LIDS-P-2290 March 1995

Analysis of Robust H

2

Performance Using Multiplier Theory

Eric Feron*

Abstract

In this paper, the problem of determining the worst-case H2 performance of a control system subject to linear time-invariant uncertainties is considered. A set of upper bounds on the performance is derived, based on the theory of stability multipliers and the solution of an original optimal control problem. The numerical issues raised by the resulting computational problems are discussed: in particular, newly developed interior-point convex optimization methods, combined with Linear Matrix Inequalities apply very well to the fast and accurate solution of these problems. The new results compare favorably with prior ones. The method can be extended to other types of perturbations.

Keywords: H2 performance, stability multipliers, convex optimization, linear matrix inequalities.

AMS subject classification: 93B40, 93D05, 93D09, 93D10, 93D25. Abbreviated title: Analysis of robust H2 performance

Introduction

Among all performance indices known to control engineering, the H2 performance index holds a special place for historical and practical reasons. The historical reasons are that minimizing the H2 norm of a linear control system via feedback, better known as the LQG problem, is among the first optimal control problems to have been solved analytically (for an extensive presentation and bibliography, see [1]). The practical reason is that this problem can be solved using reliable and fast computational procedures [2, 21, 11].

It is however well-kn wn that the performance of the LQG-optimal controller can be very sensitive to perturbations on the nominal system [12]. In view of this fact, devising analysis and synthesis tools that will respectively evaluate and minimize worst-case H2 norms of control systems is especially relevant.

In this paper, we consider the following specific problem: given a linear control system perturbed by linear, time-invariant perturbations, what is its worst-case H2 norm? This question has remained open until recently when some attempts have been made at its solution. Packard and Doyle [27], and Bernstein and Haddad [4, 5, 6] are among the first to consider the problem of robust H2 performance in the face of dynamic and parametric uncertainty. Stoorvogel [37, 38], Petersen, Rotea and McFarlane [30, 31] find bounds on the worst-case H2 norm of a system subject to norm-bounded, noncausal, possibly nonlinear and time-varying uncertainties. Peres, Geromel and Souza [28, 29] find upper bounds on the H2 norm of linear, time-varying and uncertain LTI systems based on quadratic Lyapunov functions. The book and the papers

*Department of Aeronautics and Astronautics, Massachusetts Institute of Technology, Cambridge, MA 02139 email: feronOmit.edu fax: (617) 253-4196. This work was presented at the 33rd IEEE Conference on Decision and Control. It was supported by the Army Research Office under Grant ARO DAAL03-92-G0115 (Center for Intelligent Control Systems), NSF under Grant ECS-9409715 and the Charles Stark Draper Career Development Chair at MIT.

by Boyd, El Ghaoui, Feron, and Balakrishnan [9, 16, 7, 15] show that the computation of all these bounds on H2 performance can be reduced to convex optimization problems involving linear matrix inequalities, which can be solved via efficient convex optimization techniques. In [9, 15], attempts are made to refine the upper bounds on H2 performance when dealing with particular classes of perturbations such as static nonlinearities and parametric uncertainties, using Lur'e Lyapunov functions and causal multipliers. Other attempts at obtaining reliable upper bounds on robust H2 performance include the recent paper by Paganini, Doyle and D'Andrea [14].

In this paper, we propose to extend the results presented in [9, 15] by using noncausal multipliers to evaluate the worst-case H2 norm of linear systems perturbed by linear, time-invariant perturbations. Using noncausal multipliers is a well-known technique to determine the stability of uncertain systems (see [10, 39] and references therein), and has proven to yield effective computational procedures [36, 34]. We believe this paper is the first attempt to use them to determine robust H2-performance of linear systems subject to linear perturbations. It is organized as follows:

The first part is devoted to a few definitions and notations. In particular, we recall the notions of boundedness, positivity and passivity of operators.

In the second part, we formulate the robust H2 analysis problem and sketch our line of attack to get upper bounds on worst-case H2 performance. We present a new upper bound on robust H2 performance, based on the use of certain dynamic Lagrange multipliers.

In the third part of this paper, we present a way to compute the upper bound on robust performance using convex optimization and linear matrix inequalities. In particular, we exhibit convenient linear families of finite-dimensional multipliers to perform this computation.

In the fourth part, we discuss the obtained results: in particular, we study conditions for the obtained upper bound to be finite. We also study special cases and show they correspond to results having already appeared in the literature. A numerical example is provided that illustrates the usefulness of dynamic multipliers to determine accurate upper bounds on robust performance.

1

Notation

In this paper, R (resp. C) denotes the set of real (resp. complex) numbers. R+ denotes the set of nonnegative real numbers. Rnxp (resp. CnXP) is the vector space of n x p real (resp. complex) matrices. RnX1 (CnXl) is abbreviated R' (C'). For the random variable x, E z denotes the expected value of x. For any matrix X,

XT denotes its transpose and X* denotes its complex conjugate transposed. The identity matrix is noted I. If X is invertible, then its inverse is noted X-1. When X is not invertible, its Moore-Penrose inverse is noted Xt. When X E Rnxn, TrX denotes the trace of X. A square matrix X is said stable if all its eigenvalues lie in the open left complex half-plane. Given a set of matrices X1 E R'X', .. .,XN e RnNXPN, and defining n = EN ni, p =

Ei=Pi,

diag(X,. .. ,XN) denotes the n x p matrixX1 0 ... 0

0 X2 <' j

0 ... 0 XN

Note that the Xis need not be square. From time to time, when no ambiguity is possible, diag(X1l,..., XN) is noted diag~ =(Xi), or diagi(Xi).

