IDisruption

of the Group Health Insurance in light of the

Affordable Care Act - System Approach

By

Shweta Shefali

B.Tech JMI New Delhi (Electrical Engineering)

Submitted to the Faculty in partial fulfillment of the requirements for the degree of

Master of Science in Engineering and Management

at

Massachusetts Institute of Technology

[May, 2014]

© [2014] [S

wit

] AD Rights Reserved.

The author hereby grants to MIT permission to reproduce

and to distribute publicly paper and electronic

copies of this thesis document in whole or in part

in any medium now known or hereafter created.

OF TECHNOLOGY

JUN 2

6

2014

LIBRARIES

Author:

Signature redacted

[SHWETA SHEFALI]

System Design and Management ProgramSignature redacted

Certified and Accepted by:

...

Patrick Hale

Senior Lecturer, Engineering Systems Division

Director, System Design and Management Program

Page intentionally left blank. Shweta Shefali MIT SDM Thesis MIT SDM Thesis 2 2

Disruption of the Group Health Insurance in light of the

Affordable Care Act - System Approach

By

Shweta Shefali

Submitted to the System Design and Management Program on [MONTH, DAY, YEAR] in Partial

fulfillment of the Requirements for the Degree of Master of Science in Engineering and

Management.

Abstract

Our current Healthcare system has multiple problems and it is widely perceived that it is not able

to provide quality affordable healthcare to all Americans; millions of Americans are without Health

Insurance. The Affordable Care Act (ACA) was signed into law to achieve goal of 'quality

affordable care for all American'. The ACA has focus on Individual Health Insurance and the

provision of Health Exchange Marketplaces to find and purchase Health Insurance.

Disruptive Innovation is a phenomenon in which a new entrant company disrupts the existing

established company. As ACA and Health Exchanges have provided level playing field for all

companies - new entrants and established - will this lead to disruption of Healthcare?

Disruptive Innovations is analyzed from System Approach point of view. Disruption is not limited

to two companies; Disruptor System disrupts the existing system including incumbent company.

Disruption will be spearheaded by new entrant Disruptor Company and disruption will take place

at system level.

The existing Healthcare System and Possible Disruptor Systems are defined and investigated.

Relative advantage and disadvantages to these two systems with regard to ACA regulations are

analyzed. Elements of the healthcare disruptor system are analyzed and information present in

the public domain about Health Exchange enrolment after the end of first enrollment seasons is

studied to find out who could be possible disruptor and whether disruptor system formation has

started.

Thesis Supervisor: Patrick Hale

Title: Director, System Design and Management Program

Senior Lecturer, Engineering Systems Division

Shweta Shefali

Page intentionally left blank.

Shweta Shefali

Acknowledgments

It was a privilege to work on this thesis for the past three semesters. It enriched my understanding

of the healthcare industry tremendously. While pursuing my graduate studies at MIT, I realized

the importance of being able to visualize a task or situation at the macro level. For example,

viewing a three dimensional pictorial representation always provides greater results as compared

to two dimensional objects, as you are able to see it from different angles. Similarly, being able to

view the healthcare system from different perspectives by the systems thinking developed at

SDM, provided me greater clarity and enabled me to take a sure-footed holistic approach in my

analysis. The systems learnings in the SDM program with its unique analytical pedagogy

approach with lots of knowledge, discussions and analysis helped me to take an in depth

structured approach to the thesis.

I am thankful to all my batch mates, staff and professors at MIT for making the journey at SDM

so enriching and giving me an opportunity to explore and strengthen my knowledge and

capabilities.

The resources and guest lectures offered by the 15.767 course on Healthcare Delivery in the U.S:

Market & System Challenges with industry leaders and pioneers such as Richard Baum helped

me tremendously in analyzing such a complex industry with different perspectives. The wonderful

lectures and discussions of Dr Vivek Farias were enriching and stimulating.

I want to thank my thesis advisor; Pat hale for being an incredible mentor and it was a pleasure

to work with him. I enjoyed and enriched my knowledge deeply with our wonderful conversations

and discussions on the healthcare system. I appreciate his patience, excellent guidance and

providing me with a stress free nurturing atmosphere.

I express my heartfelt gratitude to my husband Himanshu for his tremendous support,

understanding and being my rock at all times, while single handedly managing his demanding job

and being a wonderful dad to our little son Suraj. I would have never been able to complete my

thesis without his support and blessings of my loving family, who have done numerous sacrifices

for me.

Last but not the least I want to thank almighty for leading me to such an opportunity in life, which

helped me grow tremendously professionally and personally and blessing me with strength and

perseverance to deliver under pressure meeting several deadlines simultaneously.

Shweta Shefali

Page intentionally left blank.

Shweta Shefali

Table of Contents

Chapter 1: Introduction...11

Chapter 2: Current Health Insurance...

13

2.1.

Elem ents of Health Insurance

...

13

2.2. Functions of Healthcare ... 14

2.3. Types of publicly financed insurance ... 15

2.4. Types of private financed insurance... 16

2.5. Types of health insurance plans... 16

2.6. Conclusion ... 18

Chapter 3: System s Thinking ... 19

3.1. Elem ents of System ... 20

3.2. System Boundary ... 20

3.3. Relationship between Entities ... 21

3.4. Health Insurance - As a System ... 21

3.5. Conclusion ... 24

Chapter 4: Affordable Care Act ... 25

4.1. The Affordable Care Act, Section by Section ... 26

4.2. O bjectives of ACA ... 29

4.3. Conclusion ... 32

Chapter 5: Affordable Care Act - System Perspective ... 33

5.1. ACA System s Perspective ... 33

5.2. ACA objectives and their effect on Healthcare System Elements... 34

5.3. Conclusion... 36

Chapter 6: Disruptive Innovation - System Perspective ... 37

6.1. Disruptive innovation... 37

6.2. Disruption - System Approach... 37 Shweta Shefali

6.3.

Disruption in Healthcare...

40

6.4.

Conclusion

...

42

Chapter 7: (Ecosystem ) Factors leading to Disruption...

43

7.1.

Health Insurance - A Big Gap...

43

7.2.

ACA - The new Beginning

...

45

7.3.

The Penalty...

46

7.4.

Health Exchange M arketplace

...

47

7.5.

G roup Health Insurance - Health Insurance of Today... 47

7.6.

Individual Health Insurance under ACA - Health Insurance of the Future

...

50

7.7.

O ld W orld Vs New W orld

...

55

7.8.

Dilem m a of Incum bents

...

55

7.9.

Advantage to New Entrants

...

58

7.10. Conclusion

...

58

Chapter 8: Health Exchange - Sustainability

...

59

8.1.

Insurance M arketplace...

59

8.2.

Sustainability of Health Exchange (HE)...

60

8.3.

How the M odel W orks...

65

8.4.

Sim ulated Cases...

66

8.5.

Conclusion

...

71

Chapter 9 Disruption of Health Insurance...

73

9.1.

