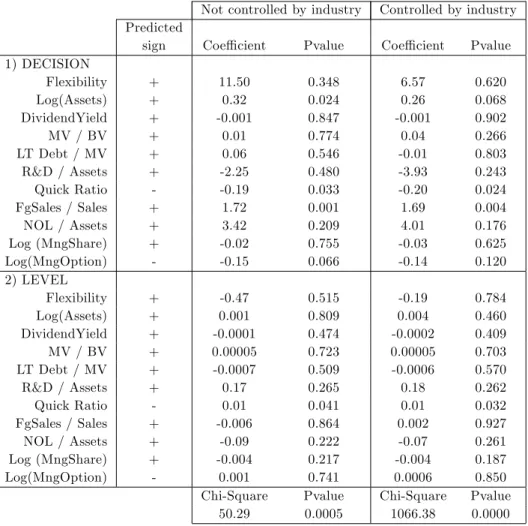

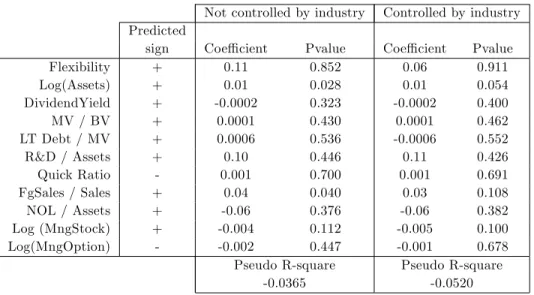

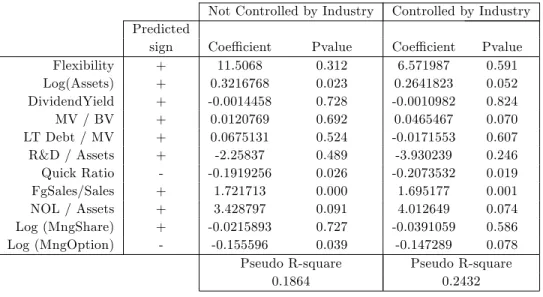

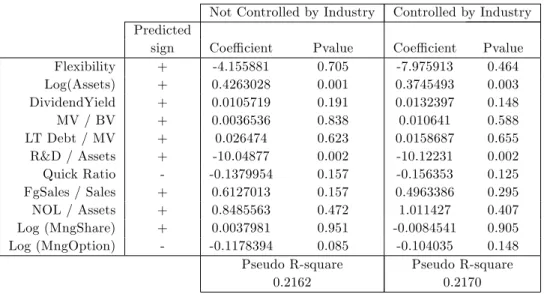

Financial Risk Management, Firm Structure & Valuation, an Empirical Analysis

Texte intégral

Figure

Documents relatifs

Hence, the measured 1.3mm residual dust is in strong agreement with the magnitude of the attenuating line-of-sight circumbinary disk material, and its location and orientation is

É provavelmente a que vem em primeiro lugar quando se interroga sobre a interculturalidade em educação: estudantes e professor podem referir-se a contextos culturais diferentes,

143 6.6 Concept alignment between Misuse cases and the ISSRM domain model 144 6.7 Asset and security objective modelling in KeS.. 149 6.9 Security requirements and control modelling

In this paper, hidden Markov models and EVT are combined to construct a variant of power laws model that forecasts the extreme observations taking into consideration both the

Key words: Enterprise Risk Management, Risk Management, Performance, Accounting performance, Market value, Audit Committee, Chief Risk Officer, Casablanca

A sensitivity equation method for unsteady compressible flows has been presented and veri- fied on some test-cases corresponding to subsonic Eulerian and subsonic laminar viscous

Figure (h) shows the result of subtracting the standard deviation of figures (f) and (g) in such a way that values less than zero indicate that the variance in figure (f) is lower

Par comparaison avec les classes de qualités [1] on conclut que la concentration moyenne en zinc dans les chaires des moules provenant de Sidi Mejdoub et de Bateau cassé est