Do Socially Responsible Investments Outperform

Conventional Ones?

Bachelor Project submitted for the degree of

Bachelor of Science HES in International Business Management by

Laurent-Xavier SCHAUB

Bachelor Project Mentor:

Frédéric RUIZ

Geneva, the 3rd of May 2020

Haute école de gestion de Genève (HEG-GE) International Business Management

Disclaimer

This report is submitted as part of the final examination requirements of the Haute école de gestion de Genève, for the Bachelor of Science HES-SO in International Business Management. The use of any conclusions or recommendations made in or based upon this report, with no prejudice to their value, engages the responsibility neither of the author, nor the author’s mentor, nor the jury members nor the HEG or any of its employees.

Executive Summary

The literature has seen a growing number of studies addressing the topic of sustainable finance, while firms also seem to be keener on undertaking and advertising societal actions. The role firms play in society has been evolving, especially due to the rising demand for corporate social responsibilities. The question that recurrently arises is whether being socially responsible will allow businesses to become financially more attractive for investors than unsustainable competitors. The literature does not unanimously provide an answer to this enquiry and results seem to have varied throughout time. The purpose of this thesis is above all to gather convergent and divergent opinions around this theme and to determine what could have caused discrepancies. The second aim is to establish a red string of arguments and empiric results until a final opinion about the initial question emerges.

Some potential errors that could have prevented previous studies from finding shreds of evidence seem to be linked to the cumulation of social responsibilities involved in inclusive criteria, as well as a surplus in demand on the socially responsible stock market potentially inaccurately adjusted in most of the models. Aggregate results appear to converge towards a lower weighted average cost of capital for sustainable firms, mostly due to cheaper access to equity by lowering the required rate of return of shareholders. As the inherent risk of a firm is negatively correlated with its environmental and social risk management strategy, a lower cost of equity does not necessarily mean lower incomes for shareholders, as these returns (i.e. dividends) shall be risk-adjusted. Results suggest that the reduction of risks a firm benefits from being socially responsible offsets the cash outflows of investing in societal programs, at least as long as the company does not need to restructure itself (i.e. changing the entire manufacturing process or investing in new technologies). Nonetheless, this effect cannot always be observed on account of a certain number of adjusting factors, such as the difference of the book-to-market ratio due to an asymmetry in the demand.

In conclusion, it appears that although the opinion that socially responsible firms outperform conventional competitors is not always well supported by empiric results, explanations of why it is the case tend to point towards confirmation of the theoretical literature, which predominantly suggests such results.

Contents

Do Socially Responsible Investments Outperform Conventional Ones? ... 1

Disclaimer ... i Executive Summary ... ii Contents ... iii List of Tables ... iv List of Figures ... iv 1. Introduction ... 1 1.1 Sustainable Finance ... 1 1.2 Theoretical literature ... 2 1.3 Outcomes ... 3

2. State of the art ... 5

3. Methodology ... 11

3.1 Development ... 11

3.2 Methodology assessment ... 11

3.3 Self-assessment ... 13

4. Results ... 15

4.1 SRI: weaker performance ... 17

4.2 Lack of disparity ... 18

4.3 SRI: better performance ... 19

5. Discussion ... 22

5.1 Market supply ... 22

5.2 Market demand ... 23

5.3 Opposing forces ... 24

5.4 Firms’ financial incentives ... 25

5.5 Effect of risk management ... 27

5.6 Recommendations ... 30

6. Conclusion ... 32

List of Tables

Table 1 Results in the literature ... 16

List of Figures

1. Introduction

1.1 Sustainable Finance

A socially responsible firm will be aware of its environment, perceptive of social, cultural, and economic consequences resulting from its operations and will contribute to the welfare of the society (Lapiņa, Borkus, Leontjeva 2012: 1606). This concept is derived from the notion of Sustainable Finance. A responsible firm, conducting a sustainable approach, is considering the future repercussions of its contemporary actions (Soppe 2004: 213). The scope of its current strategy is hence extended to a broader vision, allowing long-term benefits to overweigh the temptation of immediate rewards at the expense of forthcoming welfare. Sustainable development will therefore contribute to current and future generations (World Commission on Environment and Development 1987).

The direct consequence of a sustainable approach is that mutual and common interests are favoured rather than individual benefits at the expense of others. It hence limits the negative externalities linked to the operations of businesses. The opposite would imply that individuals or entities which are not involved in an activity and do not gain anything from it still have to bear some of the costs linked to this operation. Such costs can include health damages, polluting and unsustainable manufacturing processes, promotions of irresponsible products (i.e. contributing to child/forced labour), or practices unfairly contributing to inequalities (Biglan 2009: 1). When externalities exist, it implies that the rewards obtained throughout the activity in question will only benefit the parties involved but will generate costs for unrelated parties, causing global welfare to decrease. Whether a firm shall carry the burden of enhancing the prosperity of the society instead of exploiting common resources to serve its interest is a subjective question. At least, the law does not oblige companies to maximize revenues of shareholders (Mackey, Mackey, Barney 2005), but to execute and implement legitimate decisions taken by investors (Fairfax Annual Report 2002). This important detail leaves room for a firm to concentrate on social actions that do not necessarily maximize revenues.

The underlying purpose of this thesis is not to examine the pros and cons of conducting a sustainable approach, neither to provide a subjective opinion on the topic. The aim is to address this matter from the perspective of an investor or a board of directors, maintaining financial growth as the center of interest. The effects inherent to sustainable finance such as the preservation of the environment, the reduction of inequalities, or the

improved standards of living will not be part of the analysis, although these elements could have an indirect impact on the growth of a firm.

1.2 Theoretical literature

Considering that investments are the fuel and the root of any project or action undertaken, they are certainly a key resource in the quest for global social welfare. Yet, the allocation of investments is not always socially efficient, sometimes supporting polluting firms, child labour, encouraging modern slavery (underpaid labour), and much more. Indeed, the ultimate goal sought by investors being profit, global welfare is surely not the primary parameter that drives investments. In this context, mutual investment funds, and underlying firms are being compared based on eventual returns on investment (i.e. dividends, market shares price) relative to the risk inherent to the investment. At first glance, it seems that investors perceive a price to invest socially responsibly, meaning that such investments are considered less attractive financially speaking (Climent, Soriano 2011: 14).

