Manuscript Draft

Manuscript Number:

Title: Towards a Real Time "Feature-Based Costing" for Ship Design Article Type: Original article

Keywords: Feature-Based Costing; Shipbuilding; Cost assessment; Cost; Ship Production; Cost effective design; Life cycle cost

Corresponding Author: Jean David Caprace, Ph.D. Corresponding Author's Institution: University of Liège First Author: Jean David Caprace, Ph.D.

Order of Authors: Jean David Caprace, Ph.D.;Philippe Rigo, Professor

Abstract: Cost is perhaps the most influential factor in the outcome of a product or service within many of today's industries. Cost assessment during the early stage of ship design is crucial. It influences the go, no-go decision concerning a new development. Cost assessment occurs at various stages of ship design development. Economic evaluation as early as possible, in the design phase, is therefore vital to find the best price-function compromise for the ship projects. The authors have developed a Feature-Based Costing (FBC) model for cost effectiveness measurements intended to be used by ship designers for the real time control of cost process. The outcome is that corrective actions can be taken by

management in a rather short time

Noname manuscript No. (will be inserted by the editor)

Towards a Real Time ”Feature-Based Costing” for Ship Design

J-D. Caprace · P. Rigo

Received: date / Accepted: date

Abstract Cost is perhaps the most influential factor in the outcome of a product or service within many of to-days industries. Cost assessment during the early stage of ship design is crucial. It influences the go, no-go de-cision concerning a new development. Cost assessment occurs at various stages of ship design development. Economic evaluation as early as possible, in the design phase, is therefore vital to find the best pricefunction compromise for the ship projects. The authors have de-veloped a Feature-Based Costing (FBC) model for cost effectiveness measurements intended to be used by ship designers for the real time control of cost process. The outcome is that corrective actions can be taken by man-agement in a rather short time to actually improve or overcome predicted unfavourable performance.

Keywords Feature-Based Costing · Shipbuilding · Cost assessment · Cost · Ship Production · Cost effective design · Life cycle cost

1 Introduction

Cost is perhaps the most influential factor in the out-come of a product or service within many for today’s J-D. Caprace

ANAST – University of Li`ege, 1 Chemin des chevreuils, 4000 Li`ege, Belgium

Tel.: +32-4-3669621 Fax: +32-4-3669133

E-mail: [email protected] P. Rigo

ANAST – University of Li`ege, 1 Chemin des chevreuils, 4000 Li`ege, Belgium

Tel.: +32-4-3669366 Fax: +32-4-3669133 E-mail: [email protected]

industries. More often than not, reducing cost is es-sential for survival. To compete and qualify, companies are increasingly required to improve their quality, flex-ibility, product variety, and novelty while consistently maintaining or reducing their costs, [1].

In short, customers expect higher quality at an ever-decreasing cost. Not surprisingly, cost reduction ini-tiatives are essential within todays highly competitive market place. Concurrent engineering is one of these initiatives. Since cost has become such an important factor of success, project development needs to be care-fully considered and planned. It is essential that the cost of a new project development is understood before it actually begins. It could mean the difference between success and failure.

Cost assessments during the early stages of ship devel-opment are crucial. They influence the go, no-go deci-sion concerning a new development, [1]. If an estimate is too high, it could mean the loss of a business, for the benefit of a competitor. If the estimate is too low, it could mean the company is unable to produce the ship and make a reasonable profit.

An ability to perform effective, detailed, and reliable ship cost assessment could finally create a change in the way the shipyard is able to negotiate its contracts, [2]. Moreover, the importance of a good cost assessment particularly at the early level of design can be crucial when comparing different design proposals. A greater understanding of the factors that drive costs can hope-fully lead to a decrease in cost overruns for two reasons: 1. designers will be in a better position to quickly per-form trade off studies and therefore develop a better understanding of how their designs affect cost, 2. with an ability to perform reliable cost assessments

at the preliminary level, the shipyards will be able to Click here to download Manuscript: CAPRACE_JMST.tex

negotiate more favorable contract terms that could decrease costs.

2 State of cost assessment in shipbuilding industry

The usual methods of cost assessment are various and diversified. Large volumes have been written on this subject; many books for each class of the construction industry [3–5], but very few about the shipbuilding in-dustry.

To succeed commercially, shipyards must be able to ac-curately assess costs. Cost assessment is necessary for the bid process, to change orders, and for trade-off stud-ies. Numerous cost assessment approaches exist. They can be based on extrapolations from previously-built ships, detailed parameters, or integrated physics-based analyses. The solution for the production cost assess-ment differs in the required information (input data). The less information is needed, the earlier a method can be employed in the design process. The more in-formation is used, the finer differences between design alternatives can be analysed. [6]

The methods for estimating production cost are clas-sified into:

– Top-Down (macro, cost-down or historical, weight-based) approaches (empirical, statistical and close-form equations, etc.),

– Bottom-Up (micro, cost-up or engineering analysis, process-based) approaches (direct rational assess-ment),

– Life cycle approaches (holistic, from the birth of the ship to her dead).

2.1 Top-down

The top-down approach is a parametric cost assess-ment methodology which uses empirical relationships between product parameters and costs as a means to estimate the cost of new ships [7]. In this case, the top-down method means that the ship cost is predicted from its higher level specifications, instead of its detailed de-sign which may not be available at the time of estima-tion. Parametric relationships are estimated by using statistical regression techniques from a historical cost database. A parametric estimating system can then be continuously refined and re-calibrated.

The top-down approach, also called weight based

ap-proach, determines the production cost from global

pa-rameters such as the ship type and size, weight of the

hull, the block coefficient, ship area, complexity, etc. The relationships between cost and global parameters are found by the evaluation of previous ships [8]. Thus, the top-down approach is only applicable if the consid-ered design is similar to these previous ships. Also, the cost estimation factors in the approach reflect only past practices and experience.

Cost reductions resulting from newly adopted and de-veloping shipbuilding technologies and production meth-ods can not be reflected in the existing historical based cost estimating techniques [9]. Advanced shipbuilding technologies typically involve a modular, product ori-ented approach which cuts across elements of the exist-ing Ship Work Breakdown Structures (SWBS). More-over, these weight based cost assessment approaches do not reflect improvements that may occur in the pro-duction process [10,11]. For instance, if a new welding technique is used which takes 25% less man-hours per meter of weld, no change would be reflected in cost, because there is no change in the weight of the ship. Therefore, if a change in design or production process has no impact on weight, then the cost assessment will not change.

