017.

25http://www.gob.mx/cnbv; retrieved on 17 April 2017. 26

they still have goods to bring next time.27 Although there is not much data on the sector, a number of US-based pawnshops have also entered the Mexican market. Pawnshops have been recently considered informal institutions by the ENIF and they are not regulated.

In 2012 Congress also passed the Social Economy General Law (Ley General de Economía Social) and the Anti-Laundering Prevention Law (Ley de Prevención de Lavado de Dinero). They have both influenced the operation of microfinance institutions. The former had the objective to protect the savings of clients, while the anti-money laundering law imposed some restrictions on the operation of credit and savings institutions.28

3.2 Government’s efforts to expand financial inclusion: G2P and financial

education

Besides the efforts to create an efficient legal framework for MFIs to operate, the federal

government made “financial inclusion” a policy objective in 2009 (Zapata, 2016). Among the first key actions by the federal government was the creation of the National Council of Financial Inclusion (CONAIF) to design and coordinate the national policy on financial inclusion among diverse public and private entities. This was followed by an effort to collect data on financial inclusion via surveys, which has been implemented every three years since 2012. Two important actions were taken to promote microsavings in rural areas, including the promotion of Government to Person (G2P) transactions via electronic accounts and to increase the financial educational efforts to the general public.

A window of opportunity was opened to expand financial inclusion in rural areas when the Mexican Congress approved a law making it mandatory for all government cash-transfers, including the ones to the poor, to be dispersed electronically by 2012 (Zapata, 2013, pág. 5). With Oportunidades, a major conditional cash-transfer program in Mexico called Prospera was introduced in 2014. The program has about 6 million poor recipients alone, which means that financial services have been extended to a considerable number of poor families, which has been a long-standing policy goal. This government-to-person payment system (G2P) has even attracted the attention of international

27

http://anace.org/

28

For example, the debit card “Tarjetazo” provided by the Oxxo convenience stores have a maximum savings amount of $5,000 pesos (US$ 294) (Banamex - interview, 2015). Cajas de ahorro (savings banks) need to make additional reports per year to the federal authorities and to report any abnormal transaction (Interview Fernandez, 2015). This created additional cost for the Caja in the sense that a specialized persons needs to be hired and the systems modified in order to comply with the regulation (Interview Fernandez, 2015).

players to digitalize the accounts used by the 6 million Oportunidades recipients, such as the Bill and Melinda Gates Foundation (Zapata, 2013). Ultimately, the digitalization of accounts was done using a network of public entities and MFIs (DICONSA public stores, PEMEX gas stations, BANSEFI29 mobile units, and financial cooperatives) (Zapata, 2013, pág. 5).

The program, however, remained only a tool to allow the government to verify that recipients are still alive by making them cash the total amount of transfers once deposited; it offered no other financial services along with the digital accounts (Zapata, 2013). On the one hand, creating a bank account for all the beneficiaries of antipoverty programs, such as Oportunidades, seemed to have been a good idea. However, program officials encouraged beneficiaries to clear their accounts as soon as the conditional cash transfers arrived as proof that they received the funds. Moreover, there were no financial services offered, not even a basic savings package was linked to the accounts. Thus, there seems to still be little coordination among antipoverty programs and financial inclusion government teams.

On the other hand, the technological challenges to increasing banking services for rural populations, especially in remote areas, are quite significant. In Mexico, offering a diversity of financial services through the G2P payment system introduced with Oportunidades faced significant institutional, political, and technological challenges. Among the technological issues encountered by Zapata were: (a) the creation of electronic payment channels through “chip-based biometrically enabled bank-issued cards” that included the fingerprints of the recipients; (b) the existence of equipment at rural sites with biometrics reading capability; (c) the provision of financial services both online and offline aligned with the regulatory framework; and (d) reliable connectivity (Zapata, 2013). The decision concerning the technology chosen (in this case biometrically cards) was made according to the operational objectives of the Oportunidades program and not the financial inclusion goals. Regarding the financial educational efforts, in 2011 the Treasury Ministry and the Financial Consumer Protection Agency (CONDUSEF) headed the Committee on Financial Education to

“coordinate public sector stakeholder involvement in financial education” (Zapata, 2016). While the number of educational initiatives by stakeholders has multiplied since then and some programs have been designed for children, there is some room from improvement. According to Zapata (2016), most of the programs are based on what financial actors and public officials consider relevant, rather than the actual behavior and needs of people excluded from formal financial institutions. That is, little focus has been placed on the financial products themselves, the previous experience people have dealing with informal financial tools, nor on client-centered designs. In contrast, programs are

29

centered on formal financial services, access channels and financial management from the view of providers and policy makers (Zapata, 2016). What seems to be missing is a deeper understanding of the financial needs of the poor and to create products and services which address such needs. This could indeed be a good business opportunity for private actors.

