MITLIBRARIES

3

9080 02237 2673

i iliiiilililillli: 'am

11m

!iMliit;

iiiS

il'I'ii'.fiiiHI'iri.i:.!!/'!' lffl^^l!f!/Wli;);Mllffl;l'i::iiii

:;i|||i

^1iiii:

:;:||li|li|||j||ii|f||||||||p^^^-'iifeiisfv.,

,llliiiill

-iiiiii

iiiiiii:

Ipiiili

iiiliiiiiii

\Mi!i(i;i!i;iiSll :i,;!!iiii|i!l;:|!;!|Digitized

by

the

Internet

Archive

in

2011

with

funding

from

Boston

Library

Consortium

IVIember

Libraries

^^H^y

Massachusetts

Institute

of

Technology

Department

of

Economics

Working

Paper

Series

DO

CEOs

SET

THEIR

OWN

PAY?

THE

ONES

WITHOUT

PRINCIPALS

DO

Marianne

Bertrand,

UChicago

&

NBER

Sendhil

Mullainathan,

MIT

&

NBER

Working

Paper

00-26

September 2000

Room

E52-251

50

Memorial

Drive

Cambridge,

MA

02142

This

paper can be

downloaded

without

charge

from

the

Social

Science

Research

Network

Paper

Collection

at

MASSACHUSETTSINSTITUTE

OFTECHNOLOGY

OCT

3

2000

ABSTRACT

We

empiricallyexamine two

competing views of

CEO

pay. In the contractingview,pay

isused

to solve

an agency problem:

thecompensation committee

optimallychooses

pay

contractsthatgivethe

CEO

incentivestomaximize

shareholderwealth. In theskimming

view,pay

is theresult of

an

agency problem:

CEOs

have

managed

tocapture thepay

process so that theyset theirown

pay, constrainedsomewhat by

the availabilityof

cashorby

fearof drawing

shareholders'attention.

To

distinguish theseviews,we

firstexamine

how

CEO

pay

responds

toluck, observable

shocks

toperformance

beyond

theCEO's

control.Using

severalmeasures of

luck,

such

aschanges

in oil price for the oil industry,we

find substantialpay

for luck.Pay

responds

about asmuch

to a "lucky" dollar as to a general dollar.Most

importantly,we

find thatbetter

governed

firmspay

theirCEOs

less for luck.Our

second

testexamines

how much

CEOs

are

charged

forthe options theyare granted. Since optionsnever appear

on

balance sheets,theymight

offeran

appealingway

to skim.Here

againwe

find a crucial role forgovernance:CEOs

inbetter-governed firms are

charged

more

forthe options they aregiven.These

resultssuggestthat

both

views of

CEO

pay

matter. In poorlygoverned

firms, theskimming view

fits better(payforluck

and

littlecharge foroptions)while inwell-governed

firms,the contractingview

fitsbetter (filteringout

of

luckand

chargingforoptions).1

Introduction

There

aretwo predominant ways

to thinkabout

CEO

pay.The

first one,which

we

refer to as thecontracting view, relies

on

principal-agentmodels.Because

CEOs

oftenown

very little ofthe firmthey control, shareholders face a classic

moral

hazard problem:CEOs

may

not alwaysmaximize

firm value in

making

their decisions.Under

the contracting view, shareholders (actingthrough

the

board

or thecompensation committee)

useCEO

pay

to reducemoraJ

hazard. Explicitpay

for performance, such as long

term

contracts or options,and

implicitpay

for performance,such

as

a bonus payment,

areallused

by

boards to increaseCEOs'

incentives tomaximize

shareholderwealth.^

The

second view,which

we

referto as theskimming

view, hasbeen

championed

by

practitionerssuch

as Crystal (1991). It also beginswith

the separation ofownership

and

control, but it arguesthat this separationallows

CEOs

to gaincontrol ofthepay

setting process itself.By

packing theboard with

their friends, orany

othermean

ofentrenchment,many

CEOs

de facto set theirown

pay.

They

skim

what

theycan

from

shareholders, constrainedperhaps

by

theamoimt

offundsinthe firm,

by an

unwDlingness todraw

the attention of shareholder jictivistgroups

orby a

fearofbecoming

a takeover target.Within

these constraints, however, theypay

themselves asmuch

as possible.Whereas

pay

in the contractingview

isan

attempt

to solvemoral

hcizard,pay

in theskimming

view is the resultofmoraJ

hazard.We

propose two

tests to differentiate these models. In thefirsttest,we

examine whether

CEOs

'Murphy (1985, 1986)

b

a forerunner ofthe vast literature that has empirically analyzedCEO

compensationinthe context ofthe princip>al-agent model. The resulting literature is summarized in Murphy (1999).

The

majoreconometric work has been to test for vaJue-optimizing incentivescheme by studying the correlation between pay andperformance. Jensenand Murphy(1990) usethisframeworktoarguethatpoliticalconsiderationsconstrainpay

so that incentivesare too low. Joskow, Rose £ind Shepard (1993) empirically examine thisargument in regulated industries. Othertests ofthe agencyframework can be foundin Gibbons and

Murphy

(1990),who

testfor relativeperformance evaluation andcareer concerns, Garen (1994) and Aggarwal and Samwick (1999a), who test for

risk-return treideofe, and Hubbard and Palia (1994) and Bertrand and Mullainathan (1998),

who

test whether payare

rewarded

for observable luck.By

luck,we

mean

changes

in jBrmperformance

that arebeyond

CEOs'

control. In simpleagency

models,pay

should notrespond

to luck sinceby

definition theCEO

cannot influence luck.Tying

pay

to luck will not provide better incentives; it will onlyadd

risk to the contract (Holrostrom, 1979).^

Under

theskimming

view,on

the otherhand,

pay

willrespond

to luck since theCEO

can

divert those "lucky" dollars topay

herself as easily as shecan

divert earned dollcu^.

To

empiricallyexamine

the responsiveness ofpay

to luck,we

use three differentmeasures

ofluck. First,

we

perform a

casestudy

ofthe oil industrywhere

largemovements

in oil pricestend

to affect firm

performance on

a regularbasis. Second,we

use changes in industry-specificexchange

rate for firms in the traded

goods

sector. Third,we

use year-to-year differences inmean

indiistryperformance

toproxy

for the overalleconomic

fortune ofa

sector.This

lastmeasure

verymuch

resembles the

approach

followed in the relativeperformance

evaluation literature.For

all threemeasures,

we

find thatCEO

pay responds

to luck. Infact,we

find that for all three luckmeasures

CEO

pay

is as sensitive toa

"lucky dolleir" as toa

"general dollar."This

basic finding ofpay

for luck, however,can be

explainedby

complicating the basicagency

model.

For

example,suppose boards wanted

theirCEOs

to forecast orrespond

to luck shocks.Tying

pay

to luck in this casemay

be

necessary to provide better incentives. In the oil industry,rewarding

theCEO

after the fact for seeingan

oilshock

coming

encourageshim

tokeep

his eyesopen

before the fact. Alternatively,suppose

the "value" ofa

CEO's

hiiman

capital rises cuid fallswith

industry fortunes.One

would

then

find thatpay

correlateswith

luckbecause

theCEO's

outside

wage

moves with

luck.While

we

wiU

argue thatthesearguments

may

be

incorrect,theymotivate ustosearchforfurther ^Note our emphasis on observable luck. In any model, given the r£indomness ofthe world,CEOs

(and almosteverybody else) will end up being rewarded for unobservable luck. Note also our emphasis on the fact that this prediction holds in simple agency models. As we will discuss shortly, complications to the agency model can in principlealter thisresult.

tests.

