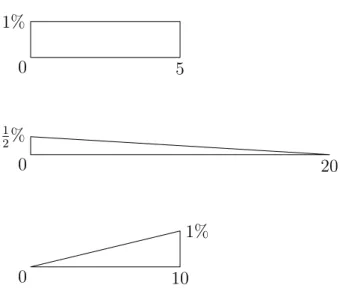

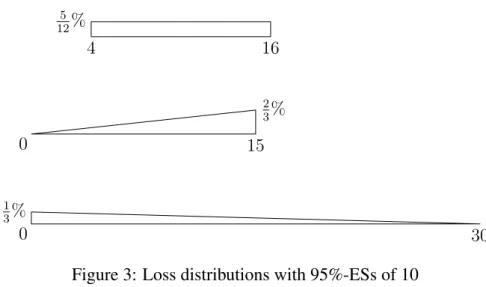

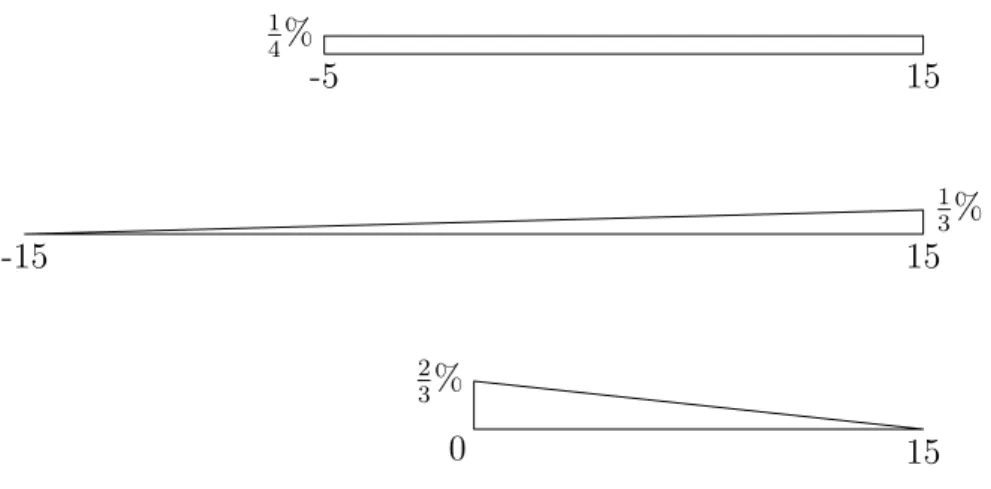

Viewing Risk Measures as information

Texte intégral

Figure

![Figure 1: The region of interest [c,d] in a loss pdf](https://thumb-eu.123doks.com/thumbv2/123doknet/13176344.390912/6.892.109.864.144.590/figure-region-c-d-loss-pdf.webp)

Documents relatifs

The second contribution of this paper is a characterization of the Lebesgue property for a monetary utility function U in terms of the corresponding Fenchel transform V introduced

The first set of experiments is designed to understand the impact of the model type (and hence of the cost function used to train the neural network), of network topology and

Nonparametric methods can naturally be used to estimate the distributions of the residuals and correct the biases in the volatility estimation (the issue of whether the scale factor

Our main interest is on extreme value theory based modes: we consider the unconditional GPD, the GARCH models, the conditional GPD, the historical simulation, filtered historical

Then, there are two natural ways to define a uniform infinite quadrangulation of the sphere: one as the local limit of uniform finite quadrangulations as their size goes to

Then, there are two natural ways to define a uniform infinite quadrangulation of the sphere: one as the local limit of uniform finite quadrangulations as their size goes to

To further understand the impact of PML and robust GARCH estimates on VaR predictions, we repeated the Monte Carlo simulation but for comparison and to regularize the

We will cover the section Darboux’s construction of Riemann’s integral in one variable faster than usual since you already know its material from MAT137. It will be easier if you