Digitized

by

the

Internet

Archive

in

2011

with

funding

from

Boston

Library

Consortium

Member

Libraries

HB31

.M415

\o.ol-Massachusetts

Institute

of

Technology

Department

of

Economics

Working

Paper

Series

CURRENT

ACCOUNT

DEFICITS

IN

RICH

COUNTRIES

Olivier

Blanchard

Working

Paper

07-06

Feb

10,

2007

Room

E52-251

50

Memorial

Drive

Cambridge,

MA

02142

This

paper can be

downloaded

without

charge

from

the

Social

Science Research

Network Paper

Collection

atMASS.' ~: ~"' ITE

OF TECH

FEE

2 22007

LIBRARIES

Current

Account

Deficits in

Rich

Countries

Olivier

Blanchard

*February

10,20007

(first draft:October

30,

2006).

*

MIT

andNBER.

Mundell-Fleminglecture given, at theIMF

inNovember2006.Ithank

Ricardo Caballero, Francesco Giavazzi, Guido Lorenzoni, AndreiShleifer, Roberto Rigobon,

andJoseTessadaforcommentsanddiscussions.Ithank TatianaDidierforexcellentresearch

Abstract

Current account imbalances havesteadily increased in richcountries over the

last 20 years. While the U.S. current account deficit dominates the numbers

andthenews, othercountries, especiallywithintheEuroarea, are alsorunning

largedeficits.

Thesedeficitsaredifferent from the LatinAmericandeficitsofthe early 1980s, or the Mexican deficit ofthe early 1990s.

They

involve rich countries; theyreflectmostly private savingand investment decisions, andfiscal deficitsoften

playa marginalrole; and thedeficitsare financed mostlythrough equity, FDI,

andown-currency bondsratherthan throughbank lending.

Yet, thereappears a widely shared worry that thesedeficits aretoo large, and governmentinterventionisrequired.

My

purpose,in this lecture,is toexaminethe logic ofthis argument. I ask the following question:

Assume

that deficitsreflect private saving and investment decisions.

Assume

also that people andfirms have rationalexpectations. Should thegovernment intervene, and, ifso,

how?

To

answer thequestion,Iconstructasimplebenchmark.Inthebenchmark, theoutcomeisfirstbest andthereisnoneed norjustification forgovernment

inter-vention. Ithen introduce simple distortionsin eithergoods, labor, or financial

markets, andcharacterizetheequilibriumin each case. Ideriveoptimalpolicy

andthe implications for the current account. I show that optimal policy

may

or

may

not lead tosmaller current account deficits.Iseethemodel andthe extensionsvery

much

asafirstpass.Sharper conclusionsrequireabetterunderstandingoftheexactnatureandthe extent of distortions,

and

we

donot have it. Such understanding is needed howeverto improvetheIntroduction

The

lasttwenty

years havebeen

characterizedby

steadily larger current ac-count imbalancesinrich countries. This isshown

inFigure 1,which shows

theevolution ofthe cross-country standard deviation ofratios of current account

balances to

GDP,

since 1988,for three sets of countries.The

firstlinegives theevolution ofthe standarddeviation forthe countries

which

aremembers

oftheOECD

today; thishowever

isan

unbalanced panel,and

new members

such asMexico

orCentralEuropean

countries are quitedifferentfrom

earliermembers.

For this reason, the second line gives the evolution of the standard deviation

for the countries that

were

alreadymembers

oftheOECD

in 1988.The

line isvery similar to the first:

The

increase is not drivenby

the addition ofthenew

members.

The

third line gives the evolution of the standard deviation for thesetofcountries

which

aretoday

in theEuro

area.The

evolutionis again quitesimilar.

Figure 1.

Standard

deviation ofCA

deficits/GDP1990 1995 2000 2005

All

OECD

Euroarea

Balanced

OECD

Source:

OECD

database.Behind

these trends aretwo

major

stories.The

first isan

increase in deficits within theEuro

area. Countries suchasPortugaland

Spainarerunningdeficits closeto10%

oftheirGDP.

The

otheris the increaseinU.S. deficits,which

now

From

the LatinAmerican

deficits ofthe early 1980s to theMexican

deficit ofthe

mid

1990s, currentaccount deficitshave regularlymade

the news.1Today's

current account deficits are

however

quite differentfrom

their predecessors.The

countries in deficit arerich countries.The

deficitsare notprimarily drivenby

fiscal deficits, but ratherby

private savingand

investment decisions.The

deficitsare typicallyfinancedthroughequityflows,

FDI

flows,and

own-currencygovernment

bonds, rather thanthrough

bank

lending.Thus,

many

oftheconcernsassociated with, say, the LatinAmerican

deficitsofthe 1980s,

seem

much

less relevant here. Yet, policymakers

and

many

econo-mists

worry

thatthedeficits are toolarge.To

caricature, there areroughlytwo

views:

The

first isknown

as the"Lawson

doctrine",named

after NigelLawson,

theChancellor ofthe

Exchequer

who

articulated it inthe 1980s. This "doctrine" isbasically a restatement ofthe first welfare theorem:

To

the extent that currentaccount deficits reflect private saving

and

investment decisions, that there areno

distortions,and

thatexpectations arerational, thenthere areno reasons forthe

government

to intervene.The

second—

and

more

prevalentview—

could be calledthe "prudential" or the"IMF"

view. It is that, even ifdeficits reflected private savingand

investmentdecisions, distortions are present

and

lead to deficitsthat aretoo large.Govern-ment

intervention toreduce these deficitsis desirable. Thisview

is reflected inthe frequent use ofsuch terms as "global imbalances"

and

"fragility" tochar-acterize current evolutions.

What

exact distortions,and whether

theseindeedjustifypolicies

aimed

at reducingdeficits, has nothowever

been

worked

out.The

purpose

ofmy

lectureistoexplorethis issue.Moving away

from

particulars,I take

up

anarrow

question, namely:Assume

that a current account deficit reflects private savingand

investment decisions.Assume

rational expectations.Is there

any

reason for thegovernment

to intervene,and

what

is the optimalform

ofthatintervention?It isclearthattheanswer

depends

on

the existenceand

thespecificform

ofdis-tortions presentin the economy. Thus, Istart

from

abenchmark

inwhich

suchdistortions are absent, the equilibrium is the first-best outcome,

and

there isno

role forgovernment

intervention. I then introduce variousdistortions,which

are often thought to be important in this context. In each case, I characterize

the effect ofthe distortion

on

the equilibrium,and

discuss the role of policy.Clearly theroleof policyis to increase welfare, not reducethedeficit perse.

As

we

shall see, optimal policymay

ormay

notimply

a reductionin the deficit.Isee the

model and

itsextensionsverymuch

asafirstpass. Sharperconclusionsrequireabetterunderstandingoftheexact nature

and

theextentofdistortions,and

we

do

not have it.Such

understanding isneeded however

toimprove

thequality ofthe current debate.