For any two matrices X and Y E RnXn, the inequality X < Y means that X and Y are symmetric, and that the difference Y - X is positive. The inequality X < Y means that X and Y are symmetric, and that the difference Y - X is positive-definite.

L2(R) denotes the Hilbert space of functions h mapping R into RnXP which satisfy

J

Tr h(t)Th(t)dt <It is equipped with the standard scalar product

Vg, h E L2(R), < g, h >-

j

Trg(t)T h(t)dt,-oo

and for all h

C

L2(R), the Euclidean norm < h, h >1/2 of h is notedjlhll

2. L2(R+) denotes the subspace of L2(R) made of the functions h satisfying h(t) = 0 when t < 0. L2, denotes the space of functions h mapping R into RnXP satisfying h(t) = 0 for t < 0 andt > 0 j Th(t)Th(t)dt < oo.

Following the usage of Francis [18], we suppress the dependence of these spaces on the integers n and p. For a given operator A and a function p mapping R into R", (Ap)(t) denotes the value taken by the image function Ap at time t. An operator A is said causal if for any function p and any time t, (Ap)(t) only depends on the past values of p up to time t. It is said anticausal if (Ap)(t) only depends on the future values of p from time t. In any other case, A is said noncausal.

Given a set of operators Al, .. ., AL, diag(Al,... AL) stands for the operator which maps the function taking the value uli(t)T ... UL (t)T]Tat time t to the function taking the value [(Alul)(t)T ... (ALUL)(t)T]T

at time t.

Let H map L2(R) into L2(R) and be linear. The adjoint of H, noted H*, is the unique linear operator satisfying:

< x, Hy >=< H*x, y >, Vx, y e L2(R).

Defining s as the usual Laplace variable, the transfer function of H is noted H(s) whenever it exists. Let us now introduce the notions of finite-gain, positivity and passivity that we will use throughout this paper.

Definition 1.1 ([32]) An operator F mapping L2(R) into L2(R) has finite gain (or, equivalently, is bounded)

if there ezists a positive 6 such that for any u 6 L2,

IFuf[2 <_ 6 ll(U12

The smallest such 6 is called the gain of F and noted IIFflo.

Definition 1.2 ([101) A linear operator G mapping L2(R) into L2(R) is said positive if for any u 6 L2(R), < Gu, u. > 0.

G is said strictly positive if there ezists 6 > 0 such that for any u E L2(R), < Gu,

U

>> 6hlul22.

Definition 1.3 ([10]) A linear, causal operator G mapping L2, into L2e is said passive if for any u E L2e

and T > O0

oT(Gu)Tudt > O.

2

Problem statement and line of attack

Consider the system

-d(t) = Az(t) + Bpp(t) + Bw(t), x(0) =o,

q(t) Cz(t) + Dqpp(t), z.(t) = Cz(t),

p(t) = (Aq)(t),

where : R -+ R, p : R- Rnt ' q : R - R-n, z :R -- Rn-, and w: R - Rn!' ' and all quantities are

equal to 0 for t < 0. Assume that the matrix A is stable. A is a perturbation that satisfies the following set of assumptions: A = diag(Al,.. ., A,,), Vu L2(R), (Aiu)(t) = 6()u(tr)(t-a) dr, "0 (2)

1o

I6(r)l dr <

x,

Ai is passive , i = 1,..., np.In the literature, the passivity assumption on A is often replaced by a finite-gain assumption [13]. Standard loop-transformations allow us to move almost freely from one framework to the other (see [10, p. 215] and the end of this paper for a more detailed discussion).

Much of the existing literature is devoted to studying the robust stability of the system (1) against the uncertainty A, in the following sense: Assume w = 0 and any initial condition xo; then the signals z, p, q and z belong to L2(R+).

In this paper, we assume the system (1) to be robustlty stable, and we are interested in evaluating its worst-case H2 performance against the uncertainty A: Let

HA(s) = H,,,(s) + Hzp(s)A(s)(I - Hqp(s)A(s))-1 Hq.(s),

where

H,,(s) = C,(sI-A)-1B,, Hzp(s) = C(sI- A)-1Bp, Hqp(s) = C(sI- A)-1Bp + Dqp, Hqw(s) = Cq(s- A)-B,.

The H2 norm of the system (1) is defined as

IIHal1

2 = (2I Tr HA(j)*HA(jw) )1/2Equivalently, using Parseval's theorem, IIHll12 may also be expressed as lihAl2, where ha is the impulse matrix of Ha. In the subsequent developments of this paper, it will also be very convenient to express it as

IIHA

2 = (E Izl2) 1,/2 (4)where z is the output of the system (1) with the following assumptions: the input w is identically 0 and the initial condition x0 is equal to B, u, where u is a random variable satisfying E uuT = I. (The expectation appearing in (4) is therefore to be taken with respect to u.)

