HB31

.M415[DEWEY

working

paper

department

of

economics

CHOOSING

THE

NUMBER

OF

INSTRUMENTS

massachusetts

institute

of

technology

50 memorial

drive

WORKING

PAPER

DEPARTMENT

OF

ECONOMICS

CHOOSING

THE

NUMBER

OF

INSTRUMENTS

StephenG.Donald Whitney K.

Newey

No. 99-05 February, 1999MASSACHUSEHS

INSTITUTE

OF

TECHNOLOGY

50

MEMORIAL

DRIVE

CAMBRIDGE.

MASS.

02142

Digitized

by

the

Internet

Archive

in

2011

with

funding

from

1

Introduction

There

hasbeen

a resurgence of interest in the applicationand

properties ofinstrumentalvariables (IV) estimators.

An

important

problem

inIV

estimationis choosing thenumber

of

vahd

instruments, ormore

generally a subset of all the instrumentsknown

tobe

valid.The

properties ofestimators are sensitive to this choice (e.g. seeMorimune,

1983), evenin applied

work

withmany

observations (e.g. seeBound,

Jaegerand

Baker, 1996).We

address this

problem by

providing simpleapproximate mean-square

error(MSE)

criteria,that

can be minimized

to choose the instruments.We

give these criteria for two-stageleast squares (2SLS), limited information

maximum

likelihood(LIML),

and

the JacknifeIV

(JIVE)

estimator of Angrist, Imbens,and

Kreuger

(1995).We

alsocompare

theapproximate

MSE

of these estimators,and

findLIML

is best.Our

criteria isbased on

higher-order asymptotic theory,Hke

that ofNagar

(1959),Anderson

and

Sawa

(1979),Morimune

(1983),and

Rothenberg

(1983).Our

approximate

MSE

criteria are like those ofNagar

(1959), beingbased

on

theMSE

of leadingterms

inan expansion

oftheestimator.Thisapproach

is wellknown

to givethesame

answer

as theMSE

of leadingterms

inan

Edgeworth

expansion,under

suitable regularity conditions(e.g.

Rothenberg,

1984),and

hasbeen used

innonparametric

and

semiparametricmodels

by

Andrews

(1991a), Linton (1995),and

Powelland

Stoker (1996). Fork-class estimators our calculationsextend

those ofNagar

(1959)and Rothenberg

(1983) to the misspecifiedfirst-stage case.

We

also providenew

results for the jacknifeIV

estimator(JIVE)

of Angrist,Imbens

and

Krueger

(1995).A

number

of recent studieshave

considered the properties ofIV

estimatorswhen

instruments areonly

weakly

correlated with theendogenous

righthand

side variables. In particularNelson

and

Startz (1990),Maddala and

Jeong

(1992),Bekker

(1994),Bound,

Jaeger

and

Baker

(1996),and

Staigerand

Stock (1997)have

shown

thatstandard

IV

estimators, including the

2SLS

estimator, tend tobe

biasedtowards

the inconsistentOLS

estimatorand

that inferencesbased

on

2SLS

canbe

quite misleading,when

themat-ter, choosing the instruments

may

helpimprove

the approximation, particularlywhen

the source of

weak

correlation is extraneous instruments that shouldbe

excluded. For example,we show

that in data like that ofAngristand Krueger

(1991) our criteria willchoose the smallest

number

of instruments,where

there is less evidence of aproblem

ofweak

correlation.Our

criteria for choosinga subset of valid instrumentsis the estimatedMSE

ofleadingterms

inan

expansion. Thisapproach

is differentthan

Andrews

(1996),who

basesinstru-ment

choiceon

theGMM

criterion function.We

are choosing instrumentsfrom

a subset that isknown

to be valid while he is searching for the largest set of valid instruments.Our

approach seems

ideally suited tomany

applications inmicroeconomic

data,where

there is a large set ofinstruments all thought to

be

valid.Examples

include the draftlot-tery

number

asan

instrument for military service, as in Angrist (1990),and

interactions of covariates with instruments, as in Angristand Krueger

(1991).Our

results also applyto the choice of nonlinear functions to use in the efficient semiparametric instrumental

variables estimator of

Newey

(1990).Here

we

derive the optimal,MSE

minimizing

num-ber of instruments to use, answering the important question of

how

to pick thenumber

of instruments in optimal semiparametric estimation.

The

number

of instruments canbe thought

of as asmoothing parameter

for thenonparametric

component,

as hasbeen

consideredby

Linton (1995)and

Powelland

Stoker (1996) for other models.In Section 2

we

describe theIV

estimatorswe

consider, present the criteria forin-strument

choice,and compare

these criteria for different estimators, seekingtheone

withsmallest higher order

MSE.

In section 3we

derive theapproximate

MSE

forLIML,

2SLS

and

JIVE when

there areno

covariates. Section 4 studies the properties of the criteriatheoretically

and shows

that they canbe

implemented

in away

that is optimal in a certain sense. Section 5 allows for covariates in the theoretical results. In section 6we

present a

Monte-Carlo

experiment. Section 7 presents the results ofapplyingthe criteria in the Angristand

Krueger

(1991) appUcation.2

The

Model,

Estimators,

and

Instrument

Selection

Criteria

The

model

thatwe

consider is,Vi

=

1^1+

2:^/3+

ei, E\ei\x^=

0,V"ar(ei|xi)=

o\, Yi=

f{x^)+

Ui,E[ui\xi]=

0,Var{ui\xi)=al,

for i

=

1, ...,N,where

yi,and

Yi are scalars, x, is a dx

1 vector ofexogenous

variables,and

Xii is a diX

1 vector ofexogenous

variableswhich

areassumed

tobe

a subset ofXi,

where

we

assume

homoskedasticity throughout.We

alsoassume

that conditionalthird

moments

are zerothroughout

the paper.The

first equation is the equation ofinterest

and

the righthand

side variable Yi is possibly correlated with e, so thatgenerally E{uiei\xi)=

aue 7^ 0,The

second equation represents thereduced

form

relationshipbetween

Yiand

theexogenous

variables Xiwhich

is allowed tobe

nonparametric, withf{xi)

=

E{Yi\x,).Because

oftheconditionalmoment

restriction E{ei\xi)—

0, functions ofXjcan be used

as instrumentsinestimating the equationofinterest. Letipf

=

(ipiKi^i),,4'KK{^i))' be

a vectorofK

functions tobe

used asinstrumental variables,where

we assume

throughout

that xpf" includes Xu.They

couldbe

approximating

functions, such aspower

seriesor regression splines, as in

Newey

(1990).The

problem

we

consider ishow

to choosethis instrument vector so that the associated

IV

estimatorshave

good

properties. Forsimplicity

we

have

allowedK

to serve asboth

thenumber

of instrumentsand

the indexof the instruments, but

we

could proceedmore

generallyby

specifying a different indexfor the instruments. If

we

did that the criteria couldbe

used tocompare

instrumentalvariables estimators with the

same

number

of instruments.We

consider several differentIV

estimators.To

describethem

let^^ =

[ip^,...,ip^]'

be

thematrix

ofobservationson

the instrumentalvariables,P^

=

^'^(^^'^'^)~i^-'^' theassociated projection matrix, y

=

(yi, ...,yn)',Y

=

(Yi, ...,y„)',Xi

=

[xn, ...,Xin]',W

=

overA,

where

Pi=

Xi(XjXi)

