DEC

21

1989WORKING

PAPER

ALFRED

P.SLOAN

SCHOOL

OF

MANAGEMENT

THE

MANAGEMENT

OF

END-USER

COMPUTING

VijayGurbaxani

Graduate Schoolof

Management

UniversityofCalifornia,Irvine

(714)856-5215

Chris F.

Kemerer

Sloan Schoolof

Management

MassachusettsInstituteofTechnology

(617)253-2971

MASSACHUSETTS

INSTITUTE

OF

TECHNOLOGY

50

MEMORIAL

DRIVE

AN

AGENCY

THEORY

VIEW OF

THE

MANAGEMENT

OF

END-USER

COMPUTING

VijayGurbaxani

Graduate Schoolof

Management

UniversityofCalifornia, Irvine

(714)856-5215

ChrisF.

Kemerer

SloanSchool of

Management

Massachusetts Instituteof

Technology

(617) 253-2971Lastrevised: October 1989

Research support

from

theMIT

CenterforInformation Systems Research andtheMIT

International FinancialServices Research Centerare gratefullyacknowledged.MIT

Sloai\School

WP

#2094-88

Draft - Please

do

not

quote, duplicate, or distributewithout

the authors'written

An

Agency

Theory

View

oftheManagement

ofEnd-user

Computing

ABSTRACT

The

rapidgrowth

in end-usercomputing

(EUC)

inorganizationsand

itsimplications for thedegree

of centraHzation ofthe information services functionhave

led to theneed

for a theorythatwill assist in themanagement

ofthis process. Thispaper employs

microeconomics

and, inparticular,agency

theory todevelop

a positivemodel

ofthegrowth

ofEUC.

The

theorydeveloped

here is evaluated usingdescriptive datafrom

earher

EUC

research.The

model

isshown

to possess considerable explanatorypower,

suggesting that

agency

theory providesclear insights into themanagement

ofcomputing,

and

has significantnormative

implications forthemanagement

ofcomputing

in organizations.1.

INTRODUCTION

The

dramatic

decline in the costsofhardware and

the trendtowards

the increasedpower

ofmicrocomputers

and minicomputers have enabled

significantgrowth

in end-usercomputing

(EUC).

This trend has implicationsnot only for themanagement

ofEUC

butalso for the

degree

ofcentralization ofthe InformationSystems

(IS) functionin organizations. Therefore, there hasbeen

increasedfocuson

the organizational issuessurrounding

EUC,

asevidenced by

senior IS executives' responses inseveral recentsurveys.^

Management

issues related to decentralization of the ISdepartment

alsoranked

high

on

theirlist of concerns.This interest in

EUC

has resulted innumerous

articles in theacademic and

practitioner literature.The

primary

thrust ofmany

of these articles isprescriptiveand

suggests alternative

managerial

strategies forEUC

(Alavi etal. (1987), Gerrityand

Rockart

(1986),Henderson

and Treacy

(1985),Munro

etal. (1987)).Some

studieshave

analyzed the characteristicsofend-users

and

their tasks (Rivardand Huff

(1985),Quillardetal. (1983),

Rockart and Flannery

(1983))and

how

these tasks evolve(Huff

et al. (1988)).However,

the previous researchdoes

notdevelop

positive models,namely

those"thatprovide

knowledge

about

how

theworld

behaves" (Jensen (1983)).A

positivemodel

ofend-user

computing

would

link the process ofitsgrowth

to underlying theories ofmanagerial

behavior.Robey

and

Zmud

(1989)have

recentlycriticized theEUC

hteraturefornot

being "grounded

inspecific theoriesof organizational behavior."The

currentpaper proposes

the use ofagencytheory as a theoreticalbase

and

integrativeapproach

within

which

tounderstand

theEUC

phenomenon.

The

aims

ofthispaper

are todevelop

apositivemodel

ofthegrowth

ofEUC

inorganizations

and

to studyits implications.End-user

computing

hasbeen

defined as "the capability ofuserstohave

direct control oftheirown

computing

needs" (Davisand Olson

Firstmostimportantinalistof22issues,ArthurAndersen(1986);secondmostimportantinalistof19

(1985)). This definition of

EUC

emphasizes

the control aspects of theproblem

which, it will beargued

later, are at the heart of the issue. In particular, it highlights the division ofcontrol

between

the end-userdepartments and

the central IS organization.The

reference disciplineemployed

in thispaper

ismicroeconomics encompassing

agency

theory, as originally suggested by Kriebeland

Moore

(1980).While

traditionalmicroeconomics

hasproven

useful in analyzinga large variety ofproblems, it has notbeen

'videly

used

in analyzingintra-firm managerial controlproblems due

to itsassumptions

of costless information transferand

of goalcongruence

ofmanagers

within the firm.Agency

theory extendi the

microeconomic approach

by relaxing theseassumptions

and, therefore,is

shown

to be particularly appropriate for the intra-firm nature of theEUC

controlproblem.

The

theorydeveloped

here has significantnormative

implications forthemanagement

ofcomputing

in organizations.The

outline ofthispaper

is as follows.The

researchproblem

and approach

arepresented in Section 2. Section 3 introduces the principal-agent

problem

in IS within amicroeconomic

framework

and

analyzes itsimpact

on

the optimal production strategies forinformation services. In Section 4, the

model

ofEUC

is illustrated usingindependent

secondary

descriptive data.Managerial

implicationsand

concludingremarks

are presentedin Section 5.

2.

THE

RESEARCH

PROBLEM AND APPROACH

This section begins with

an

introduction of the researchproblem

-

control ofthe provision ofIS services. Next, the salient features ofthe traditionalmicroeconomic

approach and

its shortcomings in analyzingmanagerial

behavior in this context arepresented. This is followed by a briefdiscussion of

agency

theory,which

extends the traditionalmicroeconomic approach

to address these deficiencies.A-

Research

Problem

Given

the nature ofthe supply ofand

demand

for informationservices, theorganization

must

determine

how

the internal provisionof information serviceswillbe

organized so as to

maximize

the netvalue ofinformation services. Traditionally, IS activitieshave

been

grouped

into the following categories: administration, systemsdevelopment,

operationsand

technical services(Zmud

(1984)). Administrative tasksinclude capacity planning, systems planning,budgeting,

and

standardsdevelopment.

