MIT LIBRARIES

3 9080 02618 3548

ttto

*

/

\

*

LIBRARIES

Digitized

by

the

Internet

Archive

in

2011

with

funding

from

Boston

Library

Consortium

Member

Libraries

HB31

/j-..M415

i*^t%\

4-5

2.oo5>

Massachusetts

Institute

of

Technology

Department

of

Economics

Working

Paper

Series

ANNUITIES

AND

INDIVIDUAL

WELFARE

Thomas

Davidoff

Jeffrey

Brown

Peter

Diamond

Working

Paper

03-1

5

May

7,2003

Revised:

March

17,2005

Room

E52-251

50

Memorial

Drive

Cambridge,

MA

021

42

This

paper can

be

downloaded

without

charge from

the

Social

Science

Research Network Paper

Collection atMASSACHUSETTS

INSTITUTE OFTECHNOLOGY

APR

2 6AW5

Annuities

and

Individual

Welfare

March

17,2005

Abstract: Advancing annuity demandtheory,wepresentsufficientconditions forthe optimalityoffull

annuiti-zationundermarket completenessthat are substantiallylessrestrictivethanthoseusedbyYaari (1965).

We

examine demand withmarket incompleteness, finding that positive annuitization remains optimalwidely, but complete an-nuitization doesnot.How

uninsured medical expensesaffect demandfor illiquidannuitiesdepends critically onthe timingoftherisk.A

newset ofcalculationswith optimalconsumptiontrajectoriesverydifferent fromavailableannu-ity income streamsstillshowsa preferencefor considerable annuitization,suggesting that limited annuity purchases are plausiblydueto psychologicalor behavioralbiases. (JEL Dll,D91, E21, H55, J14, J26)

Since the seminal contribution ofYaari (1965)

on

the theory ofa life-cycleconsumer

with anunknown

date ofdeath, annuities have played a central role in economic theory. His widely citedresultisthatcertainconsumersshouldfullyannuitizealloftheirsavings. However, theseconsumers were

assumed

tosatisfy severalveryrestrictiveassumptions: theywerevon

Neumann-Morgenstern

expected utilitymaximizers withintertemporally separableutility, they faced no uncertainty other than time of death, they

had no

bequest motive,and

the annuities available for purchase were actuariallyfair. While thesubsequent literatureon annuitieshas occasionally relaxed one ortwo ofthese assumptions, the "industry standard" is to maintain

most

ofthese conditions. In particular,theliterature has universally retainedexpected utility and additive separability, the latter

dubbed

"not a very

happy

assumption" byYaari.While

Yaari (1965)and

Bernheim

(1987a,1987b) provideintuitive explanations of

why

the Yaari resultmay

notdepend on

these strict assumptions, thegenerality ofthisresult has not been formally

shown

in theliterature.The

first contribution of this paper isto present sufficient conditions substantiallyweaker thanthose imposed by Yaari under which full annuitization is optimal.

The

heart of theargument

can be seen by comparing a one- year

bank

certificate of deposit (CD), paying an interest rate rto a security that pays a higher interest rate at the end of the year conditional

on

living, but pays nothing if you die before year-end. If you attach no value to wealth after death, then the second, annuitized, alternative is a dominant asset. This simplecomparison ofotherwise matchingassets,

when

articulated in a setting that confirms its relevance, lies behind the Yaari result.The

dominance

comparison ofmatching assets is not sensitive to their financial details, but does relyon theidentical liquidity inthe annuitized and non-annuitized assets.

This paper explores the implications of this comparison forasset

demand

in different settings,including both

Arrow-Debreu

complete marketsand

incomplete market settings. In theArrow-Debreu

complete market setting, sufficient conditions for full annuitizationto be optimal are that consumers havenobequestmotiveand

thatannuitiespayarate ofreturntosurvivinginvestors, netofadministrative costs, that is greaterthanthe return

on

conventional assetsofmatchingfinancial risk. Thus,when

marketsarecomplete, fullannuitization isoptimalwithout assumingexponential discounting, the expected utility axioms, intertemporal separability, or actuarially fair annuities.We

also relate thesizeof the welfare gain tothe trajectory ofoptimal consumption.A

second contribution is toexamine

annuitydemand

insome

incomplete market settings. Ifsome

desired consumption paths are not availablewhen

all wealth is annuitized in an incomplete annuity market, full annuitizationmay

no longerbe optimal. For example, ifan individualdesiresasteeply

downward

slopingconsumptionpath, butonly constant real annuities are available, thenfull annuitization is no longer optimal. Thus,

we

explore conditions for theoptimum

to includepartial annuitization.

We

also consider partial annuitization with a bequest motive.Another example involves the relative liquidity of annuities

and bonds

inthe absence of insur-ance for medicalexpenditure shocks.The

effect on annuitydemand

depends on thetiming oftherisk.

An

uninsurablerisk early inlifemay

reduce the valueofannuities if itisnot possibletosellor borrowagainst futurepayments

ofthe fixed annuitystream but it is possible to do sowithbonds.Incontrast, loss of insurabilityofa shockoccurring later in life

may

increase annuitypurchases asa substitute for medical insurance that has an inherent annuity character. Thus, an annuity can be a bettersubstitute than a

bond

for long-termcare insurance.Most

practical questions about annuitization (e.g., the appropriate role ofannuities in public pension systems) are concerned with partial annuitization.The

general theory itselfis insufficient to answer questions about the optimal fraction of annuitized wealth, and thus a large simulationliteraturehas developed.

Our

third contribution is to extend the simulation literature by creating anew

"stresstest" ofannuityvaluation.We

dosoby

generatingoptimal consumption trajectoriesthat differ substantially from

what

is offered by a fixed real annuity contract, and showing that evenunder these highlyunfavorable conditions, themajorityofwealthis stilloptimallyannuitized.allowa person'sutility to

depend on

how

present consumption compares to astandardof livingto which the individual hasbecome

accustomed, which is itselfa function ofpast consumption.We

model

this "internal habit" as inDiamond

and Mirrlees (2000).1These results imply that annuities are quite valuable to utility maximizing consumers, even under conditions that result in a very unfavorable

mismatch

between available annuity income streamsand

one's desired consumption path. Thus, while incomplete markets,when

combined

with preferences for consumption paths that deviate substantially from those offered by current annuityproducts, can certainly explain the lack offull annuitization, it is difficult to explain the near universal lack of any annuitization outside of Social Security

and

defined benefit pensionsplans, at least at the higher end ofthe wealth distribution

where

SocialSecurity is a small part ofone'sportfolio

and

SSI is not relevant. This findingis strongly reminiscent oftheliterature on lifeinsurance, which is a closelyrelated product.2

The

literatureon

life insurance hasdocumented

asevere

mismatch

betweenlife insurance holdings ofmost

householdsand

their underlying financial vulnerabilities (see e.g. Bernheim, Forni, Gokhaleand

Kotlikoff (2003);Auerbach and

Kotlikoff(1987),

Auerbach and

Kotlikoff (1991)). Thesepapers, takentogether, are suggestiveofpsycholog-ical or behavioral considerations at play in the market for life-contingent products that have not

yet beenincorporated intostandard economicmodels.