3.3. Disruptive Business Models: Compartamos, Banco Azteca, OXXO

targeting the ‘base of the pyramid”

The successful conversion of microfinance institutions into viable commercial banks, such as Banco and Compartamos, has become a case for much international discussion in regard to being able to make profits by assessing the financial needs of the poor. Compartamos operations started as a project conducted by a group of students motivated by Mother Teresa of Calcutta’s visit to Mexico City. Starting originally as an NGO in 1990, Compartamos did not look for government support to avoid non-compliance by clients confusing subsidies with credits. It then began growing rapidly with financial and technological support from the IADB and the CGAP, respectively. In 2006, it became a bank and the following year gained the status of an IPO (initial public offering), the first among institutions that lend to the poor. Compartamos obtained US$ 450 million for 30 % of their current stock in international markets, which was 12 times its book value.30 Compartamos’ successful IPO showed that targeting the poor (otherwise called the “base of the pyramid” in business circles) could be a quite disruptive and profitable business model. By 2016, Compartamos had already reached almost 3 million clients.31

In the 2000s, large consumer goods retailers have been entering the microfinance sector by offering credit and savings services to low income families, sometimes setting up their own banks (Bruhn & Love, 2009). In 2002, Grupo Elektra, a large consumer retailer, opened 800 bank branches within its stores from one day to another (Bruhn & Love, 2009). Elektra’s bank and Banco Azteca benefited from the extensive databases put together through years of selling consumer products to their

current and past customers, who were mainly individuals without banking services (Bruhn & Love,

2009). Many of them were also cashing remittances sent by their relatives in the USA, right there at the store. Similar accomplishments have been conducted by Coppel and Wal-Mart by suddenly expanding their infrastructure to access people who did not have accounts in formal banks.

30

http://www.cgap.org/sites/default/files/CGAP-Focus-Note-CGAP-Reflections-on-the-Compartamos-Initial-Public-Offering-A-Case-Study-on-Microfinance-Interest-Rates-and-Profits-Jun-2007.pdf Retrieved on 16 April, 2017

31

What is remarkable is that Banco Azteca was able to tailor its products to specific market segments not only through data-mining, but through identifying behavior patterns among its clients as well (Zapata, 2016). The bank moved one step closer from financial inclusion to building financial capability by having staff training customers on how to “use a card, transact at the teller with their fingerprint, pay credit installments and understand the consequences of non-payment” (Zapata, 2016). As the bank and the retail store won the trust and confidence of its clients, they started to not only use in-store-credit, but several financial products (Zapata, 2016). Understanding the behavior of low income consumers through data analytics helped create this transition.

In the same way, formal banks that lacked contact with low income segments started offering basic financial services to people through correspondents such as drugstores, supermarkets, convenience stores, and even mom & pop shops (Zapata, 2013, pág. 14). By 2012,15 formal banks have

established points-of-service (POS) through such banking correspondents, extending financial access to more urban clients. At the end of 2012, there were 23,626 POS equipped retailers working with commercial banks (CONAIF, 2013, pág. 29), reaching almost 43,000 by 2017. The correspondent used most often, OXXO, is also the largest convenience chain in Mexico with 11,000 stores. In OXXO stores, people can pay their utility bills, transfer cash, buy air-time for cellular phones and acquire microinsurance programs. Since 2014, OXXO, Banamex (Citibank) and VISA have created debit cards linked to savings accounts called Saldazo, through which people can save up to 3,000 UDIs per month (US$ 900 approx.) and does not require signing any banking contract or credit history. With

Saldazo, people can conduct transactions at ATMs, OXXOs stores and places with internet where