Systems

development

activities include in-house softwaredevelopment

and maintenance,

as well as

hardware

and packaged

software selection.Operations

include activitiessuch asjob scheduling,

hardware maintenance and

machine

operation, while technical servicesinclude database

and

telecommunications

support.^The

focushere

ison

the controlissues related to the internal provision of theseservices. Control

means

the ability to i)choose

the decision initiativetobe

implemented

and

ii) tomeasure

theperformance

ofagentsand

implement

areward

structure(Fama

and

Jensen

(1983)).Control

issues thatgovern

IS activitiesinclude the choice oftheorganizationstructure ofthe IS

department,

managerial

compensation

contracts, the decision tomandate

thata servicebe

acquiredfrom

the central ISgroup,chargeback

systems forinformation services,

and

budget

allocationmechanisms.

The

choice ofcontrolmechanisms

is naturally amajor determinant

ofthe effectivenessofIS activities.The

authority todetermine

how

aspecific activity isperformed

istermed

here as adecision right.

Formal

approaches

recognize that initiallyall decisionrights reside with topmanagement,

who may

decide to allocatesome

orall of these rights to ISand

end-user departments.Then,

the locusofcontrol isdetermined by

the partitioning of decision rightsbetween

the differentmembers

ofthe organization. Thus, the controlproblem

may

be

viewed

asdetermining

the optimalpartition of these decisionrights.Fortheremainderofthispaper, operationsandtechnicalserviceswillbe consideredtogetherinone categor)',operations/technicalservices.

Decentralized computing, defined here as the transfer of control

from

centralized ISdepartments

toend-user or functional departments, has continued togrow

in scopeand

in degree (Arthur

Andersen

(1986)).The

decentralization ofcomputing

cannotbe

explained simply by

examining

theeconomics

of the productionof information services. Ifthat

were

true,one might

witness thegrowth

ofdistributedcomputing

as distinguishedfrom

decentralized computing. Distributedcomputing

is defined as the location ofhardware, softwareand

personnel atvarious sitesthroughout

the organization with the importantprovision that control decision rights

remain

vested in a central authority.An

underlying factor in thegrowth

ofdecentralizedcomputing

was

the dissatisfaction of userswith the centralized environment.'' In theory, it is feasible todevelop

a centralized plan for the provision ofinformation serviceswherein

all users aresatisfied. Yet, this has rarely occurred. It shall

be argued below

that thedominant

factor that resulted in asignificant decrease in the likelihood ofsuccess ofa centralized ISorganization is aprincipal-agent

problem.

However,

before developing thisargument,

the traditionalmicroeconomics

argument

is presented to provide aframework

withwhich

to build theagency model.

B.

The

TraditionalMicroeconomics

View

The

microeconomics approach

to developingpositive or descriptivemodels

ofaphenomenon

assumes

netvaluemaximizing

behavior.To

develop

a positive theory of ISmanagement,

one

would

build amodel

ofthisprocessby assuming

that practices relating to themanagement

ofcomputing

arean

outcome

of net valuemaximizing

behavior(Silberberg (1978)). Thus,

one

would assume

that the goal of the firmwould

be

tomaximize

the net value ofinformation services to the organizationand

derive, forexample,

the testable implication that in the early years ofcomputing, firms centralizedcomputing

services to exploit

economies

ofscale in hardware.These

hypotheses ofmanagerial

behavior

could thenbe

tested against empirical data todetermine

the validityofthemodel.

One

traditionalmicroeconomic

approach

hasbeen

toassume

anumber

ofideal conditions,under which

it hasbeen

shown

that optimizing behavioron

the parts ofindividuals

and

firmsunder

pure-competitionleads to a Pareto-optimal socialoutcome,

i.e.,

one where no

otherallocationmakes

all partiesconcerned

at least as well offand

one

or

more

partiesbetteroff(Hirshleifer (1980)). It implies that,under

certain conditions, social welfare ismaximized

simplyasa result ofthe individualeconomic

players actingout ofself-interest.More

formally, a Pareto-optimalallocation results in a competitiveequilibrium implyingefficiency

among

consumers

in the allocation ofconsumption

goods,efficiency

among

resourceowners

in the provision of resources forproductive uses,and

efficiency

among

firms in the conversion of resources intoconsumable

goods.While

theabove

discussion applies toeconomic

actors in a competitive market, itcan

alsobe extended

to apply within afirm. In the context ofthemanagement

ofIS, the parallel situationwould

be

the creationof amarket

for information serviceswithin a firm (perhapseven

includingeconomic

actors outside the firm). Thus,one

could consider asituation

where

individualdepartments

would

be

allowedto act asconsumers

orsuppliersofinformation services. Ifthe netvalue of information servicesto the organization

were

maximized

using suchan

approach,the task facing the firmwould

be

the creationand

maintenance

ofsuch a market.However,

several factorsmay

cause amarket

failurewhere

socialwelfare isnotmaximized

in amarket

situation.These

include thepresence

ofmarket

power and

the existence ofexternalities.Market

power

isusuallyseen

asmonopoly

ormonopsony

power.

Externalities occurwhen

the actions ofan

economic

agent affect the interests of other agents inaway

not capturedby

market

prices.Both

ofthese factors limit the applicabilityofthe traditional

microeconomics

resultsand

may

leadto situationswhere

apure

market-based approach

isinadequate. Vertical integrafion (corresponding todecentralizedcomputing)

is often cited as apossible solution to these problenis, since it allows theinternalization ofexternalities

and

limitsmarket

power. In this paper, it isargued

that i)both

market

power

and

externalities are present in the intra-firm IS contextand

that ii)market

power

is exercisedand aaions

that cause externalities are takenbecause

ofproblems

due

to theagencyrelationships (discussedbelow)

among

the actors within afirm.C.

The

Theory

ofAgency

An

agency

relationship canbe

said tooccurwhenever

one

partydepends

on

the actions ofanotherparty.More

formally,Jensen

and Meckling

(1976) definean agency

relationship as "... acontractunder which

one

ormore

persons (the principal(s))engage

another

person

(the agent) toperform

some

serviceon

their behalfwhich

involvesdelegating

some

decisionmaking

authority to the agent." Inan

organizational context, afirm hires

employees

(agents) in part to exploiteconomies

ofspecialization. Yet, theseemployees

often act in amanner

that is inconsistent withmaximizing

thewelfare of thefirm.

Agency

theory argues that this occursbecause:a) the goals of the principal

and

the agent are often inconsistentwithone another

("goal incongruence"),and

b) the principal cannot perfectly

and

costlesslymonitor

the actionsand

theinformationof the agent ("information asymmetries").

