© Maryse Mayer, 2021

L'élaboration des planifications fiscales : une

perspective relationnelle. Des représentations

médiatiques aux interactions du fiscaliste sur le terrain

Thèse

Maryse Mayer

Doctorat en sciences de l'administration

Philosophiæ doctor (Ph. D.)

ii

Résumé

Comment une planification fiscale s’articule-t-elle au fil des relations avec ses parties prenantes? Comment les fiscalistes parviennent-ils à se sentir à l’aise à propos des planifications fiscales qu’ils élaborent dans les multiples zones grises qui caractérisent leur pratique? En m’attardant aux processus par lequel s’élaborent les planifications fiscales, mon objectif avec cette thèse est d’illustrer, au fil de mes trois articles, comment la prise en compte des aspects relationnels permet d’éclairer certaines zones d’ombres laissées par d’autres perspectives dans la littérature académique à ce jour.

C’est à vol d’oiseau que j’ai amorcé ma trajectoire doctorale, avec un premier article très macro dans lequel je m’attarde aux normes sociétales qui façonnent la frontière entre les pratiques fiscales acceptables et inacceptables, basé sur la représentation médiatique des planifications fiscales. J’ai ensuite voulu plonger à un niveau beaucoup plus micro avec une série d’entrevues sur le terrain, pour mes deuxième et troisième articles, en m’intéressant à la perspective des fiscalistes en cabinet. J’y examine leurs interactions dans le processus décisionnel qui mène à l’élaboration des planifications fiscales : avec leur client, dans le cas du deuxième article, et avec leurs pairs lors de consultation informelle, pour mon troisième article.

iii

Table des matières

Résumé ... ii

Remerciements ... v

Avant-propos ... ix

Introduction ... 1

Article 1 The media representation of LuxLeaks: A window onto the normative dynamics of tax avoidance from a socio-legal perspective ... 11

Résumé ... 11

Abstract ... 11

1. Introduction ... 12

2. Positioning in the academic literature ... 16

3. Conceptual framework ... 17 3.1 Baier (2013) ... 17 3.2. Fairclough (1995, 2003) ... 18 4. Methodological considerations ... 20 4.1. Background ... 20 4.2. Selection of articles ... 20 4.3. Analysis ... 22

4.4. Coding and classification of data ... 23

5. Analysis... 23

5.1. The imperative dimension ... 24

5.2. The implementation dimension ... 30

6. Discussion ... 32

6.1. Influence of social norms on legal norm ... 34

6.2. Influence of social norms on multinational tax practices (without changing the legal norm) ... 36

7. Conclusion ... 39

References ... 41

Appendix 1: Articles analyzed ... 47

Article 2 Tax partners’ shared approach to decision-making in tax planning: How it takes two to tango ... 54

Résumé ... 54

Abstract ... 54

1. Introduction ... 55

2. Positioning in the literature ... 57

3. Theoretical lens ... 59

4. Methodology ... 63

4.1 Participants ... 64

4.2 Interview preparation ... 64

4.3 The interview process ... 65

iv

5. Analysis ... 67

5.1 The “balancing act” ... 67

5.2 Initial stage: sharing of information and views ... 70

5.3 Deliberation ... 79

5.4 Monitoring (post-decision) ... 81

Shared decision-making: An overview ... 82

6. Discussion ... 83

7. Conclusion ... 89

References ... 91

Appendix 1: Examples of interview questions ... 95

Appendix 2: Summary of the codes ... 96

Article 3 « Fly alone, die alone » : La face cachée du clan en planification fiscale ... 98

Résumé ... 98

Préambule ... 99

1. Introduction ... 99

2. Positionnement dans la littérature ... 103

3. Lentille théorique ... 105

3.1 Berger et Luckmann (1966) ... 105

3.2 Confort... 106

4. Méthodologie ... 107

4.1 Participants ... 108

4.2 Préparation des entrevues ... 108

4.3 Déroulement des entrevues ... 110

4.4 Analyse des données ... 111

5. Analyse ... 112

1) Consulter réconforte techniquement ... 113

2) Consulter me conforte de ma place dans le clan (je consulte car je me sens redevable) ... 119

3) Consulter me conforte à l’égard des autres membres du clan (je m’attends à ce que les autres consultent) ... 122

6. Discussion ... 126

7. Conclusion ... 132

Bibliographie ... 133

Annexe 1 : Exemples de question d’entrevue ... 137

Annexe 2 : Codage NVivo ... 138

v

Remerciements

Le doctorat est une étrange aventure; il s’agit d’un projet extrêmement solitaire qui pourtant, je doute, ne puisse aboutir sans être bien entouré. Dans mon cas, j’ai eu la chance d’être accompagnée par la « crème de la crème », non seulement sur le plan technique mais aussi humain. Je dois beaucoup à chacune de ces personnes, que je respecte profondément. J’espère être en mesure de « redonner au suivant » comme ils ont su le faire à mon égard. En attendant, je tiens ici à les remercier plus particulièrement.

D’abord, si mon doctorat m’a paru comme un long fleuve tranquille, il faut dire que le passage de ma carrière précédente aux études doctorales a été, pour sa part, des plus chaotiques. J’exagère à peine en racontant qu’un bon matin, je me suis levée en décidant (instinctivement?) que c’était terminé : je quittais le cabinet, mon poste d’associée si durement « gagné » et l’adrénaline des transactions internationales, pour faire « autre chose ». Et surtout, prendre soin de ma petite puce de deux ans. Un grand saut dans le vide sans parachute. Un immense vertige. Deux personnes bien spéciales ont à ce moment croisé ma route, sans qui l’aventure doctorale n’aurait simplement jamais pris forme :

Nicole Prieur, mon mentor, une des meilleures professeures que j’ai eues, mais surtout celle sans qui je ne me serais jamais lancée dans le vide. Retourner aux études « à mon âge »? Je ne voulais même pas y penser. C’est mal connaître le pouvoir de persuasion de Nicole. Même si je n’ai pas aimé être confrontée à ses idées, force est de constater qu’elle avait raison (évidemment).

Caroline Lambert, une chercheure dont l’énergie est contagieuse, qui a allumé chez moi l’étincelle de la recherche terrain, qualitative, au fil d’une conversation par hasard.

Quelques mois plus tard, j’avais démissionné du cabinet, vendu la maison et ma petite famille et moi déménagions à Québec! Il ne restait qu’à faire le doctorat en question… À cet égard, je dois beaucoup aux personnes suivantes, que je remercie sincèrement:

Yves Gendron, mon directeur : le doctorat m’a semblé un long fleuve tranquille et je soupçonne fortement que ce soit grâce à son doigté. Il s’agit d’un tour de force lorsque je constate l’ampleur du gouffre qui séparait nos deux univers au départ. Directement sortie du monde des « Big Four », je me souviens encore de nos premières rencontres où j’avais le réflexe de parler le plus rapidement possible pour éviter qu’il ne charge trop de son temps à mon « WIP »… L’anecdote en dit long sur l’ampleur de la transition qui m’attendait. Il faut aussi préciser que je me spécialisais, en cabinet, dans le genre de pratiques fiscales ouvertement critiquées par le courant d’études dans

vi

lequel Yves s’inscrit. Il a pourtant su composer avec tout ce qu’impliquait mon cheminement (et mes multiples identités paradigmatiques!) avec beaucoup de patience et de délicatesse et ce, sans jamais m’imposer sa vision de la « réalité ». Sa grande curiosité et son ouverture d’esprit font sûrement partie de sa « recette »… D’un calme déstabilisant, il a aussi dû s’adapter à l’étudiante impatiente, têtue, sur-planificatrice, un peu trop enthousiaste et verbomoteur que je suis. Il est parvenu à créer les conditions idéales en trouvant l’équilibre délicat entre mon besoin d’autonomie et de supervision. Enfin, sans doute l’aspect le plus important pour moi : il a accepté mon choix de prioriser ma famille par rapport au doctorat en respectant mon rythme de travail. Merci, vraiment, je ne pouvais aspirer à un meilleur guide.

