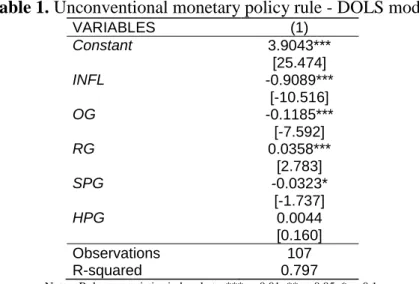

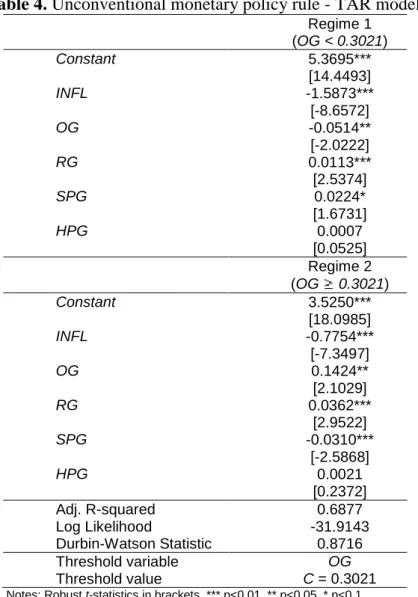

Unconventional monetary policy reaction functions: evidence from the US

Texte intégral

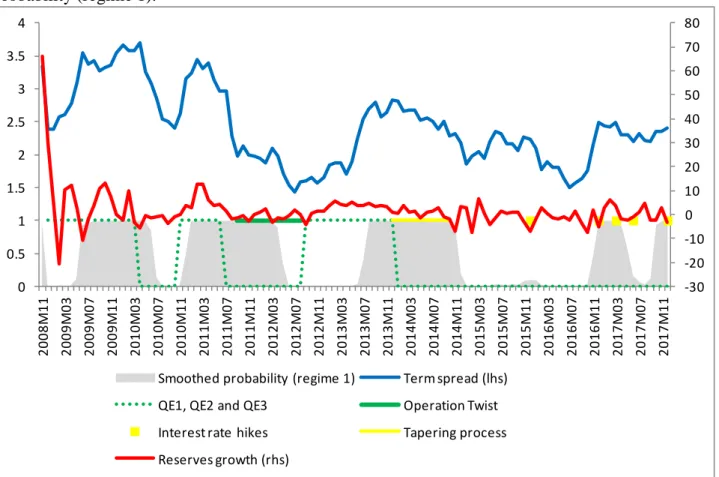

Figure

Documents relatifs

Methodologically, we develop a dynamic conditional version of the capital asset pricing model (CAPM) which allows for time-varying quantity and price of risk and

[r]

To this end we use a proxy of local hurricane destruction derived from a physical wind field model within a dynamic labour demand framework of quarterly county level

All estimates include bank-specific controls (i.e. liquid assets to total assets, equity to total assets, customer deposits to total assets, is the natural logarithm of

The Statute of the ECB and the ESCB (principally Article 3) sets out the tasks of Eurosystem NCBs as: ‘to define and implement the monetary policy of the Community’; ‘to conduct

A small electric field, which defines the quantization axis of the atoms, is applied with high uniformity by field plates above and below the atomic beam..

Therefore, even though they are very reflective (solar reflectance greater than 0.60), bare metal roofs and metallic roof coatings tend to get hot since they cannot emit the

In [KMP08] it was proven that if traffic demands are sufficiently steady the problem can be expressed in an independent form of the interference model as the Round Weighting