The

focus of the paper is on the properties of annuitydemand

in different market settings.We

do not address themore

complex equilibrium question ofwhat

determines the set ofannuityproducts in the market. In light of the value of annuities to consumers in standard models,

we

think examination of equilibrium would have to include the supply response to

demand

behavior that is not consistent with standard utility maximization.We

do not develop such a behavioral theory ofannuitydemand,

but ratherclarifythemismatch between

observeddemand

behaviorand

the value ofannuitizationin astandard utility maximizationsetting.

The

paper proceeds as follows: In section I,we

provide a general set of sufficient conditions under which full annuitization is optimal under complete markets. Section II discusses ofwhy

1

DifTerent models ofintertemporaldependencein utility arcdiscussed in, forexample, Dusenberry (1949), Abel

(1990), Constantinides (1990), Deaton (1991), Campbell and Cochrane (1999), Campbell (2002) and Gomes and

Michaelides (2003).

"AsdiscussedbyYaari (1965) and Bernheim (1991), thepurchaseofapurelifeinsurance policycan be viewed as

full annuitization

may

no

longerbe optimal with incomplete markets, payingparticular attention to the role of illiquidity of annuities. Section III briefly discusses a bequest motive. In SectionIV

we

report simulation results reflecting the quantitative importance of market incompletenesswith habit formation, showing that even

when

the liquidity constraints on annuities are binding,individuals still prefer a high levelofannuitization. Section

V

concludes.I.

Complete Markets

Much

ofthe focus ofthe annuities literature has been an attempt to reconcileYaari's (1965) "fullannuitization" result with the empirical fact that few people voluntarily annuitize any of their private savings.3 This issue is of theoretical interest because it bears

upon

the issue ofhow

tomodel

consumer behavior in the presence of uncertainty. It is also of policy interest because ofthe shift in the

US

from

defined benefit plans, which typically pay out as an annuity, to defined contribution plans that rarely offer retirees directlythe opportunity to annuitize. Annuitization isalsoimportant in the debate about publiclyprovided defined contribution plans.

Thissection derivesa generalsetofconditionsunderwhichfullannuitizationisoptimal, relaxing

many

ofthe assumptions in the original Yaari formulation.We

begin with a simpletwo

periodmodel, and then

show

formally the generalization tomany

periods andmany

states.A. The Optimality ofFull Annuitization in a

Two

PeriodModel

withNo

Aggregate UncertaintyAnalysis ofintertemporal choiceis greatly simplifiedifresource allocationdecisions are

made

com-pletely and all at once, that is, without additional, later trades.

Consumers

will be willing tocommit

to a fixed plan of expenditures if, at thestart oftime, theyare able to trade goods acrossall time and allstates of nature, as is standard in the complete market

Arrow-Debreu

model. Yaari considered annuitizationina continuous time settingwhere consumers areuncertain only about the dateofdeath.Some

results, however, canbe seenmore

simplyby dividingtime intotwo discrete periods: the present, period 1,when

theconsumer

is definitely aliveand

period 2,when

3

This assertion is consistent with the large market forwhat are called variable annuities since these insurance

products do not include a commitment to annuitize accumulations, nor does there appear to be much voluntary annuitization. SeeforexampleBrown andWarshawsky (2001).

the

consumer

is alive with probability 1-

q.4By

wiltingU

=

U(ci,C2),we

allow for a very general formulation of utility in a two-periodsetting with the assumptions that there is no bequest motive

and

that only survival to period 2 isuncertain. Lifetimeutilityisdefined overfirstperiodconsumption, c\,

and

consumptioninthe eventthat the

consumer

is alive in period 2, C2-We

drop the requirement ofintertemporal separability,allowing for the possibility that the utility from second-period consumption

may

depend

on thelevel offirst period consumption. Additionally, thisformulation does not require that preferences

satisfy the axioms for

U

to be an expected value.The

optimal consumption decisionand

the welfare evaluation of annuities can be determinedusing a dual approach: minimizing expenditures subject to attaining at least a given level of

utility.

We

measure

expenditures in units offirst period consumption.Assume

that there aretwosecurities available.

The

first is abond

that returnsRb

units ofconsumption inperiod 2, whetherthe

consumer

is alive or not, in exchange for each unit ofthe consumptiongood

in period 1.The

secondis an annuity that returns

Ra

in period 2 iftheconsumer

is aliveand

nothingotherwise.An

actuariallyfair annuitywould

yieldRa

=

i?s/(l—

g). Adverseselectionand

highertransac-tion costs forpaying annuities thanforpaying

bonds

may

drive returns belowthis level. However, because anyconsumer

will haveapositiveprobability ofdyingbetweennow

and

anyfutureperiod,therebyrelieving borrowers' obligation,

we make

theweak

assumption thatRa >

Rb-

5If

we

denoteby

A

savings in theform ofannuitiesand by

B

savings in the formofbonds,and

if there is no other income in period 2 (e.g., the individual is retired), then C2= RaA +

RbB,

and expenditures for lifetime consumption are simply

E

=

ci+ A +

B. Thus, the expenditureminimization problem can be written as:

min

ci+A +

BsX.U(cx,R

A

A

+

R

B

B)>U.

(1) cx,A,BWe

further imposethe constraint thatB

>

0, i.e., that the individual not be permitted to dieindebt. Otherwise with

Ra >

Rb,

purchasing annuitiesand

sellingbonds

in equalnumbers

wouldA

two period model with asingleconsumergood ineach datedevent precludes tradeafter thefirst period, butin a complete marketsetting,thisis irrelevant.

5

That

Rb

< Ra <

Rb/(1 —<?) is supported empirically by Mitchell et al (1999). If the first inequality werecost nothing

and

yieldpositiveconsumptionwhen

alive inperiod2,but leavea debtifdead, leavinglenders with expected financial losses in total.

This setup leads immediately to the optimality of full annuitization. If

B

>

0, then one isable to reduceexpenditures, whileholding the consumption vector fixed,

by

sellingRa/Rb

ofthebond and

purchasing one unit ofthe annuity (noting thatR& >

Rb)- Thus, the solution to thisexpenditureminimizationproblemisto set

B

=

0,i.e.,toannuitize one'swealthfully.The

intuitionis that allowing individuals to substitute annuities for conventional assets yields an arbitrage-like

gain

when

the individual placesno

valueon

wealthwhen

not alive.Such

a gain enhances welfare independentofassumptions aboutpreferencesbeyond

thelackofutility froma bequest.Nor must

annuities beactuariallyfair. Indeed, all thatisrequiredis forconsumerstohave

no

bequestmotive and forthe payouts from theannuity to exceed that ofconventional assets forthe survivor.Equation (1) alsoindicates an approachtoevaluatingthe gainfrom

an

increasedopportunityto annuitize. Consider theminimization underthe further constraintofanupperbound

on purchasesof annuities,

A

<

A

.We

know

that utility-maximizing consumers will take advantage of anarbitrage-like opportunity to annuitize as long as

bond

holdings are positiveand

can therefore be used tofinancethe purchase.With

no annuitiesavailable,bond

holdingswill be positiveifsecond-period consumption is positive, as is ensured

by

the plausible condition that zero consumption isextremely bad:

ASSUMPTION

1:limCt-+o

dU/dct

—

oo : t—

1,2

Allowingconsumerspreviously unableto annuitize anywealth to place a small

amount

of theirsavings into annuities (increasing

A

fromzero) leaves secondperiodconsumptionunchanged

(sincethe cost of the marginal second-period consumption is unchanged, so too, is the optimal level of consumption in bothperiods).