Nevertheless, we can observe that the existing theoretical literature suggests a positive causality link between social responsibilities and financial performances for underlying firms of mutual funds. According to Lammertjan Dam, responsible firms will perform better by avoiding negative outcomes thanks to the anticipation of forthcoming issues (Dam 2008: 83). Indeed, an accountable firm shall not cheat on anti-pollution tests or neglect safety procedures while shipping a cargo of oil, for instance, hence reducing the probability of an accident occurring. Both of these events, if occurring, might cause penalties which would impact future cash flows, or negatively affect the reputation of the firm along with its stock price. Moreover, a company that has anticipated new governmental measures or demand from consumers on social and environmental standards could avoid extra restructuring costs compared to its competitors by having projected them (i.e. amortized over a longer timeframe), hence gaining a competitive advantage. A good and recent example could be the new IMO 2020 regulations imposed by the International Maritime Organization aiming at reducing the sulphur content in the fuel of ships (International Maritime Organization 2020). Vessels can no longer use oil high in sulphur content, which is cheaper than low sulphur oil. If shipowners want to keep on using the high sulphur bunker1, they must equip their ships with specific scrubbers

that are also very expensive to purchase and install. A shipowner who had anticipated such measures could expect to have gained a competitive advantage over its peers if he

had purchased its new vessels in already compliant conditions, or by having purchased scrubbers on a longer period to smooth his costs curve. This suggests that firms that proactively behave responsibly will reduce their exposure to negative events causing financial distresses. This view is unambiguously shared in the theoretical literature. An important point is that regardless of the outcomes of empirical studies, it is true that a firm anticipating such incidents will reduce its exposure although it will not mean that implementing such a safeguard will be a financially attractive deal. A good analogy would be how we see health insurance in our society. Most of the time, one would have been better off without any insurance, though it seems to be a judicious choice to take one. If empiric results do not show any difference in the financial performance, one shall bear in mind that the related risk level has decreased. Hence a similar performance would be a better performance.

Nonetheless, and despite these reasoned explanations supporting a possible causality link between social responsibility and financial performances, empirical studies do not always concord with this statement. A consistent number of them suggest only a tiny, sometimes even a nonsignificant difference between the responsible stocks and conventional ones (Galema, Plantinga, Scholtens 2008: 2646). Other studies even indicate the possibility of lower expected returns for green of responsible stocks compared to others (Hong, Kacperczyk 2009: 15). This demonstrates that contradictions subsist between the theoretical literature and empirical studies, which is the principal reason for this thesis to be conducted. The purpose of this paper is to determine what parameters contribute to these disparities and to assess whether they are flawed or founded.

1.3 Outcomes

After having reviewed numerous studies, some parameters explaining incongruences with empirical work and theoretical papers emerged. Sometimes recurrent, sometimes unique, sometimes potentially flawed by the methodology, they will form the red string of the discussion of this paper. The first parameter to be analysed is the market supply of socially responsible funds. Naturally, the demand side is to be assessed as well. Another interesting element that emerged was the possibility of opposing forces within a sample of funds (Scholtens, Zhou 2008) (Galema, Plantinga, Scholtens 2008). This could alter the results of an empirical work depending on how the sample tested is composed, or simply based on the nature of the events having impacted the stock market during the period tested. Partially linked with the market supply and demand, the proportion of responsible investors and responsible stocks compared to conventional ones (or the total

population of investors and available stocks) is also a parameter that could explain dissimilarities only based on the sample, location or period the study is conducted. Lastly, the cost of financing related to environmental risk strategies, which is only indirectly linked to the operations of a firm, can also be an element of a discrepancy. This paper will analyse these parameters, predominantly trying to identify if it consists of flaws arising from methodologies and other sources, or if they reflect the reality of the market. The expected outcome is hence not necessarily an affirmative or a negative answer to the initial enquiry of whether socially responsible investments perform better, but more a conglomeration of parameters explaining why differences exist and allowing us to understand if the financial performance is destroyed or enhanced by such strategies.

2. State of the art

The role of large corporations in society has not always been studied. The relationship between society and sizeable firms had raised questions on how corporations impacted the social environment. Preston has initiated studies on the social behaviors of firms (Preston 1975). But the idea that a firm being aware of its social or ecological environment could improve its financial performance really emerged with the study named “Investors, Corporate Social Performance and Information Disclosure: An Empirical Study” conducted by Barry Spencer (1978). As its title indicates, it consisted of empirically studied whether companies performing better from a social perspective would also generate extra returns. He tested two groups of firms, one composed of companies that had had better scores at pollution tests than the others. He found that these firms had a propensity to be more profitable, though the effect was observed in the short term only.

The idea of conducting responsible investment strategies was not unanimously well perceived, and some concerns on the exclusionary implications arose. Andrew Rudd addressed the issue in the context of pension funds, implying large-scale investment flows, which would exclude some companies based on a certain type of criteria (Rudd 1981). The central argument was that the beneficiaries of these investments were deprived of numerous stocks that were prohibited. Interestingly, it was not yet a question of higher risks due to restraining the choice of stocks but truly an ethic matter. Another issue that is partially addressed in this study is the selective process of inclusive criteria. The lack of sufficient qualitative models evaluating social performances (at that time) entailed that these criteria were subjectively picked by the board of directors, leaving room for personal preferences on the type of criteria rather than a quantitative and objective assessment.

The evaluation of reactions of investors regarding governmental regulations potentially causing financial distresses on an industry appeared in 1991 when the Supreme Court in the United-States ruled that the cotton industry shall follow environmental standards administered by the Occupational Safety and Health Administration (OSHA). Freedman and Stagliano studied the effects that such information would cause on the industry. Their results eventually showed that investors had reevaluated the stocks of the industry and that the profitability of these firms had shrunk (Freedman, Stagliano 1991). This could serve as a stepping-stone for the idea that firms could avoid such effects in case of new restraining measures by anticipating them spontaneously through investments in environmental and social risk management systems.

In 1993, Hamilton, Jo, and Statman published a very consistent paper called “Doing Well While Doing Good?” (Hamilton, Jo, Statman 1993), which englobes a lot of different aspects of this topic. Firstly, they retook the four purposes of investing socially responsibly of Lowry (1993). At that time, these were to encourage the hiring and the empowerment of employees, as well as bringing back women to equal treatment, monitoring a healthy redistribution of profits, and finally proving that investing responsibly will be more profitable (Lowry 1993). Interestingly, no empirical studies were supporting those social responsibilities would pay off at that time and to my knowledge. Nonetheless, Hamilton, Jo, and Statman explored this topic aiming at discovering if responsible firms generated extra profits compared to conventional ones (i.e. excluded from SRI criteria). Their hypotheses on the outcome of the question are that if socially responsible investment funds perform better, it would entail that conventional investors do not anticipate enough ecological or social scandals firms can cause. It implies that each time it occurs, stock prices would be driven down (Hamilton, Jo, Statman 1993: 63). The other alternative is that conventional firms outperform, which entails that responsible companies are overpriced by the market (Hamilton, Jo, Statman 1993: 64). This could be identified as the book-to-market ratio, which will be addressed further. The oldest study analyzed in this paper addressing the impact that responsible actions have on the risks of a firm rather than directly compare performances is named “Does Improving a Firm's Environmental Management System and Environmental Performance Result in a Higher Stock Price?” (Feldman, Soyka, Ameer 1997). Their idea was that as a company reduces its exposure to social and environmental measures (or negative events as discussed in section 1.2), it will moderate its financial risks and this reduction will be perceived by the market. They concentrated their research on the perception of the systematic risk exposure, i.e. the Beta in the Capital Asset Pricing Model2 (Sharpe 1964). The relationship between social responsibilities and the cost of

capital (here through the perception of risk and the cost of equity) begins to be addressed. The second branch of the cost of capital, the cost of debt, is yet not part of the research. Carroll and Niehaus will partially address it, although they do not really take the perspective of social responsibilities but focus on pension plans of firms. They

