Heterogeneous Befiefs and the Choice Between Private Restructuring and Formal Bankruptcy

Texte intégral

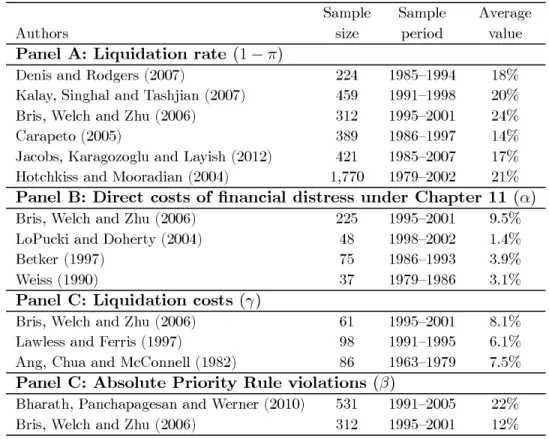

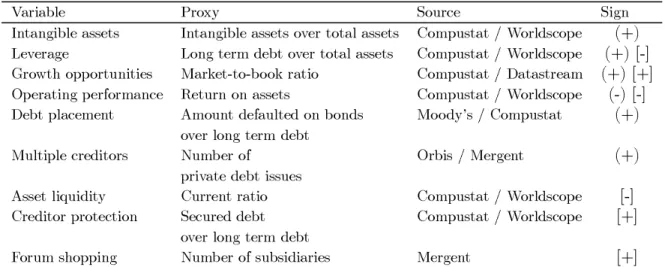

Figure

Documents relatifs

Pour l'Iran et la Russie, les deux traités de 1921 et 1940 - qui restent valables et toujours en vigueur en vertu du droit des traités et malgré la dissolution de l'URSS - forment

تايوتحملا سرهف يناثلا ثحبملا : كونبلا يف ةيسسؤملا ةمكوحلا موهفم 32 لولأا بلطلما : اهقيبطت في ينيساسلأا ينلعافلاو كونبلا في ةيسسؤلما ةمكولحا فيرعت 32

Anatole France entrait en militant dans l'Affaire Dreyfus, il ren- contrait Jaurès et se mettait en marche vers le communisme."l0 Evi- demment, Maurras,

pour se lancer, il fit appel à un modèle non professionnel, un soldat de 22 ans, Auguste Neyt, avec lequel il détermina une pose qui ne répondait pas aux critères habituels,

Pour cette évaluation, huit stations de mesure ont été mises en place sur le parc 2 du site Manitou, dont quatre dans la partie avec végétation, et quatre dans la partie

Associations entre classes (diagramme de classes) : Tout objet d’un diagramme d’objets doit être une instance d’une classe définie dans le diagramme de classes correspondant :

Les mêmes rayons de gouttes sont trouvés quel que soit le système ; à base d’eau (Figure 90, CNa/Cu-eau-w) ou en présence de NPs CuABP (Figure 103, CNa/Cu-w). b) Graphique

Therefore, the environment contributions to the total dipole cancel out, and only the displacement and charge of the MA contribute to the polarization work and the variation of