The

lecture is organized as follows.Section 1 looks at current account deficits within the

Euro

area, with apar-ticular focus

on

Portugal,which

is, inmany

ways, a poster child for the issuesraised in thislecture. Section 2 brieflyreviews the evidence

on

the U.S. currentaccount deficit,

and on

"global imbalances".Section 3develops the

benchmark.

My

focusbeingon

distortions, Idevelop thesimplest

benchmark

needed

for the purposes,namely

a two-periodeconomy,

withtradables,non-tradables

and

leisure, log-logpreferencesand Cobb-Douglas

production. I focus

on

the effects ofa shift in preferences,namely

a decrease in the discount factor.As

is well understood,two

mechanisms

are at work: intertemporal reallocation ofconsumption

(and leisure) across periods,and

in-tratemporal reallocation of production

between

tradablesand

non-tradables.Distortions

may

affect either orboth

mechanisms,

and by

implication, affectcurrent account deficits. Sections 4 to 6 look at the implications of different

distortions.

The

first-best equilibrium is associated with increases in the relative price ofnon-tradables

and

in thewage

in the first period,and

corresponding decreasesinthesecond period. Section 4looks at the implications of price or

wage

rigidi-ties,

and

characterizes optimal policy.The

optimal policy is to eliminate theboom/slump

innon-tradables generatedby

priceorwage

rigidities; thismay

ormay

not imply a decrease in the current account deficit.The

first-best equilibrium is also associated with a decrease in the productionoftradables in the first period,

and

an increase in the production oftradablesinthe second period.

One

may

thinkof distortionswhich

may

make

it difficultto recover

and

expand

production in the second period. Financial constraintsthe funds

needed

for production in the second period. Section 5 looks at theimplications ofsuch adistortion,

and

characterizesoptimalpolicy.The

purposeofoptimal policy in this case is clearly to limit the decrease in tradables

pro-duction in the first period. This

may

ormay

notimply

a decrease the currentaccount deficit.

One

ofthe current worries of policy makers, even in theUnited

States, is thepossibility of a

"sudden

stop", a sharp increase in the rate ofreturn requiredby

foreign investors.By

itselfand

absentdomesticdistortions, thepossibilityofa

sudden

stop does not changethe first-best nature ofthe equilibrium: Privateagents will take this possibilityinto account

when

making

plans.The

questionis

whether sudden

stops can interact with distortions in away

that justifiesgovernment

intervention.Many

potentialmechanisms

havebeen

identified, butmost seem

largely irrelevant in rich countries. Section 6 discusses these issuesby

extending thebenchmark

to athree-period model. This allows us tolook at the effects of a positive probability of asudden

stop in the second periodon

the equilibrium,

and

the potential role ofpolicyin that context.There

is a long leapfrom

these simple exercises to actual deficits. Section 7nevertheless takes the leap,

and draws

tentative policy implications,both

forcountries within theEuro,

and

for "global imbalances".1

Current account

deficitswithin the

Euro

area

Today,

two

member

countries oftheEuro

area, Spainand

Portugal,havecurrentaccountdeficitsclose to

10%

ofGDP.

Inthe contextofthispaper, theexperienceofPortugal is particularly interesting, solet

me

start there.2The

basicmacroeconomic

evolutions areshown

in Figure 2,which

gives theevolution of the

unemployment

rate,and

of the ratio of the current accountdeficit to

GDP

in Portugal, since 1995.The

figure points totwo

very differentperiods:

The

first isan

economic

boom, from

1995 to 2000.There

is generalagreement

that the sources of the

boom

were twofold,both

associated with the prospectofjoining the Euro.

The

firstwas

a steady decrease in real interest rates,due

in large part to the disappearance of the currency

premium.

The

secondwas

theexpectationthat joiningthe

Euro would

accelerateconvergence,and

lead tohigherproductivity growth.

Both had

theeffect ofincreasing private spending,leading

both

to higher outputgrowth and

to a steady increase in the currentaccount deficit.

By

2000, theunemployment

ratewas below 4%, and

the currentaccount deficit slightly above

10%

ofGDP.

Figure 2.

Unemployment

rateand

currentaccount

deficitPortugal,1995-2007

gm

Q.D

co<3( CO CD O (0 1995 19961997 1998 1999 20002001 2002 2003 2004 2005 2006 2007 Unemploymentrate CurrentaccountdeficitNote, as this goes to the

theme

ofthe lecture, that expectationsmay

not havebeen

rational, butwere

surely not crazy.Note

also that theboom

was

drivenby

private spending, not public spending.From

1995 to 2000, the ratio ofthe

budget

deficit toGDP

decreasedfrom

5%

to3%;

theOECD

measure

ofthe cyclically-adjusted deficit

remained

roughly constant.Note

finallythat theboom

was

associated with steady real appreciation:From

1995 to 2000, unitlabor costs increased

by

12%

relative to theEuro

area average.Expectations offasterconvergence

may

havebeen

reasonable.But

theyturned out not tobe

borne outby

the facts: Productivitygrowth

hasremained

verylow, indeed lower

than

itwas

in the 1990s. Starting in 2001, privatespend-ing

growth

sharply decreased, leading to lowgrowth

and

a steady increase inunemployment. Attempts by

thegovernment

to sustaingrowth

have led toan

increaseinfiscaldeficits,

which

arenow

around

5%

ofGDP.

The unemployment

rateis

back around 8%.

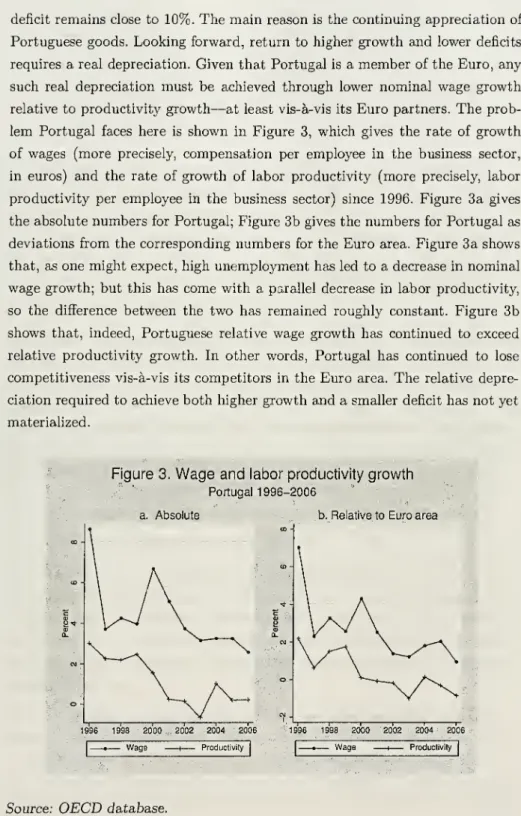

deficit remains close to 10%.