Marion Brivot et Michèle Rodrigue, les membres de mon comité de thèse : je me considère très privilégiée d’avoir pu bénéficier de la rétroaction de chercheures de leur trempe pour ma thèse. Ces grandes dames sont surtout devenues des modèles pour moi, par leur rigueur, leur énergie contagieuse, leur générosité et leur façon de ne jamais me faire sentir imposteur dans ce nouveau monde où j’ai pourtant tout à apprendre. Leur présence rassurante m’a donné confiance et permis de trouver tranquillement ma place. Un peu comme des étoiles, je savais qu’elles étaient là, même quand je ne les voyais pas.

Lynne Oats, une pionnière de la recherche fiscale qualitative, pour les échanges stimulants lors de ma visite au Royaume-Uni et sa générosité, même à distance.

Claire-France Picard, qui a joué un grand rôle dans mon parcours (et certainement le plus polyvalent!) lorsqu’est venu le temps de transposer la théorie en pratique. Méthodologie, rôle du chercheur dans la société, petites angoisses du moment; je ne l’ai pas épargnée avec mes questions. Ses idées constructives, son écoute, son enthousiasme contagieux, son sens de l’humour et sa façon – sans filtre – d’échanger ont clairement contribué à ce que je m’approprie tranquillement, à ma façon, mon nouveau rôle de chercheure. En cours de route, j’ai aussi découvert une amie que j’apprécie énormément.

Les membres du corps professoral de l’École de comptabilité qui m’ont supportée, que ce soit par leur enseignement ou lors de différents événements, pour leur curiosité et leur intérêt pour ma recherche. À défaut de tous pouvoir les nommer, un merci particulier à Jean-François Henri, Carl Brousseau et Mélanie Roussy. Sur un ton plus personnel, je ne saurais passer sous silence le rôle

vii

de Jean Bédard et de sa joyeuse tribu (Martine et les filles), une famille inspirante, pour (entre autres) l’accueil chaleureux dans ma région adoptive.

Les différents organismes qui m’ont soutenue financièrement : le Conseil de recherches en sciences humaines du Canada, la Fondation de l’ordre des CPA du Québec, l’École de comptabilité de l’Université Laval ainsi que Rachel et Jean-Marie Gagnon.

Les associés en cabinet qui ont très généreusement accepté de participer à mon projet, sans qui ma thèse n’aurait pu se concrétiser.

Ann Gallon, traductrice-fée des mots, pour sa minutie et sa rigueur.

Mes collègues, ami(e)s doctorant(e)s :

Janie Bérubé, ma fidèle collègue doctorante et amie. Bien plus que la parfaite compagne de voyage, elle m’a surtout enseignée, sûrement à son insu, l’attitude « just do it » qu’elle maîtrise si bien : difficile à décrire, il s’agit d’un mélange de pragmatisme, de discours anti-victimisation et d’optimisme à toute épreuve, doublé d’une efficacité redoutable. J’ai tant apprécié partager et discuter au fur et à mesure que nous découvrions ensemble en quoi consistait le doctorat… Une de ces rencontres qui aura teinté l’ensemble de mon parcours et ma façon de voir les choses. J’espère que nos routes se recroiseront.

Till-Arne Hahn, mon très précieux « tax buddy », pour tous les échanges intéressants et le partage d’expérience, avec qui j’espère collaborer dans un avenir rapproché.

Baptiste, toujours disponible pour apaiser mes petites crises existentielles : pour son écoute exceptionnelle, son sens de l’humour, sa bonne humeur imperturbable (malgré sa perception…), sa présence rassurante et le plaisir de discuter plein-air pour aérer nos esprits.

Cynthia, pour sa générosité et les discussions travail-famille que j’ai tant appréciées. Éliane, pour sa présence motivante et nos discussions sport-étude-nutrition-méthodologie-environnement. Stéphanie, avec qui je partage les repères de mon ancienne carrière, pour son support même à distance et nos échanges qui me sont bien précieux.

viii

Enfin, sur une note plus personnelle : si le doctorat m’a paru un long fleuve tranquille, c’est aussi (surtout?) grâce à mon « noyau », mon entourage rapproché qui a « subi » cette traversée à mes côtés sans pour autant l’avoir choisie. Merci d’être là:

Louis-Philippe, mon roc, mon complice des 21 dernières années, avec qui tous les projets deviennent possibles – même ceux qui donnent l’impression de repartir à zéro et qui impliquent de « s’évader en région ».

Megan, mon petit « Bouddha » qui me permet de tout relativiser, qui est passée d’un bébé en plein « terrible two » à une pétillante fillette de sept ans, le temps d’un doctorat.

Mes chers parents, qui m’ont outillée de tout ce qu’il faut – et vraiment beaucoup plus – pour avoir confiance en moi et réaliser tous mes projets.

Ma chère sœur, Véro, maître dans l’art de dédramatiser. Mon cher beau-frère Fred, entre autres pour sa métaphore du combat de boxe.

Mes ami(e)s, qui étaient là, surtout lorsque mon « saut dans le vide » me donnait un peu le vertige. Un merci bien spécial à mes amies et ex-collègues Josiane Gagnon et Jodi Kelleher, qui ont compris mes choix.

ix

Avant-propos

Ma thèse comporte trois articles. Le premier, « The media representation of LuxLeaks: A window onto the normative dynamics of tax avoidance from a socio-legal perspective », a été soumis à la revue Critical Perspectives on Accounting en août 2018. La lettre éditoriale de deuxième ronde a été reçue le 6 mars 2020, faisant état d’une invitation à resoumettre l’article une fois retravaillé. Mon deuxième article, qui s’intitule « Tax partners’ shared approach to decision-making in tax planning: How it takes two to tango », a pour sa part été soumis à la revue Contemporary Accounting Research en octobre 2020. Enfin, le troisième article, « « Fly alone, die alone » : La face cachée du clan en planification fiscale », est quant à lui en cours de traduction; je compte ensuite le soumettre à la revue European Accounting Review.

Quant à mon rôle à l’égard de ces trois études, j’en suis l’auteure principale pour en avoir effectué la collecte de données, l’analyse des résultats ainsi que la rédaction. Monsieur Yves Gendron en est le coauteur, pour son éclairage inestimable à chacune des étapes du processus et ses précieux commentaires lors de la révision des manuscrits.

1

Introduction

Les trois articles de ma thèse gravitent autour de l’incertitude entourant la planification fiscale, cette zone grise où le contribuable possède une certaine latitude (ex ante) quant à la façon de structurer ses transactions parmi un continuum d’options plus ou moins agressives, « as tax planning often involves ambiguous law, necessitating the exercise of professional judgment » (Hasseldine et Fatemi 2019, 303). L’élaboration de planifications fiscales est un terrain étonnamment sous-étudié empiriquement (Frecknall-Hughes et Kirchler 2015) comparativement à celui de la conformité fiscale. Pourtant, les fiscalistes disposent d’une toute autre marge de manœuvre décisionnelle lorsqu’ils doivent structurer une transaction aux fins fiscales, par rapport à la détermination du traitement fiscal après que cette transaction ait eu lieu, ce qui justifie d’autant plus que l’on s’intéresse au contexte de planification. Comment une transaction commerciale en vient-elle à être structurée, aux fins fiscales, d’une certaine manière? La question n’a rien d’anodin puisque la façon selon laquelle les décisions relatives aux planifications fiscales se prennent détermine en bout de piste la charge fiscale des contribuables et donc les fonds publics générés par le système d’imposition. C’est d’un angle relationnel que cette vaste problématique m’interpelle ici : comment une planification fiscale s’articule-t-elle au fil des relations avec ses parties prenantes? Ces dernières prennent une forme très macro dans mon premier article, où je m’attarde aux normes sociétales susceptibles d’influencer les planifications fiscales, ainsi qu’aux interrelations entre ces normes. À un niveau plus micro, mes deux autres articles portent, quant à eux, sur les interactions du fiscaliste avec son client (article 2) ainsi qu’avec ses pairs (article 3) dans le processus décisionnel qui mène à l’élaboration des planifications fiscales. Les paragraphes qui suivent en présentent un survol.