^X[.The main

class ofestimators considered is the k-classwhich

includes estimatorswhich have

the form,6={{1

+ k)W'P^W

- kW'W)-\{1

+

K)W'P^y -

nWy)

where

the scalark

is given by,ad

+

j^

K

=

l-a9-j^

for constants a

and

b. This class of estimators includes2SLS,

where

a=

b=

0,LIML,

where

a=

1and

6=

0,and

a bias-corrected2SLS

estimator like that ofNagar

(1959),denoted

hereby

B2SLS,

where

a=

and

b=

K

—

(2+

di). This class of estimators issimilar to that considered

by

Rothenberg

(1983).The

other estimator considered is the JackknifeIV

estimator(JIVE)

proposed

by

Angrist,

Imbens

and Krueger

(1995). It has the form,(

IJ\

_

{

y'C'Y

Y'C'X,

\~

Y

Y'C'y \

[Pj

)-[

X[Y

X[X,

)

[X[y

)

where

C

is the matrix with Cij=

Pij/{1—

Pa) for i 7^ jand

Cu

=

0.Note

thatCY

has the interpretation as the vector of predictions of the Yi given all but the ith observation,hence

the Jackknife terminology.The

instrument selection criteria arebased

on

theapproximate

mean

square error(MSE)

for theendogenous

variable coefficient estimator 7.Implementing

these criteriarequires preliminary estimates of

some

of the parameters ofthemodel

and

agoodness

offit criteria for estimation ofthe reduced

form

using the instruments ipf. Let 6 denote apreliminary

IV

estimatorand

let e=

y—

W6.

Also, letu

denotesome

preliminaryreduced

form

residual estimator, such as that obtainedfrom

the residualsfrom

the regression ofy

on

^^

forsome

fixedK.

Then

leto-,^

=

e'e/N,al=

u'u/N,

Uu^=

u'e/N.It is

important

inwhat

follows thatnone

ofthese preliminary estimatorsdepend

on

K.

For

example

Smight be an

IV

estimator with just one instrument for Yi, or itmight be

offit criteria given below. Similarly, the

reduced

form

residualu

might be from

the firststage regression

with

the best fit. Inany

case these estimatesmust

remain

fixed as thecriteria for different instruments sets is calculated.

The

reduced form goodness

offit criteria canbe

formed

in at leasttwo

ways. Letu^

denote

thereduced form

residual vectorfrom

regressingY

on'^^

.The

Mallows goodness

of fit criterion for the

reduced form

isR{K)

=

{u^'u^/N){l

+

~^)

The

cross-validationgoodness

of fitmeasure

is^f)

2Eitherofthese will

have

suitabletheoretical properties forusein theinstrument selectioncriteria.

The

preliminary estimatesofcovarianceparameters

can be

combined

with

thereduced

form goodness

of fitmeasures

toform

criteria for the choice of instruments foreach

of2SLS,

LIML,

and

JIVE

asS2SLs{K)

=

al^

+

aUR{K)

- al^)

suml{k)

=

^![m)~^^)

For each estimator, choosing

K

tominimize

the correspondingS{K)

will result in7

that has relatively smallMSE

asymptotically.These

criteria also will applywhen

K

is notthe sole index of the instruments, e.g. for

comparing two

different sets of instruments thathave

thesame

number

ofinstruments.Choosing

the estimatorwhere

the expressionon

the right-hand side is smallest will result in the bestasymptotic

MSE

in that case as well.It is interesting to

compare

the size of the criteria for different estimators,because

LIML

and

JIVE

criteria areboth

of smaller orderthan

the2SLS

criteria. This reflectsthat the bias of

2SLS

increases with thenumber

ofinstruments at a higher ratethan

theother estimators, a result previously established

by

Morimune

(1983). Consequently, forlarge

numbers

of instrumentsboth

LIML

and

JIVE

shoulddominate

2SLS

interms

ofMSE.

Also, the criteria forLIML

is smallerthan

that forJIVE,

so thatLIML

is bestamong

these three estimators.As

previouslyshown

by Rothenberg

(1983) for the fixedinstrument case, it turns out that

LIML

is bestmedian

unbiasedto the orderwe

considerin the k-class of estimators.

3

The

Mean

Square

Error

For

much

of this sectionwe

focuson

the simplestmodel

which

is a special case of themodel

considered in Section 2. In particularwe

focuson

the model:Vi

=

lYi+

Ci Yi=

f{x,)+

Uiforz

=

I, ...,N,where

yi,Y^and

e, are all scalarsand where

Yi is possibly correlated withCj. In Section 3.5

below

we

show

how

theMSE

criteriacan

be extended

tomodels

withcovariates as considered in Section 2. In this case, the estimator for

7

is given by,7

=

((1+

K,)Y'PY

-

kY'Y)-\{1

+

K)Y'Py

-

KY'y)where,

l-a9-j^

N

with

6 being theminimum

value of, X'Y'PY

X/

X'Y'Y

\.The

other specific estimator considered isJIVE, which

isdenoted

by,7j

=

(Y'C'Yy^Y'C'y

where

C

was

described in Section 2. UnfortunatelyJIVE

does notappear

to fit into the k-class of estimators so thatMSE

calculations willhave

tobe

performed

separately.3.1

Calculation

Our

approach

to finding theapproximate

MSE

is similar to that ofNagar

(1959). Firstwe

normahze

the estimator (let7

denote a generic estimator),ViV(7-7)

=H-^h

where

H

and

h

are different for different estimatorsand

have

population counterparts,h

=

i/'e

and

Then we

use the expansion.„_f'f

H-'h

=

[{I-{H-H)H-^)H]-\h +

Ch-h))

=

H-\h

+{H

- H)H-^h

+{H-

H)H-\h

-

h)+

{H

-

HfR-'^h

+

...and

note that sinceH"^

is acommon

factor for allterms

in the expansion, Avecan

calculate

an approximate

MSE

by

taking expectations of the square of the expression,Hy/N{^-^)

=

h

+

{H-H)H^^h

+{H

-

H)H-\h

-h)

+

{H-

HfH-'^h

+

...Then

followingNagar

(1959)we

find theMSE

of this expression using the largest (inprobability)

terms

inthe squareofthisexpression, althoughsincewe

are interestedin theselection of

K

and

allowK

—

>• 00we

include only thoseleadingterms

in theMSE

that arepertinent tothe choice of

K

for the estimator of interest.Thus

terms

thatdo

notdepend

on

K

willbe

omitted.Because

of this fact,terms

beyond

thesecond

willnot (ingeneral)contribute to the

approximate

MSE

criteria tobe used

for selection ofK

, eventhough

they

do

contribute to theMSE

in the casewhere

one has a fixedK

and

one

obtainsan

approximation

to theMSE

to0{\/N).

For the purposes of completenessand

to enable other types ofcomparisons

we

also provideapproximate

0{1/N)

MSE

calculations forfixed

K. These

calculations extend thework

ofNagar

(1959)and

Rothenberg

(1983) tothe case

where

there is a possible misspecification in the first stage. In such a calculationthe third

and

fourth termsdo

contribute to theapproximate

(to0{\/N)) MSE.^

Note

that the leadingterm

(which is 0(1)) in theapproximate

MSE

willbe

E{hh!)