Thus

a small increase inA

from zeroreduces the cost of achievinga givenlevel ofutility by 1

—

(Ra)/{Rb)

<

0. This isthe welfaregain fromincreasing thelimit on available annuities foran optimizingconsumer

with positivebond

holdings.6Iftheupper

bound

constrainton availableannuitiesislargeenough

thatbond

holdingsarezero,thenthepriceofmarginalsecond period consumption (uptoA) fallsfrom 1/(Rb) to \/{Ra).

With

a fallinthecost ofmarginalsecond-period consumption, its

compensated

level will rise.Thus

the welfare gain from unlimited annuity availability ismade

up

oftwo parts.One

part is the savings while financing thesame

consumption bundle aswhen

there is no annuitization,and

the secondis the savings from adapting the consumption bundle to the change in prices.

We

canmeasure

the welfare gainin going from

no

annuitiesto potentiallyunlimited annuities from theexpenditure function defined over the price vector (l,p2)and

the utility level U. Integrating the derivative ofthe expenditure function evaluated at the two prices

1/Ra

and

1/Rb'-rl/RB

E\A=0

-

E\A=00=

E(l,1/R

B

,U)

-

£7(1, 1/Ra,U)

=

-

c2(p2)dp2, (2)Jl/RA

wherec2(p2) is

compensated

demand

arisingfrom

minimization ofexpenditures equal to c\+

c2p

2subject to the utility constraint without a distinction between asset types.

Consumers

who

savemore

(havelargersecond-periodconsumption)benefitmore

fromtheabilitytoannuitize completely.B. The Optimality ofFull Annuitization with

Many

Periodsand

Many

StatesWhile

a two-periodmodel

with no uncertainty other than length of life has a clarity that derivesfromitssimplicity, realconsumersface a

more

complicated decision setting. Inparticular,theyfacemany

periods of potential consumptionand

each periodmay

haveseveralpossible states ofnature.For example, a 65 year-old

consumer

hassome

probability ofsurvivingto be a healthyand

active80 year-old,

some

chance offinding herself sickand

ina nursinghome

at age 80,and some

chance ofnotbeing alive at all at age 80. Moreover, returnson

some

assets are stochastic. Inthis section,we

show

that theoptimalityofcompleteannuitizationsurvivessubdivisionoftheaggregated futuredefined

by

c2 intomany

future periods and states, as long asmarkets are complete.A

simple subdivision would be toadd

a third period, while continuing with the assumption ofno

other uncertainty. In keeping with the complete market setting,we

havebonds and

annuitiesRa3-7

That

is, defining bondsand

annuities purchased in period 1 with the appropriatesubscript:E

=

a

+ A

2+

A

3+

B

2+

B

3 (3)C2

=

RB2B2

+

RxiM

(4)c3

=

RB3B3

+

R

A3A

3 (5)Ifourassumptionthatthe return

on

annuitiesexceeds thatofbonds

holdsperiodbyperiod, then ourfulloptimizationresultextendstrivially.Note

that thestandarddefinitionofanArrow

security distinguishes betweenstateswhen

an individualis alive andwhen

heor sheisnot alive.That

is, a standardArrow

security isan"Arrow

annuity."We

havesetup what

we

call "Arrow bonds" (hereB

2and

B3)by

combiningmatched

pairs ofevents that differinwhether theconsumer's death hasoccurred. This representative of a standard

bond

iswhat becomes

a dominated asset once one canseparate theArrow bond

into two separateArrow

securities,and

theconsumer

can choose to purchase only one ofthem. In a settingwith additional sources ofuncertainty, thecombination ofa

matched

pair of events todepict a non-annuitized asset is straightforwardwhen

thedeath oftheparticular

consumer

is independent of other events and unimportant in determining equilibrium. Insome

settings theremay

not be such a decomposition of abond

because the recognition of important differencesbetween different eventsis stronglyrelated to thesurvival oftheindividual.8To

take the next logical step,and

assumingwe

candecompose

Arrow

bonds,we

continue totreat c\ asa scalarand interpret c2,

B

2and

A

2 as vectorswith entriescorresponding to arbitrarilymany

future periods (t<

T), within arbitrarilymany

states ofnature {u><

Q). Rj\% {Rb2) isthena matrix with columns corresponding to annuities (bonds)

and

rows corresponding to payoutsby

period and state of nature. Thus, the assumption of no aggregate uncertainty can be dropped. Multiple states of nature might refer to uncertainty about aggregate issues such as output, or

individual specificissues

beyond

mortality such as health.To

extendthe analysis,we assume

that the consumer is sufficiently "small" (and with death uncorrected with other events) that for eachstate of nature where the

consumer

is alive, there exists a state where the consumer is dead and 7In keeping with the complete market setting, there is no arrival of asymmetric information about future life

expectancy.

8

Ifthe deathof aconsumer only occurs with otherlarge changes, then there is no waytoconstruct an Arrow bondthatdiffers from anArrowannuity onlyinthedeathofasingleconsumer, forexample,ifan individualwilldie insomefuture periodifand onlyifaninfluenzaepidemicoccurs.

the equilibrium relative prices are otherwise identical. Completeness of markets still has

Arrow

bonds

that represent the combination oftwoArrow

securities. Note, however, that the ability to construct suchbonds

isnot necessary fortheresultthataconsumer without abequest motivedoes not purchase consumptionwhen

not alive in the completemarket setting.Annuities paying in only one dated event are contrary to conventional life annuities that pay out in every yearuntildeath. However, with complete markets, separate annuities with payouts in

each year can be

combined

to create such conventional annuities.Itisclearthat theanalysis ofthetwo-period

model

extendsto this setting,providedwe

maintain the standardArrow-Debreu

market structureand

assumptions that do not allow an individual todie in debtsincethe consumer can purchaseacombinationofannuitieswith a structureof benefits across time

and

states as desired. In addition to the description of theoptimum,

the formula forthe gain from allowing

more

annuitization holds forstate-by-state increases in the level ofallowedlevel ofannuitization. Moreover, by choosing any particularprice path

from

theprices inherentin bonds to the prices inherent in annuities,we

canmeasure

the gain in goingfrom no annuitizationto full annuitization. This parallels the evaluation oftheprice changes brought about

by

alumpy

investment (see

Diamond

andMcFadden

(1974)). Hence, withcomplete markets, preferences only matter through optimal consumption; this factmay

clarify, for example, the unimportance of additive separability tothe result ofcomplete annuitization.Statingthe result

more

formally, the full annuitization result is acorollary ofthefollowing:THEOREM

1: //there is no future trade once portfolio decisions have been made, ifthere is nobequest motive and ifthere is a set of annuities with payouts per unit of investment that dominate the payouts of

some

subset of bonds that are held, then a welfare gain is available by selling the subset ofbonds and replacing the bonds with the annuities, so long as this transferdoes not lead to negative wealth in any state.COROLLARY

1: In a complete market Arrow-Debreu equilibrium, aconsumer

without a bequestmotive annuitizes all savings.

Thus, with completemarkets, theresult offull annuitization extends to

many

periods, thedependentutilitythatneed notsatisfy the expectedutility axioms. This generalizationofYaari holds

solongasmarkets arecomplete. Thus, ifthe puzzleof

why

sofew individuals voluntarily annuitizeis to be solved within a rational, life-cycle framework,

we

haveshown

that the answer does notlie in the specification of the utility function per se (beyond the issue ofa bequest motive).