2 𝑅

"= 𝑅$%+ 𝛽 × (𝑅+− 𝑅$%)

Where:

Ra = expected returns Rrf = Risk-free rate

Rm = expected market returns b = systematic risk

confirmed that unfunded liabilities can be considered as more debts for companies, hence weakening their debt rating, which would cause higher interest rates (Carroll, Niehaus 1998). Having premium pension plans is part of social performances (or score) of firms, but this study is too specific regarding the subject of this paper.

The cost of equity of firms keeps on being the main element of comparison, notably with an article published by Heinkel, Kraus, and Zechner on the behavior that firms will adopt regarding their cost of equity (Heinkel, Kraus, Zechner 2001). They have built a model displaying the variations of the cost of equity due to the proportion of green investors. In this model, green investors undertake an exclusionary investment strategy by avoiding polluting firms. The more ecological-friendly investors there are the more concentrated the risk will be among stockholders of polluting firms. This will cause the stock price of polluting firms to decrease and the cost of equity will increase accordingly. Heinkel, Kraus, and Zechner have computed an intercept between the rise of the cost of equity and the presumed costs for polluting firms to restructure their business model to become green (i.e. investing in new technologies). This model demonstrates that investing ecologically affects the behaviors of firms, although an important proportion of green investors is necessary to trigger a reaction from businesses.

The demand for corporate social responsibilities is also addressed in this thesis. Mcwilliams and Siegel had published an article in 2001 that tackles the demand side. They established the demand as a request coming from consumers, governments, shareholders (especially institutional investors), employees, and other external stakeholders (Mcwilliams, Siegel 2001: 119). To respond to this demand, firms shall integrate corporate social responsibilities in their cost function (Mcwilliams, Siegel 2001: 122). Indeed, their model defines social actions as a firm making an extra effort to satisfy the requirements of the community than the law obliges to. This entails an extra cost relative to other firms, assuming the others do the strict legal minimum. The supply and demand character of this model brings an interesting element that all supply and demand models share in common: an equilibrium. Here, the extra costs a firm will incur by conducting a social action will allow it to face a higher level of demand than its competitors for the same price. Oppositely, the savings an irresponsible firm will make by avoiding any implementation of actions none profit-driven will lead it to face less demand at any given price (Mcwilliams, Siegel 2001: 124). The stakes of this model are that there is an optimal quantity of corporate social responsibilities in society.

This new notion raises the question of what happens if the supply or the demand for socially responsible activities deviates from the equilibrium. A theoretical model has been

built answering this enquiry in 2005 (Mackey, Mackey, Barney 2005). The model puts in relation the value of a firm with the value of social actions the company can undertake. It suggests that depending on the settings of the market, operations maximizing the firm’s social value shall be conducted, taking precedence over activities maximizing the business’ financial value. As any equilibrium model, it also suggests than in different market settings, the opposite can occur. When the demand for responsible investments is greater than the supply (i.e. more responsible investors than the number of firms matching the social responsibility criteria), a company has great interests in initiating social activities. It will drive its share price up despite the cash outflow that its actions generate immediately. In the case where the supply is greater than the demand, the opposite will occur, as too few investors would perceive value in investing in responsible firms with a harmed cashflow due to non-profit actions. Lastly, if the market is at the equilibrium, firms shall not alter their strategy as any action (reducing or increasing socially responsible activities) will lead to an oversupply in either responsible or irresponsible firms, causing a decrease in the stock price (Mackey, Mackey, Barney 2005: 6). Similarities between this model and the one previously discussed firms’ financial incentives to invest in a restructuring (Heinkel, Kraus, Zechner 2001).

In 2006, an interesting question that could explain why so many inconsistencies exist in empirical results is addressed: whether socially responsible investment funds really conduct a different strategy than conventional ones, i.e. do managers of such funds truly invest responsibly (Benson, Brailsford, Humphrey 2006). Fundamentally, the strategy is not different as both fund managers will invest in the firms they choose to be the best fit in their strategy, although socially responsible funds will restrict their range of choices. The question is justified especially as so few differences between the two strategies have been observed in terms of returns. Fortunately, they found that parameters clearly indicate variances between the two such as the market risk. Nonetheless, these differences seem to vary from year to year, which of course indicates another element that could alter results while comparing SRI and non-SRI funds.

An empiric test showed that a portfolio having been managed under a long-short strategy on socially responsible stocks during the timeframe 1992 - 2004 would have had better results than a similar portfolio under a similar strategy with non-responsible stocks, although some adjustment factors could not be tested (Kempf, Osthoff 2007: 13). With this long-short strategy, researchers simulated an investment scheme where they would have bought stocks that scored well on social and environmental criteria whilst sold the stocks that scored poorly. Their results are partially inconsistent with the outcomes harvested in the study of Climent and Soriano, though not entirely. Indeed, they also

conducted an empiric study where they observed the opposite within the period between 1987 – 2001 (Climent, Soriano 2011: 13). Thereafter, they found that between 2001 and 2009, this underperformance readjusted to a non-significant difference. Of course, although both studies analyzed American firms, their methodologies differ, especially concerning the investment strategy of Kempf and Osthoff whilst Climent and Soriano conducted a match-paired analysis of two sorts of investment funds. Moreover, Climent and Soriano focused their attention on green firms, i.e. scoring well on environmental criteria, which narrow down the range of firms to invest in, whilst the approach of Kempf and Osthoff was a bit broader.

In 2008, three researchers explored why so few empirical studies have supported the theoretical literature hypothesizing that socially responsible firms shall outperform their conventional competitors (Galema, Plantinga, Scholtens 2008). They demonstrated that the book-to-market ratio (addressed in section 4.1) is the main cause of a significant difference in performances. It also implies that outperformance is not always concretized as a high or low book-to-market ratio does not necessarily impact immediately the performance, which explains why variations are not always measurable. They hypothesized two errors that would have prevented previous studies from finding pieces of evidence supporting that socially responsible investments outperform their conventional peers. They conducted multiple regressions and statistical tests, giving them relatively solid robustness of results. Nonetheless, some adjustments factors are still not perfectly tested and some shreds of evidence are less statistically robust than they would like to, especially the pressure of the opposing forces within an aggregate analysis of portfolios (further explained in section 5.3) (Galema, Plantinga, Scholtens 2008: 2653).