The main

reasonisthe continuing appreciation ofPortuguese goods.

Looking

forward, return to highergrowth

and

lower deficitsrequires areal depreciation.

Given

that Portugalis amember

ofthe Euro,any

such real depreciation

must be

achieved through lowernominal

wage

growth

relative to productivity

growth

—

at least vis-a-vis itsEuro

partners.The

prob-lem

Portugal faces here isshown

in Figure 3,which

gives the rate ofgrowth

of

wages (more

precisely,compensation

peremployee

in the business sector,in euros)

and

the rate ofgrowth

oflabor productivity(more

precisely, laborproductivity per

employee

in the business sector) since 1996. Figure 3a gives theabsolutenumbers

forPortugal; Figure 3bgivesthenumbers

forPortugalasdeviations

from

the correspondingnumbers

for theEuro

area. Figure3a

shows

that, asone

might

expect, highunemployment

has ledto a decreaseinnominal

wage

growth; but this hascome

with a paralleldecrease in labor productivity,so the difference

between

thetwo

hasremained

roughly constant. Figure3b

shows

that, indeed, Portuguese relativewage growth

has continued to exceed relative productivity growth. In other words, Portugal has continued to lose competitiveness vis-a-vis itscompetitors in theEuro

area.The

relativedepre-ciationrequired toachieve

both

highergrowth and

asmallerdeficit has notyetmaterialized.

Figure 3.

Wage

and

labor productivitygrowth

Portugal 1996-2006 a. Absolute....

.

. .

b.RelativetoEuro area

Wage Productivity Wage Productivity

Should

Portuguesemacroeconomic

policyhavebeen

different inthesecondhalf of the 1990s?Given

what

we

now

know, namely

that expectationswere

toooptimistic, the answeris obviously yes.

The

relevantquestion ishowever

what

should have

been

done

givenwhat was

known

then? Shouldgovernment

poli-cieshave

reduced theboom,

limited the appreciation,and

limited the currentaccount deficit?

The

question ofwhat

should havebeen done

during theboom

in Portugal isnow

academic.But

the question is very relevant for Spain today. Since themid-1990s,steady

growth

hasledto alargedecreaseintheunemployment

rate,down

from

20%

tounder

9%

today—

a decreaseoften referred to asthe "Spanishmiracle." This

growth

hasbeen

sustainedby growth

inprivate spendingratherthan

public spending:The

fiscal positionhas turned from a largedeficit in themid

1990s toasurplus of1%

ofGDP

today.At

thesame

time,growth

hascome

with a steadyrealappreciation. Since 1995,unit labor costs haveincreased

by

21%

relative to theEuro

area.The

currentaccountdeficithasincreased

from rough

balanceinthemid

1990sto9%

ofGDP

today. This raises aset ofobvious questions. Will Spain go through the

same

adjustment

processasPortugal?Should government

policieshave beendifferent overthelastdecade?Should

they havelimitedoutput growth,appreciation,and

thecurrent account deficit?

What

should the Spanishgovernment

do today?2

The

U.S. current

account

deficitThe

U.S. current accountdeficit hasdominated both

thenews and

much

oftheresearch ininternational

macroeconomics

inthe recentpast.3My

purposehereis onlyto pointto the aspects directlyrelevant to the

theme

ofthelecture, therole of private saving

and

investment versus fiscal policy, theway

the deficithas

been

financed,and

the rationality ofexpectations underlying decisionsand

investors's choices:

The

U.S. deficit is very large,and

reflected in current account surplusesvis-a-vis the

United

States inmost

regions of the world.The

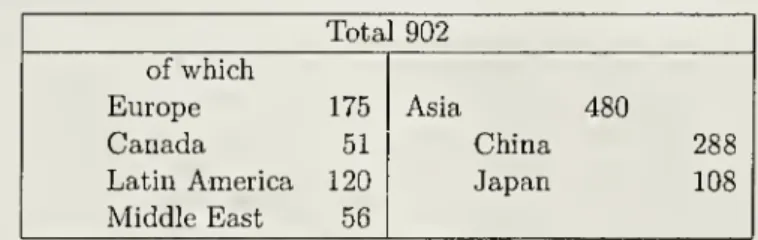

composition of the3.

A

goodsurveyoftheoriesand factsis providedbyCline (2005).An

insightfulanalysis ofthe relative roles of saving, investment, andporfolio flows, intheUnited States andcreditor

corresponding current account surpluses for the third quarter of

2006

is given in Table 1.Roughly

half is accountedby

Asia, primarilyChina and

Japan.Roughly

one fourthis accounted forby

Europe.Of

the rest, an increasing but stiUsmall proportionisaccountedforby

theMiddle

East, reflectingthe increasein oil prices.

Table

1.The

U.S. current

account

deficitand

itscounterparts.

2006-3, in billions

of

dollars, atannual

rates.Total 902

of

which

Europe

175 Asia 480Canada

51China

288Latin

America

120Japan

108Middle

East 56Source:

BE

A

International Transactions. Table 11,January 2007

The

U.S. deficitand

the corresponding foreign surpluses havemany

causes.I believe that there is

now

a broad consensusabout

the following proximatecauses. First, low U.S. saving, reflecting primarily low private saving, but also

budget

deficits. Second, high foreign saving, particularly from Asia—

what

Ben

Bernanke

(2005) has referred to as the "savingglut." Third, lowforeign invest-ment, inboth

Europe and

Asia. Fourth, a strong preferenceby

investors forU.S. overforeign assets. All four factors are

needed

to explain thecombination

ofcurrent accountbalances, thestrongdollar,low world realinterest rates,

and

apparently low expected returns

on

U.S. assets.4The

important point formy

purposes is that fiscal policies,whether

in theUnited

States or abroad, while notirrelevant,are clearlynotthemain

cause ofthe U.S. current accountdeficit.Private saving

and

investment decisions—

sometimes mediated

through policy,such as the combination of capital controls

on

capital outflowsand

reserve ac-cumulation inChina

—

around

theworld are.Bank

lending,which

was

central to the LatinAmerican

deficits, is nearlyir-relevant in the case of theU.S. deficit.

The

composition offoreign holdings of4. For more discussion, see in particular Bernanke (2005), Blanchard, Giavazzi, and Sa

(2005), and Caballero, Farhi,and Gourinchas (2006).

financialassets, for

both

stocksand

flows,is giveninTable 2.The

compositionof flows has

changed

over time, but the picture givenby

the stocknumbers

isvery clear: In the third quarter of 2006, gross foreign holdings of U.S. assets were roughly equal to 11 trillion dollars.