Since agents are usually better

informed

thantheir principalsabout

their tasks, organizationswould

do

better ifall information couldbe

shared atzero cost, or iftherewas no

divergencebetween

the goals of the principalsand

the agents.The

economic

loss that occursdue

to theabsence

ofsuch optimal conditions is called theagency cost.The

components

ofagency

costs are: monitoringcostsexpended

by the principal to observe the agent,bonding

costs incurred by the agent tomake

hisor her servicesmore

attractive,and

residual loss,which

are the opportunity costsborne

by the principaldue

to the difference inoutcomes

thatwould

obtainbetween

the principal'sand

agent's execution of the taskmaximization

and

the existence ofagency

costsis that theprincipal seeks tominimize

agency

coststhrough

theuse ofcontrolmechanisms.

The

primary

controlmechanisms

inorganizations are the

performance

measurement and

evaluation system, thereward

and

punishment

system,and

the system for assigningdecisionrightsamong

participants intheorganization(Jensen (1983)).

In the case ofcostlessinformation transfer

and

theabsence

ofagency

costs, as isassumed

by

the traditionalmicroeconomics

approach, the controlproblem

isinconsequential.

One

can

simplyassume

thatall information that a centralplanner

requires tomake

a decisionand

that is possessedby

other actorswithin the firmcan

be

acquired costlessly. Further, since allactors

behave

in amanner

thatis consistent withmaximizing

the value of the firm,no

controlmechanisms

are requiredto ensure theconsistency of

managerial

behavior with the goals of the firm.However,

ina realistic setting, the controlproblem

assumes importance because

ofthe existence ofinformationasymmetries

and

goal incongruenciesand

the resultingagency

costs.Eisenhardt

(1989) has articulatedthe usefulnessofagency

theoryinanalyzingmanagerial

problems

characterizedby

goal conflicts,outcome

uncertainty,and

unprogrammed

or team-orientedtasks.Many

IS activities fitthis description,and

it hasbeen

suggested thata largenumber

oforganizationalproblems

inthemanagement

ofIScan

be

analyzed successfully inan agency

context(Gurbaxani

and

Kemerer

(1989),Robey

and

Zmud

(1989)).The

design ofeffective controlmechanisms

forIS activitiesisparticularly difficult, since the

agency

relationshipoccurs in adynamic,

rapidlychanging

environment

and

management

practiceshave

little time to stabilize(Nolan

(1979),Gurbaxani

and

Mendelson

(1989)). In this paper, the focusison

theimpact

ofagency

costson

the organization ofthe internal provision ofinformationservices.^ SpecificallyAn

alternativeapproachwouldbetransactioncosteconomics,anapproachwithsimilaritiestoagency theoryinitsemphasisoninformation anduncertainty(Williamson(1985)). Eisenhardt(1989) notesagency theory's inclusionof the notions ofriskaversionandinformationasacommodityas distinctionswith transaction costeconomics. Moreover,transaction cost theory'sprimary (though notexclusive) focusison

8

examined

are theimpaa

ofagency

costson

thegrowth

ofEUC

and

the implications for the degree of centralization of the information services functions.3.

AN

AGENO

MODEL

OF

INFORMATION

SERVICES

The

key issues that arise inan

agent-theoretic analysis of themanagement

ofIS arean

identification of theeconomic

actorsand

their objectives,an

analysis ofhow

theseobjectives result in conflict,

and an

analysis of the nature of the resulting organizationalcosts.

These

issuesmust be

considered in conjunction with themicroeconomic

and

technological characteristics of the IS

environment

todetermine

the optimal strategies for themanagement

of IS resources.A-

The

Agency

Structure of TraditionalComputing

inOrganizations

In order to provide a

model

ofcurrent end-usercomputing,

it is helpful to begin with a brief discussion oftraditionalcomputing

in organizations toshow

the origins ofEUC.

The

level of analysis is thedepartment

and

three types ofeconomic

unitswillbe

relevant: top

management,

the centralized IS department,and

end-userdepartments

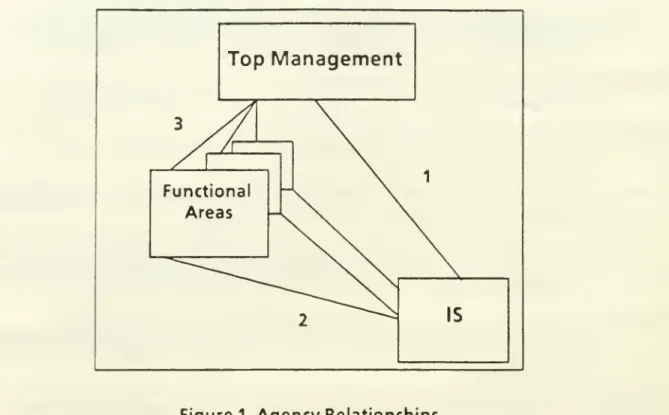

(seeFigure 1).^

There

are three resulting principal-agent relationships. Intwo

of these relationships, the principal is topmanagement

and

the agents are the functionaldepartments and

the IS department. In the third relationship,each

end-userdepartment

isa principal

and

the ISdepartment

is the agent.'^The

objectives ofeach

of these actors areintrafinn relation.ships.Thus, transactionscosteconomicsseems most appropriateforthe study ofthe

externalprovision ofinformationservices,while agencytheoryismoreapplicabletowithin firm

transactions.

Consistent withthisapproach,the behavioralassumption ismade thatalleconomicunits act out of self-btcresl. Whilethere arc obviousdivergencesbetweenthegoals of individual actors within eachof the three

unitsandthe goals oftheirmanagers,these are ofsecondaryimportance inthe currentanalysis. Thus, for

the purposesof exposition, the idealized assumptionsaremade thattopmanagement attemptstomaximize

the value ofthe firm, that end-userswthin afunctionaldepartment attempt tomaximize the"objective

function" of the department head andthat the centralISstaffattempts tomaximizethe "objective function" ofthe ISmanager. Henderson (1987) usesasimilarapproachin studying the ISdesignenvironment. Withthe possible exception of organizationswhose primaryexternalproduct isinformationservices,

information systemsarc asupport orstafffunction and, therefore, theISdepartment "worksfor," inan agencysense, the end-user dLpartmcnis, andnot theotherway around.

consideredin turn, focusing

on

the IS aspects ofthe principal-agent relationships. Itwillbe argued

in Section3.B that the individual objectivesofeach

ofthese actorscan be

in conflictwithone

another

and

result inagency

costs.However,

beforecoming

to that conclusion, it isusefultoexamine

how

this structure forproviding informationserviceswithin the organization

came

about.When

computing

was

first introducedinto organizations,most

end-usersand

topmanagement,

specifically,were

unfamiliarwith the technology. Thisresulted in topmanagement

creating ISdepartments

and

hiringspecialists intheproduction

of information services.For

thesame

reason,most

decision rights related to themanagement

ofcomputing

were

allocated to the IS department.The

decision to centralizecomputing

was

driven primarilyby

the costs ofcomputing.^The

demand

generated by any

single end-user

group

oftendid notjustifysuch a large investment.Thus,

thedemands

of various end-usergroups

had

tobe

aggregated to justify the investment.The

decisionrights related tohardware

and

software selectionwere

typically located in the ISdepartment.