However this approach is often used for its ease of use at the very early design stages due to the fact that it is easier to apply and obtain quicker ”results”, and does not require many design details. Weight is often used as the primary driving factor for cost assessment as it encapsulates the amount of material and to some extent the work associated with an item. Weight is an important characteristic to establish early in the design of any vessel and there are several parametric rules such as shown by [12–16], which can be used to estimate weight based on such minimal information as the main dimensions and hull form coefficients.

2.2 Bottom-up

The traditional cost assessment top-down method us-ing system-based, weight-driven cost models are not al-ways sensitive to changes in production processes and advanced manufacturing techniques [11]. Thus the need exists for a cost model which can better relate to de-sign, construction product and process issues, to enable cost conscientious decision making and more affordable ships.

The alternative method to compute the product cost is called bottom-up approach. This engineering analy-sis cost assessment approach breaks the project down

into smaller and smaller intermediate products until the most basic product (e.g. plate) is described. All costs for machining, tracking, coating, assembling this prod-uct, along with its associated intermediate products, into the next, more mature intermediate product are estimated. The estimated cost of each layer interme-diate product is summed up with all preceding layers, thus obtaining an aggregated cost which reflects an en-gineering analysis of the building process [7,8]. In fact, the bottom-up approach breaks down the project into elements of work and builds up a cost estimate in a detailed engineering analysis. [17–19], and [20,21] de-veloped simplified cost models based on direct calcula-tion using quantities and unit cost to assess the global production cost. Taking the technology of plate weld-ing as an example, there are many factors affectweld-ing the project time and working hours such as welding length, plate thickness, welding type, welding position, bevel type and welding accessibility.

The major advantage of this technique is that it specif-ically considers the actual work content of the product and provides a realistic cost estimate for the construc-tion effort.

The bottom-up approach requires more effort and detailed information than the top-down approach, but unlike the top-down approach, the bottom-up approach captures differences in design details and is thus suit-able for scantling and shape optimisations [22,23]. Chang-ing the local hull geometry influences the number of frames which require bending, the effort in plate bend-ing, and the degree of weld automation which depends on the curvature of the weld joints. All these effects are reflected by an appropriate break down of the to-tal work process into its individual components. At present, such an approach is not yet available in most shipyards; and neither are historical databases from which it could be developed. It is thus necessary to develop an appropriate approach, and collect the data required to use the approach. An advanced optimisa-tion applicaoptimisa-tion in this field is the work of [24–26] for ship structures using the LBR5 system.

2.3 Life cycle

In order to improve the design of products and reduce design changes, cost, and time to market, life cycle en-gineering has emerged as an effective approach to ad-dress these issues in today’s competitive global market. As over 70% of the total life cycle costs of a product is committed at the early design stage [27], designers can substantially reduce the Life Cycle Cost (LCC) of

products by considering the life cycle implications of their design decisions.

People are always concerned about product cost, which encompasses the entire product life from conception to disposal. Manufacturers usually only consider how to reduce the cost of materials acquisition, production, and logistics. In order to survive in the competitive mar-ket environment, manufacturers now have to consider reducing the cost of the entire life cycle of a product, called the LCC, [28]. In case of a ship, it consists of the fabrication phase in the shipyard, such as design and assembly, and a maintenance phase in service, such as inspection, repair and painting, as well as disposal costs. [29–31] have recently implemented methods for the investigation of economic and environmental costs within a marine system. The LCC assessment approach is a promising future holistic methodology in order to maintain the effectiveness of ships during their overall life. But all the authors are unanimous concerning the difficulties due to the variety of levels of production and maintenance.

3 Challenges of cost assessment

The organisation of a production control and cost con-trol system in a shipyard is not an easy task for different reasons [32].

3.1 Disconnection between decision and cost

Cost assessments are typically not available at the point when a decision needs to be made. Any cost esti-mate (be it high or low quality) is typically not available until after the part is sourced or in production. Indeed it is a well-accepted fact that 70-90% of product costs are decided in the first 20% of the product development cycle, [33–35].

3.2 Inaccuracy of the cost assessment

Cost assessments (especially early ones) often lack suf-ficient rigour and thoroughness to be used reliably in decision-making. Because historical costs lag behind the point in time for decisions to be made, the shipyard is forced to make rough estimates from the fragmented information as it can gather.

3.3 Cost evaluated only once

Once a cost assessment has been created, it typically doesn’t change or get updated as new information be-comes available. If an employee is lucky enough to be provided with a cost estimate early in the development process, this estimate is likely not included in the Enter-prise Ressource Planning (ERP) of the shipyard. There-fore, if new or better information becomes available to help the user refine the cost assessment and increase the quality of the cost number, it is an arduous process to take advantage of the new information and recalculate the cost assessment.

3.4 Multiple versions of the cost

Multiple cost assessments exist which have been cre-ated from different sources (i.e. different quantity, at different times, etc.). Because most cost assessments are generated by itinerant spreadsheets or from systems used only by cost experts and are off-line from the peo-ple that actually make the design, different costs start appearing. Sometimes this is because not everyone has received the latest quantity from the designer or they have an old version of the spreadsheet. At other times this occurs because different people in the shipyard have separate methods for calculating the same cost.

3.5 Measure of real costs

To ensure the effectiveness of any cost model, a basic requirement is that the measurement of the real cost has the same breakdown structure as the model. Within cost assessment the estimator is bound to use some

”standard” of comparison, not a fixed or immutable

standard, but nevertheless a standard, whether such a standard is the written record of actual previous costs of identical or similar products. Good estimates are made by accurate comparison with the previous costs, allow-ing for any special changes in equipment or method, and hence a good estimate becomes a standard with which to compare the actual cost when the production is completed, and thus shows any increase or reduction in the efficiency of the shipyards in respect to the par-ticular product.

3.6 Uncoupling between design and cost engineering Cost is often a secondary consideration for the engi-neers concentrating on delivering the technical aspects of a new design [36]. Indeed, cost evaluation can only

be performed once the technical details have been re-solved. Moreover, after that, it is possible to review the composition of the design. This two stage process re-sults in a degree of separation between technical and cost engineering departments working on the project and creates the situation where there may be a need for further design iterations. While these two engineering groups (design and cost engineers) operate separately there may be little opportunity to go through an opti-misation process to improve cost.

3.7 Cost assessment in early design stage - a real challenge

New production technologies and organizational im-provements in shipyards have resulted in a continuous reduction in man-hours/ton over time especially inside the dry dock. In general, the nature of the shipping business leads to situations that place an excessive dif-ficulty on effective cost estimation even for the most experienced ship cost estimator.