Disruption - Disruptor System Elem ents... 73

9.2.

Disputed System Issues - Opportunities for Disruptor System

...

80

9.3.

Conclusion

...

85

Chapter 10: W ho Could be Possible Disruptor

...

87

10.1. Desired Q ualities needed in New Disruptor Com pany... 87

10.2. Possible Suitors

...

89

Shweta Shefali

1 0 .3 . C o n c lu s io n

...

9 2

Chapter 11: Early Trends

...

93

11.1. Provider - CVS Minute Clinic and W algreen Health Clinic

...

93

11.2. Health Exchange Marketplace

...

95

11.3. Federal Health Exchange Data (March, 2014 Release)... 97

11.4. Existing com panies...

109

11.5. Independent New Entity by Existing Insurance Provider

...

109

11.6. CO-OP Com panies

...

111

11.7. Other Com panies on Exchange

...

115

11.8. Disruptor System

...

115

1 1 .9 . C o n c lu s io n

...

1 16

Chapter 12: Challenges for Disruptor

...

117

12.1. Challenge for Disruptor System

...

117

12.2. Challenge for Disruptor System Elements...

117

12 .3 . C o n c lu s io n

...

12 0

Chapter 13: Conclusion...

121

A p p e n d ix

...

1 2 3

1.

Maxim us Cost Breakdown of MNSure...

123

2.

Heath Exchange Sustainability Vensim Model

...

126

R e fe re n c e s ...

1 2 7

T a b le o f F ig u re s ...

12 8

T a b le o f T a b le s ... ...

129

Table of Abbreviation

...

130

In d e x

...

1 3 1

Shweta Shefali MIT SDM Thesis 9Page intentionally left blank. Shweta Shefali MIT SDM Thesis MIT SDM Thesis 10 10

Chapter 1: Introduction

People use health care services for many reasons: to cure illnesses and health conditions, to mend breaks and tears, to prevent or delay future health care problems, to reduce pain and increase quality of life, and sometimes merely to obtain information about their health status and prognosis. America has witnessed incredible change in healthcare services delivery in recent past and tremendous progress has been made in the ways healthcare services are provided and delivered.

When we speak about healthcare we include providers, insurance companies, health insurance, and everyone else related with healthcare - and this makes healthcare into a complex healthcare system. We will analyze healthcare in America from a systems perspective as healthcare system.

With the recent changes and technological advancements, healthcare services have undergone an increase in cost and complexity. At the same time, the role of employer sponsored insurance and insurance companies have taken individuals and the families out of control of their healthcare. The Affordable Care Act was passed by the congress and signed into the law by president of United States on March 23, 2010 to put individuals, families, and small business owners back in control of their health care and provide affordable-high quality healthcare to all Americans.

The Affordable Care Act (ACA) aims to provide affordable and high quality health care to all Americans. The ACA's health insurance marketplaces are intended to promote price competition in the individual and small group markets through greater transparency. They will help consumers by presenting all alternatives under a single window, comparing all plans in terms of cost and value, and helping them to make an educated decision.

Will this open a window for disruption of Healthcare in America? Or, in other words, will a new healthcare system will evolve to provide affordable, effective, and quality healthcare to replace the present healthcare system?

We will try to find out answers to these questions in coming chapters. However, before we jump to these questions, we will level set our understanding about present day healthcare, healthcare system, ACA, ACA in system perspective, and Health Exchanges.

Shweta Shefali

Chapter 1: Introduction

(Page intentionally left blank for notes)

Notes:

Shweta Shefali

Chapter 2: Current Health Insurance

The health insurance is a complex system if systems with multiple stakeholders such as hospitals, clinics, patient homes, doctors (Primary care physicians and specialized doctors), and insurers; and these stakeholders interact in a nonlinear fashion. The healthcare is dynamic, exhibits emergence, and is governed by simple rules.

The main functions of healthcare system include financing, insurance, delivery of services, and payments. These functions are performed by the elements such as payer, provider, beneficiary etc. Interaction takes place among these elements while they perform the functions enumerated and information, money, and services flow from one element to others.

Let us analyze the elements of health insurance.

2.1. Elements of Health Insurance

Following are the element of Health Insurance.

Insurance Coverage

Health insurance provides coverage for medicine, visits to the doctor or emergency room, Hospital stays and other medical expenses. The employee pays a pre-decided monthly premium to the Insurer. The various health insurance plans differ in what they cover, deductible, and/or co-payment, of coverage, and the options for treatment available to the policyholder. The insurance company also functions as a claim processor and manages the funds to pay the providers.

Provider

Health care provider or simply Provider is a person or healthcare facility licensed, certified or otherwise authorized or permitted by the law of the state to administer health care or dispense medication in the ordinary course of business or practice of a profession. In general terminology, provider includes the physician, specialist, hospital, nurse etc. who provide healthcare to beneficiaries.

Payer

In simplest words, in the healthcare industry, the payer is an insurance company authorized to provide health insurance in the state. The payer is also responsible for handling claims for healthcare services, collecting premiums from clients, and paying claims to healthcare providers. Sometimes words Insurer or Insurance Company and Payer are used interchangeably and denote the same entity - the payer. In the subsequent chapters, the term Insurer or Insurance Company is used to denote the payer.

Shweta Shefali

Chapter 2: Current Health Insurance

Health Insurance Plan or 'Product'

Healthcare Plan is the product of Insurance Company that offers in the market. Health care plans are programs to which people pay premiums to protect against high health care expenses in the future. There are multiple types of health care plans, though a person will be limited by which plan their employer or the government offers.

Employer

Employer is a person or entity that hires individuals - a person, business, or organization that hires and pays one or more workers - and in healthcare context, an employer is a person or business that pays for an employer sponsored group healthcare plan. The employer enters into a contract with the Payer (Health insurance Company) and is responsible to pay the premiums.

Beneficiary

The Beneficiary is an individual who is benefited by the health insurance contract by receiving care and medical services / products. For group insurance, the beneficiary is either an employee or his /

her family members. Though the beneficiary is not a party who signs the contract in group insurance, he needs to enroll in the plan in order to receive benefits.

Regulator

The Regulator is a regulatory authority - body of statutory law and administrative regulations - that governs and regulates the healthcare and health insurance industry and those who are engaged in business of healthcare and health insurance.

2.2. Functions of Healthcare

All these elements provide following functions of healthcare.

Financing

Health care expenditures can be very expensive with all the required tests, doctor appointments and hospital stays. Financing is necessary to pay for these health care services. Financing is provided primarily through insurance and generally the health insurance is employer-based, where the employers buy health insurance for their employees from an insurance company. Dependents of employee are also often covered under this insurance.

Payments

Providers are reimbursed by the insurer for the services delivered. Each service provided has a pre-determined reimbursement for the service provided.