Applications software

was

developed

almost exclusivelyby

professionalswho

were

locatedin the IS

department.

Sinceindividual end-userdepartments

were

uncertain oftheirfuturedemands

for software services, the appropriate strategy forthe location ofsoftwareprofessionals

was

to centralize theprogramming

functionsince thiswould

simplifythemanagement

of theseprofessionals.Therefore, the centralization of

computing

was

aresult of organizations seeking to exploiteconomies

ofscaleand

of specialization thatwere

warranted by

the high costs ofcomputing.

Due

to supply-side considerations inthat time, thecosts ofproductionoutweighed any

other costs indetermining the strategy forthe provision ofinformationservices.

The

net result of the centralization ofcomputing

was

thatcomputing

became

apublicgood. Inthe case ofpublicgoods, the decision

problem

isto find the solution thatInparticular,therewere significanteconomiesofscale inhardwaretechnologies, as isembodiedinGrosch's law(Mendelson (1987)). Moreover,not onlyweretheunitcostsofcomputinghigh,buthardwarecapacity

10

maximizes

publicwelfare over a large set of diverse users,and

the resultingsocialoptimum

may

not be anyuser group's localoptimum.

This idea is critical to the discussionbelow

of the impacts ofagency

costson

the provision of information services.B.

Market

Failures in OrganizationalComputing

Due

toAgency

As

the unit costs ofcomputing

decreased over time,and

asminicomputer and

microcomputer

technologybecame

available, decentralizedcomputing

became

feasible, aswall be seen below.

However,

thechanging

economics

ofinformation systems supply are anecessary but not sufficient condition for decentralized

computing

(asopposed

tomerely

distributed computing).To

see this, the nature ofagency

costs ina centralizedenvironment

are discussed below.B.l. IS

department

asan

agentoftop

management

In the traditional environment, top

management

reliedupon

IS specialists as theiragentsto provide IS services.

These

agentswere

typicallyorganized intoone

centralizeddepartment due

to theeconomies

ofscaleand

specializationnoted

above.However,

thisagency

relationship introduces costs to the organization through goal incongruenciesand

information asymmetries.

While

netvaluemaximization

ofinformation servicesis oftenthe stated intent of ISmanagers,

their actual behavior patternssometimes

suggest that their "objective function"may

be

quite different.For example,

the salariesof thesemanagers

is often related to the scale of the operation, inducingthem

to indulge in so-called"empire

building."A

related cost arisesbecause

of the valuemanagers

placeon

the control of a resource thatmay

increase their politicalpower

within the organization.Another problem

istermed

the"asymmetric

cost"problem (Mendelson

(1990)).Here,

managers

oftenmake

sub-optimaldecisions

because

the cost of the decision to themanager

may

be

quite different than thatincurred by the firm.

For example,

amanager's

evaluation issometimes based on

the quality of services provided rather thanon

itscost effectiveness. This is often stated in the11

practitioner literature as

"No

one

evergot fired forbuying

IBM."

This isan example

of the risk-averse nature ofthe IS manager-agent. ISmanagers

also often sufferfrom

the "professionalsyndrome"

(Mendelson

(1990)),wherein

theyhave

incentives toacquire thenewest

hardware

and

software technologies with insufficient regard for cost justification.Thisis consistent with

maximizing

behavior ofthe IS professionalwhose

market

value ispartly

determined by

hisfamiliaritywithnew

technologies.The

optimal allocation ofinformation servicestypicallyrequires that the marginal value ofinformationservices to adivisionequal the marginal cost of providing theseservices (Hirshleifer (1980)). Ifinformation transfer

were

costless,one

couldassume

that the ISdepartment

possessed both the costand

value information required toimplement

such

an

allocation. Thus, informationasymmetries

would

notbe an

issue.Furthermore,

since their actionswould

be

completelyknown

to topmanagement,

the ISdepartment

could

be expected

tomaximize

the netvalue ofinformationservices to the firm.However,

the existence ofasymmetric

information precludes such a solution.The

primary

informationasymmetry

inthe IS context is thatknowledge

ofthevalue ofa

givenIS task is almost always possessed

by

the end-user,while informationabout

the execution ofthe task is possessedby

the IS department. This informationasymmetry

also extends totop

management,

who

are neither completelyaware

ofthe value ofinformationgenerated

by

IS activities to the end-userdepartments nor

ofthe costand

technological information possessedby

the IS department. Thus, topmanagement

is facedwith theproblem

ofconstructinga control

system

thatwillmaximize

the netvalue ofinformationservices to the firmwhile taking into accountthe existence ofthese information asymmetries.The

control

problem

is therefore ofconsiderable importance.Top management

traditionallyimposed one

oftwo

control structures: a profitcenter

approach

or a cost center approach. In aprofit center, theperformance

ofthe ISmanager

ismeasured

by

themagnitude

ofprofits thathe

orshe generates,while inthe case ofa

cost center,theperformance

metrics arerelated toadherence

to budgets orby

12

comparison

with "standard costs."Each

ofthese creates verydifferent sets ofincentives for the ISmanager.

The

profit centerencourages

efficiency in the production ofinformation serN-ices. but also creates incentives for the IS

manager

to actas amonopolist

to increase profits. This, in turn, raises the likelihood that the prices ofcomputing

serviceswill

be

higher than optimal.The

cost center,on

the other hand,does

not create incentives for higher prices,but neitherdoes

itencourage

efficient production.*In both of these control structures, thewelfare ofthe organization is

reduced by

theagency

costs that resultfrom

theaaions

ofthe ISmanager.

When

the ISdepartment

issetup

as acost center, the costs resultfrom

the inefficient production of informationservices. TTiese costs are manifested as delays in operations, backlogs insoftwaredevelopment, and

higher total costs (as distinguished

from

unit costs) for information services. In the case ofaprofit center, such costs are incurred primarily as higher

monopoly

prices rather than asfree-market prices for services.