Of

those, roughly40%

took theform

ofholdingsofcorporateequities

and

directinvestment—

a verydifferentpicturefrom

the financing ofLatinAmerican

deficits.Table

2.Composition

of foreignholdings

ofU.S.

assets (billionsof

dollars).

2006

Flows

Stocks Total 1,406 11,946 T-bills 101 2,069 Official holdings 111 1,371 Privateholdings -10 698 Corporate equities 112 2,601Corporate bonds

377 2,596 Direct investment 185 2018Source:

Flow

of Funds, FederalReserve Board. TablesF.107,and

L.107. Stocks:"Total U.S. financial assetsheld

by

therestofthe world", asof2006:3. Flows:"Net acquisitionoffinancial assets

by

therestoftheworld", over thefirstthreequartersof2006.

There

hasbeen

much

discussion as towhether

investors behind these capitalflows

have

rational expectations.There

isno

question that, sooner or later,current account deficits will have to decrease,

and

this willmost

likely requireasubstantialrealdepreciation of U.S. goods. For thisreason,

and

given thelowU.S. interest rates, a

number

ofeconomists have argued that foreign investorswere

too optimisticabout

expected returnson

U.S. assets. If investors havea strong preference for U.S. assets however,

and

if they anticipate the rateof depreciation to be positive

but

small, then the evidence against rationalexpectationsis

much

weaker. Indeed, overthepastfewyears, financialinvestorsrather

than

these economists appear to havebeen

right about the strength ofthedollar.

In short: Current "global imbalances" appear to

come

primarilyfrom

shiftsin private saving

and

investment. In the absence of strong evidence to thecontrary, the

assumption

that expectations are rational does not appearun-reasonable. This takes us back to the question raised in this lecture.

Beyond

reducingthe U.S. budget deficit

—

a reductionwhich

indeed appearsjustifiedon

its

own,

but,by most

estimates,would

onlymake

a dentinthe current account deficit—

should the U.S. (andother)governments

aim

atreducingtheremaining imbalances further?Why,

and

ifso,how?

3

A

benchmark

For this

and

the next three sections, I shall focuson

the followingnarrow

question:

Assume

current account deficits are the result ofprivate savingand

investmentdecisions.

Assume

expectationsare rational. Shouldthegovernment

intervene,

and

ifsohow?

To

do so, I startwith the followingbenchmark:

The

model

The economy

goeson

—

and

peoplelivefor—

two

periods.Ineachperiod,peoplederive utility

from

theconsumption

oftwo

goods, tradablesand non

tradables,and from

leisure.5Utility is given by:

where

and

maxV =

U

+

/3U'U

=

\og(C)+

<j>\og(L)\og(C)

= hog(C

T

)+

^\og(C

N

)where

primes denote second period variables,Ct

and

Cn

denotetheconsump-tionoftradables

and

non-tradables respectively,and

L

denotesleisure. (3 is thediscount factor.

As

is wellknown,

the log-log assumptions,and

the implication of equalin-fratemporal

and

intertemporal elasticities of substitution eliminate anumber

5. Iintroducealabor-leisurechoicebecause,when,later, Iintroducedistortionswhichimply that employment ispotentially offthe labor supply, I wantto be ableto assess thewelfare

cost ofsuchadeviationandderivethe optimalpolicy.

of interesting issues, in particular with respect to the path of tradables

con-sumption.6; but they are fine for the points I

want

tomake

in this lecture.Taking

tradables as thenumeraire,and assuming

for simplicity that the world interest rate, theinterestrate intermsof tradables,isequaltozero, thebudget

constraint ofconsumer-workers isgiven by:

qC

N

+

C

T

+

q'C'N

+

C

T

= A = w(N

t

+

N

N

)+

w'(N

T

+

N'

N

)+ir

+

n'with

N

T

+

N

N

= L-L,

N

T

+

N'

N

=

L

-

L'where

A

is total wealth,Nx

and

Nn

denoteemployment

in the tradablesand

non-tradables sector respectively, q

and

iu denote the relative price ofnon-tradables

and

thewage

in terms in tradables respectively. 7r is profit. For themoment,

there isno

government; I shall introduceit later.On

the production side, competitive firms in the tradablesand

non-tradablessectors

maximize

profitsubject to the following production functions:Y

T

=

Nf,

Y

N

=

N

N

awith similar equations holding for the second period. Capital is implicitly

as-sumed

tobe fixed, sothere isno

investment decisionin themodel. I shallfocuson

current account deficitscoming

fromvariations in saving.The

equilibrium

Equilibrium requires that,ineach period, the non-tradables

and

the labormar-ket clear. This gives us four equations:

_

111.

,W

a/(a-l)C

N

=

Y

N

=>-

—

—

-

A =

—

2 1+

p

q aq18

1 w' /(0_1)and

»r T r ,W,l/(a-l),W

,1/(0-1) ? 1N

T

+

N

N

=

L-L

=>(-)

+(—

)=L

a aq 1+

Q

w

6. Seeforexample ObstfeldandRogoff(1996), 4-4, equation(34), and Dornbusch (1983).

w' 1/(a_1) w' 1/(a_1)

6

where

1 '

' '

'W

A =

Y

T

+

Y^

+

qY

N

+

q'Y^The

four equilibrium conditions are straightforward:Wealth

is equal to thepresentdiscounted valueofoutputintermsof tradables.

Spending

on

tradables,on

non-tradables,and on

leisure are all proportional to wealth.The

supplyof non-tradables

—

equivalently thedemand

for laborfrom

the non-tradablessector

—

is a decreasing function of thewage

in terms of non-tradables; thedemand

for laborfrom

the tradables sector is a decreasing function of therealwage

in terms oftradables.If

=

1, (so thediscount rate is equalto theworld interest rate,namely

zero), then the equilibrium is thesame

inboth

periodsand

the current account isbalanced. Itwill benotationally convenient to

assume

that, in thisequilibrium,all quantities are equal to one, i.e. that Cj

=

Yi=

TVj=

L

=

C[=

Y(=

N[

=

L'=

1, for i=

T,N.

This in turn requires thatL

=

3and

<j>=

a/2. Forour purposes, these restrictions are innocuous.

Under

this normalization also, q=

q'=

1,and

w

=

w'=

a. It is alsoconvenient to introducew

=

w/a,

so inthe initial equilibrium

w =

w'=

1.Increased

impatience

and

current

account

deficitsI shall consider throughout the effects of

an

increase in impatience,d0

<

0,starting

from

=

1. Exactly thesame

analytical resultswould

obtain—

with aminor

differencewhich

Ishallpointoutbelow

—

if Ilookedinsteadatadecreaseinthe rate ofinterest at

which

thecountrycan borrow, dr<

0,startingfrom

r=

—

anexperiment

which

would

capture forexample

part ofwhat happened

in Portugalinthe 1990s.Other

shocks,forexample

the anticipation of increasesin productivityineithertheproduction oftradables or non-tradablesnextperiod,would

lead todifferentanalyticalresults,butthesame

generalconclusionsabout distortions,and

the role for policy.The

decrease in leads totwo

reallocations, intertemporal,and

intratemporal:•

Being

more

impatient, peoplewant

tospend

more and work

lessin thefirstperiod.