=

a'J-^

and

that this willbe

common

to all of ourapproximate

MSB's.

Since thisterm

hasno

bearingon

the choice ofK

and

since it iscommon

to all of our estimatorswe

omit

theterm from

the expressionswe

presentand

focuson

theremaining

terms. All calculations aredone

conditionalon

theexogenous

variables Xi,The

assumptions which

are used to derivean approximate

MSE

arenow

statedand

discussed.

Assumption

1Assume

that {xi,Ui,ei] are iid,and

satisfy,(i) E{u^\xi)

=

E{ei\x^)=

0,(ii)

<

E{uf\xi)=

al<

ooand

<

E{ej\xi)=

a^<

oo,(in) E{ui'ei^\xi)

=

0, forj+

k being a positiveodd

integer such that k+

j<

5,(iv) E{\ui\^\ei\^\xi)

<

oo, forany

positive integers jand

k such that k+

j<

5,(v) Xi have support

X

C

R^

that is the Cartesian product ofcompact

intervals.Assumption

l(i)was noted

in Section 2.Assumption

l(ii) is a homoskedasticityassump-tion that simplifies the calculations while

Assumption

l(iii) is asymmetry

assumption

which

implies thatboth

residualshave

symmetric

distributions. This willbe

satisfied iftheresiduals arejointly

normally

distributed.Assumption

l(iv) requires the existence ofat least five

moments

for the residuals.Assumption

l(v) is standard in the literatureon

series

based

nonparametric

regression.The

nextAssumption

concerns the nature of theoptimal instrument function /.

Assumption

2The

function f{xi)=

E{Yi\xi) is such that,(i)

f

:X

-^R

and

hasan

extension to all ofR^

that is s>

times continuouslydifferentiable in x,

(a) with probability 1,

<

c<

N~^

'^^^-^ f{xi)'^<

c~^ forsome

small constant cuniformly in

N

.

Assiimption 2(i) is a

smoothness

condition that allows one to obtainapproximation

rates for series

based

methods.

The

second part of thisassumption

isan

identificationassumption

that requires that /(xj) notbe

identicallyzerowhich

would

result in7

beingunidentified. This will

be

modifiedwhen we

consider the introduction of covariates intothe structural equation.

Assumption

3: LettingPa

denote the ith diagonal element ofP,

assume

thatsup

Pu

-^i<7V

as

N

^>- 00 withprobability one.It should

be

stressed that thisassumption

is not required forone

toshow

thatyN{'y

—

'y) is asymptotically normal,and

is only necessary to obtain tractable expressions for theMSE.

It requiressome

restrictionson

the rate atwhich

K

increaseswith

thesample

sizethat are

much

strongerthan

thoseneeded

toshow

asymptotic normalityoftheestimators.It should

be noted

however

that as long as s inAssumption

3 is sufficiently large therestrictions will allow for

K

to increase at a rate that results in the fastest possible rate ofconvergence oftheMSE

expression to zero.^Our

first result givesan approximation

to theMSE

for a subclass of the k-classestimators

we

are considering. In obtaining all ofourapproximations

we

have

restricted attention to k-class estimators thathave

values of aand

b that satisfy certain properties. In particular it isassumed

that a=

0(1)

while b=

0{K),

which

includes all of the Donald(1997) hasshownthatforpowerseriesonerequiresthatK^/N

—

>when

Xi hasa continuousestimators

mentioned above and

ensures that the estimators willbe

consistent.'^The

first subclass of estimators consists of those for

which

theapproximate

bias (to orderN~^^'^) is increasing in

K.

Unless otherwise stated allMSE

will refer to theterms

in the largesample

largeK

MSE

that aredominant

amongst

those that increasewith

K

and

those that decrease with

K.

Proposition

1Given Assumptions

1-3,assuming

that a—

0(1)

and

b=

0{K)

suchthat {l

—

a)— b/K

isbounded

away

from

0, theMSE

for\/N{'y—^)

is approximately[{l-a)K~bf

,,f'{I-P)f

crL-

U€h

+

(y.N

'N

It is straightforward to

show

that theapproximate

bias, to0{N

^/^) is of the form^[(l_a)/<-6-(2-a)]a„,

ff'fY'

/TV

\N

•^^-^

and

that for estimators in the classunder

considerationwhose

biasterm grows with

K

,

the leading

term

in theMSE

comes

directlyfrom

the squareof this bias.The

secondterm

in our

approximate

MSE

comes from

theapproximation

error inherent in the estimationof

/ by

a seriesbased

approximation.The

result in Proposition 1 leads directly toan

approximate

MSE

for2SLS

which

is the only estimatorunder

considerationwhich

fallsinto this class.

Corollary

1For 2SLS,

72, which has a=

and

6=

0, the approximateMSE

of^(72 —

7),under Assumptions

1-3, is given by,,

K^

J'{I-P)f

ut

N

'

N

Notethat,aswillbeseen,theseconditionsontheirowndonot ensureroot-Nconsistency. Ingeneral this will require restrictionson therate of increase ofK.

''See Rothenberg (1983) forexample. Also note that the expression forthebias isthesame asNagar

The

result in Proposition 1 does not reveal the largeK

approximate

MSE

for eitherLIML

orB2SLS

because neither of these estimatorshave

a bias (to 0{N^^^'^)) thatdepends on

K. Thus

we

need

to providean

additional result that will yieldapproximate

MSE's

for such estimators.Proposition

2

Given Assumptions

1-3,assuming

that a=

0(1)

and

b=

0{K)

suchthat (1

—

a)K —

b=

0(1), theMSE

for •\/iV(7—

7) is approximately{K -

2aK

-

2ab)K

J'{I

-

P)f

"^

N

"^"^

A^ '

N

This

resultcan

be used

to obtainapproximate

MSE's

forLIML

and B2SLS.

Corollary

2For

LIML,

'Jl,'whichhas a=

1and

b=

0, theapproximate

MSE

Jory/N{'^L—

7)

under

Assumptions

1-3, is given by,K^.

-0^+^.

—

-^

—

Corollary

3

For

B2SLS,

'^b,"which has a=

and

b=

K

—

2, theapproximate

MSE

for\fN{ffs

~

7)under

Assumption

1-3, is given by,/ 2 2

2^K

J'{I-P)f

The

expressions derived thus fardo

not allowone

to derive a criteria forJIVE.

Interestingly, the following resultshows

thatJIVE

has thesame

MSE

expression asB2SLS.

Proposition

3

For JIVE,

7j, the approximateMSE

fory/N{'yj—

7) is given by3.2

Discussion

Some

insight into the differencesbetween

theapproximate

MSE

for the estimators canbe

gainedby

looking at theterms

in theexpansionofeach that contributes to the leadingterms

in theMSE

expressions. For2SLS

thisterm

has the form,'Pe 1

/

^

ATw

\where

thefirstterm on

the rightreflectspartofthebiasthat occursdue

totheendogeneityin the

model

(i.e. correlation of Uiand

e,)and

which grows

with K.^The

square of thisbias

term

gives the leadingterm

in theMSE

for2SLS.

The

variance of thecomplete

expression contributes0{K/N)

terms to theMSE,

and

these aredominated by

theleading bias squared term.

Both

LIML

and

B2SLS

have the leading biasterm

(whichdepends

on

K)

removed

and

so the leadingterms

in theirMSE

come

from

the varianceterms.