Insurance

Insurance is a way of protecting against financial risk. One pays small, fixed amounts in order to protect oneself from having to pay a much larger amount in the event of an economic loss. An Shweta Shefali

Chapter 2: Current Health Insurance

individual who is protected against the risk, is called the insured and the organization that assumes the risk is called the insurer. Health insurance pays specific benefits if an insured person becomes ill or is injured. A health insurance policy is a contract between an insurance company and individual.

Delivery of Services

Services are delivered to the beneficiary by healthcare provider. These services are in form medical services and medical care.

There are two types of insurance coverage in the market - Public Financed Insurance and Private Financed Insurance. Public Financed Insurance is the insurance that is funded by government using taxpayers' money. There are strict eligibility criteria to qualify for this type of insurance. Privately Funded Insurance is available to all who can afford it.

2.3. Types of publicly financed insurance

The government has played a key role in expanding healthcare services to those who otherwise would not be able to afford it. Public financing supports categorical programs, each designed to benefit a certain category of people e.g. Medicare and Medicaid.

Medicare

The Medicare program finances medical care for people 65 years or older, disabled individuals who are entitled to social security benefits, and people who are in end stage disease. The federal government is a payer and purchaser of healthcare benefits and various standards have been established for the participation for Medicare providers, federally qualified HMOs, and health plans for federal employees. The healthcare benefits are provided directly or through grants and are administered within the Department of Health and Human Services (HHS) by the Centers for Medicare and Medicaid Services (CMS).

Medicaid

It is a joint federal and state program providing hospital and medical expense to low-income population and certain aged and disabled individuals. The program is jointly financed by the federal and state governments. The federal government provides matching funds to the state. The Federal Matching Assistance percentage (FMAP) is between 50-83% per law. In order to deliver care to eligible recipients Medicaid contract with health plans, prepaid health plans, and primary care case managers.

SCHIP (State's Children Health Insurance Program)

SCHIP provides health assistance to uninsured, low-income household children. The program was designed to cover uninsured children in families with incomes that are modest but too high to qualify for Medicaid.

Shweta Shefali

Chapter 2: Current Health Insurance

2.4. Types of private financed insurance

Private financed insurance is financed by insurance company. Insurance company signs a non-equal value contract with premium payer to pay for beneficiary's healthcare cost. Types of private financed insurance are as below.

Group Insurance

Group insurance is the most prevalent health insurance. It is generally obtained through the employer, unions or through a professional organization. In a group, the risk is shared within a large pool of people. In most cases the group itself, rather than the individual members of the group must meet underwriting requirements. The underwriters determine whether a group of people can be expected to have a predictable loss rate.

The contract is signed between the premium payer and the insurance company. Premium payer is generally the employer and the beneficiaries are employee and their dependents.

Individual Insurance

Most professionals like the family farmer, self-employed, retirees etc., who could not obtain coverage through the employer sponsored group insurance get coverage through the individual insurance. The premiums are higher, as there is no large group to share the risk. The insurer may require an individual seeking coverage to provide proof of insurability, which consists of the applicant's current health records and the health and illness history and any activities (e.g. smoking) that affect the applicant's health.

2.5. Types of health insurance plans

There are various types of health insurance plans available in the market. Most common types of health insurance plans are as below.

Indemnity

In Indemnity or fee for service plan, a fixed cash amount is paid to the beneficiary per procedure or service. The beneficiary is examined by the provider chosen by him/her and he/she is responsible to pay the provider. As the more times an insured visits the provider, the more money the provider makes, the systemic error can be an unfortunate scenario where the provider is rewarded for an beneficiary's excessive utilization of medical services.

Managed Care Plans

Managed care plans generally provide comprehensive health services to the members, and offer financial incentives for patients to use the providers who belong to the plan. MCO's provide a range of services including preventive care and primary care services.

Shweta Shefali

Chapter 2: Current Health Insurance

Various types of managed care plans

There are many types of managed care plans in the market. Following are the most popular managed care plans.

The HMO Plan or the Health Maintenance Organization

The HMO is a healthcare entity that assumes the financial risk of healthcare as well as co-ordinates the delivery of the healthcare, providing comprehensive medical services to the enrolled members in return for a fixed monthly premium. There are federal as well as state laws to regulate the HMO's. To function, the HMO's need to obtain a license as well as they must get a license in the states in which they have been incorporated and must comply with statuary requirements for the state in which they conduct business.

The HMO delivers care to members by entering into contracts with providers to form a network. This network may contain participating physicians, hospitals and other medical ancillary service providers, delivering care in exchange for a pre-determined compensation. The monthly compensation paid to an HMO generally covers most healthcare services that members might need; no matter how often the members use the medical services. HMO's offer individual as well as group insurance plans, obtained through the employer. HMO members include employees, their dependents, and individuals. HMOs require plan members to choose a primary care physician (PCP).

The PPO Plan or the Preferred Provider Organization

PPO's combine the advantages of both indemnity and HMO health insurance plans. This model came about, as a need to expand outside the HMO provider network and provide flexibility to the consumer. There is a financial incentive for members who opt for PPO in the form of lower copayments/coinsurance and maximum limits on an in network out of pocket expense. Insurance companies own more than half of the PPO plans in the United States.

In the PPO model, the providers contract with the insurance company to accept pre-decided reduced fee for their services and agree not to bill the patients for the differences between the normal and the reduced fee. The PPO provides medical services at a lower cost than the traditional health insurance plans. As the doctors are paid for each patient visit, there may be a tendency of unnecessary doctor / patient encounters. There is no need of a PCP physician in the pan and the members can see in network as well as out of network doctors.

The POS Plan or the Point of Service Plan

The Point of Service (POS) Plan delivers healthcare services using the both HMO network and the Indemnity plan, where individuals can utilize services outside the HMO network. When the members need medical care, they choose at the point of service, if they want to go to the provider within the plan or seek medical care outside the network.

Shweta Shefali

Chapter 2: Current Health Insurance

The Exclusive Provider Organization

The EPO plan is a hybrid of the POS plan. It is a more restrictive type of preferred provider organization plan in which employees must choose the provider from a specified network of providers and hospitals. No coverage is provided for care received out of network. The objective of this plan was greater flexibility at a lower price by combining various plans.

2.6. Conclusion

Health Insurance in America is very complex, and serves a vast variety of customers. All this makes Health Insurance difficult to manage and regulate.

At the same time, health insurance cannot work in a silo; it interacts with other entities to form a system to deliver healthcare to millions of Americans.

In the next chapter, we will investigate more about healthcare system and will define healthcare system with its elements and their form and function.

Shweta Shefali

Chapter 3: Systems Thinking

Systems thinking recognizes when some entities are working as a system - individual entities are integrated together and working coherently to achieve goals or to produce desired output. A system can receive input from environment and can send outputs to environment. Entities of system must be related either directly or indirectly and a system has well defined system boundary.

As per Prof. Crawley (Prof. Crawley, 2013) definition of system 'is

"A

system is a set of elements or entities, and their relationships, whose functionality is greater

than the sum of the individual entities."

