Dynamic Programming for Mean-Field Type Control

Texte intégral

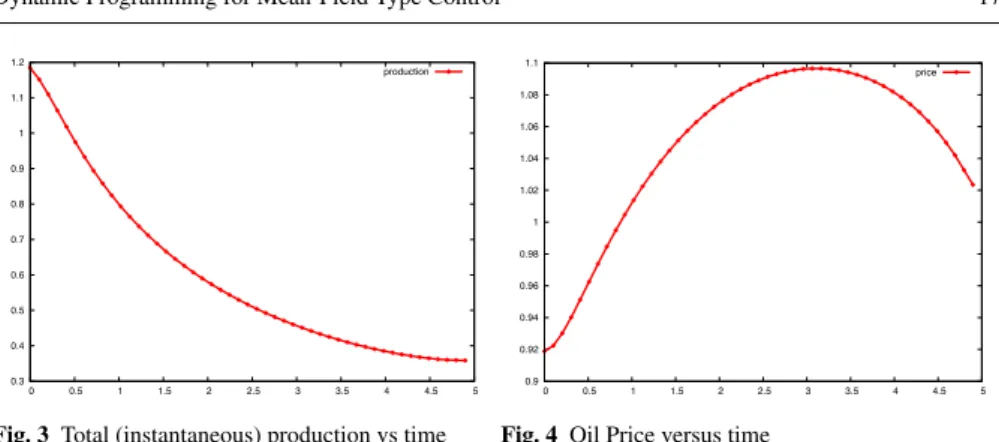

Figure

Documents relatifs

Russell used acquaintance to that effect: ÒI say that I am acquainted with an object when I have a direct cognitive relation to that object, that is when I am directly aware of

We also use the Poincar´ e-type inequality to give an elementary proof of the exponential convergence to equilibrium for solutions of the kinetic Fokker-Planck equation which

A general formulation of the Fokker-Planck-Kolmogorov (FPK) equation for stochastic hybrid systems is presented, within the framework of Generalized Stochastic Hybrid Systems

Keywords: general stochastic hybrid systems, Markov models, continuous-time Markov processes, jump processes, Fokker-Planck-Kolmogorov equation, generalized Fokker-Planck

The problem turns into the study of a specic reected BSDE with a stochastic Lipschitz coecient for which we show existence and uniqueness of the solution.. We then establish

Averaging with respect to the fast cyclotronic motion when the Larmor radius is supposed finite, leads to a integro-differential version of the Fokker-Planck-Landau collision

Abstract— A Model Predictive Control scheme is applied to track the solution of a Fokker-Planck equation over a fixed time horizon.. We analyse the dependence of the total

Unit´e de recherche INRIA Rennes, IRISA, Campus universitaire de Beaulieu, 35042 RENNES Cedex Unit´e de recherche INRIA Rh ˆone-Alpes, 46 avenue F´elix Viallet, 38031 GRENOBLE Cedex