In most cases ship construction contracts are signed before the completion of a detailed design. The reason for this is that detailed designs with a detailed cost as-sessment are very expensive and excessively time con-suming [8]. Shipyard work in terms of work specifica-tions is difficult to formalize and predict directly from intricate detailed ship designs. This induces a very large risk to both the buyer who might end up overpaying for a ship and the seller who might have to incur exorbitant costs due to the lack of a clear definition of the work.

3.8 Specificities of the shipbuilding industry

Cost assessment and production simulation allows man-agement to predict the effectiveness of processes in the shipyard. These methods are most frequently used in industries involved in mass production. This is not the case for the European shipbuilding, which can be char-acterized by:

– small series production, – short time to market,

– many different work disciplines, – large number of different work tasks, – high complexity,

– high degree of manual work, – difficult working conditions,

– very difficult to identify and quantify work activi-ties.

Thus, with production processes more complicated, and production parameters more difficult to quantify,

production simulation and cost assessment are not as used in the shipbuilding industry as in certain other industries such as automotive industry.

3.9 Intricate control of schedules and costs

The importance of planning and control to ship con-struction is generally, if not universally, accepted. Man-agement of work is synonymous with manMan-agement of costs [32,37]. The preparing of detailed schedules for every piece of material that enters into the ship is re-quired, so as finally to ensure that the various groups or sub-assemblies of materials will arrive at the build-ing sites or at the outfittbuild-ing quay in the proper way and without any missing pieces. The first thing to remember is that the objective is to gain and keep control of the project. That is, the plan must be produced enough to be used as an actual driving force and the control sys-tem must give enough information to permit corrective action when necessary. Hierarchical planning is essen-tial. This typically gives three levels of planning, which correspond to different time horizons and levels of de-tail. Typically these will be:

– Strategic – covering all project or development with a time horizon of years

– Tactical – covering a project or development with a time horizon of months

– Operational – covering work stations with a time horizon of weeks

3.10 Cost variation factors

Worldwide competition and an increase of the costs of materials place massive pressure on shipyards to release a cost linked to design. However, capturing construction cost during the design of a new ship is one of the most difficult parts of the design process [35,2,36]. Construc-tion costs must be tracked during the design process to ensure that the project remains viable to both yard and customer particularly as late changes introduced into the design can have considerable cost impacts. The fac-tors that cost depends on are always changing and only once the production design is finalised is it possible to make a direct evaluation.

The main factors that could result in cost changes are: 1. Technology change:

– New production processes – New materials

– New designs

2. Social, economic and political situation:

– Changing workforce (productivity) – Economic downturn and unrest 3. Shipyard backwardness:

– Intense backwardness causes confusion – Few orders results in loss of skill 4. Labour rates:

– Different for each shipyard – Effect of learning

– Unpredictable changes 5. Material cost:

– Vendor base changes

– High fluctuation of steel rate 6. Regulation:

– New rules 7. Inflation:

– Fluctuates unpredictably – Different rates for each item

3.11 Increasing Costs

For the last two years, all shipbuilding costs have con-tinuously increased all over the world. These costs in-clude the cost of building materials like steel and non-ferrous metals (copper, nickel and aluminium), the cost of marine equipment and supplies and, last but not least, labour costs, [38]. In principle, most marine equip-ment markets can be considered as global with similar conditions for shipyards around the world. Neverthe-less, yards are also in some areas confronted with spe-cific local market conditions. While generally benefit-ing from a tight network of highly specialised quality producers in Europe, the example of steel plates for shipbuilding is quite illustrative of a major competitive disadvantage.

3.12 Data and DB management problems

The quality of cost assessment which requires accu-rate, reliable, repeatable and understandable results de-pends mainly on the quality of the input data. More-over, the implementation of cost assessment models nec-essarily involves the manipulation of large amounts of data from both the ship and the manufacturing en-vironment. It follows several types of problems, often very cumbersome, tedious and time consuming to solve. Here are presented the major problems that we may en-counter [39,40]:

– Lack of available data – Insufficient data definition – Inconvenient data format – Unknown validity of data

– Inaccessibility of data – Quality of the data – High quantity of data – Data integrity

– Data temporal heterogeneity

Consequently, without disciplined capture of cost data and full support for this activity from manage-ment it is very difficult for any cost assessmanage-ment process to function adequately.

3.13 Aggravating factors

Cost assessment in ship production is complicated by the fact that:

– there is insufficient cost data and the quality of this information is often quite low in these early phases – the data is usually distributed on different ERP and

CAM systems which are complicated to handle – sometimes the required cost information exists only

in printed tables, or even in the knowledge of a single expert

– the production process are changing continuously in a shipyard so that the historical cost database cannot be used for a long time

– different types of ships induce different types of cost and it is often impossible to compare their relative cost data

– the cost information always subject to high level of confidentiality and protection to avoid leakages These circumstances produce different difficulties: – Estimating and planning the ship costs takes a lot of

time for manual system queries and following cost aggregations. The pressure on time makes the as-sessment of exact and robust cost information diffi-cult.

– The possibility of cost estimating belongs to a few experts. Besides this fact, the quality of estimations, based on the knowledge of experts, differs widely (variation on average ± 30%).

– The existing database, generated from past projects, is far from being complete, due to the lack of an integrated system for managing and providing the cost information.

4 Cost estimation methods

Cost assessment occurs at various stages of ship design development. Economic evaluation as early as possible, in the design phase, is therefore crucial to find the best

pricefunction compromise for the projects or product. However, economic evaluation during the design phase is not easy. It is very different from assessment when the product/process design is complete and detailed which allows the cost of all optimisation choices to be taken into account. In the design phase, the project or prod-uct is never completely defined. It is necessary in this phase to implement rapid and more or less precise cost estimation methods (depending on available data) al-lowing the designer to select one solution in preference to another on economic grounds.

In general, cost-estimating approaches can be broadly classified as intuitive, parametric or statistical tech-niques, and analytical models. However, the most ac-curate cost estimates are made using the analytical approach. Among the many methods for cost estimat-ing, at the design stage, are those based on knowledge bases, features, operations, weight, material, physical relationships, and similarity laws [41]. In this paper we present a development based on a Feature-Based Cost-ing (FBC) method.

4.1 Feature-Based Costing (FBC)

Feature-Based Costing is a method for estimating the cost of a product based on the analysis of a series of its elementary characteristics, called product features. Products can essentially be described as a number of associated features such as holes, inner contour, outer contour, welding length, welding position, cut-outs, bevels, etc. It follows that each product feature has cost impli-cations during the product life, since the more features a product has the more manufacturing, planning and maintenance it will require. The growth of CAD/CAM technology and that of 3D modelling tools have largely influenced the development of FBC [42]. With this ap-proach, it is possible to evaluate the consequences in-cluding or exin-cluding the feature will have on the costs of a single component, but also on the system of costs of the entire life cycle of a product consisting of several components.