We

thereforeexamine

another direct implication of theskimming

model, thatskimming

willbe

less important in well governed firms.Good

governance willmake

ithard

for theCEO

to gaincontrol ofthe

pay

process.So

ifpay

for luckcomes from skimming,

we

expect to see less of it in the bettergoverned firms.We

test this hypothesis usingseveralmeasures

ofgovernance: presenceof largeshareholders {onthe

board

and

overall),CEO

tenure (interactedwith

the presence of large shareholders to betterproxy

for entrenchment),board

sizeand

fraction of directors that are insiders. Consistentwith

skimming,

we

generally find that the bettergoverned

firmspay

less for luck.^These

effects are strongest for the presence of large shcireholderson

theboard

who

reducepay

for luckby

between

23

and

33%.

Large shareholders are especiallyimportant

asCEO

tenure increases, consistentwith

the idea that

unchecked

CEOs

can

entrench themselves over time.The

findingson

governance

castdoubts on

the alternative interpretationswhich

make

pay

for luck optimalthrough

complicationsto the agency model. If

pay

forluckwere

infactoptimal,we

would

not expect to see wellgoverned

firms use less ofit. For example,

whether

or not a large shareholder is present,CEOs

would have

to

be

rewairded for arise in the vcilue of theirhumjin

capital.These

findings instead suggest thatat least

some

ofthepay

for luck in poorly governed firms isdue

toskimming

by

CEOs.

Our

second test revolvesaround

another aspectofCEO

compensation

that hasreceivedatten-tion in recentyejirs: the greinting of

new

stock options. Principal-agenttheory predicts thatwhen

options aregranted, other

components

ofcompensation

shouldbe

adjusteddownwards

to leave theCEO

indifferent. In other words, theCEO

shouldbe charged

for the options she is granted, ifnottheir Black-Scholes value

then

atleast this value timesa

riskcorrectionfactor.'* Supporters ofthe ^Wheneverwe refer to "less pay for luck" we meanthat there is less payfor luck relativeto theamount ofpayfor performance. Thus, these results would not be driven bywell governed firmssimply givingless overedl payfor performance.

^Thebasic ideais that options havevalue. For example, supposea

CEO

isgranted 10,000 options with astrike price of50,a horizonof 3years andthefirmiscurrentlytradingat 50. Theseoptionshave valueinandofthemselves because evenifthefirmunder-perfonns relative tothemarketandearnsacumulative3-year{nomincil)returnofonlyskimming

view,on

the other hand,emphasize

that stock optionsdo

notappear

on

balance sheets.Because

ofaccounting treatments, firmsdo

not takea

financial chargeforgranting options.CEOs

can

thereforepay

themselvesthrough

option grantswithout

affecting thecompany's

bottom

line.Under

theassumption

that shareholders only (or mostly)pay

attention to the accountingbottom

line,thegrantingof

new

stock optionswould

representan

easyway

toskim

more

without

attracting shareholders' attention.No

cut in the othercomponents

ofpay would

be

necessary.Thus

whileagency

theory predictsa

largecharge for options,skimming

predictsabout no

charge.Unfortxmately,

a

directmeasure

ofhow much

CEOs

are in factcharged

for their options isnot possible

because

ofa

naturalomitted

variable bias.Taking

oiu: leadfrom

thepay

for luckfindings,

we

thereforefocuson

the questionofhow

governance

affectsthe charge for options.Using

the

same

measures

ofgovernance,we

generally find thatmore

poorlygoverned

CEOs

arecharged

less for their

new

options grants. Forexample,

foran

options grantworth

1 million dollars (inBlack-Scholes terms),

an

extra large shareholderon

the bocird increases the charge for optionsby

between

30and

50 thousand

dollars.As

before,we

also find that asa

CEO

tenure increases, thecharge for optionsdiminishes in firms

without

a

large shareholder.In

summary,

thispaper

containsthreemain

results. First,CEO

compensation shows

on

averagea

significantamount

ofpay

forluck. Second,wellgoverned

firms displaylesspay

forluck, suggestingthat it is possibleto filterout luck. Third,

CEOs

in well governed firms arecharged

more

for theirstock options grants.

At a

first glance, these resultsseem

to providesupport

for theskimming

view.

CEOs

arerewarded

for luckand

seem

tobe

able toskim

using options.But

noticethatthey

also provide

support

for the contracting view.Well

governed firmsdo

manage

to filter outsome

luck

from

performance

and do

manage

to chargemore

for options.We

feel thattheresults suggest10%, hestillgains(.1) 50 10,000

=

50,000dollars. Eveniftheoptionisgranted outofthemoney,the sameeffect will arise becausethe optionmay

come into the moneyjust because ofmovements in share pricethat comes fromthefirm's natural volatility. Agency theory therefore predictsthat

CEOs

shouldbe chargedforthe gift implicit inas a

whole

thatboth

views ofCEO

pay

are true. In practice, executivecompensation seems

tobe

better characterized

by

either theskimming

or the contractingmodel

depending

on

the extent towhich

there isan

active "principal" (or principals) present toactually designpay

contracts. Bettergovernance

means

that there ismore

ofan

active principaland

optimal contracting fits better.Worse

governance

means

that there is less ofan

active principaland

theCEO

ismore

likelyto sethis

own

pay.^The

rest ofthispaper

is organized as follows.We

startby

presenting our test of the lack ofperformance

filtering (section 2).We

first presenta

very simple theoreticalbackground

(section2.1), review the existing evidence (section 2.2)

and

explain the empiricalmethodology

(section2.3).

We

then

establish the existence of pay-for-luck,both

in the specific case ofthe oil industry(section 3.1)

and

formore

general sets of industries (section 3.2). In section 3.3,we

demonstrate

the role of

governance

in limiting the extent of pay-for-luck. In section 4,we

establish that thesame

governance

variables alsomatter

in limitingthe gift nature ofnew

stock option grants.We

siunmarize

and

concludein Section 5.2

Pay

for

Luck

Test:

Background

2.1

Theoretical

Background

Our

first test focuseson

whether

CEOs

arerewarded

for observable luck.A

simple theoreticalmodel

willmake

precisewhat

agency

theory saysabout

thereward

for luck.Consider

astandardagency

setupwhere

risk-neutral shareholders,perhaps

operatingthrough

theboard, try to inducea risk-averse top

manager

tomaximize

firm performance. Since the actions of theCEO

can

be

'This confirma the sentiment that emerges from conversations with compensation consultants as they describe being hired bytwotypesof firms: the oneswheretheyclearly havetorespondtotheCEO

andthe oneswherethey clearly have torespondtotheshaureholders.hard

to observe, shareholders willbe unable

to signa

contractthatspecifies these actions. Instead,shareholders will offer a contrax:t to the

CEO

where

hercompensation

level ismade

todepend

on

the firm's performance. Letp

represent firmperformance

and

a

theCEO's

actions,which by

assumption

areunobservableby

theshareholders.Firm

performance depends

on

theactions oftheCEO

and

on

random

factors.We

split therandom

feictors intotwo components:

those thatcan be

observed

by

shareholdersand

those that cannot.For

an

oil firm, the price ofcrude

oilwould

be

an

observablerandom

factor. Lettingo be

the observable factorand

u

be

the unobservable noiseterm,

we

assiune thatperformance

can

be

written as:Under

some

technicalconditions,Holmstrom

cuidMilgrom

(1987) calculatetheoptimal

incentivescheme

for this model.^ Let sdenote

this incentive scheme. Since shareholderscan

only observetwo

variables,p and

o, the incentivescheme

could atmost

depend on

thesetwo

variables. In fact,shareholders

wiU

onlyreward

CEOs

forperformance

net ofthe observablefactor.s

=

Q

+

/3(p-

Jo)=

a

+

;0(a+

u) (1)In other words, the optimal incentive

scheme

filters theobservable luckfiromperformance.This

is because leaving o in the incentive

scheme

providesno added

benefit to the principal as,by

definition, the agent has

no

control over o. "Incentivizing" heron

o has thereforeno

incentiveeffects.