Une perspective relationnelle

D’emblée, il me faut préciser que j’étais très familière avec l’élaboration des planifications fiscales avant même d’entamer mon doctorat, d’un point de vue purement légal et technique, pour avoir travaillé durant de nombreuses années en tant que fiscaliste au sein d’un grand cabinet. Durant ma scolarité doctorale, j’ai découvert la recherche en comptabilité menée selon la perspective sociologique interprétative, et plus précisément la sous-lignée d’études qui considèrent la fiscalité comme une pratique relationnelle et sociale (Oats 2012). En situant l’élaboration des planifications fiscales dans leur contexte social, cette approche parvient à mettre en lumière certaines nuances, de même qu’un niveau de complexité des pratiques fiscales, qui résonnent beaucoup avec mon expérience professionnelle antérieure. Ceci explique d’ailleurs peut-être, du moins en partie, mon intérêt pour ce type de recherche. Par rapport à la littérature académique en fiscalité, la perspective

2

sociologique interprétative, embryonnaire quoiqu’en plein essor, permet ainsi de jeter un éclairage distinct sur les enjeux fiscaux que ne permettent pas les recherches menées en fonction d’autres perspectives (p.ex. économique, comportementale ou légale)1, par exemple en s’intéressant au « comment », à partir d’entrevues sur le terrain (plutôt que des données d’archives ou des expériences en laboratoire). C’est ce que j’espère avoir réussi à illustrer avec cette thèse qui, en ce sens, se veut un plaidoyer pour la prise en compte des aspects relationnels dans l’étude des pratiques fiscales. Je souhaite de cette façon approfondir l’étude du processus par lequel s’élaborent les planifications fiscales et influencer l’agenda des chercheurs. Dans les prochains paragraphes, j’explique comment j’ai décliné cette perspective relationnelle au fil de mes trois articles de thèse et j’y positionne brièvement ma recherche par rapport à la littérature.

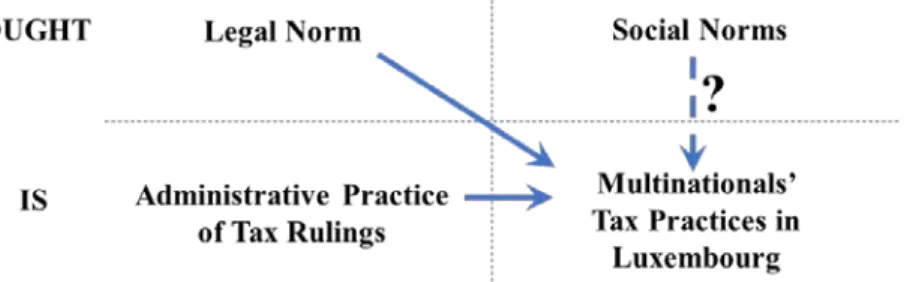

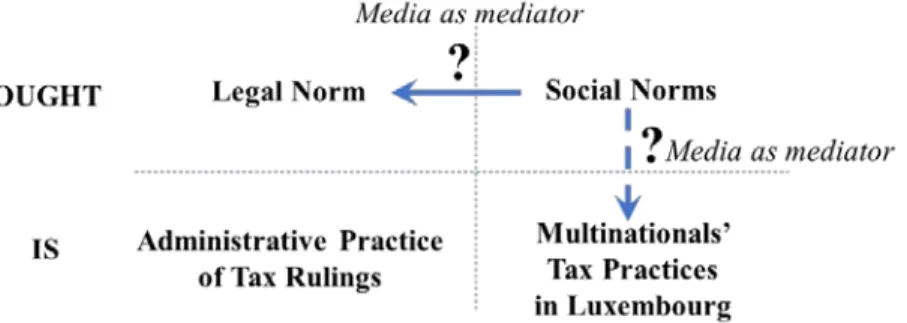

Les représentations médiatiques : un regard macro, socio-légal sur la planification fiscale Mon premier article a d’abord été pour moi l’occasion de me détacher par rapport à mon parcours professionnel précédant le doctorat, et surtout, de ré-apprivoiser mon objet d’étude. En effet, dès le départ, j’ai dû prendre un recul par rapport à ma pratique en cabinet et apprendre à re-considérer la planification fiscale avec mon nouveau chapeau de chercheure, d’un angle sociologique. J’ai donc choisi, pour ce premier article intitulé « The media representation of LuxLeaks: A window onto the normative dynamics of tax avoidance from a socio-legal perspective », d’examiner les planifications fiscales telles que perçues au-delà de « ma réalité » de praticienne, à l’extérieur de la firme. En analysant des représentations médiatiques touchant un « scandale » fiscal d’envergure, j’ai constaté comment un phénomène en apparence aussi technique que la planification fiscale peut effectivement faire l’objet de différentes représentations, de différentes « réalités » qui s’entrecroisent dans la presse écrite et, par ricochet, dans la société. Cette façon très macro d’envisager la planification fiscale a permis de faire ressortir diverses normes sociétales (légales et sociales), plus ou moins contradictoires, mobilisées par la presse pour façonner la frontière entre les pratiques fiscales acceptables et inacceptables. Ce constat m’amène à poser la question suivante. Comment le problème de l’évitement fiscal (et conséquemment sa solution) peut-il être délimité sans que l’on ne s’entende, en tant que société, sur la norme, le critère à utiliser pour l’évaluer? Voilà la piste de réflexion centrale que suscite mon analyse. J’y discute de la pertinence d’explorer les relations entre les normes légales et sociales afin de faire avancer le débat sur l’évitement fiscal.

1Voir notamment Boll (2014) pour un survol des différentes perspectives en recherche fiscale, de même que la

3

Pour ce faire, je suggère d’importer à la fiscalité les travaux de Baier (2013), qui s’inscrivent dans la littérature en sociologie du droit. Cette idée de s’inspirer des études socio-légales m’est venue après avoir constaté que la compréhension de l’évitement fiscal qu’offre la littérature académique fiscale à ce jour est très compartimentée. En effet, la littérature considère généralement le sujet soit d’un angle légal/fonctionnaliste2, soit d’un angle moral/social3, avec peu d’interaction entre ces deux lignées de recherche. Or, mes motivations à user des travaux de Baier (2013) tiennent justement à son intérêt pour l’interdépendance, la dynamique entre les normes légales et sociales. À mon sens, la perspective normative de Baier (2013) « which centers on normative issues relating to the law’s operations in society (Banakar 2013) », permet de mettre au jour des questions socio-légales susceptibles de réconcilier les deux dimensions jusqu’ici examinées séparément, afin d’élargir et de nuancer la compréhension de l’évitement fiscal. C’est ce que j’espère être parvenue à illustrer dans ce premier article. Enfin, je note avec du recul que cette conceptualisation socio-légale était peut-être pour moi une manière d’effectuer une transition professionnelle en provoquant la rencontre du monde légal, dans lequel j’avais évolué avant le doctorat, à la perspective sociologique à laquelle je m’intéressais maintenant. Après ce premier article, où j’aborde les planifications fiscales de manière plutôt conceptuelle et très macro, en m’attardant aux normes sociétales susceptibles de les façonner, je suis retournée au terrain qui m’était le plus familier pour étudier la perspective des acteurs au cœur de ma problématique.

Retour au terrain : les interactions du fiscaliste dans l’élaboration des planifications fiscales C’est à un niveau beaucoup plus micro que j’ai ensuite décliné la perspective sociologique pour étudier l’élaboration des planifications fiscales, en interviewant les fiscalistes en cabinet, « key players (…) in an increasingly complex world of regulation » (Frecknall-Hughes et Kirchler 2015, 290). Comment parviennent-ils à se sentir à l’aise à propos des planifications fiscales qu’ils recommandent à leurs clients dans les multiples zones grises qui caractérisent leur pratique? Quelles interactions interpersonnelles y entrent en ligne de compte, et comment? Mon objectif était de mieux comprendre les processus derrière l’élaboration des planifications fiscales, dans leur contexte social, tels que les perçoivent les fiscalistes.

2 Par exemple, voir Hanlon et Heitzman (2010) pour une revue de la littérature fiscale de perspective

fonctionnaliste économique.