If we holistically see a system then it is more than its parts. It's similar to the figure below - individual parts of the figure do not make an inverted white triangle; however, when we see this figure as one system, we do see the white triangle - the sum of the parts, put together in a systematic way, is more than the individual parts.

Figure I - Gestalt Psychology Triangle2

1 Prof. Edward Crawley, Systems Thinking, 2013

2 Gestalt Psychology is an early school of psychology "The whole is more than the sum of its parts":

Reference - Introduction to Psychology by Morgan and King 2000: Chapter: The Science of Psychology Shweta Shefali

Chapter 3: System Thinking

In system thinking, we do not merely look at the individual elements but also about their relationship and interactions. Once a system is formed, an event in one element of the system will influence the event in another element of the system and similarly the output from system is not compounded from simple outputs of elements of the system, rather, it consists of organizations and patterns of outputs from individual elements. This organization and pattern of output makes them more meaningful than just the sum of individual elements' output.

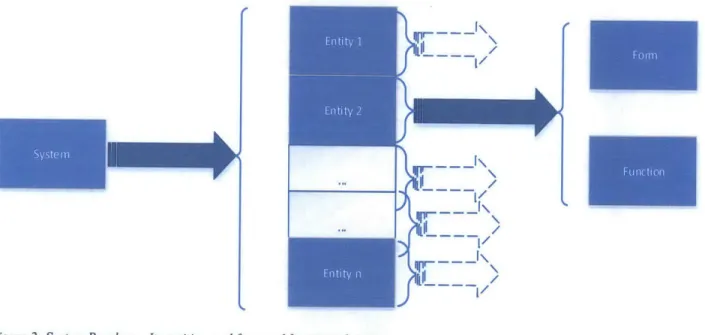

3.1. Elements of System

Systems can be divided into entities or elements and each entity has form andfunction3. These entities constitute the system and can be treated as a smaller system in themselves. All entities must be related to each other in some ways and should interact either directly or indirectly.

~iLIII

1~

/K

IF~~ \II

/qpr

II

/qp'---- ~

/L

Figure 2: System Breakup - Its entities, and form andfunction of entities

3.2. System Boundary

The system boundary defines the scope of the system - which entities, forms, and functions are part the system. Everything else is considered outside the system and we can collectively refer to it environment. A system may interact one or many other systems outside boundaries.

of

as

To study a system, system boundaries should be well defined, as system boundaries define the scope of the system and study. A system will have inputs and outputs; and all elements of system interact with the input and each other, either directly or indirectly.

3 Prof. Edward Crawley, System Thinking, 2013

Shweta Shefali

Chapter 3: System Thinking

Form

Form is what system or its entity is. This exists physically such as provider and Employer. Form is the agent which does the work or on which the work is done.

Function

Function is what system or its entities do. These may not exist physically; in health insurance, the provider - the form - (does) assumes the risk of health expense for beneficiary and pays for it. Therefore, thefunction of provider is to assume the risk of health expense for beneficiary and pay for it whenever it occurs. Similarly, function of employer is to buy group health policy for employees and pay its premium.

3.3. Relationship between Entities

Within a system, entities are related to each other - either directly or indirectly - and interact with each other - either directly or indirectly. If any entity is not related to any other entity then it may not be the part of the system. These relationships explain the organization of the system and help us in understanding how they process the input and produce output.

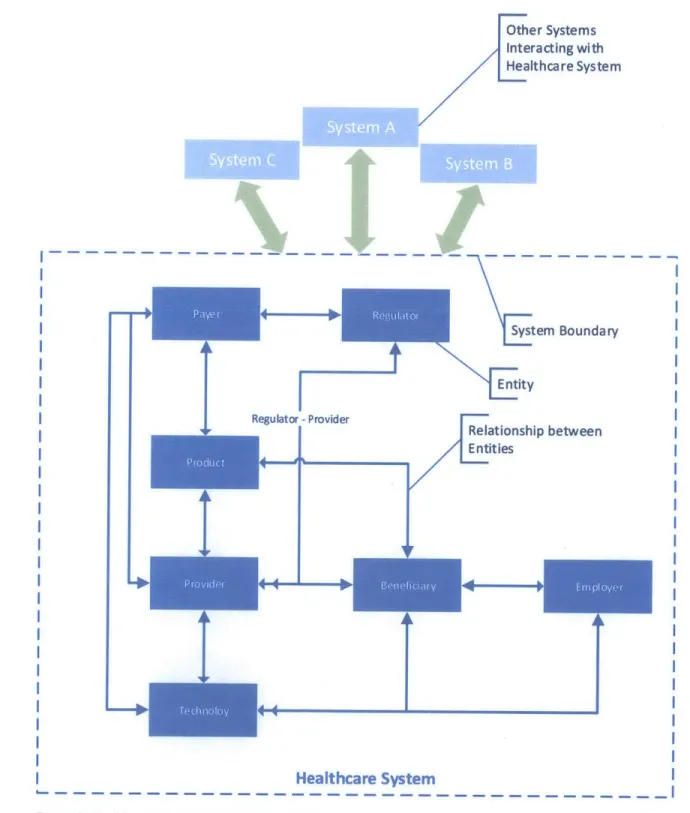

3.4. Health Insurance - As a System

Health Insurance works as a system: elements of the health insurance interact with each other to provide healthcare services to the beneficiary. Well defined relationships exist between the elements of health insurance. Using system thinking, Health Insurance or Healthcare can be explained as a system -Healthcare System.

Let us list entities of this Healthcare System in system perspective.

System boundaries, Entities, and Relationships

A pictorial representation of a Healthcare System can be seen in Figure 3. This figure puts all elements of the Healthcare System together in form of a system. It also represents relationship between entities clearly defines system boundaries. In Figure 3

Blue boxes denote the elements of the system

Pointed (single headed and double headed) arrows denote relationships among entities The outer dotted line marks the system boundary

Light blue boxes denote other systems outside the system boundary interacting with healthcare system

With System representation, in Healthcare System, as denoted in the figure

Payer, a part of the system, interacts with other parts of system such as Provider, Regulator, Product, and Technology.

Similarly, other entities in system interact with each other.

Shweta Shefali

Chapter 3: System Thinking

/ System A, System B, and System C are outside of Healthcare System boundary and interact with the Healthcare System.

Every entity represented in this system can be represented as a system in itself and can have further entities. Other Systems Interacting with Healthcare System I -System Boundary Entity Regulator -Provider Relationship between Entities I I

Healthcare System

Figure 3: Healthcare System from System PerspectiveShweta Shefali MIT SDM Thesis

I

40

Chapter 3: System Thinking

Healthcare System - Form and Function

Let us examine form and function of Healthcare System and its entities. Table 1 represents forms and

functions of the Healthcare System.

Healthcare System

The Healthcare System is Form - a physical entity - in itself and the Function of the Healthcare

System is to supply Healthcare to the beneficiary.

Payer

The Payer physically exists in Form of the Insurance Company and its Function is to collect the

premiums from the policy owner and pay the provider for healthcare services. The Payer is in the

epicenter of the system and it interacts with all other elements of the system directly.