An

alternative derivation ofLIML

shows

how

this bias reduction occurs. In particular theLIML

estimator 7/, canbe

shown

tobe

the solution to the followingproblem,

mm

^^

where

Y

=

{y,Y),and

7;^=

(1,-7).Given

this, it is straightforward toshow

that theLIML

estimator satisfies the following first order condition,where

e{f)i)=

U~ IlY

Letting,y'<iL)

KlL)

=

we

can rewrite the first order condition as,1

(F-<5(7je(7L))'Pe(7L)

=

0. (3)Since 6 can

be

interpreted as being the coefficient in thehnear

regression ofy

on

e thefirst

term

in theabove

canbe viewed

as being the residualfrom

this regression,which

should then not

be

linearly related to e.Thus

theterm

forLIML

that corresponds to (2)has the form,

1 v'Pe

=

-. /N

N

N

\-=

IY^

v^SiPu+

J2Y1

""^^^-^v 1 (4)/N

where, O-ue Vi=

Ui -Ciis

by

construction rmcorrelated with Cj.Note

also that the leadingterm

in theMSE

expression forLIML

is equivalent to, cr^cr^.The

term

forB2SLS

corresponding to (2)and

(4) is equal to,(3)

Vn

^ f

N

N

N

\where

the leadingterm

has,by

construction, zero expectation. This, again, results in a lower order leadingterm

in theMSE

forB2SLS.

The

lower leadingterm

forLIML

compared

tothat ofB2SLS

comes about because

ofthe lower variance that arisesbecause

Vi is rmcorrelated

with

ejand

because Vi has a lower variancethan

tij. Finally, it is easyto see

why

JIVE

has thesame

leadingterm

asB2SLS,

sinceforJIVE

the expression thatis analogous to (2), (4)

and

(5) has the form,in

1 /^

^

2^2^zx,e,Q,

(6)v^

v^

V.=l ,^.which

has zero expectation. This expression resultsbecause

of the use of the Jackknifein the first stage.

3.3

Further

Comparisons

Our

discussionthus farhasindicated that,in termsofdominant terms

intheapproximate

(large

K) MSE,

LIML

dominates

JIVE

and

B2SLS

and

that all of these estimatorsdominate

2SLS

because of the larger order (inK)

leadingterm

of the latter.Another

type of

comparison

that canbe

made

is in terms of theMSE

for a fixed value ofK

for which, generally speaking, the chosen instrument set

may

be

suboptimal.The

nice feature ofthis comparison, is thatifthe expansion is takenup

toterms

oforderN~^

thenone

can see clearly theopposing

effects ofincreasingK

more

clearly. In addition suchan

expansion extends thework

ofNagar

(1959)and Rothenberg

(1983) to the misspecifiedfirst stage case

and

may

revealany

potential differencesbetween

estimatorswhen

one

uses

an

imperfect fixed set of fixed instruments in the first stage. ^Proposition

4:Given Assumptions

1, 2(i), 3,assuming

that a,band

K

are fixedand

that (forsome

small constant c),f'-Pf 1

0<c<

^-—^ <c-^

N

with probability 1, uniformly in N, then the

MSE

forviV(7

—

7) usingterms

upto those of

0{N~^)

is approximately2lf'PfY\

2[{l-a)K-b]'

ff'Pf^-'

N

J ""'N

\N

^ 2 ,{{K-2aK-2ab)-8[{l-a)K-b]}

\ /fPp

"' "^ IN

J \

N

, , .{K-2[{l-a)K-b]}

\ff'Pf

„

,'12-

Aa-a^\

ff'PfY^

, ,/4

-

2a\

ff'Pf

-2+2a

,,a{K-l)

+ b\f'{I-P)f

ff'Pf

N

N

\N

The

conditions used to derive the expression in Proposition 4 are thesame

asused

previously except thatwe

have

introduced a condition that modifiesAssumption

2(ii) to^Indeed our result reduces to that of Nagar (1959) in theperfect first stagecase when o

=

as heassumed. The expression obtained in Proposition 4 does differ from the

MSE

expression one obtainsfromTheorem 2 ofRothenberg (1983). Additionally, inthe a

=

case, the expression oneobtains from Rothenberg (1983) is not consistent with that obtained by Nagar (1959). The difference between that obtained from Rothenberg (1983) and Nagar (1959) andours is minorand appears appearto bedue totypographical error in thestatement ofTheorem 2 ofRothenberg (1983). Indeed asingle sign change

ensure identification in the fixed

K

case.Note

that the leadingterm

in this expression,when

taken to the Hmit, is the asymptotic variance of the estimator,when

K

is fixed.When

K

is fixedand

when

the instruments are imperfect (in the sense that theycannot

predict

/

perfectly) then it is the case that,since /'(/

—

P)f

>

which

follows because /—

P

is positive semidefinite. In factif the instruments are imperfect (in the sense that they

cannot

predict/

perfectly)then

it is the case that the inequality is strict.Note

that the expressionon

the rightof the inequality is the lowest variance possible for this particular problem.

Given

the expressionin Proposition4,one

can then see clearly that increasingK

willhave opposing

effects. First, increasing

K

will cause the limiting variance tobe

closer to the optimalapproximate

variance for the estimator.That

is,because

when

K

-^ oo thenby

Assumption

2, f'{I—

P)f/N

-^ 0.On

the otherhand

theother

terms

will generally increase.Our

expressions derived earlier, involve the largestterms

reflecting each of these effects.The

optimal choice ofK

, then, willbe

theone

that balances these

two opposing

effects.The

expression in Proposition 4 can alsobe used

tocompare

the different estimatorsin the class

under

consideration. In particular theapproximate

MSE

for2SLS

is,^^

1,^

+

r-

[

—

N

—

)

+^"^^^^/

[-^r)

for

LIML

we

have,and

finally forB2SLS

we

have,To

allowcomparisons

ofthese k-class estimators withJIVE

inthe fixedK

casewe

derivethe appropriate

MSE

expression forJIVE

below

in Proposition 5.Proposition

5:Given Assumptions

1, 2(i), 3,assuming

that a, band

K

are fixed,supjPii

=

0{N~^)

and

that,0<c<^<c-i

iV

with probability 1, uniformly in N, then the

MSE

for \/iV(7j—

7) usingterms

up

to those

ofO{N-^)

fPfV

, ..2 ,..J<

ff'P'fV"

, ,,0.2 , . . 2x 1ff'P'f

a'(^)

.«..x,f(^)-.(i..i...>n^(^)

^^^,,ni-p)p{i-p)f\

ff'P'f

-2N

\N

Note

the additional condition in the statement ofthe resultwhich

concerns the rateat

which

the largest diagonal of the matrixP

goes to zerowhich

is a strengthening ofAssumption

3and

is notneeded

forany

other result. Itis fairlyeasytoprovideconditionsthatjustify this conditionin the fixed

K

case considered in the result-

for instance giventhat

Assumption

2 holds onecan

verify this condition if the smallest eigenvalue of thematrix

"^'"^/N

isbounded away

from

zero.The

reason forimposing

this condition is to getan

estimate of,'f'PfY^

ff'C'f\

"^f'C'Cf ff'C'f\

"^N

J \N

J

N

\N

where

the complicatedform

forJIVE

comes from

the use of the Jackknife in the firststage,

and

similar to the results forLIML

and B2SLS,

introducesan

additional0{N~^),

term

in theMSE.

