Mean Field Games of Controls: Finite Difference Approximations

33

0

0

Texte intégral

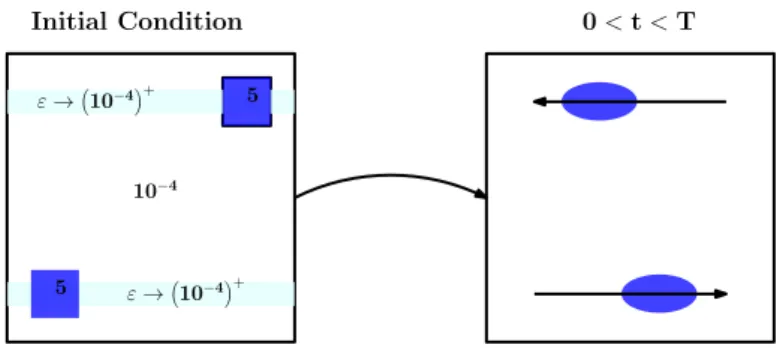

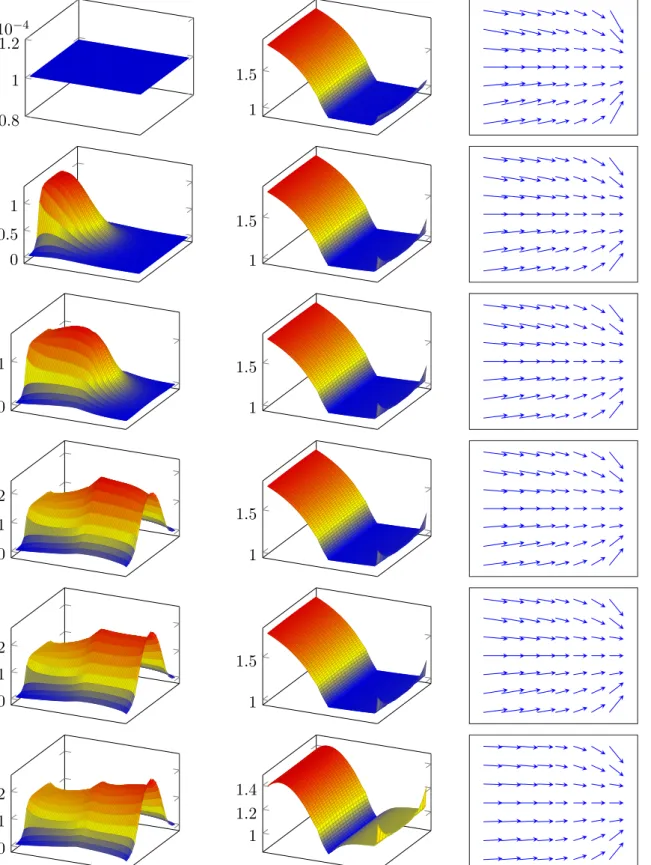

Figure

+7

Documents relatifs