Table 1: Healthcare System Form and Function

Provider

Form - Hospitals, clinics, medical practitioners are provider and their function is to provide Medical Services to the beneficiary.

Shweta Shefali

Chapter 3: System Thinking

Product

The Product is the insurance policy or the contract with which these entities are elements. Function of the product is to mitigate the beneficiary's medical expense risk. This risk is assumed by the payer as negotiated in the product (contract).

Employer

The Employer (Form) buys (Function) a group insurance product or policy for its employees or beneficiaries and pays (Function) the premiums.

Beneficiary

Form - Employee, dependents of the employee; Function -to receive medical healthcare services. Beneficiary is the end user of medical product and services.

Technology

When we speak about technology in context of Healthcare System, we talk about two very distinct domains of technology - Medical Technology and Information Technology - both complementary to each other in the system. Therefore, Forms of technology are medical technology and information technology.

Function - Technology provides necessary tools for Healthcare System. Medical Technology is the backbone of medical services - X-Ray, Cardiogram, CT scan, medicines, surgical instruments etc. It provides necessary medical information about patient to the medical provider.

Similarly, Information Technology integrates all entities into a system using power of computing.

Regulator

Government organizations and institutes (Form) which supervise (Function) that rules are being followed and fair practices are used. They also make (Function) new rules and regulation or amend

old ones as necessary.

3.5. Conclusion

We have defined the elements, their form and functions, and boundary of healthcare system. This healthcare system works to provide healthcare services to America in an organized manner. This healthcare system does communicate with its environment and other systems, and exchanges information. This interaction and exchange of information makes it a dynamic and open to change system.

Shweta Shefali

Chapter 4: Affordable Care Act

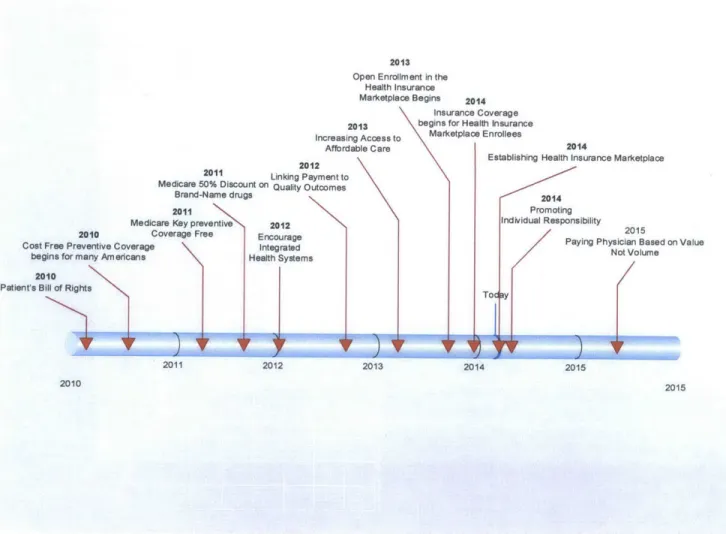

On March 23, 2010, President Obama signed the Affordable Care Act. This law puts in place comprehensive health insurance reform that will roll out over four years and beyond.

ACA aims to reform all functions of Health Care - Coverage, Cost, and Care. ACA reforms are continuous

process that started in 2010 with 'Patient's Bill of Right' and will continue in 2015 as well. The timeline below gives overview of Health Care Law over time.

The objective of Affordable Care Act (ACA) is to put consumer back in charge of his/her (and of her family)

healthcare. Under the law, a new "Patient's Bill of Rights" gives the American people the stability and

flexibility they need to make informed choices about their health.

Inc

2012

2011 Linking Paymt

Medicare 50% Discount on Quality Outco Brand-Name drugs

2011

Medicare Key preventive 2012

2010 Coverage Free Encourage

Cost Free Preventive Coverage Integrated

begins for many Americans Health Systems

2010

Patient's Bill of Rights

2011 2012 2010 reasi Afford ntto mes 2013 Open Enrollment in the

Health Insurance Marketplace Begins 2014

Insurance Coverage 2013 begins for Health Insurance

ng Access to Marketplace Enrollees

able Care 2014

Establishing Health Insurance Marketplace

v

)I

2013IF

2014 Promoting Individual Responsibility 2015Paying Physician Based on Value Not Volume

2015

2015

Figure 4: Affordable Care Act on Timeline4

4 Information for this timeline was collected from website Shweta Shefali

MIT SDM Thesis

25

Chapter 4: Affordable Care Act

4.1. The Affordable Care Act, Section by Section

The ACA is divided in 10 Titles as below. sEach Title has multiple section in it. The ACA, as presented in 2010, is a very large document running through 995 pages but these 10 titles give fair understanding about

the act and the objectives it is designed to achieve.

Title

1.

Quality, Affordable Health Care for All Americans

This Act puts individuals, families and small business owners in control of their health care. It reduces

premium costs for millions of working families and small businesses by providing hundreds of billions of dollars in tax relief - the largest middle class tax cut for health care in history. It also reduces what families will have to pay for health care by capping out of pocket expenses and requiring preventive care to be fully covered without any out of pocket expense. For Americans with insurance coverage who like what they have, they can keep it. Nothing in this act or anywhere in the bill forces anyone to change the insurance they have, period.

Americans without insurance coverage will be able to choose the insurance coverage that works best

for them in a new open, competitive insurance market - the same insurance market that every

member of Congress will be required to use for their insurance. The insurance exchange will pool buying power and give Americans new affordable choices of private insurance plans that have to

compete for their business based on cost and quality. Small business owners will not only be able to choose insurance coverage through this exchange, but will receive a new tax credit to help offset the cost of covering their employees.

It keeps insurance companies honest by setting clear rules that rein in the worst insurance industry abuses. In addition, it bans insurance companies from denying insurance coverage because of a person's pre-existing medical conditions while giving consumers new power to appeal insurance

company decisions that deny doctor ordered treatments covered by insurance.

Title II. The Role of Public Programs

The Act extends Medicaid while treating all States equally. It preserves CHIP, the successful children's insurance plan, and simplifies enrollment for individuals and families.

It enhances community-based care for Americans with disabilities and provides States with opportunities to expand home care services to people with long-term care needs.

The Act gives flexibility to States to adopt innovative strategies to improve care and the coordination of services for Medicare and Medicaid beneficiaries. And it saves taxpayer money by reducing prescription drug costs and payments to subsidize care for uninsured Americans, as more Americans gain insurance under reform.

http://www.hhs.gov/healthcare/facts/timeline/timeline-text.htm

5 Ten Titles of ACA are present at the location http://www.hhs.aov/healthcare/rights/law/index.html.

Information present in the box is the summary of information present at this source. Shweta Shefali

Chapter 4: Affordable Care Act

Title Ill. Improving the Quality and Efficiency of Health Care

The Act will protect and preserve Medicare as a commitment to America's seniors. It will save thousands of dollars in drug costs for Medicare beneficiaries by closing the coverage gap called the "donut hole." Doctors, nurses, and hospitals will be incentivized to improve care and reduce unnecessary errors that harm patients. In addition, beneficiaries in rural America will benefit as the Act enhances access to health care services in underserved areas.