As

the costs ofcomputing

continued to decrease over time,and

asminicomputer

technology

became

a feasible option, the decision nottomandate

that allcomputing

servicesbe

acquiredfrom

central ISmeant

that individual end-userdepartments were

given the right to

implement

decentralized computing.The

fact that decentralizedcomputing

was implemented

bysome

end-users-

even though

itwas

initiallymore

expensive than centralized

computing

servicesdue

to the fixed costsand

losteconomies

of scaleand

specialization -- strongly suggests that these end-userswere

incurringcostsbeyond

those seen in accountingstatements. This suggests that end-userdepartments

exercised this option tominimize

theagency

costsresultingfrom

the self-interestedbehavior of the IS department. Decentralized

computing

is thereforean

effectivemeans

oflimiting the

market

power

of IS departments.'For

13

B2

User

department

asan

agent of topmanagement

Analogous

to the IS department's role asan

agent to the firm,each

end-user or functionaldepartment

also acts asan

agent (Figure 1). Therefore, theirbehavior

alsoreflects goal incongruencies

and

informationasymmetries

intheirrelationshipwith the topmanagement

principal.The

discussion here,however,

willbe

limited to the effectof thesefactors

on

the allocationofIS resources withinthe firm.Decisions that

maximize

the netvalue of informationservices to thefirmmay

notbe

locallyoptimal, that is, theymight

notmaximize

thenet value of information services tothe individualend-user departments.

End-users

may

be

dissatisfiedwith resourceallocation decisions.

For example,

in amainframe

acquisitiondecisionwhere

there aremany

possible end-users,each

set of end-usersmay

prefera differenttype ofmachine.

In the casewhere

there is insufficientdemand

to justifythepurchase

ofmore

thanone

machine,

only a subset of end-userswill receive themachine

offirst choice,and

otherswillhave

tomake

do

with alower

rankingchoice.' Similarsituations arise inthe acquisition ofsoftware

packages

aswell.The

analogous

situationexists in the case of a softwaredevelopment

task.The

globally optimal specifications forsuch a taskmay

be an

outcome

ofmeeting

thedemands

ofnumerous

end-user groups. Individual end-usergroups

would

prefercustomized

applicationsthat, in all likelihood,

would

alsohave

betterperformance,

since theywould

not

be

constrainedby

therequirements

of otherend-users.Moreover,

end-userswhose

application

development

requests arequeued

behind

others ofhighervalue tothe organization incurwaitingcosts.End-user departments

alsohave

incentives thatencourage

them

to control theirown

information.There

areseveral possible reasons forthis.The

possession ofinformation that is ofsignificantvalue to the firm often results inincreased

power

to theNotethatinfonnationsystemsmanagers

may

alsohavetheirownpreferencesthatare usually drivenbya14

owTier of the information.

Another

reasonmay

be

that the informationmay

allow topmanagement

tomonitor

theperformance

of aend-userdepartment

more

closely,a possibly undesirable situation for the end-user.In all of the

above

situations,undoubtedly

some

end-userdepartments

couldbe

made

betteroff ifthe resource allocation decisionswere modified

in their favor.From

an

individual end-user department's perspective, they are incurring the costs ofexternalitiesimposed

byothers. Therefore, the end-usersnow

perceive that theycan

increase theirwelfare by biasing the information they provide the IS

department

to increase thelikelihood of a

more

favorableoutcome.

For example, an

end-usermay

request a higherpriority

on

a timesharingmachine

than is reallywarranted

bythe task ormay demand

amore

powerful personalcomputer

than theone

that is themost

cost-effective. In suchcases, the cost

imposed on

other end-usersstems

from

a reduction inresources available tothem. Since end-usersare believed to

be

acting out of self-interest, theyare likely todo

so.

Of

course, they are subject tomonitoring by

topmanagement

that limits theamount

of bias in information that they provide.However,

monitoring

is rarelyperfect,and

indulgingin

monitoring

activities also results inmonitoring

costs.The

net result is that resourceallocation

schemes

that are insome

partdependent

on

the disclosure of informationby

agents, are unlikely tobe

very successful inpractice.The

challenge facing the organizationis to

develop

a control strategy that aligns the self-interest ofagents with the interestsofthe firm.

BJ

ISdepartment

asan

agent ofend-userdepartments

TTie third

and

finalagency

relationship, consistent with the ISdepartment

being a"staff as

opposed

to "line" function inmost

organizations, is that ofthe centralized ISdepartment

acting asan

agent foran

end-user department. This relationship also providesfor a strong additional source ofconflict within the organization.

The

ISdepartment

iseffectively the agentof multiple principals (i.e., the top

management

principaland

the end-user principal)whose

goalsmay

not converge, as has alreadybeen

discussed in Section B.2.15

Added

to thismay

be

the IS department'sown

agenda

(the potential conflictwith topmanagement

havingbeen

discussed in Section B.l). Therefore, conflictbetween

the ISdepartment and an

end-userdepartment can

come

about because

a) the ISdepartment

istrying to act as

an

agent fortopmanagement

and, therefore,may

not act inaccordance

with the desired behavior ofthe self-interested end-user,

and/or

b) the ISdepartment

is itselfengaging

in self-interestedbehavior at theexpense

ofthe userdepartment.

Tiere

areseveralforms

that thesegoal incongruenciesmay

take inthe IS context.Assuming

that the ISdepartment

isactingon

behalf ofthe organization, then theywillbe

providing software systems

and hardware

services thatmeet

theneeds

ofthe entire organization, notjustan

individual end-user department. Therefore, a decision that ISmay make

on

behalf ofthe organizationmay

be

sub-optimal forany

given department. Inparticular, the IS

department

willengage

in activities topromote

the long-termcomputing

environment

serving avarietyof end-users. Therefore,any

particularend-userwillbear

additional costs, includingdelay costsand

integration costs,because

they are usingsharedresources.

Another

aspect to thisshared resourcephenomenon

isthat itmay

appear

tobe

a public

good

to the end-user.Given

self-interestedbehavioron

the partofthe end-user, itis expected that theywill tend to

over-consume

publicgoods, that is,usemore

ofthe ISresource than

might be

globallyoptimal forthe organization, ifthe controlmechanisms do

not insure that the end-user bears the costs ofsuch

consumption.