3 Un nombre croissant d’études des plus diversifiées ont été publiées sous cet angle dans le but de mieux

comprendre l’évitement fiscal. Par exemple, certains auteurs interprètent l’évitement fiscal comme un enjeu de responsabilité sociale (p. ex. Ylonen et Laine 2015, Lanis et Richardson 2015), alors que d’autres le considèrent d’après des critères liés à l’éthique (p.ex. Payne et Raiborn 2018) ou à la philosophie (p.ex. West 2018).

4

Du côté de la littérature, on en connait encore bien peu sur la façon selon laquelle les fiscalistes composent, dans l’action (plutôt que basé sur des expériences en laboratoire, par exemple), avec la marge de manœuvre dont ils disposent lorsqu’ils élaborent une planification fiscale. À cet égard, Cloyd (1999) reconnait d’ailleurs le défi, pour la recherche comportementale sur la prise de décision et le jugement, de parvenir à comprendre l’environnement du fiscaliste et d’élaborer des questions de recherche ancrées dans leur quotidien. Il est également surprenant de constater à quel point les interactions impliquées dans les processus décisionnels derrière les planifications fiscales sont sous-étudiées. En effet, la lignée d’études relative au jugement et à la prise de décision des fiscalistes, pourtant bien développée aux États-Unis (Hasseldine et Fatemi 2019), porte surtout sur la prise de décision au niveau individuel4 ou encore dans le cadre d’un processus de révision hiérarchique5 (Bobek et al. 2019). En ce qui concerne la littérature fiscale de perspective sociologique, on y a surtout abordé les planifications fiscales pour les critiquer, sans grand soutien empirique (p.ex. Sikka et Hampton 2005, Sikka 2008). En choisissant de retourner sur le terrain des cabinets, j’espérais donc contribuer à jeter les bases qui permettraient de mieux comprendre les interactions derrière le processus qui mène à l’élaboration des planifications fiscales. Comme le remarquent à cet égard Malsch et Salterio (2016, 17), « by going deep into the field and collecting data about « real » practices, field researchers have the potential to expose new research questions for experimental or archival researchers. » Décrypter les pratiques fiscales sur le terrain – ici celles d’associés typiquement difficiles d’accès – offre un point de vue privilégié pour examiner « the actual human interactions, meanings, and processes that constitute real-life organizational settings » (Gephart 2004, 455). J’ai donc effectué une série d’entrevues auprès de 40 fiscalistes en cabinet, à l’été et l’automne 2018. Mes résultats illustrent comment l’élaboration des planifications fiscales est imbriquée dans les relations sociales, que ce soit avec le client (article 2) ou au sein du clan dans lequel évolue l’associé (article 3). Les paragraphes qui suivent en présentent un survol.

Le processus décisionnel entre le fiscaliste et son client

Pour mon deuxième article, « Tax partners’ shared approach to decision-making in tax planning: How it takes two to tango », je me suis concentrée sur les interactions qui interpellaient le plus les participants lorsqu’ils s’exprimaient en entrevue à propos du processus décisionnel menant à une planification fiscale, soit celles avec le client. Le point de départ de cette étude repose sur l’idée que le fiscaliste et son client sont interdépendants (Mills et al. 1983), l’un possédant les compétences techniques poussées pour maîtriser les règles fiscales complexes, l’autre, les connaissances relatives

4 Par exemple : Kadous et al. 2008, Ashton et Roberts 2011, Magro et Nutter 2012. 5 Par exemple : Hatfield 2001, Barrick et al. 2004.

5

au contexte précis auquel la loi est appliquée (Morris et Empson 1998). Dans ce contexte, comment les fiscalistes perçoivent-ils leur rôle dans le processus décisionnel qui mène à une planification fiscale avec leur client? Voilà la question de recherche que j’ai choisi d’examiner dans cette deuxième étude.

Pour ce faire, j’emprunte à la théorie sociale du monde médical la conceptualisation de la décision partagée de Charles et al. (1997, 1999), notamment pour la réflexion qu’elle permet quant aux rôles et pouvoirs respectifs des parties dans le processus « co-décisionnel ». Mes résultats illustrent que les associés poursuivent deux objectifs difficiles à concilier lorsqu’ils élaborent une planification avec leur client. D’un côté, ils sont préoccupés de préserver l’autonomie décisionnelle de leur client alors que de l’autre autre côté, ils se voient aussi responsables vis-à-vis de leur client, ce qui les incite à s’ingérer davantage dans le processus décisionnel dans certaines circonstances. Les associés sont ainsi inconfortables dans un rôle paternaliste ou informatif, aux deux extrêmes du spectre interactionnel de la prise de décision de Charles et al. (1999). L’analyse détaille comment l’approche décisionnelle partagée, dont les étapes sont conceptualisées par Charles et al. (1999), peut permettre aux fiscalistes de se rassurer quant à leur capacité à réduire l’asymétrie informationnelle entre eux et leur client tout en manœuvrant, au quotidien, de façon à maintenir ce « balancing act » délicat. Les résultats mettent en lumière la dynamique interactionnelle qui permet aux fiscalistes, souvent, de se conforter et de s’adapter tout au long du processus décisionnel avec le client, de manière itérative. Plus précisément, mon analyse indique qu’ils adaptent non seulement leurs recommandations mais aussi leur niveau de participation dans le processus décisionnel, selon l’autonomie décisionnelle de leur client telle qu’ils la perçoivent au fil de l’interaction. Le fiscaliste s’ajusterait ainsi d’un client à l’autre, mais également en cours de processus décisionnel pour un même client.

Conceptualiser ainsi comment le fiscaliste aborde le processus décisionnel avec son client permet d’apporter certaines nuances susceptibles de jeter les bases pour susciter de nouvelles questions de recherche. Par exemple, la relation entre certaines caractéristiques du client et les recommandations du fiscaliste a été étudiée dans la littérature expérimentale. Toutefois, l’idée que certaines situations soient en mesure d’affecter le niveau de participation du fiscaliste dans le processus décisionnel n’a, à ma connaissance, jamais été explorée à ce jour. Or, d’après mes données, le fiscaliste s’intègre dans le processus décisionnel de manière plus marquée auprès de son client (1) s’il perçoit qu’une planification est potentiellement trop risquée ou complexe pour le client ou (2) s’il ne parvient pas à se conforter que le client comprend les options envisagées. Il s’agit d’une dimension intéressante pour comprendre comment se déploie le rôle du fiscaliste, dans l’action, au niveau de l’adaptation du

6

fiscaliste par rapport aux préférences du client. Ainsi, le fiscaliste s’adapterait à la tolérance au risque qu’il perçoit chez le client mais pas à n’importe quel prix : il s’y adapterait à moins que cette tolérance lui semble trop élevée, ou encore lorsque qu’il estime que le client n’en comprend pas les tenants et aboutissants. Ces résultats contredisent, en partie, les travaux qui reconnaissent, quoiqu’en contexte de conformité fiscale, l’effet de la préférence du client quant au niveau de risque sur la recommandation du fiscaliste (p.ex. Tan 2011, Schisler 1994). Cet effet serait, d’après mes résultats, assujetti à cette « boundary condition ». Il s’agit d’une nuance importante aux travaux expérimentaux publiés à ce jour, dans l’ensemble encore mitigés, quant à savoir jusqu’à quel point le fiscaliste suit le niveau de risque souhaité par le client.