The robust H2 analysis problem is to compute the worst-case H2 norm of the system (1) over all possible values of A that satisfy (2). This computation is in general quite a complicated problem. Thus, we propose to replace it by the computation of upper bounds on robust H2 norm, using a technique similar to the classical technique of Lagrange multipliers: Consider any family M of operators M mapping L2(R) into L2(R) such that the operator M*A is positive for any A satisfying (2). The following lemma gives us an

upper bound on the worst-case H2 norm of the system (1).

Lemma 2.1 We have the inequality:

maxE III12 < min E max IIZj12 + 2 <P,Mq>, (5)

where P, q and z are the inputs and outputs of the system

dtx(t) = As(t) + BpP(t), (O) = B u,

q(t) = Cq;(t) + Dqppi(t) (6)

Z(t) = CZ(t)

where all variables belong to L2(R+), and u is a random variable satisfying E uuT = I.

Proof: Consider the system (1). For any M E M, we have < p, Mq >=< Aq, Mq >=< M*Aq,q >> 0, since M*A is positive. Therefore, for any A satisfying (2), any initial condition x: and any M E M, we have

Ilz112

< ilzl2 + 2 < p, Mq >. Since p E L2(R+), we furthermore haveIlz1j2 + 2 < p, Mq >< max 112 + 2 < P, MM >,

- fEL.(R+)

where the right-hand side of the inequality may be infinite. Taking expected values (with respect to the random variable u) on both sides of these inequalities, we conclude that

EIIzt2~ < E max

ll112

+ 2 <1, Mq >.

- E L2(R+)This ends the proof of our lemma. ·

Note that the multiplier M can indeed be seen as a Lagrange multiplier. Such an approach is not unlike the one encountered in the papers by Yakubovich [41, 17, 42] and Megretsky [22, 23, 24], where it is named S-procedure. In the remainder of this paper, we will show that a suitable choice of the family of multipliers

M allows for the right-hand side of (5) to be easily computed.

3

Upper bound computation via linear families of finite-dimensional

multipliers

3.1

Linear families of finite-dimensional operators

Following an idea arising in [8, 33, 9], we consider finite-dimensional, noncausal operators M E M, where

M = diag(M1,..., Mn,),

Mi(s) = mio+ E+ (j + w

M'

M¥j)

'-- +(-s

1+

'

M(jw)

> O, Vw E R,

mij E R, l<i< nP, O < j < N

(We refer the reader to [18] for a complete discussion of the representation of noncausal operators via transfer functions with unstable poles.) Thus, the set M is parameterized by the real numbers mij, i = 1,..., n, j =

0,..., N. Each transfer function Mi(s) may alternatively be written as Mi(s) = CMj(sI-AMj)-1BM +DMI,

where

CMi = [ Ccai Caci

'

BMi = -Baiand

--1 1 0 ... 0

0 -1 1

Acai = . ' . . 0 Aaci =Acai Acai E RNXN,

'.. -1 1 (8)

0 ... ... 0 -1

Bcai = [ O 1 ] Baci = Bcai

Ccai = [ riN "' il ], Caci =Ccai, i = 1 * ... ,

np-Likewise, the transfer function M(s) may also be written as M(s) = CM(SI - AM)-'BM + DM, with

Aca 0c

AM =

[

[

_B ]CM = [ Cca Cac ] DM = diagi(mio),

and

Aca = diagi(Acai), Aac = diagi(Aaci),

Bca = diagi(Bcai), Bac = diagi (Baci) (10)

Cca = diagi(Ccai), Cac = diagi(Caci),

i = 1,...,np.

To check M is indeed an admissible set, we must check that for any M E M and any A satisfying (2), M*A is positive. Since M*A is a diagonal operator, we just need to check that M* Ai is positive for i = 1,..., np.

From [10, p. 174], passivity of Ai is equivalent to the inequality

Ai(jw)* + Ai(jw) > 0, Vw E R. (11) By hypothesis, Mi(jw) is real and nonnegative. Thus, the inequality (11) implies

Ai(jw)*Mi(jw) + Mi(jw)Ai(jw) > O. (12) Thus, positivity of Mi*Ai holds, since by Parseval's theorem, we have

< u, M*Aiu >

- 2 u(jw)*(Ai(jw)*Mij(jw) + M(jw)Ai(jw))u(jw)dw, Vu E L2(R).

The inequality Mi(jw) + Mi(jw)* > 0 for all w E R can be expressed in a convenient form via a straightfor-ward application of Theorems 3 and 4 of Willems [40]:

Lemma 3.1 The inequality

Mi(jw) + Mi(jw)* > O, Vw E R is satisfied if and only if there ezists a symmetric matriz Pi satisfying

AMTPi + PiAMi PiBMi - CM

1

<0. (13)

BMiTPi - CM -(DMi +DM) I

Note that this lemma requires controllability of (AMi, BM;) to hold and that this assumption is indeed satisfied.