4.1.1 Principle and process

This approach allows the evaluation of cost from a breaking down of the required work into elementary tasks and relies on detailed engineering analysis and calculations. To apply this approach, the cost analyst needs detailed design and configuration information for system components and accounting information for all materials, equipment, and labour. This method assumes its usefulness when costing information for workshop

processes is readily available. Given sufficient design de-tail, this method can make very accurate cost estimates. However, it is very time-consuming and does require de-tailed knowledge about the product being designed and the relevant processes.

One of the prerequisites of this approach is that the product model needs to be detailed enough to allow materials and production labour to be established. This means that the structural definition, systems and equip-ment need to be defined and may rule out this approach being used in the earliest stages of design [36]. However, as ship design tools are continuously improved, it is be-coming easier to add preliminary production details at the start of the design so that production considera-tions can be incorporated in the design process. Conse-quently, this technique may be employed shortly after the initiation of a design project.

4.1.2 Strong points and drawbacks

The advantages of this approach are evident [42,43, 36]:

– a clear link between the design choices and their implications in term of cost, and as a consequence an increase of the potential capacity for correcting and optimising the design;

– easy to use compared to other approaches, by virtue of a simplification of data collection to calculate the cost of a product;

– the transverse nature of the main feature typologies and the resulting possibility of applying the method even when no similar studies exist and no previous data are available.

Other reasons for using FBC are that the same fea-tures appear in many different parts and products; there-fore, the basic cost information prepared for a class of features can be used comparatively often (for instance for welding features). Furthermore, manufacturers will have numerous past geometric data that can be related to features. Another reason developers explore whether costs should be assigned to individual design features is that it would provide the designer with a tool to vi-sualise the relation between costs, and aspects of the design that can influence the production in real time.

Moreover, this approach will capture enough details to allow the effectiveness of production processes to be evaluated and potentially optimised. In the past, ex-tracting the information from the design to perform this kind of analysis would have been very laborious

because the cost engineer would have to measure pro-duction details directly from plans. However, with mod-ern ship product modelling software, the identification of parts and junctions can be automated, providing the cost engineer with a full breakdown.

5 A Feature-Based Costing for ship design

5.1 Introduction

As shown previously, cost assessment can be frustrat-ing for shipyard personnel. Cost estimators may lack timely technical information and face data inconsisten-cies. Ship engineers and naval architects commonly lack feed-back on the cost impacts due to their technical de-cisions. Managers often lack information denoting the level of confidence in cost assessment when they must make business decisions.

Furthermore, many approaches to cost assessment are mysterious and not formally validated (each cost estimator has his own black book), complicated (too time consuming to be of use to decision makers), or diffi-cult to use, or too simplistic (based on the ship weight). Thus the typical cost estimation techniques used during early design have become increasingly inefficient and ineffective, taking days to generate cost estimates of-ten based on historical data, and that become instantly out-of-date every time a design, manufacturing or pro-curement assumption changes.

To overcome these shortcomings, we have implemented a FBC prototype by integrating all the design criteria and the production parameters. Beside the opportunity of saving time for the cost assessment itself, this tool provides the following capabilities and benefits:

– Assesses production cost for ship steel structure – Assesses cost by product and/or process

– Offers electronic imports, aggregates, and stores re-turn cost data

– Provides multiple views of cost by products or pro-cesses

– Reduces the time and increases the accuracy of de-veloping assessments of production planning by the reduction of all manual statements (risks of omis-sions, typing errors, inaccuracies, etc.)

– Identifies cost drivers and their impacts so that de-signers can design ships which are easier and less costly to build

– Provides meaningful information for production pro-cess improvement

In this application, attention will be especially devoted to estimating the cost of steel hull manufacturing. Es-timating the cost of material presents no major diffi-culty for an experienced estimator having a complete list of the required material. Therefore, the material costs have not been taken into account in the techniques presented herein.

5.2 Cost structure

A key difficulty in developing an effective approach to design for production is the selection of a common factor which links the variable parameters of design with the parameters affecting production costs. Deci-sions concerning the blocks and unit breakdown of the ship are made at a reasonably early stage in the design process. It is the first obvious stage at which informa-tion is generated by the designer considering the rele-vant production constraints. This information includes all the significant parameters in the design which might be considered as variables in a production costing and is therefore suited to modelling design variables. It is also clearly an excellent mechanism for estimating produc-tion costs since it deals with a key unit of output from the fabrication shops and the basic unit at the assem-bly stage. Thus the large majority of production costs can be directly and accurately related to the production unit and blocks itself and the details of its construction. In this paper the Cost Work Breakdown Structure (CWBS) is composed of 3 structures:

1. Ship Work Breakdown Structure (SWBS) – The modular concept technology leads to breaking down the ship into definable sub-products with a path like

Ship – Blocks – Sections – Assemblies – Sub Assem-blies – Parts. The present definition of the

hierar-chical structure containing 6 main levels has been retained for this study.

2. Hierarchical work stages – The hierarchical work stage is composed of 3 hierarchical levels (shipyard

sectors – workshops – process stages) e.g. the block

erection sector relies to the dry dock workshop. 3. Hierarchical work types – The hierarchical work type

is composed of 2 hierarchical levels following the lev-els of the hierarchical work stages (operation –

na-ture) in order to form the complete path (sectors – workshops – stages – operation – nature).

Opera-tions can be seen as basic work tasks while natures describe the type of the tasks. An operation can contain different natures e.g. the continuous weld-ing of longitudinal members consists of various kind of natures such as machining, preparation, welding, tracing, etc.

5.3 Cost Evaluation Relationships (CERs)

Eq. 1 gives the expression of the labour cost for a simple manufacturing activity e.g. the welding of two assemblies, the tacking of steel profiles, etc.

CO = CQ × CU × CK × CA × CW (1)

where CO Labour cost (man-hours),

CQ Quantity (welding length, number of brackets, etc.),

CU Unitary costs (cost-per-unit), CK Corrective coefficient used to

cali-brate the unitary costs,

CA Accessibility/Complexity coeffi-cient,

CW Workshop coefficient.