VISA is accepted. They can also make cash-transfers to other people’s cards. The card costs US$ 2.70 and each withdraw costs US$ 0.50 plus VAT.32 By the end of 2016, 6.6 million Saldazo accounts had been issued and OXXO became a point-of-service for Banorte, HSBC, and Western Union.33

In contrast, banking correspondents provide a limited range of banking services, with 76% offering 4 or fewer financial services, however most provide savings and payments services (CONAIF, 2013, pág. 31). Such extensive used of banking correspondents since to be a phenomenon specific to Mexico. Such a la mexicana, market-oriented financial inclusion has taken place mainly in urban areas. However, financial inclusion in rural areas with less than 15,000 inhabitants remains very low at just 22% and it seems unlikely that the market mechanism can reach them (Zapata, 2013, pág. 14). In fact, 51% of the municipalities in Mexico with less than 50,000 inhabitants do not have a single POS (CONAIF, 2013). Such a la mexicana trend is mainly an urban phenomenon.

32 See company websites: http://www.saldazooxxo.com;

http://www.femsa.com/es/medios/innova-oxxo-en-méxico-y-lanza-la-tarjeta-saldazo-con-banamex; http://www.oxxo.com/telefoniayservicios/preguntas-frecuentes.htm: retrieved on 18 April 2017.

33 2016 FEMSA Annual Report; http://www.femsa.com/sites/default/files/Informe_Anual_FEMSA_2016.pdf;

3.4 Digital and Mobile Banking

The option of expanding financial services as a way to reduce the informal economy and expand financial inclusion through digital and mobile technologies has been attractive to the Mexican government (Del Angel, 2016). The introduction of digital and mobile services also started late in Mexico, but they have been adopted rather quickly. On the one hand, regulations for mobile banking only started in 2009 (Del Angel, 2016) as banks and telecom established their first pilot platforms. On the other hand, mobile banking contracts are increasing at fast rate (188% annually), but the number of accounts (883,657 in 2013) still represent less than 1% of mobile users in Mexico

(CONAIF, 2013, pág. 32). Both public and private actors are still struggling with how to expand digital and mobile services to reach more people.

For one thing, it seems that technology is not a problem. For mobile technologies to operate, banks and telecom firms set up a platform where users make transactions through their mobile devices. There might be some issues regarding the proprietary and monopoly power of some telecom firms because one firm controls 70% of the market in Mexico, however its network has also been used as a channel for the mobile operations of other banks (Alonso et al., 2013). Ownership of mobile phones might not be an issue now since 75% (57.1 million people) of people between the ages of 18-70 owned a mobile phone in 2015 (ENIF, 2015).

What has occurred in Mexico is that individual institutions are setting up their own network. As the experiences of Peru and Kenya show, this might not work due to the small fees per transaction in digital/mobile operations and the need for high volume to make a profit in each network. In Peru, the Banking Association made “cooperation” among the stakeholders a priority. This was possible by having a vision for the sector and the right regulation in place for both telecoms and banks. In Kenya, it seemed that one single individual network was established right at the beginning of the

introduction of mobile technologies. In Mexico, the players have not yet been able to “cooperate” to create one single platform and then “compete” based on the quality of their services. When each stakeholder has their own individual platform, the transaction cost becomes higher, and only institutions that can pass this cost to their clients can continue with the mobile banking operations. In addition, by having several platforms in place, both consumers and firms need to decide which network to use when buying and selling products, thus increasing the transaction costs. By the end, it would be easier to just use cash.

Nevertheless, as the competition among banks with mobile and digital products intensified, they developed innovative business strategies to position their network in the market. In April 2012, Banamex, together with Telcel (the dominant telecomm firm in Mexico and its bank Inbursa), created a mobile platform called Transfer.34 Legislation was adopted to allow users to open

“simplified” accounts via banking correspondents (Alonso et al., 2013). This allowed Banamex to link

Transfer to the Saldazo OXXO card in October 2013. This became a break-through in the mobile

financial industry as people with Saldazo cards could now open a Banamex-Transfer banking account and then link both to their mobile number using any type of cellular phone.35 By the end of 2015, 1.8 million people opened Transfer accounts via OXXO stores and 81% of them linked their account to their cellular phone. Other banks have developed similar programs (Bancomer-Express Account and Banorte-Mifon). However, Banamex-Transfer became the dominant player with 70% of the market (Del Angel, 2016).