When q C L2(R+), a simple state-space representation of Mq can be given that will be useful in the subsequent developments in this paper:

Lemma 3.2 For any q E L2(R+), we can write Mq as the output of the system

d xM = AMxM + BMq, xM(0)= [ o ] T, (4)

dt

ac (14)M4 = CMZM + DMQ,

where xacO is the unique initial condition such that limt-oo ZM = 0, given by

aco

= X eA Bac(er)dr. (15)A proof of this lemma may be found in the appendix.

3.2

Upper bound computation

Having identified an appropriate family of multipliers M, we can now describe a numerical implementation of the upper bound on worst-case H2 norm given in Lemma 2.1.

We first proceed to compute E maxpEL (R+) 1[5,[2 + < P, M4 > for a given operator M, where /, q, and

z satisfy (6) and j:(0) = B,,u, where E uuT = I. Introduce the augmented system

t--(t) = AMHi(t) + BMHP(t), ( = [ (o)T o) co ] '

(Mq)(t) = CMHi(t) + DMHP(t), (16)

Z(t) = CMH, (t) where AMH, BMH, CMH, DMH, CMHz are given by

AMH =[ A BMCq H [ B qp]

AMBMCqAm BM Dqp

CMH = [ DMCq CM ], DMH = DMDqp,

CMH. = [ C O ],

and zaco is given by (15). From Lemma 3.2, computing maxpEL2(R+)

II112

+ 2 < p, Mq > is equivalent tocomputing

max

I

2(t) l

T[

c ZCMHzCMH,

[

(t

,

(17)

EL,(R+) 1o 5P(t) L CMH DMH + DTMH L (t)

where P and 2 satisfy (16). If the initial condition z(O) was constant, the solution to this quadratic optimal

control problem could be obtained by standard methods such as the ones described in [40]. Unfortunately, this is not the case, because the noncausal multiplier M is involved, which makes .(0) depend on P through the relation (15). In fact, assuming (AMH, BMH) is controllable (we will make this technical assumption from now on), Xaco spans all of RNn, as p spans all of L2(R+). Therefore, in order to compute (17) subject to the constraints (16) and (15), we propose the following 2-step strategy:

(i) Fix ,aco. Compute (17) subject to the constraints (16) and

jfo

°eA" Bac(Tr)dr = xaco.

(ii) Maximize the resulting solution over zaco E RNn,.

From Lemma 3.2, the step (i) is equivalent to computing (17) subject to the constraints (16) and limt-,o0 (t) = 0. This is a well-known problem, whose solution is given, for example, by Willems:

Lemma 3.3 ([40], Theorem 3) Assume that (AMH, BMH) is controllable. The value of (17) subject to

the constraints (16) and limt- jo 2.(t) = 0 is finite if and only if there ezists a symmetric matrix P satisfying

the matriz inequality

[ TMBHP + PAMH + C<MHZCMHZ PBM H < (18)

[MHP +CMH CMH+DMH

It is then given by i.(0)TP- .(0), where P- is the smallest (in the sense of the partial ordering of symmetric matrices) among all matrices P satisfying (18).

In particular, we see that P- is independent from the initial condition ~(0). Therefore, the step (ii) is simply done by maximizing

[T o o 0T p- [ T 0 aT ] T

over xaco. Partitioning P- as

P1l P12 P13

P-= P;2 P22 P23 ,

pGT TP2 P33

this problem is equivalent to maximizing

,(xaco) = 20 P1ixo + 2Xzo P;Xaco + Xaco P33- aco.

The function 0 is quadratic in Xaco. Thus, it has a maximum if and only if P;3- < 0 and it has a stationary point Zaco, solution to the equation P13T = -P3a32c:o. In this case, the maximum value of q is given by

X:oT (P- PP P3T):o, (19)

Assume now that xo = B,, u, where u is a random variable satisfying E uuT = I. Then

E max

IIj112 + 2 <

P,

MQ >

(20)

1EL,(R+) is finite if and only if

P33 < o,

(21)

Vu E Rn' , 3Xaco such that PT Bw = -P3Xac (21)

Then, from (19), the value of (20) is

EuTB4(P - 1P - P13PP3 3 P13 )Bu

- -T~~~~ p;- -p;3-t

~(22)

=Tr B, (Pi - PP33P/ T 3 ) Bw,,.It is possible to write the second condition in (21) in a more compact manner, by remarking that it is equivalent to the requirement that P-3 TB, lie in the range of P3-3, or, equivalently, in the nullspace of

Introducing the symmetric matrix r E Rn' xn' as a slack variable, we can also write the value of (22) together with the condition (21) as the minimum value of Tr r subject to the conditions

T (p~- _ p~- -t-T

BT(Pl- P13 p3t P3 T)Bw

<

r,P33 < 0, (23)

(I - p,3tP-3)P3T B, =0.