The Act takes important steps to make sure that we can keep the commitment of Medicare for the next generation of seniors by ending massive overpayments to insurance companies that cost American taxpayers tens of billions of dollars per year. As the numbers of Americans without insurance falls, the Act saves taxpayer dollars by keeping people healthier before they join the program and reducing Medicare's need to pay hospitals to care for the uninsured. And to make sure that the quality of care for seniors drives all of our decisions, a group of doctors and health care experts, not Members of Congress, will be tasked with coming up with their best ideas to improve quality and reduce costs for Medicare beneficiaries.

Title IV. Prevention of Chronic Disease and Improving Public Health

The Act will promote prevention, wellness, and the public health and provides an unprecedented funding commitment to these areas. It directs the creation of a national prevention and health promotion strategy that incorporates the most effective and achievable methods to improve the health status of Americans and reduce the incidence of preventable illness and disability in the United States.

The Act empowers families by giving them tools to find the best science-based nutrition information, and it makes prevention and screenings a priority by waiving co-payments for America's seniors on

Medicare.

Title V. Health Care Workforce

The Act funds scholarships and loan repayment programs to increase the number of primary care physicians, nurses, physician assistants, mental health providers, and dentists in the areas of the country that need them most. With a comprehensive approach focusing on retention and enhanced educational opportunities, the Act combats the critical nursing shortage. And through new incentives and recruitment, the Act increases the supply of public health professionals so that the United States

is prepared for health emergencies.

The Act provides state and local government's flexibility and resources to develop health workforce recruitment strategies. In addition, it helps to expand critical and timely access to care by funding the expansion, construction, and operation of community health centers throughout the United States.

Title VI. Transparency and Program Integrity

Shweta Shefali

Chapter 4: Affordable Care Act

The Act helps patients take more control of their health care decisions by providing more information to help them make decisions that work for them. Moreover, it strengthens the doctor patient relationship by providing doctors access to innovative medical research to help them and their patients make the decisions that work best for them.

It brings greater transparency to nursing homes to help families find the right place for their loved ones and enhances training for nursing home staff so that the quality of care continuously improves. The Act promotes nursing home safety by encouraging self-corrections of errors, requiring background checks for employees who provide direct care and by encouraging innovative programs that prevent and eliminate elder abuse.

Finally, the Act reins in waste, fraud, and abuse by imposing tough new disclosure requirements to identify high-risk providers who have defrauded the American taxpayer. It gives states new authority to prevent providers who have been penalized in one state from setting up in another. In addition, it gives states flexibility to propose and test tort reforms that address several criteria, including reducing health care errors, enhancing patient safety, encouraging efficient resolution of disputes, and improving access to liability insurance.

Title VII. Improving Access to Innovative Medical Therapies

The Act promotes innovation and saves consumers money. It extends drug discounts to hospitals and communities that serve low-income patients. In addition, it creates a pathway for the creation of generic versions of biological drugs so that doctors and patients have access to effective and lower cost alternatives.

The Secretary of Health and Human Services has the authority to implement these provisions to help make medications more affordable.

Title VIll. Community Living Assistance Services and Supports Act (CLASS

Act)

The Act provides Americans with a new option to finance long-term services and care in the event of a disability.

It is a self-funded and voluntary long-term care insurance choice. Workers will pay in premiums in order to receive a daily cash benefit if they develop a disability. Need will be based on difficulty in performing basic activities such as bathing or dressing. The benefit is flexible: it could be used for a range of community support services, from respite care to home care.

No taxpayer funds will be used to pay benefits under this provision. The program will actually reduce Medicaid spending, as people are able to continue working and living in their homes and not enter nursing homes. Safeguards will be put in place to ensure its premiums are enough to cover its costs.

Title IX. Revenue Provisions

Shweta Shefali

Chapter 4: Affordable Care Act

The Act makes health care more affordable for families and small business owners by providing the

largest middle class tax cuts for health care in American history. Tens of millions of families will

benefit from new tax credits, which will help them, reduce their premium costs and purchase

insurance. Families making less than $250,000 will see their taxes cut by hundreds of billions of dollars.

When enacted, health reform is completely paid for and will reduce the deficit by more than one

hundred billion dollars in the next ten years.

Title X.

Reauthorization of the Indian Health Care Improvement Act

The Act reauthorizes the Indian Health Care Improvement Act (ICHIA), which provides health

care services to American Indians and Alaskan Natives. It will modernize the Indian health care system

and improve health care for 1.9 million American Indians and Alaska Natives.

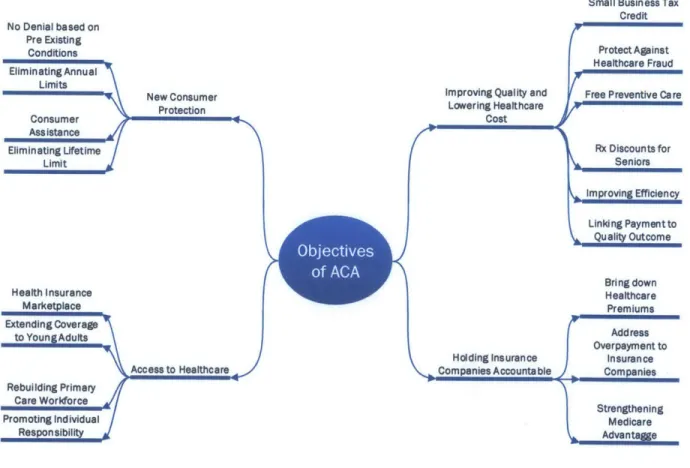

4.2. Objectives of ACA

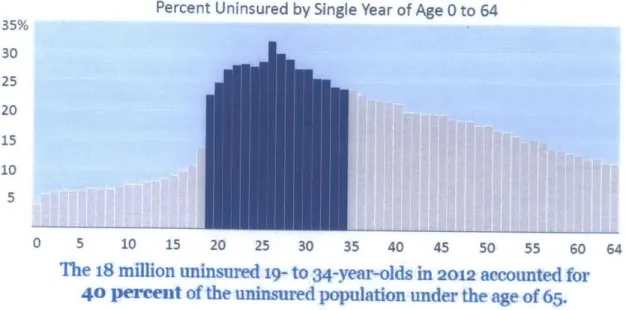

The main focus of ACA is to provide affordable healthcare to all American. Currently a large number of

American do not have health insurance coverage and a good percentage of them are young adult (See

Chapter 7 for more details)

No Denial based on Pre Existing Conditions Eliminating Annual Limits SNew Consumer ConsmerProtection Ass ista nce

Eliminating Uifetime

i

Limit Health Insurance Marketplace Extending Coverage to Young Adufts i Access to Healthcare / Rebuilding Primary Care Workforce i Promoting Individual ResponsibilityFigure 5: Objectives of Affordable Care Act

Small Business Tax

Credit

Protect Against

Healthcare Fraud

Improving Quality and Free Preventive Care

Cost reAdess ar Lowering Healthcare Rx Discounts for Seniors \Improving Efficiency Linkd ng Payment to Quality Outcome Bring down Healthcare Premiums Overpayment to Holding Insurance Insuran ce

Companies Accountable Companies

Strengthening Medicare Advanta Shweta Shefali MIT SDM Thesis

MIT SDM Thesis

2929

Chapter 4: Affordable Care Act

ACA aims to remove all hurdles between this uninsured population and the health insurance. There are

series of measures ACA has started to achieve this goal.

