working

paper

department

of

economics

COMPARATIVE

STATICS

UNDER

UNCERTAINTY:

SINGLE

CROSSING

PROPERTIES

AND

LOG-SUPERMODULARITY

Susan Athey

96-22

July1996

massachusetts

institute

of

technology

50 memorial

drive

Cambridge, mass.

02139

Susan Athey

Digitized

by

the

Internet

Archive

in

2011

with

funding

from

Boston Libr^y

iCoii^brtium

IVIember

Libraries

COMPARATIVE

STATICS

UNDER

UNCERTAINTY:

SINGLE CROSSING PROPERTIES

AND

LOG-SUPERMODULARITY

Susan

Athey*

July,

1996

Department of

Economics

MassachusettsInstituteof

Technology

E52-251B

Cambridge,

MA

02139

EMAIL:

[email protected]

ABSTRACT:

This paper develops necessaryand

sufficient conditions formonotone

comparative statics predictions in several general classes of stochastic optimization

problems.

There

aretwo main

results,where

the first pertains to single crossingproperties (ofmarginalreturns,incrementalreturns,

and

indifferencecurves) in stochasticproblems

with a singlerandom

variable,and

thesecond

class involveslog-supermodularityoffiinctions withmultiple

random

variables(where

log-supermodularityofa densitycorresponds to thepropertyaffiliation

from

auction theory).The

results arethen applied to derive comparative statics predictions in

problems of

investmentunder

uncertainty, signaling

games,

mechanism

design,and

games

of incomplete informationsuch

as pricinggames

and

mineral rights auctions.The

results are formulated so as tohighlight the tradeoffs

between assumptions

aboutpayoff

functionsand assumptions

about probabiUty distributions; further, they apply

even

when

the choice variables arediscrete, there are potentially multiple optima, or the objective function is not

differentiable.

KEYWORDS:

Monotone

comparative statics, single crossing, affiliation,monotone

likelihoodratio,log-supermodularity,investment

under

uncertainty,riskaversion.I

am

indebtedto Paul Milgrom andJohn Roberts,my

dissertation advisors, for their advice and encouragement. Iwould furtherlike to thank Kyle Bagwell, Peter Diamond, Joshua Gans, Christian GoUier, Bengt Holmstrom, Eric

Maskin, Preston McAfee, Chris Shannon, Scott Stem, andespecially Ian Jewitt for helpful discussions.

Comments

from seminar participants at the Harvard/MIT Theory Workshop, University of Montreal, and Australian National

University, aswell asfmancial supportfromtheNational Science Foundation,the State Farm Companies Foundation,

1.

Introduction

Since

Samuelson, economists have

studiedand

applied systematic tools forderiving comparativestatics predictions. Recently,this topic has received

renewed

attention(Topkis

(1978),Milgrom

and

Roberts (1990a, 1990b, 1994),

Milgrom

and

Shannon

(1994), Athey,Milgrom,

and

Roberts(1996)),

and

two main

themes have emerged.

First, thenew

literature stresses the utilityof

havingsimple, general,

and widely

applicabletheorems

aboutcomparative

statics,thusproviding insight intothe roleof various

modeling assumptions and

eliminating theneed

tomake

extraneous assumptions.Second,

this literatureemphasizes

the roleof

robustnessof

conclusionstochanges

inthe specificationof

models,

searching for theweakest

possible conditionswhich

guarantee that a comparative staticsconclusion holds across a family

of models.

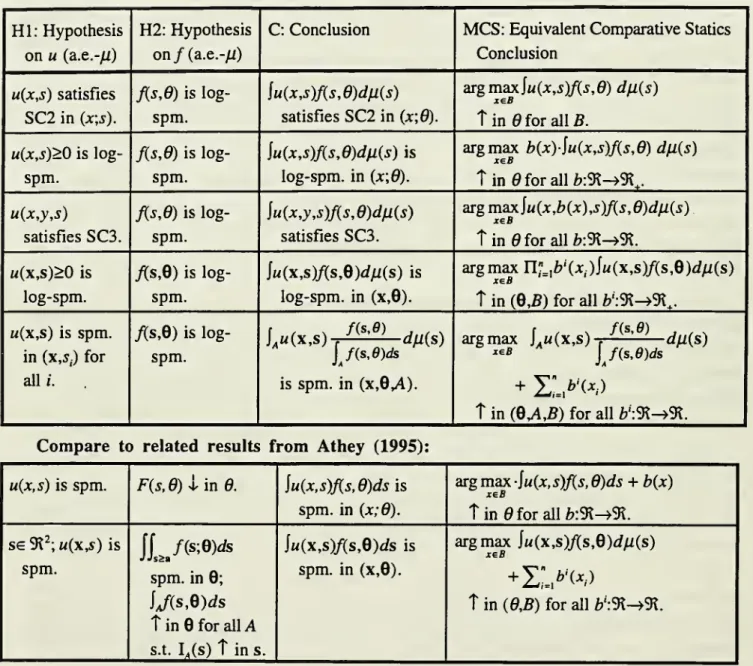

Athey,Milgrom, and Roberts (1996)

demonstrate thatmany

of the robust comparative statics resultswhich

arise ineconomic

theory relyon

threemain

properties: supermodularity,' log-supermodularity,2

and

singlecrossing properties.In

keeping

with thethemes of

thenew

literatureon

comparative statics, thispaper

derivesnecessary

and

sufficientconditionsforcomparative

statics predictions in several classesof

stochasticoptimization

models,

focusingon

single crossing propertiesand

log-supermodularity(Athey

(1995)studies supermodularity in stochastic problems). Further, the results apply

with

equalpower

when

the additionalassumptions

forstandardimplicitfunctiontheorem

analysis aresatisfied.The

theorems

aredesignedto highlight the issues involvedinselecting

between

differentassumptions

about a givenproblem,

focusingon

the tradeoffsbetween assumptions

aboutpayoff

functionsand

probabilitydistributions. This

paper

thenapplies thetheorems

toseveraleconomic

contexts,such

asproblems of

investment

under

uncertaintyand

games

of

incomplete information, in particular the mineral rightsauction.

The

analysis extends the literature in these areas,and

furtherclarifies the structure behind,and

parallelsbetween,

anumber

of

existingresults.Stochasticoptimization

problems

are particularly well-suited for systematic analysis with thenew

tools. It often

seems

thateach

distinct literature has itsown

specialized setof

techniques.When

implicit function

methods

cannotbe

applied, resultsmust

oftenbe

derived using lengthy revealedpreferencearguments,

and

itbecomes

difficult to assesswhether

theassumptions

of

themodel

are tooweak

or too strong. Further,when

the choice variable is a parameterof

a probability distribution,concavity

assumptions

are oftenproblematic (see Jewitt (1988) orAthey

(1995)),and

we

might

alsowish

to consider discrete choicesbetween

different investments. Additionally,many

areasof

microeconomic

analysis(i.e.,auction theory) require the analysisof

comparative statics in stochasticproblems

where

an

agent's objectivedepends

on

functionswhich

willbe determined

in equilibrium,so that it is convenient to

be

able analyze the agent'sproblem

withouta

priori restrictions (such asquasi-concavity ordifferentiability)

on

these functions.'

A

functionona productsetissupermodularifincreasing any one variable increases the returns to increasing each ofthe othervariables; for differentiablefunctions this correspondsto non-negative cross-partial derivatives between each

pairofvariables. SeeSection2forformaldefinitions.

