MIT LIBRARIES

3

9080 01917 6335

.'4

Digitized

by

the

Internet

Archive

in

2011

with

funding

from

Boston

Library

Consortium

Member

Libraries

HB31

.M415

1\oW)-ll-\

working paper

department

of

economics

The

Cost of Recession

Revisited:A

Reverse-Liquidationist

View

Ricardo

J.Caballero

Mohamad

L.Hammour

No.

99-22

October 1999

massachusetts

institute

of

technology

50 memorial

drive

Cambridge,

mass. 02139

WORKING

PAPER

DEPARTMENT

OF

ECONOMICS

The

Cost

ofRecession

Revisited:A

Reverse-Liquidationist

View

Ricardo

J.Caballero

Mohamad

L.Hammour

No.

99-22

October 1999

MASSACHUSETTS

INSTITUTE

OF

TECHNOLOGY

50

MEMORIAL

DRIVE

CAMBRIDGE,

MASS. 02142

-MASSACHUSETTSINSTITUTE OFTECHNOLOGY

The

Cost

of

Recessions

Revisited:

A

Reverse-Liquidationist

View

Ricardo

J. CaballeroMohamad

L.Hammour*

August

30,1999

Abstract

The

observation that liquidations areconcentratedinrecessionshas longbeenthe subjectofcontroversy.

One

viewholds that liquidations arebeneficialinthatthey result in increased restructuring. Another view holds that liquidations are

privatelyinefficient and essentiallywasteful. Thispaper proposesan alternative

perspective. Based ona combinationoftheory withempiricalevidence ongross

jobflowsand onfinancialand labor marketrents,

we

find that, cumulatively,re-cessionsresult inreduced restructuring,andthatthisislikelytobesocially costly

once

we

consider inefficiencieson both the creationand destruction margins.1

Introduction

The

concentrated liquidation during recessions of significant segments of theecon-omy's productive structure has been a source of controversy

among

economists atleast since the pre-Keynesian "liquidationist" theses ofsuch eminent economists as

Hayek, Schumpeter,

and

Robbins.Those

economistssaw

intheprocess of liquidationand

reallocation offactors ofproduction themain

purposeofrecessions. In thewords

of

Schumpeter

(1934): "depressions are not simplyevils,which

we

might attempt tosuppress, but ... forms ofsomething which has to be done, namely, adjustment to ...

change" (p. 16). This led

him

and

others to advocate apassivegovernment

attitudeat the onset of the Great Depression. (See

De

Long

1990 for historical survey,and

Beaudry and

Portier 1998 for amodern

formulation of the liquidationist argument).•Respectively:

MIT

andNBER;

DELTA

(jointresearch unit,CNRS

-ENS

-EHESS) andCEPR.

Wc

arcvery grateful toFernandoBroncr, ChristianFrois,Roberto Ncut, RobertoRigobon andTanyaRoscnblat for excellent research assistance; and to Robert Gordon, John Haltiwanger and Glenn

Hubbard for providing uswith dataand references.

Wc

havebenefited from commentswe receivedfrom Daron Acemoglu, Steven Davis, Robert Hall, Guido Kuersteiner, Jaume Ventura, Fabrizio

Zilibotti, andtwo anonymous referees; as well as from seminar participants at Columbia,

DELTA,

Entc Enaudi, EUI, IGIER, the

NBER

Summer

Institute, MIT, the Minneapolis Fed, Stanford,Toulouse,

UCSD,

Virginia, Yale, andconferenceparticipants at theAFSE, theCEPR

ESSIM, andthe

NBER

EFG

meetings. Ricardo Caballero thanks theNSF

for financialsupport, and the AEI,where part ofthis paperwas written, forits hospitality andsupport. Earlierversions ofthispaper

Although

few economists todaywould

take theextreme

position of earlyliq-uidationists,

many

see in increased factor reallocation a silver lining to recessions.Although

recessions perse are undesirableevents, they are seen as a timewhen

the productivity of factors of production is low and, therefore, offers a chance to un-dertakemuch

needed restructuring at a relatively low opportunity cost.Observed

liquidations are considered a prelude for increased restructuring. (See

Aghion

and

Saint-Paul 1993 for a survey ofthis viewof recessions as reorganizations).

At

the polar opposite of liquidationism, an alternativeperspectiveholds that con-centrated liquidations duringrecessions—

large-scalejoblossesand

financial distress—

are associated withsignificant waste,which

we

ought tofindways

to avoid.Look-ing

more

specifically at workers, the recent labor-market literatureon

the costs ofjob loss

documents

the apparently large private losses that resultfrom

a significantfraction of separations (see, e.g., Topel 1990; Farber 1993; Jacobson, Lalonde

and

Sullivan 1993;

Anderson

and

Meyer

1994).As

Hall (1995) shows, the product of those private losses with the sharp increase in separationsamounts

to a substantialcost of recessions.1

The

debate surrounding the costs or benefits of liquidations during recessionsseldom

considerstwo

central dimensionsofthisissue.The

first relatestothecommon

inferencethatan

aggregate recession increases the overallamount

ofrestructuringinthe economy.

From

the increase in liquidations during recessions—

asdocumented,

for example, in the gross job flow series of Davis

and

Haltiwanger (1992)--it

istypically concluded that recessions increase overall factor reallocation. Indeed, this

is

what

onewould

expect in a representative-firm economy, as the representative firmmust

replace each job it destroys during a recessionby

creating anew

job during the ensuing recovery. This is illustrated in panel (a) of figure 1.1,which

depicts the

way

theemployment

recession-recovery episode in panel (d) materializesin this case. However, once

we

consider a heterogeneous productive structure thatexperiences ongoing creative destruction, other scenarios are possible. For example,

the

peak

indestructionduringthe recessionmay

befollowedby

an equal-sized troughin destruction during the recovery, adding

up

to a zero cumulative effect.More

generally, as illustrated in panels (a)-(c), the cumulative effect of a recession

on

overall restructuring

may

be positive, zero, or even negative,depending

not onlyon

how

theeconomy

contracts, but also onhow

it recovers. Thus, the relationbetween

recessionsand economic

restructuring requires us toexamine

theeffect ofa recessionon

aggregate separations not only at impact, but cumulatively throughoutthe recession-recovery episode.

Second, the

argument

that increased restructuring following recessions iswaste-ful relies

on

what

is ultimately a failure in private contractingon

the destructionmargin,

which

results in privately inefficient liquidations. However, thesame

typeof contracting failures are also a well-known source of under-investment, which, in

general equilibrium, naturally leads to insufficient restructuring (see, e.g., Caballero

and

Hammour

1998a). Thisform

of "sclerosis" ofthe productive structure suggestsHall acknowledges that his calculation captures only one aspect of the problem, and that a

that accelerated restructuring

may

bebeneficial. Thus, thesame

contractingproblem

points at a possible cost or benefit ofincreased restructuring, depending on

whether

it is consideredfrom

the destruction or creation margin. It is therefore essential to consider distortionssimultaneouslyon

both margins to assessthe social-welfareeffectof increased (or reduced) restructuring.