We

briefly consider the role of annuitization with a bequest motive below. However, the results do demonstrate the importanceofmarket completeness, an issue that

we

turn to next.II.

Incomplete

Markets

With

complete markets, a higher yieldofanArrow

annuityover thematchingArrow

bond, datedevent

by

dated event, leads directly tothe result that aconsumer

without a bequest motive fully annuitizes.But

markets arenot complete. Therearetwo formsofincompleteness thatwe

consider.The

first is that thesetof annuities is highlylimited, relative totheset ofnon- annuitizedsecuritiesthat exist.9

The

second isthe incompleteness ofthe securitiesmarket.A. IncompleteAnnuity Markets

Most

realworld annuitymarketsrequirethataconsumer

purchaseaparticulartimepathofpayouts,thereby combining in a single security a particular

"compound"

combination ofArrow

annuities.Privately purchased immediate life annuities are usually fixed in nominal terms, or offer a prede-termined nominal slope such as a 5 percent increase per year. Variable annuities link the payout

to the performance ofa particular underlying portfolio of assets and combine

Arrow

securities inthat way.

CREF

annuities are also participating, whichmeans

that thepayout also varieswiththe actualmortality experience forthe class of investors.To

exploreissues raised by such restrictions,we

restrict our analysis to a single kind of annuity - a constant real annuity - althoughwe

statesome

ofourresults inamore

general vocabulary.We

examine

thedemand

forsuch anannuity,dis-tinguishingwhether alltrade

must

occur ata singletime orwhether it is possible to also purchasebonds

later.Trade Occurs All at

Once

Explainingwhy this isthe casewould take usintotheindustrialorganization of insurance supply, which would

necessarilymakeuseofconsumer understanding andperceptions of insurance. These'issuesarewellbeyondthescope

of this paper. Rather,we analyze rational annuitydemandin different marketsettingsthat aretaken as given.

For the caseofa conventional annuity,

we

must

revise the superior return conditionforArrow

annuities thatRauj

>

RBt^tu:.An

appropriate formulationforacompound

securityisthatitcost less than purchasing thesame

consumption vector using bonds. Defineby

£ arow

vector of ones withlength equal to thenumber

of states ofnature occurringin the annuityand

so distinguished bybonds. Let the set ofbonds

continue toberepresentedby

a vector with elements corresponding to thecolumns

ofthe matrix ofreturnsRb

and

letRa

be a vector ofannuity payouts multiplying the scalarA

to define state-by-state payouts.Then

the cost ofthebonds

exceeds the cost ofthe annuity under the assumption:ASSUMPTION

2: For anyannuitized assetA

and

any collection of conventional assetsB,RaA =

R

B

B

=»A

<

IB.For example, ifthereis an annuity that costs oneunit offirst period consumptionper unit

and

pays

Ra2

perunit ofannuity inthesecond periodand

Ra3

per unit ofannuity inthe third period, thenwe

would

have 1<

Ra2/Rb2

+

Ra3/Rb3-

10By

linearity of expenditures, this implies that any consumption vector thatmay

be purchased strictly through annuities is less expensivewhen

financed through annuities than

when

purchased by aset ofbonds

withmatchingpayoffs.Consider a three-period model, with complete

bonds

and

a single available annuity and no opportunity for trade after the initial contracting.The

minimizationproblem

isnow

min

:a

+

B

2+

B

3+ A

(6)cx,A,B

s.t. :

U(c

1,R

B2B2

+

Ra2AR

B3B

3

+

R

A3A)>U

(7)B

2>

0,B

3>

(8)Given our return assumption and positive consumption whenever alive, then,

we

have an arbitrage-likedominance

of the annuity over the matching combination ofbonds

as long as thistrade is feasible.

Thus

we

can conclude thatsome

annuitization is optimaland

that theoptimum

has zero

bonds

in at least one dated event.The

logic extends to a setting withmore

dates andstates.

However

we

would

not get complete annuitization if the consumption pattern with com-plete annuitizationis worth changing by purchasing a bond.That

is, purchasing abond would

beThe righthandside representsthe required investmentsintwo Arrowbondsthat costone uniteachin the first

period to replicatetheannuitypayout.

worthwhile if it raises utility

by more

than the decline from decreased first period consumption. Thus, denotingpartialderivativesoftheutilityfunction withsubscripts, there willbepositivebond

holdings if

we

satisfy either oftheconditions:U

1(c1,R

A2A,R

A3A)

<

R

B2U

2(Cl,R

A2A,R

A3A) (9) or Ui(Cl,R

A2 A,R

A3A)

<

R

B3U

3(Cl,R

A2 A,R

A3 A). (10)By

our return assumption,we

can not satisfy both ofthese conditions at thesame

time, butwe

might satisfy one ofthem.

Additional Trading Opportunities

The

previous analysis stayed withthe setting of asingle time to trade. Ifthere are additional trading opportunities, the incompleteness of annuity marketsmay

mean

that such opportunitiesare taken. Staying within thesettingofperfectlypredicted futureprices and assuming thatprices for the

same commodity

purchased at different dates are all consistent,we

can see that repeatedbond

purchasemay

increase thedegree ofannuitization. Ifdesired consumption occurs later thanwith

consuming

all ofthe annuitized benefit, then the abilityto save by purchasing bonds, rather thanconsuming

all ofthe annuitypayment,means

that annuitization ismade

more

attractive.Returning to the three-period

model

with only mortality uncertainty,we

can write thisby

denoting savingattheendofthesecondperiod

by

Z

(Z>

0).We

assumethatthe returnonsavings betweenthesecondand

thirdperiodsZ

isconsistentwiththe otherbond

returns(Rz

=

Rbz/Rb2)-The

minimization isnow:min

ci+

B

2+ B

3+A

(11)d,A,B,Z

s.t. :

U(

Ci,Rb2B

2+

R

A2A

-

Z,R

B3B

3+

R

A3A +

{R

B

z/Rb2}Z)

>

U. (12)The

restrictionofnot dyingindebtisthe non-negativityofwealth (includingthe value offuture payments) ifA

equals zero:R

B2B

2+

{R

B2/R

B3)R

B3B

3>

(13)R

B3B

3+

(R

B3/R

B2)Z

>

0. (14)Dissaving after full annuitization (ifpossible)

would

not be attractive if:R

B2U

2(cuRa2A,R

A3A)<

R

B3U

3(c1,Ra2A,R

A3A). (15)Under Assumption

2, (15) isnow

sufficientfor theresult offull annuitization ofinitial savings.To

see this, note thatAssumption

2 implies thatR

B3<

Ra2^z

+

R-A3- Thus, holdings ofB

3 are dominated by the annuity with the second period return fully saved. Positive holdings ofB

2 areruled out

by Assumption

2and

condition (15) sincethey imply:R

B2U

2<

R

A2U

2+

{RA

3/Rb3)Rb2U

2<

RA2U2

+

RazU

3, (16)whichis inconsistent withthe

FOC

forpositiveholdings ofbothA

and

B

2 (andsome

annuitizationispart ofthe

optimum)