2

A

function is log-supermodularifthe log ofthat function is supermodular. Log-supermodularity of a probabilityof

seemingly

unrelatedcomparative statics resultsfrom

the literature.There

aretwo main

classesof

resultsinthe paper,

where

bothcan be

appliedtoderivecomparative

staticswhen

an agentmakes

one

or

more

choices tomaximize

the expected value ofapayofffunction.One

class ofproblems

involvessingle crossing properties in

problems

with a singlerandom

variable,and

the other involveslog-supermodularity in

problems

with multiplerandom

variables.The main

results in this paper aresummarized

inTable

1.The

firstclassof

results in thispaper

involve singlecrossing properties,which

provide necessaryand

sufficient conditions forcomparatives statics inmany

contexts,such

as finance, auction theory,and

mechanism

design.Consider

first aproblem

where

an agentchooses

x

tomaximize

Iu(x,0,s)f(s;9)ds. In a"mineralrights" auction,

x

represents aplayer's bid,6

is her signalon

thevalueofthe object,

and

sisthehighest signalamong

her opponents;u

is the agent'spayoff

function,and

f{s;d) is the conditional densityof

theopponent's

signal. Thispaper

derives conditionsunder

which

theoptimal bidis nondecreasinginhersignal(which can

intum

be used

to establish existenceof a pure strategy equilibrium

when

players bid in discrete increments). Inan

investmentunder

uncertainty

problem,

;cisan

investmentin a risky project,whose

returns are parameterizedby

s,and

affectsthe agent's risk preferences and/or the distribution

over

the returns to the investment.The

problem

can alsobe

formulated so that the agentchooses

the distribution directly,from

a classof

parameterizeddistributions.

Both

formulationsare treatedin thispaper.In this first class of

problems,

the results canbe

succinctlysummarized

in termsof

a pair ofhypotheses

and

a conclusion.One

hypothesis concerns properties ofthepayoff

function, while theotherhypothesisconcernspropertiesofthe distribution

(more

general rolesof

the different functionswill also

be

treated).The

conclusion ofinterest in thisclassof problems

is (C) single crossing of the function \u{x,s)fis;0)ds in (x;d): that is, in order to guaranteemonotone

comparative staticsconclusions, the incremental returns to the choice variable (x)

must

change

in sign only once,from

negativeto positive, asa functionof

exogenous

variable (9).The

hypothesesare asfollows:(HI)

thepayoff

functionu

satisfies singlecrossingin (x;s) (i.e.,singlecrossing ofthe incremental returns tox

ins),and (H2)

thedensity/is log-supermodular.^The

paper

shows

thatHI

and

H2

arewhat

I call"identifiedpairofsufficientconditions"relative tothe conclusion C:

HI

and

H2

are sufficient forC,

and

further if either hypothesis fails, the conclusion willbe

violatedsomewhere

that the otherhypothesis is satisfied.

Thus, each

hypothesis is necessary ifthe conclusion is to holdeverywhere

thattheotherhypothesisissatisfied.

The

first classof

results is thenextended

to treatproblems of

theform

\v(x,y,s)dF(s,6),characterizing single crossing of the x-y indifference curves,

which

is important for deriving^UJ{s;0)isa parameterizeddensityonthe real line, log-supermodularity

of/

is equivalentto the requirement that the densitysatisfytheMonotoneLikelihood Ratio PropertyasdefinedinMilgrom(1981).monotonicity conclusions in

mechanism

designand

signalinggames

."^ In a variationon

the classiceducation signaling

model, workers observe

a noisy signal, 6, (such as the resultsfrom

an aptitudetest)abouttheirability,

and

thenchoose

education investments (x).Firms

offerwages

w{x).Then,

the conclusion of interest is that, for

any

wage

w(x), the choiceof

x

which

maximizes

iv{x,w(x),s)dF{s,6) is

nondecreasing

in 6.The

second

classof

problems, studied in Section 5, takes theform

U(x,Q)

=

f u{x,B,s)fis,B)dn(s),

where

each

bold variable is a vectorof realnumbers

and

the functionsJseA(x.e)

arenonnegative. I derive necessary

and

sufficient conditions forsuch

objective functions tobe

log-supermodular; thispropertyis inturn sufficient for the optimal choices

of

some

components

ofx and

6

toincrease inresponsetoexogenous changes

in othercomponents.

Further, inan

important classof

economic problems

(those with a multiplicatively separable structure), log-supermodularity isnecessaryfor

monotone

comparative

staticspredictions.The

resultsmay

alsobe used

to extendand

simplify

some

existing results(Milgrom and

Weber,

1982; Whitt (1982)) about monotonicityof

conditional expectations.

The main

resultisthat(HI)

log-supermodularityof

u,and

(H2)

log-supermodularity off, are anidentified pair

of

sufficientconditions (in thelanguage

introducedabove)

relative to the conclusionthat the integral is log-supermodular.

To

connect this result to the existing literatureon

games

of

incompleteinformation, aprobabilitydensity is

log-supermodular

ifand

only iftherandom

variablesareaffiUated.

The

resultisappliedtoa

Bertrandpricinggame

between

multiple (possiblyasymmetric)

firmswithprivateinformationabouttheirmarginal costs. Inthis

problem,

x

is a firm'sown

price,9

is a parameter

of

the firm's marginal cost,and

the vector s represents the costs ofeach

of theopponents,

which

enter the firm's payoffsthrough

the opponents' pricing strategies.The

resultsprovide conditions

under

which

each

firm's price increaseswith

its marginal cost parameter,which

can

inturnbe used

toshow

thatan

equilibriumexists inadiscretizedgame.

All

of

theseresults buildon

theseminalwork

of Karlin (1968)and

Karlinand

Rinott (1980)inthestatisticsliterature, as well as closely related

work

ineconomics

by Milgrom

and

Weber

(1982)and

Jewitt (1987).

The

firstmain

difference is that thispaper

identifiesand emphasizes

the necessityof

theclose pairing

between

singlecrossingpropertiesand

log-supermodularity,and

it further illustrateshow

severalimportantvariationson

one of

thetwo

hypotheses

lead tochanges

in the other. In thisform, it ispossibletoidentifythe precise tradeoffsinvolvedinmodeling.

Second,

theemphasis

hereisdifferent: Iformulatethe

problems and

selectthe propertiestocheck based

on

thenew

methods

forcomparative

statics,and

further thetheorems and

applications are statedinaform

which

is appropriatefora

wide

varietyofproblems

outside the classic investmentunder

uncertainty literature.The

recenttheory of

comparative

staticsbased

on

latticetheory motivates acloser integrationof

existing research^Athey,Milgrom, andRoberts (1996)showthatawidevarietyofunivariatechoiceproblems can bestudied by writing

the objectiveintheformV(x,gix),0),andtheyfurthershow that in such problems, the Spence-Mirrlees single crossing condition(studied inSection5.3) is the critical sufficient condition forcomparativestatics predictions to be robust to variationsinthefunctiong(x).