Simplified accounts linked with cellular phones can be used as “electronic wallets for making payments in multiple establishments, but also as a means of transferring money to other accounts and for completing deposits and withdrawals…” in ATM machines and banking correspondents (Alonso et al., 2013). Simplified accounts are easy to open and use, and the cost is low for both users and banks (ibid). In terms of financial inclusion, the establishment of nearly 24,000 banking

correspondents as points-of-service to open simplified accounts linked with cellular phones, such as pharmacies, retail and convenience stores, and post offices, is a remarkable achievement. Now public and private stakeholders are looking into ways to expand services, such as by adding “voluntary savings in pension funds, sending and receiving remittances; loans, micro-insurance policies, investments in government bonds, online transactions and conditional direct transfers from the government” (Alonso et al., 2013).

As this takes place, other product-specific financial providers called FinTech platforms are entering the market. Examples of these types of platforms include crowdfunding, payments and remittances, insurance, personal financial management, savings, and financial education, among others.36 By early 2017, 158 mainly business to consumer (B2C) FinTech startups, had been established in Mexico, the largest number in Latin America.37 They don’t even provide financial services directly to consumers, but their main tool is the “disintermediation of key actors of the traditional value chain,

34 Banamex 2015 Company Report, p. 44:

https://www.banamex.com/resources/pdf/es/acerca_banamex/informacion_financiera/banco_consolidado/e mision_deuda/infoanual2015.pdf; retrieved on 19 April, 2017.

35 Ibid. 36 http://eleconomista.com.mx/sistema-financiero/2017/03/21/banca-digital-se-intensifica-vienen-las-fintech; retrieved on 19 April, 2017. 37 https://www.startupbootcamp.org/blog/2016/10/mexico-becomes-largest-fintech-market-latin-america/ ; retrieved on 20 April, 2017.

including banks and other financial institutions”.38 Even though regulation is still in process, it is expected that FinTech firms will take 30% of the financial market by 2027, thus accelerating the digital and mobile strategies of the Mexican banks.39 For example, in regards to micro-savings, ZAVE App and KIWI promote goal-based savings solutions for people who wish to travel or need medical treatment, such as cataract surgery or diabetes and dental treatments (Zapata, 2016).

IV.

Conclusion and Policy Recommendations

The case study about financial inclusion in Mexico provided insightful policy implications. First of all, setting financial inclusion as a policy goal is not enough. Governments need to make sure that the financial and savings needs of the poor are addressed. This requires not only addressing the physical

and legal requirements for making financial services accessible, but addressing the behavioral needs

of the poor to best determine what kind of savings product should be offered. That is, on the one hand, microsavings require the presence of financial infrastructure, such as institutions, technology, and legislation. On the other hand, financial services should be tailored to the financial needs and behavior of the poor in order to be used. In this regard, financial inclusion surveys and data analytics of consumers by retailers, as well as users of banking correspondents, have been rather useful to understand current behavior of low income families.

Second, as the Mexican government enhances regulations to foster microsavings it must ensure that transparent information on the cost of all financial services is provided. It may even be advisable to establish limits on interest rates charged by private institutions, especially in situations involving default and when credits are backed up by the client’s own savings. Competition and education have not been enough to bring rates down and to allow consumer to choose the best option, especially in rural areas where the provision of financial services is limited.

Third, it is recommended that government entities responsible for anti-poverty programs and financial access coordinate with each other since they address the same target group. Such efforts show potential in G2P, but have not been successful thus far.

Finally, the potential benefits of mobile banking should be further explored by policymakers. There are a number of questions that still exist, such as how to most efficiently set up a system to be cost effective, but this tool has much potential to increase financial inclusion for the poor. It is worth noting that in cases where people are transferring small amounts of money, mobile banking is most cost-effective when there is a large volume of transactions and providers can achieve economies of scale. In Mexico, each bank has set up its own mobile network; leadership is needed to encourage the “cooperate and compete” model.

