Does ownership matter? : Asia and the global operations of multinational corporations

67

0

0

Texte intégral

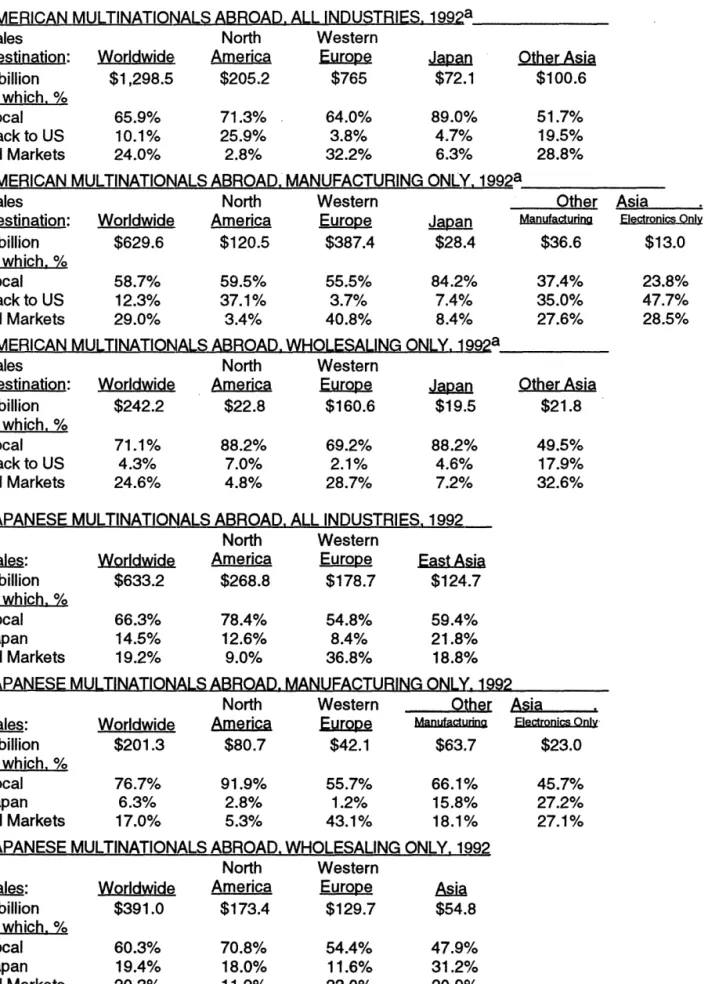

Figure

Documents relatifs