In partial contradiction with these results, a study in 2009 has shown that irresponsible stocks could have higher expected returns (Hong, Kacperczyk 2009). It suggests that investors do not underestimate the probabilities of harmful events linked with companies involved in unethical activities, which leads them to expect higher returns to compensate for the risks. In that case, it also suggests that institutional investors incurred foregone revenues by following investing norms. We can draw a parallel of this approach and the book-to-market ratio, although the views are inverted.

Meanwhile, researchers discuss more recent concepts than social responsibilities such as creating share value (CSV). Creating share value implies increasing both financial and social values for the firm concurrently (Lapiņa, Borkus, Leontjeva 2012: 1605). It shows that these concepts are constantly evolving over time and remind us that some

historical studies might not be relevant anymore, as businesses are evolving, and new managerial perspectives emerge constantly.

Over time, the database of studies has cumulatively increased. This makes room for new research to observe possible correlations or other reflections on larger quantities of data, such as Mattingly who examined an aggregation of empiric studies to find coherent or incoherent observations in firms’ conduct (Mattingly 2017).

3. Methodology

3.1 Development

The research is essentially based on the existing literature. The first phase consists of gathering information on what has been published around this topic, what are the current ideologies as well as what is being debated and why. The aim of this stage is merely to acquire knowledge about the subject, but also to identify what could be explored and where are the shadow zones that shall be addressed. Hence, the process is predominantly to enquire oneself on a subject and to try to find answers on the existing literature. If responses can be found, the next step is to test them and to try to undermine them, either by finding flaws in the methodology or by discovering contradictory studies, which themselves will also be assessed. Of course, the standpoints that cannot be undermined at this level are to be kept for further examinations.

This process will be successful only once a debatable question emerges from the research. At that point, some studies might contradict each other or simply slightly differ, but none could clearly respond to the enquiry without any counterarguments or disputable elements. As a reminder, the principal aim of this thesis is to provide a thorough picture of the current findings, not necessarily to respond affirmatively or negatively to the initial enquiry.

Subsequently, the research will be oriented around this main question. The next purpose is to classify the related literature found and to group similar arguments, or studies supporting the same philosophies. The assessment of methodologies used even within the same group of studies could strengthen or weaken the viewpoint in question. Finally and ideally, if some studies appear to be stronger or more reliable than others, the final purpose would be to identify them and draw a conclusion with a plausible answer to the original inquest.

3.2 Methodology assessment

The kind of studies that will be addressed usually employs high-level statistical methodologies that are well above the academic standards of this thesis. Indeed, the topic of this research requires statistical tests on a very large scale. Testing mutual funds implies assessing the sizing of each investment fund, i.e. the maturity and size of each firm that is purchased by a fund, but also the geographical regions, the currencies, and other elements that require complex models which are out of the scope of this paper. Moreover, an assessment of the parameters allowing funds to be considered socially

responsible is necessary. Fortunately, some of the studies already report some potential rooms for errors in what they have computed, whilst others point out the strengths of their model and some even compare their methodology to what has been previously published. Reporting these strengths or flaws will help to identify the different studies that shall be considered.

Additionally, my academic background allows me to determine four potential flaws that I consider likely to occur or that I have already observed in the literature prior to the Research Proposal. The first one is to immediately identify if the researchers have used adjusted returns in their comparison of performance. If these returns are not risk-adjusted, it is certain that the outcomes will be flawed, or at least not relevant for what is addressed in this paper. Secondly, and as it will more often be about regressions (i.e. performances with and without inclusive criteria to social responsibilities categories), the type of regression is a fundamental parameter and will play a determinant role regarding the final results. I will not have the capabilities to identify every potential weakness of each type of regressions. Nonetheless, the identification of different methods used will be useful to formulate plausible reasons for different outcomes, or even to strengthen an opinion if it is supported by many different approaches. Another parameter that will be investigated is the type of inclusive criteria in order to consider an investment as being socially responsible or not. That will be done by assessing from where the data come from (i.e. KLD or other external data providers), aiming at identifying an eventual correlation between different types of criteria across distinctive studies, or simply to identify a potential source for disparities in outcomes. The last factor that will be scrutinized is if the study takes into consideration the book-to-market ratio or not (see section 4.1). Indeed, a lot of researchers use in that context the Fama and French regression (Fama, French 1992) which does not include the book-to-market ratio (Galema, Plantinga, Scholtens 2008: 2647).

Of course, the assessment of social responsibilities criteria is also to be undertaken. Not all studies use the same database and the same criteria. Although the definition of social responsibilities is not subject to changes. the inclusive standards have changed over time. “Doing Well While Doing Good?” (Hamilton, Jo, Statman 1993) is an excellent example of this fact. At that time, they excluded all firms that were conducting operations which had something to do with South-Africa. Back then, it surely could have been immoral to have business relationships in this country, given the racist politic that was conducted back then. However, this criterion is totally irrelevant nowadays and including firms in a responsible fund because they do not have a relationship with South-Africa could surely alter our results. This is an important reason to carefully select a

bibliography that is homogenous enough to be comparable, but not too much either in order to avoid an anchoring bias3.

3.3 Self-assessment

This methodology that will be used throughout the research is composed of one major flaw. It is linked to the anchoring bias. The chronological process of my methodology implies that my research will be evolutive. The further the research progresses, the more arguments will be learned. The weakness and the risk of it are that the first studies that will be assessed might play a predominant role compare to the following ones. As each study relies on a bibliography, it will provide many similar results. Moreover, the first pieces of information learned in the process may become the central point of the following research instead of conducting an authentic (non-biased) study.

A manner to partially remedy it is to create a database of academic papers related to the problematic prior to the initiation of the analysis of these sources. This will allow the research to build a grounding of sources without being influenced by the results of each of them. Of course, it only limits the bias during the initial phase of the thesis, as the database will be expended with the advancements of the research. Nonetheless, this phase will provide a starting point around which the study shall gravitate, especially after having explored parallel problematics in order to not get lost in a different sphere. It will also be a helpful basis to compare the final outcomes with the initial problematic of the research.