Of

course, the ISdepartment

may

not alwaysact inaccordance

withwhat

the topmanagement-principal

may

desire either.Given

the difficulty inassessing thevalue ofIS services,many

organizationsmay

treat it asa "utility,"where

the ISdepartment

management

is evaluated essentiallyon

the abilityto delivera consistent quality ofservice.This

might be

implemented

by

metrics such asmachine

ornetwork

uptime, orlow

levels of end-userproblem

reports. Inthis type ofenviroimient, ISdepartment

management

can

become

veryrisk averse, aschanges

may

involve disruptions inservice levels. Therefore,16

be discouraged. This

phenomenon

isparticularly relevant in IS servicesdue

to the rapid rate of technologicalchange

in this area.In

summary,

conflictbetween

the end-user-principaland

the ISdepartment-agent

can

develop

from

either the ISdepartment

role in representing its topmanagement

principal or

due

to the goals of the ISdepartment

itself.C.

Conclusions

Given

theabove

discussion, amodel

of the provision ofinformationservicesmust

incorporate the behavioral

assumptions

that the goals ofprincipalsand

agentsmay

divergeand

that agents act outof self-interest. It should also recognize that information transfer is costly,and moreover,

it cannot bepresumed

thatan

agent willbe

willing to reveal privateinformation ifsuch revelation is inconsistent with his or hergoals.

Based

on

theabove agency

model

of IS provision, there existsan

essential tensionbetween

the centralizationand

decentralization of IS services. Existing centralized ISdepartments

will prefer the status quo, in part tomaximize

theirown

welfare. End-userswill desire greater

autonomy

over theircomputing,

in part in order to avoid the externalitiesand agency

costswhich

arise in the centralizedsolution. Into thisenvironment

comes

the technical feasibility of end-user computing. This providesan

option for end-usersto provide at least

some

oftheirown

IS services.That

this option hasbeen

actedupon

in practice suggests support for theagency model.

This idea is exploredfurther in the next section.

4.

AGENCY THEORY

PROPOSITIONS

AND

EMPIRICAL

EVIDENCE

A. Introduction

The

preceding section introducedan agency

model

ofEUC.

Following thesecondary data

approach

ofSwanson

(1989), anumber

ofpropositions are generatedfrom

themodel

and

arecompared

with observationsfrom

previousindependent

empiricalEUC

17

categories ofISactivities: i) systems

development,

ii) administration,and

iii)operations/technical services. It is

shown

that the predictions oftheagency

model

are consistentwiththe resultsobtainedby

the empirical research.B.

Systems

Development

A

number

ofdifferences areapparent

between

traditional systemsdevelopment,

where

the ISdepartment

agent develops systems atthe request ofthe end-userprincipal,and

EUC,

where

end-usersdevelop

theirown

systems.These

differences relate tothe costof buildingsystems, the

methodology

ofsystemsdevelopment,

and

the qualityof systems.The

agency

theorymodel,

drawing

on

the constructs ofmonitoring

costs, information asymmetries,and

riskaversion providesan

explanation of thesedifferences.Because

oftheagency

relationship,many

systemsdevelopment

activities are noteasily

observed

by

the end-userprincipal. Therefore, the principal will eitherremain

unaware

of these activitiesorwillexpend

monitoringcosts (intheform

ofadding

auser to the projectteam,

forexample)

tobetterobserve IS.Consider

the followingproposition:PI:

Information

asymmetries

and

highmonitoring

costs fortheend-user

principal willtend to increase the cost ofIS-developed systems to theend-user.

For example,

IS activitiessuch as infrastructure buildingand

integration with other systemscan

be observed

only imperfectlyby

users. Thisis amajor reason

why

naiveusers,whose

onlyexperience with systemsdevelopment

may

be

small, self-developedpersonalsystems, feel that IS costs are too large (Cash,

McFarlan and

McKenney

1988). Inorderfor end-users to

have

full information, highermonitoring

costs are required, typicallyin theform

ofusermembers

on

the projectteam. Relative to this option,EUC

development

isoften attractive.

Moreover, even

when

end-users observe these activities, they oftendo

not valuethem

even

when

theymay

be

oflongterm

valueto the firm.A

typical userresponseis

noted by

Benson

in his study ofEUC:

A

number

ofacquisitionshave

been

justifiedon

the basis thatdevelopment

costs, including hardware,were

less than softwaredevelopment

costs for the18

Accounting

systemsmay

also contribute to these informationasymmetries and

cost perceptions. AJl of the IS costs are typicallycharged back

to the end-user, often inways

that unfairly apportion fbced costs

and/or

are set ata rate simply to balance the ISbudget

(Nolan

(1977)).An

example

ofsuchan

accountingcalculation isnoted

byRivard

and

Huff:

I

wTOte

down

the time for developing thisparticular application:40

hours.DP

would

have taken 8 hours just to cost it outand

would

have charged

me

$41.50

an

hour

todo

so." (Rivardand

Huff

(1988), p.559)TTie cost of deriving the estimate isalso a

fomi

ofmonitoring

cost for the principal.Even

ifchargeback

isdone

appropriately, the calculation of the relative costs of IS versusEUC

solutions

may

be

difficultdue

to the typicallyuncounted

opportunity costs ofhavingend-users

become

amateur

systems developers (Hurst (1987)).Thus

the costs ofmaintaining theagency

relationship,coupled

with the difficulty inapportioning fixed costs,

make

IS-developed systems generallyappear

more

expensive thanthe

EUC

alternative.Of

course, insome

cases,IS-development

is trulymore

expensive, particularlyon

very small systems,due

in part, to the costsofworking

with a sharedresource.

However,

the true net costmay

be

difficult to determine, given that the highmonitoring

costsmay

be

offsetby

theuncounted

opportunity costs.A

second

systemsdevelopment

proposition relates to themethodology

of building systems. In particular, usersappear

to prefermethodologies

such as prototyping, while the central ISdepartment

prefersusingthemore

formal systemsdevelopment

life cycleapproach.

The

following proposition offersan

explanation for this observation:P2:

Risk

aversionon

the part of the IS agent willmake

IS prefer input-based, ratherthan

outcome-based,

control strategies.Traditionally, large systems

have

been

developed

using the systemsdevelopment

lifecycle

(SDLC),

a process designed to initially elicit systemrequirements

from

end-users,and

then tobuild systems in a carefullyplanned

series of sequential stages thatemphasize

systemvalidity, correctness

and

maintainability, rather thanspeed

ofdevelopment.