Le fiscaliste et la consultation informelle au sein de son clan

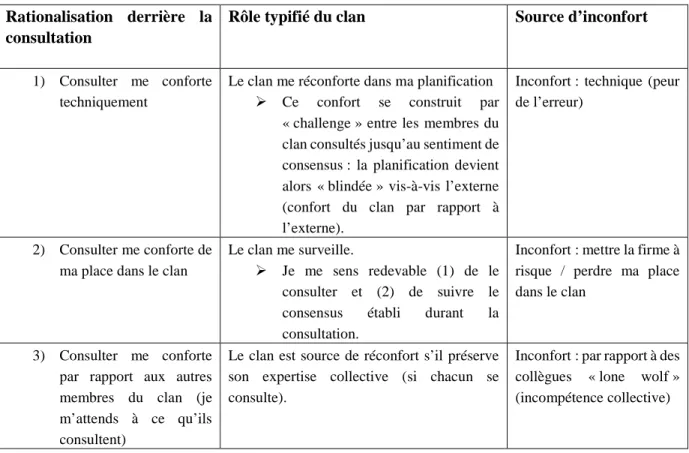

Après m’être intéressée au processus décisionnel du fiscaliste et de son client, je me suis attardée, pour mon troisième article, « « Fly alone, die alone » : La face cachée du clan en planification fiscale », à la consultation informelle entre pairs. Il s’agit d’une autre interaction, omniprésente dans les entrevues, qui entre en ligne de compte lorsque le fiscaliste tente de se faire une tête à propos d’une planification fiscale. Malgré toutes les ressources techniques des grandes firmes, la consultation informelle semble effectivement la norme chez les participants interviewés et ce, sans qu’elle ne soit exigée ou balisée par un mécanisme de contrôle formel. Comment les fiscalistes perçoivent-ils leurs collègues lorsqu’ils tentent de se faire une tête dans les multiples zones grises? Et comment font-ils sens de cette norme de consultation informelle à laquelle ils s’adonnent? Enfin, comment en sont-ils venus à tenir cette pratique pour acquise, comme étant la « norme » et comment celle-ci se maintient-elle? Ces questions me semblent essentielles pour mieux comprendre l’élaboration des planifications fiscales dans leur contexte social. Je les ai abordées avec la question de recherche qui suit : quels sont les processus qui participent à la (re)production de la norme informelle de consultation entourant la planification fiscale et comment opèrent-ils? La littérature fiscale est encore ici peu loquace à ce sujet. On sait néanmoins – et depuis longtemps – que les décisions fiscales en situation ambiguë sont généralement prises en consultant d’autres d’individus (Carnes et al. 1996). On sait aussi, d’après Doyle et al. (2013), que la socialisation en contexte professionnel affecterait bel et bien les fiscalistes. Dans la littérature sur les firmes de services professionnels, la recherche sur la consultation informelle entre pairs, bien qu’encore embryonnaire, est un peu plus développée du côté de l’audit. Trotman et al. (2015, 57), dans leur revue de littérature expérimentale sur le sujet, soulignent que « consultation with other auditors (i.e., advice seeking and giving) is common and can reduce uncertainty about difficult decisions and help auditors defend a position to various stakeholders. » Qu’en est-il des fiscalistes, sur le terrain, lorsqu’ils élaborent une planification fiscale?

7

Mes résultats mettent en lumière le rôle du clan derrière l’élaboration des planifications fiscales, ainsi que la notion de confort, par laquelle la relation entre l’associé et son clan s’articule. Plus précisément, en mettant en exergue trois processus de rationalisation à l’égard de la consultation informelle, j’explique comment ces processus impliquent des rôles typifiés du clan, qui auraient ici un effet de contrôle en définissant un modèle prédéfini de conduite (Berger et Luckmann 1966) chez les associés. Ces rôles complémentaires du clan – qui, à la fois, réconforte et contraint – participeraient à ce que la norme informelle de consultation « colle ensemble » et se maintienne. En ce sens, mes résultats illustrent empiriquement comment la notion de clan, développée dans la littérature surtout dans un contexte de gouvernance, peut aussi opérer plus directement dans la production de l’expertise par l’entremise d’une « réalité partagée » qui sous-tend une norme informelle quant à la consultation entre pairs. Ainsi, considérer la consultation informelle sous la perspective sociale constructiviste permet de mieux comprendre comment l’élaboration de planifications fiscales est imbriquée dans les relations sociales au sein de la firme. Il s’agit de l’un des principaux arguments de cette étude, qui couvre en ce sens un angle mort de la recherche fiscale produite à ce jour sur la planification fiscale.

8 Bibliographie

Ashton, R., et M. Roberts. 2011. Effects of dispositional motivation on knowledge and performance in tax issue identification and research. The Journal of the American Taxation Association 33 (1): 25– 50.

Baier, M. 2013. Social and legal norms: Towards a socio-legal understanding of normativity. Surrey, England: Ashgate.

Banakar, R. 2013. Can legal sociology account for the normativity of law? In Social and legal norms. Towards a socio-legal understanding of normativity, ed. M. Baier, Surrey, England: Ashgate, 15–38.

Barrick, J. A., C. B. Cloyd, et B. C. Spilker. 2004. The influence of biased tax memoranda on supervisors’ initial judgments in the review process. The Journal of the American Taxation Association 26 (1): 1–19.

Berger, P. et T. Luckmann. 1966. La Construction sociale de la réalité. Paris, France: Armand Colin. Bobek, D. D., D. W. Dalton, A. M. Hageman, et R. R. Radtke. 2019. An experiential investigation of tax professionals' contentious interactions with clients. The Journal of the American Taxation Association 41 (2): 1–29.

Boll, K. 2014. Shady car dealings and taxing work practices: An ethnography of a tax audit process. Accounting, Organizations and Society 39 (1): 1–19.

Carnes, A. G., G. B. Harwood, et R. B. Sawyers. 1996. A comparison of tax professionals’ individual and group decisions when resolving ambiguous tax questions. Journal of the American Taxation Association 18 (2): 1–18.

Charles, C., A. Gafni, et T. Whelan. 1997. Shared decision-making in the medical encounter: What does it mean? (or it takes at least two to tango). Social Science & Medicine 44: 681–692.

Charles, C., A. Gafni, et T. Whelan. 1999. Decision-making in the physician-patient encounter: Revisiting the shared treatment decision-making model. Social Science & Medicine 49: 651–661. Cloyd, C. B. 1999. Discussion of contextual features of tax decision-making settings. The Journal of the American Taxation Association 21 (S-1): 74–77.

Doyle, E., J. F. Hugues, et B. Summers. 2013. An empirical analysis of the ethical reasoning of tax practitioners. Journal of Business Ethics 114 (2): 325–339.

Frecknall-Hughes, J., et E. Kirchler. 2015. Towards a general theory of tax practice. Social & Legal Studies 24 (2): 289–312.

Gephart, R. P. 2004. Qualitative research and the Academy of Management Journal. Academy of Management Journal 47 (4): 454–462.

9

Hanlon, M. et S. Heitzman. 2010. A review of tax research. Journal of Accounting and Economics 50 (2–3), 127–178.

Hasseldine, J., et D. Fatemi. 2019. Tax practitioner judgements and client advocacy: The blurred boundary between capital gains vs. ordinary income. EJournal of Tax Research 16 (2): 303–316. Hatfield, R. 2001. The effect of staff accountant objectivity in the review and decision process: A tax setting. The Journal of the American Taxation Association 23 (1): 61–74.

Kadous, K, A. Magro, et B. Spilker. 2008. Do effects of client preference on accounting professionals’ information search and subsequent judgments persist with high practice risk? The Accounting Review 83 (1): 133–156.

Lanis, R., et G. Richardson. 2011. The effect of board of director composition on corporate tax aggressiveness. Journal of Accounting and Public Policy 30 (1): 50–70.

Magro, A., et S. Nutter. 2012. Evaluating the strength of evidence: How experience affects the use of analogical reasoning and configural information processing in tax. The Accounting Review 87 (1): 291–312.

Malsch, B., et S. E. Salterio. 2016. Doing good field research: Assessing the quality of audit field research. Auditing: A Journal of Practice & Theory 35 (1): 1–22.

Mills, P.K., J. Hall, J. K. Leidecker, et N. Margulies. 1983. Flexiform: A model for professional service organizations. The Academy of Management Review 8 (1): 118–131.

Morris, T., et L. Empson. 1998. Organisation and expertise: An exploration of knowledge bases and the management of accounting and consulting firms. Accounting, Organizations and Society 23 (5): 609–624.

Oats, L. 2012. Tax as a social and institutional practice. In Taxation: A fieldwork research handbook, ed. L. Oats, Oxford, UK: Routledge, 3–8.

Payne, D. M., et C. A. Raiborn. 2018. Aggressive tax avoidance: A conundrum for stakeholders, governments, and morality. Journal of Business Ethics 147 (3): 469–487.

Schisler, D. L. 1994. An experimental examination of factors affecting tax preparers’ aggressiveness – A prospect theory approach. The Journal of the American Taxation Association 16 (2): 124–142. Sikka, P. 2008. Enterprise culture and accountancy firms: new masters of the universe. Accounting, Auditing & Accountability Journal 21 (2): 268–295.

