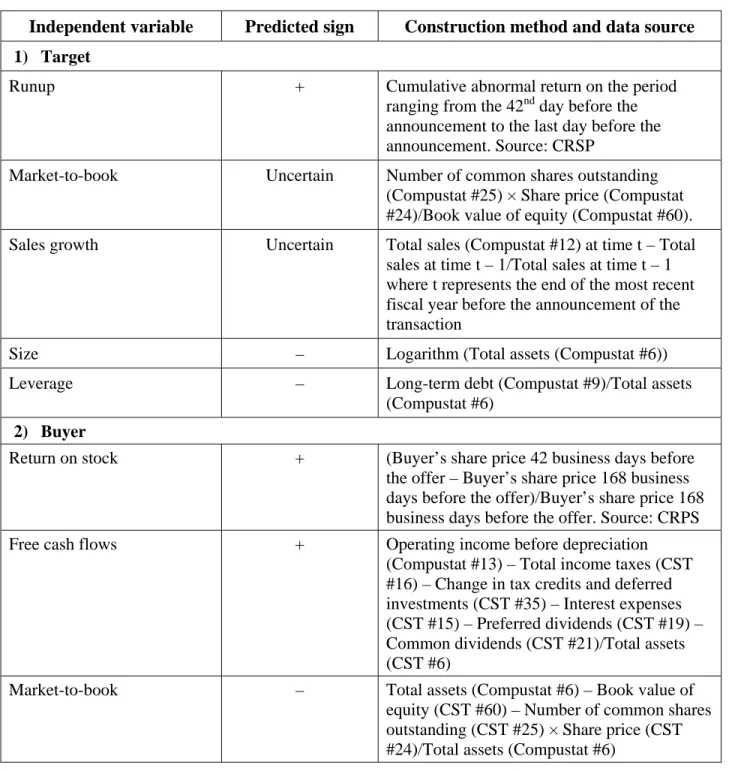

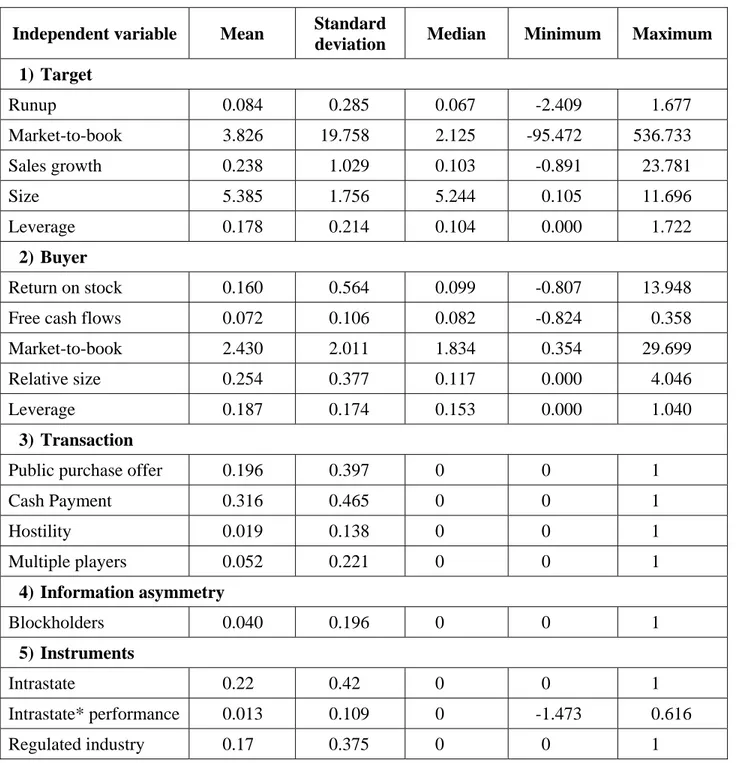

Does Asymmetric Information Affect the Premium in Mergers and Acquisitions?

Texte intégral

Figure

Documents relatifs

As a consequence we show that the Gaussian mollifier of the Wigner function, called Husimi function, converges in L 1 ( R 2n ) to the solution of the Liouville equation..

It differs from the Control Experiment in that each game is followed by a second stage that allows targeted interactions (in this treatment, peer punishment opportunities) at

We describe a CHSH-Bell test where one photon of an entangled pair is amplified by a Measure and Prepare cloner and detected by using threshold detectors and a postselection

Introduction Corporate Governance __ Supervisory Board Business Model Strategy Management Report Segment Reports Financial Statements Useful Information.. In the year under review,

Furthermore, another breakthrough made by Muto ([Mut]) showed that Yau’s conjecture is also true for some families of nonhomogeneous minimal isoparametric hypersurfaces with

While a model with a single compartment and an average factor of reduction of social interactions predicts the extinction of the epidemic, a small group with high transmission factor