predictions

on

setsof optima, orwhen

theoptimum

isnotalways

interior.Other authors

who

have

studied comparative statics in stochastic optimizationproblems

includeDiamond

and

Stightz (1974),Eeckhoudt and

Collier (1995),GolUer

(1995), Jewitt (1986, 1987,1988b, 1989),

Landsberger

and

MeiUjson

(1990),Meyer

and

Ormiston

(1983, 1985, 1989),Ormiston

(1992),and Ormiston and

Schlee (1992a, 1992b); see Scarsini (1994) for a survey ofthemain

results involving riskand

risk aversion.Each

of

these papers ask questions abouthow

anagent's investment decisions

change

with the nature of the risk or uncertainty in theeconomic

environment, or with the characteristics

of

the utility function.Most

of

this hterature isbased

on

implicit function

methods

(Jewitt'swork

isanexception).The

analysesgenerally focuson

variationsof standard portfolio

and

investment problems; thus,emphasis

is placedon

exploring propertiesof

utility functions

and

investment or savings behavior. Recently, Collierand Kimball

(1995a, b)develop a general

approach

to the study of the comparative statics associated with risk. This paperdiffers

from

thisliterature inthatitemphasizes

applicationsoutside finance, asmotivatedby

the recentliterature

on

monotone

comparative

statics,and

shows

thatthesame

simpletheorems

arebehind

many

ofthe existing

comparative

statics results.This

work

is also related toAthey

(1995),who

derives necessaryand

sufficient conditions for theproperty supermodularity instochastic

problems,

where

supermodularity is the appropriate conditionto

check

in order tomake

comparative statics predictions inproblems

where

the agentchooses

parameters

of

the probability distribution(which might

interact),and each

choicevanable

has anadditively separablecostterm. In contrast to supermodularity, the single crossing properties studied

in this

paper

are not robust to the additionof

an additively separable cost term.The

mathematicaltools

used

tocharacterizesupermodularityinAthey

(1995) aredistinctfrom

those in this paper;Athey

(1995)

draws

parallelsbetween

"stochastic supermodularitytheorems"

and

stochasticdominance

theorems, basingthe

arguments

on

thelinearityoftheintegraland

itsrelationship toconvex

analysis.This

paper

isorganizedas follows: Section2

provides formal definitionsof

log-supermodularityand

the single crossing propertieswhich

willbe used

throughout the paper. Section 3proves

themain

single crossing theorems. Section4

applies thesetheorems

to auction theory, finance,mechanism

design, signalinggames,

and

aconsumption-savings

problem.

Section 5 studiestheorems

aboutproblems

withmany

random

variables, applying the analysis to a Bertrand pricinggame

with incomplete information. It furthershows

how

these results canbe used

in the studyof

conditional expectations. Applicationsfollow.

Most

of

theproofsarerelegated to the appendix.For

readers interested

mainly

inapplications, themost

importanttheorems

are the single crossingtheorem

(Theorem

3.2, applied throughout Section 4)and

the log-supermodularitytheorems

(sufficiency in2.

Definitions

2.1.

Single

Crossing

Properties

and

Comparative

Statics

This section introduces the definitions of the single crossing properties

which

arise frequently inthestudy of comparative statics analysis.

We

willbe

concerned

withthree differentkindsof

singlecrossingproperties,

which

we

will refer to asSCI, SC2,

and

SC3.

To

begin,let us defineSCI,

single crossing ina single variable

(where

all functions are real-valuedunless otherwise noted,

and

italicized variables arerealnumbers).^

Definition 2.1 g(t) satisfies single crossing in

a

single variable(SCI)

in t if,for

all tf,>ti^,(a)

g{ti)>0

impliesgit„)>0, and(b)

g(ti^)>0 impliesg(r„)>0.

Thisdefinition simply says that ifgit)

becomes

nonnegative as s increases, it stays nonnegative;and

ifg{t)becomes

strictly positive, it stays strictly positive.Thus,

it crosses zero, atmost

once,from below

(Figure 1).We

will alsobe

interestedinweak

and

strictvariationson SCI,

as follows:Definition 2.2 g(t) satisfies

weak

single crossing ina

single variable(WSCl)

in t if,for

alltn

>

h'

8(h)

>

if"P^ies S(tH)^

0-Definition 2.3 g(t) satisfies strict single crossing in

a

single variable(SSCl)

in tif,for

alltn

>

h'g(h)

^

implies git„)>

0.8(t)

f^,

^\rJ

Figure

1: g{t) satisfiesSCI

in t.r^\yo

g(f)

/\z.

Figure

2: g{t) satisfiesWSCl

in t.These

definitions areillustrated in Figures 1through

3.SSCl

arises in differentiable, univariateoptimization problems:if

an

agentsolves Tazxh{x,t), thenh{x,t) is strictly quasi-concave ifand

onlyifh^ satisfies

SSCl

in-x

(that is, the marginal returns tox

change

from

positive to negative as ;cincreases). Further, if

h

is strictly quasi-concave, then the (unique) optimal choicex\t)

is5 Part(b)ofDefinition2.1 isomitted inKarlin's (1968)andJewitt's (1987)workinvolving singlecrossing properties. Part{b)isrequiredformonotonecomparativestaticspredictions

when

thereisthe possibility formultiple optima, since (a)allowsan agenttobeindifferentbetweenxhandx^.atr„,buttheagentstrictlyprefersxhtox^atti-statics results innon-differentiable

problems

orproblems

which

arenotquasi-concave.Definition 2.4h{x,t)satisfies single crossing in

two

variables(SC2)

in {x;t) if,for

alla;„>;c^,g{t)

=

h{x„;t)-

h(x^^;t) satisfiesSCI.

The

definition saysthatif Xfj is (strictly) preferredtoXi forti, thenx^

must

stillbe

(strictly) preferredto Xi if/ increases

from

ti to t^. In otherwords,

theincremental

returns tox

cross zero atmost

once,

from

below,

asa function oft.Note

the relationshipisnotsymmetric.

Milgrom

and

Shannon show

thatSC2

istherightcondition forgeneralizedmonotone

comparativestatics analysis:

Lemma

2.1(Milgrom

and

Shannon, 1994)

Let /z: SR^—

>SR.Then

argmax

/i(x,r) ismonotone

nondecreasing

intfor

allB

ifand

only ifhsatisfiesSC2

in {,x;t).Ifthere isaunique

optimum,

the conclusionof

thistheorem

is straightforward. Ifthere are multipleoptima, the set increases in the "strong set order," as will

be

formally defined in Definition 2.8;according to this definition, ifa

maximizer does

not exist, the comparative statics conclusion holdstrivially (thus, throughout the paper, the convention

of

treating comparative staticstheorems

separately

from

existence of amaximizer

willbe

maintained).The

theorem

also holds ifwe

restrictattentiontothelowest orhighestmaximizers.

The

comparative statics conclusion inLemma

2.1 involves aquantificationover

constraint sets.Thisis

because

SC2

isarequirement about everypairof

choicesofx

Ifthe choicebetween

two

jc'sisneverrelevant for a comparative statics conclusion given an objective function/, then

SC2

cannotbe

necessaryforcomparative

statics.Many

ofthecomparative

staticstheorems of

thispaper

eliminatethequantificationoverconstraintsets. Instead, the

theorems

requu^e the comparative statics result toholdacrossaclass

of

models,where

thatclass issufficiently richsothata global conditionisrequiredfora robust conclusion.

We

will introduceSC3,

single crossing of indifference curves,and

other comparative staticstheorems

asthey arise inthepaper.2.2.

