Nonlinear Features of Realized FX Volatility

Texte intégral

Figure

Documents relatifs

The aim of the article is an analysis of software that is popular among economists and modeling of financial time series volatility using software packages R, Gretl,

The second chapter reviews and proposes realized volatility measures which are able to deal with the challenge posed by the presence of microstructure effects on the basis of a

P (Personne) Personnes âgées Personnes âgées Aged Aged : 65+ years Aged Patient atteint d’arthrose Arthrose Osteoarthritis Arthrosis I (intervention) Toucher

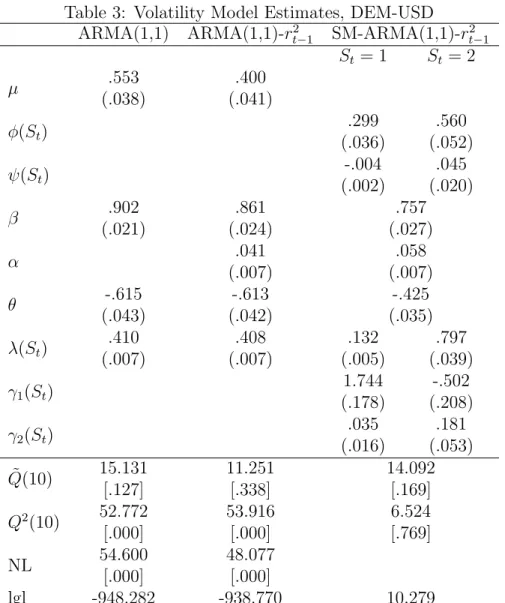

Our results show that when regimes are difficult to identify (i.e., many regimes switches or one regime occurs few times) and data are generated in the sense of Klaassen,

When forecasting stock market volatility with a standard volatility method (GARCH), it is common that the forecast evaluation criteria often suggests that the realized volatility

These results thus provide further evidence in favor of a warning against trying to estimate integrated volatility with data sampled at a very high frequency, when using

We document the calibration of the local volatility in terms of lo- cal and implied instantaneous variances; we first explore the theoretical properties of the method for a

In this paper, we obtain asymptotic solutions for the conditional probability and the implied volatility up to the first-order with any kind of stochastic volatil- ity models using