Using Schur complements (see [9, p. 28] for details), it is also the minimum value of Tr r subject to the single constraint

ur B T ] < 0, p iTB

B

P -3We now remark that for a general symmetric matrix P partitioned as P1 2 P13 P= PT2 P22 P23 PIT3 P2T3 P3 3 the matrix X(P) = B[ P11B B BTP1 3 PT Bw P3 3

varies monotonically with P, meaning that if P1 < P2, then X(P1) < X(P2). Therefore, given the definition of P- in Lemma 3.3, we may compute the value of E maxEL,(R+) 11j112 + 2 < P, Mq > by minimizing Tr r over the variables P and r subject to the matrix constraints (18) and

[

BTPB,,,-P B, PBr- w BTP13]<~ wl < 01U 0. (24)Pl2; BJ P3 3

Thus the value of minMEM E maxp-EL II12[ + 2 < p, Mq > is obtained by minimizing Tr

r

over the variables P, r and M G M subject to the matrix constraints (18) and (24). Remarking that M E M if andonly if the inequality (13) holds, we can now summarize the computation of the upper bound on robust H2 performance in the following Theorem:

Theorem 3.1 Consider the system (6). The quantity

min E max

I1Z112

+ 2 < p, M >,

MEM

PEL,(R+)

where z, p and q satisfy (6) is computed as the minimum of Tr r over the variables r, P, P1,..., P,, mij,

i = 1,..., np, j = 0,..., N satisfying the constraints AM.Pi + PiAMi PiBM-C

ByMiPi - CMi -(DCMi + D Ti) <0 -' ' ' P, (25)

AMHP + PAMH + CMHZCMHZ PBMH+ CTH < 0, (26) BMHP + CMH DMHDH + D(26) and [BPi Bw-y BTP1 3 < 0, (27) PTBw

]P33

where P1 1 P1 2 P13 P= P1T2 P22 P23 (28) P1T3 P2T3 P33has been partitioned conformally with the dimensions of A, Aca and A,, (where Aca and Ac are given

by (10)).

4

Discussion

In this section, we discuss the main result of this paper and compare it with some previous approaches.

4.1 Computational issues

We see that Theorem 3.1 gives us effective means to compute the upper bound on the worst-case H2 norm

of the system (1): indeed, we have to minimize the linear objective Tr r over the variables r, P, P1,..., Pno,

rnij, i = 1,..., np, j = 0,..., N, which appear linearly in the matrix constraints (25)-(27). In particular,

new interior-point convex optimization algorithms will solve this problem very efficiently [26, 9]. Note also that the size of the optimization problem grows with the dimension N of the family of multipliers used. Note finally that the solution of the optimization problem in Theorem 3.1 via interior-point methods requires that all soft inequality signs of the form < appearing in the constraints (25)-(27) be replaced by strict inequality signs. This does not present significant problems in most practical cases. (For a detailed discussion, we refer the reader to [9, § 2.5]).

4.2

When is the obtained bound finite?

Theorem 3.1 provides an upper bound for the worst-case H2 norm of the system (1). However, it does not

guarantee that this upper bounds is finite. Thus, it is interesting to examine cases for which this bound is guaranteed to be finite.

One such case arises when there exists M E M such that -MHqp is strictly positive, where Hqp is the

operator whose transfer function is given in (3). Then there exists a positive 6 such that Vp E L2(R), < p, MHqpp >< -6 < p, p >.

Define the impulse matrices

(=

CzeAtBwfor

t > 0,

h,,, (t) = 0 otherwise and ( CqeAtBw for t > 0, hq (t) 0 otherwiseThen, for any A > 0, any initial condition 3.(0) = Bu and any ii L2(R+) in the system (6), we have

IIti2 + 2Ax

<p,

Mq >= Ih,,u+ HpPjll2 + 2A <P, MHqpP + Mhqtju>

<

IIhZ,1UI11

+ 2(llh.zUI2

IIH

Ipoo

+ A

lth1uII

2IMllo)

1I112

+(llHZ~Pl2

-2x6)

II

12 Choosing A = (llRHpll11 + 1)/26, we therefore haveIIp112 + 2x < P, Mq >

<

lIhzwUII2

+2(UlhzwuII

2IIHZPII,,±

+

A

jlhqwU

IIMIL) 11P1

2-III2

•

II

~

hz.U112

ul Ih 2+ (11h..u.1

U12 2IIHzp,1oo+ A Ihqwu.

22IIMIJ.)

2•

Ilhzwul,11

+ 2(11h~UII| IIHtP1 +

A2(IhqwtUt21

IMIl2).

(Note that the quantities l[MIoo and [IHzplooK are well-defined, since the corresponding transfer functions have no poles on the imaginary axis.) Taking expected values with respect to the random variable u, we have

EmaxPEL (R+) IlII,2 + 2A < PI Mq >

< llih

ll2 +

2(Iih

l

112

IIH+zpI2

+

A2 lhqw j IIMI12).Noting that M E M implies AM E M, we conclude our upper bound is finite.

It is interesting to remark that the strict positivity of -MHqp is one of the conditions used in the classical theory of stability multipliers to prove stability of the system (1) as described in [10, p. 203]. Thus, whenever stability of the system (1) can be proved via stability multipliers, then we can provide finite bounds on its worst-case H2 performance. Note that numerical methods involving linear matrix inequalities to prove robust stability of the system (1) using linear families of finite-dimensional multipliers may be found in [3, 35].

4.3 Special cases and comparison with earlier results

In this section, we investigate what happens when considering special cases of the system (1) and of the multiplier M.