Log-Supermodularity

and

Related

Properties

Thissectionintroduces the definition

of

log-supermodularityand

several related definitionsfrom

the existingliterature,highlighting theconnections

between

them. Idiscuss these definitions insome

detail

because

theirconsequences

willbe

exploitedthroughout thepaper; further, it is useful toshow

the differentcontextsin

which

the subsequentresultscan

be

used.However,

because

Sections 3and

4

of the paper treat special casesof

onlyone

choice variableand one

random

variable, theBefore introducingthe formal lattice theoretic notation

and

definitions, consider the special cases of the definitions ofsupermodularity

and

log-supermodularitywhen

/i:??"—>SR,and

we

ordervectorsintheusual

way

(i.e.,one

vectorisgreaterthananother ifit is (weakly) largercomponent by

component). Topkis

(1978)proves

that ifh

is twice differentiable,h

issupermodular

ifand

only if-^^Kx)

>

forall/^j. If/i isnot suitably differentiable,then the discrete generalizations of these cross-partialconditionsmust

hold:thatis,h

issupermodular

ifand

onlyif, forall i^j, all x_,^,and

allx">xl',

h{x",x_i)-h{xl-,\_i) isnondecreasing

in Xj. Ifh

is non-negative, thenh

islog-supermodular

ifand

only if log(/z(x)) issupermodular.

Thus,

supermodularity (respectivelylog-supermodularity)

can

be

checked

pairwise,where

each

pairof

variablesmust

satisfythecondition thatincreasing

one

variableincreases the returns (resp. relative returns) to increasing the other.Observe

that it follows

from

these definitions thatsums

ofsupermodular

functions aresupermodular, and

products

of log-supermodular

functions arelog-supermodular.Log-supermodularity

arises inmany

contexts ineconomics.

To

seesome

simpleexamples,

consider a

demand

function D{P,t). This function islog-supermodular

ifand

only if the priceelasticity,£(/*)

=

P—

^—

^—

, isnondecreasing

in t.Log-supermodularity

also arisescommonly

in theuncertainty literature.

A

marginal utility functionU'{s-w)

islog-supermodular

in {w,s)(where

w

often represents initial wealth

and

s represents the return to arisky asset) ifand

only if theArrow-Pratt risk aversion, ;

—

, is nonincreasing (i.e., decreasing absolute risk aversion(DARA)).

A

parameterizeddistributionF(^s;d) has a

hazard

ratewhich

isnondecreasing

in6

if\-F{s;d)

islog-supermodular, that is,if

—

—

' is nonincreasingin ft1

-

F{s;d)In their study

of

auctions,Milgrom

and

Weber

(1982) define a related property, affiliation,which

willbe

discussed Sections 4.2.3and

5.3.The

important point is thatMilgrom

and

Weber

(1982)

showed

thata vectorof

random

variablesvectors isaffiliatedifand only

ifthe joint density,/(s), is

log-supermodular

(almost everywhere). Section 5shows

that the propertylog-supermodularity isinterestingnot only in its relationship to density functions, but also in thecontext

of deriving

comparative

staticspredictions formore

generalobjective functions.Finally,log-supermodularityisclosely relatedtoa property

of

probability distributionsknown

asmonotone

likelihood ratioorder

(MLR).

Consider

a probability distribution F(s;6).When

thesupport

of

F,denoted

supp[F],6 is constant in ftand

F

has a density/, then theMLR

requires thatthelikelihoodratiois

nondecreasing

ins,as follows: l(s;e„,e^)=

[

"

is

nondecreasing

inson

supp[F]

forall6h>9i^.

6 Formally, supp[F]

=

{s\F{s+

£)-

F(j-

e)>

Ve

>

o}with varying support

and

without densities (with respect toLebesque measure) everywhere.

In general,we

can define a "carryingmeasure,"

C{s\d,^,6fj)=

j(Fis;6i^)+

F{s;6fj)), so that bothF{;6fj)

and

F{;6i^) are absolutelycontinuous with respectto Ci\6i^,6„).Then,

we

are interested inlog-supermodularity

of

theRadon-Nikodyn

derivative '.

These

constructions canbe

dC(s;eH,6^)

used

tointroduce adefinitionoftheMLR

which

isslightlymore

generalthanthe standardone.^Definition 2.5

The parameter

6

indexes

the distribution F{s;6)according

to theMonotone

Likelihood

Ratio

Order (MLR)

if,for

all6^

>

0^, islog-supermodularfor

C-dC{s;e„,ei)

almost

all Sfj>s^ in SH^.Note

thatwe

have

not restrictedF

tobe

a probability distribution.Consider any

nonnegativefunctionk{s;6)

and measure

fisuch

thatk{s;d)

>

0,and

^(^;0)=£_it(r,0)J//(r) is finite foralls. (A2.1)It isthenstraightforward to verifythatK{s;0)satisfies

MLR

ifand

only ifk{s;6) islog-supermodular

for//-almostallSfj>Si^ inSR^. This

makes

itfairly easy tomove

back and

forthbetween

formulationswhere

we

are interested in a general distributionF, and

formulationswhere

we

are interested in the"density"k(s;d) directly(for

example,

k

willbe

a marginalutilityinmany

ofourexamples,

but it willalso

be

a probability density).Now

consider the general lattice theoretic definitions,which

allow for amore

notationallyconvenient analysis of multivariate log-supermodularity in Section 5.

Given

a setX

and

a partialorder>, the operations

"meet"

(v)and

"join" (a) are defined as follows:x

v

y

=

inf{z|z>

x,z>

y|

and

X

A

y

=

sup|z|z<

x,z<

yj

. InEucUdean

space with the usual order,x

v

y

denotes thecomponentwise

maximum

oftwo

vectors, whilex

a

y

denotes thecomponentwise

minimum.

With

this notation,

we

definetwo

veryuseful propertiesofreal-valued functions(where

A!" is a lattice, i.e.,an ordering

and

asetwhich

isclosedunder

meet

and

join):Definition

2.6

A

function

h.X—>Si

issupermodular

if,for

allx.yeX,

hix

V

y)+

/z(xA

y)>

/i(x)+

/i(y).Definition 2.7

A

non-negative function

h'.X-^Si islog-supermodular^

if,for

allx.yeX,

/i(xvy)-/i(xAy)>/z(x)-My).

^ Notethatthe

MLR

impliesFirstOrderStochasticDominance(FOSD)

(butnotthe reverse): theMLR

requires that foranytwo-pointsetK,the distribution conditional on

K

satisfiesFOSD

(thisisfurtherdiscussedinAthey(1995)).^ In particular, absolute continuity ofF{;6h) with respect to F(;OJ on the region of overlap of their supports is a

consequenceofthe definition,nota required assumption. Further,Idonotassumethat

F

isa probabilitydistribution.In thecase

where

X

isaproductset, afunctionissupermodular

ifincreasingone

component

increases the returns to every othercomponent,

and

log-supermodularity requires that increasingone

component

increases therelativeremms

toeveryothercomponent.

While

theprimary

focus in this paper willbe

on

the casewhere

X=

9t"and

we

use the usualcomponent-wise

order,we

will alsobe

interestedinthespaceofsubsetsof

SR" togetherwith an orderknown

as (Veinott's)strong setorder. This willarisewhen

we

are interested in setsof

optimizersof

a function

and

how

theychange

withexogenous

parameters.We

willalsobe

interested inchanges

inthe support of a distribution.