Beyond

providingno

benefit, it actually costs the principalbecause

not filtering out luckincreases the variance oftheincentive scheme, thereby forcing the principal to increase

mean

pay

to

compensate

the risk averse agent.^

How

might

we

expect filteringof lucktooccur

in practice? Explicit incentive contracts,such

as'Essentially,

we

need toassume thattheCEO

hasCARA

utility andthat outcomes followa Brownian process.A

much

moregeneral result can be found in Holmstrom (1979).options, rarely filter. For example, options axe rarely ifever

indexed

againstmarket

performance.This need

notbe

inconsistentwith

alack offiltering, however.One

might

expect that thebestway

to filter luck is

through

theuse of subjectiveperformance

evaluation. Inpractice,we

would

expectthe

board

tobe

theprimary

mechanism

for doing this.The

board

should use the discretionarycomponents

ofpay, suchas bonus, salary ornew

options grants, torespond

to luck shocks.2.2

Existing

Evidence

Previous

work

already hints ata

relationshipbetween pay

and

luck. First, Blanchard,Lopez-de-Silanes

and

Shleifer (1992) find that windfallgainsfrom

court rulings raise thepay

ofCEOs.

Second, as

we

just mentioned, the stock options that are granted toCEOs

are very rarely indexedto the market.

While

interesting, thesetwo

facts are only suggestive.A

court rulingmay

notbe

luck, but rather the result ofthe

CEO's

work.And,

as noted, while optionsmay

notbe

indexed(perhaps for simplicity or tax reasons), the

board

can always reissuethem

or adjust other parts ofpay.

For

many,

the apparent lack of relativeperformance

evaluation(RPE)

isprobably

the best existing piece ofevidence ofpay

for luck.*Even

with this evidence though,some

problems

arise.First,

mean

industrymovements

aiea

specialform

of luck. Filtering this specific kind ofluckmay

notbe

optimalfrom an

agency

theoretic point of view. In fact.Gibbons and

Murphy

(1990)themselves note that relative

performance

evaluationcan

distortCEO

incentives iftheycan

"takeactions that affect the average

output

of the reference group."^Aggarwal

and Samwick

(1999b)alsodevelop

a

specificmodel

inwhich

relativeperformance

evaluationschemes

may

notbe

optimcil*While Gibbons and Murphy(1990) findsomeevidenceforRPE, someof their resultsarepuzzling. Forexample, there appears to be more filtering of general stock market shocks than of shocks specificto the relevant industry.

Most ofthe otherwork on thetopic,suchasJanakiraman et al. (1992) andAggarwalandSajnwick (1999a), findno

evidenceof

RPE.

®They list four different kinds of such actions: sabotcige, collusion, choice of reference group and production

for shareholders aa they try to provide

CEOs

with

the best incentives.^"^Our

test addresses thesecriticisms.

We

willexamine

a variety of shocks, including but not restricted tomean

industrymovements.

We

willverify thatothershockstoperformance

that areeven

more

objectivelybeyond

managerial influence,

such

as shocks to theprice ofcrudeoil orexchange

rates shocks, also fail tobe

filtered.2.3

Empirical

Methodology

Within

theagency framework,

moat

ofthe empirical literature estimatesan

equation ofthe form:Vit

=

oii+

at+

ax

*^it+

P

*per

fit+

eu (2)where

yit denotes totalCEO

compensation

infirmi attime

t, a,- are firmfixed efi'ects, at aretime

fixed effects,

Xn

arefirm (andCEO)

specificvariables such as tenure or firm size,and

per

fitrep-resents

a

performance

measure.The

coefficient^

captures the strength ofthepay

forperformance

relationship.

Performance

istypicallymeasured

eitheraschangesinaccountingprofitsorstockmarket

returnsand

we

will xiseboth

measures.^* Inmeasuring compensation,

y^t,one

problem permeates

theliterature

and

our

paper

isno

exception. Ideally, thecompensation

ina

yearwould

include thechange

in valueofunexercised optionsgranted in previous years.Such

a

calculation requiresdata

on

theaccumulated

stock ofoptionsheldby

theCEO

eachyear,whereas

existingdata

contains onlyinformation

on

new

options grantedeach

year. Consequently,our compensation

measure

does notinclude this

component

ofthechange

in wealth.As

we

discuss in Section 3.2.1, thisdata

problem

'''The basic ideaisthattheniean performanceintherest ofthe industrymay

actuallyprovide someinformationabouttheCEO'seffortto attenuate orstrengthenthelevelofcompetition inthat industry. Forexample,ifproduct marketcompetition in an industry needs to besoftened, shcireholdersmight in anefficient contracting environment rewardthe

CEO

whentherest oftheindustry isdoingwell asthis mightindicatethat theCEO

actedsuccessfullyin attenuating the competitive pressures inthat industry.

"Theseareflowmeasures. In practice,given the firmfixedeffects,wewillusemarketvalueandlevelof accounting

should, ifanything, biasour resultstowards overstating the case towardsfiltering

and

understatingthe extent of

pay

for luck.To

estimate the general sensitivity ofpay

to performance,we

willfoUow

the literatiureand

estimate equation (2) using a standard

Ordinary

Least Squares(OLS)

model.To

estimate thesensitivity of

pay

to luck,we

need

to use amore

complicatedtwo

stage procedirre. In the first stage,we

will predictperformance

using luck.This

will isolate changes inperformance

that arecaused

by

luck. In the second stage,we

will seehow

sensitivepay

is to these predictable changesin performance. This

two

stageprocedure

is essentiallyaJi Instrumental Variables (IV) estimationwhere

the luck variable is the instrument for performance.^^Letting o

be

luck, the firstequationwe

estimate is:perfit

~

ai+at

+

ax

*X^ +

b *oa

+

en (4)where ou

represents the luckmeasure

(oil price for example). Again, this equation allows us topredict a firm's

performance

using only informationabout

luck.We

then askhow

pay

respondstothisluck induced performance, perf^^:

yu

=

ai+

at+

ax

*Xu +

PlucK *per

fit+

en (5)The

estimated coefficient pLj^ck indicateshow

sensitivepay

is to changesinperformance

thatcome

firom luck. Since

such

changes shouldbe

filtered, basicagency

theory predicts /3[,y,ck should equal0.

'^One might wonder

why

we should use this procedure rather than simply include o directly into the pay forperformanceequation (2) and run

OLS

to estimate:Vit

=

at+

at+

ax

*Xit+

*perfu+

7 o+

e<e (3)This equation ishardto interpret,however. Evenifthereis no payforluck, thecoefficient 7will not equal

—p

butrather —05, aswe can seefrom equation I. Sincewe wedonot estimate S, the estimatedcoefficient7 can besmall eitherbecause thereispayforluckorsimplybecause Sis small. ThefirstequationintheIVprocedure,on the other hand,scalestheeffectofluckonperformance, circumventingthis problem.