•

Consumption

ofnon-tradablesand

tradablesincrease.The

consumption

of tradables increases

more

than theconsumption

ofnon-tradables.Tak-inga linear approximation

and

solvingthe equationsabove

gives:dC

N

=

\

T

±

ir

(-df3)>

0;dC

T

=

\{-dp)

>

16 —

la I•

Employment

decreases(leisure increases).Employment

innon-tradablesincreases, but

employment

intradables decreasesby

more:dN

N

=

i^Mfl

>

0;dN

T

=

j^i-dP)

<

•

The

price of non-tradables, q, increases.So

does the tradables productwage, w.

The

non-tradables product wage,w/q

decreases:dqv

=

-

l^±(-d0)

> dw

= ^—^(-dp)

>

2

3-2a

v '3-2a

v 'The

realconsumption

wage,w/y/q

increases.• Increased

demand

for,and

decreasedsupplyoftradables lead toacurrentaccount deficit:

1 3

d (current account deficit)

=

-

-—

—

{—dp)

>

£ o /id

• All changes hold with opposite signsin thesecond period.

•

As

a, the degree ofreturns to labor, increases, the production frontierbecomes

lessconcave,and

itbecomes

easierto shiftproductionbetween

tradables

and

non-tradables. Thus, the price of non-tradablesand

thewage

increaseby

less.The

productionofnon-tradablesincreasesby

more,theproductionof tradables decreases

by

more,leading toalargercurrentaccount deficit.

Thus, theequilibriumresponseexhibits

an

appreciation followedby

adeprecia-tion, and,correspondingly, adecreaseintheproductionoftradables followed

by

an

increaselateron.The

current accountdeficit inthefirst period,due

to bothhigher

consumption

and

lower production of tradables, is offsetby

a currentaccount surplus in the second period.7

7. Underthealternativeassumption ofa decrease intheinterestrate,dr

<

0, alltheequa-tionsabovewouldhold,with dr replacing d/3.Theonlydifferenceisthat,whilethe decrease

Clearly,

under

the assumptionsmade

so far, theoutcome

is the first-bestout-come,

and

there isno

need nor justification forgovernment

intervention.The

questionsare then:

What may

be the relevant distortionsin this context?How

do

they affect the equilibrium?And

what

is the optimal policy? In the nextthree sections, I explore three general directions:

The

potential role ofwage

or price rigidities in distorting the adjustment; the potential role of financial

constraintsindistortingadjustmentinthe tradables sector;the implications, if

any, ofthe possibility of

sudden

stops, inwhich

the countryis either cutfrom

world financial markets, or has to

pay

amuch

higher rate of return.4

Wage

and

price

rigidities,and

current

account

deficitsDuring

the 1990s, the increase in spending in Portugalcame

not only witha current account deficit, but also an output

boom

and

a large increase inemployment.

This is in clear contrast to theoutcome

in ourbenchmark,

where

the current account deficit

comes

with a decrease inemployment.

8The

result in thebenchmark

ismore

general thanitmay

first appear:The same

would be

true of an increase in expected productivity, leading to an increaseinwealth,

and

thus to an increase in bothconsumption

and

leisure in the firstperiod.Thispoints tothe potentialroleof

wage and

pricerigiditiesindistortingthe adjustment:

The

price of non-tradablesand

the realwage

may

not haveincreased

enough

to achieve the desired infratemporal reallocationbetween

thetwo

sectors.The

slump

since2000points toanother typeof potentialwage and

pricerigidity.In the first best, shifting

from

a currentaccount deficit in the first period to acurrent accountsurplusinthe secondrequires a decreasein therelativeprice of

non-tradables

and

intherealwage.Such

arealdepreciationhas provendifficult to achieve inPortugal. This points tosomething

likedownward wage

rigidity.There

aremany

ways

of formalizingwage and

pricedistortions, and, inthe end,the details matter. In this section, I take a first pass

by

simplyassuming

thatboth

qand

w

do

not adjust at all,and

thusremain

equal to one throughout.in Phas noeffectonwealth A, the decreaseinr increaseswealthbydA

=

-2dr.8. Oneofthe

many

problemsinmappingany modeltothedata: Theinitialunemploymentrate in Portugal (7% in 1995) was probably higher than the naturalrate at thetime. Thus, someoftheemployment increasein the1990swasprobablyjustified.

I

assume

thatemployment

is determinedby

labordemand.

That

is, Iassume

that, inthe tradablessector,

demand

isdeterminedby

profitmaximization,and

that, in the non-tradables sector, labor

demand

is determinedby

thedemand

for non-tradables.9 I leave the discussion of

downward wage

rigidity to later; itturns outthatitseffectsarequitedifferent

from

thoseinthis section,and

closelyrelated to the effectsoffinancial constraints, discussed inthenext section.

The

equilibrium

Inadditionto the assumptions that q

=

q'=

1and

w =

w'=

1, theequilibrium is givenby

the condition that the non-tradablesmarket

clearseach period:Y

N

= C

N

=>Y

N

!2(1+/?)

Y'N

-C'

N

=

Y'N

-^-j-^

where

2+

Y

N

+

Y^

Output

of non-tradables is givenby

thedemand

for non-tradables,which

isproportional to wealth.

Wealth

is in turn equal to thesum

of outputs in thetradables

and

non-tradables sectors over the two periods.Given

w =

w'=

1,profit

maximization

in the tradables sector implies constant production Y-j-=

Y±

=

\.Together, these

two

equations determine output of non-tradables inboth

pe-riods,

and

thus total output,and

wealth.Wealth

in turn determines thecon-sumption

of tradablesinboth

periods,and by

implication the current accountbalance.

Increased impatience

Consider again anincreaseinimpatience, adecreasein/?.

Given

wage and

price9. Theusualrationalizationwouldbetoassumemonopolisticcompetitiveprice-settingfirms

in the non-tradablesector,willing to satisfy demandso longas price exceedsmarginal cost.

An

explicit formalizationwould then havean additional distortion, namely the presenceofthe monopolisticmarkup. Thisdistortion, so long as the markupisconstant,isirrelevant for

my

purposes.rigidities, only one

mechanism

isnow

at work,namely

intertemporal realloca-tion:• People again

want

tospend

more

and work

lessin the current period.•

Consumption

ofnon-tradablesand

tradables increase,and

now

increaseby

thesame

amount. Denote

first-bestchangesby

a star.Then:

dCN

=

\{-dj3)>

dC

N

>

0;dC

T

=

\(-d(3)=

dC*

T

>

The

increase in theconsumption

oftradables is thesame

as in the firstbest. But, because the price of non-tradables does not increase, the

in-crease in the

consumption

on

non-tradables is higher than in the firstbest.