For example,

the definitionof

MLR

allows the support of thedistribution F{s;&) to

move

with

6.However,

monotonicity of

the likelihood ratio places restrictionson

how

thesupportcan

move:

itmust

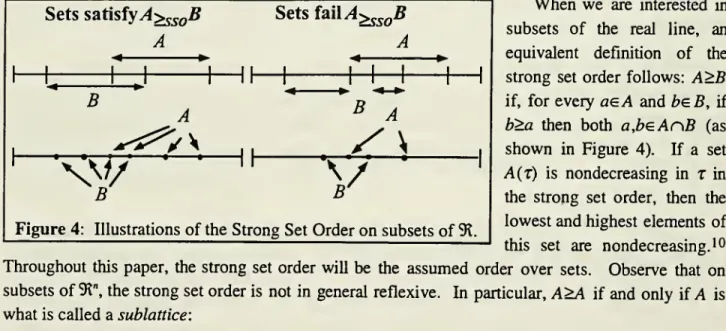

increasein thestrongsetorder,defined as follows.Definition 2.8

A

setA

isgreater

than

a

setB

in thestrong

setorder

(SSO), writtenA>B,

if,

for

any

a

inA

and

any b

inB,aw

be.A

and

a/\be

B.A

set-valuedfunction

A(t)

isnondecreasing

in the strongsetorder

(SSO)

iffor

any

Tf,>

T^,A(T„)> A(T^.

Sets

satisfyA>^^fjB

Sets

mA^^^B

A

-*A

j—\-B

^

»n5^

B

B

» ».—

t * * »^\

V

Figure

4: Illustrationsof

theStrong

SetOrder

on

subsetsof

SR.When

we

are interested insubsets

of

the real line, anequivalent definition

of

thestrong set order follows:

A>B

if, for every

aeA

and

bsB,

ifb>a

thenboth

a,beAnB

(asshown

in Figure 4). If a setA(t)

isnondecreasing

int

inthe strong set order, then the

lowest

and

highest elementsof

this set are nondecreasing.'^

Throughout

this paper, the strong set order willbe

theassumed

orderover

sets.Observe

thaton

subsets

of

SK", thestrong setorderis not in general reflexive. In particular,A>A

ifand

only ifA

iswhat

iscalleda

sublattice:Definition 2.9

Given

a

lattice X, setAciX

isa

sublattice iffor

all x,y

e.A, x

vy €A

and

X

Ay

eA.

For example, any

set [a^,a^]x[b^,b^] is asublattice of9^^

Sublattices ariseboth

in the studyof

comparative

statics(seeTopkis

1978, 1979)and

instochastic monotonicity(seeWhitt

(1982)).As

discussedabove, theMLR

has implications forhow

the supportof

the distributionsmove,

afact

which

willbe

exploitedintheproofsin thispaper:Lemma

2.2 IfF(s;d) satisfiesMLR,

then supp[F(5;a)] isnondecreasing

(SSO)

in6.

10 For more discussion ofthe strong set order, see Milgrom and Shannon (1994) or Athey, Milgrom and Roberts

3.

Single

Crossing with

a Single

Random

Variable

This section studies single crossing properties in

problems

where

there is a singlerandom

variable;

some

of

the results aresummarized

in the firstand

thirdrows

ofTable

1.Apphcations

toinvestment

under

uncertainty, auctions,and

signalinggames

follow in Section 4.These

resultsdo

not in general extend to multidimensional integrals.

The

section beginsby

introducing themain

mathematicalresults, discussing their intuition

and proof

insome

detail. Several variations are thenanalyzed,

which

areused

in Section 4.However,

readers interested primarily in apphcationsmay

find it

more

expedient to review themain

ideasof

Section 3.1,which

areTheorem

3.1 (themain

stochastic single crossing theorem)

and

Definition 3.1 (identified pairof

sufficient conditions),and

then

proceed

direcdytoSection4.3.1.

Single

Crossing

inStochastic

Problems

This section studies thefirst

main

mathematical

resultofthe paper, aresultwhich

gives necessaryand

sufficient conditions for a function of the

form

G{d)^\

g{s)k{s,d)dii{s) to satisfySCI

inG

(where

^:9l-^SR, /::9t^—>SR,

and

/x is a measure).One

model

commonly

analyzed in the investmentunder

uncertaintyliterature, for

example

in the classic articleby Arrow

(1971), is the question ofwhen

aninvestorwillincrease his investmentinarisky asset

when

hiswealth increases. Formally,an

investorwithinitial wealth

chooses

x, an investmentin arisky asset, tomaximize

\u{{6-

x)r+

sx)f{s)dsIn that case, the function

of

interest for our analysis is the first derivative with respect to x,^u'He

-

x)r+

sx){s-

r)f{s)ds.We

letg{s)={s-

r)f{s)and

k{s\e)=

u\{d

-

x)r+

sx). In anotherexample,

we

arechoosing

x

tomaximize

\u{x,s)f(s;0)ds.Many

problems

fit into thisframework,

including

ones

where

j:isafixedinvestmentwhose

returnsdepend

on

^, arandom

variable,and

we

are interestedin

how

x

changes

with the distributionover

the risky parameter s. In this case, g(s)=

u{x„,s)-

u{Xi^,s),and

k=f.The

results inthis sectionbuildfrom

Karhn

(1968)and

Jewitt (1987). Here, the results highlight theclose pairingof assumptions

on

thetwo

functions (gand

k)which

is required for each result,and

further, the results illustrate the tradeoffs

which

arisebetween

strengtheningassumptions

on one

function

and

weakening

assumptions

on

the other. Iwill alsostudy severalcaseswhere

some

a priori restrictions aremade

on

thefunctionsg

and k

which

couldpotentiallychange

the necessity sideof

thetheorems,for

example,

where

k

isrestricted tobe

aprobability density.The

assumption

that k(s;d) satisfies (A2.1)(from

Section 2) willbe

maintained throughout the paper.An

interestingcaseiswhere

^

is a probability densityand

K

is the corresponding probabilitydistribution;

however,

we

will also allow other interpretations of k. In particular,UmK(s;6)

may

J—<»

vary with 6.

The

supportof

themeasure

K

is defined in the standardway

(see footnote 6).Throughout

the analysis ofsinglecrossingproperties, thedomain

ofit(;0)willbe

the entire real line,but this is without loss

of

generality sincewe

cansimply

givemeasure

zero to regions outside theThe main

resultinvolvestwo

hypothesesand

a conclusion.Theorem

3.1(i)

The hypotheses

(HI)

g(s)satisfiesSCI

in (s) a.e.-fl'^(H2)

kis;d) islog-supermodular

a.e.-fl.are sufficient

for

the conclusion,(C)

G(6)

=

j

g(s)kis,e)d^is) satisfiesSCI

in 6.(ii) If

(H2)

fails, then there existsa k

which

satisfies(HI) such

that (C)fails. (Hi) If(HI)

fails, then there existsa g

which

satisfies(H2) such

that (C)fails.Part (i) of

Theorem

3.1 states thatthetwo

hypotheses

togetherimply

the conclusion. Parts (ii)and

(iii) state that neitherhypothesis canbe

weakened

without violating the conclusionsomewhere

thattheother hypothesis issatisfied. If

we

wish

toguarantee thattheconclusion holdsforallg which

satisfy

SCI,

thenk

must

be

log-supermodular;likewise,ifwe

wish

for the conclusion tohold

for allk

which

arelog-supermodular, theng must

satisfySCI.