. In thecommonly

usedmodel

ofintertemporally additive preferenceswithidentical period utility functions, a constant discount rate

and

a constant interest rate, a sufficientcondition for full initial annuitization in a constant real annuity is thus that 5(1

+

r)>

1. If theavailable annuity (a constant real benefit) provides consumption later than

an

individual wants, thentheassumed

illiquidityofan annuity limits its attraction.We

consider illiquiditybelow.B. Incomplete Securities

and

Annuity Markets: The Role ofLiquidityA

widely recognized basis for incomplete annuitization isthat theremay

be an expenditure needin the future which cannot be insured. This might be an individual need, like a medical expense that is not insurable, or an aggregate event such as unexpected inflation, which lowers the real

value of nominal annuity

payments

in the absence ofreal annuities.With

incomplete markets, the arbitrage-likedominance argument

used above willno

longer hold ifbonds

are liquid whileannuities are not.11

We

assume

total illiquidity ofannuities without exploring the possible arrival of asymmetric information about life expectancy which would naturally reduce the liquidity of annuities farmore

thanthe liquidity ofnon-tradedbonds

such as certificates of deposit.We

show, however, that the presence of uninsured risksmay

add

to or subtract from theoptimal fraction of savings annuitized, depending on the nature oftherisk.

We

illustrate the role ofilliquidityby examining twocases: uninsured medical expenditures,and

thearrivalofasymmetric information combined with inferior annuity returns.11

Moregenerally, it iswellknown thatlifecycle consumersmaybeunwillingto invest inilliquid assetswhen they

face stochastic cashneeds Huang (2003).

Annuities and Medical Expenditures

For concreteness, let us start with the two period

model

above,where

theonly uncertainty islength of life.

To

thismodel

let usadd

a risk of a necessary medical expense whichwe

consider separately for each period.Assume

that this expenditure enters into the budget constraint as a required expenditure, but does not enter into the utility function.Assume

further that the occurrence ofillness hasno effecton

lifeexpectancy.If it is possible to fully insure future medical expenses

on

an actuarially fair basis then the optimal plan is full medical insuranceand

full annuitization.Thus

removing the ability to insure medical expenses, while continuing toassume

that annuity benefits can be purchased separately period-by-period, can only raise thedemand

forbonds

andmay

do so if the medical risk occursin period 1, but not if it occurs in period 2.

That

is, the illiquidity of annuitiesmay

be relevantifthe risk occurs early in life, but not toward the end oflife. For example, contrast the cost ofa

hospitalization early in retirement with the need for a nursing

home

toward the end oflife.The

formercalls forshiftingexpenses toearlier and so increasesthe value ofan asset thatpermits such a change. Since medical expenses only occur for the living, annuities are a better substitute for

nonexistent insurance for medical expenses later in life than arebonds.

To

thetwo-period problem considered in (1),we

add

the risk ofafirst-period medical expenseofsize,

M,

withprobabilitym

and

insurance atcost 7,payingabenefit off3perdollarofinsurance.Ifthereis

no

additionaltrading after the initial purchases, theproblem

is:min

ci+A +

B

+

I (17)ci,A,B,I

s.t.

(l-m)U(c

1,R

AA

+

R

B

B)

+

mU{c

1-

M

+

/3I,RA

A + R

B

B)

>

U. (18)In the case of

no

trading after the initial date, annuities continue to dominate bonds. If the insurance is actuarially fair,there willbe completemedical insurance (and soc\, A, andB

arethesame

as ifthere were noriskand

expenditures were reducedby

mM)

.With

less favorable medicalinsurance, thepresence ofboth risk

and

insurance generally affects the level ofilliquid savings and sothe level of annuitization, but all savings are annuitized sincebonds

are still dominated.To

bring out the role ofliquidity,assume

thatbonds

can be sold in the first period with an earlyredemption penalty, but annuities cannot be sold.The

analysiswould

be similarwith liquid annuities thathad

alarger penalty for earlyredemption or theability toreduce spendingand

addto

bond

holdings (at a lower interest rate) after arealization ofno

health risk.Then

theproblem

becomes:

min

d+A

+

B +

I (19)a,A,B,l,z

s.t.

{1-m)

Ufa,

R

A

A

+

R

B

B)

+

mU{c

1-M

+

pi

+

aB

Z,R

A

A +

R

B

(B-Z))

>

17.(20)where

Z

is the value ofbonds withdrawn

earlyand

aB

(as<

1) is the fraction of value receivednetoftheearly withdrawalpenalty.

Since annuities still dominate any bonds that

would

never be cashed in, the level ofbond

holdings would not exceed the

amount

cashedin earlyand

we

canrewrite theproblem asmin

a+A

+

B

+

I (21)ci,A,B,I v '

s.t. {I

-m)

Ufa,

R

A

A +

R

B

B)+mU(ci-M

+

(31+

a

B

B,R

A

A)>

U. (22)Inthis case, it ispossible togenerate preferences that have an

optimum

withsome bonds

provided thereis a small differencebetween annuity andbond

returns, a small early withdrawalpenalty forbonds

and

sufficiently actuariallyunfair medical insurance pricing.We

turnnow

to a medical risk that occurs only in the secondperiod.With

medical insurancepurchased at the start of period one, expected utility can be written as (1

—

m)

Ufa,R

A

A +

R

B

B)

+

mU(ci,R

A

A + R

B

B

—

M

+

(31). Thus, medicalrisk in the secondperiod does not change thedominance

of annuitiesoverbonds

whateverthe pricingofmedicalinsurance. In theabsenceofthearrival ofinformation, there aretwoequivalent

ways

oforganizingmedicalinsurance.One

is to purchasemedical insuranceat thestartofperiodone(aswithlong-termcare insurance).The

otheris to purchase an annuity with a plan to purchase medical insurance at the start ofperiod two, if

alive.

With

bothformulations, a worsening ofthe pricing ofmedical insurancewill generally alter first-period consumptionand

so total savings. In the second formulation, this translates directly into thedemand

for annuities. In addition, therewould

generally be a change in theamount

ofmedical insurance purchased in the second period. In the first formulation, unlike the second, a change in the level of medical insurance would also change the level of annuity purchase even

if preferences were such that first-period consumption did not change. For example, going from

fair medical insurancetono medicalinsurance wouldincrease thespending on annuities bythe full

amount

previouslyspentonmedical insuranceifpreferencesweresuch that first-periodconsumptiondid not change.

That

is, removinginsurance that is effectively annuitizedcanincrease thedemand

for astandard annuity.

Thus,

we

can conclude that the timing ofthe risk ofmedical expenses is key to understanding the interaction between the availability of medical insuranceand

the purchase of annuities. In the absence of strong assumptions it is thus impossible to sign the effect of liquidity needs on annuitydemand.

In oneparameterization, Turraand

Mitchell (2004) findthattheoptimal fraction ofwealth annuitized remains large evenwhen

out-of-pocket (uninsured) medical expenditures are possibleand

are associated with truncated lifetimes. However, these simulations alsoshow

that these uninsured expenditurestend toreducedemand

for annuitiesbelow 100 percent of savings.We

haveassumed

an absence ofa relationship between medical expensesand

life expectancy.If a medical expense in period 1 implies a lower survival probability, then that

would

strengthen the value of liquid bonds.The

next subsectionbriefly considers aroleofthe arrival ofinformation about life expectancy12Since

we

examine

annuitydemand

in different settings, rather than amodel

ofequilibrium,we

do not explore the illiquidity of annuities (relative to bonds) that is present.