Most important ACA objectives are presented in the figure 5 above - they can be divided in four major

sections: Improving Quality and Lowering Healthcare Cost, New Customer Protection, Access to Healthcare, and Holding Insurance Companies Accountable.Key features of the ACA

6are given in the table below. This table is compiled from the information present

at the webpage http://www.hhs.gov/healthcare/facts/timeline/timeline-text.html. More details about

these features are present on this webpage.

Table 2: Key Features of Affordable Care Act

1 Putting Information for Consumers Online 2010

2 Prohibiting Denying Coverage of Children Based on Pre-Existing Conditions 2010

3 Prohibiting Insurance Companies from Rescinding Coverage 2010

Eliminating Lifetime Limits on Insurance Coverage

Insurance companies will be prohibited from imposing lifetime dollar limits

4 on essential benefits. 2010

5 Regulating Annual Limits on Insurance Coverage 2010

6 Appealing Insurance Company Decisions 2010

7 Establishing Consumer Assistance Programs in the States 2010

8 Prohibiting Discrimination Due to Pre-Existing Conditions or Gender 2014

Eliminating Annual Limits on Insurance Coverage

In 2014, the use of annual dollar limits on essential benefits such as hospital stays will be bannedfor new plans in the individual market and all group

9 plans. 2014

10 Ensuring Coverage for Individuals Participating in Clinical Trials 2014

1 Providing Small Business Health Insurance Tax Credits 2010 Offering Relleffor 4 Million Seniors Who Hit the Medicare Prescription

2 Drug "Donut Hole." 2010

3 Providing Free Preventive Care 2010

4 Preventing Disease and Illness 2010

5 Cracking Down on Health Care Fraud 2010

6 Offering Prescription Drug Discounts 2011

6

This information is compiled from 'Key Features of the Affordable Care Act By Year'present at location http://www.hhs.gov/healthcare/facts/timeline/timeline-text.html.

Shweta Shefali

Chapter 4: Affordable Care Act

7 Providing Free Preventive Care for Seniors

2011

8 Improving Health Care Quality and Efficiency

2011

9 Improving Care for Seniors After They Leave the Hospital

2011

10 Introducing New Innovations to Bring Down Costs

2011

11 Linking Payment to Quality Outcomes

2012

12 Encouraging Integrated Health Systems

2012

13 Reducing Paperwork and Administrative Costs

2012

14 Understanding and Fighting Health Disparities

2012

15 Improving Preventive Health Coverage

2013

16 Expanding Authority to Bundle Payments

2013

17 Making Care More Affordable

2014

18 Increasing the Small Business Tax Credit

2014

19 Paying Physicians Based on Value Not Volume

2015

Establishing the Health Insurance Marketplace

The ACA mandates establishment of Health Insurance Marketplace - a

competitive and transparent marketplace - where individuals and small

1 business can buy affrodable health insurance plans.

2014

Providing Access to Insurance for Uninsured Americans with Pre-Existing

2 Conditions

2010

Extending Coverage for Young Adults

Young adults are allowed to stay on their parents' paln until their 26th

3 birthday.

2010

4 Expanding Coverage for Early Retirees

2010

5 Rebuilding the Primary Care Workforce

2010

6 Holding Insurance Companies Accountable for Unreasonable Rate Hikes

2010

7 Allowing States to Cover More People on Medicaid

2010

8 Increasing Payments for Rural Health Care Providers

2010

9 Strengthening Community Health Centers

2010

10 Increasing Access to Services at Home and in the Community

2011

11 Providing New, Voluntary Options for Long term Care Insurance

2012

12 Increasing Medicaid Payments for Primary Care Doctors

2013

13 Open Enrollment in the Health Insurance Marketplace Begins

2013

14 Increasing Access to Medicaid

2014

15 Promotin Individual

Responsiblity

2014

1 Bringing Down Health Care Premiums 2011

Addressing Overpayments to Big Insurance Companies and Strengthening

2 Medicare Advantage

2011

Shweta Shefali

Chapter 4: Affordable Care Act

4.3. Conclusion

Affordable Care Act is an ongoing process- it has changing the face of healthcare in America and its effect will be more pronounced in the years to come. Most of its regulations are already in force and some other, such as 'Paying Physicians Based on Value Not Volume' will be implemented in 2015. One of the most significant regulation of the ACA is to setup of Health Exchange OR Health Insurance Marketplace where individuals will be able to buy Health Insurance for themselves and their family.

We will analyze the effect of ACA on Healthcare System, and its elements, in the next chapter.

Shweta Shefali

Chapter 5: Affordable Care Act - System Perspective

5.1.ACA Systems Perspective

We have seen examined elements of healthcare system in Chapter 3 and listed their form and function. With understanding of System Thinking and knowledge of Healthcare system elements, we can prepare

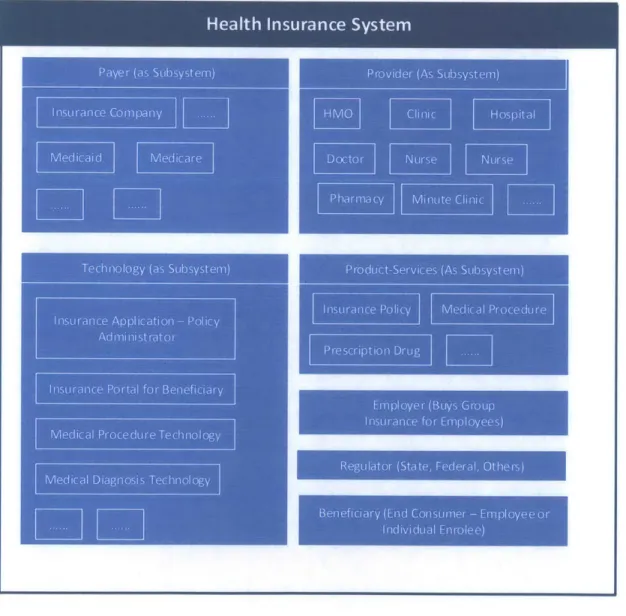

Healthcare System as shown in the in the Figure 6. In this figure, elements of the system are shown as subsystems.