Another issue of the methodology used in this research is linked to the academic level of this thesis compared with the studies it will be assessing. Most of the articles, if not all, will have been conducted at a much higher academic level, hence exceeding the scope of this research. A concrete concern and frustration for the thesis would be the assessment of the statistical methods used in each of the sources. One of the principal aims of this research could be flawed or will be at least limited due to a lack of expertise. Nevertheless, the primary objective of this study is to gather information and erect a clear picture of the arguments supporting an opinion present in the literature and of different

3 A cognitive bias often referring to the decision-making process that human beings make.

One will start to learn information that will create an opinion, and one will tend to seriously rely on this first piece of information. Moreover, further research about this information will tend to be oriented towards a confirmation of this initial opinion. For instance, if one believes in a conspiracy theory, one will tend to look mostly for sources confirming this thought, i.e. by typing “The conspiracy theory explained” on internet. Each confirmation will of course reinforce the initial opinion while decreasing the reliability of contradictory sources.

findings. The assessment of each of the studies is to be considered more as a selection process or a filter based on criteria explained in section 3.2. It will also serve the purpose of formulating plausible hypothesis in the case of disparities of outcomes between different studies, as previously mentioned.

4. Results

The results collected throughout the research concern opinions or empiric outcomes related to the question of whether socially responsible firms (or mutual investment funds) perform better than conventional ones. They are split into three categories, although these groups are precarious short-cuts and shall not be considered as an exact representation of the entire results of each study. Indeed, most of them need further explanations, or some sources only respond to the question indirectly or in a more specific manner.

The first category gathers the findings displaying an underperformance of socially responsible investments. The second group clusters results presenting no difference or very few. This neutral category does not necessarily show no difference in performance, as it could also be due to adjusting factors or flaws that led the results to be ambiguous. The last category exhibits outcomes supporting a greater performance from socially responsible investments.

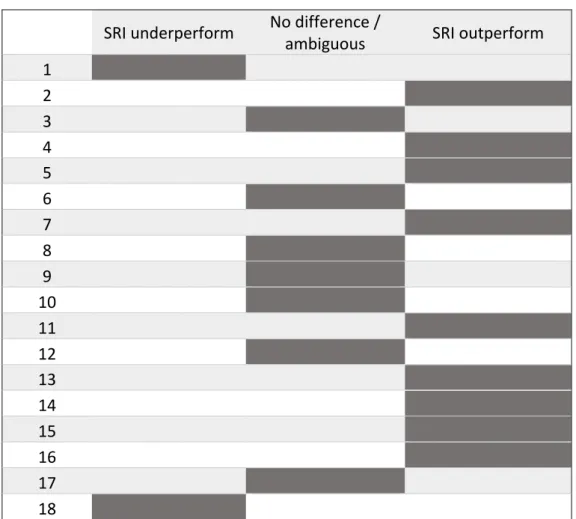

Below is a table showcasing an extract of 18 studies ordered chronologically. This chart is not exhaustive regarding the studies analyzed throughout this thesis, and the three categories of the table are as well not entirely accurate, as some studies may address a slightly different question, being conducted in different locations, or tackle a more specific theme than the question of this paper (i.e. focusing on only one social responsibility rather than aggregate criteria). Nonetheless, the following provides a raw synopsis of what will be further discussed.

Table 1 Results in the literature

SRI underperform

No difference /

ambiguous

SRI outperform

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

1. Rudd 1981 2. Freedman, Stagliano 1991 3. Hamilton, Jo, Statman 1993 4. Lowry 1993

5. Feldman, Soyka, Ameer 1997 6. Carroll, Niehaus 1998

7. Heinkel, Kraus, Zechner 2001 8. Mcwilliams, Siegel 2001 9. Mackey, Mackey, Barney

2005

10. Benson, Brailsford, Humphrey 2006

11. Kempf, Osthoff 2007 12. Fernandez-Izquierdo,

Matallin-Saez 2008

13. Galema, Plantinga, Scholtens 2008 14. Scholtens, Zhou 2008 15. Sharfman, Fernando 2008 16. Hong, Kacperczyk 2009 17. Climent, Soriano 2011 18. Pokorna 2017

4.1 SRI: weaker performance

In America, it seems that socially responsible investment funds performed less than conventional ones between 1987 to 2009, with an underperformance of 4,22% (Climent, Soriano 2011). Nonetheless, the same study shows that the cause of this overall underperformance can be entirely allocated to the period between 1987 to 2001. Thereafter, the variance in performance was not significant anymore, along with the expansion of the supply in SRI funds. The criteria of inclusivity used in that sample are mostly concentrated on environmental responsibilities. Climent and Soriano (2001) also displayed a higher market sensitivity (i.e. Beta) for green funds than for conventional ones and even other socially responsible funds (besides ecological criteria). Despite that, no reference is made on the aggregate evolution of the stock market and the correlation of these investments.

How the demand for responsible funds is affected is also a potential source of indirect underperformance. Indeed, all investors are potentially willing to invest in socially responsible funds whilst a proportion of them exclude irresponsible ones (Heinkel, Kraus, Zechner 2001: 431). Such surplus in demand for green (or other responsible) stocks could lead to overrating them, and vice-versa for the polluting (or other irresponsible) stocks (Galema, Plantinga, Scholtens 2008: 2646). Accordingly, the fewer investors sharing the ownership of a firm, the fewer there will be to support the risks. A higher risk concentration on each shareholder will lead to a higher cost of equity for the firm, as more risk per capita requests more returns (Merton 1987).

Out of various categories of social responsibilities a firm can have, it intriguingly seems that the Good Governance factor is the worst in terms of indirect performance (Galema, Plantinga, Scholtens 2008: 2653). Indeed, firms that have excellent standards of governance appears to be over demanded, which will ineluctably lower their book-to-market ratio4. This could be explained by the communication of firms about the

governance practices, the policies put in place, the feeling of security that it provides amongst shareholders, etc. Indeed, annual reports of corporations recurrently showcase such information at the beginning, and it surely reassures the shareholders that the firm they invested in is being well managed. Clearly, this does not imply that well-governed

4 The book-to-market ratio puts in relation the market value of a firm and its book value. If

the ratio is low, it implies that a small proportion of the market price of a firm will be supported by its book value, which refers to an overvaluation. Oppositely, a ratio above one implies that the book value of the firm is greater than its market price, which referes to an undervaluation. The book value varies from one accounting regulation to another which could lead to some discrepancies. Nevertheless, identifying if all firms report under US GAAP or IFRS in aggregate measurements can be too complex.

firms will underperform or will see their productivity fades. Nevertheless, it denotes that the price of a share paid by an investor is likely to be inflated by the excess in demand for this share. Consequently, purchasing a stock which is over evaluated is likely to lower the performances of the investments assuming that the market will readjust the price. Nonetheless, the market could still continue to overrate the firm over the entire period that the holder keeps his shares, thus avoiding a downward readjustment of the market price of the investment.