•

Employment

in non-tradables increases.Employment

in tradablesre-mains

unchanged.So, incontrast tothefirstbest,employment

increases:dN

N

=

—

{-dp)

> dN*

N >

0;dN

T

=

> dN%

dN =

--!-(-dp)

>

2a• Increased

demand

fortradables,togetherwithan

unchanged

supply, leadto a current account deficit:

d (current account deficit)

=

-

{—d(3)>

Because

the increase indemand

for tradables is thesame

as in the firstbest,

and

supply does not decreasewhereas

it does in thefirst best, thecurrent account deficit is actually smaller than in thefirst best.10

• All changes hold with opposite signs inthe second period.

Thus, the

economy

goes through aboom

cum

current account deficit in thefirst period, a

slump

cum

current account surplus in the second period.Both

the

boom

and slump

areinefficient.Workers

would

ratherwork

less than theydo

inthe first period,and

more

than they do inthe second period.A

role forpolicy?

10. Thisresultisnot robusttomoregeneralpreferences,and

may

notholdiftheintertemporaland intratemporal elasticities of substitution are different. But the point that the current accountdeficitneednotbe largerundersuchrigidities, is general.

Can

policyimprove

theoutcome

and, ifso,how?

A

fullanswer

would

requireafull other lecture. Let

me

briefly talkabout monetary and

tax policy,and

thendeal

more

formallywith the potential role ofgovernment

spending.Depending on

theexact natureofrigidities,monetary

policycangetthealloca-tion close to oreven

back

tofirst best.Take

forexample

the casewhere wages

are flexible

and

onlynominal

non-tradable prices are rigid(w

isflexibleand

qisfixedintermsofdomestic currency).

Then,

theappropriatenominal

depreci-ation can achievethe first-best q,

and by

implication, replicate thebenchmark

allocation

—

eliminatingboth

theboom

and

theslump, while allowingforacur-rentaccountdeficit

and

intertemporalreallocation.In thepresenceofboth

wage

and

pricerigidities,monetary

policycannot ingeneralsimultaneouslyreplicatethefirst-bestvalues of q

and

w.But

it canstillimprove

the outcome.11For the countries within the

Euro

such as Portugal,monetary

policy is notavailable

however

—

at least with respect to country-specific shocks. This shiftsthe focustowardsfiscalpolicy.

Here

again, giventhenatureofthe distortions,asufficientrichsetof taxes,say taxes

on

non-tradablesand on

labor, can achievefirst best. Let

me

however

focuson

the potential role ofgovernment

spending.Let'sextend the

benchmark

toallow utilitytodepend on government

spending,according to:

U

=

log(C)+

cj>log(L)+

a

log(G)where

\ogG=

-\og{GT

l )+

\\og{G

N

)Assume

also that allgovernment

spendingis financedthroughlump

sum

taxa-tion.

To

maintainthesimplepropertythat,if /?=

1, allsteadystateproductionsare equal to one, <j>

must

now

satisfy <j>—

(1+

a)a/2; Imake

thisassumption

in

what

follows.Given

thesymmetry

intreatmentbetween

privateconsumption

and government

spending, it is clear that, in the absence of distortions, optimal fiscal policy

would

simplybe given by:Gi

=

ad,

i=

T,TV;G

•=

a

C[, i=

T,N

11. Thisiswelltraveled groundintheresearch onoptimalmonetarypolicyin an open

econ-omy. Seefor example Devereux and Engel(2006).

so, that for /3

=

1,1+a

1+a

Ishallcallthis the "neutral"

component

offiscalpolicy,and

focuson

deviationsfrom

this neutralcomponent,

denoted dgi,i= T,N

and

dg[,i=T,N

for thefirst

and

second periodrespectively.Now

turn to the role ofgovernment

spending in the case of priceand wage

rigidities.

Given

thesymmetry

offirst-periodand

second-period effects ofthedecrease in /?, it follows that the optimal policy satisfies dg'

N

=

—dg^

and

dg'r

=

—dgr-

Thus,we

can focuson

the determination of justdg^

and

dgr-Going through

the characterization of the equilibrium,now

in the presence of the government, gives:dY

N

=

\{-dP)

+

dgN

,dCN

=

i—

L-(-d/3),dGN

=

I-5L_(-d/3)

+

dgN

z

zi

+

q

z l+

a

An

increaseingovernment

spendingon

non-tradablesincreases output ofnon-tradables one-for-one. It has

no

effecton

theconsumption

of non-tradables.The

reasonwhy

consumption

is unaffected is the absence ofa wealth effect:Any

increase indg^

is expected to be offsetby an

equal decrease in dg'N

;any

increasein

dY^

inducedby

higherdg^

is alsoexpected tobe

offsetby an

equaldecrease in

dY^:

dY

T

=

0,dC

T

=

\

-L-

{-dp),dG

T

=

I

-~

(-dp)

+

dgT

z 1

+

a

Z 1+

a

An

increase ingovernment

spendingon

tradables hasan

effect neitheron

pro-duction nor

on consumption

of tradables. Thus, it affects the current account deficit one-for-one.The

reasonwhy

consumption

is unaffected is again theab-senceofa wealtheffect.

Any

increaseindgx

isexpectedtobe

offsetby an

equal decrease indg

T

.12

Thus, the right tool to reduce the inefficiency is clearly dg^.

A

negativedg^

in the first period, associated with apositive dg'

N

inthe second period allowsthe

government

toeliminatetheboom

and

the slump.A

negative dgx, followedby

a positive dg'T

would

reduce the current account, but have no effecton

theinefficiency. This suggests that theoptimal policyis to use only

dg^

and

dg'N

.12. Theextreme formofsomeoftheseresultsdependsagainonthelog-log restrictions. But

themessage abouttherelativeeffectsofdgN and dgr isgeneral.

Indeed, under a quadratic approximation to the utility function

and

a linear approximation to the equilibrium conditions, the optimalpolicyis given by:2(a

+

a+

aa)This policy leaves the current accountdeficit unaffected, but reducesthe

boom

and

theslump.The

message

from

thisfirst extensionis that priceand

wage

rigiditiesmay

welldistort the allocation.

The

optimal policymay

nothowever

be

to reduce thecurrent account deficit. Indeed, inthe simplecase

worked

out here, the currentaccount deficit is unaffected.

One

question iswhether

more

asymmetric

formsofrigidity, such as

downward

wage

rigidity,would

leadto differentconclusions.The

answer

is yes,and

Ishall return to this below.5

Financial

constraints,

and

current

account

deficitsAdjustment

inthe first best implies first a decrease, thenan increase (equal totwice theinitialdecrease) intradables output.