5.3.1 Basic cost relation: CQ × CU

The CER provide the basic means for assessing the cost (see equation 1). It is the formula (CQ × CU ) re-lating the cost of an item to the item’s physical or func-tional characteristics or relating the item’s cost to the cost of other items or groups of item. These relation-ships are typically developed directly from a measure-ment of a single physical attribute such as dimensional data (plate thickness, profile length, profile scantling, welding length, welding throat, etc.) or quantitative data (number of profiles, number of brackets, number of cut-outs, number of holes, etc.) for a given shipbuild-ing activity (CQ), and the unitary cost of carryshipbuild-ing out the activity (CU ). For instance:

– labour for steel block assembly at n man − h/ton, – material cost for a steel profile at n euro/m, – labour for welding in a vertical position at n h/m, – labour for block painting at n h/m2.

Usually a shipyard uses the same attributes for the same activities for each ship it builds. Then, they com-pile a database of cost-per-unit of measure for each of its different activities. This cost assessment methodol-ogy can be used to determine a variety of costs and cost-related parameters, including labour hours, mate-rial costs, overhead, weight, number of items, etc. The equation coefficient and exponent values are shipyard dependent and are linked to the shipyard production facilities, tools and equipment employed, skill levels of the work, etc.

The unitary costs (CU ) vary according to the type and the size of the structure, the manufacturing technology (manual welding, welding by robot, etc.), the experience and facilities of the construction site, the country, etc. Usually, unitary costs are defined as a function of one or more design variables like (plate thickness, welding throat, welding type (butt or fillet), welding position, bevels, profile scantling, etc.).

5.3.2 Main corrective coefficient: CK

The catalogued cost scales (cost-per-unit) available do not always accurately reflect the expected costs for the cost assessment. Therefore, we can modify these cost scales thanks to the definition of an appropriate ad-justment factor (CK). This procedure has the double advantage of preserving the cost scales for control pur-poses and allowing the impact simulation of a facility or technology investment on the cost.

This coefficient can take into account the following adjustments:

– catalogued cost-per-unit adjustments,

– production facilities improvements and productivity adjustments,

– learning effect adjustments (CL), – economic inflation adjustments (CI), – high volume business material savings, – material waste adjustments,

– etc.

5.3.3 Learning effect coefficient: CL

Modularity and increased specialization reduces aver-age construction costs as more similar ships are pro-duced. This is because ship construction labour de-creases with experience as build strategy, manufactur-ing and production strategy, and management coordi-nate their efforts with a more efficient outcome. The

learning effect or the series effect corresponds to the

re-duction in man-hours required to build successive ships in a series. This basically means that to build a first ship in a series demands more man hours than it does for the second ship of the same series, etc.

Therefore the CER used for the original ship have to be modified to take that effect into account when a series of several sister ships is constructed in sequence [2].

5.3.4 Economic inflation coefficient: CI

Costs are influenced not only by various performance factors within the shipyard, but also by factors

out-side the shipyard. Costs can be influenced by infla-tion/deflation and these effects change over time. In a free market economy, increased costs are caused by in-flation and usually occur when demand overtakes sup-ply. Decreased costs are caused by the opposite, called deflation, and are caused by supply being greater than demand.

For cost assessment purposes, costs relevant during one period of time can be used as costs relevant to an-other period in time. However, these costs need to be adjusted to reflect the economic conditions of that other time period. The increased or reduced change in cost is usually treated as a general percentage e.g. if inflation has increased by 2%, then on average, goods and ser-vices have increased in cost by the same amount.

5.3.5 Workshop productivity coefficient: CW

The productivity changes from a workshop to another. Usually shipyards wish to take account of this type of change in their costs assessments. For that purpose we use another adjustment coefficient that reflects certain gains or losses in productivity within specified shipyard activities, such as in which workshop the product is assembled. This coefficient also gives the possibility of modelling the variation of productivity due to a change of personnel.

Additional information can be obtained on the rel-ative increases in productivity that can be expected by implementation changes (modern precess equipment) in the shipyard facilities and operating practices.

5.3.6 Accessibility/Complexity coefficient: CA

This additional coefficient is introduced to adjust man-ufacturing cost assessments for an increase or a decrease in the relative accessibilities/complexities of the ship or their sub-assemblies (ship, blocks, panels, etc.). The more the structure is dense, difficult to reach and com-plex, the higher the manufacturing cost will be. The ac-cessibility/complexity coefficient should be sensitive to the level of the ship hierarchical structure. For instance, the manufacturing of steel parts for a specific ship area may not be affected by the accessibility/complexity co-efficient, but the assembly of these parts in the ship area may be affected by the accessibility coefficient, such as the engine room.

Table 1 shows typical accessibility/complexity coeffi-cients for new construction working areas of passenger ships. These coefficients are used by shipyards in or-der to take into account the added difficulties when the work is performed on board the ship. The complexity

factor should be sensitive to the level of the Ship Work Breakdown Structure (SWBS) hierarchy.

Working area Accessibility/Complexity coefficient

Inside a workshop 1

On passenger deck 1.05

Double Bottom 1.25

Superstructure 1.25

Engine or pump room 1.5

Table 1 Typical accessibility/complexity coefficient for pas-senger ship working areas [44]

5.4 Extracting the required data

The implementation of a Feature Based Costing (FBC) prototype requires a connection to the database which contains all the design parameters of the ship. Basically two solutions exist to access this kind of data.

The first solution is to access the production database (often the ERP system) which collects data related to entities and assemblies to be manufactured. This solu-tion was not adopted for the simple reason that it is too late at this time for the evaluation of the cost. Whole production parameters are fixed, freedom to move the design variables is zero so that cost analysis must be introduced during the earliest stages of the design pro-cess.

It is the reason why we have chosen the second solu-tion which consists of accessing directly the CAD/CAM tool database. The ship model is often stored inside a object oriented database. For design purposes it is the most appropriated solution because of the hierar-chical structure of the product (e.g. Scheme → Plates → Holes). Nevertheless, for general-purpose queries on the same information, pointer-based techniques will tend to be slower and more difficult to formulate than re-lational databases. In fact there is an intrinsic tension between the object encapsulation, which hides data and makes it available only through the interface methods of the CAD/CAM tool. Thus the extraction of the data from the CAD/CAM tools to a traditional relational database is required for cost assessment purposes. It is a time consuming task mainly because the extrac-tion of the data pass by the implementaextrac-tion of macro using the specific export modules of the design tools. Another drawback to accessing directly the data inside

the CAD/CAM tool is that whole shipyard data con-trols and correction procedures are skipped. Moreover some computed fields specific to the shipyard and re-quired for the production are not available.

