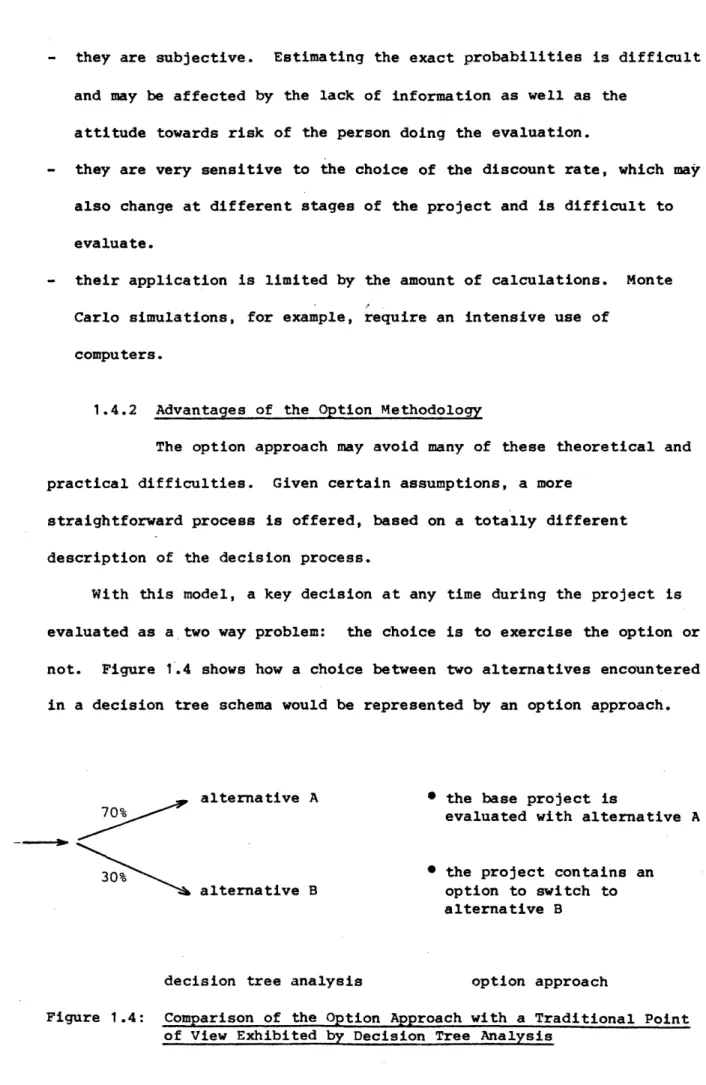

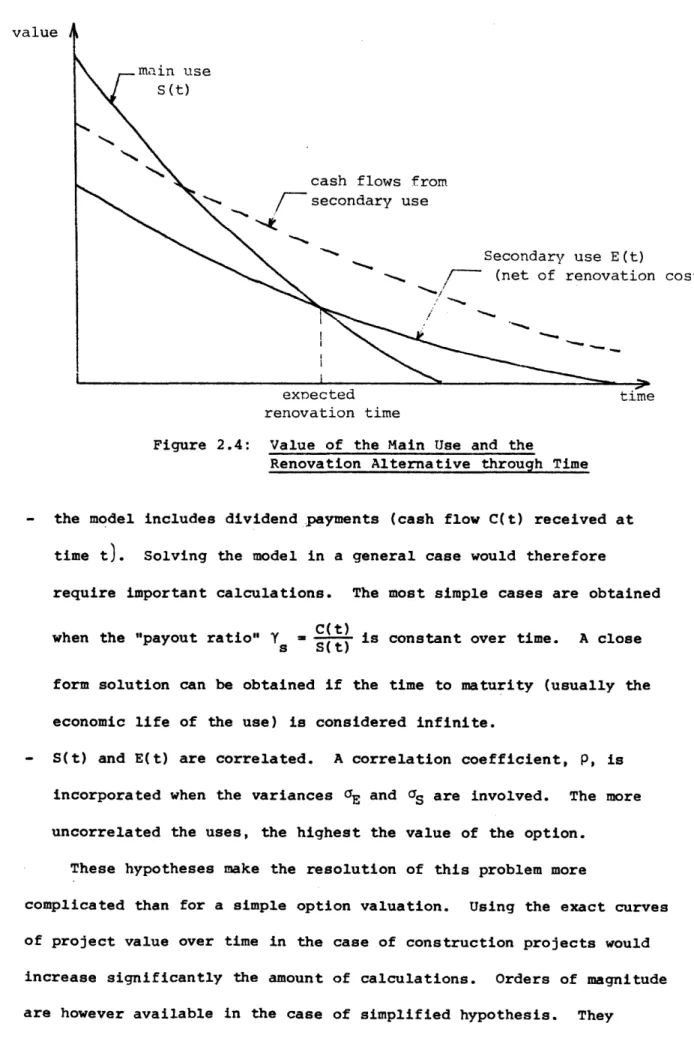

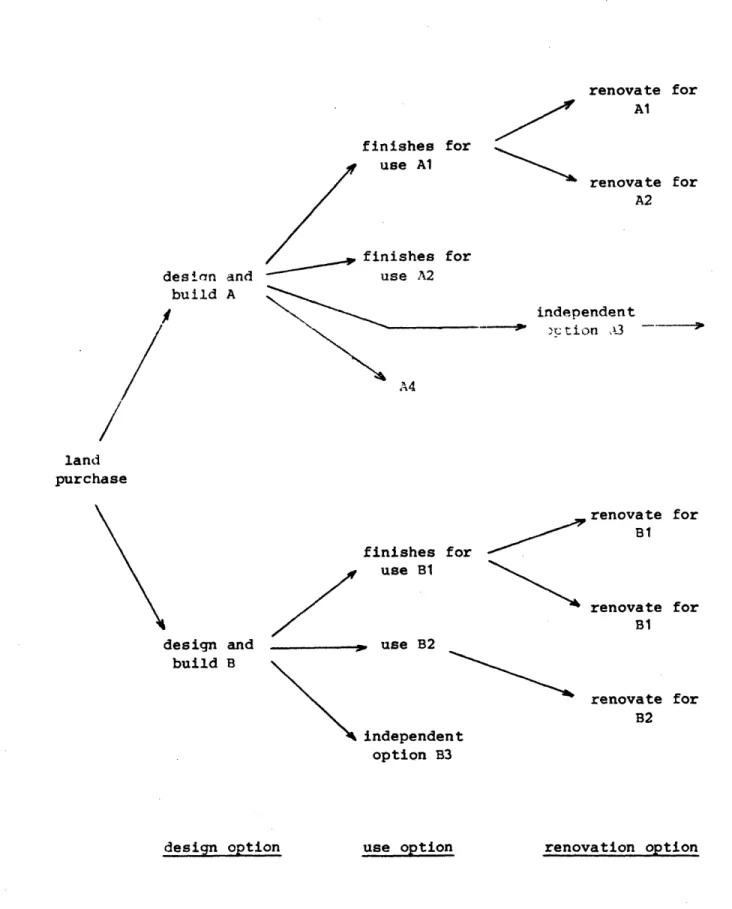

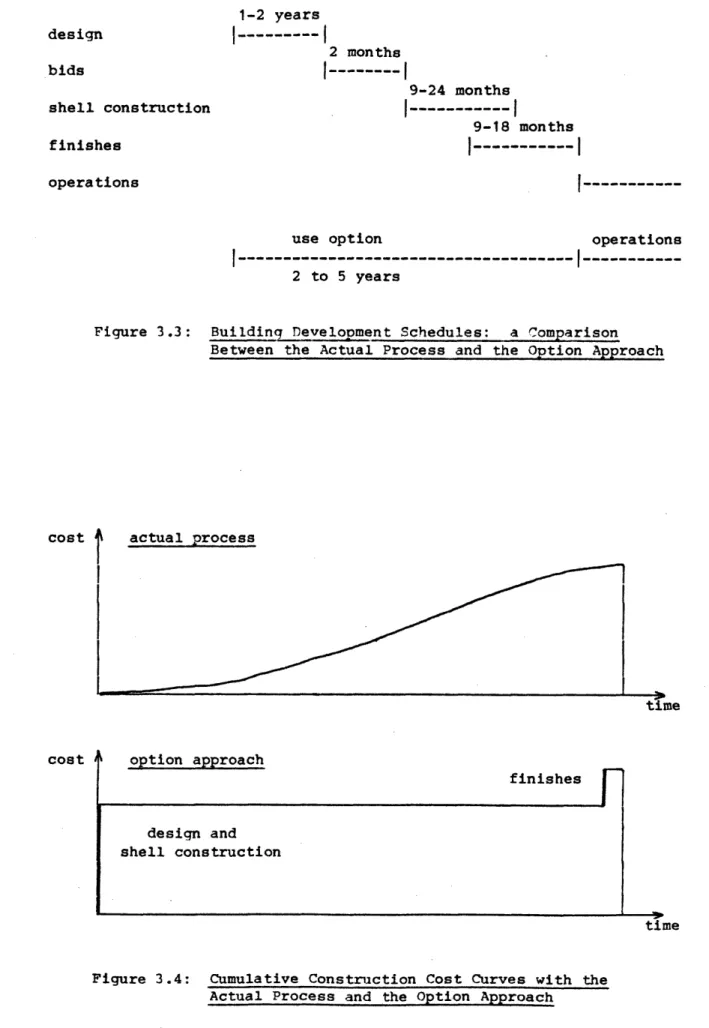

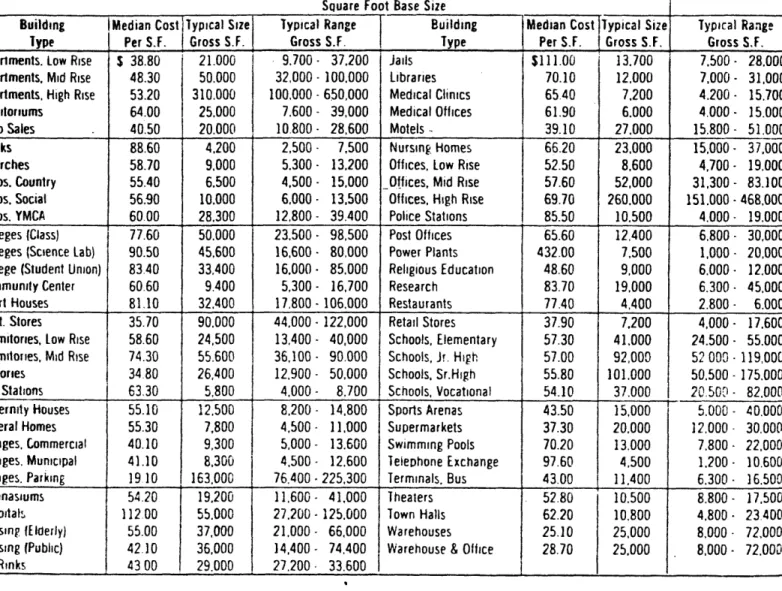

Application of the option valuation model to construction projects

Texte intégral

Figure

Documents relatifs

By using the targeted intergenic region, the aim of this study was to develop an assay to discriminate the live attenuated Romanian and Yugoslavian RM/65 SPP vaccines strains

The annexation of Crimea, the intervention in Ukraine crisis, and Putin’s meddling in the US election are what makes the current relations between them worse.. These

Ainsi, nous pouvons tenir compte de l’analyse faite à propos des compétences sociales qui semblent aboutir à la même conclusion : à savoir que la taille et la

L’archive ouverte pluridisciplinaire HAL, est destinée au dépôt et à la diffusion de documents scientifiques de niveau recherche, publiés ou non, émanant des

[24] find three types of cloud compu- ting customers based on their preference for different billing models (pay-per-use, flat rate and one-time), which provides an opportunity

Managers’ Compensation consultants justify executive behaviour optimizes value creation pay CEOs control the board in charge of their and/or shareholder wealth remuneration..

Std dev of simulated Niño 3 SSTA (K) using the ZC model background state (ZC CTR); the annual mean anomaly of the CCSM2 waterhosing experiment of wind, ther- mocline, and SST

We present an historical review on radio observations of comets, focusing on the results from our group, and including recent observations with the Nançay radio telescope, the