Even

if illiquidityof annuities were an explanation for lack of

demand

for illiquid annuities,Bernheim

(1987b) has pointed out that illiquidityis not a completeexplanation for thenear absence ofannuity markets.Bernheim

proposes the creation ofannuities that are subject tocancellation at any time. In termsofthenotation above,

bonds

would havea returnifheldtomaturity,Rg,

andareturniswithdrawn

early, as, with annuities characterized by

Ra

and

a

a-Even

with an early withdrawal option,we

might plausibly have

Rb <

Ra

and

as >

a

a- This could be theoutcome

since early withdrawal from an annuity has implications for the cost of providing the annuity, while this is less so of abond

(where withdrawalmay

just reflect available alternative investments).C. Inferior Returns to Annuities

Another route to limited annuitization is if annuity pricing

and

the arrival of asymmetricinfor-mation imply an advantage to delayed annuitization. For example, Milevsky

and

Young

(2002) 12Ifthemedicalcondition isobservabletothe provider, it maybethat bundlinginsuranceforthe cashneed with theannuity could improvepricing forboth forms ofinsuranceby eliminating adverse selectionthat would exist for

eitherproduct individually, ashasbeen proposedbyWarshawsky, Spillmanand Murtaugh (forthcoming).

consider a cost to annuitization associated with illiquidity that renders the return

on

annuitiesessentially inferior to the return on

some

bonds. In particular, theyshow

that itmay

be optimalto wait to annuitize wealth if returns

on

investment in the futuremay

exceed present returns. Similarly, ifannuities purchased later in life are pricedmore

favorably than those purchasedear-lier, deferral of annuitization

may

be optimal.13 If, however, there are utility gains to annuitizingat, say, age65,

and

yet it is optimal to delay annuitization, then this implies that there are even larger utility gains to annuitizing later inlife. Empirically, however,we

do not observe households choosing to annuitize at later ages, suggesting that such an explanation cannot fully explain the near absence ofdemand

for private market annuities.Of

course, if annuity returns, net ofadministrative costs, are inferior to those ofconventionalassets, annuity

demand

can go to zero. Mitchell et al (1999) show, however, that available pricing on annuities does notseem

to be sufficient to render annuitization unattractive. Recentwork by

Dushi

and

Webb

(2004), whichbuildsupon

previouswork by

Mitchellet al (1999)and

Brown

and

Poterba (2001) shows that a combination oflow annuity returns, within couple-risk sharing that

substitutes for a formal annuity market, and very high levels ofpre-existing annuities can render

additionally fixed annuities unattractive at any age. However, even these results suggest that

we

should observe frequent annuitization

by

surviving spouses, whichwe

do

not.III.

Bequests

Throughout

thepaperwe

havemaintainedtheassumptionthat therewas

no bequestmotive.While

a bequest motivereduces the

demand

forannuities, it does not eliminate it in general.To

see this,consider a

model

with two periodsand

uncertain survival to the second period as the sole risk.Ignoring the role of inter vivosgifts, there can be abequest at theend ofthefirst period or ofthe second.

We

model

thebequest motive asan additive term dependingon

the two levelsofbequests that mighthappen

at theend ofperiods one and two. In this case,we

canexpress utility interms ofown

consumption and thetwo possiblebequest levels.With

deathat the end ofperiod two, theDennis (2004) also finds a gaintodeferred annuitizationforsomepricepatterns.

bequest isreceived inperiod 3, involving additional interest. Using the dual formulation,

we

have:min

: ci+ A +

B

(23)c\,A,B,C2

s.t. :

U(c

1,c2)+ V(R

B

B,R

B (R

AA

+

R

B

B-c

2))>U.

(24)If the utility of bequest is the expectation of a concave value ofthe bequest, v, evaluated at the

start ofperiod three (whether given thenor earlier),

we

have:V

{R

B

B,R

b

(RaA

+

R

B

B

-

Q2))=

qv(R

B

R

B

B)

+

(1-

q)v{R

B

{RaA

+ R

B

B

-

c2)), (25)whereqisthe probability that the individualdiesbefore period 2. Forthere tobe no annuitization,

the value ofan annuity

must

be lessthanthe value ofabond, evaluated at zeroannuities:(1

-

q)R

B

RAv'

{Rb

{RbB

-

c2 ))<

R

b

Rb

{qv'{RbRbB)

+

(1-

q)v'(R

B

{R

B

B

-

c2 ))) (26)With

c2>

0, this isviolated for an actuariallyfair annuity (1—

q)RA

=

Rb, and

for annuities closeenough

to fair.Ifthe annuity is actuarially fair, then

v'

{RB

{RaA

+

R

B

B

-

c2 ))=

qv'{RB

R

B B)

+

(1-

q)v'{RB {R

B

B

-

c2 )) (27)This implies

RaA =

c2, a point implicit in Yaari (1965).That

is, annuitization equals secondperiod consumption.

Thus

with this approach to bequests, the case for significant annuitization survives the presence ofa bequest motive.14IV.

Simulations

The

theory shows that while full annuitization is not guaranteed unless everybond

is dominatedby some

annuity, an unrealistic assumption, it is also clear that partial annuitization is optimalin

many

settings.The

theory itselfis insufficient for answering practical policy questions that are1

Theuseofa "guarantee" withannuitiesiscommon. Thisoften involvesaminimumnumberofpayments,resulting

in a lowermonthly annuityfora givenpurchaseprice.

We

note that thisgeneratesarandombequest comparedwith purchasing the same lower annuity without the guarantee and bequeathing (or giving before death) the reduced purchaseprice. Inthe caseoffair annuities,theguaranteeisa pure gambleandimplausibly optimal. Withselectionissues,thedemanddepends onpricing andtheguarantee maybepartofaddressingselection issues.

often centered

on

what

fraction ofsavings is optimally annuitized in different market settingsand

withdifferent preferences. Thus, alargesimulation literaturehas arisento addressthis.

We

brieflyreview this literature,

and

then extend itby

conducting a "stress test" ofthe annuity valuationresults by considering cases that are intentionally designed to create a

more

extrememismatch

between desired consumption

and

the annuity income stream thanwe

would expect to see in practice.By

showingthat theoptimallevel ofannuitization remainshigh eveninwhat

we

consider to be extreme cases,we

conclude that the virtual absence of voluntary annuitization cannot be easily explained thestandard set ofreasons thatcome

from the life-cycleframework.Friedman

andWarshawsky

(1990)and

Mitchell, Poterba,Warshawsky and

Brown

(1999) are examples ofthe simulation literature that calculate utility gains from annuities under alternativeassumptions. These papers, like

many

others, consider an individual a retired individualwhose

preferences can be represented

by

a utility function that exhibits constant relative risk aversion,exponential discounting,

and

intertemporal separability.They

find that these consumerswould

accept a substantial reductioninwealthinexchangeforaccess to actuariallyfairannuity markets.15

Numerous

subsequent papers haveexplored the gains from annuitization under a wider rangeof assumptions, including: uncertainty about future asset returns (Milevsky

and

Young

(2002)),risk pooling within couples

(Brown

and Poterba (2003)), uninsured medical expenditures (Turraand

Mitchell (2004), Sinclairand

Smetters (2004)), actuarially unfair prices due to mortalityhet-erogeneity

(Brown

(2003),Palmon

and Spivak (2001)),and

higher levels of pre-existing annuities (Dushi andWebb

(2004)). In nearly every case, the annuity products considered in these papersare constrainedin

some

way

(i.e., annuitymarkets are incomplete), themost

common

assumption being that the annuity'spayment

stream is fixed in real terms. Consistent with our theoreticalfindings, these papersfind that thereare substantial gains to

some

annuitization, but that fullan-nuitizationis not always optimal.