Karlin (1968) discovered the sufficiency

part

of

this relationship in(1968) inhisstudy ofthe

mathematics of

"total positivity," althoughhe focused

on

aweak

versionof

the singlecrossingproperty.'^ Jewitt(1987)

was

thefirstto apply this result in

economics.

Jewitt's(1987)

emphasis

ison

thepreservationof

singlecrossing properties

of

probability distributionsunder

integration,where

the agentchooses

adistribution,

and

we

wish

toknow how

thatchoice

changes with an

exogenous

parameterwhich

shifts the risk aversionof

the agent'sutilityfunction.13

Figure

5:6

shifts k{s;9) so thatthe valuesof

s to the rightof s receive

more

weight,relativetos;

and

thevaluesofs to theleftof s receive lessweight,relativeto s

.

1^

We

willsay thatg(5)satisfies SCI almost everywhere-^ (a.e.-/i) ifconditions (a) and(b)ofthe definition ofSCI

holdforalmostall(w.r.t.theproductmeasureon5R^inducedby/i) (j^.sj pairsinSR^suchthat s„>Si.

'^Karlin analyzesthecasewhere both thepayoff function and the expectationsatisfy part (a) ofDefinition 2.1, under

the additional assumptionthatthe distributions areabsolutely continuous with respect to oneanother, proving aresult related to part(i)ofTheorem3.1;

we

willextendouranalysis toincorporate arelated notion ofweaksingle crossing ofthepayofffunctioninSection3.2. Inothereconomicsproblems,MilgromandShannon (1991) applies Karlin'sresult.

'3 Thus, Jewitt's (1987) paper studies a slightly different problem, where (in our notation and assumptions), g is restrictedtothe differencebetweentwoprobability distributions,andkisactuallythefirstderivativeofanagent's utility

function(mySection 4.2.2 analyzesJewitt's problem exactly anddescribes the relationship between ourresults). He

stateswithoutproofthataresultanalogoustoourTheorem3.1 (ii)istrue,usingpart(a)ofDefinition2.1 as his single

crossing condition on both payoff functions and objectives.

We

will see in the following sectionshow

imposingThe

intuitionbehind

the sufficiency conditions in (i) is straightforward.Consider

a payofffunction g{s)

which

satisfiesSCI,

asshown

in Figure 5.According

to the definition oflog-supermodularity,

an

increasein6

raisestherelative likehhoodthat s is high.Thus,

an increase in6

puts

more

probabihtyweight

on

thosevalues of swhere

theg

is nonnegative relative to those valueswhere

g

is nonpositive.While

thischange

in6

does

not necessarily increase the expected value, itwill not causethefunctionto

change

in signfrom

positive to negative.The

sufficiencyarguments

canbe

easilyillustrated algebraically in the casewhere

there is afixedregion

where

k(s;d) ispositivethatdoes

notdepend on

6. Letf

be

apointwhere

g

crosses zero,and

for simplicity

suppose

thatk{s

,&)[$nonzero

there.Then,

pick6h>0l-

Log-supermodularity

of itimplies that thatdie"likelihoodratio"l{s)

=

—

'—^^ is nondecreasing.Thus,

we

have:kis;ej

lgis)kis;e„)d/2is)

=

j

g(s)!^p^k(s;e,)dfiis)

=

-jl\gis)\l{s)k{s;e,)d^i{s)+

j}(s)l{s)k{s;e,)d^(s)> -lCs)Jl\g(s)HyA)Ms) +

lCs)\)(s)k(s;e,)d^i{s)=

lCs)\ g{s)k{s;e,)d^i(s)The

first equality holdsbecause g

satisfiesSCI,

while the inequality followsby

monotonicityof

/.Then

(3.1)impUes

that, if Jg(5>t(.y;0^)JjU(.y)>(>)O, thenj

g(s)k(s;e„)dfi{s)>(>)0 as well. If, inaddition, /(5) >1, then \g{s)k{s;dfj)diJ.{s)

>

\g{s)k{s;di^)din{s). Inmost

applications,however,

it will notbe

natural toassume

that l(s)>1

everywhere, and

thus (3.1) is useful to estabhsh singlecrossing but not monotonicity;

however,

we

use monotonicity inour

analysisof

investmentunder

uncertaintyin Section4.2.1.

(3.1)

g(s)

*H

Parts (ii)

and

(iii) alsohave

straightforwardintuition.

Consider

first part(ii). If

k

fails tobe

log-supermodular, thenthere exist

two

regions,S^ and

5^.,such

thatincreasing

6

placesmore

weight

on

Sirelative to S«.

The

function illustrated inFigure

6

satisfiesSCI;

but increasing6

causes

G{0)

tochange

from

positive tonegative, violating

SCI.

However,

theproof of

part (ii) involvessome

additionalwork.

Previous analysesof

closely relatedproblems

assume

(as is appropriate in thoseproblems)

that there isa

fixed regionthroughout

which

k{s;d) is strictiy positive for all 6, whileTheorem

3.1 allows supp[K(s;6„)] tomove.

The

proof of

Theorem

3.1shows

thatif(C) holdswhenever

(HI)

holds, then supp[K(s;6)]e

Figure

6:When

6

increases, S^ receivesmore

weight

relative to 5^.Even

though

g

satisfiesSCI,

must be

increasingin6

(strong setorder); itthenestablishesthrough

a seriesof counterexamples

thatlog-supermodularity oik{s;G) follows.

Now,

considerpart (iii). Ifg

fails (HI),then (withoutlossof

generality)there isSl<

Shsuch

thatgisi)>0, but g(s„)<0. Furthermore, these inequalities hold throughout

open

intervalsof

positivemeasure

fi.But

then, k{s;0) canbe

defined so thatk{s;d„) places allof

theweight

on

the intervalsurroundingpointSh, whilek{s;Oi) placesall

of

theweight

on

the intervalsurrounding

pointSl-This

functionis log-supermodular, but

G{6)

failsSCI

sinceg

does.Observe

thatnonmonotonicity

oig

and k

are critical to establishing thecounterexamples

requiredfor parts(ii)

and

(iii). Ifmonotonicityisassumed

(forexample,

ifA:isaprobabilitydistribution,not a density),thenthenecessity parts ofthetheorem break

down.

Thus,

in individualproblems,

it willbe

necessary to re-examine the logic described

above

to see ifconditionscan

be

weakened

using all ofthe structure of the particular

problem.

One

trickwhich

can

sometimes be used

when

one

of thefunctions is

nondecreasing

isto integrateby

parts;we

illustrate thistechniqueinSection4.2.2.Theorem

3.1 described a close relationshipwhich two

hypotheses

satisfy in relationship to aconclusion.

One way

tothinkaboutthisresultisthat the setof payoff

functionsg which

satisfyH

1,

together with the conclusion

C,

identifieswhether

k

satisfiesH2.

By

Theorem

3.1, ifG

satisfiesSCI

forallg

which

satisfySCI,

thenk

must

be log-supermodular

almosteverywhere;

ifnot, itmust

fail log-supermodularity. Likewise, the class

of

functionsk

which

satisfyH2

identifieswhether

g

satisfies

SCI.

