u

Digitized

by

the

Internet

Archive

in

2011

with

funding

from

Boston

Library

Consortium

Member

Libraries

i3i

Dewe

y

1415>3

Massachusetts

Institute

of

Technology

Department

of

Economics

Working

Paper

Series

A

DUAL

LIQUIDITY

MODEL

FOR

EMERGING

MARKETS

Ricardo

J.

Caballero

Arvind

Krishna

murthy

Working

Paper

02-03

June 2002

Room

E52-251

50

Memorial

Drive

Cambridge,

MA

02142

This

paper

can be downloaded

without

charge

from

the

Social

Science Research

Network

Paper

Collection at

http://papers.ssrn.com/abstract=

2971

7

iv\

Massachusetts

Institute

of

Technology

Department

of

Economics

Working

Paper

Series

A

DUAL

LIQUIDITY

MODEL

FOR

EMERGING

MARKETS

Ricardo

J.Caballero

Arvind

Krishnamurthy

WORKING

PAPER

02-03

January

2002

Room

E52-251

50

Memorial

Drive

Cambridge,

MA

02142

This

paper

can be

downloaded

without

charge

trom

the

Social

Science Research Network

Paper

Collection

at

http://papers.ssm.com/abstract=

XXXXX

MASSACHUSETTS INSI

OFTECHNOLOGY

MAR

7 2002

A

Dual

Liquidity

Model

for

Emerging

Markets

By

Ricardo

J.Caballero and Arvind

Krishnamurthy

1January

8, 2002The

last few years have seen a significant re-evaluation of themodels

used to analyzecrises inemergingmarkets. Recent

models

typically stress financial constraints or distortedfinancial incentives.

While

thiscertainlyrepresentsprogress, thesemodels

share aweakness with the earlier work: neither is uniquely about emerging markets. Adaptations of theMundell-Fleming

model

represent Argentina as aBelgium

with larger external shocks.Likewise, emerging

market models

of financial constraints are adaptations of developedeconomy

ones with tighter financial constraints.In our work,

we

have advocated amodel which

distinguishesbetween

the financialconstraints affecting borrowing

and

lendingamong

agents withinan

emerging economy,and

those affecting borrowing from foreign lenders (Caballeroand

Krishnamurthy

2001a,b, c). Financial claims

on

future flows that canbe

sold to foreignand

domestic lendersalikearelabeled international liquidity,while those that canbesoldsolelytootherdomestic

agents are labeled domestic liquidity.

Belgium

inourmodel

is a countrywhere

most

claimsare international liquidity, while Argentina is a country

where

most

claims are domesticliquidity.

The

dual liquiditymodel

offers a parsimonious description of the behavior of firms, governments,and

asset prices during financial crises. It also provides prescriptions for optimal policy responses to these crises. This paper presents a simple sketch ofour ideasin a

framework

akin to theMundell-Fleming

model.The

graphical analysis allows us topose a rich array of questions

and

illustrateshow

our answers differfrom

standard ones.The

welfare statementswe

make

below holdup

in specifications that are tighter than themodel

we

deploy (see Caballeroand Krishnamurthy

2001d).I

International

liquidity,

domestic

liquidity,

and

crises

Let us simplify matters at the outset

and assume

that all private investmentand

publicexpenditure has to be financed from abroad.

That

is,I

+

G

=

CF

where

/ is domestic investment,G

isgovernment

expenditures,and

CF

is net capital inflows.The

simplification highlights the impact ofexternal shockson

investment.Respectively:

MIT

andNBER;

Northwestern University. E-mails: [email protected],We

are grateful to GuidoLorenzoni andJaumeVenturafor theirThere

aretwo

central assumptions in ouranalysis.The

first one regulates the country'saccess to internationalfinancial markets,

and

thesecond one determines the functioning ofdomestic financial markets:

•

An

external crisis is a situationwhere

CF

is notenough

toimplement

the desiredlevelsofI

+

G.We

assume

that at thetimeof the crisis, claimson

some

specialfuturecash flows ("internationalliquidity") isallthat can besold to foreigners.

The

countryhas a stock of international liquidity given

by

IL,and

we

requirethat,CF

<

IL, sothat

I

+

G

<

IL.Loans

backedby

international liquidityare at the international dollar-rate oil*.

•

Not

all of the country's international liquidity is in thehands

ofthose that use it inreal investment.

The

latter need toborrow

some

ofthe international liquidityfrom

other domestic agents. Their domestic liquidity or net worth,

DL,

regulates theirborrowing

from

otherdomestic agents.DL

includes marketable domestic assets, such as real estateand

domestic financial assets.We

assume

thatDL

is a decreasingfunction ofip, the domestic peso-interest rate.