Our

theoretical resultsprovide aframework inwhich such results can be interpreted:when

full annuitization issub-optimal, the settings weresuch that incomplete marketsled toamismatch

betweendesired consumption trajectoriesand

available annuity incomepaths.

Even

in these cases, however, the optimal level ofannuitization was generally high.15

Anotherstrand of the literature examines the "probability of ashortfall" when aconsumer tries to self-insure

ratherthan usingformal annuity markets. Milevsky (1998) isagood exampleof this approach.

A. Relaxing Additive Separability:

A

"Stress Test" ofAnnuity ValuationA

key practical message from our theoretical results is that the welfare gains from annuitizationdepend on

preferences mainly throughtheconsumptiontrajectory. Thus, ifone isseeking torecon-cilethe theory with the empirical smallness ofvoluntary annuity markets, one ought tobe looking

forsituations inwhich thereis a severe

mismatch

betweenthe desired consumption trajectoryand

the income path provided

by

a limited set ofannuities in an incomplete markets setting.Inthis section,

we

extendthe simulationliteratureby

modelingpreferencesthat leadtoaseveremismatch

withthe goal of seeingwhethersuchmismatches canplausiblyexplain thesmallsizeofthe market.We

dothisby

exploring a class ofmodelsthat havethe realisticproperty that preferencesare not intertemporally additive

and

have the feature that different parameterizations,meant

to reflect the heterogeneity ofhousehold financial positions at retirement, lead to very different time shapes ofoptimal consumption.We

consider a 65 year-oldmale

with survival probabilitiestaken fromthe U.S. Social SecurityAdministration for theyear 1999, modified (to ease computation) so that death occurs for sure

by

age 100. His utility function is:

100

tf=£(l

+

(r

4 (Ci/Si) 1-7/(i-7)

(28) t=65When

the parameter St is constant, this is the frequentlymodeled

case ofCRRA

preferences.Followingthis literature,

we

setthereal interestrateand

discountrate(S) equalto.03and

calculatetheutilitygains from annuitization.

We

set7

=

2and

findthe consumption vectorthat solvesthe expenditure minimization problem numerically using standard optimization techniques.16We

begin by simply verifying that ourmodel

matches the results ofthe previous literature inthe case in which St is fixed at a value of one, corresponding to the

CRRA

utility case. In this setting, whichwe

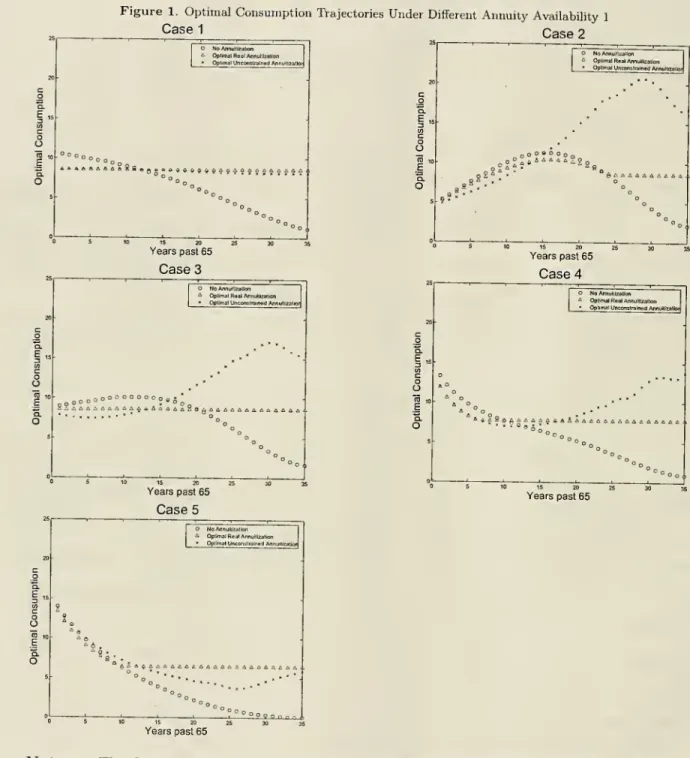

denoteas "Case 1" inTable 1,we

find thatit isoptimalfor an individualtofullyannuitizeall wealth. Moreover, with r

=

5, real annuitiesprovide the optimal annuity stream.A

rough estimate of themagnitude

ofEVs

can be obtainedby

observing the difference intrajectoriesbetween the unconstrained (circles

and

x's in figure 1, case 1) consumption plan andthe constrained real annuity (triangles in figure 1) consumption plan.

When

optimal consumptionis sharply decreasing, the constraints bind consumption

away

from the optimal path. In these16

Resultsforother levelsof riskaversion are available in someofthepapers listedabove.

cases, the benefit of annuitization is relatively small because the

sum

of future consumption isrelativelysmall

and

the gainis offset furtherby theconstraints.When

optimalunconstrained(zeroannuitization) consumption is

hump

shapedand

lesssteeply decreasing, there are greater benefitsand

the constraints impose lesscosts, so the net benefit to annuitizationis greater.What

differentiatesourmore

general set-up frompriorwork

is thatwe

can vary St inequation(1) so that the utility function exhibits an "internal habit," which

we

can then adjust to create optimal consumption trajectories that differ markedly from the usualCRRA

case.The

intuition behind our utilityfunction, taken fromDiamond

and

Mirrlees (2000), is that it is not the level ofpresent consumption, but rather the level relative to past consumption, that matters for utility.

For example, life in a studio apartment issurely

more

tolerable forsomeone

used to living in such circumstances than forsomeone

who

was

forcedby

a negative income shock toabandon

afour-bedroom

house. In choosinghow

to allocate resources across periods, "habit consumers" trade offimmediate gratification from consumption not only against a lifetime budget constraint, but also

against theeffects ofconsumptionearly in life on the standard-of-livinglater in life.

Following

Diamond

and

Mirrlees (2000),we

model

the evolutionofthe habit as follows:st

=

(st-i+

act-i)/(l'+a) (29)a

istheparameterthat governs thespeed ofadjustmentofthe habit level.When

a

is zero, the habitisconstantand we

arebackintheadditivelyseparablecase.As

a

approachesinfinity, present habit approaches last period's consumption.We

selectan

intermediate speedofhabit adjustment ofthe habit (q=1).Away

from zero,we

find that changes toa make

no substantive difference toour results,

and

thereforedo not reportresults fora rangeofa

values.17When

the habit evolves (a>

0), present consumption increases the future standard-of-living.Thisincrease in thestandard-of-living reduces the level ofutility

and

increases marginal utilityinthe future.