Finally, it is worth to remind that the possibility to diversify a portfolio is essential from an investor perspective. As Pokorna underlines, a value-driven investor has no benefits in restraining its range of investment opportunities, as it would increase his risk (Pokorna 2017: 56).

4.2 Lack of disparity

Most of the studies analysed in this paper displayed no significant differences in performance between socially responsible investment funds and conventional ones. The study “

Doing Well While Doing Good?

” has established statistically similar results, namely that mutual funds matching the inclusive criteria do not generate excess returns (Hamilton, Jo, Statman 1993: 62). The analysis covers the period between 1981 to 1990. Because of an increase of responsible mutual funds in the database used in the study, they alienated these funds in two categories, one initial and one with the more recent funds. Nonetheless, the results were similar and as it only slightly overlaps on the period observed by Climent and Soriano (2011), i.e. 1987-2009, the two studies cannot contradict each other’s outcomes. The database used by Hamilton, Jo, and Statman (1993) is provided by Lipper Analytical Services, which considers a lot of criteria in order to be responsible according to them. A few examples could be the participation in a community, the sound pollution, the energy sources, the safety of the products a firm manufactures, and much more (Hamilton, Jo, Statman 1993: 63). This could lead to the problematic of opposite forces within the sample, which will be further discussed in this paper (section 5.3). A problematic that is not addressed in the study of Climent and Soriano (2011) is the size factor. Although they use a match-paired analysis (hence including the sizing into the comparison of funds), they do not take into account that larger companies tend to attract even more investors, which will reduce their weighted average cost of capital (Gebhardt, Lee, Swaminathan 2001), neither do they consider that larger companies tend to be more involved in improving their environmental impact, hence to have more mature investments in such strategy (Bansal 2005).Although a lot of studies show an ex aequo in the competition between the two types of stocks, it is almost often due to adjustment factors. Most of the time, the causes are the demand dynamic or the book-to-market ratio (Galema, Plantinga, Scholtens 2008: 2652). These two factors can in fact be considered as a unique one. Indeed, there is a causal link between the book-to-market ratio and the demand, which is at the basis of the overpricing of socially responsible stocks. This could be the main reason why socially responsible stocks do not generate extra adjusted returns compared to stocks excluded from socially responsible criteria but do not underperform them either.

4.3 SRI: better performance

The demand, as previously saw, will drive the price of a stock, and strong or weak demand could lead a company to be over or underpriced. Results show that another effect of the demand could lead firms to have financial incentives to become socially responsible to have access to cheaper capital and gain competitive advantage (or erase their competitive disadvantage). Indeed, the demand also impacts the proportion of risk spread among shareholders, simply through the number of them. When risks drive required returns from stockholders, it also impacts directly the cost of equity of the firm. The more risk a shareholder will tolerate, the higher returns will usually be required from him. If the proportion of green investors increase compared to conventional ones, the demand for irresponsible stocks will decrease accordingly, due to the exclusionary preferences of these investors (Heinkel, Kraus, Zechner 2001: 431).

The model built by Heinkel, Kraus, and Zechner (2001) establishes the relationship between the proportion of green investors and irresponsible firms. As more green investors will reduce the demand for conventional stocks, the required returns of these stocks will increase, leading to more expensive access to equity. The main barrier for firms to reform towards a more sustainable structure is the costs that such a transition would generate. The increase in the cost of equity due to the proportion of responsible investors and the costs to restructure the firm will, at some point, form an equilibrium. Firms would then have financial incentives to restructure the company as soon as the costs of equity have overweighed the expenditures a reform would generate. Contrariwise, firms would have financial discouragements to reform when their cost of capital remains below the restructuring costs. This model shows that a proportion of at least 25% of green investors is necessary to raise the cost of equity above the outlays of reforming the firm (Heinkel, Kraus, Zechner 2001: 447). They also show empiric indications that at that time (in 1994 more precisely), only 10% of mutual funds were actually investing in socially responsible firms in the United-States, which is not enough

to induce irresponsible firms to reform but still increases their cost of equity, hence reducing global welfare.

The main weakness of this model is the assumption of the restructuring costs. It is indeed too complex to compute accurately, especially to model at a broader scale. An evolution of the technology available to the firm could for instance completely alter the costs we initially assumed. Hence, although it will not change how the model works, it will totally alter the equilibrium point. The second main weakness of this study would be the assumption that green investors only invest in green stocks. Although more responsible investors will increase the demand for responsible investments, they might also contribute to a rise in the demand for conventional stocks, although less than if they were conventional investors, but still more than if they only invested in green stocks. It would lead to an ambiguous increase in demand. This could surely alter the equilibrium points as well.

Mark Sharfman and Chitru Fernando have a slightly different opinion on this idea that the lesser investors holding stocks the higher will be the weighted average cost of capital (WACC) (Heinkel, Kraus, Zechner 2001), which as previously mentioned would be of great concerns for polluting or irresponsible firms as institutional investors neglect these stocks, depriving these firms of an important supply of capital (Hong, Kacperczyk 2009: 35). In their study about the effect that environmental risk management has on the WACC, they also assume that firms investing in environmental risk management systems will beneficiate of a lower cost of capital, however not only due to the demand but to the structure of the capital of a firm (Sharfman, Fernando 2008: 11). They discovered that as a firm improves its environmental risk management strategy, its cost of debt will intriguingly increase, which seems to go against the hypothesis that being socially responsible will grant firms cheaper access to financing. This could be partly explained by the fact that firms with a better risk management strategy have the ability to borrow more, thus to increase their level of debt (Sharfman, Fernando 2008: 22). A higher level of debt implies more cost of debt, although it could benefit the firm with the leverage effect and the tax benefice. Furthermore, they found that better environmental risk management systems will reduce the Beta (sensitivity to systematic risk) of the firm (Sharfman, Fernando 2008: 24). Moreover, improving the environmental impact of a firm will decrease the risk perceived by the market and a lower return will be required by shareholders (Feldman, Soyka, Ameer 1997: 11). In conclusion, the effect that improving a firm’s environmental risk management strategy will have on the cost of debt is ambiguous, as it directly increases it but might allow the firm to leverage its capital structure and to enjoy a tax bene1fits subsequently. On the other hand, it will positively

impact the cost of equity of the firm (reducing its cost), which will normally offset the potential rise in the cost of debt. The overall weighted average cost of capital of the firm will hence be lowered.

The methodology of Mark Sharfamn and Chitru Fernando (2008) is potentially composed of two flaws. Firstly, the aspect of investing in environmental risk management systems, and the effect on the WACC is lagged. They assume that such implementation will impact the WACC of the following year, which surely depends on the type of investment. Secondly, the relation between environmental performances and economical performances can be positively correlated (Sharfman, Fernando 2008: 30). It would imply that there is not necessarily a causal link between both and that better environmental performance simply arises due to a good economical year or vice-versa.