Figure[.I

RecessionsandCumulativeRestructuring

(a)Restructuring Increases

1 creation 1 destruction (b)RestructuringisUnchanged creation 1

r^

destruction <c)Restructuring Decreases iZT

destruction (!)UnemploymentRecession unemployment limeAn

adequatemodel

to assess the relationbetween

recessionsand

restructuring,and

its social-welfare implications,must

therefore incorporatetwo

main

elements.First, it

must

exhibita heterogeneous productivestructurethatundergoesa process of creativedestruction able tomatch

observedaggregate gross flowsand

theirdynamics. Thismakes

it possible to capture the cumulative impact ofa recessionary shock onthose flows. Second, it

must

include thepossibility of rentson both

the creationand

destruction margins, that can be calibrated to

match

the private rentsdocumented

in the financial

and

labormarket

literatures. This is needed to assess, in generalequilibrium, the social waste or benefits associated with the impact of recessions

on

gross flows.

This paper develops such a model.

We

present a stochastic equilibriummodel

of creative destruction that incorporates contracting difficulties inboth

the laborand

flows, as well as

documented

laborand

financialmarketsrents.We

combine

ourthe-oretical analysiswith empiricalevidence

on

aggregate gross flowsand microeconomic

rents,

and

revisit the debateon

the cost of recessionsand

its relation to aggregaterestructuring.

A

look at the available dataon

gross flows castsdoubt on

prevailing views.Our

time-series analysis of gross job flows in

US

manufacturing over the period 1972-93shows

thatthissector exhibited a reductionincumulativefactorreallocation followinga recession. This result contradicts the notion that recessions result in increased

restructuring. Essentially, althoughjob destruction peaks sharply at the impact ofa recessionary shock, it also falls below

normal

foran

extended period oftime duringthe ensuing recovery.

The

cumulative effect is a reduction in overall destruction.With

a stationaryemployment

response, reduced reallocation can also be seen injob creation,

which

falls during recessions but does not exhibit as a counterpart anabove-normal increase during the recovery phase.

The

existing evidence, although limitedinseveral respects, is consistent with the notion that recessions are associatedwitha "chill" ofthe restructuring process, ratherthan increased "turbulence." In the context of the

model

we

develop in this paper, the chill is in fact a natural outcome.We

identifytwo

mechanisms which

can beresponsibleforthis

phenomenon,

onefinancialand

the otherbasedon

selectionacrossheterogeneous productivities.

The

financialmechanism

resultsfrom

firms' reducedability to find financing for creation as they

come

out of recession. This impliesthat the recovery cannot take place through a

boom

in creation but rather througha reduction in destruction,

and

therefore that the recession-recovery episode resultscumulatively inreduced restructuring.

The

selectionmechanism, on

the other hand,works

through the differential impact across projects of the fall in creation duringrecessions

—

which

affects mostly low-productivity projects subject to ahigher-than-average churnrate and, thus, reduces the economy's average churn.

The

welfareimplications ofthechilldepend on which

oftwo

factorsdominate:how

sclerotic the

economy

is, in the sense that contracting obstacles in creation result inan

inefficiently lowequilibrium restructuring;and

how

wastefuldestruction is, in thesense that separations are privately inefficient.

Which

ofthosetwo

factors dominatesover the cycle determines

whether

the chill is costly or beneficial.We

argue that reasonable calibration assumptions lead to the conclusion that the chillis costly,and

that it adds

about

40 percent to the traditionalunemployment

cost ofrecessions.The

perspectivewe

put forthamounts

to a distinct alternative to prevalent viewsof recessions

and

restructuring. In particular, the traditional assessment based onthe costs ofjob loss holds that recessions are costlybecause they increase aggregate

separations,

and

that such separations are wasteful.The

view that emergesfrom

this paper also points to a cost of recessions, but that cost arises because

reces-sions decrease aggregate separations

and

therefore reducethe beneficialrestructuringassociated with such separations.

The

rest ofthe paper isorganized as follows. Section 2 presentsourmodel

econ-omy,

and

solves for equilibrium. Section 3 anchors the model's parameters basedon

macroe-conomic

evidenceon

gross job flowsand employment.

In particular, this sectiondocuments

theUS

manufacturing evidence of chill following recessions. Section 4 discusses the response ofthe restructuring process to aggregate shocks,and

itswel-fare consequences. Section 5 concludes.

2

A

Model

of

Restructuring

and

Fact

or-

Market

Rents

2.1

General

Structure

We

consider an infinite-horizoneconomy

in continuoustime,whose

general structureis outlined in figure 2.1.

Entrepreneur •Productivity:r

•Wealth: a

Figure2.1

The ModelEconomy (a)NewProduction Units

External Finance •SpecificFinancing:b=ij>tc-a •Generic Capital: (l-$)ic

(b)GrossFlows

Entrepreneurial Projects •Productivity:f(v)

•FinancingRequirements:g(b,A>

Production Structure Creation(H) 1

v

GoodSlate:n*(v, b) |,C BadStale:n'(v.b) trr. • ; Production unitsThere

is asingle durablegood

(the numeraire), that can either beconsumed

or usedas capital. Productiontakes place withininfinitesimalproduction unitsthatcombine,

infixedproportions,

an

entrepreneurialproject, a unit oflabor, and/tunits ofcapital(see panel (a) offigure 2.1).

The

output flow of production uniti at time t ismade

up

ofthree components:where

y~t isa stochastic aggregatecomponent;

V{G

[—v,T>] isapermanent

idiosyncraticcomponent

(the unit's "productivity");and

e» is a transitory idiosyncraticcompo-nent, en transits

between

two

states at probability rateA

>

0: e>

(the "good"state)

and

—

e<

(the "bad" state). Finally, production units failat exogenous rate(5>0.

Entrepreneurs, workers,

and

financiersEach

productionunitforms a nexusforatrilateralrelationshipbetween an

entrepreneur-manager, a worker,

and

external financiers.The

entrepreneur bringsthe projectand

uses his internal funds to finance it; the worker contributes his labor;

and

externalfinanciersfilltheunit's financingrequirements

when

theentrepreneur hasinsufficientfunds.

We

characterize each ofthose three parties, in reverse order.Externalfinance is provided

by

a non-resourceconsuming

competitive sector. Itmay

becalledupon

eithertofinance capital investmentat thetime a production unitis created, or to finance periods of negative cashflow during the lifetime ofthe unit.

The

stake of external financiers ismeasured by

the unit's net external liabilities, b(6

>

corresponds to positiveexternalliabilitiesand

b<

to positiveinternal funds).Workers

are infinitely-lived agentswhose

population is representedby

acontin-uum

ofmass

one.Each

workeri isendowed

with aunit of labor,and maximizes

theexpected present value ofinstantaneousutility

Cit+z(l-kt),

z>

0,linear at

any

time t inconsumption

c,tand

laborsupply llt, discounted atratep>

0.Entrepreneurs

maximize

the expected present value of consumption, alsodis-counted at rate p. All agents are therefore risk neutral,

and

themarket

discount rate will be p. Entrepreneurial projects are heldby

acontinuum

of non-activeen-trepreneurs indexed

by

i.Each

has a project for a production unit withknown

pro-ductivityVi,and

a certainamount

ofwealth that translates into a financingrequire-ment

bi—

equal to the project's investment requirementminus

the entrepreneur's wealth.2We

assume

that the distributions of wealthand

project productivities areindependent in the cross section.