2,3

Let id denote the interest rate faced

by

a firmwhen

borrowing dollars (internationalliquidity)

from

otherdomestic agents.As we

will see,this ratewill generallybe higherthan

Zq during a crisis.

Under

these assumptions, firms' investment is a decreasing function ofidand

V

. Sincefirms need to

borrow

dollars to finance investment,and

id is the dollar-cost-of-capital, arise in id lowers investment. Tighter

monetary

policy—

that is, an increase inzp—

causesDL

to fall, constraining firms ability to borrow:Taking

ipand

G

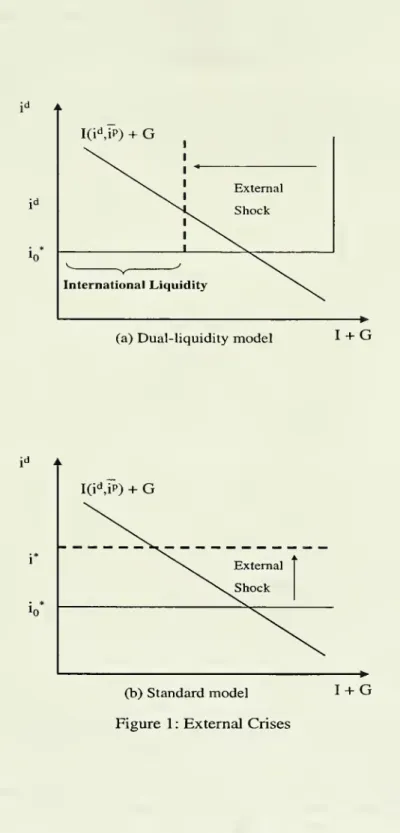

as given for now, Figure la illustrates ourmodeling

of crises.On

the horizontal axis is aggregate investment plus

government

expenditure.The

limitedinternationalliquidityofthe countryisrepresented

by

the reversed-Lshaped

supplycurve.A

crisis isan

eventwhen

the quantity of internationalliquidityislowrelativeto investmentneeds.

An

external shock decreases the available international liquidity,moving

supply tothedashed line

and

reducing aggregate investment.I(id,iP)

+

G

=

IL. (1) 2See Caballero and Krishnamurthy (2001d) fora modelconnecting domesticliquidity, monetary policy,

andinvestment.

3

Ben Bernanke and AlanBlinder (1988) alsooutline amodel in which there are twoformsofliquidity: bonds and bank-loans. Howeverin their case the twoliquiditiesare substitutes. In contrast, inour model

there isahierarchy: IL isultimatelywhatisneededfor investment, while

DL

servesonly toaggregate theIn this crisis equilibrium, domestic firms finance investment

by

selling their domesticallyliquid assets in exchange for international liquidity.

The

price ofthe limited internationalliquidity (id)risesaboveij$ toclearthemarket. Foreigninvestors

do

not arbitrage thediffer-enceofid

—

Iq because theyareunwilling toexchangeinternational liquidityfordomesticallyliquid assets.

In contrast, the lower panel represents astandard modeling ofcrises.

The

usualsmall-open-economy

assumptionmeans

that the supply of dollars is elastic at the internationalinterest rate.

The

externalshockisariseintheinterestrate (orriskpremium)

thatraisesidfrom

Iqto thedashed

line(i*). Since theinterest rateon borrowingdollars rises, investmentfalls.

While

foran appropriaterescalingthe externalshockleads tothesame

equilibriumlevelsofid

and

/ than in the dual liquidity economy, the fact that the supply of internationalfundsis inelastic at the equilibrium point inthe latter hasimportant ramificationsfor

what

follows.

II

Domestic

interest

parity

condition

Letus

now

seehow

idaffectsdomesticasset prices. Considerthemarginaldomesticinvestorinthecrisis equilibrium ofFigure lawith aunit of international liquidity (say, one dollar).

There

aretwo

options available to the agent.The

first is to lend this to a domestic firmand

earn interest at the rate ofid one period hence.The

second is to convert the dollar into pesos, at the exchange rate of eand

invest these pesos in a domesticbond

to earn interest ofip. Fixingthe future exchange rate ate,and

since the agentmust be

indifferentin equilibrium

between

thetwo

strategies,we

obtain adomestic interest parity condition:e

Rewriting

and

dropping the higher order term,we

arrive at:i

d

^i

p+

e, (2)

where

e=

e/e—

1, is the expected appreciation of the domestic currency.A

rise inid, asin the external shockofFigure la, causes theexchange rate to depreciate inorder to yield

an

expected appreciation. Alternatively, themonetary

authoritymay

defend the currencyby

raising thedomestic interest rate ofip.If

we

replace thedomesticbond

in the previousargument

with any (only) domesticallyliquid asset, then the rise in id will result in the dollar-price of that asset to fall.