Thus

motivated,Idefinean

abstractrelationshipbetween

two

hypotheses

and

a conclusion. Thisdefinition will

be used

to succinctlystatetheremaining

theorems

(aswellasthetheorems

inTable

1).Definition

3.1Two

hypotheses

HI

and

H2

are

an

identifiedpair of

sufficientconditions

relative to theconclusion

C

ifthefollowing

statementsare

true:(i)

HI

and

H2

imply

C.(ii) If

H2

fails, thenC

must

failsomewhere

thatHI

is satisfied.(iii) If

HI

fails, thenC

must

failsomewhere

thatH2

is satisfied.In the next

few

sections, this definition willbe used

to state anumber

of

variationsof

Theorem

3.1,

which

willbe

appliedin Section4.3.2.

Variations

of

Stochastic Single

Crossing

Theorems

3.2.1. Strict

and

Weak

Single Crossing

in Stochastic

Problems

This section studies variations

on

Theorem

3.2where

h

satisfiesWSCl

(Figure 2) insteadof

SCI

(Figure 1).14

Weak

single crossing arises inany

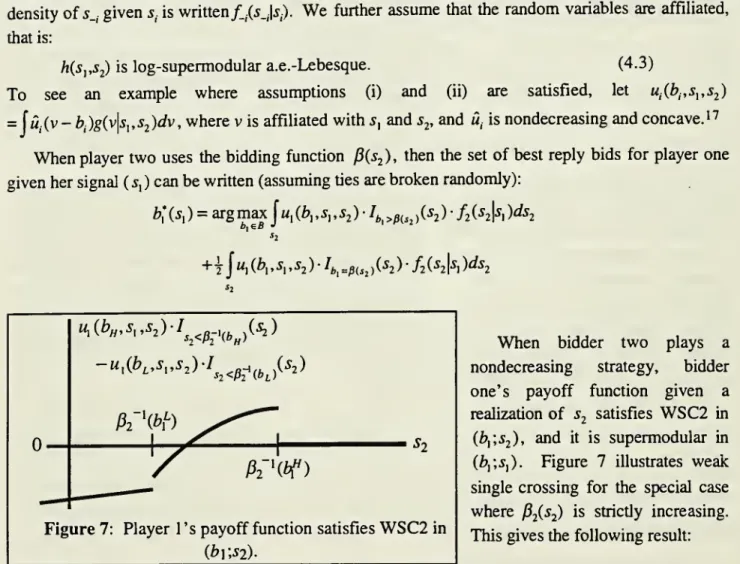

winner-take-all pricingproblem, such

as Bertrandcompetition or auctions. In those

problems,

increasingyour

bidby

a smallamount

(or decreasing•4 Ina variationon

Lemma

2.1,Milgrom and Shannon (1994) show thatWSC2

ofh(x,t) (thatis,WSCl

of/i(%,r)-hixL,t) forall x„>xj is necessary andsufficient for there to exist a selection from the set of x-optimizers which is

your

price)hasno

effectwhen

itturns outthatyour

opponent

hasdrawn

a favorable signal,and

thusplaceda

much

higherbid orcharged

amuch

lower

price.Thus,

as theopponent's

signal increases,theincrementalreturnstoincreasing

your

bidgo

from

negative(when you would

have

won

anyway),

topositive

(when you win

an auctionyou would

have

otherwise lost), to zero(when you

lose witheithera

low

ora highbid). Thus, theincrementalreturns toincreasingyour

bid satisfyWSCl.

To

seewhy

more

assumptions

are required to guarantee that the expectation satisfiesSCI when

gis) satisfies onlyWSCl,

observe that shiftingweight

from

the regionof

positive returns to theregion of zero returns is consistent with log-supermodularity of k, but

might

violate the singlecrossing property of

G

(though notweak

single crossing).To

rule outsuch

cases,we

require anadditional

assumption (non-moving

support):supp[K{s;6)] isconstant in 6.

(NMS)

Theorem

3.2Assume

(NMS).

Then

thehypotheses

(HI)

g(s) satisfiesWSCl

in s a.e.-fl.(H2)

k(s;6) islog-supermodular

a.e.-fi.form

an

identifiedpair of

sufficient conditions relative to the conclusion (C)Gid)= j

g(s)k{s;d)dfi(s) satisfiesSCI.

Now,

consider the conditionswhich

are required for the conclusion that the expectation has thestrictsinglecrossing property

(SSCl).

Milgrom

and

Shannon

(1994)prove

a variationon

Lemma

2.which shows

thatSSC2

of

h{x,t) (that is,SSCl

of

h{Xfj,t)-h{Xj^,t) for all Xij>x,) is necessaryand

sufficient for every selection

from

maxh(x,t)

tobe

nondecreasing in r for allA.

When

h(x,t)satisfies

SSC2,

ifan agentis indifferentbetween

two

choicesof

x

for alow

valueof

t, thenwhen

tincreases theagent

must

strictlyprefer thehigherofthetwo

choices.To

extendTheorem

3.2 to studySSCl,

we

willneed

to strengthenour

requirementson

thefunctionk,as follows:

Definition 3.2

A

non-negative function

k(s;d) isstrictlylog-supermodular

a.e.-jX ifit islog-supermodular

a.e.-fl,and

further,for

all 0„>6i^and

fl-almostall (Sf/,Sj)pairsinsupp[K{s;dJ]r\supp[Kis;6„)] such

thatSf,>s^, k{s^;6^)kiSfj;d„)>

k{Sfj;6^)k{Sj^;dfj).We

alsoneed

one

more

assumption:g{s)-k{s;6)9t

on

a setofpositive/i-measureforall 6.(NZ)

Theorem

3.3Assume (NMS) and

(NZ).Then

thehypotheses

(HI)

g{s)satisfiesWSCl

in s a.e.-fL(H2) k

is strictlylog-supermodular

a.e.-fi.are

an

identifiedpair of

sufficient conditions relative to the conclusion (C)0(0)=

j

g(s)kis;d)dn(s) satisfiesSSCl

in s.3.2.2.

Allowing

Both

Functions

toDepend

on

There

aretwo

generalsetsofsufficientconditionsunder

which

we

can

extendour

single crossingresults to functionsofthe

form 0(6)=

j

g{s;e)kis;e)d^is).The

first is themore

straightforward:we

require that gis;d), in addition to satisfying

SCI

in s, isnondecreasing

in 6.The

second

sufficientcondition is

more

complicated; it requires that gis;0) satisfies a variationof

log-supermodularity,where

the definitionisextended

toallow forg

totakeon

negativevalues.The

followingtheorem

considersthefirstcase.Theorem

3.4Assume (NMS)

(and, respectively, (NZ)).Suppose

that g(s;6) ispiecewise

continuous

in6 and

nondecreasing

in6

for

fi-almost alls.Then

thehypotheses

(HI)

g{s;G) satisfiesWSCl

in s a.e.-^.(H2)

k(s;6) islog-supermodular

(resp. strictlylog-supermodular)

a.e.-jLare

an

identifiedpair of

sufficient conditions relative to theconclusion

(C) G{e)=jg{s;e)k(^s;e)dii(s) satisfies

SCI

(resp.SSCl)

in 6.Thisresultis

used

to analyzethemineralrightsauctionin Section4.2.3.Now

consider thesecond

setof

sufficient conditions for the single crossing property,where

gis,0)is

nonmonotonic

in 6. Itturns outthatwe

need

a single crossing point for gis;6),denoted

Sq,which

does

notdepend

on

6.Then,

we

have

a well-defined extensionof

log-supermodularity tofunctions

which

can

attainnegative values:Definition 3.3

Consider

a

function g(s;d)which

satisfiesSSCl

in sand

such

that the crossingpoint,

denoted

Sq, is thesame

for

all 6. Thisfunction

satisfies thegeneralized

monotone

ratioproperty

iffor

all0„

>0^

and

all s">

5'€

{9^ \^q}, ^^^ '^"^>

i^li^.

gis

;0J

g(s;0J

To

seewhen

this propertymight

be

appropriate, recall that the first order conditions inArrow's

investment

under

uncertaintyproblem

takes theform

\u'((6-x)r

+

sx)(s-r)f(s)ds.