Sikka, P., et M. P. Hampton. 2005. The role of accountancy firms in tax avoidance: Some evidence and issues. Accounting Forum 29 (3): 325–343.

10

Tan, L.M. 2011. Giving advice under ambiguity in a tax setting. Australian tax forum 26: 73–101. Trotman, K. T., T. D. Bauer et K. A. Humphreys. 2015. Group judgment and decision making in auditing: Past and future research. Accounting, Organizations and Society 47: 56–72.

West, A. 2018. Multinational tax avoidance: Virtue ethics and the role of accountants. Journal of Business Ethics 153 (4), 1143–1156.

Ylӧnen, M., et M. Laine. 2015. For logistical reasons only? A case study of tax planning and corporate social responsibility reporting. Critical Perspectives on Accounting 33, 5–23.

11

Article 1

The Media Representation of LuxLeaks:

A Window onto the Normative Dynamics of Tax Avoidance

From a Socio-Legal Perspective

Résumé

Comment les médias font-ils sens du phénomène complexe, opaque et controversé de l’évitement fiscal corporatif? Basés sur les représentations médiatiques du « LuxLeaks », une fuite médiatique d’envergure internationale, les résultats mettent en lumière une lutte discursive quant à la problématisation de l’évitement fiscal, où différentes normes sont mobilisées pour faire sens du phénomène, de manière floue et ambiguë. Comment peut-on circonscrire le problème de l’évitement fiscal (et conséquemment la solution) sans s’entendre sur la norme à utiliser pour l’évaluer? Dans le but de faire évoluer le débat, nous proposons de revoir certaines prémisses normatives en intégrant à la recherche fiscale la théorie socio-légale de Baier (2013), qui focalise sur l’interdépendance entre les normes légales et sociales, plutôt que de les considérer séparément. D’après cette conceptualisation, nous établissons la structure normative du LuxLeaks à partir des discours médiatiques pour réfléchir à l’évolution de la dynamique normative propre à l’évitement fiscal. Abstract

How do the media make sense of the complex, opaque and controversial phenomenon of corporate tax avoidance? Based on the media’s discursive representations of the international “LuxLeaks” news leak, we identify a discursive battle over tax avoidance problematization which reveals a peculiar normative dynamic. We find that the field of tax avoidance is characterized by a vague and highly ambiguous normative framework, as the media use very different norms to make sense of LuxLeaks. How can the problem of tax avoidance (and consequently its solution) be delimited if there is disagreement over which norm should be used to assess it? Our study then highlights the need to step back and (re)consider broader assumptions of “normativity” in relation to tax avoidance to advance the debate. We propose to import Baier’s (2013) socio-legal perspective on normativity into the tax realm, to better understand not just the relations between legal and social norms as separate normative systems but also their interdependence. Based on discursive insights from the press, we map out the normative structure specific to LuxLeaks, as conceptualized using Baier’s platform. To exemplify how this kind of conceptualization can nurture future research, we initiate a reflection on how normativity could evolve in the tax avoidance field, considering possible implications of the press representations analyzed.

12 1. Introduction

November 2012. A short news report, edited to Hollywood standards, is playing constantly on TV networks all over the world: it shows the European Head of the multinational company Google being questioned by the UK Public Accounts Committee about alleged tax avoidance:6

Q484 Chair [Margaret Hodge]: So you [Matt Brittin, Head of Google Europe] are minimizing your tax even though it is unfair to British taxpayers.

Matt Brittin: It is not unfair to British taxpayers. We pay all the tax you require us to pay in the

UK. We paid £6 million of tax last year.

Q485 Chair: We are not accusing you of being illegal; we are accusing you of being immoral.

(HM Revenue & Customs, 2012, p. 40).7

November 2014. International corporate tax avoidance is thrust back into the international media spotlight with some sensational headlines: “Top official in E.U. faces rising furor over tax” (NYT2), “Revealed: tax deals saving firms billions: Investigation uncovers Luxembourg role in avoidance on industrial scale” (G1).8 LuxLeaks, one of the biggest financial news leaks in history (Robinson 2016), was revealing the existence of hundreds of confidential arrangements (tax rulings) negotiated by the large accounting firms and their multinational clients with the Luxembourg government, allowing them to set up tax avoidance schemes. These schemes had been carefully concealed from the public (Dowling 2014), which was now finding out that such arrangements were apparently not confined to the Googles and Amazons of this world.

In a context of growing public awareness, tax avoidance is increasingly considered as more than just a technical matter; it is also a social and media phenomenon. Unlike tax evasion, tax avoidance complies with the letter of the law while contradicting the aim or spirit of the law.9 It is widely understood that opportunities for tax avoidance have largely arisen because the legislation has not

6 The term “tax avoidance” as used in this article refers to international corporate tax although we believe our

argument, with some adaptation, could be transposed into a non-international tax setting.

7 For the sake of consistency, we took the liberty of harmonizing the spelling of all quotations using American

English, even when the original quotation was written in British English.

8 In the rest of this article, the following references are used to indicate the newspaper sources: WSJ - Wall

Street Journal, NYT - New York Times, G - The Guardian, FT - Financial Times, T - The Times, F - Le Figaro,

and M - Le Monde. The articles we examined are listed in Appendix 1. We translated the quotations from French newspapers into English.

9 This is the generally accepted definition of the term, which echoes the following definition given by the

Organisation for Economic Cooperation and Development (OECD): “A term that is difficult to define but which is generally used to describe the arrangement of a taxpayer’s affairs that is intended to reduce his[/her] tax liability and that although the arrangement could be strictly legal it is usually in contradiction with the intent of the law it purports to follow” (OECD 2018(a)).

13

evolved at the same pace as globalization (OECD 2013). This situation creates technical “grey areas” where tax avoidance is possible, giving multinationals some latitude as to the aggressiveness of their tax policies. The existing room for maneuver is precisely what makes the tax avoidance phenomenon prone to interpretation, while engendering a collective need for sense-making. Some commentators believe that the level of skepticism toward corporate taxation will inevitably continue to rise (EY 2017).

The above climate encompasses divergent perspectives depending on the social position of the actors involved (Fairclough 2003, 17, 26). Some pressure groups, for example, focus their criticism on the extent of social inequalities resulting from tax avoidance. The charity Oxfam (2016) reports that “Tax dodging by multinational corporations costs the US approximately $111 billion each year and saps an estimated $100 billion every year from poor countries, preventing crucial investments in education, healthcare, infrastructure, and other forms of poverty reduction”. Oxfam remarks that the present system of “secret subsidiaries is laughably artificial”. There is also the related issue of tax competition, often defended by states and businesses. For example, a survey carried out in the United Kingdom found that 56% of respondent businesses cited tax as an important factor influencing their location decisions in 2017 (KPMG 2018). For 81% of these companies, the most critical elements of an attractive tax regime include a low effective tax rate (KPMG 2018). Tax competition is a major issue in public policy (Fraser Institute 2014). The presumption is that since capital is mobile, firms can exercise their business activities and invest most of their capital wherever they find the most competitive tax system. As a result, a jurisdiction with high marginal tax rates could have lower entrepreneurial activity, lower corporate investments and less job creation (Fraser Institute 2014).

Divergent perspectives are also observed regarding the role of businesses in this debate. Oxfam (2016) has recommendations for multinationals on how to become “tax-responsible companies”. The corporate side of the debate has its own internal tensions. Executives wanting to adopt ethical tax policies can find themselves accused of putting shareholders at a commercial disadvantage, given that other firms have a propensity for aggressive tax planning (Christensen et al. 2004). In lawmaking, the amount of internationally coordinated action is on the rise, particularly through the OECD/G20 “BEPS” (base erosion and profit shifting) project (EY 2017), which has been described by the OECD and G20 as the “largest, and fastest, rewriting of the international tax rules in a century” (OECD 2017(a)).10 The international tax agenda aims to promote transparency and information sharing

10 “Base erosion and profit shifting” refers to “tax avoidance strategies that exploit gaps and mismatches in tax

14

between countries for tax purposes (OECD 2017(b)). These changes are not without implications for multinationals: their boards of directors must consider the risks and potential repercussions of public controversies or bad publicity (EY 2017). Finally, the role of the tax consultants who devise tax schemes is another topic of debate. Some observers accuse them of promoting avoidance strategies with no regard for the consequences for the state or society in general (Sikka 2013), while others instead consider that consultants are doing nothing more than interpreting the law (e.g. Hasseldine and Morris 2013).