Figure 6: Healthcare System with its elements as subsystem

How will ACA affect the healthcare system? - will it affect the system as a whole touching all (or majority)

of elements OR it will just touch one or two elements.

Shweta Shefali

Chapter 5: Affordable Care Act - System Perspective

If it touches all elements of the system with considerable impact then its effect on system will be far more

pronounced and it will bring some radical changes in the system.

However, if ACA just touches one element (and may be couple of other just marginally) then effects will

be localized to that element itself and ACA will not bring any radical change in the system.

If we study objectives of the ACA and what element of the system that objective would affect, it will give

us an insight into how it is affecting the healthcare system and how much impact it will have.

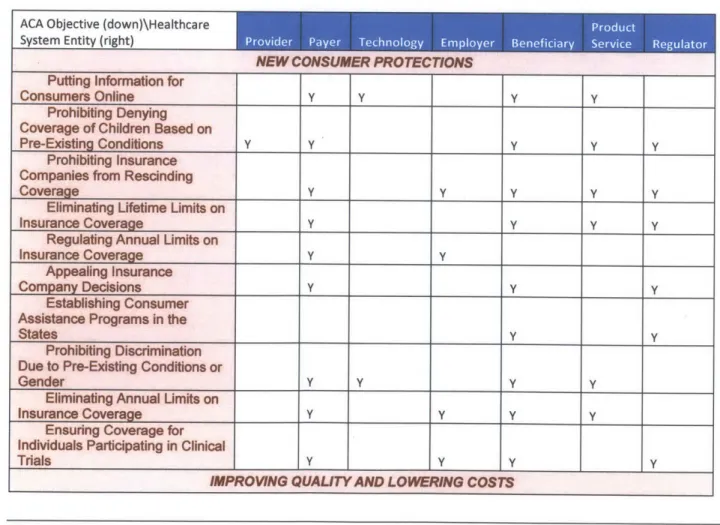

5.2.ACA objectives and their effect on Healthcare System Elements

As we have seen in Chapter 4, there are 46 major objectives of ACA grouped in four classes, most of the

objectives are already in force, and remaining will be in force soon. Each objective touches and affects

some of the elements of Healthcare System. It is not hard to find what all elements the objective will

affect and all elements the objective affects substantially can be listed.

Following table has list of all objectives taken under ACA and the element of the system they will affect.

'Y' in the box corresponding to System Entity means that this particular ACA Objective will affect the

System Entity. 'Y' is placed only when the interaction is notable and will call for changes in the entity.

Indirect interactions with little or no change are not considered for simplicity.

Table 3: ACA objectives and their effect on Healthcare System Elements

NEW CONSUMER PROT ECTIONS Puffing InformTwion for

Consumers Online y y y y

Prohibiting Denying

Coverage of Children Based on

Pre-Existing Conditions y Y y y y

Prohibiting Insurance

Companies from Rescinding

Coverage Y y y

y y

Eliminating Lifetime Limits on

Insurance Coverage y y y y

Regulating Annual Limits on

Insurance Coverage Y y

Appealing Insurance

Company Decisions Y y y

Establishing Consumer Assistance Programs in the

States y y

Prohibiting Discrimination Due to Pre-Existing Conditions or

Gender Y y y y

Eliminating Annual Limits on

Insurance Coverage y y y y

Ensuring Coverage for Individuals Participating in Clinical

Trials y Y y

y

IMPROWNG QUALITY AND LOWERING COSTS

Shweta Shefali

Chapter 5: Affordable Care Act - System Perspective

Providing Small Business

Health Insurance Tax Credits y

Offering Relief for 4 Million Seniors Who Hit the Medicare

Prescription Drug "Donut Hole." Y Y

Providing Free Preventive

Care Y Y Y

Preventing Disease and

Illness y y

Cracking Down on Health

Care Fraud Y Y Y

Offering Prescription Drug

Discounts Y Y

Providing Free Preventive

Care for Seniors Y Y Y

Improving Health Care

Quality and Efficiency Y Y Y Y

Improving Care for Seniors

After They Leave the Hospital y y y

Introducing New Innovations

to Bring Down Costs Y Y Y

Linking Payment to Quality

Outcomes Y Y Y y

Encouraging Integrated

Health Systems Y Y Y Y

Reducing Paperwork and

Administrative Costs Y Y Y Y

Understanding and Fighting

Health Disparities Y Y Y

Improving Preventive Health

Coverage Y Y

Expanding Authority to

Bundle Payments Y Y

Making Care More Affordable y y

Establishing the Health

Insurance Marketplace Y Y Y Y

Increasing the Small

Business Tax Credit Y

Paying Physicians Based on

Value Not Volume Y Y I Y

INCREASING ACCESS TO AFFORDABLE CARE

Providing Access to Insurance for Uninsured Americans with Pre-Existing

Conditions Y Y Y

Extending Coverage for

Young Adults Y Y Y

Expanding Coverage for

Early Retirees Y Y

Rebuilding the Primary Care

Workforce Y y

Holding Insurance Companies Accountable for

Unreasonable Rate Hikes Y y

Allowing States to Cover

More People on Medicaid Y y

Increasing Payments for

Rural Health Care Providers Y y

Shweta Shefali

Chapter 5: Affordable Care Act - System Perspective

Strengthening Community

Health Centers Y Y y

Increasing Access to Services at Home and in the

Community Y Y y

Providing New, Voluntary Options for Long term Care

Insurance

y Y y yincreasing Medicaid Payments for Primary Care

Doctors Y Y y

Open Enrollment in the Health Insurance Marketplace

Begins Y Y Y y y

Increasing Access to

Medicaid Y y

Promoting Individual

Responsibility _ _y y

HOLDING INSURANCE COMPANIES ACCOUNTABLE

Bringing Down Health Care

Premiums y V y Y

Addressing Overpayments to Big Insurance Companies and Strengthening Medicare

Advantage Y Y y

Score 23 19 1 10 29 13

27

The table revels that ACA will affect (is affecting) all-important elements of present Healthcare System.

Highest score of the table is 29 which is for beneficiary (end customer), which means out of 46 objectives of ACA 29 will affect customer directly and the impact is substantial. This is in line with the intent of ACA;

after all, it is aimed to remove some major pain point of the customer.

Second best (23) is scored by provider - the insurance company - and definitely, insurance company will need to accommodate major changes to fulfil objectives of ACA.

Lowest score of 10 is scored by employer, which seems logical, as they are not so active participant in healthcare system.

Other scores range between 10 and 29 means every element of healthcare system will be affected by ACA

substantially.

If all elements of the system are affected substantially, then system itself will not remain immune to the changes. The system will transform itself, although be it some trial and error, and move into the direction where ACA objectives are met more effectively.

5.3. Conclusion

All elements of Healthcare System are affected substantially and the healthcare system will see major changes due to ACA regulations. Will these changes be able to fuel disruption in healthcare system - we will examine this in coming chapters.

Shweta Shefali