3

Testing

for

Pay

for

Luck

3.1

Oil

Industry

Study

We

now

tiimto theoilindustryto testwhether

infact there iszeropay

for luck.As

Figure 1 shows,the price of crude oil has fluctuated dramatically over the last 25 years.

These

large fluctuationshave

caused largemovements

in industry profits.Over

this period,a

CEO

ofone

of these firmswould have found

thata measurable

variable (oil prices) greatly influenced theperformance

ofhis firm. Moreover, these large fluctuations in

crude

oil prices are likely tohave

been

beyond

thecontrol of

a

singleUS

CEO.

For example, the sharp decline in crude oil price at theend

of 1985was

causedby

Saudi

Arabia'sdecision toreform itspetroleum

policyand

to increase itproduction,an

action hardly attributable(and

never attributed) to theCEOs

ofUS

oil firms. Similarly, thelargeoilpriceincrease

between

1979and

1981 is usually attributed toan

internalpolicychange

by

OPEC.

Oil pricemovements

therefore providean

ideal place to test forpay

for luck: they affectperformance, are

measurable

and

axe plausiblybeyond

the control oftheCEOs.

We

usea data

seton

thepay

and

performance

for the51 largestUS

oilcompanies between

1977and

1994 toimplement

themethodology

of the previous section.^^ Beforemoving

to regressionanalysis,it is useful to look directly at

how

pay

fluctuatescompared

to themovements

inFigm-e 1.InFigure2,

we

have

graphed

changes inoil prices for each yearand

changes

inmean

logpay

intheindustry.

Two

strikingfacts emerge. First,pay changes

cind oil pricechanges

correlate quite weU.In 12 ofthe 17years, they areofthe

same

sign:both

au^eup

orboth

aredown. This

issuggestiveofa

largeamount

ofpay

for luck.The

second factcomes

firom theremaining

5 yearswhere

they are'^We are extremely grateful to Michael Haid for making the data set used in this Bection available to us. See

Haid (1997) for further details about the construction of the data set. Tiible

Al

in the appendix providesmean

and standard deviationsfor themain variables ofinterest. Whiletheoriginal datasetcovers 51 companiesoverthe period1977 to 1994,informationon

CEO

payisavailable foronly 50 of theseoriginal 51 companies. Moreover,CEO

pay isavailablefrom 1977 onforonly 34 of these 50 companies. The finaldataset

we

use covers 827company/year observations.ofoppositesign: all these 5 years cire years in

which

oilpricedropsbut pay does

not.This

hints atan

asymmetry:

whileCEOs

are alwaysrewarded

forgood

luck, theymay

not alwaysbe

punishedfor

bad

luck.While

we

will not formallypursue

theasymmetry,

it isworth

keeping inmind.

This

figure, however, does not allowus toquantify thesize ofpay

for luck:how

does itcompare

to the

pay

for general performance? It also does not control for other firm specific variables thatmight

be

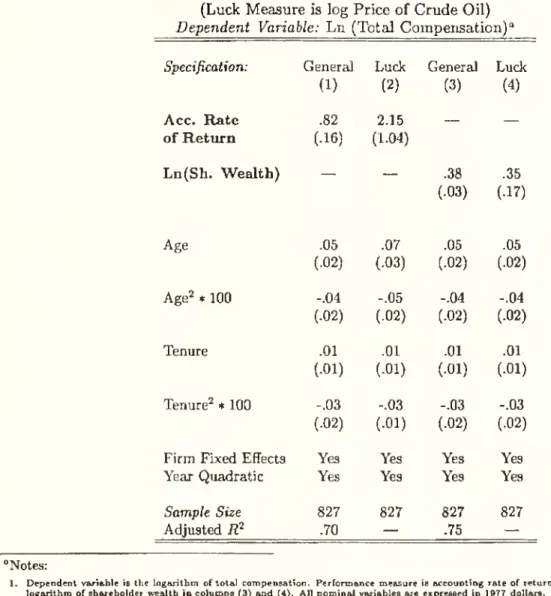

changing over time. Table 1 follows the empiricalmethodology

presented in Section 2.3,which

allowsamore

systematic analysis.The

regressionsuselog(totalcompensation)

asdependent

variable

and

include firm fixed effects, ageand

tenure quadraticsand

a performance

measure

asdependent

variables.*'*We

also allow for a year quadratic to allow for the fact thatCEO

pay

has

been

trendingup

duringthis period.Column

(1) estimates the sensitivity ofpay

to a generalchange in accounting performance.

The

coefficient of .82 suggests that ifan

oil firm increases itsaccounting return

by

one

percentage point, totalcompensation

risesby

.82 * .01=

.0082«

1 logpoints. Roughly, a

one

percentage pointincreaseinaccountingreturns leads toa

.8percentincreaseinpay.

Note

that the signand

magnitude

ofallthe othercovariates in theregressionseem

sensible.Pay

increases with ageand

to a lesser extent with teniu-e.Both

the ageand

tenure profile areconcave (the negative coefficient

on

the quadratic term).Colimin

(2)estimatesthesensitivityofpay

toluck.As

described,we

instrumentforperformance

withlog oil prices.'^

This

aUows

us tonarrow

down

on

movements

in accounting returns that aredue

to oil price changes.The

coefficient incolumn

(2)now

rises to 2.15.This

suggest thata one

percentage point rise inaccoimting returns

due

to luckraisespay

by

2.15 percent.Given

the largestandcird errors, one cannot reject that the

pay

forluckcoefficientand

pay

forgeneralperformance

coefficient are the Scune.

One

can

however

strictly reject the hypothesis ofcomplete

filtering: oil '"Tbtal compensation in this table and all others includessalary, bonus, other incentive payments and value of options grantedinthat year."This table does not report the first stage regressions ofperformance measure on oil price. But as one would

CEOs

are paid for luck thatcomes

from

oil pricemovements.

Columna

(3)and

(4)perform

the Scune exercise but for amarket

measure

of performance:shareholder wealth.

The

coeflBcient of .38on column

(3) suggests thata one

percent increase inshareholder wealthleads to roughly

a

.38 percent increase inCEO

pay. Incolumn

(4),we

find thata one

percent increasein shareholder wealthdue

to luck leads to .35 percent increase inCEO

pay.Again,

pay

for luckmatches

pay

for general performance.3.2

More

General

Tests

The

oil industry case study hasbeen

instructiveabout

themagnitude

ofpay

for luck.CEO

pay

responds as

much

toa

lucky dollarthan

to ageneralperformance

dollar.This

is onlyone

industry,however,

and

one might

askhow

generalizable these results are. In this section,we

willexamine

luck shocks that affect

a

broader set of firms.We

focuson two measures

ofluck:movements

inexchange

ratesand

mean

industry performance.By

affecting the extent ofimport

penetrationand

hence

foreign competition,exchange

ratemovements

can

strongly affecta

firm's profitabihty.Movements

inmean

industryperformance

alsoproxy

for luck to the extent thata

CEO

does notinfluence

how

the rest of her industry performs.^^3.2.1

CEO

Compensation

Data

To

implement

these tests,we

usecompensation

dataon

792 large corporations over the1984-1991 period.