While far from exhaustive, this brief overview of tensions around tax avoidance points to a key current debate in society, which could be summed up as: where should the line between acceptable and unacceptable tax practices be drawn? And based on which criteria? Is it enough for actions to be legal? What about being moral? There are certainly many levels of tax aggressiveness along the continuum of acceptability. So whose job is it to determine where to “draw the line” on that continuum, more broadly, as a society? These are questions over which different actors do battle and influence each other as they collectively trace out the complex, unclear boundary between acceptable and unacceptable tax practices (Gracia and Oats 2012). A better understanding of collective construction processes surrounding the normative boundaries of tax avoidance is the general aim driving the present research.

In academic research, the tax avoidance debate is now very topical. For example, a recent study by Anesa et al. (2019) concludes that while the legitimacy of “aggressive” tax practices has been challenged, corporate tax minimization practices are still commonplace. Although the number of academic studies on tax avoidance is growing, understanding of the phenomenon is fragmented. Most research on tax avoidance considers it from one of two separate angles, the moral/social perspective or the functionalist perspective, and there is little or no interaction between these research streams. In attempting to develop a broader view that reconciles these two separately-addressed dimensions, we rely on Baier’s (2013) socio-legal perspective on normativity. Baier’s perspective belongs to the field of law and social norms, and is founded on the idea that “accurate accounts of the relationship between law and society can lay the basis for addressing normative issues arising out of the law’s operations in society” (Banakar 2013b, 33). Echoing many sociology of law studies, we suggest that the study of tax avoidance may benefit from a greater understanding of the relationships between legal and social norms (Baier 2013, 6). Importing this normative socio-legal framework into the tax realm may translate into a fuller, subtler understanding of tax avoidance.

15

Considering LuxLeaks as a “concrete normative instance in which law and social norms are active” (Baier 2013, 7), we conducted a discursive analysis of press representations through the media discourse lens of Fairclough (1995, 2003) to understand how the media, normatively speaking, make sense of LuxLeaks. Our discursive analysis illustrates that even an apparently “technical” tax event such as LuxLeaks can be the subject of different, coexisting representations in press articles. Considered from Baier’s socio-legal perspective, this discursive battle over the problematization of LuxLeaks indicates a normative negotiation (Baier 2013). It became evident that the press uses norms as a discursive resource to draw boundaries between acceptable and unacceptable tax practices and make sense of LuxLeaks. Our point is that the media develop different versions of “reality” about LuxLeaks using different conceptions of normativity.

According to our analysis, the field of tax avoidance is characterized by a highly uncertain, ambiguous and vague normativity that is currently open to negotiation. We believe there is a need to step back and (re)consider broader assumptions of normativity in the tax avoidance area to advance the debate. Working on the premise that Baier’s work provides a meaningful template for understanding, sorting and conducting empirical studies relating to social and legal norms (Baier 2013, 8), we use his conceptual platform to map out the normative structure specific to LuxLeaks based on insights into press discourse.

This study attributes a dual role to the media. First, the media are considered as a reflection of society, a kind of arena for discursive battle between different social groups over the construction of social reality (e.g., Gamson and Modigliani 1989; Greenberg 2002). Second, the media are considered as an actor in their own right, with the potential to take part in the battle through their ability to influence public opinion (e.g., Barker and Knight 2000, 167–168). The complexity and controversial nature of tax avoidance make LuxLeaks a very suitable subject for interpretation. In such a situation, which version of reality (Fairclough 1995, 103) or normative stance do the media choose to present with respect to LuxLeaks? The lack of transparency in tax avoidance makes the question particularly relevant. Since our perceptions of the world outside the sphere of our everyday experience are very often influenced by the media (Thompson 1995, 34), the public is particularly likely to draw on media reports to make sense of an event as difficult to grasp as LuxLeaks.

We aim to contribute to the literature on tax avoidance by importing into the tax realm Baier’s (2013) socio-legal perspective on normativity, which to our knowledge has not yet been used in tax research. Examining subjects at the socio-legal intersection can give rise to new reflections or avenues for

16

research, with the ambition to be part of what Alvesson and Sandberg (2014) call a “box-breaking research” trajectory – which in our case considers ideas and resources found in the “research box” of the sociology of law, in addition to the specific “research box” of international corporate taxation. We also aim to exemplify how tax empirics can be used to develop a better understanding of socio-legal normative issues and stimulate further interest in developing new research avenues inspired by the sociology of law.

The structure of the paper is as follows. In the next section, we position the study in the academic literature. We then introduce our theoretical underpinnings derived from the work of Baier (2013) and Fairclough (1995, 2003). Next, methodological considerations are outlined. Discursive insights from press representations of LuxLeaks are then analyzed to bring out the normative structure specific to LuxLeaks, based on Baier’s (2013) social/legal perspective on normativity. Finally, the discussion explores the normative dynamics of tax avoidance – how it works and how it may evolve – including a reflection on the possible implications arising from the press representations we analyzed.

2. Positioning in the academic literature

Researchers have taken different approaches in seeking to make sense of tax avoidance and in examining how boundaries are set between acceptable and unacceptable tax practices. Most research on tax avoidance considers it from one of two angles: the functionalist perspective11; and the moral/social perspective. Tax research within the latter perspective has produced an increasing number of widely diverse attempts to make sense of tax avoidance. To name just a few, certain authors (e.g. Ylӧnen and Laine 2015; Dowling 2014; Lanis and Richardson 2015) interpret tax avoidance as a social responsibility issue, whereas Bird and Davis-Nozemack (2018) propose to approach tax avoidance as a sustainable development issue. Other researchers make sense of tax avoidance by drawing on ethical criteria. For example, West (2018) prioritizes philosophical analysis of the ethics of multinational tax avoidance, including the role that accountants play in these activities. Frecknall-Hughes et al. (2017) empirically examine how far tax practitioners take a consequentialist or deontological approach when considering moral dilemmas related to tax avoidance. Finally, Payne and Raiborn (2018) offer an ethical review of the morality of aggressive tax avoidance, presenting three ethical frameworks to consider whether aggressive tax avoidance is ethical or unethical.

11For example, see Hanlon and Heitzman (2010) for a review of tax research from a functionalist economic

17

Our study belongs to a research line that considers taxation as a social and institutional practice, beyond the traditional purely technical view (Oats 2014).12 In particular, we suggest considering the sociology of law as a meaningful theoretical angle to inform tax research. The specific angle we use is Baier’s normative perspective – which centers on normative issues relating to the law’s operations in society (Banakar 2013b).

3. Conceptual framework 3.1 Baier (2013)

No concept is invoked more often by social scientists in the explanation of human behavior than “norms” (Sills 1968, 208). Baier (2013) sees the concept of the norm as a key perspective in understanding socio-legal problems. The idea that the sociology of law should treat norms as a platform from which to explore the relationship between law and society is motivated by the assumption that norms are the fundamental constitutive parts of action systems and as such, they govern human behavior (Banakar 2013b, 15). Baier (2013) considers that social norms are imperatives and/or expectations that guide actions and/or behavior, engendering a sense of normativity and social order (Baier 2013, 59). Baier’s (2013) work is also based on the premise that any given norm is relative and constructed (Hechter 2008). The content of a norm varies according to a particular society or culture.

Baier proposes a conceptual matrix (see Figure 1) to make sense of normative interdependencies between legal and social norms (Baier 2013, 67). The term “legal norm” refers to the category of institutionalized norms that are intended to regulate society, and the term “social norm” is used as a comprehensive category covering all other kinds of norms. Each category of norm (legal and social) is divided into two dimensions: the imperative property (“ought”) and the implementation property (“is”), two essential properties under Baier’s integrated definition of the norm. More specifically, Baier (2013) considers norms as the nexus between the “ought” and the “is” (Baier 2013, 59) as they help transform values into actions (Baier and Svensson 2009, 183). These two categories of norms and these two properties together make up Baier’s conceptual platform. Baier considers normativity as an “outcome of normative interdependence and co-production” between the four components of this platform.