At any

time t, the marginal density of projectproductivities is given

by

f{u);and

the marginal density of project financingre-quirements is

g(b;A

t),where

A

t isan

index of the aggregate wealth of non-activeentrepreneurs.3

Factor-market rents

The

employment and

financing relationshipswithinproduction units sufferfrom

con-tractingobstacles.We

assume

that a fraction(j)G

(0,1] ofa productionunit's capitalisspecific, in the sense thatits productive valuedisappearsifeitherlabor or the

man-agerleavesthe unit. Specificity withrespect to labor

and

management

isintended to2

Notethat if 6i

<

0, the unitstartswithpositive internal funds.Byfixingthe distributions of project productivitiesandfinancing requirements,weavoidhaving

to model the detailed population dynamics of potential entrepreneurs. Implicitly, we assume the process by which potential entrepreneurs invent or lose ideas for projects is suchthat it results in

capture the edge that such "insiders"

may

acquire to appropriate quasi-rents within thenexus ofthefirm.4 It creates a classic "holdup" problem. Agents' ex ante termsof trade need to

be

protected through a fully contingent contract. However, suchcontracts

may

be unenforceable or excessively complex,and

specific quasi-rents willinstead be divided according to the parties' ex post terms oftrade.5 This constrains certain

employment and

financing relationshipsfrom

being formed,and

results inrent

components

ofwages

and

profits thatwe

analyze in sub-section 2.2.The

non-specificcomponent

ofcapital, (1—

4>)n, hasfullcollateralvalue,and

givesrise to

no

contracting difficulties. Itsowner

canwithdraw

it atany

timefrom

therelationship,

and

use it elsewhere withno

loss ofvalue.Without

loss of generality,we

consider that it is always leased at a rental cost r>

0,which

covers the costof capital adjusted for depreciation. Because the rental cost of generic capital

and

the marginalutility ofleisureareunproblematic,

we

netthem

out ofproduction-unitoutput

and

definey~s=y

—

r(l—

<J))k

—

z.Production structure

dynamics

At

any time t, the distribution of production units is givenby

the density n^(b,v)of units that operate in the

good

state with external liability band permanent

pro-ductivity v,and

the equivalent density nj(b,u) of units in thebad

state.The

totalnumber

of units in thegood and

thebad

states are/V

r+oo r"u /-+oo/ nt(b,i/)dbdi>

and

Nf

=

/_/

n^{b,i/)dbdv,-VJ—oo J—VJ—oo

respectively. Total

employment

is, therefore,Nt

=

N+

+

Nf

and

unemployment

isU

t=

1—

Nt

Aggregate output isY

t=

J J

[(yt+

v

+

e)nf

(b,v)+

(yt+

v

-

e)rq

(6,i/)] dbdu.Four factors drive the distributional

dynamics

ofproduction units (see panel (b)of figure 2.1): (i) units are continuously created; (ii) units are also continuously

destroyed; (Hi) units

decumulate

or accumulate b, depending onwhether

theyexpe-riencepositiveornegativecashflows;

and

(iv) unitstransitbetween

thegood

and

thebad

idiosyncratic state at probability rate A.The

effect of distributionaldynamics

on

aggregateemployment

is captured by the aggregate gross rates of creationand

destruction ofproduction units

—

which

we

denoteby

H

tand

D

t, respectively.Creation of

new

production units requirestwo

conditions thatwe

derive in sub-section 2.3: the projectmust

be profitable,and

itmust

find financing.At

any pointInvestment specificity

may

result from firm-specifichuman and organizationalcapital, or fromtheadvantagethatapartycangainthroughgovernmentregulation. Itisclearlyonlyasimplification

toassumethat it isthesame fractionofcapitalthat isspecific to both laborand management.

'For a discussion ofthis "holdup" problem thatresultsfromspecificity, see,e.g.,Klein, Crawford

and Alchian (1978) andHart (1995, chapter 4). For adiscussion ofitsmacroeconomicimplications,

see Caballeroand

Hammour

(1998a).'This contractualform is not unique. Non-specific capital couldalso befinanced througha fully collateralized loan. As longasthe price of capitalremainsconstant, thetwocontracts arcequivalent

in time, allprojects thatsatisfy

both

conditions arestarted.The

entrepreneurhiresa worker,makes

aspecificinvestmentof0k,and

rents (1—

</>)kunitsof genericcapital.Ifthe entrepreneur'swealth isaz, theinitiallevel ofexternal liabilitiesisbt

=

4>k—

a*.We

assume

that allnew

production units start in thegood

state.Destruction ofproductionunitsisof

two

types. Itmay

eitherbedue

toafailureof the production unit (at the above-mentioned rate6), ordue

to a separation decision within a functioning production unit. Inboth

events, specific capital loses all valueonce factors separate.

The

latter type of destruction takes place during periodsof negative cash flows,

when

the entrepreneur stopsmaking

the investment that isnecessary to cover negative cash flows

and

continue operations.We

restrict ourselvesto a range of

model

parameters such that operational cash flows are always positivein the

good

stateand

negative in thebad

state. In thegood

state, positivecashflows allow a unit to reduce its liabilities over time, then accumulate internal funds; onceit transits to the

bad

state, the unitmust

decidewhether

to interrupt operationsor fund negative cash flows with the

hope

of reverting to thegood

state. Similarly to creation investment, thiscontinuation investment decision requirestwo

conditions thatwe

also derive in sub-section 2.3: the entrepreneurmust

find it profitable to cover the unit's negative cash flow,and

hemust

find financing for it. Destructiontakes place

when

one of thosetwo

conditions fails to be satisfied. Failure of theprofitabilitycondition results in privatelyefficientseparation

between

factors; failureofthe financing condition results in privately inefficient separation.7

2.2

Contracting

Failures

inthe

Labor

and

Financial

Markets

We

now

turn to the determination of factor rewardswhen

a fraction <j> of capitalis specific with respect to labor

and

to the entrepreneur-manager.The

contractingproblem

consists in the assumption that laborand

the entrepreneur cannotcontrac-tually

precommit

not to withhold theirhuman

capitalfrom

the relationship.We

analyze theeffect ofspecificitywith respect tolabor

on

theemployment

relationship,and

ofspecificity with respect to the entrepreneuron

the financing relationship.The

employment

relationshipWe

consider that laborand

capital (theentrepreneurand

external financiers) transactas

two

monolithic partners.8Because

of the contracting problem, specificquasi-rents

must

be divided ex post, after investment is sunk.We

assume

this divisionis governed

by

continuous-timeNash

bargaining.Labor

obtains, in addition to itsBecause we have assumed no joint-ownership of production units, a literal interpretation of

privatelyinefficientseparationsisintermsofbankruptcy. Thisinterpretationcan belooselyextended

topartialliquidations of afirm's activitiesbecauseoflimited funds. Ifanentrepreneur wereallowed

tooperateseveralproductionunitsata time,whicheffectivelyshareinthesamepoolofliabilitiesor

internal funds, financialconstraints

may

leadhim toinefficientlyliquidatesomeunitsbutnot others.One reason why labor

may

not be able to deal separately with the entrepreneur and externalfinanciers is informational. The entrepreneur

may

be able to disguise internal fundingin the formof external financing. If, however, labor isable to separatebetween the two, externalliabilities can

be used as a way to reduce the rents appropriable by labor. Sec Bronars and Deere (1991) for a

outsideopportunitycost, a share/3

G

(0,1) ofthe present value5

of the unit's specificquasi-rents, su;

and

capital obtains a share (1—

0)S.The

quasi-rents inproduction uniti aresit

=

{y!+

Vi+

eu)-

jtiwhere

w°

denoteslabor's flow opportunity costof participating in a production unit,abovethe marginal utility ofleisure (which isdirectly subtracted

fromy

s).