Such an

additionalterm

does notappear

in the expression for2SLS.

the variances

and

covariances but alsoon

the degree ofmisspecification ofthe first stage.It is interesting to notethat althoughthis misspecificationobviously affects allestimators

through

the leadingterm

(theapproximate

variance) it also affectsLIML,

B2SLS

and

JIVE

in the smaller order terms. Indeedone

could envision scenarioswhere

K

is fixedat

some

largenumber

and

where

there is still a great deal of misspecification in the firststage - in such a scenario it

may

be

possible for the finalterm

in theMSE

forLIML,

B2SLS

and

JIVE

tobe

largeand

indicatepoor

behavior of these estimators relative to2SLS.

One

can

do

more

generalcomparisons

of the estimators in the casewhere

there isa correct specification in the first stage so that

Pf

=

f

. In this case the lastterms

inthe

MSE

forLIML,

B2SLS

and

JIVE

would be

omitted.Comparing

the resultingMSE

reveals that althoughJIVE

and

B2SLS

have

similar bias reduction propertiesand

thesame

criteria for pickingK,

B2SLS

appears tobe

superiorwith

respect toterms

thatdo

notdepend

on

K

(at least using theapproximate

MSE

to0{N~^)).

A

comparison

ofthe

MSE

forLIML

and

B2SLS

reveals thatLIML

has a lowerMSE.

The

comparison

of2SLS

with

the other estimatorsdepends

on

the variancesand

covariances in the model.Not

surprisingly large (fixed) values ofK

and

reasonable levels of covariancebetween

theresiduals

would tend

to lead to superiorMSE

for the other estimators relative to2SLS.

The

expressions in Propositions 4and

5 alsomakes

it possible to considerwhat

happens

when

there isno

endogeneity problem, so that aue=

0.When

aue=

0, theoptimal

number

of instruments forJIVE

and

B2SLS,

using the criteriadeveloped

inSection 3.2, is exactly the

same

as forLIML,

which

is equal to the optimalnumber

ofterms

required forestimating/

in thefirst stage.On

the otherhand, theMSE

expressionjust given for

2SLS,

(when

a^e=

0) is monotonically decreasing inK

which

indicatesthat the optimal choice of

K

is as large as possible. This, not surprisingly,makes

2SLS

identical to

OLS, and

isdue

to the fact thatwhen

a^^=

0,OLS

is the Best LinearUnbiased

Estimator.The

reason that this does not occurwith

LIML

is that theLIML

estimator

would

no

longerbe

definedwhen

there areasmany

instruments as observations while the delete-one nature of the first stageused

inJIVE

makes

first stage predictionsbased on

asmany

instruments as observations very unreliable.Because

ofthedependence

ofcomparisons

on

the degree ofcorrelationbetween

resid-uals, it is difficult to use the expressions in Propositions 2and

4 to derivean

convenient optimal estimator in the classunder

consideration. It is possible,however

to describethe optimal estimator for classes of estimators that

have

similar bias properties.^The

first result will use the expression in Proposition 2 to give a class of estimators that are

optimal with respect to the large

sample

largeK

MSE

to orderK/N. The

classunder

consideration consists of those estimatorswhose

bias is of 0{N~^''^) (andhence have

asquared

bias of0{N^^))

which, asnoted

earlier, places restrictionson

aand

b that ruleout

2SLS

but includeLIML

and

B2SLS

as possibilities. This result is statedbelow

inLemma

1and

isan immediate consequence

of Proposition 2.Lemma

1 In the casewhere

K

^

oo in such away

that {l— a)K —

b=

0(1), the optimalestimator, with respect to the large

sample

(largeK)

MSE

to0{K/N)

must

have a=

\and

b=

0(1).Note

that this result does not pindown

a single estimator, sinceone

can pickany

constant value for band

stillhave

thesame

leadingterms

in theMSE

expansion, sinceterms

involvingK/N

willdominate

those of0{N~^)

for largeK.

It does suggest,how-ever, that

LIML,

beingone

such estimator, willhave

better (largeK)

MSE

propertiesthan

the other estimatorsunder

consideration. Note, again, that2SLS

does not fit intothe class of estimators

under

consideration because its bias is not 0{N~^''^) (again asK

—> oo) as the condition in the result requires.The

next result is for the class ofestimators that are unbiased to 0{N^^/'^)

and

follows similarlyfrom

Proposition 2.Lemma

2 Restricting attentionto estimators that are suchthat (1—

a)/C—

6—

(2—

a)=

0,the optimal estimator, with respect to the large

sample

largeK

MSE

to0{K/N)

must

have a=

1and

consequently 6=

1.''Indeed this was done by Rothenberg (1983) for theclass of(approximately) median unbiased esti-mators, in which

LIML

was optimal.This result states that the optimal estimator in the class of estimators that are

unbi-ased to 0{N~^/'^) is thebias adjusted

LIML

estimator. It shouldbe

noted, however, thatfor such

an

estimator the optimal choice ofK

is completely unaffectedby

the biasad-justment

and

that the criteria for choosingK

willbe

identical tothat obtained forLIML.

A

similar result to that inLemma

2 is obtainedwhen

oneassumes

thatK

is fixedand

considersapproximately

mean

unbiased estimators withM3E

givenby

the expression inProposition 4.

Lemma

3

Restricting attention to estimators that are such that {l— a)K—b—{2—a)

=

0,theoptimal estimator, withrespect to the large

sample

fixedK

MSE

to0{N~^)

must

have

a=

1and

consequently 6=

1.This result

shows

thatwhen

there is misspecification in the first stage (ashappens

in general

with

K

fixed) the bias adjusted LIA-IL estimator is optimalwith

respect tothe

MSE

to0{N~^).

This is aminor

extension, to the misspecified first stage case, ofthe conclusions

one

draws

from Rothenberg

(1983) concerning the optimality of the biasadjusted

LIML

estimatoramong

the classofapproximately

mean

unbiased

estimators. Inadditionto this,

Rothenberg

(1983)showed

that forfixedK

and

a correctly specified firststage

LIML

is optimal (with respect to theMSE

to0{N~^))

among

all (approximately)median

unbiased

estimators.Thus

based on both

thedominant terms

in largeK

MSE

and

peripheral or second order terms there appears tobe

ample

evidence to suggest the use ofLIML

or bias adjustedLIML.

3.4

Admitting

Covariates

In this section

we

generalize the results to the model,Vi

=

lYi+

x\iP+

ewhere

x^

is a rfjx

1 subvectorofx^.The

most

important

difference that arisesinthemore

/5i)'-However,

itcan

be

shown

that theMSE

of estimators of Pi are directlyand

positivelyrelated to the

MSE

of estimators of 7. In particular,assuming

thatXu

is included inthe instrument set (which

would be

the case if one were usingpower

series) thenany

estimator of/^jwillhave

the form,where

Xi

denotes theN

x

di matrix with zthrow

qual to Xu. ^ Since for all threeestimators the

MSE

of Pidepends

on

K

onlythrough

itsdependence on

7,we

can

focus directlyon

theMSE

of the7

in each case.When

covariates are present the estimatorsof

7

take the form,7

=

((1+

k)Y*'PY*

-

kY*'Y*)-\{1

+

K)Y*'Py

-

KY*'y)where

Y*

=

[I—

Pi)Y

with Pi being the projection matrixformed

using Xi.The

JIVE

estimator will take the form,

^j

=

{Y'C'{I-

Pi)YY'Y'C'{l

-

Pi)y.Before presenting the

MSE

calculationswe

modify

Assumption

2 as follows, letting ttdenote the population regression coefficients

from

the regression of Yion

Xu.Assumption

2'The

function f{xi)=

E{yi\xi) is such that,(i)

f

:X

^

R

and

hasan

extension to all ofW^

that is s>

times continuouslydifferentiahle in

x

and,(a) with probability 1

<

c<

N~^

X]i=i(/(^i)~

^'u^)'^

<

^~^ /'^'^some

small constantc uniformly in

N

(Hi) the smallest eigenvalue of

X'lXi/N

isbounded

away from

zero uniformly inN

with probability one.