The

data

setwas

graciouslymade

available to usby

David

Yermack and

Andrei

Shlerfer. It is extensively described inYermack

(1995).Compensation

data was

collectedfrom

the corporations'

SEC

Proxy, 10-K,cmd 8-K

filings.Other data

was

transcribedfrom

the Forbesmagazine annual

survey ofCEO

compensation

as well asfrom

SEC

Registrationstatements, firms'As we mention before, this \ast assumption is more questionable. In practice,

we

find thatmean

industryAnnual

Reports, directcorrespondencewith

firms, press reports ofCEO

hiresand

departures,and

stock prices

pubhshed

by Standard

&

Poor's.Firms

were selected into thesample

on

the basisof their Forbes rankings. Forbes

magazine

publishes annual rcinkings of the top500

firmaon

fourdimensions: sales, profits, assets

and

market

value.To

qualify for thesample

a corporationmust

appear

inone

of these Forbes 500 rankings at least four timesbetween

1984and

1991. In addition,the corporation

must have been

publicly traded forfour consecutive yearsbetween

1984and

1991.Yermack

data is attractive in that it providesboth governance

variablesand

informationon

options granted, not just information

on

options exercised. It does not, however, include changesin the valueofoptions held.

Our

compensation

measure, therefore,wiU

not include thechange

invalueof pre-existing options. Ifanything, this biases us towardsfinding less

pay

forluck than thereis. Since options are not indexed, changes in the value ofoptions held

wUl

covary perfectlywith

luck. Including

them

would

onlyincrease themeasured pay

for luck.This data

limitationthereforepushes us towards favoring the filtering hypothesis,

making

our statistical rejection ofcomplete

filtering that

much

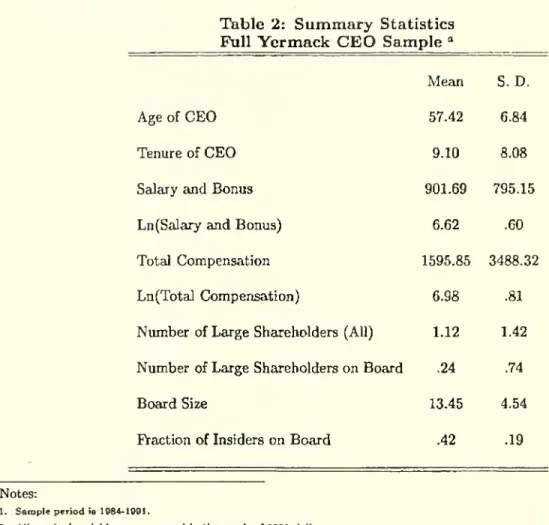

stronger.Tkble

2 presentssummary

statisticsforthemain

variablesofinterest inthefullYermack

data.^'^All

nominal

variables are expressed in 1991 dollars.The

averageCEO

earns 900thousand

dollars insalaryand

bonus. His totalcompensation

is nearly twice thatamount

atone

millionand

600thousand

dollars.The

differenceindicatesthelarge fraction ofa

CEO's

pay

thataredue

tooptionsgrants.

The

averageCEO

is roughly57

years oldand

hasbeen

CEO

ofthe firm for 9 yccirs.As

far asgovernance

goes, the average firm in oursample

has 1.12 large shareholders, ofwhich

lessthan a

fourth are sittingon

the board.There

cireon

average 13 directorson

a board. 42 percentof

them

are insiders.^®'''in practice,depending onthe requiredregressors, the varioustestsin thefollowing sectionswillbe performed on

various subsamplesoftheoriginal data. None of these main variables of interest significantly differ in any ofthese subsamples.

3.2.2

Exchange

Rate

Movements

asMeasures

of

Luck

Our

first generalmeasure

of luck focuseson

exchange

ratemovements.

We

exploit the fact thatexchange rates

between

theUS

dollarand

othercountry currencies fluctuate greatlyover time.We

alsoexploit thefact that different industries are affected

by

different countries'exchange

rates. Forexample,sincethetoy industry

may

be

more

affectedby Japanese

imports while thelumber

industrymay

be

more

affectedby

Bolivia, thesetwo

industriesmay

experience very different shocks in thesame

yeax.This

allows us to construct industry-specificexchange

ratemovements

which

we

arearguably

beyond

CEOs'

control since they are primarilydetermined by

macroeconomic

variables.The

exchange

rate shockmeasure

isbased

on

the weighted average ofthe log realexchange

ratesfor

importing

countriesby

industry.The

weights are theshare of each foreign country'simport

intotal industry

imports

in abase year (1981-1982).Real

exchange

rates arenominal exchange

rates(expressedin foreigncurrency perdollar) multiplied

by

U.S.CPI

and

dividedby

theforeigncountryCPI.

Nominal

exchange

ratesand

foreignCPI's

arefrom

the International FinanciaJ Statistics ofthe International

Monetary

Fund.

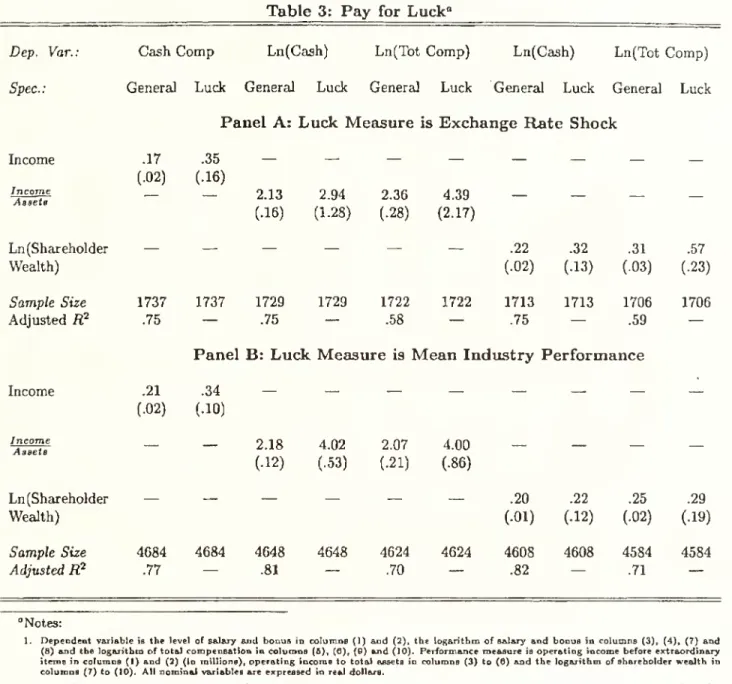

Panel

A

ofTable

3examines

the effect of thismeasure

of luck.Note

that since theexchange

rate

measure can

onlybe

constructed for industrieswhere

we

have imports

data, thesample

sizeis

much

smallerherethan

forour

fullsample. All regressions controlfor firmand

yearfixed effectsas well as for quadratics in tenure

and

age.^^Column

(1) uses asdependent

variable the level(not the log) of cash (not total) compensation.

Thus,

relative toour standard

specification,we

run

this regressionin levelsand do

not includeVcilue ofoptions granted. Sinceprofitsarereportedin millions

and

pay

is reported in thousands, the coefficient of .17 incolmnn

(1) suggests that thatisa currentorformerofRcer ofthecompany.A

greydirectorisarelativeofacorporateofficer, orsomeonewho

hassubstantial businessrelationshipswiththe company.'*We do not report thecoefficientson age Jind tenureto savespace, butthey resemble theoil indxjstry findings: positivebutdiminishingeffectsoftenureand age.

SI,

000

increasein profitsleads toa

17 cent increase in performance.Column

(2) performs thesame

exercisebut

now

forpay

forluck:we

instrument forperformance

using theexchange

rateshocks.^'^As

in the oil case,we

finda

pay

for luck coefficient that is ofthesame

orderofmagnitude

as thepay

for generalperformance

coefficient.Columns

(3)through

(6)run

themore

standard regressionwhere

we

use the logarithm ofpay

and an

accountingmeasure

ofperformance

(operatingincome

dividedby

total assets). Incolumns

(3) BJid (4)

we

use only cash compensation, whileincolumns

(5)and

(6)we

usetotalcompensation.In

both

cases,we

find the sensitivity ofpay

to luck tobe

about

thesame

as the sensitivity ofpay

to a general shock.