Consider first the case when the system (1) is perfectly known, that is: Bp = 0, Cq = O, Dqp = O. The optimization problem in Theorem 3.1 is solved by choosing rmj = 0 for all i and j, Pi = 0 for all i,

P-1 0 ]

P= 0 0 0

where P1 1satisfies ATP11 + P1 1A + CTCQ = 0, and r B, PB,U. P1 1 is the observability Gramian and the obtained bound is then exact.

Second, consider the case when N = 0 and np = 1, that is, when the multiplier M = mlo = m is simply a nonnegative scalar. Then, applying Theorem 3.1 leads to the computation of

min E max Jl12 + 2m < , > (29)

m>O PELL(R+)

via convex programming and linear matrix inequalities.

This special case in which scalar, memoryless multipliers are used has already appeared in the literature, for example in the papers by Stoorvogel [37, 38], although in a different format: in these papers, the problem under consideration is to compute the worst-case H2 norm of the system

d(t) = Ax(t) + Bp(t) + Bw(t), x(0) = xo,

4(t) = 6q(t) + bqpP(t), (30)

z(t) = Cz(t), when P and 4 E L2(R+) are subject to the constraint

II l2l < ll2 2I .(31)

Stoorvogel obtains an upper bound on the worst-case H2 norm for this system by relaxing the constraint (31) and by computing

minE

max

IIz112+ 2m(ll1i112

-_llp2)

(32)

m>O

PEL

2(R+)where z, P, and

4

satisfy (30), subject to the boundary conditions x(0) = Bu, w(t) = 0 and u is a randomthe scattering variables q = (P + 4)/2 and p = -(P - 4)/2. Then, following the same reasoning as in [10, p.

215], the system (30) and the constraint (31) can also be written as

dx(t) = Ax(t) + Bpp(t) + B,w(t), x(0) = xo,

q(t) = Cq(t) + Dqpp(t), (33)

z(t) = C, z(t), and

< p,q >> 0, (34) where A, Bp, Cq and Dqp are determined from A, Bp, Cq and Dqp via the relations

A = A + fBp(I- bqp)-Cq, Bp = -2B(I - bqp)-1

Cq -+ - Dp -(I bqp)(I - bqp)- .

(These relations are valid if and only if I - Dqp is invertible.) The upper bound (32) can then be written as minE max IIz12 + 2m < p,q >, (36) m>O PEL2(R+)

where z, p, and q satisfy (33), subject to the boundary conditions x(0) = B,,u, w(t) = 0 and u is a random variable satisfying E uuT = I. But then the quantity (36) is the same as our special case (29). Thus, the problem considered in [37, 38] involves perturbations that are more general than ours (since A passive and p = Aq implies < p, q >> 0 but the converse may not hold), but the resulting bounds on H2 performance are always larger than ours, because the approach taken in [37, 38] is in fact a special case of our approach.

Similar comments may be made about the results presented in [30, 9, 15, 20].

5

Example

In this section, we present an example to illustrate the developed method, and compare it with earlier results. We consider the system (1) with

-0.1 -0.1 0 0 0 0.1 0.1 0 0 0 0 0 A= 0 0 -0.2 -0.2 0 Bp= 0.1 , B = 0 0 0.1 0 0 0 0 0 0 0 -2 0.001 1 Cq= 11.98 0 0.01 0 20 ], Dqp =-12, C = 0 0 0 2 0]

and the perturbation A is any passive, linear, time-invariant and single-input, single-output system. It is easy to check (via a Nyquist plot, for example) that the transfer function -H(s) = -Cq(sI- A)-1Bp - Dqp

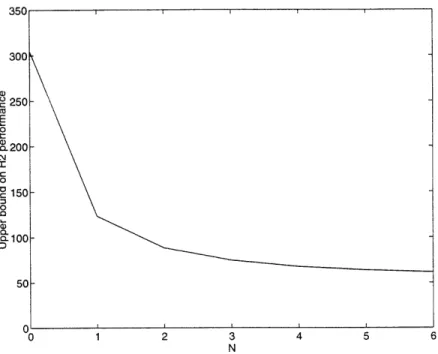

has positive dissipation, such that by application of the Passivity Theorem [10], the system (1) is stable. Using the software described in [19, 25], we have plotted the bounds on the square of its H2 norm as a function of N, (2N is the order of the noncausal multiplier which is used). Thus, N = 0 corresponds to the use of simple constant-gain, memoryless multipliers. As can be seen, the use of dynamic, noncausal multipliers improves the estimate on the square of the worst-case H2 norm by a factor of 5. Note also that the best upper bound converges to a steady state value quite fast with the size of the multiplier. This result is indeed obtained at the expense of increased computations.

350 3000 c 250 -200 i150 \ '0100-C50

1

50 0 1 2 3 4 5 6 NFigure 1: Upper bound on worst performance as a function of multiplier order

6

Conclusion and extensions

In this paper, we have considered the problem of determining an upper bound for the worst-case H2 norm of linear systems subject to linear time-invariant uncertainties, by extending the theory of stability multipliers to handle H2 performance.

We have shown this bound appears as the solution of a convex optimization problem involving linear matrix inequalities. Thus there exist algorithms that will compute it fast and accurately.

We have shown this bound is always sharper than the ones devised earlier for larger classes of uncertainties. One example shows that this improvement can be significant.