The

model

thus provides a simple account ofthefall in domestic asset pricesand

exchangeratedepreciations

accompanying

external crises.It is also

worth

noting that the fall in domestic asset prices isdue

to an aggregateshortage of international liquidity, as

opposed

to aproblem

of domestic assets - i.e. theprice of real estate falls not because real estate will generate less revenues in the future,

id , I(idJp)

+

G

External id Shock ; * J v ^\.

•y ^v InternationalLiquidity(a)Dual-liquidity

model

I+

G

(b)Standard

model

I+

G

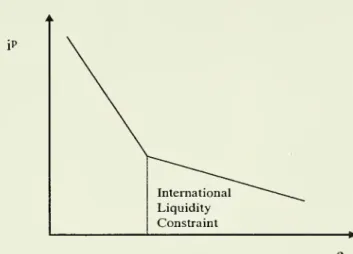

Ill

LM

curve

and

Equilibrium

The

peso-interest rate ip is determinedby

a (nearly) conventionalLM

curve,L(ip,I

+

G)

=

M,

(3)where

we

have used nominalmoney

stockon

the right-hand-side, asopposed

to^

or^.

Using realmoney

stock does lead tosome

interesting issueswhen

the centralbank

post-crisis inflation target is not credible (see Caballero

and

Krishnamurthy, 2001d). But, forpresent purposes, it onlycomplicates the analysis.

iP

M

International Liquidity Constraint I+

G

Figure 2:EquilibriumFigure 2 depicts the equilibrium of (1)

and

(3).The

curve IS' corresponds to a casewhere

international liquidity isnot scarce, while thedual liquiditymodel

is represented by75.

The

international liquidity is constrained in the verticalsegment

oftheIS

curve,and

I

+

G

is determinedby

IL

asopposed

to ip. Figure 2 along with Figure la describe theequilibrium of (I

+

G,id,ip).Combined

with (2), this also describes the exchange rate.IV

Monetary

policy

From

theIS' curvewe

notethestandard effectofmonetary

policyinmodels

with financialconstraints.

An

expansionin money, shiftsout theLM

curve, loweringip.The

latter raisesfirms' net

worth and

thereby relaxes their domestic financial constraintand

facilitatesinvestment.

In our modeling of crises (IS), this logic does not apply.

Monetary

policy hasno

contemporaneous

effecton

investment. This is becausewe

assumed

that at the aggregateIf

we

imagine an experimentwhere

we

increased theDL

of a single firm, holding allother firm's

DL

fixed, it willbe

true that this firm's investment will raise.The

firm willsell its extra

DL

forsome

IL

and

thereby increase its real investment. However, loweringiv has the effect ofincreasing all firm's

DL.

Since in aggregateIL

is fixed, this action willonlybid

up

the domestic price of international liquidity. It will shiftup

theI(i ,rP) curvein Figure la,

and

raise id.iP

International Liquidity

Constraint

Figure 3: Interest

and

Exchange

RateFigure3illustratesthe

impact

ofmonetary

policyonexchange

rates inourmodel. First,from

(2), loweringip whileholdingid fixedleads tothestandardexchange

ratedepreciation.This is the first

segment

in thedownward-sloping

curve. However, in our model,when

IL

is constrained, lowering ip also causes id to rise. This shift in the domestic interest-parity

condition reinforces the

exchange

rate depreciation.Thus

thecurvebecomes

flatterat thispoint (the second segment). 4

These

last observations lead toan

insight regardingmonetary

policy: If ratherthan

expanding, the central

bank

tightensmonetary

policy during a crisis, it does not reduceinvestment further, but it does alleviate the exchange rate depreciation that a crisis-high

id

would

bring about. If themonetary

authority is at all concerned about meetingan

exchange

rate/inflation target, it will tend to tightenmonetary

policy duringacrisis.Thus

our

model

rationalizes "fear offloating" as apositivedescription of centralbanks

behavior inemerging

markets (see Guillermo Calvoand

Carmen

Reinhart, 2000).4

An

interesting detour isobtained ifwe write the international liquidity constraint asI+

G

=

IL(e).Thisis the casewheredevaluations

may

increaseexportsthatcountas internationalliquidity. Inthiscase,loosening monetary policy depreciates the exchange rate and increases output, via relaxing the external

constraint.