When

accountingperformance

risesby

one

percentage pointcompensation

(either total or cash) rises

by about

2 percent,whether

that risewas

due

toluck—

exchange

ratemovements

—

or not.Colmnns

(7)through

(9) replicate these foiir colimansbut

formarket measures

ofperformance.Again,

we

findpay

for luckthatmatches

thepay

sensitivitytoa

generalshock.A

riseinshareholderwealth of

one

percentleads toa

riseinpay

(again either total or cash) ofabout

.3percentirrespectiveof

whether

this risewas

causedby

luck.Two

importantpoints shouldbe

takenaway

from

thispanel. First, toa

firstapproximation, theaverage firm rewards its

CEO

asmuch

for luck as itdoes

for a generaJmovement

in performance.There seems

tobe

verylittle ifany

filtering. Sincewe

use a totally different shock, these findingsaddresstheoreticalconcerns

about

the useofmean

industryshocks (suchasthoseraised inGibbons

and

Murphy

(1990)and

Aggaxwal and

Samwick

(1999b))and

shows

that the lack of filteringobserved in

RPE

findings generalizes to other sources ofluck.Second, there is as

much

pay

for luckon

totally discretionarycomponents

ofpay

(salaryjmd

^''Firststageregressionsarereportedin'RibleA2. In practice

we

use as instrumentsasetofdummy

variablesthat indicate any significantexchangerateappreciations ordepreciations in the currentand past year. The instruments arejointlyhighly significant.bonus) as there is

on

othercomponents

such as options granted.This

rules out the notion thatpay

for luckmight

arise because firmscommit

(implicitly or explicitly) to multi-year stock optionplans

where

thenumber

ofoptions grants is fixedahead

oftime.As

firm vaJues rise, the prices ofoptionsrise

and

so does the value of options grants (Hall, 1999).More

generally,bonus

is themost

subjective

component

ofpay

forperformance

sensitivity.To

findpay

forluckon

thiscomponent

isquite suggestive.

Boards

are rewardingCEOs

for luckeven

when

they could filterit.3.2.3

Mean

Industry

Movements

as

Measures

of

Luck

In Panel

B

ofTable 3,we

replicatePanel

A

except that ourmeasure

ofluckbecomes

mean

perfor-mance

of the industry,which

ismeant

to capture external shocks that are experiencedby

all thefirms in the industry.

More

specifically, asan

instrument for firm-level rate ofaccounting returnin a given year,

we

use the weighted average rate ofaccounting return in that year in the 2-digitindustrythatfirmbelongs to, excluding thefirmitself

from

the calculation.^^The

weightofa

givenfirmin

a

given year is theshare ofitstotal assets in the "total" total assets ofthe 2-digit industrythe firm belongs to. Similarly, as

an

instrument for firm-level logarithm of shareholder wealth ina

given year,we

use the weighted average of the log values ofshareholder wealth in the 2-digitindustryin that year, again excluding the firm itself

from

thecalculationand

using total assets toweight each individualfirra.^^

Like in Panel A, all regressions includefirm fixed eflFects

and

year fixed efiects.We

also controlfor a quadratic in

CEO

ageand

a

quadratic inCEO

tenure.The

regressions includemore

than

twice the

data

points ofPainelA

because

we

can

now

use all firms, not only those in the traded'*

We

also investigatedthe useof 1-digit and3-digltindustrymeansasinstrumentsandfoundqualitcitivelysimilar

results.

'^These mean industry performance measures are constructed from

COMPUSTAT.

To maximizeconsistency of theperformancemeasuresbetweenYermaclc'sfirmsandtherestof industry,we

alsocomputeshareholderwealthand incometo assets ratiosfromCOMPUSTAT

for the firmsinYermack's. Because notallfirms in Yermack'sdata aie presentinCOMPUSTAT

in everyyear, weloseabout 800 firm-yearobservations.goods

sector. PanelB

shows

a pattern quite similar to Panel A.The

pay

for luck relationship inall specifications again roughly

matches

thepay

for general performance. Besides reinforcing thefindings of Panel A, these latest findings suggest that previous

RPE

results arose probably notbecause of

miameasurement

ofthe reference industryor ofthe industryshockbut

because of truepay

for luck.3.2.4

Could

Pay

forLuck

Be

Optimal?

Sincethe resultsso far clearlyestablish

pay

for luck ora

lackofperformance

filtering, it is naturaltoask

whether pay

for luck could infactbe

optimal.Are

therecomplicationstothe agencymodel

that

would

generatepay

for luck inan

optimal

contract?We

could think ofat least three.First,

we

have

assumed

thato

is contractible. Ifocannotbe

contractedupon

ormeasured

well,the empiricaltesta developed in section 2.3 are

no

longer valid. In practice,we do

not believe thisis

important

formost

ofourfindings. First,it is difficultto believethat non-contractingissuescan

explain

our

resultsintheoU

industrycase study: theprice ofcrudeoilcan

easilybe measured

ajidwritten into a contract. Second, even inthe presenceof non-contractibility, subjective

performance

evaluationshould efl'ectively filter (seeBaker,

Gibbons and

Murphy,

1994).The

onlyproblem with

subjective

performance

evaluation relates tocommitment

issues,but

these are unlikely tobe

a

problem

for theboards

of directors ofthe large firmswe

study

here.Second,

we

have

neglected the possibility of indirect incentivesone

may

want

to provideto theCEO,

forexample

to forecast,respond

to, orhedge

against luck.^^This

kind ofargument can

be

most

readilyevaluated in ouroil industryapplication.Suppose

aparticularlytalentedCEO

in theoil industry

understood

the political subtleties oftheArab

countriesand

forecastedthecoming

of^'

An

argumentsimilar tohedging hasbeenmade

byDiamond

(1998). Tying paytoluckmay

generateincentives for theCEO

tochangehiscorrelationwith the luckvariable. In practice, diversificationwouldseem tobeintheinterestofmanagementandnotsheixeholders. Tiifano (1996),forexample,demonstratesthat managerialcharacteristics,such

the positive oil shock at the beginning of the 1980's.

By

increasingoutput from

existing oil wells,increasing inventories, or intensifyingsearchfor

new

wells, he couldhave

increased hisfirm's profitswhen

theshock

didcome.

Shouldn't shareholdersreward

thisfarsightedCEO?

The

important

pointhereis that those

CEOs

who

were

exceptionalinhaving

forecasted should indeedbe

rewarded.But

thisis not

what

we

testfor.We

usenone

ofthe firm to firm variation in responseto the oil shock.We

merely testwhether

the average firm experiences arise (orfall, for the negative shocks) in pay.Put

another

way, our results suggest thata

CEO

who

responds to theshock

exactly thesame

way

as every other oil

CEO

is rewarded.This

cannotbe

areward

forhaving

forecasted well. Again,one

may

want

toreward

CEOs

for exceptional responsiveness to shocks,but

there is little reasonto

reward

them

forjust average responsiveness.Third, the reservation utility ofthe

CEO

couldbe

affectedby

therandom

factor o.When

theoil industry enjoys

good

fortune, thehuman

capitalofoilCEOs

may

simply

become more

valuable.Firms then

pay

their oilCEOs

more

simply

tomatch

their increased outside options. Thus,pay

for luck is optimal here not as

an

incentive device, butmerely

becatise theoptimal

level ofpay

increases

with

luck.Some

objectionscan

be

raisedagainst thisview

aswell. First, it isunclearwhy

CEO

human

capitalshouldbecome

more

valuableasindustryfortunes rise. Forexample, itmay

be

exactlyin

bad

times thathaving

therightCEO

ismost

valuable.A

priori,eitherrelationshipseems

plausible. Second,

we

have found

some

evidence ofasjonmetries in the pay-for-luck relationship that arehard

to reconcilewith

thatview

(and easy to reconcilewith a

skimming

view)."Good

luck"

seems

tomatter

more

than

"bad

luck".For

example, averageCEO

compensation

in the oilindustry always goes

up when

the priceof crude oilgoesup

but

does not alwaj^ godown when

theprice of

crude

oil goesdown.