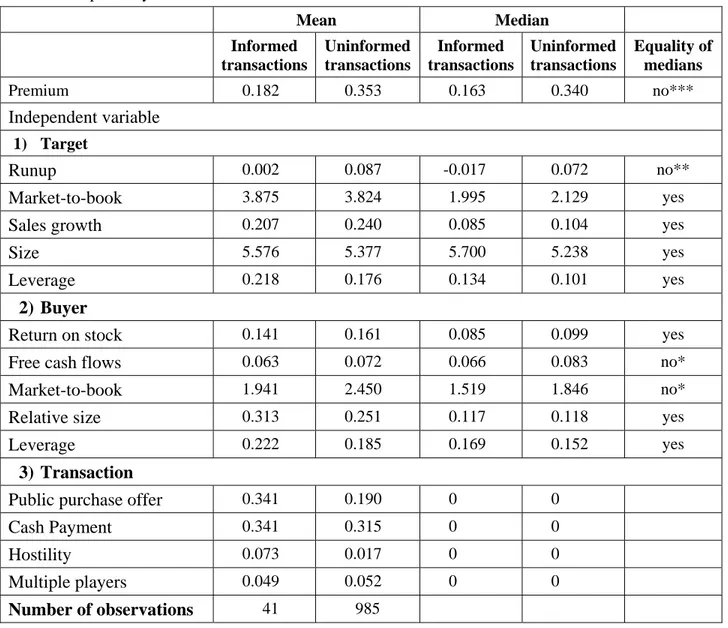

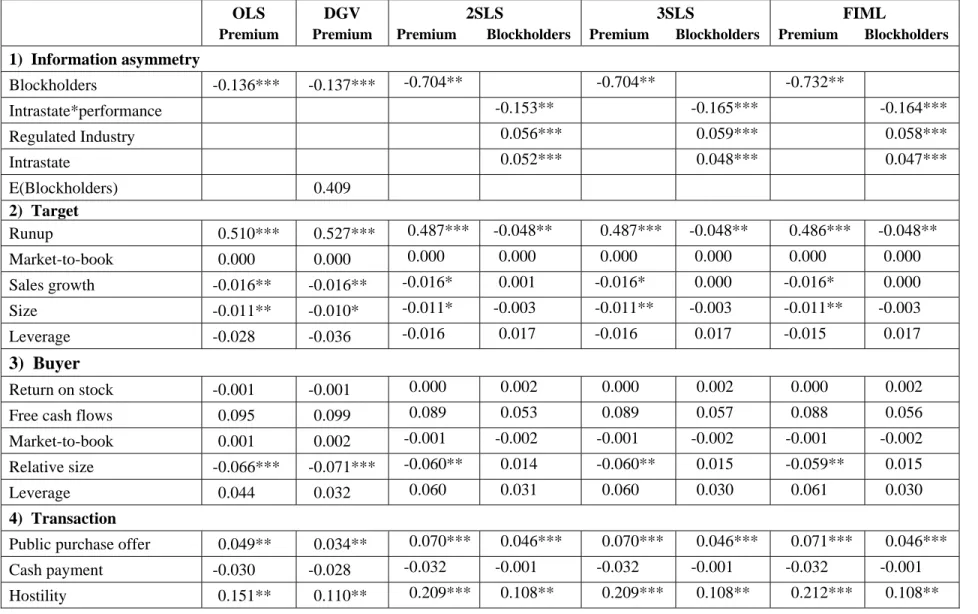

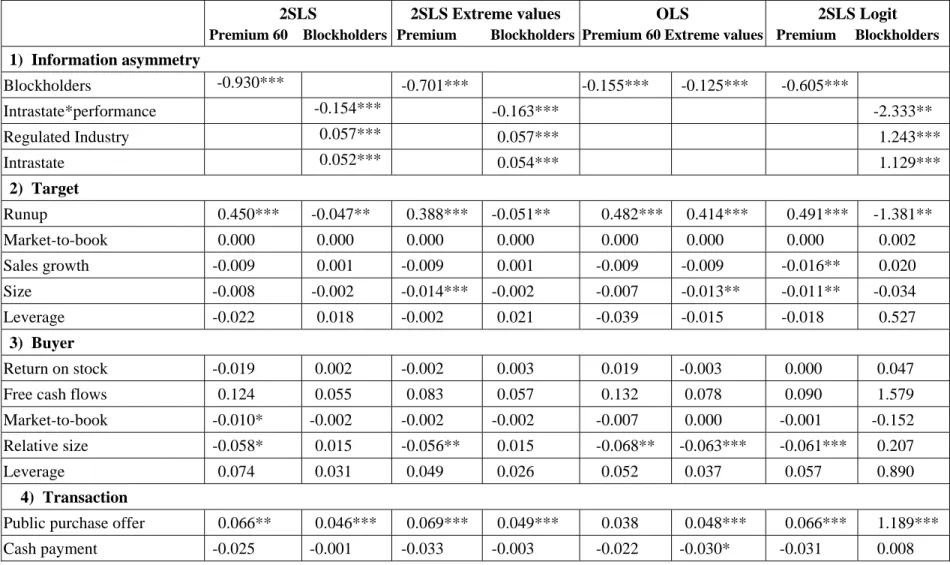

The Blockholders variable is equal to 1 if the buyer holds a block (more than 5%) of the target’s shares before making the offer. If this variable is significant, our

safekeeping. The pynabyte utility DYNASTAT displays your current system configuration. 'The steps described below will change the drive assignrnentsso that you will