We

solvefor a

wage

path for each production uniti,wu

=

w°

+

(3sit, (1)which

gives the worker a share j3Sin present value atany

point in time. Profits are therefore equal toK

it=

(y~t+Vi

+

ea)-

w

it=

(1-

0)sit. (2)Finally, labor's opportunity cost is given

by

w°

t=^(3E

v[St]. (3)Ut

As

is standard in equilibrium bargaining models, it is equal to the rateH

t/U

t atwhich an unemployed

worker expects to findemployment,

multipliedby

the share 3Ev[St] he expects to obtainofthe surplus from hisnew

job.9Expression (2) allows us to defineprofit functions

nu

=

ii+

{vi\ Sit) in thegood

id-iosyncratic state

and

TXu=

7r_

(^,; £lt) inthe

bad

state,where

fit isa state vector thatconstitutes asufficient statistic forcurrent

and

futureaggregateconditions (includingvariables yf

and

w°). Ifthe unit has net uncollateralized liabilitiesblt, the expectedpresent discounted value ofprofit flows is a function

H

+

{bit,Vi\Clt)when

the unit isin the

good

stateand

U~(bit, Vi]Qt)when

it is in thebad

state.Those

functions are (weakly) decreasing in b, because, aswe

argue below, a higher 6 generally increases the probability of privately inefficient liquidation. Henceforth,we

will replace theargument

Qt by a time subscript to saveon

notation.The

financing relationshipThe

financing relationshipisrestricted to uncollateralizable investments, becausethecollateralizable share ofcapital (1

—

4>)k is unproblematicand

is considered rented.Specificity with respect to the entrepreneur-manager gives rise to contracting

prob-lems similar to those that arise in the

employment

relationship.The

entrepreneur-manager

can always threaten ex post towithhold hishuman

capitalfrom

theproduc-tion unit,

and

attempt to renegotiate with the financieron

that basis.We

assume

that

Nash

bargainingwould

givea sharea

G

(0,1) ofthe present valueIIofprofits to the manager,and

ashare (1—

a) to the financier. Therefore,any

external claim forthe financier above (1

—

q)II will be renegotiated down. This putsan upper-bound

on the external claims a production unit cansupport.

For a detailed derivationofa similarexpression, see the appendixin Caballero and

Hammour

(1998b).The

inability to find financingmay

preventan

entrepreneurfrom

starting anotherwise profitable project; or

may

forcehim

to liquidate a highly productive unit that runsinto aperiodofnegativecash flows (seesub-section 2.3).As

aconsequence, an optimal policyfortheentrepreneurthatminimizestheriskofinefficientliquidationis not to

consume

dividends until the production unit fails or is liquidated.10 Thisimplies, in particular, that

repayments

to the financier are effectivelymade

at thefastest possible rate.

A

contractthatminimizesthefinancialconstraintmust

satisfythe followingprop-erties: (i) thefinancierexpects toget his

money

backin present value; (ii) theabove-mentioned

re-negotiation constraint is notviolated;and

(Hi) theentrepreneur cannotconsume from

the project's cash flow before thefinancier's claim hasbeen

fully paid.A

financial contract with those properties can be thought of as a senioruncollater-alized claim b over the unit's cash flow held by a single financier, with a preferred

return equal to the risk-adjusted opportunity cost of funds.

Our

model

does not distinguishbetween

differentinstitutional arrangements—

debt-likeor equity-like—

aslong asthey result in the

same

investment decisionsand

net transfersbetween

thetwo

parties.2.3

Creation

and

Continuation

We

now

derivethe conditions underwhich

creationand

continuation investmentsareundertaken.

The

former investment consistsofthe specific investment4>krequired to createa production unit.The

latterconsist ofthe investmentsmade

tocover periods ofnegativecash flows in order to hoardthe unit's specific assets.By

its very nature, continuation investment is fully specificand

subject to contracting obstacles.Both

types of investments are subject to a financial

and

a profitability constraint.They

will only be undertaken if

both

constraints are satisfied.Creation investment

Suppose an

entrepreneur with wealth a has a project for a production unit withproductivity v.

To

create the unit, the entrepreneur needs to incur a net liabilityb

=

4>k—

a.The

two

conditions for undertakingthe project are as follows. First, theentrepreneur

must be

able to attract the required financing,which

we

have seen islimited to the

maximum

liability6<(l-a)II+(M.

(4)Second, the project

must

be profitable:4*K<nt(b,u).

(5)10

This statement must bequalifiedby theobservation that, ifthe aggregatevariabley has finite

support, there is a level baafc

<

of internal funds beyond which the production unit is immunefrom inefficient liquidation. Thishappens whenthe interest incomepb3afe on internal funds covers

any possible negative cash flow7r~ in the bad state. Beyond b3afe, the entrepreneur is indifferent

between consumingdividends ornot.

Since IT+ is decreasing in 6, constraints (4)

and

(5) can be rewritten as4>k

-

a<

bt{v)=

min{6f+(z/),^+

(i/)},rf

(6)

tp

where

b\ isdenned

implicitly by taking the financial constraintwith equality,and

bt is definedby

takingtheprofitability constraintwithequality (eithervariablecantake value+oo

when

the constraint isnot binding). Figure2.2(a) illustratesthe operationofthe profitability

and

financialconstraintson

the creation ofprojects withproduc-tivities v\

and

^2? v\

<

v%-For projects with productivity v\, it is the profitability vi) that is binding; while for projects with productivity V2, it is

—P-r

constraint b

<

b/+/

the financial constraint b

<

b (1/2).Figure2.2

ConstraintsonCreationand Continuation

(a)Creation Investment

n-(6.v. Ob<"(.,)h'•(,,> (b)ContinuationInvestment IT(*.-,) ITli.vj Continuation investment

Given

our restriction to parameters such that cash flows are positive in thegood

state

and

negative in thebad

state—

i.e.^t(

u)>

and

7rt~(^)

<

—

continuationinvestment is always required in the

bad

state. It faces financialand

profitability constraints, bt (v)

and

bt (v), similar to the constraintson

creation.The

financial constraintmay

affecta

unit in thebad

state withno

internal fundsto cover its negative cash flow (6

>

0). This can be illustratedmost

easily in asteady-state setting,

where

aggregate conditionsQ

are invariant. In the absence of financing constraints (i.e., taking the limit b—