With

later consumption, there are fewer future periods that are adversely affectedby

an

increased standard-of-living.While

some

researchers have attempted to measure parameters of alternative habit formationmodels, largely involving "external habit" formation incalibration exercises, there istoour knowl-edge no empirical study that provides estimates ofthe initial standard S65

m

our model. This isAdditional resultsareavailablefrom theauthorsupon request.

not a major limitation, however, asour objective isnot to carefully calibrate arealistic

model

ofa representative lifetimeoptimizingconsumer, but rather to createoptimal consumptiontrajectoriesthat create an intentionally

more

severemismatch

with the available annuity structure thanwe

actually observe in available consumption data

and

to recognize the wide diversity in wealth atretirementrelative to lifetime income.

Doing

so allowsus to "stress test" the annuity valuations inorder toseeifone canplausibly explain the paucityofvoluntary annuity purchases within astrictly rationalmodel.

We

do

soby

consideringinitialstandards oflivingthat generateconsumption

paths thatare both extremely friendlyand

extremely unfriendly to annuitization.The

first four columns ofTable 1 indicate the casenumber

and

the relevant parameters thatare varied across cases.

Column

(5) reports the fraction of wealth that is optimally placed in a constant real annuity instead ofbonds. Incolumn

(6),we

report the equivalent variation ("EV")associated with this optimal

amount

of real annuitization. This is the increase in wealthrequiredtohold utilityconstant while

moving

from havingtheoptimalamount

annuitized in areal annuity,tohavingallofwealthinbonds.

Column

(7) reportsthe gainsfromannuitization (againas anEV)

for thecase in which the individualis permitted to choose an optimal payout trajectory, i.e., they

are no longer constrained to purchase a constant real annuity. For shorthand,

we

refer to this asthe "complete markets" result, although strictly speaking, all that is necessary is that the subset

of annuities that aredesired

by

this individualbe available.Because an internal habit introduces a

new

cost to early consumption, one might expect thatthe fixed real annuity will be even

more

desirable with an internal habit (a>

0) than without.However, the accuracy of this intuition hinges

on

the level of the initial habit S65 relative toresources at retirement. If the initial habit is small, then it is correct that the presence of a

potentiallyincreasing habit leads to deferred consumption and increased valuation ofthe annuity. However, if the initial habit is so large as to be unsustainable, so that the habit level

must

fallover time, then the presence ofthe habit will

push

optimal consumption earlier, because ofthedesire to

smooth

the ratio ofconsumption to habit across time. If the habit decreases with time, then smoothing likewise requires that consumption decrease with time.Hence

a very high initialhabit relative to resources provides a

mechanism beyond

heavy discountingwhereby

the deferred consumption requiredby

a constant real annuitymay

be very burdensome.To

calibrate the model,and

to buildsome

intuition,we

first consider an individualwho

hasreached retirementwithresourcesthat,

when

annuitized, aresufficientto exactlysatisfy theirhabitlevel of consumption for the rest of their lifetime. In this scenario, labeled "Case 2" in Table 1,

the individual entersretirement witha habit level S65 that ispreciselyequal tothe annual annuity value oftheirwealth.18

As

expected, the presence ofapotentiallyincreasinghabitleads todeferred consumption, i.e.,and upward

sloping consumption path inthe earlyyears (see Figure 1, Case 2).When

only real annuities are available, the optimal allocation is to fully annuitize, because doingsoprovides the individual withthe highest possible returnwithout imposing any bindingliquidity constraints.

While

the utilitygain iseven higher than inour base case, the utilitygains are higherstill if the individual is able to purchase annuities in a complete market,

and

thus exactlymatch

the desired consumption trajectory. In this latter case, the ability to choose an optimal annuity trajectoryis equivalent in utility terms to nearly doubling ofnon-annuitized wealth.

Reachingretirementwithpreciselythe resources requiredtomaintainone'spast livingstandard

is not the empirical norm, however. Indeed, given the wide range ofretirement resources across

thepopulation, it wouldnot

make

sense toconsider acommon

levelofpre-retirement consumption relative to retirement resource across the entire population.Hurd and Rohwedder

(2004) providenew

evidenceon

thedistribution ofthepercentagechangeinspendingfrompretopost retirement.They

find amean

consumption drop of 13 - 14 percent.At

the 20th percentile, they find a 30percent decline in consumption, whereas at the 95th percentile they find a 20 percent increase in

consumption.19

We

choose toexamine

evenmore

extreme points in the consumption distributionby

evaluatingthe case inwhichthe habit levelofconsumption is 50 percent and 200 percent oftheamount

that can be sustained by one's retirement wealth.In Case3ofTable 1 and Figure1, the individual hassufficient wealthtopurchaseareal annuity stream that is double the initial habit level in retirement.

As

in cases 1and

2, it is still optimalto fully annuitize all wealth.

Doing

so in a constant real annuity generates a utility gain that isequivalent to a 67 percentincrease innon-annuitized wealth.

The

abilitytomatch

annuities tothedesired

upward

sloping consumption trajectory is evenmore

valuable.More

interesting forpurposesofour "stress test" is toexamine the caseinwhich the individual onlyhashalf ofthelevel ofwealth thatwould

berequiredto sustain their initialhabit consumptionls

Givenour mortality assumptions, the annual annuityvalueof$100 of startingwealth is$8.59.

19

Hurdand Rohwedderdonot report pointsinthe distribution belowthe 20thpercentile.

level.

As

can be seen in Case 4, this leads the individual towant

to sharply reduce consumption early inretirement, inordertorapidlybringdown

thelevelofhabit toamore

sustainablelevel.As

such, the optimalfraction ofwealthheld ina real annuity declines to 90 percent, asthe individual uses the 10 percent ofnon-annuitized wealthtosupplement consumptionin the first 10 years,and

then

consumes

the annuity fortheremainder oflifeafterbring the habitdown

to a lowerlevel.Pushingthe "stress test" evenfurther, Case 5 adds a high discount rate to the low wealth-to-habit ratio.

By

holdingr fixed at .03and

raisingthe discountrateto .10, theoptimal consumption trajectory, asshown

in Case 5, is evenmore

heavily front-loaded,and

thus themismatch

with the real annuity income stream is particularly severe.Even

so, the individual would optimally annuitize three-quarters of their wealth. In results not reported,we

have found that evenwhen

the individual's habit is so high that retirement wealth can provide for

an

annuity that is only one-sixth ofthe initial habit level, the optimal fraction ofwealth invested in a real annuity is stillnearly two-thirds ofinitial retirement wealth.

Thesesimulationsindicatethatit isextremelydifficulttogenerateoptimalconsumptionprofiles

such that the optimal fraction ofwealth annuitized drops

much

below two-thirds ofinitial wealthat retirement without appealing to

many

additional factors. This suggests that the absence ofannuitization outside of Social Security

and

defined benefit pensions cannot be easily explained within a rational life-cycle model, even with preferences that lead to a severemismatch

between desired consumptionand

availableannuity paths.V.

Conclusions

and

Future

Directions

With

complete markets, the result of complete annuitization survives the relaxation of severalstandard, but restrictive assumptions. Utility need not satisfy the von

Neumann-Morgenstern

axioms

and

need not be additively separable. Further, annuities need not be actuarially fair, but onlymust

offer positivenet premiaover conventional assets.With

incomplete markets, thefull annuitizationresultcanbreakdown when

thereis asufficientmismatch

between the optimal consumption pathand

the income stream offeredby

the annuitymarket. In the much-studied case ofa worldwhere only individual mortality is uncertain,

we

findthat there