One

worry

isthat itmay

indeedbe difficultforthetradables sector to

expand

aftera long periodof appreciationand

low production.One

may

think of anumber

of reasonswhy

thismight

be. Internal costs ofadjustment are not the issue:

These

will indeed affect the adjustment,and

thus affect in turn first-period decisions

and

the current account deficit; but,absent other considerations, the

outcome

will stillbe

the first-best outcome,and

there isno

role forgovernment

policy.Other

distortionsmay

however be

relevant.

Krugman

(1987)emphasized

forexample

external learningby

doing,and

the fact that a long period of low productionmay

lead topermanently

lower productivity. Others have

emphasized

financial constraints, the fact thatthe tradables sector

may

not, after a long period oflowprofits, have thefundsneeded

to investand

increase production later on.I explore this idea

by

making

a simple, ifhighly reduced form, assumption. Iassume

that production oftradables in the second period is givenby:w

a~1Y±

=

min(Y

T

,(-)

)Production

of tradablesisequal totheminimum

oftheprofitmaximizing

levelof

output

in the second period,and

the level of production oftradables in thefirstperiod. Fortheshock

we

shalllookat,namely

anincreaseinimpatience,theconstraint is binding,

and

second-period tradables output is thus constrainedto be

no

larger than first-period output.Some

generalitywould

be obtainedby

allowing the parameter in front offirstperiodoutput tobe different

from

one; but thisisinessential.A

rough

justifica-tion for this

assumption

may

be the following: Tradables firms canborrow

up

to

some

multiple offirstperiod earnings—

which

areproportional tooutput—

topay

the second-periodwage

bill,which

is itself proportional to second-period output.A

more

explicitand

richer micro-grounding is givenby

Caballeroand

Lorenzoni (2006):

During

the appreciation period, firms incur losses.Because

of financial constraints, these losses

may

forcethem

to decrease their capitalstock

beyond

what

would

be efficient, putting constraints on the recovery inthe second period.

Another

issueiswhether

firmsinthe tradables sector internalizethis constraintwhen

takingoutput

decisions in the first period (and so choose a higher levelofproduction in the first period inorder to relaxthe constraint

on

production in the second period). Thisdepends on whether

the constraint holds at thelevel of the firm or for the tradables sector as a whole. I

assume

that theconstraintholdsforthe sector asa

whole

(thatthereis,forexample, asegmented

financial

market where

only tradables firms can participate),and

so firmsdo

not internalize it intaking decisionsinthe firstperiod.

The

equilibrium

Equilibrium requiresthat the tradables

market

and

the labormarket

eachclearineach period, yielding four equilibrium conditions. Let

me

introduce thegov-ernment from

the start, soas to prepare forthe discussion of policy later on:C

N

+

G

N

=

Y

N

=>1-LpkA

+

dgn

=

(f) o/( ° !)N

T

+

N'

N

=

L-L'

=> ffii/(*-D+

(f)^"-1)=

I-^A

where

A =

(YT

+

Y

T

+

qY

N

+

q' Yj,)-

(q dgN

+

q' dg'N

+

dgT

+

dg'T

)Leaving aside the additional terms

coming from

the presence of fiscal policy,the onlydifference

between

these equationsand

thoseofthebenchmark

areinthe specification ofthe second-period

demand

for labor in the tradables sectorin the fourth equation:

Assuming

the constraint is binding, labordemand

inthe second periodis equal to labor

demand

in the first period,and

sodepends

on

the first-period rather than the second-period realwage.The way

fiscalpolicy entersisalsostraightforward,dgn

and

dg'N

directlyaffect thedemand

fornon-tradables,both

directlyand

throughtheir effect on wealth.dgT and

dg'T

affectspendingand

laborsupply onlyto theextentthat theyaffectwealth. This is

what

isshown

in thelast equation.Increased

impatience

Consider

now

the effects of an increase in impatience, d(5<

0,assuming

firstthat there is

no

fiscal policy response, so all dg's are equal to zero.Then:

• Just as in the

benchmark,

peoplewant

to intertemporally substitute,enjoy

more

consumption

and

more

leisure in the first period.But

theynow

also take into account that lower tradables production in the firstperiodimplieslower tradablesproductioninthesecond period,

and

thus lowerincome

in the second period. This leads to a decrease in theirwealth,

and

thus lowerconsumption and

higher labor supply inboth

periods.

• Thus,the

demand

fortradablesand

non-tradablesincreases, but,inboth

cases,

by

lessthan

in the firstbest:dC

N

+dG

N

= dY

N

=

J(-d/3)>

dC'

N

+dG'

N

=

dY^

=

%{-d0)

>

D

dC

T

+

dG

T

=

^—^-(-dp)

>

dC'T

+

dG'T

=

-i±i£(-d/?) <

6

Both

because the increasein non-tradables outputin the first period issmaller than in the first best,

and

because the decrease in labor supplyis smaller than in the first best, the decrease in tradables output in the

first period is alsosmaller than in the first best.

As

the financialmarket

constraint is binding, the decrease in tradables output in the second

period is the

same

as in thefirst period.dy

r

=

-|(-d/3)<o

dy^

=

-^(-d/?)

<

oHigher

demand

and

lower supplyof tradables lead to acurrent accountdeficit.

The

current account deficit ishowever

smallerthan

in the firstbest:

d(current account deficit

=

-(—

d(3)>

Because

the increase in thedemand

for non-tradablesis smallerthan inthe first best, so are theinitial appreciation

and wage

increase:dg

=

^(-d/3)>0

dq'=

_l±£(-d/3) <

dw

=

^-—

-(-dp)

>

dw'=

-

a^{-dp)

<0

In contrast to the first distortion, adjustmentsin the second period are

not mirror images ofthose in the first period.