Fig. 1 shows the implemented solution of the data ex-traction procedure used for the Feature Based Costing (FBC) prototype. The geometries and data extraction from the object oriented CAD/CAM database are trig-gered after the quality control has been done by the designer/manager. Afterwards, the computation of ad-ditional fields starting from the production rules can take place through the engine interpretation. This task is required to complete the design for production e.g. the computation of the manufacturing place of assem-blies starting from properties like weight, size, etc. Con-trol, filtering and correction of the data was also im-plemented to extract only relevant and accurate data. For instance, we avoid extracting some items like steel support, methodological entities, fictitious entities, not produced assemblies, etc. described in the model but not useful for our study. After the extraction of each section of the ship, xml messages are created and sent through the MQ series system to the CAD/CAM re-lational database. This solution allows a progressive feeding of the relational database during developments with a data follow-up during the evolution of the model i.e. data are stored at different design maturity of the project. Another interesting point is that the relational database can be fed by several sources of CAD/CAM object databases provided by various subcontractors.

CAD/CAM OBJECT DB CAD/CAM RELATIONAL DB Data Extraction Geometry Extraction MQ Series transfert (XML messages) Extraction Computation Control Creation Queues Trigger on Quality Control Rules Engine Internal Network Production Rules DB

Feature Based Costing Prototype CAD/CAM data extraction process

Fig. 1 Data extraction from the CAD/CAM object database

5.5 Computing the costs

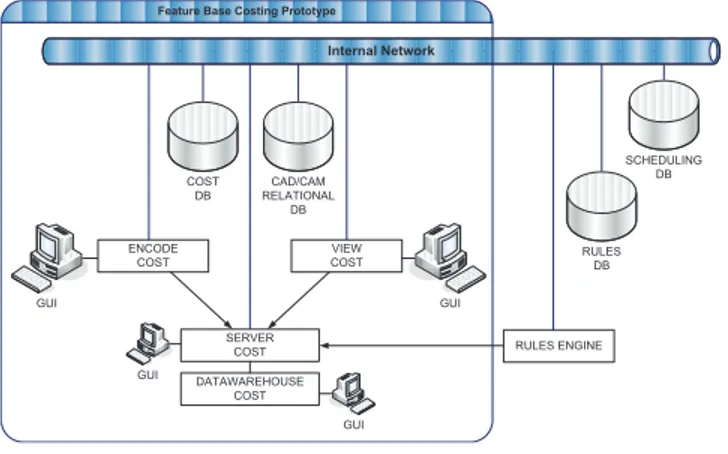

Fig. 2 shows the flow diagram of the developed proto-type. The software is built around several sub-modules and databases: an encoding module (EncodeCost ), a

computation module (ServerCost ), a graphical visual-ization module (ViewCost ), a data-warehouse module (DatawarehouseCost ), the CAD/CAM database which stores the Ship Work Breakdown Structure (SWBS) and finally the cost database storing the cost structure. The complete data which are required for the cost as-sessment as well as the results are stored in the rela-tional cost database.

RULES ENGINE VIEW COST DATAWAREHOUSE COST Internal Network CAD/CAM RELATIONAL DB GUI ENCODE COST SERVER COST COST DB RULES DB SCHEDULING DB

Feature Base Costing Prototype

GUI

GUI GUI

Fig. 2 Workflow architecture of the FBC

5.5.1 Encode Cost

This module is designed to introduce the inputs cost data. A hierarchical Work Breakdown Structure con-sistent with specified scheduling requirements has been used to define work scope and to subdivide the work into logical tasks. This structure is organised in a hierar-chical tree structure where each node is ready to return a computation cost result. The project work scope will be broken down into manageable and relatively small work task elements to facilitate the productive effort. Actual cost data are collected at the work task element level.

5.5.2 Server Cost

This module is an independent module which consults the CAD/CAM database, the cost database as well as the scheduling database and the production rules database to perform the evaluation of the cost. Within a few seconds after the geometry on a 3D ship model is altered, the cost processing module updates its assess-ment to provide an accurate product cost, allowing de-signers to investigate the cost impact of design changes much earlier in the development cycle, when changes are exponentially less expensive.

5.5.3 ViewCost

The display module collects the assessed data from the cost database and shows the results according to the user requirements.

A major innovation concerns the cost that can be calculated for any sub-assemblies of the ship, from the smallest up to the largest. The highest levels of the cost hierarchy are both the ship and the shipyard. The aggregate total of the lower level budgets linked to the ship breakdown structure and to the cost breakdown structure will be traceable to the project budget.

5.6 Utilization

Within an analysis concerning the production cost of a project, the FBC prototype can help the designer or the manager to determine the cost drivers that have the biggest influence on these costs. When the accumulated actual costs during the building of the ship are stored, the prototype could be used for a comparison between the planned and actual data with reference to different levels of the ship structure at any time of the project. Thereby, possible cost variances can be identified. So that we can assess indicators for inefficient manufac-turing, so that controlling measures can be taken to minimise the cost overrun. Cost performance is mea-sured by comparing actual costs for work performed with planned costs at the work task element level and at appropriate higher levels. Cost data and cost perfor-mance data are aggregated to upper levels of both the Cost Work Breakdown Structure (CWBS) and the Ship Work Breakdown Structure (SWBS).

The FBC prototype supports the cost analysis by a number of performance features:

– Several cost filters enable the user to deduce the different cost components separately, so that he can get an overview of the cost structure at different structural levels and the analysis will have a high relevance to the problem at hand.

– The shipbuilding structure included in the cost eval-uation prototype leads to a standardisation that en-ables cost benchmarking of even different elements of similar ships. Thereby, similarities can be sought or in-house benchmarking can be carried out. – A cost driver analysis shows the main cost focus:

after determining a cost limit by the user, the mod-ule marks those cost items on every level of the cost structure that exceed this limit cumulatively, relat-ing to the next level. For example, if the cost limit is fixed at 80%, the most expensive cost items, which

share 80% of the total cost amount of the superior level were accentuated. Thereby, the objects caus-ing the highest costs can be detected immediately at each structural level and for each building group, and looking for cost reduction opportunities will be very efficient.

5.6.1 Data-warehouse

The data-warehouse module is designed to consult the repository of the cost database and facilitate reporting and analysis. The use of several connected databases considerably enriches information which the user can obtain on each ship element. Formerly it was necessary to consult several databases. Today, the system is de-signed so that whole users can have access to the same information. Moreover, it will be possible to follow the evolution of the ship design, since the databases are gradually fed during the project. Some advance func-tions to retrieve and analyse data, to extract, trans-form and load data, and to manage the data dictionary are also implemented inside this component. One of the main objectives is to follow the cost evolution along the project time line of the project.