On

the other hand, onemay

also believe thatDL

is decreasing in e, perhaps because firm'shave asubstantial amountof dollar debt, sothat devaluations decrease their networth. Inthis case, the

opposite conclusion

may

obtainifthe decline inDL

is sharpenough sothat the countryendsup wasting aggregateinternational liquidity (seeCaballero and Krishnamurthy2001b).V

Fiscal

policy

The

model's implication for fiscal policy are alsoworth

highlighting. In the standardMundell-Fleming

setup, an expansionaryfiscal policy (right-shift inIS') raisesipand

intheprocess partially crowds out I.

The

rise in the peso-interest rate appreciates the exchangerate.

In the dual liquidity economy, fiscal policy

competes

with the private sector forinter-national liquidity,

and

sinceIL

is fixed it crowds out private investment one-for-one.An

expansionary fiscal policy has

no

effecton

the vertical part ofIS.The

competition forIL

raises id rather than ip.As

a result, the domestic interest parity condition shiftsfrom

the(new) kink to the right

and

causes a depreciation ofthe exchange rate (see Figure 4).iP

Figure4:

Expansionary

FiscalPolicyThe

differences areeven starkerin afixed exchange rate regime. Inthestandard model,fiscal policy is potent because it is reinforced

by

anendogenous

expansion inmonetary

policy:

The

rise in ip tends to appreciate the exchange rate,which

is offset onlyby

amonetary

expansion. In contrast, in the dual liquiditymodel

the exchange rate tends todepreciate as aresult ofthe fiscal expansion sinceid rises,

and

hencemonetary

policywillhaveto tighten topreservethe peg.

VI

Overborrowing

and

Ex-ante

Policy

Options

During

acrisis, the stock ofIL

fullydetermines investment. Let us imagine shifting priortothe crisis, to apoint in time

where

privateand

centralbank

actionsmay

influence thisstock.

We

will discusstwo

actions thatmay

affect IL: private external borrowing,and

centralbank

reserve accumulation. DefineILq

as the initial international liquidity,Do

asrateto one,

we

haveIL

=

ILq

-

D

+

R

-A

private agent contemplating takingonsome

external debtand

importinggoods

facesa tradeoff: Importing

goods

increasesconsumption

or investment today, but reducesIL

thatwould

otherwiserelax theaggregateinvestment constraintduringthecrisis.The

agentvalues thelatter benefit atid.

We

haveshown

elsewhere (see Caballeroand

Krishnamurthy,2001a) that

when

domestic financial markets are underdeveloped there is an externality-akin to a free-rider

problem - whereby

themarket

value of this benefit, id, is less than itssocial value. In this circumstance, the private sector overborrows

and

arrives at a crisiswith too little IL.

There

arethree basic instruments at the Central Bank's disposal to offsetthe tendencyofthe private sector. First, it can increase foreign reserves (Rq)

and

thereby increase IL.Our

model

provides a natural motivation forboth

centralized holding ofreserves, as wellholding

them

in theform

of international liquidity.One

concern here is that, insome

circumstances, increasing

Ro

may

in turn exacerbate the external overborrowingproblem

and

raiseDo

(see Caballeroand

Krishnamurthy

2001c). Second, it can tax capital inflowsand

directlyreduce Do, so as to increaseIL.Of

course, taxesmay

leadtootherdistortions.Third,

and

most

interestingly, it cancommit

to expandmonetary

policy during the crisis—

just the opposite as it will be inclined todo

during the crisis. Since loweringip duringthe crisis raises id, it increases the private sector's valuation of

IL

and

alters the privateReferences

[1] Bernanke,

Ben

and Alan

Blinder, "Credit,Money

and

AggregateDemand,"

American

Economic

Review,May

1988, 75(2), pp. 435-439.[2] Caballero, Ricardo

and

Arvind Krishnamurthy. "Internationaland Domestic

CollateralConstraints in a

Model

ofEmerging Market

Crises," JournalofMonetary

Economics.December

2001a, 48(3), pp. 513-548.[3] Caballero, Ricardo

and

Arvind Krishnamurthy, "Excessive Dollar Debt: FinancialDevelopment and

Underinsurance."Mimeo,

MIT,

2001b.[4] Caballero, Ricardo

and Arvind

Krishnamurthy. "International Liquidity Illusion:On

the Risks ofSterilization."

Mimeo,

MIT,

2001c.[5] Caballero, Ricardo

and

Arvind Krishnamurthy."A

Vertical Analysis ofCentralBank

Interventions

During

Crises."Mimeo, MIT.,

2001d.[6] Calvo, Guillermo,

and

Carmen

Reinhart. "Fear of Floating."Mimeo,

University ofDate

Due

^M/m

MIT LIBRARIES