+—

oo), one canshow

that the value of the option to cover negative cash flows in thebad

state is7r-(t/)

+

An+(-oo,i/)

P+S+X

'{)

However, because the

manager would

renegotiate the debtdown

tobf+ (i/)

=

(1- a)n+

(bf+(i/),z/)once in the

good

state, one canshow

that the value to the financier ofthe option tofinance negative cash flows is

no

greater thanir~(u)

+

X(l

- a)U+

(bf+{v),v)p

+

6+

X

which

is obviously smaller than the private value (7) of continuation. It is therefore possible for privately inefficient liquidation to take place,where

continuation haspositive present value but cannot be financed externally.11'12

Furthermore, one can

show

that if the entrepreneur is able to attract external finance for continuation, he will be able todo

so irrespective ofthe current level of1 L

Conceivably, the financier

may

offertheentrepreneuran "insurance" arrangement throughwhichhe commits to finance negative cash flows in the bad state in exchange for an insurance premium

paid inthegood state. With largeenough cashflowsin thegoodstate, the financiermay beableto

breakeven. However, insurancegivesrisetoaninformationalproblem ifthe financiercannot observe

the unit's idiosyncratic state. The entrepreneur need only claim to be in the bad state to collect

the insurance. As is well knwon, the informational problem is less severe under a simple liability

arrangement,wheretheentrepreneurmust liquidatehis productionunitto discontinuepayments to

thefinancier. 1

When

a privately inefficient separation takes place, both theentrepreneur and labor lose theirshare ofthe production unit's surplus

S

t~(6,i/). Could labor come to the rescue by taking a wagecut? One canshowthatthemanager-owner isalsosubjectto afinancing constraint withrespect to

the worker, similar to that with respect to anexternal financier.

We

constrain theparameter spacesothatthisworker-financing constraintis always binding.

To see this, consider the continuous-time Nash bargaining solution behind wage equation (1),

wherelaborandtheentrepreneurget orcontributetheirshare

—

/3and(1—

/?)—

ofthe flow surplusst. Iftheentrepreneur runs outof internalfundsin thebad state,andisunabletofinance hisshare

ofthe negative surplus, the Nash bargaining problem becomes constrained and the above solution

breaksdown. It

may

make sense for theworker, in that case, to finance thewhole ofs^(u) in thebadstateinorder to retainhisshare/3S

4 +

(6,v) inthegoodstate. Thesteady-stateconditionfor this tohappenis

st"(^)

+

A/35t+(-oo,^)

>

0.

On

the otherhand, thecondition forcontinuation tobeprivately efficientisSt{y)

+

ASt+

(-oo,i/) >0.

It is therefore clear that as long as (3

<

1, financing may not be worth it for labor even whencontinuation isprivately efficient.

b

>

O.13 In other words, themaximum

liability b (u) for continuation financing tobe feasible can take only

two

values: or +00.The

interesting case for us iswhen

continuation in the

bad

state cannot be financed.We

therefore restrict ourselves toparameters under

which

negativecash flows in thebad

state are significant enough,so that the finance constraint

on

continuation is always binding:b{~(v)=0,

v e

[-V,V], t>

0.The

financial constrainton

continuation is illustrated in figure 2.2(b),where both

production units are financiallyconstrained in the

bad

state.Let us

now

turn to the profitability constraint for a unit that still has internalfunds (6

<

0) to cover negative cash flows. Profitability requiresnr(fc,z/)

>o.

This leadsus to define

V

t (u) as the lowest value ofb for

which

IIt ~(6,u)

=

0.One

canshow

that, in steady state,V

t also takes onlytwo

values:—00

or 0."In other words, if a unit has internal funds

and

transits to thebad

state, it eithercontinues until forced to exit

when

b reaches ~bt

=

0; or it exits voluntarilyupon

transitinginto the

bad

state, irrespective ofits level ofb. In theformer scenario, theunit isfinancially constrained; in the latter, it is profitability constrained.

2.4

Aggregate

Dynamics

We

close themodel

by discussing the distributionaldynamics

that govern theaggre-gate production structure.

We

examine, inturn, thedynamics

ofaproduction unit'sexternal liabilities; the aggregate gross creation

and

destruction rates of productionunits;

and

the wealthdynamics

that determinenew

projects' financingrequirements.Dynamics

ofertemal liabilities''

Consider two non-negative levelsofexternal liability,6i,isi>

>

&i »->

0. Ifthefinancieriswillingto financecontinuation at6iow, he has all the more reasonto financeit atfchigh, since his returnin

that case can only begreater. Conversely, ifcontinuationis financed at6|,igi,, theentrepreneur can

alwaysfind an interest rate path that willattract finance at&]„»•• Onesuchpath is to increase the

liability instantly to &i,ig h, at which levelwe knowthat external finance can beinduced. This path

ispreferablefortheentrepreneur to inefficient liquidation, although hegenerallyhasmore favorable alternative paths.

'''The argument why, gcnerically, b (v) € {-00,0} in steady state is as follows. LetVd

be the

levelofproductivityatwhichaunitwithinfinitefunds(6

=

—00)isindifferentbetween continuingorliquidatinginthebadstate,i.e. n~(T/d)+\Tl+ (-00,

P

d

) =0. (i)

When

v=

Vd

,the value

n~

ofa unitinthebadstateiszero,irrespectiveofits levelof6; whichimplies thatitsvalueIT inthegoodstate

isalsoindependentofb. Thus, anyunitinthebadstatewillalso findthatir~(J)d)

+

An

+ (b,T'd'\

=

irrespective of6, and will be indifferent between continuation and liquidation, (li)

When

v<

Vd,

it is clear that continuation is undesirable for any unit in the bad state, irrespective ofthe level of 6. (in)

When

u>

Vd, continuation is strictly desirable irrespective of6 for any unit in the bad

state,becauseit must bestrictlymoredesirablethanin the casev

=

Vd. From alloftheabove,oneconcludesthat, gcnerically, b (1/) takes either value—00 (whenv

<

~vd) or (when v> Vd ).

The

dynamics

of a production unit's external liabilities, b, are determined by the required risk-adjusted return.They

are given by15;

_

j (p

+

S+

X)b

t-n

t, bt>

0;1

\

pbt-n

t,h<0.

Recallthat

we

have restrictedourselves to the casewhere

negativecash flows cannot be financed externally in thebad

state.With

positive external liabilities (bt

>

0) - which,by

assumption, onlyhappens

in thegood

state—

the external financierrequires a return

p

+

6+

A, to cover the opportunity cost p ofcapital as well as the probability 6+

A of failure or bad-state liquidation.With

positive internal funds(bt

<

0), the entrepreneur earns the interest ratep.Gross Creation

For each productivityu,

we

haveseen that there isminimum

wealth compatiblewithcreation constraints (6)

—

which

translatesintoan

upper-bound

6<

bt (v)

on

initialleverage.

