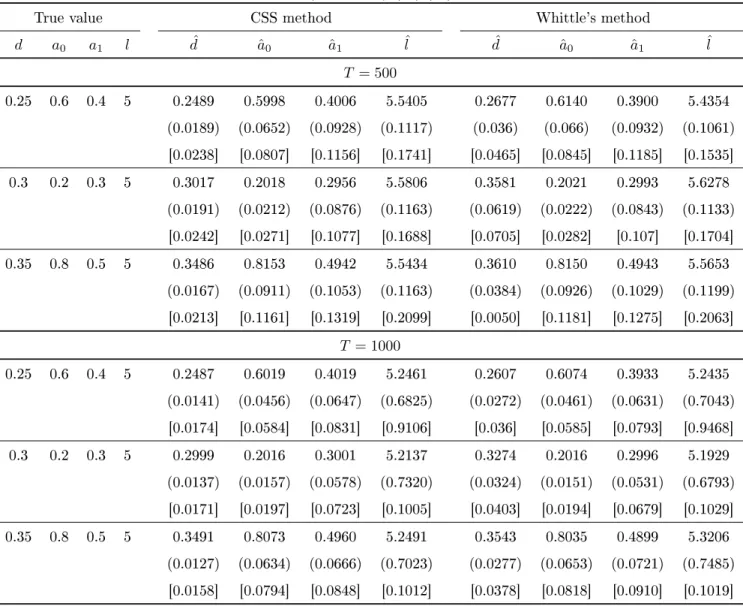

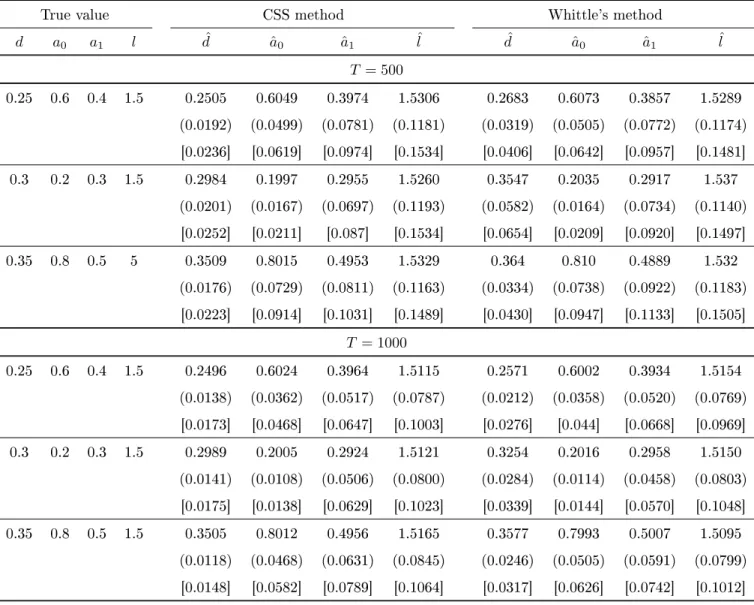

Estimation of k-Factor Gigarch Process: A Monte Carlo Study

Texte intégral

Figure

Documents relatifs

Simulate one game until a node (=position) L of T (thanks to bandit algorithms); put this simulation S in memory..

Keywords: Markov-switching, Dynamic Factor models, two-step estimation, small-sample performance, consistency, Monte Carlo simulations.. P ARIS - JOURDAN S CIENCES

Implementation, autocorrelation times The implementation of ECMC with factor fields for hard spheres does not require numerical root finding: an active particle i, moving to the

A methodological caveat is in order here. As ex- plained in §2.1, the acoustic model takes context into account. It is theoretically possible that the neural network learnt

Elle définit les principes généraux communs qui sont au nombre de cinq (par.. La médiation est un procédé librement consenti et auteur comme victime doivent pouvoir revenir sur

In Section 4 we show some results on the Collins e↵ect for transversely polarized u quark jets and compare them with the Collins asymmetries measured by the COMPASS Collaboration

As an improvement, we use conditional Monte Carlo to obtain a smoother estimate of the distribution function, and we combine this with randomized quasi-Monte Carlo to further reduce

We compare two approaches for quantile estimation via randomized quasi-Monte Carlo (RQMC) in an asymptotic setting where the number of randomizations for RQMC grows large but the