38 https://www.startupbootcamp.org/blog/2016/10/mexico-becomes-largest-fintech-market-latin-america/: retrieved on 20 April, 2017. 39 https://www.startupbootcamp.org/blog/2016/10/mexico-becomes-largest-fintech-market-latin-america/ ; retrieved on 20 April, 2017.

Bibliography

Banamex - interview. (2015). Banamex.

Bruhn, M., & Love, I. (2009). The Economic Impact of Banking. Development Research Group, Finance and Private Sector Team. The World Bank.

CONAIF. (2013). Reporte de Inclusión Financiera 5. Consejo Nacional de Inclusión Financiera, Mexico. Retrieved March 30, 2014, from http://www.cnbv.gob.mx/Inclusión/Paginas/Reportes.aspx Del Angel, G. A. (2016). Cashless Payments and the Persistence of Cash: Open Questions About

Mexico.

Demirgüç-Kunt, A., Klapper, L., Singer, D., & Van Oudheusden, P. (2015). The Global Findex Database

2014: Measuring Financial Inclusion around the World. World Bank Policy Research Working Paper 7255. https://doi.org/10.1596/1813-9450-7255

Fiorillo, A., Potok, L., & Wright, J. (2014). Applying Behavioral Economics to Improve Microsavings

Outcomes. Gammen Foundation. Ideas42.

GPFI. (2015). Financial Inclusion Action Plan 2014. Retrieved September 23, 2015, from

https://g20.org/wp-content/uploads/2014/12/2014_g20_financial_inclusion_action_plan.pdf

Hulme, D., Moore, K., & Barrientos, A. (2009, October). Assessing the insurance role of microsavings. (U. Nations, Ed.) DESA Working Paper, ST/ESA/2009/DWP/83(83), 20.

Jack, W., & Suri, T. (2011, January). Mobile Money: the Economics of M-Pesa. NBER Working Paper

16721. Retrieved March 31, 2014, from http://www.nber.org/papers/w16721

Kumar, K., McKay, C., & Sarah, R. (2010). Microfinance and Mobile Banking: The Story So Far. The Consultative Group to Assist the Poor. Retrieved March 30, 2014, from

http://www.gsma.com/mobilefordevelopment/wp-content/uploads/2012/03/fn62rev2.pdf Matin, I., Hulme, D., & Rutherford, S. (1999). Finance and Development Research Programme, (9). Mortera, E. (2012). The Golden Age for Pawnshops Current Social Factors that Drive their Success in

the Mexican Market. School of Doctoral Studies (European Union) Journal, 177-186. Retrieved March 31, 2014, from http://www.iiuedu.eu/press/journals/sds/SDS-2012/SSc_Article3.pdf

Shepherd, A., Scott, L., & Mariotti, C. (2014). Te Chonic Poverty Report 2014-2015: The road to zero

extrem poverty: Executive Summary and Overview. Chronic Poverty Advisory Network

(CPAN). Overseas Development Institute (ODI).

Singh, J., & Yadav, P. (2012). Micro Finance As A Tool For Financial Inclusion & Reduction Of Poverty.

Journai of Bussiness Management and Social Science Research Management and Social Science Research, 1(1), 1–12.

Sinclair, H., & Gamser, M. (2013). Crossfire: ‘Should financial inclusion be part of the next set of MDGs?’. Enterprise Development and Microfinance, 24(4), 275-281. Retrieved March 30, 2014, from

http://practicalaction.metapress.com/content/02765nv146420t2x/?genre=article&id=doi%3 a10.3362%2f1755-1986.2013.026

Stuart, G. (2007). Dinámica de la regulación: Implementación de la Ley de Ahorro y Crédito Popular en México. Foro de Microfinanzas. Monterrey, Nuevo León, México.

Wisniwski, S. (1998). Savings in the Context of Microfinance – Lessons Learned from Six Deposit-Taking Institutions. Presented at Interamerican Forum on Microenterprise. Mexico City. Zapata, G. (2013). Correspondent Banking in Mexico's Rural Areas: Lesson from a G2P Payment

Digitization. Bankable Frontier Associates, LLC, Somerville, MA. USA.

Scientific Coordinator : Xavier Oudin ([email protected]) Project Manager : Delia Visan ([email protected])

Find more on www.nopoor.eu Visit us on Facebook, Twitter and LinkedIn