An

19

limitedset offunctionality. In prototyping,

development

work

continuesuntil the user issatisfied. Thus, prototypingis essentially

an outcome-based

controlstrategy, while thesystems

development

life cycle,with itsextensive task checklists,is essentiallyan

input, or behavior-basedapproach (Ouchi

(1979), Eisenhardt (1985)).Agency

theorywould

predict that the risk-averseagent (centralIS)would

prefera

behavior-based approach, since theoutcome-based approach

entailsgreaterrisk. Conversely, theend-userprincipal,who

cannot

perfectlymonitor

the agent'sbehavior,would

preferan

outcome-based

approach.Infact, these preferences are

observed

inpractice.For

example, Rockart

and

Flannery

note,For

a significant portion of theirnew

applications, users find the tools,methods,

and

processesadhered

toby

the information systems organizationas entirely inappropriate.

(Rockart

and Flannery

(1986), p. 288)In addition, while end-users are participants in

most

phases ofthe systemsdevelopment

lifecycle, they are rarelyincontrol ofit. In large

mainframe

enviroimients, often the criticalissues

were

perceived tobe

outsidethe range ofthe user'sexpertise, therefore, ISstaffwere

invariablyplaced in charge ofprojects. This control structure isstilltypical today,unnecessarily so in the

minds

ofsome

end-users.As

noted by Rivard

and

Huff,UDA

[userdeveloped

applications] also has the potential ofmaking

application

development

amore

flexible process, so userscan

readilyadapt

their applicationswhen

theneed

arises. (Rivardand

Huff

(1984), p. 40)Due

to the ease ofmaking

modifications, particularly inthe early stages of a prototypedsystem, end-users

may

perceive that theywill retainmore

control over the systemand

itscontinuing

enhancement.

Thisserves as furtherincentive againstthe life cycleapproach.Of

course, the actualevolution ofsuch projectsin reality, differsfrom

this ideal.Note

that the directvalue ofan

applications projectis derived onlyby

the end-user(s)who

requested it.

On

the otherhand, the costs ofmaintainingit are often incurredby

the ISdepartment,

even

when

theuser hasdeveloped

the system (Scheler (1989)).Unless

itremains

standalone, a quickly prototyped systemis likelytoresult in increasedfuturemaintenance

costs to the ISdepartment due

to the typicallackof upfront design.20

However,

the benefits of the shorterdevelopment

time accrue primarily to the end-user.Therefore, it is predictable that IS

would

prefer tousedevelopment approaches

that arebelieved to ease future

maintenance.

This risk aversionon

the part ofIS hasbeen noted

byGuimaraes

(1984,p. 6):"MIS

departments

tend toshyaway

from

userdevelopment

requests involving ill-defined, unstruaured, or volatile requirements."

Of

course, it isexactly these types ofsystems for

which

prototyping isrecommended

(Davisand

Olson,(1985)).

In addition, the use of the systems

development

life cycle is often perceived by theIS

department

as necessary in order todetermine

theimpact

ofnew

systemson

the existing base, or in order to integrate thenew

systems with older applications. Prototypingmethodologies, while delivering

new

functionality to the user expeditiously, tend todo

soby ignoring or delayingactivities such as integration.

Moreover,

end-userswant

their applicationsdeveloped

in themost

rapidand

effectivemeans,

whereas

IS has the application portfolio of the entire firm as its responsibility. Therefore,for anumber

of reasons, ISwould

prefer to use theSDLC,

an

input-based control strategy, rather thanan

outcome-based

control strategy, such as prototyping, thatwould

shift the risk ofrequirements

uncertainties tothem.

A

thirdand

final proposition regarding systemsdevelopment

concerns the overall quality ofsystems builtby

end-users asopposed

to those built by the ISdepartment.

P3:

Goal

incongruenciesbetween

the central ISdepartment

and

theend-userdepartment

and

risk aversionon

the part of the IS agent willcause

end-user developed systems tobe inconsistent nith IS

standards

in areas like integrationand

quality.In the issue of integration, the divergence in goals

between

user-developersand

central IS is readily apparent.As

the goal of central IS is tosupport theneeds

of the entire organization, theneed

for integration is clearand

vital. Also, as a centralprovider ofservices, IS can exploit scale

economies by

developing policiesand procedures

that providea consistent

and

integrated base, such as a central database,development

platforms or interface standards.End-user departments

may

have

neither the incentive nor thescale to21

justify thistype ofeffort.

Moreover,

with a centralized controlmechanism, redundant

efforts are less likelyto occur, aresult that is consistent withthe goals ofthe organization.This divergence ofgoals has

been

noted by

severalEUC

researchers interms

ofthe lack ofeffortexpended

toward

integrationand

coordination.For example,

Guimaraes

notes:

In the early stages of personal

computing

implementation, users often arepreoccupied

with operationalproblems

and

ignoremanagerial

considerations. Consequently,

problems

withmicrocomputer

compatibilityhave

besetmany

oftheusers mterviewed.(Guimaraes

(1984), p,5)Similarly, Alavi has observed:

The

uncontrolledgrowth

ofmicrocomputers can

lead to such difficulties asmultiple versions of incompatible data

and

incompatiblemachines

thatcan

not easily

be

linked into networks...Uncoordinatea proliferation of end-usertools (particularly

microcomputers)

most

likely leads to difficulties in integratingand

establishingcommunication

linksamong

these tools. (Alavi (1985), p. 17)Another example

of the likely lower quality ofEUC-developed

systemsis the widelynoted

lack of

documentation.

Most

observers of theEUC

arena

have noted

this, forexample:

In almost all cases, the necessary

documentation

and/or

controls usuallydeveloped by

I/S professionals for operational systemswere

lacking in theend-user

developed

systems.(Rockart

and Flannery

(1986),p. 307)It

was

felt that thetendency

of end-users to eliminate formalvahdation

techniques, extensive testing,

documentation

and

audit trails increases thedata integrity

and

securityrisks. (Alavi (1985), p. 177)To

most

personalcomputer

users,"documentation"

was an

unknown

word.

(Benson

(1983), p. 40)This issue

goes

directly togoal incongruence.As

noted by Rivard

and

Huff, the costsofthe lack ofthese "systems hygiene"features are incurred by,

and

therefore arean

issue to,the central IS agent, while the benefits accrue to the end-user. Conflict inevitablyresults:

Some

users indicated that they did notdocument

their applicationsand

thatthey are the only

ones

who

know

how

the applicationswork.