This work can be extended in many directions. For example, the theory of stability multipliers has proven to be effective not only on linear time-invariant perturbations, but also other classes of uncertainties, including memoryless, sector-bounded and monotonic nonlinearities, or constant, unknown linear gains (parametric uncertainties). Thus, this paper could be easily extended to these cases (with the restriction that H2 norms of nonlinear systems require careful definition). The set of allowable multipliers M would then be different.

Appendix: Proof of Lemma 3.2

Using inverse Fourier transforms, it is easy to show that for any q E L2(R), we have

t Oo

(Mtq)(t) =

j

CcaeAc-(t-7)Bcaj(r)dr + DMQ(t) + CaceAc(r-t)Bacr(T)dr. (37)Thus, (Mq)(t) is the sum of three parts: the first integral accounts for the causal part of H, the midterm represents a possible feedthrough term, and the second integral accounts for the anticausal part of M (this is the reason for using the subscripts 'ca' and 'ac', which stand for 'causal' and 'anticausal' respectively).

When q E L2(R+), the first integral in (37) is easily computed as rc~(t), the output of the system

dXca(t) Acazca(t) + Bcaq(t), ca(O) =0,

Tca(t) = Ccaca(t).

The second integral can be transformed the following way:

j

CaeAl(T o -t)Baci(r )drCae· A, *( t)Ba q(r)dr-/ CceA- b .. ( )Bac'(r)dr

- Cac -eAzct

j

eA.cTBacQ(ir)dr -j

e-Ac(t-T)Bac4(ir)dr]Therefore, defining

Zaco =

j

eAcBac(r)dr,

(Xaco is always defined and finite, since q E L

2(R+) and Aac is stable), the second integral term in (37) can

be written as rac(t), the output of the system

dZac(t) : -Aacxac(t)- Bac(t), Xac(O) = XacO,

rac(t) =

Cacxac(t)-Thus the expression (14) for (Mq)(t). The fact that limtO, xc,,(t) = 0 is a direct consequence of the fact

that Aca is stable; the fact that limt-oo zac(t) = 0 follows from the identity

x,(t) =

f

eAc(T-t)Bac(r)dr.Conversely, consider the system (14), and let aaco be such that limt,., xac(t) = 0. Then

sac(t)

= e-AL.ctXaO _-

e-A'(t-7)q~()dr.If limto, z,c(t) = 0, then limt-,, eA-ctXc(t) = O. Therefore, from the above equality, we must have lim

I

' eA c7q(r)dr = 2aco,which proves Xaco is indeed unique.

References

[1] B. ANDERSON AND J. B. MOORE, Optimal Control: Linear Quadratic Methods, Prentice-Hall, 1990.

[2] W. F. ARNOLD AND A. J. LAUB, Generalized eigenproblem algorithms and software for algebraic Riccati equations, Proc. IEEE, 72 (1984), pp. 1746-1754.

[3] V. BALAKRISHNAN, Y. HUANG, A. PACKARD, AND J. DOYLE, Linear matriz inequalities in analysis with multipliers, in Proc. American Control Conf., Baltimore, Maryland, June 1994, pp. 1228-1232.

[4] D. BERNSTEIN AND W. HADDAD, LQG control with an Ho performance constraint: A Riccati equation approach, in Proc. American Control Conf., 1988, pp. 796-802.

[5] -- , LQG control with an Hoo performance bound: A Riccati equation approach, IEEE Trans. Aut.

Control, AC-34 (1989), pp. 293-305.

[6] , Robust stability and performance analysis for linear dynamic systems, IEEE Trans. Aut. Control, AC-34 (1989), pp. 751-758.

[7] S. BOYD, V. BALAKRISHNAN, E. FERON, AND L. EL GHAOUI, Control system analysis and synthesis

via linear matriz inequalities, in Proc. American Control Conf., vol. 2, San Francisco, California, June

1993, pp. 2147-2154.

[8] S. BOYD AND C. BARRATT, Linear Controller Design: Limits of Performance, Prentice-Hall, 1991.

[9] S. BOYD, L. EL GHAOUI, E. FERON, AND V. BALAKRISHNAN, Linear Matriz Inequalities in System

and Control Theory, vol. 15 of SIAM Studies in Applied Mathematics, SIAM, 1994.

[10] C. A. DESOER AND M. VIDYASAGAR, Feedback Systems: Input-Output Properties, Academic Press,

New York, 1975.

[11] P. V. DOOREN, A generalized eigenvalue approach for solving Riccati equations, SIAM J. Sci. Stat. Comp., 2 (1981), pp. 121-135.

[12] J. DOYLE, Guaranteed margins for LQG regulators, IEEE Trans. Aut. Control, AC-23 (1978), pp. 756-757.

[13] -- , Analysis of feedback systems with structured uncertainties, IEE Proc., 129-D (1982), pp. 242-250.

[14] R. D. F. PAGANINI AND J. DOYLE, Behavioral approach to robustness analysis, in Proc. American

Control Conf., Baltimore, MD, 1994, pp. 2782 - 2786.

