When and Why Does It Pay To Be Green?

Texte intégral

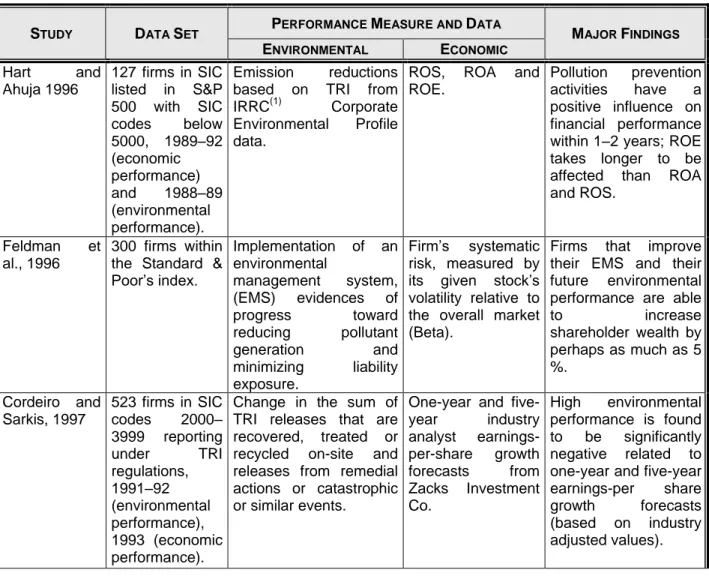

Figure

Documents relatifs

The predictions are the following: (i) a switch from a fixed to a variable wage increases the average level of effort, (ii) introducing the possibility for

a Department of Cardio-vascular Surgery, University Hospital CHUV, Rue de Bugnon 46, 1011 Lausanne, Switzerland b Department of Radiology, University Hospital, 1011

The field of ICT governance defines a management analysis framework through appropriate organizational structures that allow controlling and ensuring that ICTs contribute

Rhumatologie Neuro-chirurgie Anesthésie Réanimation Anesthésie Réanimation Anatomie Biochimie-chimie Dermatologie Chirurgie Générale Traumatologie orthopédique Hématologie

Table 5. reports the Pearson correlations between the model variables. Pearson correlations vary between 1 and -1 and measure the linear relationship between two

The first stage measures firm operational performance through DEA efficiency scores to identify the best-perform- ing firm practices, and the second consists of a bootstrap pro-

In this paper we draw on insights from theories in the management and corporate governance literature to develop a theoretical model that makes explicit the links between a

ا اخث ذنننننن يمثها نننننن ذ لهثانننننننلخاي نننننن مثاثلننننننحاي اخذننننننسث دمثانننننننلخادننننننيدرمثاتنننننن بادننننننقه ي الماحترنننننن لحثا