Also,when we

separate positiveand

negativemean

industry shocks,(whilethere are

no asymmetries

in the sensitivityofpay

to individual firm performance).^^Finally,

one might

argue thatpay

for luck is aform

ofrisksharingbetween

CEOs

ajidfirms. Iffirms are effectively risk averse,

perhaps

because of liquidity constraints, theymay

want

to sharesome

ofthe risks they facewith

theirCEO.

This

argument

is best evaluated in the context ofouroil industry study. It is

hard

to imaginewhy

the large oil producerswe

study,which

are usuallyawash

incashand

haveexcellentbond

ratings (perhapsbecause

largeholdingsofpledgeableassets),would need

to shareriskwith

theCEO.

Even

ifthese firmsneeded

to lay offrisk, theycan

readilytake futures positionsin oil

which would

allowthem

to shaxe theriskwith

amarket

better able totake

on

theriskthan

theCEO.

Similarly,exchange

rate futuresmarkets

areactive.Of

course,one

could argue that for

mean

industrymovements

futuresmarkets

may

notbe

as readily available.But

this explanationwould

then only apply to this third luck measure,whereas

our results holdsimilarly forall the measures.

While

we

have

providedarguments

against these variousextensions ofthesimpleagency

model,in the

end

we

stiU believe that they merit serious consideration.They

suggest to us that thepay

for luck findingdoes not per se ruleoutagency

models.We

dealwith

this issueby examining

how

corporategovernance affects

CEO

pay.3.3

The

Effect

of

Governance

The

skimming

view

makes a

further prediction. Since itemphasizes

theCEOs'

ability to gaincontrol ofthe

pay

process, corporate governance should playan

important

role inskimming.

It isexactly in the poorlygoverned firms

where

we

expectCEOs

tomost

easilygain control of thepay

process. This suggests that

we

should expectmore

pay

for luck in the poorlygoverned

firms.To

examine

how

pay

for luck differsbetween

welland

poorly governed firms,we

estimatetwo

'*Theseresults, notdirectlyreported here,aieavailableuponrequestfrom the authors. They holdquitestrongly

equations. First, in order toprovide

a

baseline,we

askhow

pay

forgeneralperformance

(not luck)differs

between

welland

poorly governed firms.We

estimatean

OLS

equation similar to equation(2) except that

we

allow thepay

forperformance

coefficient todepend

on

governance:Vit

=

ai+

at+

ax

*Xu

+

ao

*Govu

+

0*

perfu

+

7

*{Govu

*perfu}+

eu (6)where

Govu

is ameasure

ofgovernance.To

xmderstand

this equation,differentiateboth

sideswithrespect to perfu:

dperfit

The

sensitivity ofCEO

pay

toperformance depends on

thegovernance

variable.A

positive valuefor

7

would imply

that bettergoverned

firmsshow

greaterpay

for performance.Equation

(6) ofcourse tells usnothing about

pay

for luck,merely about pay

for performance.To

get atpay

for luck,we

re-estimate this equation using ourtwo

stage instrumental Vcuriablesprocediire.'^

We

then

compute

an

estimate of the effect ofgovernance

on

pay

for generalperfor-mance,

7

and

an

estimate ofthe effect ofgovernance

on

pay

for luck,^luck-Oiu- test

then

consists incomparing

7

and

jLuck-We

willspeak

ofmore

pay

for luck inpoorlygoverned firms

when

poorly governed firms displaymore pay

for luck relative topay

for generalperformance. Ifpoorly

governed

firmssimply gavemore pay

forperformance

and pay

for luck roseas

a

consequence,we

would

not refer to this asmore

pay

for luck. In practice,we

willsee that itis

pay

for luck that changeswith

governance, whilepay

forperformance

hardly changes.^"'Anextremelyimportantcaveathere: our approcich allowsforthepossibilitythat bettergovernedfirms

may

have adifferentresponsivenessofperformancetoluck. Technically, performance perfa, theendogenous variable we needtoinstrument,appearsbothdirectly andindirectly (theterm Govit*perfu) in this equation. ^Vhenwe instrument,

we perform two first stages, one for the direct effect perfu and one for the interaction term GotHt*ptrfu- This

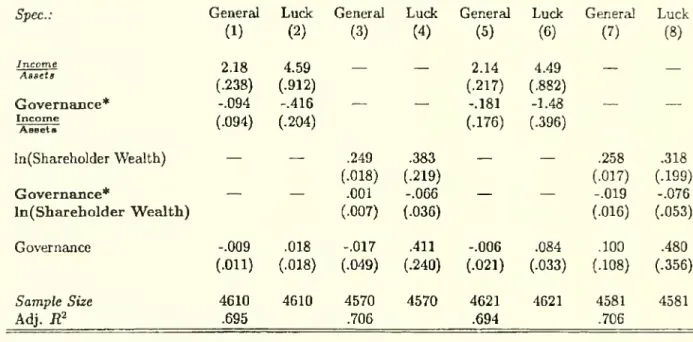

3.3.1

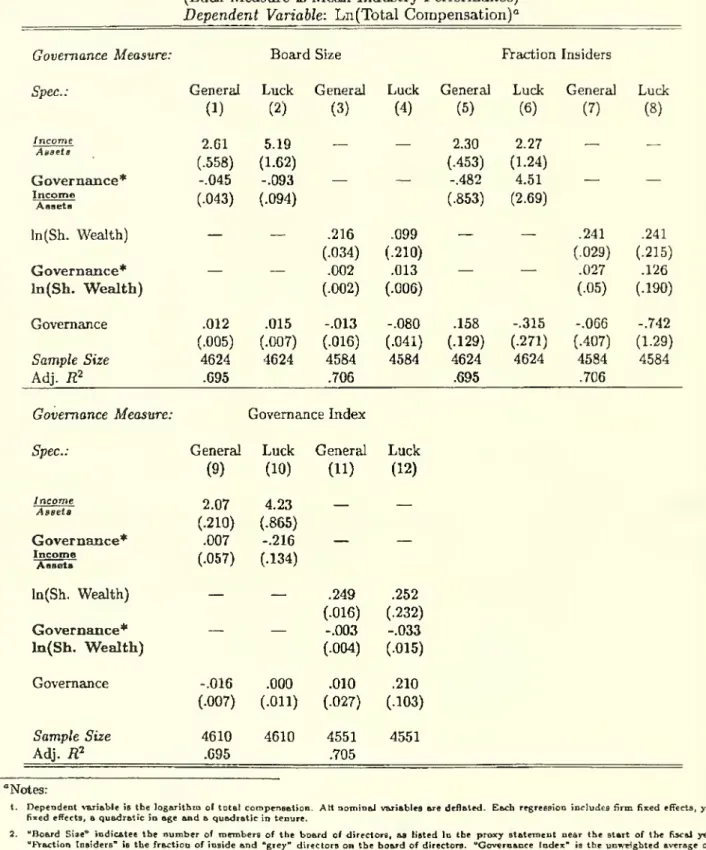

Large

Shareholders

In Table 4,

we

implement

thisframework

for the case of large shareholders.We

askwhether

thepresenceof large shareholdersaffects

pay

for luck. Shleiferand Vishny

(1986),among

others, arguethat large shareholders

improve

governance ina

firm.A

single investorwho

holds alarge block of shares ina

firm willhave

greater incentives towatch

over the firmthan

a dispersedgroup

ofsmallshareholders.'^ In our context, the idea oflarge shareholders fits

most

naturally as thismatches

our intiiition of "having a principal around."