The

adjustments

inAssumption

3' aredue

to thefactthat theidentification conditionnow

suggests that Xi explain Xjibeyond

that providedby

ahnear

regressionon

x^.^

The new

condition (iii) along withAssumption

l(v) isused

tobound

the elements ofthevector, (/

—

Pi)/

and

the variancesand

covariances ofelementsof[I—

Pi)u

and

[I—

P\)e.Indeed

these conditions ensure that the variance of a typical element of (/—

Pi)u, sayUi

—

P'liU (with Pii denotingcolumn

i of Pi), is equal to that ofw, plus aterm

that is0{N~^)

and

thatany

covariancesbetween

these elementsare ofsecond

order importance.The

same

holds true for the vector (/—

Pi)eand

for covariancesbetween

these vectors.Once

this hasbeen noted

one can obtain largeK

MSE

expressions for the estimatorsof interest that are the

same

as in the case ofno

covariates provided that the set basisfunctions

used

as instruments contain linearterms

in Xu.Corollary

4

Given

Assumptions

1,2'and

3 plusPPi

=

Pi the conclusions ofCorol-laries 1, 2

and 3 and

Proposition3

all hold.It is easy to see

why

this result holdswhen PPi

=

Pi.The

only difference thatwould

obtain

by

allowing forexogenous

covariates in the equationwould

be

that thesecond

terms

in theapproximate

MSE

would have

the form,/'(/

-

Pi)(/-

P)(/

-

Pi)//A^=

/'(/-

P)/

where

the equalitycomes from

the fact thatPPi

=

P\.A

simpleconsequence

of this result is that rules for choosingK

and

any optimahty

results discussed previouslyapply

carry over to the situationwith

covariates.4

Feasible

Optimal

Estimation

of

K

In this section

we

consider the properties of the estimatedMSE

criteria discussed inSection 2.

Throughout

this sectionwe

will use the followingassumptions

concerning the preliminary estimation of the parameters, o"^, o"^and

a^^.®This is essentially a relevance condition and Donald (1997) has considered tests for the failure of this condition in contexts wherethere are anarbitrary numberof righthand sideendogenousvariables.

Assumption

4

Assume

thefollowing,(^) ^l

-

ol,(n) al

^

al(Hi) Gut -^

O-uc-As

noted

in Section 2, this canbe

achievedby

usingsome

prehminary

set of estimatesof the

model

obtainedby

using thenumber

of instruments that provide the optimal fitin the first stage,

based

on

either the cross-validation orMallows

criteria.Note

that theother key ingredient used to

form

the estimated criteria isR{K)

which

can eitherbe

based

on

cross validation or theMallows

criteria as discussedin Section 2. Li (1987) hasshown

that each of these criteria are asymptotically optimal in the sense that the value ofK

that minimizes these criteria,denoted

K,

satisfies the condition,RJK)

, .

infx /?(/<) '

in probability.^° For a generic estimator

7

with estimated criteriaS{K)

and

true criteriaS{K) we

will define the data driven optimal choice of thenumber

ofinstruments by,K

=

argminS{K).

The

minimum

and

allinfimum

willbe

relative toan

index set ofK

values,which

may

require

some

restrictions in order to prove certain results. Also, notice that althoughR{K)

only estimatesR{K)

up

to a constant,which

does notdepend

on K, one

canremove

this constantfrom

R{K)

and hence from

S{K)

without affecting the choice ofK.

To

analyze the properties ofK

we

follow theapproach

of Li (1987)and

Andrews

(1991b). In our casewe

use the following definition of optimality.Definition:

A

method

ofselectingK

is defined to he "higher order asymptoticallyopti-mal

with respect to the criteriaS{K)

" ifit can beshown

that,s{k)

,inf;,5(/^)

^"Andrews (1991) proved the same results for appropriate adaptations ofthese criteria in the case

The

use of theterm

"higher order" is necessitatedby

the fact that the optimalMSE

convergence rate in all cases willbe

A'^"^ (asN

—

> oo)which

cannotbe improved upon,

and

the criteriabased

on

S{K)

concerns thenext largestterms

intheMSE

thatdepend

on

the choice ofK.

A

vital step inshowing

that the criteria are higher orderasymptotically-optimal, is

showing

thatR{K)

consistently estimatesR{K)

up

to the constant in the sense that, in probability,This is the condition

used

by

Li (1987) toshow

theasymptotic

optimalityoftheMallows

criteria

and

cross validation. Inordertobe

able toverify this resultwe employ

conditionssimilar to those of Li (1987).

Assumption

5:Assume

that thefollowing conditions hold,(i) E{u\\xi)

<

ooand

(a) inf^

NR{K)

-^ oo,and

in additionwhen

R{K)

is the cross validation criteria,assume

(Hi) the index set satisfies the condition that

sup^

sup^F^j -^ in probability.The

conditions (i)and

(ii) inAssumption

5 areneeded

forboth

theMallows

criteriaand

cross validation, to

show

that they satisfy (7).These were

employed by

Li (1987) toshow

that these criteria are asymptotically optimal. Here, this isan

intermediate step toshowing

higher orderasymptotic

optimality.The

second of these requires either that/

nothave

a finiteorder representationinterms

ofthebasis functions orelse that the lowerbound

on

the set ofK

values overwhich one

is doing the minimizationgrows with

A'^,which

isperhaps

undesirablefrom

a practical standpoint.The

condition (iii) is requiredonly forthe cross validation

based

method,

and

is similar to the conditioninAssumption

upper

bound

on

the rate atwhich

the index set cangrow

with thesample

size ^^The

followingresults

show

that for each estimator the estimated criteria provides ameans

toobtain higher order asymptotically optimal choices for the

number

of instruments.Proposition

6:Given Assumptions

4 o-'^d 5, then the rule "select the valueK

thatminimizes

S^{K)

" ishigherorderasymptotically optimalwith respect to the criteriaSl{K).

Proposition

7:Given Assumptions

4 o-iT^d 5, then the rule "select the valueK

thatminimizes

S2{K)

" is higherorderasymptotically optimal withrespect to the criteriaS2{K).

Proposition

8:Given Assumptions

4and

5, the rule "select thevalueK

thatminimizes

Sj{K)"

is higher order asymptotically optimal with respect to the criteriaSj{K).