6 Analysis and results

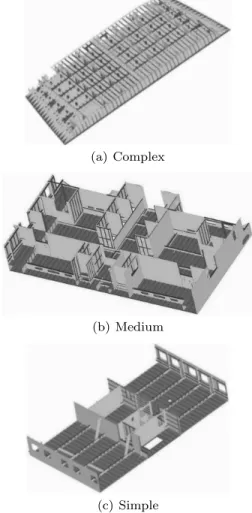

The FBC module has been validated over 37 sections of a real passenger ship vessel. These sections have been gathered according to their complexity structure as shown on Fig. 4. Moreover, Fig. 3 shows the sections considered for the validation.

Complex Medium Simple

Fig. 3 Sections selected for the validation

For each work process the number of man-hours is computed by multiplying the average man-hours per unit with the number of units for this work process. Units for a work process could be: ”number of frames and plates requiring bending”, ”welding length”, etc. The total number of necessary man-hours is then the sum of all man-hours for the individual work processes. The sum of all work processes gives the total labour cost.

Tab. 2 shows the results of the FBC calculation of the labour cost for hull production. It presents the error between the total labour cost assessed manually and automatically with the FBC module. Results show that average errors are largest for complex sections (-22.3%) than for simple ones (1.7%). A thorough investigation revealed the following points:

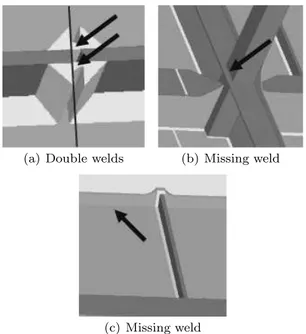

– The accuracy of welding data is not very good. Low accuracy leads to relatively large errors when the complexity of the section is large. Some welding er-rors like missing welds, bad welding position or dou-ble welds have a large impact on the cost results (see Fig. 5).

– The functional identity of steel parts and assem-blies (e.g. deck, brackets, transversal frame, pillar, etc.) is not always well defined by the designers. The main issue is that this field is not used for the same purpose in the shipyard. This may cause conflicting problems for the FBC module. For instance, the au-thor found that some brackets have been declared as transversal frames. Unfortunately, the unitary cost

(a) Complex

(b) Medium

(c) Simple

by meter length is absolutely not the same for these two functional entities which can cause serious mis-calculations.

After a manual correction of the input data, results shown in Tab. 2 highlight that the average error can be confined to below 2% whatever the level of section complexity and the maximum error can be confined to below 5%.

Average error Maximum error

Number Before After Before After

of data data data data

Section cor. cor. cor. cor.

Complex 16 -22.3% -1.6% -28% -4%

Medium 8 -9.2% -0.8% -14% 5%

Simple 13 1.7% 1.7% 3% 2%

Table 2 FBC validation results respectively before and after data correction – negative and positive means respectively below and above the average

(a) Double welds (b) Missing weld

(c) Missing weld

Fig. 5 Wrong detection of welds

7 Conclusions

Most people tend to view ship construction from a technical perspective: requirements, design, engineer-ing, analysis, production plannengineer-ing, and production. What is sometimes forgotten by engineers is the fact that ship construction is a business venture and must succeed fi-nancially as well as technically.

Cost assessment carried out for each individual opera-tion as presented in this paper takes considerable work. Moreover, the few extra people to do this work are of-ten required to gather all the data needed. Considering the extra cost of this method, it may be asked: Does it pay? According to our opinion we can answer that there is always a total net saving in every job properly planned and scheduled.

The FBC prototype provides:

– a true return-on-investment by enabling organiza-tions to identify quantifiable savings in labour while evaluating alternative designs and processes. – the ability to generate cost assessments in a limited

time period significantly speeds up the development process, because designers, manufacturing planners, and sourcing professionals never have to wait for cost information.

– elimination of the time-consuming task of providing hand calculated in house cost estimates, and releases cost experts for higher-value tasks such as finding cost reduction opportunities.

– the ability to generate cost from the first design stage, allows what-if alternative designs and engi-neering changes to occur very early in the design process, when they are exponentially less expensive to make.

– the ability to monitor productivity by the compari-son between the real cost and the planned cost. The author considers that the methods presented herein are straightforward and easy to use. The validation tests have yielded results that are consistent with the findings of the shipyards from which the designs were obtained. The time taken to make a comparative deter-mination of the effects of a change in design and its con-sequent impact on cost has been reduced. The accuracy of the cost assessment approaches a detailed engineer-ing estimate without the incurred cost and time lost to carrying out studies. It also gives ship designers a bet-ter understanding of the cost implications of the design decisions that they make and ultimately results in pro-ducing lower cost vessels. Nevertheless some additional work must be carried out to speed up the estimation process time and also to improve the accuracy of the input data.

After 20 years of high activity and good earnings, the shipbuilding and shipping industry are today facing the consequences of a world economy recession and the fi-nancial crisis. The above developments are expected to lead to a consolidation of the maritime industry and increase pressure towards sustainable development and

competitive products and services. The ability of a ship-yard to compete effectively on the increasingly compet-itive global market is influenced to a large extent by the cost as well as the quality of its ships. A wider under-standing of the methods and problems of cost assess-ment will result in clearer specifications, more econom-ical and prompt performance, and a consequent saving of time, effort, and money for both the operators of ships and the shipyards that build and repair them.

Systematic and objective analysis of cost effectiveness and complexity in ship design are important for sev-eral reasons. First, it helps design engineers to develop a better understanding of various aspects of complex-ity and thereby evolve toward simpler design solutions. Second, it enables design automation tools to system-atically evaluate different design alternatives based on their inherent complexities.

Finally, with these tools, the designers should obtain well-defined and unambiguous metrics for measurement of the different types of cost effectiveness and complex-ities in engineered artefacts. Such metrics help the de-signers and design automation tools to be objective and perform quantitative comparisons of alternative design solutions, cost estimation, as well as design optimiza-tion.

References

1. Roy, R. and Kerr, C. (2003) Cost Engineering: Why, What and how?. Cranfiel University.

2. Miroyannis, A. (2006) Estimation of Ship Construction Costs. Master’s thesis, Massachusetts Institute of Tech-nology (MIT).

3. Holm, L., Schaufelberger, J. E., Griffin, D., and Cole, T. (2004) Construction Cost Estimating: Process and Prac-tices. Prentice Hall.