We

define y^ as the productivity atwhich

an entrepreneur with infinitefunds

would

be indifferentbetween

creating or not. Total gross creation isr77 flt {u)

H

t=

g(b;A

t)f(v)dbdv.Jvf J—oo

With

the accounting ofthe units that are created atany

point in time at hand,we

can go back

and

explicit labor's flow opportunity cost (3),by

writing an expression for the quasi-rents a worker expects to capture in a futurejob:EASt]

=

T^pL

tL

n

"

M

—

m

—

dbdv

-Gross destruction

The number

D

t of production units destroyed atany

point in time ismade

up

ofthreecomponents:

A

=

Df

+

D

ts+

D{,

where

Df

=

6(1-U

t); (8)D?

=

A

f

'_ ' / *n+

(b,is)dbdv

+

max{p

d t,0}f

n^(b,is?)db; (9) J—V J—oo J —ooD

*=

X

[l

[*"?&,»)

dbdv

+

r

nt (0,v)bt \ dv. (10) Jvd t JoJ-V

l(6,e)=(0,-e)The

three terms correspond, respectively, to exogenous failures, "privately efficient"(or "Schumpeterian") destruction,

and

"privatelyinefficient" (or "spurious")destruc-tion, (i)

The

first term,D$

, captures the flow of units that failforexogenous reasons.'Wcfollow the conventionofdenotingthe time-derivative ofafunctionx(t) by

i=

dx/dt.(ii) Privately efficient (or Schumpeterian) destruction

D

s captures units destroyedbecause they hit a profitability constraint

on

continuation. Define vf as the level ofprofitability at

which

a unitwith infinite internalfundswould

be indifferentbetween

continuing or not in the

bad

state.The

firstterm

captures units that turnunprof-itable because they enter the

bad

state with productivity v<

vf; the second, unitsthat turn unprofitable because theycrossthat threshold while inthe

bad

statedue

todeterioratingaggregate conditions. This type of destruction is a

form

ofSchumpete-rian destruction, by

which

unproductivecomponents

of the economy's productivestructure are renovated.16 (Hi) Privately inefficient (or spurious) destruction,

D{

,measures destruction

due

to financial constraints.The

firstterm

inD(

is the flow of units that turnbad and must

be liquidated because of insufficient capitalization;the second

term

captures the flow of units in thebad

state that run out of internalfunds.17

Initial wealth

dynamics

Recall that

we

specified the marginal density g(b;At) ofnew

projects' financingre-quirements as a function of an index

A

t of the aggregate wealth of non-active en-trepreneurs. Inorder to allow foran

effect ofaggregateconditionsy~ton

the latter—

as emphasized,e.g., by

Bernanke

and

Gertler (1989)and

Kiyotakiand

Moore

(1997)-

we

assume

thatA

t follows the followingprocess:A

t=

4iyu

A

t),V-i>0,

4> 2<0.

(11)Our

model

is focusedon

tracking in detail the internal fundsdynamics

ofproduc-tion units in operation, but not the population

and

wealthdynamics

of potential entrepreneurs.Although

itwould

be methodologicallymore sound

to track thede-tails ofthelatter, doingso

would

add

anotherdimension ofcomplexity to our model.Our

specification uses ashort-cut designedto capture the essence of the distributionofinitial wealth

and

its cyclical dynamics.3

Empirical

Anchors

In thissection,

we

discuss the empiricalevidenceon theUS

economy

which

we

use to"anchor" our model's parameters.

Our

missionisclearly nottoresolve thecontrover-sies that characterizethe relevant empirical literatures, or todemonstrate that there

isonlyone defensibleparametrization.

What

we

argueis that a reasonable reading ofthe evidence

—

not necessarily the only reasonable reading—

leads to a perspectiveon the cost of recessions that is surprisingly different

from

prevailingviews. 1'Thisisa rather simplisticviewofSchumpeteriandestruction. See, e.g.,Caballeroand Hamraour

(1994) for a vintage model of creative destruction. In contrasting Schumpeterian with spurious destruction, we do not mean to attribute to Schumpcter the view that separations are privately efficient.

What

weattribute to him is the idea—

central to his "liquidationist" view of recessions—

that destructionis highlyselective.All else beingequal, the lower a unit's productivity, the more likely it is to be liquidated due

tofinancialconstraints. This "selectivity" ofspurious destruction makesthe differencewith

Schum-peterian destructionless stark than mayappearat firstglance.

The

evidence that plays a central role in this exercise relates to (i) averageand

cyclical features of aggregate

employment and

ofjob flows;and

(ii) private rents tofirms

and

workerson

the creationand

destruction margins.We

generally relyon

existing literatures for evidence. However, there is one central question concerning

which, asfaras

we

areaware, thereisno

empiricalliterature—

namely

thecumulative impact ofaggregate shockson

grossjob creationand

destruction flows.We

start byexamining

this question in sub-section 3.1,and

advance the case of chill following a contractionary aggregate shock.We

then turn to calibrating the model'sparametersinsub-section3.2, based

on

existingevidence as wellas theresults ofsub-section3.1.3.1

Semi-structural

Evidence:

A

Case

of

Chill

Using data

from

theUS

manufacturingsector over the period 1972:1-1993:4,we

pro-pose

two

approaches toexamine

the cumulativeimpact of "aggregate" business cycleshocks

on

job flows.The

"single-factor" approachassumes

that aggregate shocks are the only driving factor behindemployment

fluctuations; the "two-factor" approachassumes

there aretwo

factors, aggregateand

reallocation shocks. In both cases,our time-series results indicate that

US

manufacturing exhibited a chill followingrecessions.

The

evidencewe

find does not support thecommon

presumption

thatrecessions are associated with a cumulative increase in restructuring.18

The

dataFigure3.1presentsour data

on

manufacturingemployment and

gross flows.The

solid line in panel (a) depicts manufacturingemployment

divided by itsmean.

Forcom-parison,the

dashed

linepresents theeconomy-

wideunemployment

series (rescaled).19The

two

series clearlypresent a very similarcyclicalpattern, a featurewe

will exploitwhen we

testand do

not reject the stationarity of theemployment

series. Panel(b) reports the pathof grossjob creation

and

destructionflows, defined as the basic quarterly creationand

destruction rates reported by Davis, Haltiwangerand Schuh

(1994, henceforth

"DHS")

multipliedby

the aggregateemployment

seriesfrom

panel(a).20 All dataare seasonally adjusted using the

Census

Xll

procedure.18Data

limitations do not allow us to analyze sectors outside manufacturing. Sincea significant

portion oflayoffsin

US

manufacturingarctemporary, thisbiasesour resultsagainstthechillfindingbecausethe resultingturbulencedoes notcorrespondtotrue restructuring.

On

theotherhand,someworkers who are laid offfrom manufacturing may find temporaryjobs in other sectors. This may

meanthattheaggregateeconomyexhibitslesschillthan manufacturing, butagaintheappearanceof

thosetemporaryjobs

—

whichinvolve negligibleinvestment—

does notrepresenttrue restructuring. 19Source:

FRED.