Ifwe

letg(s;9)=u\(^d-x)r

+

sx){s-r), then the fixed crossing point is Sff=r,and

g{s;9) satisfies thegeneralized

monotone

ratiopropertyifand

only ifthe investor has decreasing absolute risk aversion.Note

that in this simple, separable case,we

couldhave

analyzed theproblem

usingTheorem

3.1,letting g(s)

=

f{s)is-r)and

kis;6)=

u'{{d-x)r

+

sx).However,

we

might

wish

to studymore

general functional

forms

for thepayoff

function, orwe

might

wish

to analyze theproblem

withoutrelying

on

firstorderconditions.Theorem

3.5Suppose

that thefollowing

conditionshold

a.e.-fl: (i)forall 6, gis;G) satisfiesSSCl

in s, (ii) the crossingpoint,denoted

Sg, is thesame

for

all d; (Hi)g

satisfies thegeneralized

monotone

ratioproperty,and

(iv) k(s;6) islog-supermodular

a.e.-fL Then,G(d)=jgis;e)k(s;e)d^iis) satisfies

SCI

in 6.This resultis

used

when

we

study investmentunder

uncertaintyproblems

where

analysisbased

on

firstorder conditionscannotbe

applied.conclusions in a

number

of applications. It is interesting to seehow

thesame

simpletheorems

areused

to provide comparative statics conclusions in awide

varietyof

problems.The

applicationssimplify

and

generalizesome

existing results,and

providenew

results inseveral cases.Thissectionbegins with

problems

of theform

\u(x,s)dF(s,d), finding necessaryand

sufficientconditions for the choice of

x

to increase with 6. Applications to several classes ofeconomic

problems

followin Section4.2.4.1.

Problems

of

the

Form

{u(x,s)dF(s,0)This subsection

shows

how

Theorem

3.1 canbe

extended to provide necessaryand

sufficientconditions for the choice of

x which

maximizes

\u{x,s)dF(s,6) tobe

nondecreasing in 6.The

sectionproceeds

by

characterizingSC2

inobjectivesof

theform

U{x,6)

=

\u(x,s)dF(s,6) (recall the close relationshipbetween

SCI

and

SC2

from

Section 2: U{x;d) satisfiesSC2

in {x;d) ifand

only iftheincremental returns to

x

satisfySCI

in 6).The

theorems developed above

involved quantificationover

any

nonnegative function k{s;6), including caseswhere

the supportmight

vary with 6. Further, the resultsassumed

that the "distributions," K{s;d),were

all absolutely continuous with respect to ameasure

/i. Sincewe

aremaintaining slightly different

assumptions

than in thetheorems

above,we

might imagine

that thenature of the

theorems

could change. It turns out,however,

that the differences are minor, asdemonstratedinthefollowingresult:

Theorem

4.1Assume

thatF

isa

probability distribution.Then

thefollowing hypotheses

(HI)

u{x;s) satisfiesSC2

in (x;s).(H2)

F(s;9) satisfiesMLR.

are

an

identifiedpair of

sufficient conditions relative to the conclusion(C) U{x;e)

=

^u{x,s)dF{s,e)

satisfiesSC2

in (x;0).Observe

that(HI)

requiresSCI

to holdeverywhere,

since the distribution canmake

any

point amass

point. Further,we

have

stated(H2)

interms oftheMLR

asopposed

tolog-supermodularity, sothat the hypothesis

makes

senseeven

when

no

absolute continuityassumptions

are maintained apriori.

Theorem

4.1 has severalconsequences

for the analysisof

comparative statics.Consider

the solution to thefollowing optimization problem:X*(0,fil«,F)=argmax

\u{x,s)dF(s;e)Likewise, denotethe solution to the hypothetical optimization

problem under

certainty (that is,when

x'(s, 5|w)

=

argmax

u(x,s)xsB

The

following aretwo

consequences

ofTheorem

4.1 for comparative staticsunder

uncertainty (theseare stated separately

because

thecomparative

staticsconclusions areslightlydifferentineach

case).Corollary

4.1.1The

following

two

conditionsare

equivalent:(i)

For

allu such

that x'(s,B\u) isnondecreasing

insfor

allB,X'{6,^u,F)

isnondecreasing

in 6. (ii)F

satisfiesMLR.

Corollary

4.1.2The

following

two

conditionsare

equivalent:(i)

For

allF

which

satisfyMLR,

X'{6,B\u,F)

isnondecreasing

in6

for

allB.(ii) x'{s,B\u) is

nondecreasing

insfor

allB.Corollary4.1.1 states that

comparative

staticsresultsextend

from

the caseof

certainty to the caseofuncertaintyif

and

onlyifthe probability distribution satisfies theMLR.

Note

thatthe comparativestaticsconclusion,

X'(0,^u,F)

isnondecreasing

in 6,can

be

stated with or without reference to the additional clause "for all B."The

quantificationover

B

is notrequired

in the conclusion because,given a probability distribution F, I can

always

choose

appropriatepayoff

functionswhich

make

a

given choiceof;coptimal.

Corollary 4.1.2 states that the comparative statics result holds

under

uncertainty forany

distribution with the

MLR

ifand

only if the comparative statics result holdsunder

certainty.We

might,

however,

be

interestedina

problem where

the constraintsetis fixed, so that the quantificationover

B

in the comparative statics statementsof

Corollary 4.1.2would

be

unnecessary. It turns outthatthequantification

over

B

can

be

omittedfrom

both

(i)and

(ii) ifwe

are onlyconcerned with

theresult that (i) implies (ii).

However,

it is required for (ii) implies (i) because, givenF

and

u, theremight be

a valueofx,denoted

x',which maximizes

U{x,6)forsome

6,butwhich

does

notmaximize

u{x,s) for

any

value of s. Insuch

cases, (ii)would

not placeany

restrictionson

the behaviorof

u{x',s),

and

thuswe

would

notbe

able todraw

conclusionsabout

thebehavior of

U{x\6).With

additionalrestrictions,however,

Corollary4.1.2can be

modified:Corollary

4.1.3(Ormiston

and

Schlee,1993)

Assume

that U(x,d)and

u(x,s)are

strictlyquasi-concave

and

differentiable inx

and

that theoptimum

is interior.Then

thefollowing

two

conditions

are

equivalent:(i)

For

allF

which

satisfyMLR,

X'(6,B\u,F)

isnondecreasing

in 6. (ii)x'(s,^u)

isnondecreasing

ins.The

assumption

thatthere is a unique, interioroptimum

allows us toremove

the quantificationover the constraint set in the comparative statics conclusion

because

strict quasi-concavity, togetherwith (ii), implies that

u

satisfiesSC2;

we

can then applyTheorem

3.1.However,

the extrarestrictions required in order to apply Corollary 4.1.3 eliminate a variety

of

interestingeconomic

problems.