4. Babbitt, C., Baker, T., Balboni, B., and Bastoni, R. A. (2009) Building Construction Cost Data. R.S. Means Company.

5. Karim, A. (2007) Construction Scheduling, Cost Opti-mization and Management. Taylor & Francis.

6. Bertram, V., Maisonneuve, J., Caprace, J., and Rigo, P. (2005) Cost Assessment in Ship Production. RINA. 7. Geiger, T. and Dilts, D. (1996) Automated

Design-to-Cost: Intagrating Costing Into the Design Decision. Computer-Aided Design.

8. Barentine, J. (1996) A Process-Based Cost Estimating Tool for Ship Structural Designs. Master’s thesis, Mas-sachusetts Institute of Technology (MIT).

9. Christiansen and Walter (1992) Self Assessement of Ad-vanced Shipbuilding Technology Implementation. NSRP Ship Production Symposium, pp. 1–19.

10. Chalmers, D. and Frina, C. (1986) Structural Design for Minimum Cost. Advances in Marine Structures.

11. Ennis, K., Dougherty, J., Lamb, T., Greenwell, C., and Zimmermann, R. (1998) Product-Oriented Design and Construction Cost Model. Journal of ship production, 14.

12. Careyette, J. (1977) Preliminary Ship Cost Estimation. RINA, pp. 235–249.

13. Kerlen, H. (1985) ber den Einflub der Vlligkeit auf die Rumpfstahlkosten von Frachtschiffen. IfS Rep. 456 . 14. Schneekluth, H. and Bertram, V. (1998) Ship Design for

Efficiency and Economy.

15. Deschamps, L. and Trumbule, J. (2004) Chapter 10 - Cost Estimation. SNAME .

16. Ross, J. and Hazen, G. (2002) Forging a Real-Time Link Between Initial Ship Design and Estimated Costs. IC-CAS 2002, pp. 75–88.

17. Southern, G. (1980) Work Content Estimating from a Ship Steelwork Data Base. RINA, 121.

18. Moe, J. and Lund, S. (1968) Cost and Weight Minimiza-tion of Structures with Special Emphasis on Longitudinal Strength Members of Tankers. RINA, 110.

19. Winkle, I. and Baird, D. (1986) Towards more Effective Structural Design through Synthesis and Optimisation of Relative Fabrication Costs. RINA, 128.

20. Rigo, P. (2001) Least Cost Structural Optimization Ori-ented Preliminary Design. Journal of Ship Production, 17.

21. Rigo, P. (2003) How to Minimize Production Costs at the Preliminary Design Stage – Scantling Optimization. Proceedings of the 8th International Marine Design Con-ference, May.

22. Caprace, J., Rigo, P., Warnotte, R., and Viol, S. L. (2006) An Analytical Cost Assessment Module for the Detailed Design Stage. COMPIT’06 .

23. Bole, M. (2006) Parametric Cost Assessment of Concept Stage Designs. COMPIT’06 .

24. Toderan, C., Pircalabu, E., Caprace, J., and Rigo, P. (2007) Integration of a Bottom-Up Production Cost Model in LBR-5 Optimization Tool. COMPIT’07 . 25. Caprace, J., Bair, F., and Rigo, P. (2010) Scantling

Multi-objective Optimisation of a LNG Carrier. Marine Struc-tures, 23, 288–302.

26. Caprace, J., Bair, F., and Rigo, P. (2010) Multi-criterion Scantling Optimisation of Cruise Ships. Ship Technology Research, 57, 56–64.

27. Eyres, D. (2001) Ship Construction. Butterworth and Heinemann.

28. Seo, K., Park, J., Jang, D., and Wallace, D. (2002) Ap-proximate Estimation of the Product Life Cycle Cost Us-ing Artificial Neural Networks in Conceptual Design. The international journal of advanced manufacturing tech-nology.

29. Landamore, M., Birmingham, R., and Downie, M. (2007) Establishing the Economic and Environmental Life Cycle Costs of Marine Systems: a Case Study from the Recre-ational Craft Sector. Marine Technology, 2, 106–117. 30. Gratsos, G. and Zachariadis, P. (2007) Life Cycle Cost

of Maintaining the Effectiveness of a Ships Structure and Environmental Impact of Ship Design Parameters. Hel-lenic chamber of shipping.

31. Turan, O., ler, A., Lazakis, I., Rigo, P., and Caprace, J. (2009) Maintenance/Repair and Production Oriented Life-Cycle Cost/Earning Model for Ship Structural Op-timisation during Conceptual Design Stage. Ships and Offshore Structures, 10, 1–19.

32. Ferguson, W. B. (1944) Shipbuilding Cost & Production Methods. Cornell Maritime Press.

33. Boothroyd, G., Dewhurst, P., and Knight, W. (2002) Product Design for Manufacture and Assembly. 34. Hundal, M. (1993) Rules and Models for Low Cost

De-sign. ASME Design for manufacturability conference. 35. Fischer, J. O. and Holbach, G. (2008) Cost Management

in Shipbuilding. The Naval Architect, pp. 58–62. 36. Bole, M. (2007) Cost Assessment at Concept Stage

De-sign Using Prametrically Generated Production Product Models. ICCAS07 .

37. Bruce, G. and Reay, K. (1991) Cost-effective Planning and Control. Journal of SHip Production, pp. 183–187. 38. CESA (2006-2007) Annual Report. Tech. rep., CESA. 39. Koenig, P. (2002) Technical and Economic Breakdown of

Value Added in Shipbuilding. Journal of ship production, 18.

40. Ross, J. and Aasen, R. (2005) Weight-Based Cost Esti-mating During Initial Design. COMPIT’05 .

41. Shehab, E. and Abdalla, H. (2002) An Intelligent Knowledge-Based System for Product Cost Modelling. The international journal of advanced manufacturing technology.

42. Giudice, F., Risitano, A., and Rosa, G. L. (2006) Product Design for the Environment - A Life Cycle Approach. CRC Press.

43. Rush, C. and Roy, R. (2000) Analysis of Cost Estimating Processes Used within a Concurrent Engineering Envi-ronment throughout a Product Life Cycle. 7th ISPE In-ternational Conference on Concurrent Engineering: Re-search and Applications.

44. Lamb, T. (2003) Ship Design and Construction. Society of Naval Architects and Marine Engineers.

![Table 1 Typical accessibility/complexity coefficient for pas- pas-senger ship working areas [44]](https://thumb-eu.123doks.com/thumbv2/123doknet/5855614.142327/11.918.72.413.221.317/table-typical-accessibility-complexity-coefficient-senger-working-areas.webp)