Non disponible

Texte intégral

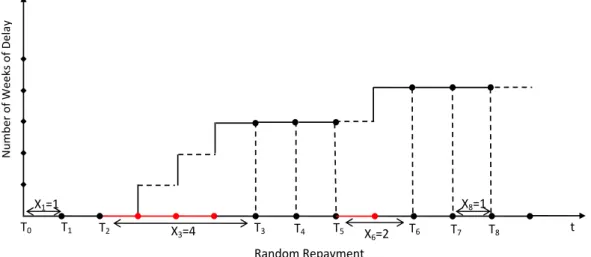

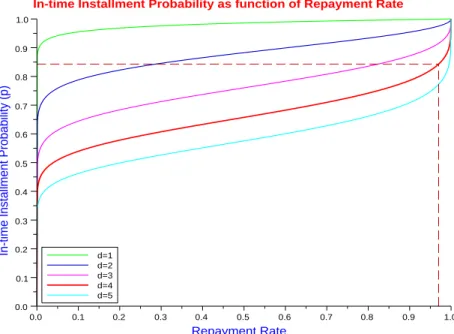

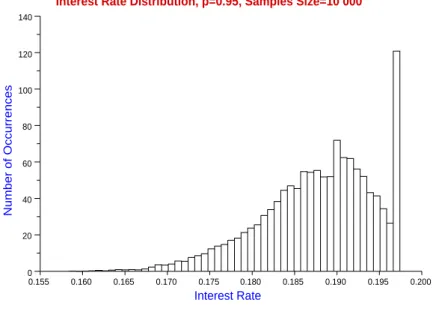

Figure

Documents relatifs

Consequently, we show that the distribution of the number of 3-cuts in a random rooted 3-connected planar triangula- tion with n + 3 vertices is asymptotically normal with mean

On va donc essayer de suivre l’évolution de la précipitation discontinue dans cette solution solide sursaturée déformée et non déformée, au cours d’un chauffage anisotherme

The light clock is a much used conceptual device to demonstrate time dilation and length contraction in in- troductory courses to special relativity (see e.g. [1]; [2] gives

elements of this potential between the original wave functions 4, are then infinite. Therefore, a matrix formulation of the Dirichlet problem with a perturb- ed boundary is

It is my feeling that, in many case studies handling numerical fuzzy data, such fuzzy data are used as intermediate summaries of complex information (but not always, as for instance

Si para Bermúdez la noción de “contenido no conceptual” se construye sobre la base de que el sujeto no posee ciertos conceptos necesarios para especificar el contenido, y si tenemos

joli (jolie), pretty mauvais (mauvaise), bad nouveau (nouvelle), new petit (petite), little vieux (vieille), old.. ordinal

It is known that the development of suffusion processes intensity of geodynamic changes of local sites of geological environment characterized by much greater performance than that