Yermack

data

contains a variablewhich

counts thenimiber of individuals

who

own

blocks of at least 5 percent of the firm'scommon

shares.^^We

further

know

whether

these large shareholdersareon

theboard

or not.A

priori,one might

expectthat large shareholders

on

theboard have

the greatestimpact.They

can

exert their controlnotjustthrough

implicitpressureor voting, but alsowith

adirectvoiceon

thebocird. Sincetheinformationis available,

we

willconsider theeffectofboth

alllarge shareholdersand

of onlythoseon

theboard.The

first fourcolumns

of T^ble 4 useaU

large shareholders as ourmeasure

of governance.AU

regressions include the usual controls.Column

(1) estimateshow

the sensitivity ofpay

toperformance

depends

on governance

for accountingmeasures

ofperformance.The

firstrow

tellsus that afirmwithno

large shareholdersshows

asensitivityof logcompensation

toaccounting returnof 2.18.

An

increase in accounting return ofone

percentage point leads toan

increase inpay

ofabout two

percent.The

second

row

tells usthatadding a

large shareholder onlyweakly

decreasesthe sensitivity of

pay

to general performance,and

this effect is not statisticadly significant. Forexample,

a one

percentage pointincrease inaccounting retm^inow

leads to a2.09 percent increasein

pay

when

the fixm hasone

large shareholderand

nota

2.18 percent increase in pay.Colmnn

They alsopointout apossibleoppositeeffect: verylargeshareholders

may

have agreater ability toexpropriate rentsfor thenaselves. This effectislikely tobegreatest in othercountrieswhere investorprotectionisweakest.(2) estimates

how

large shareholders affectpay

for luck.^As

before, the firstrow

tells us thatthere is significant

pay

for luck.The

secondrow

here tells \is, however, that thispay

for luckdiminishes significantly inthe presence of a large shareholder.

A

one

percentage point increase inaccounting returns

due

to luck leads to roughly a4.6 percent increaseinpay

when

there isno

largeshareholder but only a 4.2 percent increase in

pay

when

thereisone

more

largeshareholder.Each

additional large shareholder decreases this effect

by

.4 percent.This

is a10%

drop

in thepay

forluck coefficient foreach additional large shareholder.

,/;

Columns

(3)and

(4) estimate thesame

regressions usingmarket measures

of performance.In this case, the

pay

for generalperformance

does notdepend

at aJlon

the existence of a largeshareholder (a coefficient of .001 with a

standard

errorof.007).We

again find, however, thatpay

for luck diminishes

with

the presence ofa

large shareholder.WhUe

the result is only significant atthe

10%

level, theeconomic

magnitude

islarger.The

pay

for luck coefficientnow

drops^

«

17%

for each large shareholder.

In

columns

(5)through

{8)we

repeat theabove

exercisebut

altering thegovernance

measure.We

now

focus onlyon

large shareholderson

the board.Comparing

columns

(6)and

(2),we

see that the

governance

effect strengthens significantlywith

respect to the filtering ofaccountingperformance.

We

see thatthepay

forluckdrops by

33 percentforeachadditional large shareholder.The

results are very statistically significant.On

market performance

measures,we

find the effect also risesbut

less dramatically. Incolumn

(8), thepay

for luck drops 23 percentwith each

largeshareholder

on

the board. Moreover, this last result is insignificant. Insummary,

our findings inTable 4 highlight

how

large shareholders (especially thoseon

the board) affect the extent ofpay

forluck.

Firms with

more

large shareholdersshow

farlesspay

for luck.*In all that follows, we will usemean industry performanceasotirmeasureofluck since this produces themost

3.3.2

Entrenchment and

Large Shareholders

The

results in Table4 simplycompare

firmswith

largeshareholders to firms without. Thisignoresthe effects of

CEO

tenure, anotherimportant determinant

of governance.A

common

beliefis thatCEOs

who

havebeen with

the firm longerhave

had

a chance tobecome

entrenched, perhapsby

appointing friends

on

the board. In this case,we

woxild expect high tenureCEOs

toshow

thegreatest

pay

for luck. Moreover,we

would

expect this effect tobe

strongest in those firmswhere

governance is

weak

and

thereisno

large shareholder present to limit the increased entrenchment.Hence, in the absence of large shareholders,

we

expect fairly stronggovernance

early in aCEO's

tenure but this

governance

shouldweaken

overtime

as he entrenches himself. In the presence oflarge shareholders,

we

not only expect stronger governcince but aJso that this strongergovernanceshoiddlast

throughout

theCEO's

tenure. It is harderfor aCEO

to begin stacking theboard

when

thereis

a

largeshareholder aroimd.Thus

we

expect ariseinpay

forluckwith

tenureintheabsenceofalarge shareholder,

but

lessof a rise (oreven

no

rise) in the presence ofa

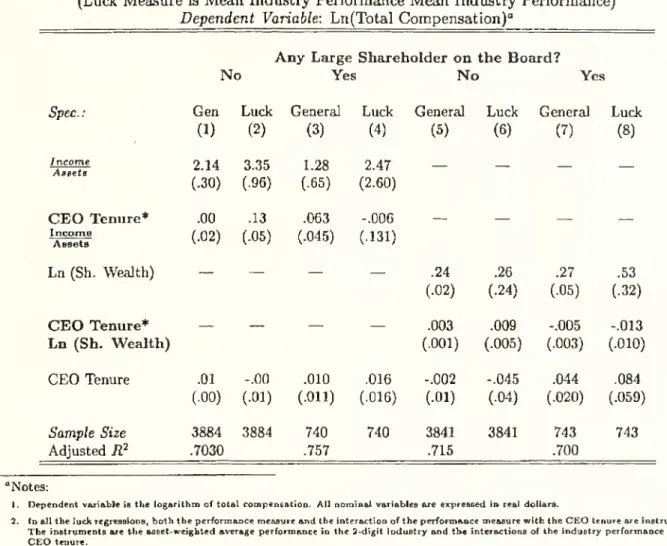

large shareholder.T^ble 5 tests this idea.

We

first sort firms intotwo

groupsbased on whether

theyhave

alargeshareholder present

on

the board.^^This

produces 740 or sodata

points forfirms with largeshareholders

and 3880

or sodata

pointsfor firmswithout

large shareholders. For each set,we

now

separatelyestimate regression 6 for these

two

groupswith

tenureasour governance

measure.Columns

(1)and

(2) focuson

accountingmeasures

ofperformance

in firms without a largeshareholder.

The

secondrow

tells us that while tenure does not affectpay

for performance, itgreatly increases

pay

for luck. In fact, aCEO

with

(roughly) themedian

teniure of 9 yearsshows

about

^5^

w

35%

greaterpay

for luckthan one

who

justbegan

at the firm. Let us contrast thiswith