Direct and Indirect Effects of Index ETFs on Spot-Futures Pricing and Liquidity : Evidence from the CAC 40 Index

42

0

0

Texte intégral

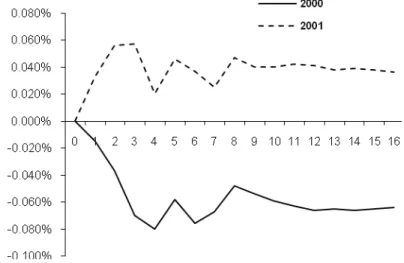

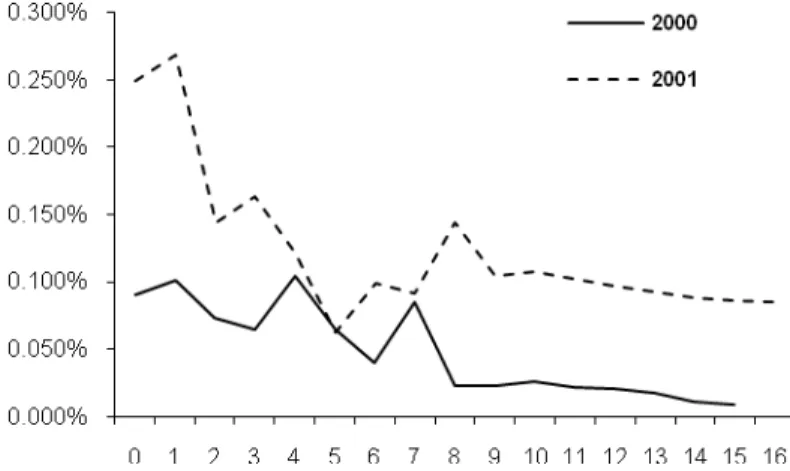

Figure

+3

Documents relatifs