5

Simulation

Study

In this section

we

report the results ofa smallMonte-Carlo experiment

which

hasbeen

designed along the lines of that used in Angrist,Imbens

and

Krueger

(1995) (hereafterAIK). Three

basic designs are used. All experiments arebased

on

the estimation of theequation,

Yr

=

Po+

PiXn

+

e, (8)where

d^o,A)

=

(0, 1)and

where

X^

isan

endogenous

explanatoryvariable.Three

cases are consideredand

are distinguishedby

differencesbetween

Xn

and

a set of potentialinstruments.

Case

1: In this caseXn

is related to either A;=

10 or /c=

20independent standard

normal

random

variables, Z^jthrough

the linear equation,k

Xii

=

7^0+

^

'n-jZij +r]i (9)^^Asnotedbelow Assumption3, basedonDonald(1997) hasshown,usingtheresults in

Newey

(1995),that forpowerseries,ifx; hasa continuousdistributionwithdensitythat isbounded andbounded away

with TTi

=

0.3and

iVj=

for j 7^ 1, so that only the first Zij is relevant for predictingXii- In this case the residuals in the

two

equations are generated as,m

J

VV

y 'V 0-20 0.25

This case is identical to

Model

2 ofAIK,

who

used

acomplete

set of/c=

20 instrumentsin their experiments.

Case

2: This is thesame

as inCase

1, except thatnow

in (9) ir^=

0.3and

ttj=

forj

^

5 so that only the fifth instrument is relevant.Again experiments

areconducted

forboth

A:=

10and

A;=

20 potential instruments (in addition to the constant).The

errors are generated in thesame

way

as inCase

1.Case

3: This is thesame

asModel

3 ofAIK

and

specifies,Xi,

=

710+

^2

'^^^^^+

0-3Y.

4

+

^^0Y^

zy\^

(10)with

TTi=

0.3and

tt^=

for j 7^ 1, so that in addition to the first regressorbeing

relevant the others enter in a nonlinear fashion. Additionally, the errors in the first

stage are heteroskedastic.

The

selection process will, however, only consider using theZij variables themselves,

and

will consider eitherup

to the first /c=

10 instruments orthe first fc

=

20 instruments.The

residuals in the pair of equations (8)and

(10) aregenerated as,

^^\

Ajff

^\

f

1-00 0-807?zo y

Vv

y

A

0-so 1-00For

each of the three cases, experiments areconducted

withsamples

of size A'^=

100and

A'^=

400,and

using amaximum

number

of instruments of /c=

10and

k=

20.Thus

for each case a total of four different experimentswere

conducted.The number

of replicationswas

set at 5,000. In eachexperiment

the2SLS,

LIML

and

JIVE

estimatorswere

obtained using thenumber

of instruments thatminimized

the objective functionsdiscussed in the previous

two

sections.These

criteriawere

constructed using delete-one cross validation of the first stage relationship, alongwith

estimates of cr^^, a^and

cr^which were

obtained as discussed in Section 4, using a preliminary estimatorwhich used

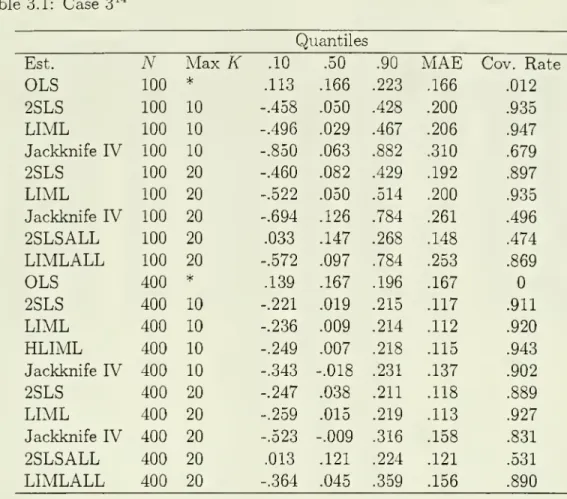

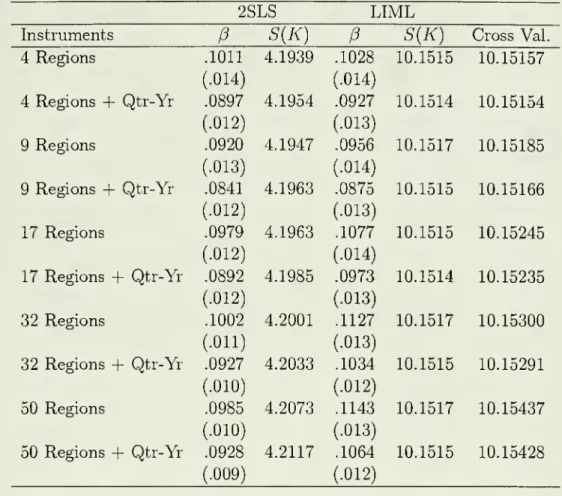

all ofthe instruments.Tables 1.1, 2.1

and

3.1 contain the relevantsummary

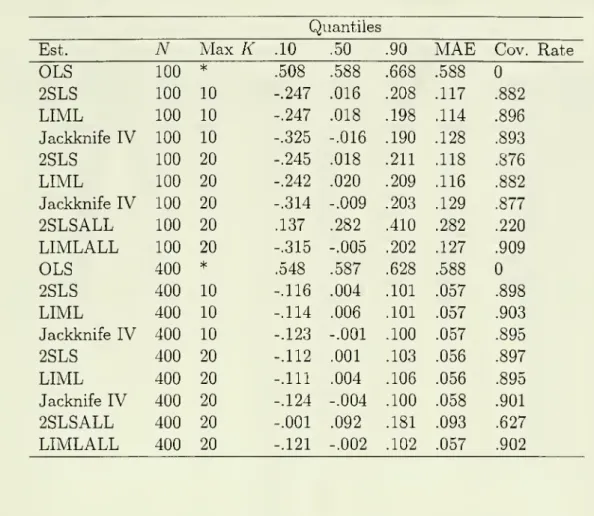

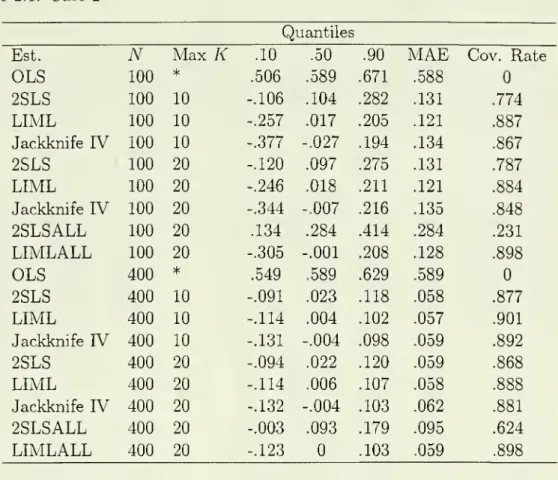

statistics for each of the three cases respectively. In each tablewe

report themedian

of the 5,000 estimates along withthe 0.1

and

0.9 quantiles ofthe estimates.The

differencebetween

thesecan be

considered away

ofmeasuring

dispersion. Additionallywe

report theMean

Absolute

Error of theestimates,

which

isan

alternativemeasure

of dispersion, and, finally, the coverage rate of anominal

95 percent confidence interval for each estimator. Additionallywe

reportthe relevant statistics for the

OLS

estimator as well as2SLS and

LIML

estimators that use all fc=

20 instruments.These

statistics were reported inAIK

(1995, Tables 2and

3). In Tables 1.2, 2.2

and

3.2we

report the frequencies withwhich

the various possibleK

valueswere

chosen in the experiments.A

few features ofthe results areworth

noting. First, themost dramatic improvements

occurinthe use of2SLS

with theoptimalnumber

ofinstrumentsbeingused.As

indicatedin Tables 1.1

and

3.1,2SLS

which

uses all the instruments has verypoor

properties,and

is biased towardsOLS.

