Implementing Tax Coordination and Harmonization through Voluntary Commitment

34

0

0

Texte intégral

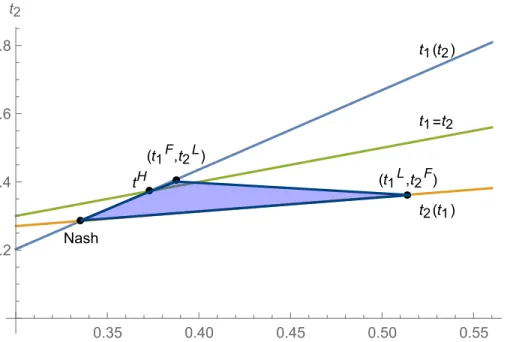

Figure

Documents relatifs