Moreprecisely,

DHS

calculatetheircreationanddestruction rateseriesastheratioofjobflows toaverageemploymentfor plantsin theirsample. Forconsistency, wefirst transformthedenominator

ofthe

DHS

series from average to lagged employment.We

then multiply by lagged manufacturingemployment, measured inthemiddlemonth ofthe quarter, toobtain our flowscries.

Instead of using aggregate manufacturing employment, we could have used employment in the

DHS

sample. The latter serieshas a time-trend that is not present in the former, but the two areotherwise broadlyconsistent.

We

ranourregressionsusing theDHS

employmentseriesandobtainedverysimilar results.

Figure31a

ManufacturingEmploymentand [-JCivilanUnemployment

c?o 62

year Figure3.1b

JobCreationa-id Destruction Flows

M

/! 1 ' k ' '.AiiyUAfsiU

L/\.

/llv

A/ h V »' v ' V t 1~:

B2 year 90 94We

denote theemployment,

creation,and

destruction series in deviationfrom

their

mean

by

Nt, fit,and

D

t, respectively. In principle, those series are related bythe identity

AN

t=

H

t-

D

t. (12)In practice, this identity does not hold strictly because of the

way we

constructedourjob flow series

—

as the product ofDHS

rates times manufacturing rather thanDHS

employment.

Single-factor approach

We

firstassume

thatemployment

fluctuations are drivenby asingle aggregate shock. Since creationand

destruction are related by (12), a linear time-seriesmodel

for the response ofjob flows to aggregate shocks can generally be written either in terms ofcreation:

H

t=

h(L)(-N

t)+4;

(13) or in terms of destruction:D

t=0

d(L)(~N

t)+

ef; (14) 17where

L

is the lag-operatorand

6X

(L)

=

9X+

9\L

+

9XL

2+

... . If identity (12)were exact, those

two

equationswould

be equivalent, with e1}=

ed.Given

the noiseintroduced into (12), there are grounds for estimating each equation independently.

We

report results for the following specification:211

—

p

LiPanels (a)

and

(b) offigure 3.2 portray the estimated impulse-response function of (minus)employment and

job flows, respectively, to a 2-standard-deviationreces-sionary shock.

As

iswelldocumented by

DHS,

atimpact job destructionrisessharplyand

job creation declines to a lesser extent. Lessknown

iswhat comes

next.Along

the recovery path, job destruction declines

and

falls below average for a significantamount

of time, offsetting its initial peak.On

the other hand, job creation recovers to its averagelevel but does not exceed it toany

significant extent tooffset its initialdecline.22

Assuming

stationaryemployment,

the qualitative difference in thetwo

series' behavior, if significant, is only consistent with a chill effect. This is

shown

inpanel (c),

which

reports the cumulative responses ofjob creationand

destruction.Given

(12), the stationarity ofemployment

impliesthat6h(l)—0

d(l)=

0.We

test thishypothesisand do

notreject itat anyreasonablesignificancelevel. Stationarity ofemployment,

however, does notmean

that 9h(l)and 0(1)

are equal to zero.On

the contrary, the constraint 9 (1)

=

9 (1)=

is clearly rejected in favor ofan

alternative that sets 9h{\)

—

9 d(l)

<

0.24 Thismeans

that the cumulative effectof a shock

on

gross flows is significantly negative.On

a series-by-series basis, it isdestruction that ismostly responsible for this rejection.25

Two-factor approach

The

chill result does not changemuch

in a richer,more

standard time series setting.We

now

assume

thatemployment

fluctuations are driven bytwo

types of shocks,and

use a semi-structuralVAR

approach to identify them.Given

the previous test,we

maintain the assumption thatemployment

is stationary.By

equation (12), theintegral of

H

—

D

must

therefore be stationary.20 For chill or turbulence effects tobe

consistent with this fact, the integrals ofH

and

D

must

be cointegrated with2

'Ourqualitative, andtoalarge extent quantitative, resultsarerobust todifferentlag structures. 22

Hall (1999) coins theterm "concentrated series" to describe serieswhich lump adjustment, in

the sense thata burst of activitytoday predictsabelow averagelevel ofactivity in thenear future.

Thisis a necessarybut not sufficientconditionforachill, which requires thatreduced activitymore

thanoffsetstheintial burst. He findsthatwhilejob destructionisconcentrated, job creationis not,

whichisconsistent with ourfindings.

"Estimatingjointly equations (13) and (14) without imposing stationarity, h(l)

—

6d(l)=

0,yieldsa likelihood of675.5; while imposingstationarity onlylowers the likelihood to674.8.

2

'Ifweimpose h(l)

=

d(l)=

onthejointestimationof(13)-(14),the likelihooddropsto671.4."Estimating equation (13) separately with and without the constraint that 9h(l)

=

yieldslikelihoodsof346.8and347.3, respectively. Doingthesamefor (14) withandwithoutthe constraint 6d(l)

=

yieldslikelihoods of323.5and 327.0, respectively.''Thisassumes that the measurement noise introducedintoequation (12) is stationary (possibly

witha deterministic trend)

—

a hypothesiswecannotreject.cointegrating vector (1,-1). Using this low-frequency restriction efficiently suggests

running a

VAR

with the cointegrating vector (equal toN)

and

one ofthe integralsfirst-differenced (e.g., D).

We

write our semi-structuralVAR

asNt

£>t

=

A(L)

where A(L)

=

Ao

+

A\L

+

A^L

+

...and

(e", e[) represent i.i.d. innovations thatcor-respond to aggregate

and

reallocation shocks, respectively. Besides normalizations, achieving identification requirestwo

additional restrictions. For this purpose,we

as-sume

that thetwo

innovations are independent ofeach other,and

that, at impact,a recessionary shock raises destruction

and

lowers creation.Based

on

Davisand

Haltiwanger (1996),

we

set the relative size of the absolute response of destructioncompared

to creation to 1.6,which

is roughly the value thatmaximizes

thecontri-bution of aggregate shocks to net

employment

fluctuations with their estimates.We

experimented with values ofthe relative response of destruction to creation in the

range [1,2], without a significant change in our

main

conclusions.bnsulw roesonBB(angle doctor): (minus)Emp'ovmsnt

Fgm-«32b

Impu'WRwacnso(»nBte foclor]JobCr^olionend Dwt/uctwn

Since

we

are particularly concerned withmedium

and

low frequency statistics,we

used a fairly non-parsimonious representation ofthe reduced-form

VAR

and

allowedfor five lags.

The

firstand

secondcolumns

offigure 3.3 represent impulse-responsefunctionscorresponding to recessionary 2-standard-deviation aggregate

and

realloca-tion shocks, respectively, for (minus)employment,

gross flows,and

cumulative grossflows.