However,

thisand

other secuntyand

validity issues, such as the lack of audit trails,were

mentioned

by only7.8%

of the respondents,whereas

DP

professionalswere

quick to point to these as

major

problem

areas. (Rivardand Huff

(1985), p.22

Other

related concerns expressedby

DP

managers

included the lack ofproper

documentation,

audit trails,and

other operating controls...in userdeveloped

applications...any attempt to install rigid controls overUDA...

would

be self-defeatingand

probably impossible toimplement.

..Unfortunately, all such effortswork

against theprimary

criticalsuccess factor of

UDA:

the reduction ofdevelopment

time for smaller-scale,user oriented applications. (Rivard

and Huff

(1985), p. 101)The

lack of these features introduces riskto the central IS group,who

may

be

calledupon

to take over operational responsibility forthe end-user

developed

systems. Insummary,

these oft-cited deficiencies of

EUC-developed

systems are quite readily explained byself-interested behavior

on

the part ofthe principalsand

agents intheEUC

systemsdevelopment

process.C.

Administration

The

activities inZmud's

(1984) administrative categoryencompass

those activities thatconstituteoverhead and

thatprovide long-term benefits, such as capital plarming,budgeting

and

standardsdevelopment.

Many

of the empiricallyrecorded

differenceshave

been

in such activities, particularly those thatmay

be

unobserved by

users. Insome

cases, the activitiesmay

be observed by

users, but are lessvalued bythem

thanby

the ISdepartment.

The

agency

model

leads to the following proposition:P4:

Goal incongruence between

the end-user organizationand

the firm as represented bycentral IS v,i\\

cause

EUC

systems to be biasedtowards

shortterm

goals,which

may

be sub-optimal for the firm.

The

EUC

literature has long recognized that end-user developers are often in conflictwith central IS.For example,

considerthis typicalquote

from an

end-userdeveloper:

"When

you develop

applications yourself,you

are theone

who

decideswhat

isimportant.

With DP,

what

is important foryou

is not importantforthem"

(Rivardand

Huff

(1988) pp. 559).The

essential tension in the relationshipseems

tostem from

theend-user's preoccupation with the short

term

resultsof delivering the systemsversus central IS'slonger

term view

ofhow

systemswillneed

tobe

integratedand

maintained. This conflict in orientation hasbeen

noted

in severalways

byRivard

and

Huff:23

Finally,

because

usersspend

little timeon

documentation

and

other"DP

hygiene" factors, additional resources are saved (although the longer-term

cost ofsuch shortcuts

may

welloutweigh

the savings achieved)." (Rivardand

Huff

(1985),p. 101).Others,

however,

recognized that the cost of the application theydevelop

may

notbe lower

for the organization as a whole.Because

of their lack ofexpertise, users

may

takemuch

longer thanDP

professionals todevelop

an

application,

and

theprogram

itselfmay

be

less efficient, less welldocumented,

lesswell tested, etc." (Rivardand Huff

(1988), p.559)Problems

with integratinguserdeveloped

systems withcentral IS systems or otheruser-developed

systemsgenerally surface laterwhen

there is adesire toexpand

thescope

ofsuccessfuluser

developed

systems, eitherthroughadded

functionality orthrough

making

itavailable to otherusers. Initially,

EUC

developersneed

only supportthenarrow

goals oftheir

department,

and

the designs ofsuch systemsmay

prove

tobe poor

platforms forexpansion.

This short

term

orientationmanifests itselfinanumber

ofways.One

piece of evidence is the differing attitudestoward

quality:A

relatedconcern

involved the accuracy of the informationproduced by

user-developed

application.As

Davis

has pointed out...,many

users areunable

or unwilling to apply strict quality assurance to the applications they develop, leading to the likelihood of conflicting values forsome

of thecompany's

key measures...Suchproblems

are especiallyworrisome

incases ofuser-developed

transaction processing applications, since these aremost

likely to

become

imbedded

in a department's operating procedures. Iftheyproduce

unreliable outputs, incorrect decisionsmay

be

made,

possiblycausing substantial

harm

to the firm. . . .Many

DP

managers

reporteda

sense of frustration; while such errors

would

clearlybe

the user's "fault," asdata processing professionals the

DP

managers

know

that theywould

also feel responsible.''^(Rivardand

Huff

(1985), p. 101)This observation also highlightsa

dilemma

facedby

the ISdepartment

in reconciling local goals with organizational concerns.A

second

commonly

observed

manifestationis the choice ofdevelopment

toolschosen by

EUC

developers, aswitnessedby

these observationsfrom

EUC

researchers:Otherwise, as

was

quite clearly occurring inmany

of the organizationswe

studied, users will stretch the available

end

user software products todo

jobsin a

manner

far less efficient than couldbe

done

with the appropriate24

It also helps to explain our observation that

many

userswould

use aparticular

programming

tool for a variety of different types of applicatioris,in

some

cases applications forwhich

the toolhad

clearly notbeen

designed.Rather

than investmore

time to learn to use anew

tool, userswould

make

do

withone

they alreadyknow

how

to usethough

not well suited for the application at hand. (Rivardand Huff

(1985), p. 100)Finally, it is suggested that it

may

notbe

in the best interests of the firm to have, forexample,

marketing

analysts developing systemsthat couldbe developed by

central IS ifthe

marketing

analysts, in so doing,end

up

notdoing

theirmarketing

tasks,but ratherbecome

involved in systemsdevelopment.

This over-involvementmay

be

due

to so-called"enrapturement"

wherein

the end-userbecomes

so involvedand

interestedwith thetechnology that

he

or she investsmore

time in the application than itsbusiness functionwould

otherwisewarrant(Waldman

(1987)). In ordertodetermine

themost

efficientapproach

from

the organization's perspective, the opportunity cost ofthe users' timeand

the general loss that occursdue

to the possibly greater total labor cost'° to the firm ofthistype of

development

is required.However,

usersmay

perceiveEUC

as personallymore

rewarding

interms

of acquiringcomputer

system-related skills toenhance

theirown

worth

in thejob

market

at theexpense

ofwhat

themanagement

ofthe organizationmight

prefer.Therefore, a short

term

orientationon

the part ofEUC

developers isseen throughmany

examples, includingdocumentation,

testing, integration, data integrity, tool choice,and

task selection. This behavioris entirely consistentwith thatpredictedby

theagency

model

ofEUC.

D.

Operations/Technical

ServicesThe

thirdand

final category involvesoperationsand

support ofactivities crucial to the successful continued operation ofthe IS function.For example,

such activities asmachine

operation,hardware maintenance,

systems softwaremaintenance, and

databasesupport are included here.