Finally, the scope of social responsibilities can be genuinely broad. It implies that surely not every social responsibility of a firm has the same effect on its financial performances. It seems that three categories of social responsibilities have positive effects on returns, which are the diversity, environment, and product (Galema, Plantinga, Scholtens 2008: 2653). These categories are extracted from the KLD database5. The first classification is

about the assortment of the top management and Board of Directors, but also the entire workforce of the company. The environment criteria are based on the impact the firm’s operations have on the ecosystem, while the product category is more concentrated on the manufacturing process and product attributes that the firm commercializes.

5 The MSCI KLD 400 Index has been established in 1990 and has been updated on a

regular basis by MSCI (Morgan Stanley Capital International). It gathers data and rates firms on the basis of their environmental, social and governmental (ESG) values, and attributes strengths and weaknesses among them. For more information, consult https://www.msci.com/msci-kld-400-social-index

5. Discussion

5.1 Market supply

Francisco Climent and Pilar Soriano in their study entitled

“Green and Good? The

Investment Performance of US Environmental Mutual Funds”

found that environmental funds between 1987 to 2001 performed less than conventional ones (Climent, Soriano 2011). However, from 2001 to 2009, no statistically significant difference has been observed. Overall, socially responsible investment funds in the United-States performed less by 4.22%, only due to the primary period. As this study focuses mainly on environmental funds, the researchers have also compared them with aggregate socially responsible investment funds (except Green funds), which englobe all sorts of responsibilities such as social aspects, good corporate governance, practices aligned with human rights and more. Green funds can be seen as one layer more specific within the SRI funds. Nevertheless, they tend to show similar results, except for one being the market sensibility, called “Beta

” according to the Capital Asset Pricing Model (Sharpe 1964). Indeed, it appears that the Beta of green funds compared to other SRI funds (but also to conventional ones) is greater, implying a higher market sensitivity (Climent, Soriano 2011). Besides these elements, we will not differentiate SRI from green funds further in this thesis.Many different statistical tests have been conducted in this study, with often some discrepancies in the statistical significance of the differences in adjusted returns of SRI and non-SRI funds. The differences may be substantial or not depending on the market proxy used, on the risk-adjusted method (i.e. using the sharp ratio versus R-squared), the model used (here CAPM model / Multi-Factor model, etc), the sampling methods, the exclusionary criteria of irresponsible stocks or simply the period that has been analysed.

Still according to Francisco Climent and Pilar Soriano (2011), it seems that if the adjusted returns of green funds are lower than their conventional peers, it is rather due to a higher risk than a lower return. Indeed, environmental funds holders invest in a discriminatory way, limiting their stocks to only eco-friendly ones thus decreasing their diversity. Other results further discussed in section 5.6 will partially contradict this statement. Additionally, socially responsible investment funds must monitor each of their stock in order to meet the requirements of their standards. Hence, they tend to invest in fewer stocks than their conventional peers, as each stock causes additional work. This inferior diversity is the main cause of the superior risk according to this study. It creates a

paradox between two perspectives: the firm and the investor. Being more responsible will normally lead the firm to decrease its inherent risk, by reducing the probabilities of negative events as explained in section 1.2. On the other hand, we see that an investor, although investing in these underlying firms, may experience the opposite effect due to the nature of mutual investment funds. These different perspectives depend on what one is really focusing on: a business or an investment strategy.

The disparity between the first period (1987 – 2001) and the second (2001 – 2009) is thus mainly due to the number of green stocks available on the market and the firm’s financial evolution. The criteria of compliance with the concept of social responsibility also changed over time, which may be another reason for this difference.

This study deeply compares the performance of socially responsible investments against conventional ones in the United-States, and also more precisely against only green funds, which mostly behaved likewise. Nonetheless, the lack of analysis of the demand side (i.e. the investors) could be confusing. Indeed, the paper showed the variation between two periods of time and with it the evolution of responsible stocks. But if the amount of green and responsible stocks has increased over the last two decades, the demand has also considerably risen. This has certainly impacted the value of SRI stocks and must be taken into account. The demand side shall be investigated as well in order to enlighten this shadow zone.

5.2 Market demand

In the study entitled “

The stocks at stake: Return and risk in socially responsible

investment

” conducted by Rients Galema, Auke Plantinga, and Bert Scholtens, the effects of the demand side are deeply explored (Galema, Plantinga, Scholtens 2008). They hypothesize that the value of socially responsible investment funds has been altered by a robust increase in demand over the last two decades. This paper displays how the rise in demand for responsible stocks inflates the value of these underlying companies without real financial funding to support such an increase in price. This will lead responsible stocks to be overpriced compared to their book value. On the other hand, a shortage of demand regarding non-responsible stocks occurs, leading them to be under-evaluated regarding their book value.Their results are consistent with their theoretical hypothesis regarding the overpricing effect. This is demonstrated in particular with the book-to-market ratios they computed. This ratio compares the book value of a listed company with its market capitalization, i.e. the market price of its shares. A low book-to-market ratio implies that the market

overvalues the company. They overall found that socially responsible stocks have a lower book-to-market ratio than their conventional peers. In order to investigate why, the study deepens its analysis by segmenting different social responsibilities attributes in different categories. They found that variations amongst different attributes can be significant (see section 5.6).

5.3 Opposing forces

Portfolios cannot be considered as one single stock. That may be one of the main reasons why so few shreds of evidence of social responsibilities enabling a better performance are found in the literature (Galema, Plantinga, Scholtens 2008). Opposite forces interact within a portfolio. Hence, a positive event for an ecological-friendly stock might impact negatively a good corporate governance stock (Scholtens, Zhou 2008), whereas fewer forces interact within a single entity. Rients Galema, Auke Plantinga, and Bert Scholtens have integrated this notion in their analyses and computed the “

strengths

” and “concerns

” of each category of portfolio. They found that only the Community portfolio had a positive score (strengths minus concerns). The portfolios that have the lowest book-to-market ratios are the ones composed of green stocks. As environmental issues have become an urgent and global matter now more than ever, it is understandable that the demand of ecological-friendly investments has seen a steeper increase than for other responsible funds. We can also assume that green funds managers struggle more to diversify their investments than other SRI funds managers. Less diversity in a fund will increase risk, hence destroys value of risk-adjusted prices and lower the book-to-market ratio. Conclusively, all this demonstrates why one should not gather all socially responsible attributes together while assessing their performances. This could be one of the main reasons why the theoretical idea that a socially responsible firm will be more sustainable than a conventional one struggles to find empirical evidence. Indeed, a certain number of social objectives might not be in line with financial ones, while some others will, and some could have either a positive or a negative impact. For instance, having poor pension plans for one’s own employees might prevent a company from being socially responsible but will result in lesser financial obligations, impacting positively expected cashflows. On the other hand, Thomas J. Carroll and Greg Niehaus demonstrated that firms increasing their unfunded pension liabilities (implying a riskier pension plan for its employees) will see their debt rating worsening (Carroll, Niehaus 1998). A worse debt rating will lead lenders to request higher interests which will increase the weighted average cost of capital of the firm, thus decreasing cashflows.For these reasons mentioned above, it appears that the sustainability of firms is neither guaranteed nor enhanced only by being socially responsible. Moreover, SRI criteria are to be assessed individually in order to have a clear understanding of how the responsibility of a firm impacts expected returns.