12 This type of research, which is still in its infancy although growing fast, provides a different understanding

of tax issues that cannot be generated by other types of tax research (taking an economic, behavioral or legal perspective). See Boll (2014) and Oats (2014) for an overview of the various perspectives in tax research, and the contribution that sociological tax research can make to the field of tax research in general.

18 Figure 1: Baier’s (2013) conceptual platform

As shown in Figure 1, the first component of the matrix is the “ought” property of law (labelled “legal norms”), referring to the dogmatic view of legal norms, often referred to as “law in books”. It is defined here from a socio-legal perspective as a formalized, binding and enforceable system of imperatives stemming from the political system (Baier 2013, 58). The second component of the matrix is the “is” property of law (labelled “legal practices”), often referred to as “law in action”. It can be seen as “legal decision-making” (Baier 2013, 65), how law is actually executed within society (De Kaminski et al. 2013, 311) (e.g., tax administration, case law, appeals system). The third component of the matrix is the “ought” property of social norms (labelled “social norms”), which by default comprises all norms other than legal norms (Baier 2013, 59). It refers to the imperative aspect of social norms, which may find themselves under debate and scrutiny in the same way as legal norms, but within civil society (Baier 2013, 60). The fourth and final component is the “is” property of social norms (labelled “social practices”), reflecting the application of the social norm (Baier 2013, 60). Baier’s (2013) matrix thus conceptualizes the production and application of the legal and social norms as interrelated normative systems, which might even “merge” into a single socio-legal practice (Baier 2013, 6). Several combinations of social and legal norms exist, forming different kinds of normativity that are deployed differently in different fields (Baier 2013, 54).

To apply this conceptual platform in the field of tax avoidance, we complement Baier’s approach with Fairclough’s (1995, 2003) discursive analysis framework.

3.2. Fairclough (1995, 2003)

In Fairclough’s approach, discourse is the use of language as a specific way of constructing a social practice (Fairclough 1995, 2, inspired by Foucault 1972). Text is not isolated from discursive and sociocultural practices, but rather involved in a dialectical relationship with them. Texts are thus

19

socially constructed, and construct society and culture in turn (Fairclough 1995, 19, 55). The objective of transcending the traditional divide between social theory-inspired discursive analysis and textually-focused discursive analysis is what distinguishes Fairclough’s (2003) discursive approach from the many other versions of discursive analysis that exist (Van Dijk 1997; Fairclough 2003, 2). The concepts of representation and discourse play significant roles in Fairclough’s framework.

Fairclough (2003) sees representation as a process of social construction of practices: representations penetrate and shape practices and social processes (Fairclough 2003, 206). Discourses differ in the way they represent social events, what they include and leave out, the level of abstraction in reporting events, and the specific way they represent the processes, relationships, social actors, times, and places associated with the events (Fairclough 2003, 17). Discourse, in the view of Fairclough (2003), constitutes a social practice constructed from a specific perspective that aims to make sense and confer meaning. Importantly, Fairclough (1995) applies his discursive approach to media texts. In his view, the media provide a selective representation of the world, making certain choices in their texts (e.g., the vocabulary and grammar used), and consequently in the meaning given to the things being represented (Fairclough 1995). In other words, media texts do not, as might be naively assumed, reflect “reality”. Rather, they are a representation of reality, which depends on the social position and interests and goals of the actors who produce it (Fairclough 1995, 103). In short, we rely on the conceptual foundations proposed by Fairclough (1995, 2003) to examine the construction of meaning in the press articles on LuxLeaks – since this approach may reveal certain textual dynamics that would otherwise go unnoticed (Vaara and Tienari 2008). This is especially relevant in our context to bring out (often very subtle and implicit) normative insights from the discourses studied. In other words, we assume that the media, through their articles, articulate the components of Baier’s normativity as they seek to make sense of the LuxLeaks saga.

Fairclough’s discursive framework is not without its critics. In particular, some believe it fails to give due consideration to the audience reaction (e.g., Ferguson 2007). Thompson (1990) gives a good description of the risk involved when a discursive analysis is conducted without systematically consulting the audience concerned, potentially leading to speculation about the effects of the texts studied. The study presented here subscribes to the arguments made by Fairclough (1995) in response to such criticisms. He argues that consideration of how texts are received should not be applied to the detriment of the analysis itself. Fairclough claims that the range of possible interpretations of a text will in any case be restricted and delimited by the nature of the text (Brunsdon 1990). Textual analysis thus remains a central element of media analysis, although it can be complemented by analysis of the

20

audience reaction and production of the text (Fairclough 1995, 16). The comments made by Fairclough (1995) about the – moderate – version of social constructivism to which he adheres also clarify his perspective on this point: “(…) so we can accept a moderate version of the claim that the social world is textually constructed, but not an extreme version. (…) we may textually construe (represent, imagine, etc.) the social world in particular ways, but whether our representations or construals have the effect of changing its construction depends upon various contextual factors – including the way social reality already is, who is construing it, and so forth.” (Fairclough 2003, 8– 9).

4. Methodological considerations13

4.1. Background

The International Consortium of Investigative Journalists (ICIJ 2014) describes LuxLeaks as a collaborative investigation endeavor that exposes for the first time on a global scale how Luxembourg works as a tax haven. The ICIJ mentions “at least 548 tax rulings in Luxembourg from 2002 to 2010”, referring to “legal secret deals” that feature “complex financial structures designed to create drastic tax reductions.” The ICIJ also explains the following:

The rulings provide written assurance that companies’ tax-saving plans will be viewed favorably by Luxembourg authorities. Companies have channeled hundreds of billions of dollars through Luxembourg and saved billions of dollars in taxes. Some firms have enjoyed effective tax rates of less than 1 percent on the profits they’ve shuffled into Luxembourg. Many of the tax deals exploited international tax mismatches that allowed companies to avoid taxes both in Luxembourg and elsewhere through the use of so-called hybrid loans.

4.2. Selection of articles

The media texts analyzed were selected from the following newspapers: Wall Street Journal, New York Times, The Guardian, Financial Times, The Times, Le Figaro, and Le Monde. These newspapers were initially chosen for their large readership and their “quality press” reputation, but also for their overall diversity in terms of geographic area, type of readership (general public, or business readers) and political profile.

13This section is written in the first person singular, as the first author played a central role in collecting the press article data. The second author was involved in discussing emerging issues with the first author during data collection, and in commenting on and improving the previous versions of this paper.

21

The articles were found in the Factiva database (Dow Jones Factiva), except those from Le Monde (which is not included in Factiva), which come from the Eureka platform. The following key words were used to identify relevant articles:

- English-language newspapers: Luxembourg and tax* OR LuxLeak*

- French-language newspapers: LuxLeaks OR LuxLeak OR (Luxembourg and (impôts OR fiscalité OR fiscaux OR fiscal OR rulings OR LuxLeaks OR fisc*))

Some broader additional searches were carried out in the case of the English-language newspapers, to find texts that could have escaped the chosen key words. The resulting articles were then sorted manually to eliminate non-relevant texts, many of which concerned tax evasion and official European Union investigations concerning Luxembourg.

Regarding the choice of period from which the data were collected, note that the results of the investigation by the journalists’ consortium behind LuxLeaks were published in November and December 2014. Data collection relates to the period from November 1, 2014 to October 18, 2016. Articles were included up until that date to ensure that the context and events related to LuxLeaks were properly covered. From detailed scrutiny of the articles collected, two categories were identified. The first category consists of articles directly concerning LuxLeaks, i.e. which had LuxLeaks as their main topic, generally published in the weeks just after the event. The second category consists of texts that cover LuxLeaks indirectly, often through references that are much briefer but still provide meaningful representations of the event. One of the principal methodological difficulties was identifying these indirect articles, given the large number of articles on the political and legislative changes that relate to tax avoidance but only very indirectly to LuxLeaks itself. The general rule was that any text mentioning LuxLeaks, even in just a few sentences, was included in the analysis, and only the sentences concerning LuxLeaks were coded. Table 1 gives details of the direct and indirect articles examined.14