[15] E. FERON, Linear Matriz Inequalities for the Problem of Absolute Stability of Control Systems, PhD thesis, Stanford University, Stanford, CA 94305, Oct. 1993.

[16] E. FERON, V. BALAKRISHNAN, S. BOYD, AND L. EL GHAOUI, Numerical methods for H2 related problems, in Proc. American Control Conf., vol. 4, Chicago, June 1992, pp. 2921-2922.

[17] A. L. FRADKOV AND V. A. YAKUBOVICH, The S-procedure and duality relations in nonconvez problems

of quadratic programming, Vestnik Leningrad Univ. Math., 6 (1979), pp. 101-109. In Russian, 1973.

[18] B. A. FRANCIS, A course in Hoo Control Theory, vol. 88 of Lecture Notes in Control and Information Sciences, Springer-Verlag, 1987.

[19] P. GAHINET AND A. S. NEMIROVSKII, General-purpose LMI solvers with benchmarks, in Proc. IEEE

Conf. on Decision and Control, 1993, pp. 3162-3165.

[20] S. R. HALL AND J. P. How, Mized H2/p performance bounds using dissipation theory, in Proc. IEEE Conf. on Decision and Control, San Antonio, Texas, Dec. 1993.

[21] A. J. LAUB, A Schur method for solving algebraic Riccati equations, IEEE Trans. Aut. Control, AC-24 (1979), pp. 913-921.

[22] A. MEGRETSKY, S-procedure in optimal non-stochastic filtering, Technical Report TRITA/MAT-92-0015, Department of Mathematics, Royal Institute of Technology, S-100 44 Stockholm, Sweden, Mar. 1992.

[23] X, Power distribution approach in robust control, Technical Report TRITA/MAT-92-0027,

Depart-ment of Mathematics, Royal Institute of Technology, S-100 44 Stockholm, Sweden, 1992.

[24] -- , Necessary and sufficient conditions of stability: A multiloop generalization of the circle criterion, IEEE Trans. Aut. Control, AC-38 (1993), pp. 753-756.

[25] A. S. NEMIROVSKII AND P. GAHINET, The projective method for solving Linear Matrix Inequalities, in

Proc. American Control Conf., 1994, pp. 840-844.

[26] Y. NESTEROV AND A. NEMIROVSKY, Interior-point polynomial methods in convez programming, vol. 13 of Studies in Applied Mathematics, SIAM, Philadelphia, PA, 1994.

[27] A. PACKARD AND J. C. DOYLE, Robust control with an H2 performance objective, in Proc. American Control Conf., 1987, pp. 2141-2146.

[28] P. L. D. PERES AND J. C. GEROMEL, H2 control for discrete-time systems, optimality and robustness, Automatica, 29 (1993), pp. 225-228.

[29] P. L. D. PERES, S. R. SOUZA, AND J. C. GEROMEL, Optimal H2 control for uncertain systems, in Proc. American Control Conf., Chicago, June 1992.

[30] I. R. PETERSEN AND D. C. MCFARLANE, Optimal guaranteed cost control of uncertain linear systems,

in Proc. American Control Conf., Chicago, June 1992.

[31] I. R. PETERSEN, D. C. MCFARLANE, AND M. A. ROTEA, Optimal guaranteed cost control of discrete-time uncertain systems, in 12th IFAC World Congress, Sydney, Australia, July 1993, pp. 407-410.

[32] F. RIESZ AND B. Sz.-NAGY, Functional Analysis, Dover, New York, 1990.

[33] M. G. SAFONOV AND R. Y. CHIANG, Real/complez Km-synthesis without curve fitting, in Control and

Dynamic Systems, C. T. Leondes, ed., vol. 56, Academic Press, New York, 1993, pp. 303-324.

[34] M. G. SAFONOV AND P. H. LEE, A multiplier method for computing real multivariable stability margin, in IFAC World Congress, Sydney, Australia, July 1993.

[35] M. G. SAFONOV, J. LY, AND R. Y. CHIANG, On computation of multivariable stability margin using generalized Popov multiplier-LMI approach, in Proc. American Control Conf., Baltimore, June 1994.

[36] M. G. SAFONOV AND G. WYETZNER, Computer-aided stability criterion renders Popov criterion ob-solete, IEEE Trans. Aut. Control, AC-32 (1987), pp. 1128-1131.

[37] A. A. STOORVOGEL, The robust H2 problem: A worst case design, in Conference on Decision and Control, Brighton, England, Dec. 1991, pp. 194-199.

[38] -- , The robust H2 problem: A worst case design, IEEE Trans. Aut. Control, 38 (1993), pp. 1358-1370. [39] J. C. WILLEMS, The Analysis of Feedback Systems, vol. 62 of Research Monographs, MIT Press, 1969.

[40] -- , Least squares stationary optimal control and the algebraic Riccati equation, IEEE Trans. Aut.

Control, AC-16 (1971), pp. 621-634.

[41] V. A. YAKUBOVICH, The S-procedure in non-linear control theory, Vestnik Leningrad Univ. Math., 4 (1977), pp. 73-93. In Russian, 1971.

[42] X, Nonconvez optimization problem: The infinite-horizon linear-quadratic control problem with quadratic constraints, Syst. Control Letters, (1992).