Output

oftradablesgoesdown

inboth

periods, output of non-tradables goes up.The

currentaccount deficit

comes

with aslump

in the tradablessector.The

misallocation of laborbetween

thetwo

sectorsinthe second periodleads to a decrease inwealth,

and

to afirst-order loss in welfare:dA

=

-|(-d/3)

<

0;dV

=

-a{1

+

a

\

-d/3)<

Optimal

fiscalpolicy

Given

thisoutcome,

is there a role for fiscal policy? Intuition suggests thatthere is:

A

decrease inGn

can decrease thedemand

and

the production ofnon-tradables,

and

thus increase the production of tradables in the firstpe-riod and,

by

implication, in the second period. Increases in eitherGt

or G'T

,while theyhave

no

directeffecton

the productionof tradables, decrease wealthand

thusprivate spending, includingspendingon non-tradables. This againin-creases production of tradables in the first period,

and by

implication, in thesecond period. This suggeststhat optimalpolicyincludes decreasesinG/v,

and

increases in

Gt

and

G'T

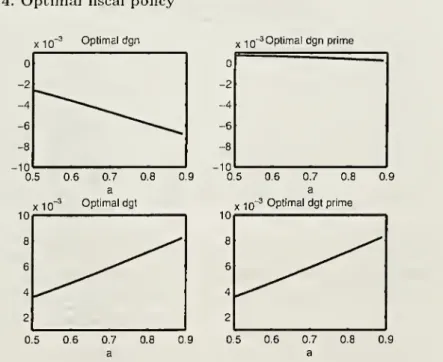

.Figure

4.Optimal

fiscalpolicy

X 10~3 Optimaldgn x-jo -3Optimaldgnprime x10 0.7 a Optimaldgt 0.9 0.7 a x -|q-3Optimaldgtprime 0.9

This is indeed the case. Figure 4 gives the optimal values of the dgi's (the

deviation from neutral fiscal policy) obtained

by

maximization of asecond-order

approximation

to the utility function subject to a linear approximationofthe equilibrium conditions given above.

The

figure gives values fora

=

0.5and

a rangingfrom

0.5 to 0.9. Itshows

that, indeed, optimaldg^

is negative,optimal dg'

N

is close to zero,and

optimaldgr and

dg'T

are equal to each otherand

positive.Figure5

shows

the deviation of the currentaccount deficitfrom

itsvalueabsentfiscalpolicy.

Note

thatthe current accountdeficitis actually larger underopti-mal

fiscalpolicy (forexample, 0.004 higherifa=

0.9).The

reason isthatwhilethedecrease in

government

spendingon

nontradables increases the productionof tradables, the optimal policyalso requires

an

increaseingovernment

spend-ing

on

tradables,which

directly increases the currentaccount deficit. Isee thisresult not as a

major

implication, but, again, as awarning

that the presenceofdistortions does not necessarily require policies

aimed

at reducingthe currentaccount deficit.

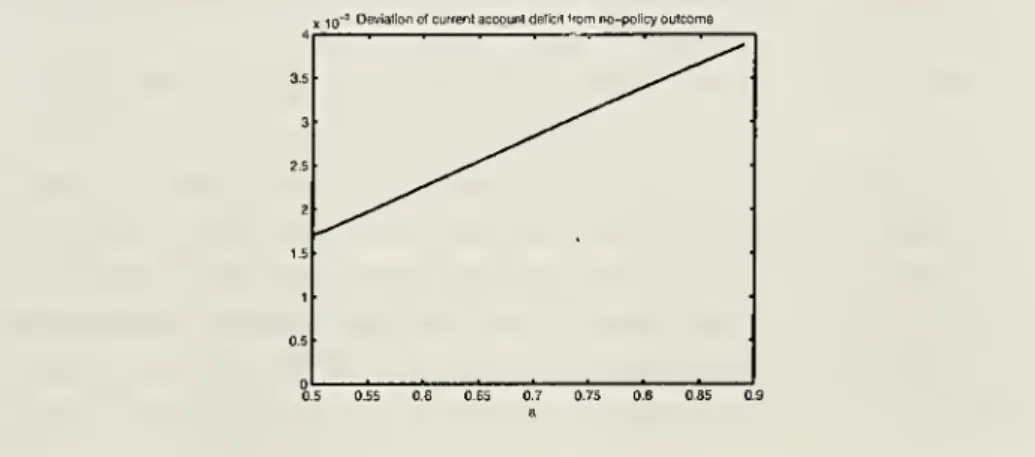

Figure

5.Current account

deficit,with

and

without

fiscalpolicy

Deviationofcurrentaccountdeficit'rom no-policyoutcome

0.55 0.6 0.65 0.7 0.75 0.6 0.85 0.9

The

message

from this second extension is that, to the extent that financialconstraints matter in the tradables sector, there is indeed a role for policy to

limit reallocation in the first period.

The

optimal policyhowever

may

ormay

not decrease the current account deficit.

How

important are the relevant financialmarket

imperfections,and

how

much

do

theylimitreallocation?13One

might

guessthat tradables firmsinrich coun-trieswould

beamong

those with the best access tofinancialmarkets,and

thuswould be

least likely to be financially constrained. But, as far as I can tell,we

do

notknow. Recent work by

Calvo, Izquerdio,and

Talvi (2006) suggeststhat,eveninArgentinaafterthe collapse

and

thedisorganization ofcreditmar-13. The question has been explored, in a different but related context, by Caballero and

Hammour

(2005), who have looked at whether recessions lead tothe disappearance oflow productivity versusfinanciallyconstrainedfirms.kets, tradables firms have

been

able to increase production in response to the(admittedlyverylarge) peso depreciation.

Let

me

return briefly to an issue I left aside in the previous section,namely

the implications of

downward wage

rigidity.Under

theassumption

that thewage

in terms of tradables can increase but cannot decrease, the equilibriumlooks very

much

like the equilibrium I havejust characterized. In response toan

increaseinimpatience,downward

rigidityprevents thefirst-bestreallocationofproduction:

The

realwage

goesup

in the first period, but cannot godown

in the second period, leading to lower production of

both

tradablesand

non-tradables in the secondperiod. Anticipations oflower future income,

and

thuslower wealth (relative to first best), lead people to

want

toconsume

lessand

work

more

inthe first period (again,relative to first best).The

result is a lowercurrent accountdeficit

and

boom

in the firstperiod,and

an outputslump

cum

current account surplus inthe second period.

Note

that,under

financialmarket

constraints,the labormarket

clears inthesec-ond

period, but the allocationis distorted towards non-tradables; underdown-ward

rigidity, the labormarket

does not clear,and both

the production oftradables

and

non-tradables are lower. In terms of policy however, thecon-clusions are roughlysimilar.

Optimal

policy requires measureswhich

limit thewage

increaseinthefirstperiod, eitherby

decreasingdemand

for non-tradablesor the supply of labor.

6

Sudden

stops, distortions,

and

policy

I suspect that,

up

to this point, I have not dealt with themain

worry

in themind

ofanumber

ofeconomistsand

policymakers,namely

"suddenstops."Thisis the

worry

that a countrymay

find itselfsuddenly cutfrom

world financial markets, ormore

realistically for a country such as the United States, thatforeign investors

may

ask suddenlyfor amuch

higher rate of return.14That

sudden

stopscanhappen

isamply

demonstrated

by history,most

recentlyby

theAsiancrisis.15That

they canlead tosharpdepreciations,and sometimes

14. Thisis forexamplea recurringtheme inNourielRoubini'sblogcommentary on the U.S.

current accountdeficit.

15. TheAsiancrisisindeedshowsthatsuddenstopscanhappeneveninthe absenceof large

current accountdeficits.