Moreover, confidence intervals generallyhave

a verypoor

coverage rate with the worst occurring inCase

1 with A'^=

100where

thenominal

95%

confidence interval contains the true value just

22%

of the time.The

other cases are similarly poor.When

the criteria are used to choose thenumber

ofinstruments there isa substantial reduction in the bias (as

measured by

themedian)

and

the coverage ratesfor the confidence intervals are

much

closer to thenominal

rate of95%

generally beingaround 90%.

The

only exception to this isCase

2 with A'^=

100where

the coveragerate is

below 80%,

although this is a dramaticimprovement from

the23%

coverage ratewhen

all instruments are used.The

other noticeable difference in2SLS

when

the criteriais

used

is that the dispersion ismuch

lower as evidencedby reduced

MAE

and

a lower spreadbetween

the10%

and

90%

quantiles. It alsoworth

noting that theperformance

of

2SLS

using the criteria is not sensitive to themaximum

K

being considered.Indeed

the results for2SLS

when

one uses the criteria to pickK

with amaximum

possibleK

of 10 are almost identical to thosewhen

themaximum

possibleK

is 20.For

LIML

on

the other hand, themain

improvements

relative to the estimator thatby

MAE

or as the differencebetween

the .1and

.9 quantiles. This isbecause

LIML

performs

fairly wellwhen

all of the instruments are usedand

isapproximately

median

unbiased

and

provides confidence intervals thathave

a coverage rate that is reasonablyclose to the

nominal

rate of95%

beingaround 90%.

The

coverage rate forLIML

when

the criteria is

used

is slightly lowerthan

forLIMLALL

inCases

1and

2. InCase

3,however, there is

an

improvement

in the coverage ratewhen

the criteria isused with

therate being very close to the

nominal

rate.The

main

improvement

thatcomes from

theuse ofthe criteriais in the decreaseddispersion ofthe estimator

which

results in all cases.The

performance

ofJIVE

is a little bitmixed

relative to the other estimators.The

bias (using themedian)

ofJIVE

insome

cases appears tobe

the lowestamong

theestimators

and

other cases (notablyCase

3 with 100 observations) is the worst so thatthere is

no

clearly superior estimator as far as bias is concerned.What

is striking is that the dispersion forJIVE,

using either measure, is larger in practically all cases relative to either theLIML

or2SLS

estimators that resultfrom

the use of the criteria for picking thenumber

of instruments.There

is alsono

clearimprovement

in the coverage ratesfrom

the use ofJIVE

ratherthan

either2SLS

orLIML

estimators that use the criteria for picking thenumber

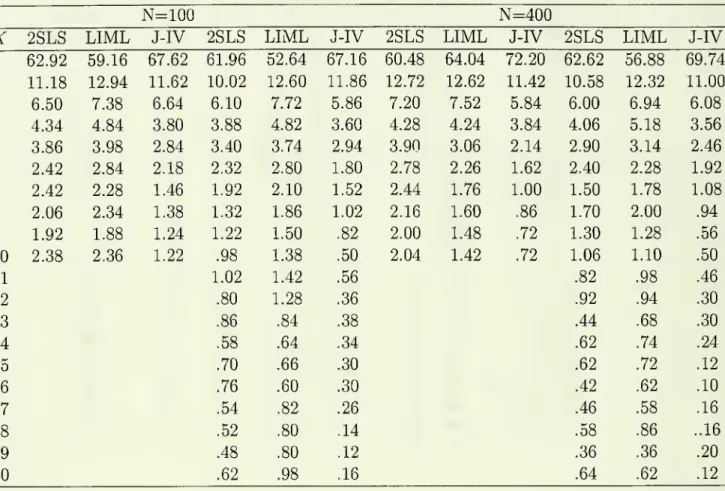

of instruments.In Tables 1.2, 2.2

and

3.2we

have

provided frequencieswith

which

the criteria chose the respectivenumber

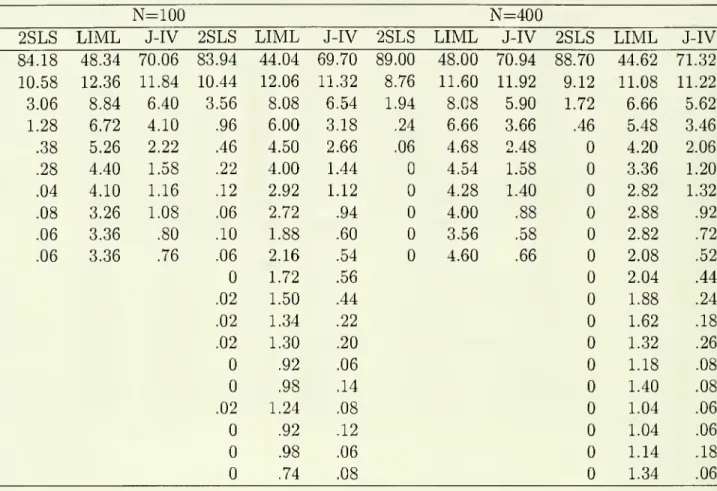

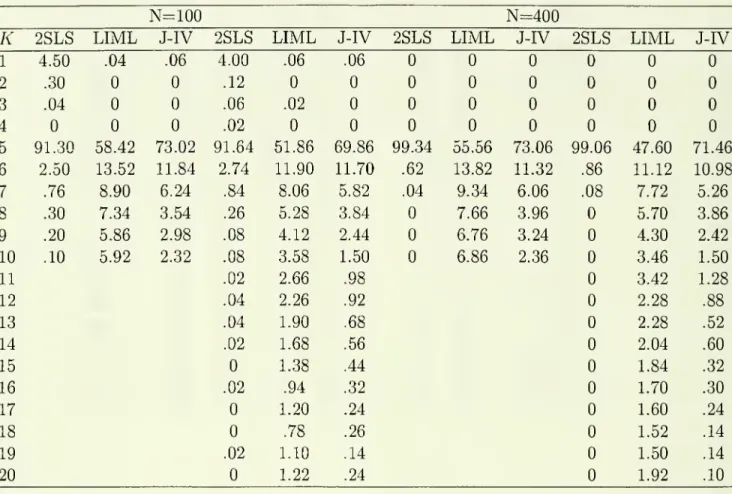

of instruments for each estimator in each case.A

few

featuresstand

out. First, for all estimators the criteria usually points to a value ofK

that is at least as large as is required to include the relevant instrument-

in Cases 1and

3 this \sK

=

\ while inCase

2 this is /C=

5.What

is also interesting, is that inCase

2 thecriteria generally pick the correct

number

ofinstriimentsmore

than

halfthe time. Also,as

one

might

expectfrom

the discussioninSection 3, thecriteriafor2SLS

generallypointsto smaller values of

K

than

does the criteria forJIVE,

while the latter generally picks values forK

that are smaller (on average)than

those forLIML.

With

LIML

and

JIVE

the criteria