5.4 Firms’ financial incentives

Josef Zechner, Robert Heinkel, and Alan Kraus have built an interesting model which puts in relation the proportion of polluting and non-polluting firms with the proportion of green and conventional investors in their study entitled “

The Effect of Green Investment

on Corporate Behavior

” (Heinkel, Kraus, Zechner 2001). This paper investigates the effect of the strategy conducted by green investors and how it will drive firms’ behaviour, and also the financial rationales behind the conduct of firms toward environmental responsibilities. This article also shows that green stocks trigger a superior risk than others as fewer investors are holding them (prior 2001), leading to having more units of risk per capita (consistent with what previously mentioned in section 5.1). Nevertheless, they still emphasize in their model that the exclusionary investing strategy of green investors will cause polluting firms to attract fewer stockholders, as some of them boycott such firms. The study aims to discover how many green investors the market needs to incentivize polluting firms to change their behaviour. They first start to illustrate their model with the simple assumption than the market is equally composed of green and conventional investors as well as polluting and non-polluting firms. In that case, half of the investors would completely exclude 50% of stocks, whereas normal investors could invest in 100% of stocks.As polluting businesses see the number of their main suppliers of capital decreasing and the risk per capita of investors increasing (less risk sharing amongst stockholders), their weighted average cost of capital will tend to raise. When managers and boards of directors see their financing costs grow, we can assume that a reaction will be triggered. That could lead to a restructuration of the company, a re-positioning of their value on the market, or depending on the health of the economy (i.e. interest rate) and the capital structure of a firm (i.e. its debt ratio), even an adjustment of the financing strategy. The important property we need to bear in mind while investigating aggregate behaviours in the economy is the importance of financial perspective against emotional ones. We assume that businesses are more rational financially speaking than human beings, as shareholders predominantly seek profit. That would explain why firms are not socially responsible if no financial incentives exist. Here, J. Zechner, R. Heinkel, and A. Kraus

state that polluting firms will change their behaviour if the increased weighted average cost of capital becomes more expensive than the costs of restructuring themselves in order to be socially responsible (Heinkel, Kraus, Zechner 2001).

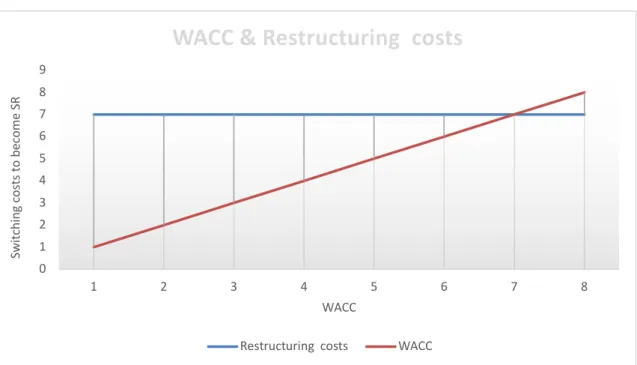

We can illustrate this by a two-dimensions graph:

Figure 1 WACC & restructuring costs

Here we assume that the switching costs to become environmental-friendly (or socially responsible) are fixed and do not vary throughout the time (i.e. neither new recycling technology to facilitate the resettlement nor new patents to pay in order to acquire such technology). Another perspective would be to see it as a caption of today’s situation without any time perception. The differences between the orange and the blue curves, represented by dark thin vertical lines, are the gains or losses of switching or not switching behaviour. As long as the increased WACC remains below the switching costs, the company does not have financial incentives to become ecological-friendly. As soon as the two lines intercept and above, the firm will have financial reasons to reform its current state and to become socially responsible.

We can easily identify two difficulties that will be encountered in the construction of this model. Firstly, the computation of the restructuring costs can drastically differ from what has been initially assumed. One reason is that the foundations of this assumption are wobbly and highly uncertain. One can only estimate such costs based on projections that do not have any historical data most of the time, unless the company has already faced a major and comparable restructuration and that it occurred in a similar context.

0 1 2 3 4 5 6 7 8 9 1 2 3 4 5 6 7 8 Sw itch in g co st s t o be co m e SR WACC

WACC & Restructuring costs

Moreover, once computed, the costs may considerably fluctuate depending on the strategy used (how deep we restructure the firm), on the technological assets or means of the company, and much more.

The second difficulty is to determine the increase in the weighted average cost of capital. The effect that the number of shareholders has on the WACC is, although not ambiguous, impossible to assess with certainty. The only manner to accurately draw it as we did just above would be to actually do the restructuration and to collect data. These two flaws weaken noticeably the model in my opinion. It provides us with a useful theoretical tool to reflect on but does not allow any empiric and concrete data to be analysed.

Nevertheless, J. Zechner, R. Heinkel, and A. Kraus concluded that the proportion of green investors must represent approximately 25% of the total population of American investors in order to financially incentivize polluting firms to reform their technology. They also discovered that currently, only 10% of investment flows in the United States can be identified as being socially responsible (Heinkel, Kraus, Zechner 2001). In their model, this proportion of exclusionary investors increases the aggregate weighted average cost of capital but is not sufficient to incite polluting firms to reform.

5.5 Effect of risk management

Mark Sharfman and Chitru Fernando bring a more micro-economical view in their paper published in the Strategic Management Journal called “

Environmental Risk Management

and the Cost of Capital

”. They address the relationship between the environmental risk management level of a firm and its cost of capital (Sharfman, Fernando 2008). The main objective of their research was to empirically test whether a company monitoring its environmental risk better will see its cost of capital decreases. It could have been problematic for us if they analysed small and medium companies as many parameters could be different. The capital structure of smaller firms or the manner they access to new capitals are often different than public firms and it could alter our results. Nonetheless, their paper is highly relevant in the context of our study as they use a sample of the S&P500.Their methodology is to gather economical knowledge from the existing literature and to establish some hypotheses to test within their sample. A firm investing in an environmental risk management strategy becomes less risky, facing weaker probabilities of cash outflows due to litigations, prosecutions, or restructuration costs due to newly imposed measures. The question that subsists is whether the market rewards the firm