The

firstcolumn

exhibits a case of chill following a recessionary aggregateshock,

which

is qualitatively similarand

quantitatively larger thanthe chillobtainedwith the single-factor approach.27

The

secondcolumn

depicts responses torealloca-tion shocks, which, not surprisingly, generate turbulence.28

Figure 3.3o flggr.Impulse(minua)Employment

Figure 3.3b Pmo\.Inpulw:[mnuOEmployment.

figure 3.3c

Agar,impulse:JobCraH'JcnendDestruction

Figure 3.3C

fleallimputes:JobCreator,andDestruction

Figure3Je Figure3JF

Aggr.Impulse-CunJabCreationandDestruction Reel.Impulse:Cum.JobCr-eatcnend Deetructon

27

We

ran bootstrapstotesttheno-chillhypothesis,andrejectedit. Thecorrespondinghistogramsarepresented intheworking-paper version ofthisstudy (Caballeroand

Hammour

1998c).Our qualitative resultsare robust to thenumberoflagsused (we tried between 2 and 6lags), to

whetherthe 1974-75 recessionisexcluded, or toestimatingthe

VAR

forthelogarithmsof(N,D/N)

ratherthan (N,D).•"'"SeeDavis andHaltiwanger (1999) fora comprehensive study oftheresponse ofjob flows to oil shocks,which havea significant reallocationcomponent.

3.2

Parameter

Choice

We

cannow

turn to the choice of parameter values in our model. Six parameterscharacterize technological aspectsofproductionunits: k,e, A,6, 4>,r;

two

characterizeinstitutionalaspectsofrentsharing:

a

and

/?;and two

characterize preferences:p and

z.

We

alsoneedto specificityfunctional forms with theirassociated parameters.The

joint distributionof project productivitiesv

and

financing requirements bisassumed

uniform in

v

on

the interval [—V,V]and

uniform in bon

[0, 6max

], with total

mass

At?

9The

dynamic

process ip{y,A) that governs internalfunds available for creationis

assumed

linear. Finally, "business cycle"dynamics

for the aggregatecomponent

yt offirmoutput is

assumed

to follow an Ornstein-Uhlenbeckprocess:dyt

=

-l{yt-

V)dt+

adWt,

j,a

>

0,where

Wt

is astandardBrownian

motion.30Table 1

summarizes

the valueswe

chose for the above parameters, basedon

ob-served features of theUS

economy.We

firstdiscuss calibration ofsteady-statefeatures ofourmodel

basedon

evidence concerning (i) general features oftheeconomy

that are less central to our argument; (ii) factor-market rents;and

(Hi)unemployment

and

gross flows.We

then discuss the aspect of calibration that is basedon

cyclicalfeaturesoftheeconomy.

A

number

ofparameterswerecalibratedby fittingquantitiesthat arise endogenously within our model.

Although

thisamounts

to asimultaneousequationsexercise, it will be intuitivetothink ofit in termsoftheassignment ofone parameter for each fitted quantity.

Generalfeatures ofthe

economy

(i)

The

discount ratewas

set top

=

0.06. (ii)The

gross rental-cost of genericcapital

was

set to r=

0.135.Given

the discount rate, thismeans

a depreciationrate of 7.5 percent,

which

fallsbetween

the rates of depreciation of structuresand

equipment

(source:BEA).

(Hi)The

aggregatecomponent

yofproduction-unit.outputwas

chosen in such away

as to normalize aggregate output to one. (iv)The

capitalrequirement ofa production unit

was

set to k=

1.94, which is the value needed tomatch

the observed capital/output ratio (equal to 1.9 for theUS

business sector in1995; source:

OECD).

31 (v) Entrepreneurs' share parametera

determinesthe return29

By

definition,6max mustsatisfy the constraintbmax<

4>k.''"Strictlyspeaking, some realizations ofan Ornstein-Uhlenbeck process will violate two

assump-tions we made in sub-section 2.3

—

namely that we restrict ourselves to parameters suchthat the following propertiesalwayshold: (i) nf>

and n^<

0; and (ii) bt=

0.We

therefore need to assume that the process foryt is adequately regulated so as tosatisfy those two assumptions; andcheck that theyarc alwayssatisfied inour simulations.

Another, relatively minor issue is that expression (9) for D\ is not compatible with an

infinitc-~

—dvariations specification for y, because term utis ill-defined.

We

chose to retain this expression forexpositional simplicity. This is of no practical relevance to our simulations, which are based on a

disretized version of the model.

3

'One mustdistinguish between the amount of capital actuallyutilized in production units, and

capitalas measured using national accounts perpetual inventory procedures. In our case, since the separation rate ishigher thanthe depreciation rate of generic capital, the former stock of capitalis less thanthelatter. Ourcalibrations areaimed at matchingmeasuredcapital.

premium

on

internal funds,and

hence the economy's profit rate.We

set it to the valuea

=

0.7 that yields a profit rate of 15 percent, (vi) For the dispersion of project productivities,we

setV

=

0.106 near themaximum

value compatible withthe model's constraint

on

bad-state financing. This corresponds to±10

percent ofaverage productivity.

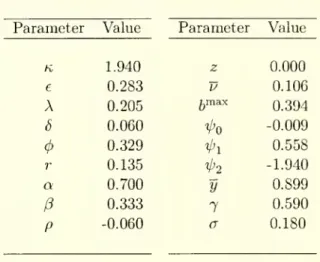

Table 1:

Model

ParametersParameter

ValueParameter

ValueK

1.940 z 0.000 € 0.283V

0.106X

0.205 i.max 0.394 8 0.060 V'o -0.009 4> 0.329 V'i 0.558 r 0.135 i>2 -1.940a

0.700 y 0.899P

0.3337

0.590 P -0.060a

0.180 Factor-market rentsOur

model

exhibits private rents to laborand

firmson

the creationand

spurious destructionmargins, (i)Abowd

and

Lemieux

(1993) estimate the equivalent oflabor'sshare of rents to fallin the range [0.23,0.39].32 Usinga value of(3

=

1/3 for labor'sbargaining share,

we

obtain an average rentcomponent

of wages equal to 8 percent oftheaverage wage.33 (ii) Aldersonand

Betker (1995) estimate the liquidation value of a firm to be about 2/3 of firm assets. This leads us to set the capital specificityparameter cj> to about 1/3,

which

results inan

average flow renton

the firm's sideequivalent to 6 percent of the average wage. (Hi)

On

the destruction side, privatelyinefficient separations can cause rent losses to labor

and

to the firm.The

literatureincludes a wide range of estimates for the cost of job loss, that range

from

lessthan 2 weeks of

wages

to substantiallymore

than a year.3'

1

Using

unemployment

insurance data,

Anderson

and

Meyer

(1994) estimatean

average worker loss of 14weeksofwages.

Although

this isan estimated averageoverallpermanent

separations- including privately efficient ones

—

we

apply it conservatively to the privately inefficientcomponent

ofseparationsD?.

35The

literatureon

the firm side ismuch

less developed.Hamermesh

(1993, pp. 207-209) surveys various estimates, with32

Scc Oswald (1996) forasurveyof the related literature. 3,!

Expressions for private rentson the creationand spurious destructionmargins can be found in

theworking paper version (Caballeroand

Hammour

1998c).3'4

See, e.g.,

Ruhm

(1987), Topel (1990), Farber (1993), Jacobson, LaLonde and Sullivan (1993),and Whelan (1997).

In fact, the median loss is ofonly about one week ofwages while about 9 percent of workers

suffer aloss ofmorethan a year.